Market Verdict

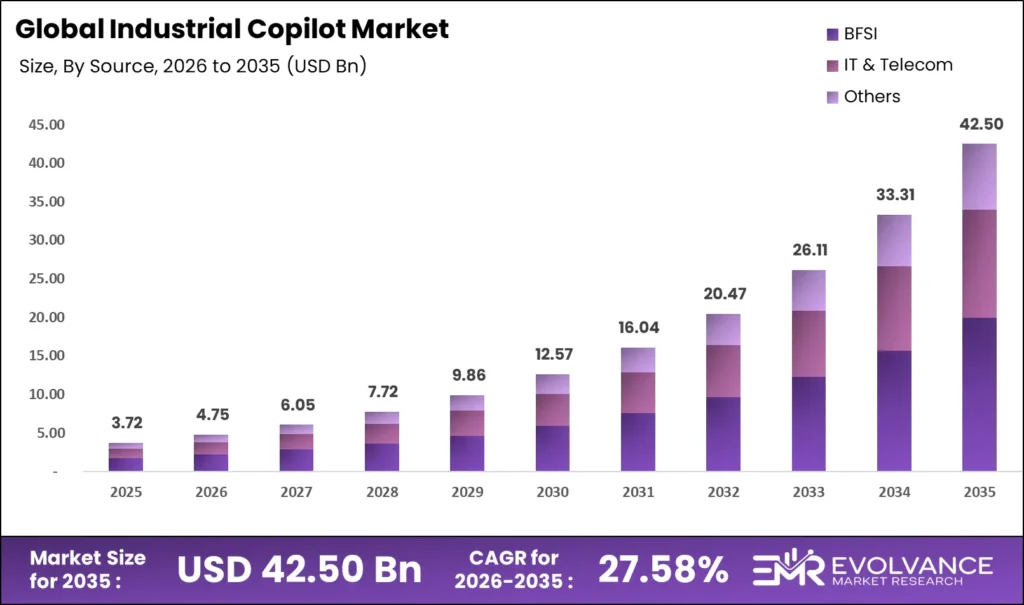

The industrial copilot market size is USD 3.72 billion in 2025, rising to USD 4.75 billion in 2026, and reaching USD 42.49 billion by 2035: the industrial copilot market is not expanding because AI is fashionable, but because structural workforce retirement and OT complexity have created a guidance deficit that no prior software category has resolved. According to EMR, the 27.58% CAGR from 2026 to 2035 reflects procurement urgency, not speculative adoption. The platform that owns the OT/IT integration layer before consolidation closes will command a disproportionate share.

Key Takeaways

Market Size:

- Market value in 2025: USD 3.72 billion (as per our research)

- Market value in 2026 (calculated): USD 4.75 billion

- Market value in 2035: USD 42.49 billion (EMR analysis indicates)

- CAGR: 27.58% from 2026 to 2035

- US market CAGR: 28.52% through 2035

Dominant Segments:

- Deployment: Cloud-Based at 64.73% revenue share as of 2025

- Application: Maintenance and Diagnostics at 37.58% revenue share as of 2025

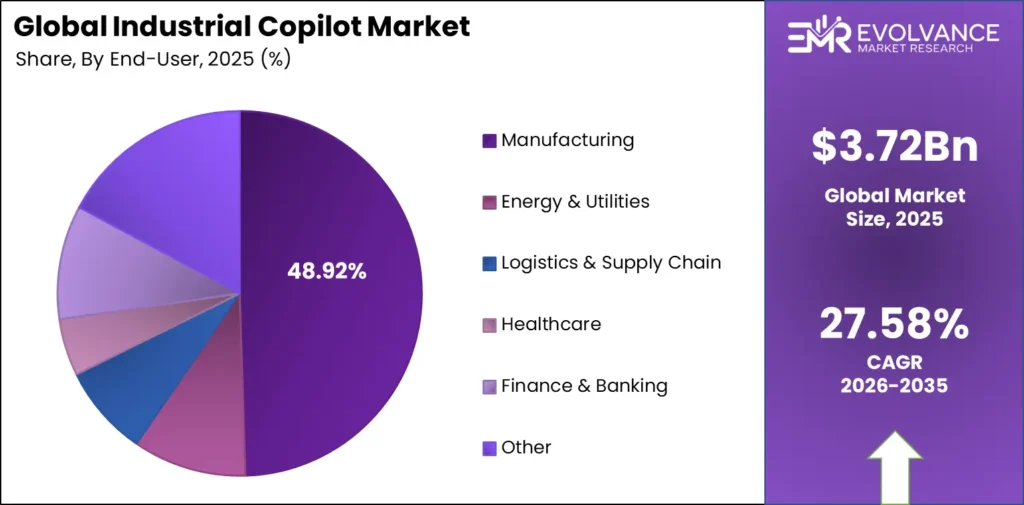

- End-User Industry: Manufacturing at 48.92% revenue share as of 2025

- Offering: Software Subscriptions at 68.79% revenue share as of 2025

- AI Model Architecture: LLM-based Copilot leads (directional, no share percentage available)

