What is the Carbon Neutral Construction Materials Market Size?

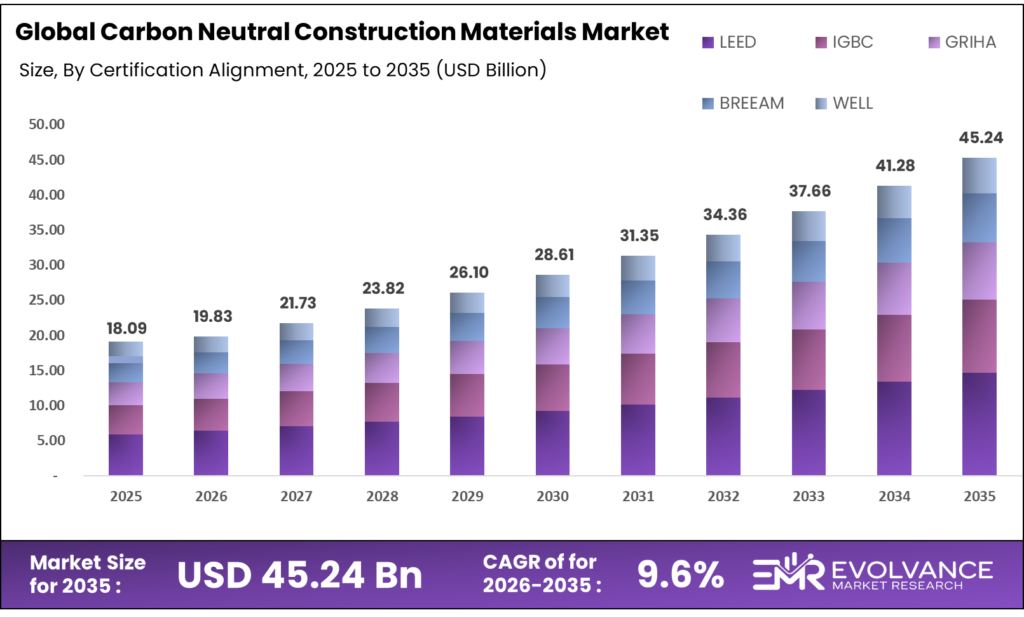

The Global Carbon Neutral Construction Materials Market size will be worth around USD 45.24 Billion by 2035 from USD 18.09 Billion in 2025, growing at a CAGR of 9.6% during the forecast period 2026 to 2035. This pace reflects builders and developers replacing carbon-heavy inputs with verified low-emission alternatives faster than most vendors planned. Public procurement mandates and buy-clean policies have shifted large institutional spending toward materials with measurable embodied-carbon credentials. Supply-side scaling of fossil-free steel and carbon-neutral cement remains a bottleneck, with billions in capital still needed before production meets projected global demand.

Market Highlights

- Global Carbon Neutral Construction Materials Market valued at USD 18.09 Billion in 2025; forecast to reach USD 45.24 Billion by 2035 at a CAGR of 9.6%