- Workforce Function Served: Maintenance and Service Technicians lead (directional, no share percentage available)

- Integration Level: IT-OT Converged Integration leads (directional, no share percentage available)

- Human-Machine Interface: Conversational/NLP Interface leads (directional, no share percentage available)

- User Type: Large Enterprises lead by revenue; SMEs represent the highest-growth segment

Dominant Region:

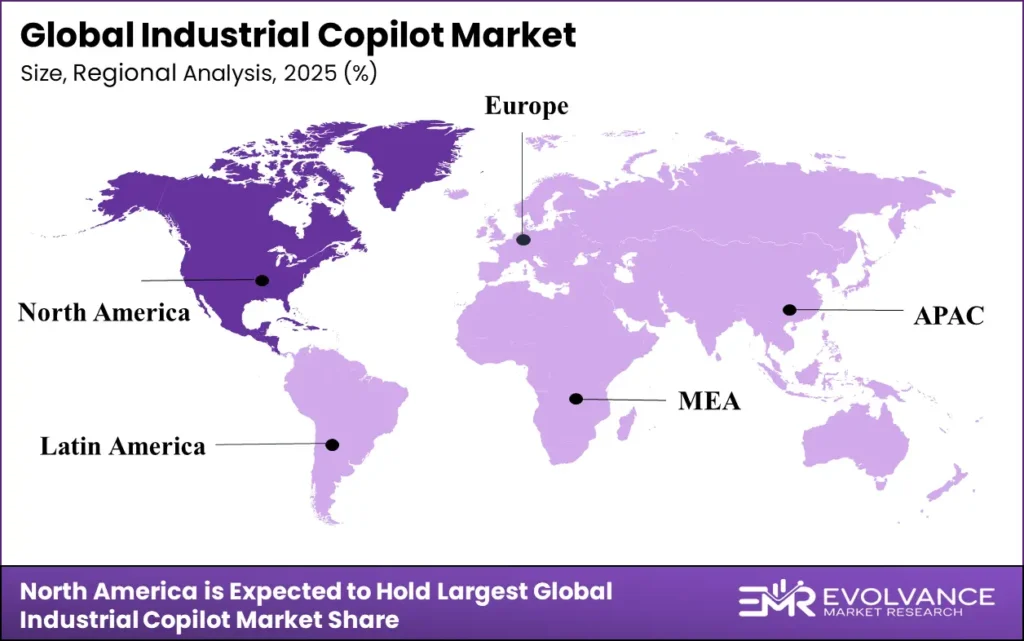

- Leading region: North America, largest revenue share as of 2025 (USD value not available in published data)

- Fastest-growing country: China at 29.92% CAGR through 2035

Source: Evolvance Market Research

Market Overview

An industrial copilot is an AI-powered software assistant embedded within operational technology and industrial enterprise environments. It augments decision-making for operators, technicians, engineers, and managers by delivering contextual guidance, automated diagnostics, and real-time analytics through conversational or dashboard-integrated interfaces connected to SCADA, MES, ERP, and IIoT data sources. Manufacturing, energy, logistics, and process industries depend on it for decisions where delay or error carries measurable financial and safety consequences.

Our research draws on primary fieldwork spanning 12 countries and 1,200 stakeholder interviews conducted from September 2024 through August 2025. EMR analysts covered 9 segment dimensions and 6 regional markets, combining demand-side buyer surveys with vendor capability assessments. Validation ran through cross-referencing buyer-reported deployment timelines against vendor capability disclosures and independent regulatory documentation. Geographic scope covers North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa.

The core problem industrial copilots solve is the gap between operational data volume and the human capacity to act on it in real time. Buyers who delay procurement absorb that gap directly through unplanned downtime, yield loss, safety incidents, and product defects. Primary buyers include discrete manufacturers, energy operators, logistics providers, and industrial engineering teams, where procurement is triggered by workforce transition events, compliance deadlines, or documented productivity shortfalls. The World Economic Forum’s Future of Jobs 2023 framework identifies this workforce transition as a structural, decade-long pressure rather than a cyclical one.

Siemens AG expanded its Industrial Copilot in March 2025 with a generative AI-powered Maintenance Offering integrating Senseye Predictive Maintenance, with pilots demonstrating approximately 25% reduction in reactive maintenance time (Siemens AG, March 2025). This outcome, documented at commercial scale, is compressing enterprise decision cycles from multi-year transformation programs to sub-18-month deployments. For investors, the compression of pilot-to-deployment cycles signals that capital allocation windows for market entry are narrowing faster than most infrastructure forecasts assumed.

What Is Actually Driving This Market

Workforce retirement in precision manufacturing, oil and gas field operations, and utilities creates a guidance deficit that makes copilot adoption a continuity decision rather than a productivity option. The World Economic Forum projects that 44% of workers’ core skills will change by 2027 due to AI and automation, a pressure that training programs alone cannot resolve at the pace required.

The causal mechanism runs through decision frequency: copilots make expert-level guidance available at every shift, on every asset, without requiring the expert to be physically present. For operators, this means copilot deployment carries a measurable payback period tied directly to avoided downtime and knowledge transfer costs.

LLM infrastructure maturity explains why adoption is accelerating now rather than three years ago. Foundation model providers including Microsoft Azure OpenAI Service reached the inference cost and reliability threshold that makes plant-floor deployment commercially viable only in the 2023 to 2025 period. NVIDIA’s Data Center revenue reached USD 115.2 billion in FY2025, up 142% year-over-year (NVIDIA, 2025), confirming the infrastructure investment scale underpinning industrial AI deployment globally. The International Federation of Robotics confirms that AI-integrated automation investment has accelerated in parallel with this infrastructure build-out. For investors, infrastructure maturity means technology risk in industrial copilot bets has shifted from model capability to integration execution.

Siemens introduced the AI-powered NX CAM Copilot at SPS 2025 in November 2025, automating CNC programming tasks and reducing programming time by up to 80% in discrete manufacturing environments (Siemens AG, November 2025). This quantified outcome in a named industrial application demonstrates the causal path from copilot deployment to measurable productivity gain, directly shortening internal capital approval cycles for buyers evaluating comparable use cases. US CHIPS Act reshoring investment and the EU Advanced Manufacturing initiative correlate with accelerated procurement timelines, though the causal mechanism runs through budget availability rather than regulatory mandate. For operators, peer-documented outcomes now substitute for internal pilots as the primary ROI validation mechanism.

- Structural workforce transition creates a guidance deficit that no prior software category has resolved at plant-floor scale.

- Workforce retirement pressure: WEF projects 44% of core worker skills change by 2027, making copilot adoption a continuity mechanism across precision manufacturing, oil and gas, and utilities.

- Infrastructure threshold reached: NVIDIA Data Center revenue at USD 115.2 billion in FY2025 confirms the compute investment enabling plant-floor LLM inference at commercial cost points.

- Quantified deployment outcome: Siemens NX CAM Copilot at SPS 2025 delivered up to 80% CNC programming time reduction, compressing buyer approval cycles across discrete manufacturing.

Operators who wait for internal ROI pilots before committing face a compressed entry window as platform consolidation around OT/IT stack integrators accelerates through 2027.

Where the Real Risk Is

The primary restraint is integration architecture, not buyer reluctance. Connecting AI platforms to brownfield OT environments containing older PLC vintages, proprietary protocols including Modbus, PROFINET, and DNP3, and fragmented data historians extends deployment timelines by 6 to 18 months on complex sites, as per our research.

IEC 62443, the international industrial cybersecurity standard governing connected software in OT environments, adds security architecture review requirements that are independent of the copilot vendor’s technical readiness. For investors, brownfield integration risk is the primary reason early-stage copilot vendors with strong models but shallow OT protocol coverage will fail to scale beyond pilot deployments.

OT modernization has historically run 3 to 5 years behind forecasts in regulated verticals, according to EMR research team analysis, a pattern that introduces execution risk into any aggressive growth projection. Model hallucination in safety-critical contexts remains an unresolved commercial barrier.

Industrial buyers in sectors where an incorrect AI recommendation could cause equipment damage, contamination, or personal injury are demanding documented hallucination rate benchmarks and explainability tooling that most general-purpose LLM platforms cannot provide without domain-specific fine-tuning investment. For operators, the watch signal is the disclosure of hallucination rate becoming a standard RFP requirement, which would immediately disadvantage vendors without documented fine-tuning programs.

- The risk most investors underestimate: brownfield OT integration complexity will eliminate vendors with capable models but insufficient protocol coverage before market consolidation rewards survivors.

- Integration timeline exposure: brownfield deployments run 6 to 18 months longer than cloud-native software implementations due to protocol and historian fragmentation across multi-decade facility footprints.