- Asia Pacific leads with 37.2% market share, valued at USD 6.78 Billion

- Structural Materials dominates By Material Category with 39.2% share

- Carbon-Reducing Materials leads By Carbon Strategy with 46.5% share

- Residential leads By Building Type with 42.7% share

- LEED leads By Certification Alignment with 37.4% share

- Developers lead By Buyer Type with 32.9% share

- Direct B2B Procurement leads By Distribution Channel with 41.6% share

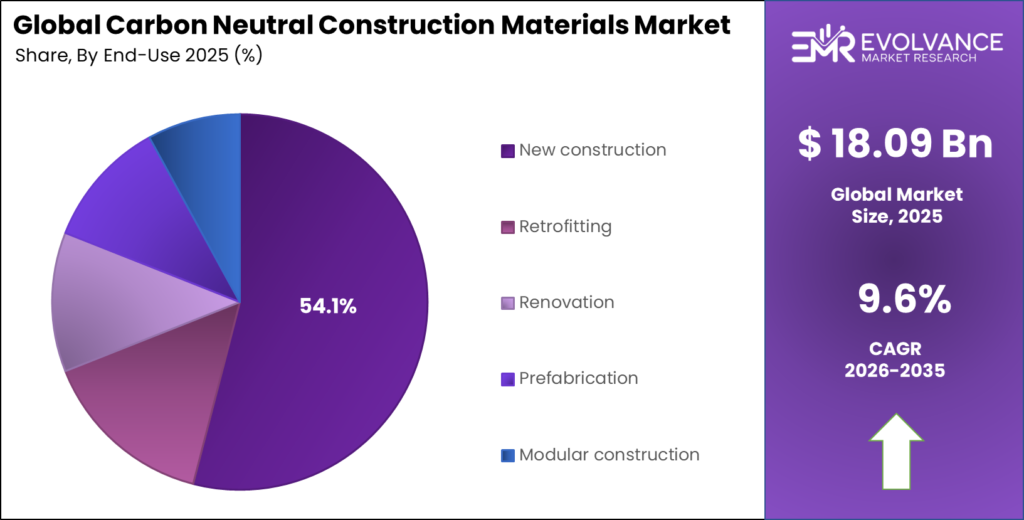

- New Construction leads By End-Use with 54.1% share

Market Overview

The carbon neutral construction materials market covers all building inputs designed to cut, offset, or absorb CO₂ across their full lifecycle. Products range from low-carbon cement and fossil-free steel to mass timber, geopolymer concrete, and bio-based insulation. What ties them together is a shared goal: meeting net-zero commitments without sacrificing structural or thermal performance.

Construction accounts for a large share of global industrial emissions, making material substitution a priority target for climate policy. Buyers are no longer choosing these materials purely on green values. They are responding to mandatory embodied-carbon limits in tenders, investor ESG pressure, and cost parity that now favors several low-carbon materials options over their conventional counterparts.

Government investment is accelerating production scale. In the United States, the Department of Energy initiated discussions worth up to $500 million to support SSAB’s fossil-free steel expansion in Iowa during 2024. Europe’s industrial decarbonization funds are similarly channeling capital into low-carbon cement, circular concrete, and bio-based materials manufacturing.

Carbon Neutral Construction Materials are engineered to offset or eliminate carbon emissions during production, transport, and installation. From mass timber to recycled steel, these solutions help developers meet increasingly strict environmental regulations. When combined with Low-Carbon Construction Materials, they form a comprehensive strategy for reducing a project’s total carbon footprint while supporting the broader transition to Green Building Materials.

Low-carbon materials reduced construction energy use by 22.3%, including a 27.4% reduction in material-processing energy, and cut lifecycle carbon emissions by 29.8%. These figures show that switching to lower-emission inputs is not a marginal adjustment — it is a structural shift in how buildings consume energy from raw material through to end-of-life.

IIT Indore’s cement-free geopolymer concrete can cut CO₂ emissions by 80% and construction costs by up to 20% while achieving high strength in just three days. This development signals that performance and cost are no longer trade-offs — a combination that removes the last pricing objection for developers in cost-sensitive markets.

Material Category Insights

Structural materials dominates with 39.2% due to high-volume embodied-carbon exposure in core building frames.

In 2025, Structural materials held a dominant market position in the By Material Category segment of the Carbon Neutral Construction Materials Market, with a 39.2% share. Structural components — steel, concrete, and timber — carry the highest embodied-carbon load per building. Decarbonizing them delivers the greatest measurable emissions cut per procurement decision. Based on data from BuildSteel, low-embodied-carbon steel made via electric arc furnace routes can deliver up to 30% less embodied carbon than steel made through conventional raw-material inputs — a margin large enough to shift specification decisions at scale.

Finishing materials cover surface applications including paints, coatings, tiles, and cladding. Buyer demand for low-emission finishes is rising as whole-building lifecycle assessments become standard in commercial projects. Vendors offering verified Environmental Product Declarations are capturing a growing share of architecture-specified purchases.