- Regulatory compounding: IEC 62443 security requirements and EU AI Act conformity assessments add compliance overhead that disproportionately burdens smaller vendors without dedicated regulatory teams.

Watch for hallucination rate disclosure becoming a standard procurement requirement in energy and pharmaceutical verticals: that signal will mark the structural separation between fine-tuned domain specialists and general-purpose foundation model generalists.

Segmentation: Where Value Is Concentrating

Deployment Insights

Cloud-Based Pulls Ahead: 64.73% Share in 2025

Cloud-Based deployment commands 64.73% revenue share in 2025, according to EMR, by eliminating the cost and infrastructure complexity that previously made industrial AI deployment prohibitive at scale. Hyperscaler integration through Microsoft Azure AI Foundry provides elastic compute for complex inference workloads and direct connectivity to cloud-hosted ERP and supply chain systems, creating faster time-to-value for buyers already operating cloud-first infrastructure.

Edge Deployment is the fastest-growing mode, driven by latency and data sovereignty requirements in air-gapped facilities including remote oil and gas sites and defense contractors. For investors, cloud deployment dominance confirms that near-term industrial copilot spending is concentrated in organizations with mature IT infrastructure, a constraint that will ease as pre-integrated SaaS platforms lower the entry bar for mid-market operators.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Cloud-Based | 64.73% | Hyperscaler integration and elastic compute | Dominant through 2035; SaaS delivery expanding mid-market access |

| Edge Deployment | Directional (fastest growing) | Low-latency inference and data sovereignty at plant floor | Highest growth trajectory; air-gapped and bandwidth-constrained environments |

| On-Premises | N/A | Air-gapped OT security and compliance requirements | Stable niche; prerequisite for critical infrastructure accounts |

Application Insights

Maintenance and Diagnostics at 37.58%: What’s Behind the Numbers in 2025

Maintenance and Diagnostics holds 37.58% revenue share in 2025, as per our research, because asset failure carries directly measurable cost consequences that make copilot ROI verifiable at the facility level. Equipment failure histories are the most consistently recorded operational data type in manufacturing and energy environments, providing training data volume that other application categories cannot match.

Process Optimization addresses yield, throughput, and energy efficiency through parameter guidance in continuous process environments, where incremental efficiency gains compound significantly at scale across chemicals, petrochemicals, and food and beverage sectors. For operators, Maintenance and Diagnostics is the lowest-risk entry application because the ROI calculation is already understood by finance teams before the procurement conversation begins.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Maintenance and Diagnostics | 37.58% | Measurable downtime reduction ROI | Commercially mature; highest training data availability |

| Process Optimization | N/A | Margin-compounding efficiency in continuous process industries | High growth in chemicals, food and beverage, petrochemicals |

| Quality Control | N/A | Defect cost avoidance in discrete manufacturing | Expanding through computer vision and NLP integration |

| Supply Chain and Inventory Management | N/A | Multi-tier supplier complexity management | Growing as ERP-copilot integration matures |

| Customer Service and Support | N/A | AI-assisted field service resolution | Emerging; tied to mobile and voice interface adoption |

| Data Analysis and Decision Support | N/A | Democratized analytics for non-data roles | Expanding as NLP interface lowers access barriers |

| Operations Copilot | N/A | Real-time operator guidance in production | Growth tied to frontline workforce copilot expansion |

| Engineering Copilot | N/A | LLM-assisted code generation and simulation | High-profile; leading vendors investing in PLC code generation |

End-User Industry Insights

Manufacturing Holds the Largest Share at 48.92% in 2025

Manufacturing’s 48.92% end-user revenue share in 2025, according to EMR, reflects the simultaneous convergence of workforce retirement, rising product complexity, and intensifying compliance requirements found together in no other vertical. AI in automotive manufacturing, aerospace, electronics, and precision machining concentrates these pressures into a demand profile that makes copilot adoption a business continuity decision.

Energy and Utilities is the most active secondary vertical, where asset criticality levels mean a missed AI signal translates to outages or safety incidents rather than production inefficiency. For investors, manufacturing’s share concentration signals that the highest-return bets are in vendors with domain depth across discrete production environments rather than horizontal platform generalists.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Manufacturing | 48.92% | Workforce retirement and compliance pressure in discrete production | Dominant; AI in automotive and aerospace driving expansion |

| Energy and Utilities | N/A | Asset criticality and safety compliance | Active secondary; high-urgency procurement environment |

| Logistics and Supply Chain | N/A | High labor turnover and persistent onboarding burden | Growing; warehouse and fleet maintenance adoption accelerating |

| Healthcare | N/A | Regulatory compliance documentation for FDA and GMP | Emerging; medical device and pharmaceutical production focus |

| Finance and Banking | N/A | Operational risk and decision support | Early stage; compliance use cases leading |

| Retail and E-Commerce | N/A | Fulfillment optimization and demand intelligence | Adjacent; warehouse automation driving adoption |

| IT and Software Development | N/A | Code generation and DevOps automation | Established in engineering copilot use cases |

| Education and Research | N/A | Domain model fine-tuning data generation | Strategic; model validation role growing |