Insulation materials attract interest from both new builds and retrofit projects. Bio-based and recycled-content insulation products are gaining ground in European markets, where building energy performance rules create a consistent procurement driver across residential and commercial sectors.

Carbon Strategy Insights

Carbon-reducing materials dominates with 46.5% due to established supply chains and proven performance track records.

In 2025, Carbon-reducing materials held a dominant market position in the By Carbon Strategy segment of the Carbon Neutral Construction Materials Market, with a 46.5% share. These materials lower emissions relative to conventional alternatives without requiring full carbon neutrality certification. Their commercial maturity means buyers face less procurement risk than with carbon-negative or sequestering alternatives still in early rollout. CarbonCure’s technology, used by concrete producers, typically achieves 3–5% less cement use per pour — a small per-batch saving that compounds into meaningful tonnage reductions across large-volume buyers.

Carbon-neutral materials represent the fastest-growing sub-segment by buyer inquiry. These are products where lifecycle emissions are fully offset through certified credits or verified sequestration. Heidelberg Materials pre-sold all of its 2025 output of zero-emissions cement from its Brevik plant — clear evidence that verified net-zero products command premium pricing and face no demand shortfall when supply is constrained.

Carbon-negative materials absorb more CO₂ than they emit across their lifecycle. Mass timber, hempcrete, and bio-based composites represent the core of this sub-segment. Timber pile research shows embodied-carbon reductions of about 70% in clayey soils compared with solid concrete piles — a performance advantage that is now quantified in environmental product declarations used in competitive tenders.

Carbon-sequestering materials go further by permanently locking carbon into the built environment. Technologies such as mineralized CO₂ injection into concrete, as used by CarbonCure, and bio-based composites storing atmospheric carbon define this emerging category. CarbonCure’s 2025 case study shows that every 1 metric ton of CO₂ mineralized in ready-mix concrete enables roughly 50 metric tons of CO₂ reduction through combined cement savings and sequestration.

Building Type Insights

Residential dominates with 42.7% due to large project volumes and rising green home buyer expectations.

In 2025, Residential held a dominant market position in the By Building Type segment of the Carbon Neutral Construction Materials Market, with a 42.7% share. Housing construction generates the broadest material demand base. Government-backed affordable housing programs with embodied-carbon requirements — such as France’s circular concrete housing projects using 100% recycled materials — are extending low-carbon procurement beyond premium developments into mass-market builds.

Commercial buildings drive high-value per-project spend. Hyperscale data center developers, including AWS, are now specifying fossil-free structural materials for new digital infrastructure builds. This procurement shift is pulling forward demand for fossil-free steel at volumes that justify new supply agreements and long-term off-take contracts.

Industrial buildings are increasingly constructed with low-carbon structural steel and recycled concrete. Sweden’s first commercial building made with SSAB fossil-free steel and Ruukki structural systems demonstrates that the industrial sector can serve as a live showcase for next-generation material supply chains.

Certification Alignment Insights

LEED dominates with 37.4% due to global recognition and deep integration in commercial project financing.

In 2025, LEED held a dominant market position in the By Certification Alignment segment of the Carbon Neutral Construction Materials Market, with a 37.4% share. LEED certification is a financing and leasing requirement in many Class A commercial markets, creating mandatory material-quality floors that channel procurement toward low-carbon suppliers. Its global reach and recognizability make it the default standard for cross-border institutional investors assessing building asset quality.

IGBC drives material specification in India’s commercial real estate sector. As India’s urban commercial pipeline expands, IGBC-aligned projects create growing local demand for LC3 cement, geopolymer concrete, and other low-carbon inputs that meet its environmental performance criteria.

BREEAM remains the dominant certification in the UK and parts of Europe. Its material credits system rewards suppliers with verified Environmental Product Declarations, giving certified low-carbon materials a direct scoring advantage in competitive project tenders.

Buyer Type Insights

Developers dominate with 32.9% due to volume purchasing power and green asset value incentives.