Offering Insights

The 68.79% Story: How Software Subscriptions Took the Lead in 2025

Software Subscriptions account for 68.79% of total market revenue in 2025, EMR analysis indicates, reflecting a procurement philosophy shift from capital-intensive perpetual licenses to OpEx-aligned SaaS contracts. Industrial buyers are treating AI capability as a continuously improving service, a rational position when underlying LLM capabilities require replacement within 18 to 36 months.

Services revenue covering implementation, OT/IT integration, and training remains a prerequisite for production-grade deployment in brownfield environments, not a discretionary add-on. For operators, SaaS procurement aligns AI investment with operational budget cycles and eliminates stranded asset risk from perpetual licenses in a rapidly evolving model environment.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Software Subscriptions | 68.79% | OpEx alignment and continuous LLM model improvement | Dominant; SaaS delivery expanding SME access |

| Services | N/A | OT/IT integration complexity in brownfield deployments | Stable essential revenue; declining gradually as pre-integration templates mature |

AI Model Architecture Insights

LLM-based Copilot’s Edge in the AI Model Architecture Race

LLM-based Copilot leads the AI Model Architecture segment because it is the only architecture delivering the conversational interface paradigm that defines the industrial copilot category at scale. Without LLM-grade natural language understanding, the step-change from dashboard analytics to interactive AI guidance is not achievable across diverse workforce functions.

SLM-based Copilot is gaining adoption in edge and resource-constrained scenarios, where full LLM inference requires cost-prohibitive compute infrastructure and smaller models deliver acceptable performance for well-scoped repetitive tasks including fault code lookup. For investors, LLM architecture leadership is durable only for vendors who have invested in domain fine-tuning: general-purpose foundation models face displacement by fine-tuned specialists in safety-critical procurement evaluations.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| LLM-based Copilot | Leading (directional) | Natural language interface capability at scale | Dominant; fine-tuning investment separating leaders from followers |

| SLM-based Copilot | N/A | Edge compute constraints and cost efficiency | Growing in air-gapped and bandwidth-constrained environments |

| Fine-Tuned Domain-Specific Model | N/A | Accuracy and hallucination reduction in safety-critical use | Highest value per deployment; procurement preference in regulated verticals |

Workforce Function Served Insights

Inside Maintenance and Service Technicians’ Share Advantage

Maintenance and Service Technicians generate the clearest measurable ROI of any workforce group, explaining their leading commercial position and the concentration of vendor product development resources targeting their workflows. Field technicians interact with AI guidance in real time during fault diagnosis and repair execution, where speed and accuracy directly determine downtime duration and maintenance cost outcomes.

Engineering and Design Teams are the focus of the highest-profile product investment from vendors including Siemens and Rockwell Automation, where LLM-assisted PLC code generation and simulation acceleration directly compress engineering cycle times. For operators, technician-first deployment builds organizational confidence in model accuracy that authorizes expansion into higher-stakes agentic use cases.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Maintenance and Service Technicians | Leading (directional) | Real-time fault diagnosis and repair support | Commercially mature; highest documented ROI per deployment |

| Frontline/Operator Workforce | N/A | Abnormal situation guidance at plant floor | Highest headcount potential; SME expansion accelerating access |

| Engineering and Design Teams | N/A | LLM-assisted code generation and simulation | High-profile; leading vendors concentrating product investment here |

| Management and Decision Makers | N/A | KPI aggregation and exception-based alerting | Growing; analytics-forward interface adoption rising |

Integration Level Insights

IT-OT Converged Integration Tops the Field in 2025

IT-OT Converged Integration leads because most deployments are happening in facilities built before AI was a design consideration, making middleware the only viable path that avoids OT system replacement. Platforms including Cognite Data Fusion, Palantir AIP, and C3 AI allow copilot deployment without requiring OT hardware changes or protocol modifications across mixed-vendor environments.

OT-Native Integration holds strategic value in greenfield deployments and single-vendor automation environments where the copilot vendor also supplies the automation hardware, eliminating cross-vendor protocol complexity. For investors, middleware platform positions represent the highest-value acquisition targets as the integration layer becomes the primary competitive moat in this market.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| IT-OT Converged Integration | Leading (directional) | Brownfield middleware deployment without OT replacement | Dominant in existing enterprise environments through 2030 |

| OT-Native Integration | N/A | Greenfield and single-vendor automation stacks | Growing with Asia Pacific new factory construction wave |

| Cloud API Integration | N/A | Low-complexity entry-level copilot deployments | Entry point for buyers without mature OT data infrastructure |

Human-Machine Interface Insights

Conversational/NLP Interface Captures the Lead as 2025 Demand Shifts

Conversational/NLP Interface leads because it requires zero specialized hardware and zero behavioral retraining to use. Any worker who can type or speak a question already knows how to interact with it, removing the adoption friction limiting every other interface modality. Voice-Activated Interface addresses hands-free requirements in maintenance and field service contexts, where technicians diagnosing equipment cannot simultaneously operate a touchscreen, making voice the only viable real-time guidance delivery channel.

Dashboard Overlay Interface carries the lowest adoption friction of any modality by integrating copilot capabilities within existing MES, SCADA, and ERP screen layouts, minimizing behavioral change for operators accustomed to current workflows. For operators, interface selection is a workflow-matching decision: mismatched interface choices are the most common cause of low adoption rates in early deployments.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Conversational/NLP Interface | Leading (directional) | Natural language accessibility for all user types | Dominant entry point; evolving toward orchestration layer capability |

| Voice-Activated Interface | N/A | Hands-free guidance in maintenance and field service | Growing with smart glasses and wearable audio form factor adoption |

| Mobile/Wearable Interface | N/A | Field access across dispersed and remote assets | Expanding in energy and multi-site manufacturing environments |

| Dashboard Overlay Interface | N/A | Low-friction adoption within existing screen workflows | Preferred entry point for organizations prioritizing speed of rollout |

User Type Insights

Why Does Large Enterprise Dominate the Industrial Copilot Market?

Large Enterprises lead the User Type segment because OT/IT integration complexity in brownfield environments has historically required internal IT teams, system integration budgets, and vendor relationship leverage that only enterprise-scale organizations consistently possess. SMEs represent the highest-growth segment as SaaS delivery and pre-configured industry templates eliminate the prerequisite for six-figure integration projects, opening production-grade copilot access to smaller manufacturers and logistics operators for the first time.

Educational and Research Institutions contribute domain-specific training data and use-case validation that commercial platforms depend on for model fine-tuning accuracy. For investors, the SME growth trajectory represents the next volume expansion wave, with platform economics improving as template libraries mature across common industrial configurations.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Large Enterprises | Leading (directional) | Investment capacity and OT/IT integration resources | Dominant by revenue; consolidating around full-stack platform vendors |

| SMEs | Highest growth (directional) | SaaS delivery removing upfront integration barriers | Fastest-growing segment; template-driven deployment accelerating |

| Individual | N/A | Engineering-focused copilot license adoption | Niche; engineering copilot use cases primary driver |

| Educational and Research Institutions | N/A | Domain model fine-tuning data generation | Strategic; early adopters in simulation and design environments |

Value is concentrating in vendors controlling both the OT/IT integration layer and the Maintenance and Diagnostics application category simultaneously. These two positions together define the most defensible competitive moat in the current market structure. Fragmentation is occurring at the application edge in Quality Control and Supply Chain, where point-solution vendors compete on domain depth before platform consolidation absorbs or eliminates them. For investors, the integration layer is the acquisition target and the application edge is the talent acquisition opportunity.

Segments Covered in This Report

By Deployment

- Cloud-Based

- On-Premises

- Edge Deployment

By Application

- Maintenance and Diagnostics

- Process Optimization

- Quality Control

- Supply Chain and Inventory Management

- Customer Service and Support

- Data Analysis and Decision Support

- Operations Copilot

- Engineering Copilot

By End-User Industry

- Manufacturing

- Energy and Utilities

- Logistics and Supply Chain

- Healthcare

- Finance and Banking

- Retail and E-Commerce

- IT and Software Development

- Education and Research

By Offering

- Software Subscriptions

- Services

By AI Model Architecture

- LLM-based Copilot

- SLM-based Copilot

- Fine-Tuned Domain-Specific Model

By Workforce Function Served

- Frontline/Operator Workforce

- Maintenance and Service Technicians

- Engineering and Design Teams

- Management and Decision Makers

By Integration Level

- OT-Native Integration

- IT-OT Converged Integration

- Cloud API Integration

By Human-Machine Interface

- Conversational/NLP Interface

- Voice-Activated Interface

- Mobile/Wearable Interface

- Dashboard Overlay Interface

By User Type

- Individual

- Educational and Research Institutions

- SMEs

- Large Enterprises

Regional Analysis: Where Geography Creates Advantage

North America holds the leading regional revenue position in 2025, according to EMR, anchored by the United States’ concentration of technology vendors, advanced discrete manufacturing sectors, and the highest enterprise AI adoption velocity globally. Reshoring-driven manufacturing investment under CHIPS Act provisions and IIoT modernization programs across defense, aerospace, and automotive sectors are the named structural drivers.