In 2025, Developers held a dominant market position in the By Buyer Type segment of the Carbon Neutral Construction Materials Market, with a 32.9% share. Property developers control the material specification decision at the earliest stage of a project and face direct pressure from ESG-focused investors and green building certification requirements. This combination makes developers the most influential buyer group in redirecting construction spend toward low-carbon suppliers.

Architects shape material choices through specification before tender. As embodied-carbon design tools become standard practice in architecture, early-stage material selection increasingly favors suppliers with published and verified lifecycle assessment data over those without.

EPC contractors buy in large quantities under fixed-price contracts. Their adoption of low-carbon materials depends on supply reliability and cost parity. Where those conditions are met — as with recycled-content concrete in Western Europe — EPC procurement has become a consistent volume driver for circular construction material suppliers.

Distribution Channel Insights

Direct B2B procurement dominates with 41.6% due to volume discounts and supply reliability requirements.

In 2025, Direct B2B procurement held a dominant market position in the By Distribution Channel segment of the Carbon Neutral Construction Materials Market, with a 41.6% share. Large developers, EPC contractors, and institutional buyers purchase directly from manufacturers to secure consistent product quality, verified environmental credentials, and pricing terms that distributors cannot match. This channel also allows supply agreements to be tied to specific project embodied-carbon targets.

Construction distributors serve mid-size contractors and regional builders who lack the scale for direct manufacturer relationships. Their ability to stock and deliver multiple low-carbon product lines makes them a critical channel for broadening market reach beyond major metro projects.

Specialty sustainability suppliers focus exclusively on low-carbon, circular, and bio-based materials. Their expertise in Environmental Product Declarations and certification alignment makes them the preferred procurement partner for architects and green consultants working on high-certification projects.

End-Use Insights

New construction dominates with 54.1% due to design-stage integration and whole-building carbon accounting.

In 2025, New construction held a dominant market position in the By End-Use segment of the Carbon Neutral Construction Materials Market, with a 54.1% share. New builds allow full material optimization from the design stage, enabling whole-building lifecycle carbon assessments that drive specification toward verified low-emission inputs. This design-led procurement advantage, combined with the volume of new construction activity across Asia, the Middle East, and North America, makes new construction the largest and most structurally consistent demand channel.

Retrofitting is a fast-growing end-use as existing building stock comes under pressure to meet net-zero targets. Insulation, envelope upgrades, and low-carbon roofing systems dominate retrofit material demand, with Europe’s building renovation wave creating the largest near-term pipeline.

Prefabrication offers a high-leverage channel for low-carbon material adoption, as off-site manufacturing allows tighter process control and material efficiency than site-built construction. Factory production reduces waste and enables consistent use of recycled-content and bio-based inputs at scale.