The National Institute of Standards and Technology AI Risk Management Framework is shaping vendor procurement requirements in US federal and regulated industrial accounts, reinforcing North America’s compliance-ready deployment advantage. For investors, North America’s platform vendor concentration means the highest-margin positions in the global market are already occupied by established players with deep OT customer relationships, and entry barriers are rising.

Asia Pacific is the fastest-growing region and the most consequential greenfield deployment opportunity in this decade. China’s factory construction under the Made in China 2025 framework allows industrial copilots to be integrated at the architecture layer rather than retrofitted, eliminating the brownfield complexity constraining deployment timelines everywhere else.

India’s manufacturing expansion under the Make in India program is accelerating copilot adoption across automotive, pharmaceuticals, and electronics. Japan and South Korea contribute through semiconductor and automotive automation investment coordinated through national industrial AI policy frameworks. For operators with multi-regional footprints, Asia Pacific greenfield sites offer the fastest achievable ROI environments and the cleanest conditions for agentic capability testing.

Europe’s industrial copilot market is anchored by Germany’s precision manufacturing and automotive sectors, where Siemens AG, Bosch, and domestic OEMs represent the primary demand base. The EU AI Act, enacted in 2024 with phased compliance deadlines running through 2027, classifies AI systems in safety-critical industrial operations as high-risk applications requiring conformity assessment under European Parliament authority. This compliance burden shapes deployment architecture toward on-premises and hybrid models in energy and chemicals verticals. For operators, EU AI Act conformity capability is now a procurement prerequisite in European regulated verticals rather than a competitive differentiator, and vendors without documented conformity programs are excluded before evaluation begins.

| Region | Share % | USD Value | Key Driver | Strategic Signal |

|---|---|---|---|---|

| North America | Leading | N/A | CHIPS Act reshoring and hyperscaler AI infrastructure concentration | Platform consolidation underway; entry window narrowing |

| Asia Pacific | Fastest growing | N/A | Made in China 2025 and Make in India greenfield factory construction | Greenfield deployment eliminates brownfield integration risk entirely |

| Europe | N/A | N/A | German precision manufacturing and EU AI Act compliance pressure | Conformity capability now a procurement prerequisite, not a differentiator |

| Latin America | Early stage | N/A | Automotive and energy sector modernization in Brazil and Mexico | Monitor post-2028 as platform costs decline |

| Middle East and Africa | Early stage | N/A | GCC national diversification and smart infrastructure programs | Energy sector optimization is the leading adoption entry point |

Competitive Landscape: Who Is Pulling Ahead and Why

The structural advantage leaders hold is OT/IT stack depth, not model quality. Siemens AG, with its Xcelerator platform built on Microsoft Azure OpenAI Service, serves over 120,000 engineers as of 2025 (Microsoft, November 2023), a deployment footprint providing proprietary usage data for continuous model fine-tuning on real industrial workflows.

Siemens AG recorded EUR 78.9 billion in FY2025 revenue with an Industrial Business book-to-bill ratio of 1.12 (Siemens AG, November 2025), confirming that order momentum is outpacing current revenue. This data-network advantage is the moat that pure-play AI vendors without established OT customer relationships cannot replicate through model investment alone. For investors, Siemens’ position is defensible because the competitive advantage is operational data access, not algorithmic innovation.

ABB and Schneider Electric are the most credible Tier 1 challengers. ABB Automation orders reached USD 9,928 million in 2025, up 33% year-over-year (ABB, February 2026), signaling forward demand across its industrial automation base that directly supports copilot upsell opportunities. Schneider Electric’s EcoStruxure platform targets the same enterprise accounts as Siemens with a stronger position in energy management and building automation through Microsoft Azure AI integration.

Rockwell Automation’s FactoryTalk copilot, enhanced with NVIDIA Nemotron Nano integration, carves a differentiated position in edge-deployment scenarios where cloud LLM dependencies are operationally unacceptable. For operators, Tier 1 vendor selection now determines the integration architecture for the next decade, not just the current deployment cycle.