Market Segments Covered in the Report

By Material Category

- Structural materials

- Finishing materials

- Insulation materials

- Envelope materials

- Roofing systems

- Flooring systems

By Carbon Strategy

- Carbon-reducing materials

- Carbon-neutral materials

- Carbon-negative materials

- Carbon-sequestering materials

By Building Type

- Residential

- Commercial

- Industrial

- Institutional

By Certification Alignment

- LEED

- IGBC

- GRIHA

- BREEAM

- WELL

By Buyer Type

- Developers

- Architects

- EPC contractors

- Government agencies

- Infrastructure companies

- Green consultants

By Distribution Channel

- Direct B2B procurement

- Construction distributors

- OEM partnerships

- Online procurement platforms

- Specialty sustainability suppliers

By End-Use

- New construction

- Retrofitting

- Renovation

- Prefabrication

- Modular construction

Regional Insights

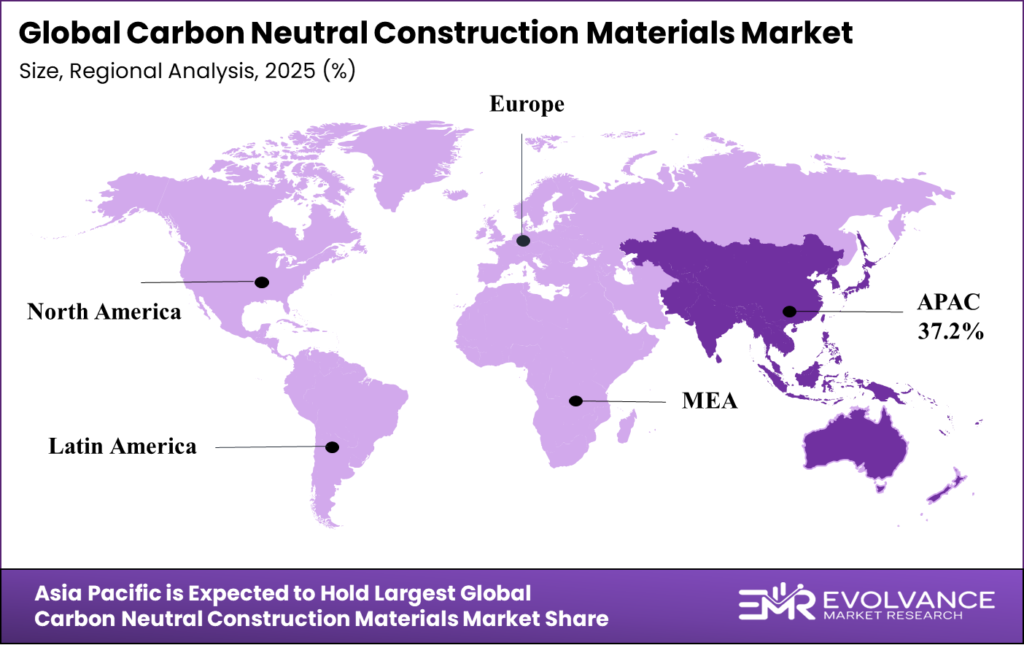

Asia Pacific Dominates the Carbon Neutral Construction Materials Market with a Market Share of 37.2%, Valued at USD 6.78 Billion

Asia Pacific holds 37.2% of the global market, valued at USD 6.78 Billion, driven by China’s national carbon-neutrality commitments and India’s growing adoption of low-carbon cement technologies. India’s first use of LC3 cement at Noida International Airport — emitting up to 40% less CO₂ than Portland cement at 25% lower production cost — signals that cost parity is removing the primary adoption barrier across price-sensitive high-volume Asian markets. This makes APAC the largest and fastest-converting regional demand base.

North America Carbon Neutral Construction Materials Market Trends

North America holds the second-largest regional position, driven by U.S. federal Buy Clean policies and state-level embodied-carbon limits entering building codes. The Department of Energy’s discussions worth up to $500 million for fossil-free steel expansion in Iowa directly links public investment to supply scaling. This level of government procurement commitment signals that the U.S. market is moving from pilot projects toward procurement at national infrastructure program scale.

Europe Carbon Neutral Construction Materials Market Trends

Europe leads in regulatory maturity, with embodied-carbon limits embedded in national building codes across France, the Netherlands, and Finland. The EU Taxonomy and Carbon Border Adjustment Mechanism are pushing construction supply chains toward verified low-emission inputs. Holcim’s ECOCycle platform — using up to 100% recycled demolition materials across more than 100 recycling centers — shows European circular construction moving from concept to industrial-scale operation.

Latin America Carbon Neutral Construction Materials Market Trends

Latin America is an early-stage but structurally important market. Brazil’s social housing programs and Mexico’s urban infrastructure investment create volume demand that is beginning to attract low-carbon material suppliers. Green building certification adoption in commercial real estate in São Paulo and Mexico City is creating an initial high-value demand base that will expand as regulatory requirements follow.

Middle East and Africa Carbon Neutral Construction Materials Market Trends

The Middle East’s mega-project pipeline — including NEOM and multiple net-zero urban developments in the UAE — is creating concentrated, high-value demand for verified low-carbon structural and finishing materials. Governments in the GCC are embedding green building standards into large-scale construction programs. Africa’s market is earlier-stage, with South Africa leading through green building council activity and select institutional projects setting embodied-carbon benchmarks.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

In 2024, the U.S. General Services Administration expanded its Buy Clean Construction Materials initiative, requiring federal building projects to meet embodied-carbon thresholds for steel, concrete, glass, and flat glass. This rule applies to new federal construction contracts above specified value thresholds and directly shapes procurement volumes in the world’s largest single-buyer construction market.