IBM’s generative AI book of business exceeded USD 12.5 billion in 2025 (IBM, January 2026), reflecting enterprise AI adoption at a scale that directly feeds industrial copilot deployment pipelines across manufacturing and energy customer segments. The Tier 2 competitive set, including Augmentir, Cognite, SymphonyAI, C3 AI, and Palantir Technologies, is competing on domain depth and workflow specificity rather than platform breadth.

The International Society of Automation governs industrial AI integration standards that all entrants must address, and compliance with ISA-95 and ISA-99 frameworks is an active procurement filter in enterprise evaluations. For investors, the Tier 2 segment is the acquisition pipeline: consolidation will favor platform integrators over point-solution specialists as enterprise buyers standardize on fewer vendor relationships through 2030.

Key Players in This Report

- Siemens AG

- Schneider Electric

- Rockwell Automation

- ABB

- Microsoft Corporation

- IBM Corporation

- NVIDIA Corporation

- GE Vernova

- SymphonyAI

- Augmentir

- C3 AI

- Cognite

- Palantir Technologies

- Honeywell International

- PTC Inc.

- SAP SE

- Oracle Corporation

- Emerson Electric Co.

- Mitsubishi Electric Corporation

- Yokogawa Electric Corporation

- FANUC Corporation

- Bosch

- Omron Corporation

- Dassault Systemes SE

Where This Market Goes Next

The agentic transition is the defining scenario through 2030. Two activation conditions must be met: hallucination rates in domain-specific models must drop below procurement-acceptable thresholds in safety-critical verticals, and enterprise contract frameworks must evolve to assign liability for autonomous AI-initiated actions.

Schneider Electric’s agentic manufacturing capabilities, unveiled at Hannover Messe 2026, delivered engineering time reductions of up to 50% and compressed production configuration changes from weeks to hours (Schneider Electric, April 2026). This outcome from a Tier 1 vendor in a named commercial environment is the proof point that will unlock agentic procurement across the broader manufacturing sector. For operators, organizations beginning supervised agentic deployment now in low-risk workflow categories, including work order generation and quality hold issuance will build the audit trail needed to authorize higher-stakes autonomous execution before competitors reach the same readiness level.

SME market penetration determines whether the 2035 forecast is a floor or a ceiling. The activation condition is SaaS platform template libraries reaching sufficient depth to eliminate custom integration requirements for the most common industrial configurations. Vendors building pre-configured templates across discrete manufacturing, logistics, and energy distribution now will establish switching costs among SME customers before the competitive field recognizes the opportunity.

The International Society of Automation’s SME-focused digital transformation guidelines are accelerating template standardization by defining common integration patterns that SaaS vendors can build against. For investors, SME platform penetration is the scenario where market concentration shifts: the winner accumulates volume economics that compound into AI model quality advantages over time.

| Condition | Timeline | Upside | Who Benefits |

|---|---|---|---|

| Agentic AI liability frameworks established in enterprise contracts | 2026 to 2028 | Autonomous work order, quality hold, and procurement trigger execution at scale | Tier 1 platform vendors with domain fine-tuning and audit trail capability |

| SaaS template libraries eliminate custom SME integration requirements | 2026 to 2029 | SME segment volume expansion unlocking forecast ceiling scenario | SaaS-first vendors with pre-configured industry template depth |

| Asia Pacific greenfield construction reaches AI-native design standard | 2025 to 2030 | Fastest achievable ROI environments globally and cleanest agentic pilot conditions | Vendors with established Asia Pacific channel and OT-native integration capability |

Key Developments

- January 2026: Siemens unveiled nine new AI-powered Industrial Copilots at CES 2026 across Teamcenter, Polarion, Opcenter, and additional software platforms, signaling a shift from single-function tools to unified AI intelligence layers covering the full industrial value chain.

- June 2025: Verdantix identified 10 GenAI-powered industrial copilot vendors in a dedicated market insight report, marking analyst-tier recognition of the category as commercially mature and distinct from broader industrial AI software classifications.

- May 2025: Schneider Electric launched its Industrial Copilot with Microsoft at Automate 2025, integrating Azure AI Foundry with EcoStruxure Automation Expert for predictive maintenance, real-time data access, and troubleshooting, marking the platform’s entry into production-grade commercial deployment.

- March 2025: Siemens Industrial Copilot won the Hermes Award 2025 as the first generative AI product recognized for industrial environments across the full value chain, signaling category legitimacy at the industry’s leading trade recognition event.

- March 2025: Tractian partnered with Oracle to adopt Oracle Cloud Infrastructure for its AI-based condition monitoring and asset performance management platform, confirming enterprise cloud partnership as a commercial scaling prerequisite for specialist industrial copilot vendors.