The European Union’s 2024 revision of the Energy Performance of Buildings Directive added embodied-carbon reporting requirements for new large commercial buildings, phasing into mandatory limits by 2030. Member states including France and the Netherlands introduced national embodied-carbon caps ahead of the EU-wide deadline, accelerating specification of low-carbon structural and finishing materials in those markets.

In 2024, the UK’s Future Homes Standard consultation included embodied-carbon provisions requiring whole-life carbon assessments for new residential builds. Combined with the Green Public Procurement criteria requiring Environmental Product Declarations for government contracts, these standards are embedding lifecycle carbon data as a procurement requirement across both public and private UK construction.

Driving Factors

Industrial Decarbonization Investment and Technology Launch Drive Low-Carbon Material Supply

Holcim’s 2024 launch of Europe’s first industrial-scale calcined clay cement plant in France, producing 500,000 tons of ECOPlanet cement annually with a 50% lower CO₂ footprint than conventional CEM I, shows that low-carbon material production has crossed the threshold from pilot to commercial scale. This is not a marginal efficiency gain — it cuts cement’s carbon intensity in half on a per-ton basis, which changes the economic math for developers facing embodied-carbon limits.

A 2025 academic study found that using low-carbon materials reduced construction energy use by 22.3% and cut lifecycle carbon emissions by 29.8%. These performance figures give buyers quantified evidence to support specification decisions, removing the uncertainty that previously slowed adoption. When a buyer can prove measurable carbon and energy savings, low-carbon material selection becomes a risk management decision, not just a values choice.

SSAB’s 2024 strategic supply agreements with Firth Steels and AWS for fossil-free structural steel signal that hyperscale commercial buyers are locking in supply before the market tightens. This type of long-term off-take commitment from anchor customers gives material producers the revenue visibility needed to justify large-scale capital investment in new production capacity.

Restraints

High Capital Requirements Slow Production Scale-Up for Fossil-Free Construction Materials

SSAB’s fossil-free mini-mill in Sweden requires a €4.5 billion capital investment for operations scheduled to begin in 2028. This level of upfront cost means that fossil-free steel production will remain capacity-constrained for years. Buyers seeking to specify fossil-free structural steel at volume face supply availability limits that no amount of procurement intent can resolve in the near term.

The capital barrier is not unique to steel. Carbon-negative cement, bio-based insulation at industrial scale, and low-carbon glass all require new production infrastructure that existing manufacturers are only beginning to fund. These investment cycles run five to ten years from commitment to full output. Market growth will outpace production capacity across several material categories through the late 2020s.

Limited availability of scrap steel and green hydrogen supply chains restricts scalable production of near-zero-emission structural steel for global construction demand. Without reliable, low-cost green hydrogen, fossil-free steel production costs remain above conventional alternatives in most markets — a pricing gap that slows adoption among buyers without explicit carbon procurement mandates or green financing incentives.

Opportunity

Circular Construction Models and EAF Expansion Create New Supply and Demand Pathways

France’s large-scale affordable housing projects using 100% recycled concrete materials are creating a replicable model for urban circular construction across Europe. When recycled-content concrete delivers cost-competitive performance in government-funded mass housing, it establishes a procurement template that other national housing programs can adopt without the premium pricing risk that previously limited circular material adoption.

According to EMR, 93% of newly announced 2024 steel projects targeted lower-emission electric arc furnace technology instead of coal blast furnaces. This shift in capital allocation means that the next generation of global steel production capacity is being built around lower-emission methods — a structural change that will reduce the cost premium for low-embodied-carbon steel across all construction buyer segments within this decade.

Heidelberg Materials’ Brevik CCS plant captures about 400,000 metric tons of CO₂ per year — roughly 50% of the plant’s total emissions. The fact that Heidelberg pre-sold its entire 2025 output from this facility confirms that buyer appetite for verified net-zero cement exceeds current supply. That demand-supply gap is the clearest market signal available for where new capital investment in low-carbon cement production will generate returns.

Trends

Recycled Feedstocks and Fossil-Free Building Systems Define the Next Production Standard

Holcim has set a target of 20 million tons of recycled construction materials annually in Europe by 2030, backed by its ECOCycle platform operating across more than 100 recycling centers globally. This scale of circular material processing signals a shift from waste diversion as a side activity to recycled demolition feedstock becoming a primary raw material input for mainstream concrete production.

Sweden’s first commercial building made with SSAB fossil-free steel and Ruukki structural systems marks a transition point. Industrial buildings are not premium showcase projects — they are high-volume, cost-sensitive builds. When fossil-free steel is specified in a standard industrial building, it means the product has crossed the cost and availability threshold required for broad adoption beyond prestige commercial projects.

Warm-mix asphalt lifecycle assessments show 18% lower fossil-fuel use and 24% lower air-pollutant emissions than standard hot-mix asphalt. Infrastructure spending on roads and pavements represents one of the highest-volume material procurement categories in construction. This performance data, combined with the ability to blend in up to 50% reclaimed asphalt in sub-surface layers per UK road standards, gives infrastructure agencies a cost-effective and verified path to embodied-carbon reduction at national scale.

Carbon Neutral Construction Materials Market Key Companies Insights

Holcim has built a multi-pronged low-carbon position that is hard to replicate at speed. Its ECOPlanet cement range — anchored by Europe’s first industrial calcined clay plant in France producing 500,000 tons annually — gives it a verified low-carbon product at commercial scale. The ECOCycle platform adds circular feedstock capability across more than 100 recycling centers. This combination of new-material production and circular input sourcing creates a dual cost advantage over competitors who have invested in only one pathway.

Heidelberg Materials occupies a singular position in the net-zero cement segment with its Brevik CCS plant. Pre-selling its entire 2025 net-zero cement output before the year began demonstrates that verified zero-emission cement commands a demand premium that justifies the carbon capture capital cost. This gives Heidelberg a first-mover advantage in supplying certified net-zero cement to the most sustainability-focused institutional and commercial buyers — a segment likely to grow as embodied-carbon targets tighten.

CEMEX has pursued low-carbon innovation through strategic investment in early-stage technology companies. Its participation in Cambridge Electric Cement’s £2.25 million funding round alongside Legal & General reflects a strategy of acquiring optionality in breakthrough cement technologies before they reach commercial scale. This positions CEMEX to integrate recycled cement production from electric arc furnace steel slag into its product range as the technology matures, without bearing full development cost alone.

CarbonCure operates a capital-efficient model by retrofitting its CO₂ mineralization technology into existing concrete plants rather than building new facilities. Its technology enables producers to achieve 3–5% less cement use per pour, and its 2025 case study with Deloitte demonstrates that every 1 metric ton of CO₂ mineralized enables roughly 50 metric tons of total CO₂ reduction. This multiplier effect means CarbonCure’s market value is not measured in direct CO₂ capture alone — it is measured in the much larger cement reduction it enables across its network of partner producers.

Key Companies

- Holcim

- Heidelberg Materials

- CEMEX

- Kingspan

- Saint-Gobain

- Plantd

- Hempitecture

- GreenJams

- CarbonCure

- CarbiCrete

- Carbonaide

- Skanska

- AECOM

- L&T

- ArcelorMittal

- Tata Steel

- Nucor

- Stora Enso

- Mercer Mass Timber

Recent Development

- In February 2024, Sublime Systems secured $75 million in Series C funding led by CRH Ventures, Holcim, and Lowercarbon Capital to commercialize its electrochemical low-carbon cement technology in the United States.

- In May 2024, Cambridge Electric Cement raised £2.25 million from investors including Legal & General and Cemex Ventures to scale recycled cement production using electric arc furnace steel slag.

- In September 2024, Brimstone received up to $189 million in U.S. Department of Energy support for its carbon-negative cement manufacturing plant in Nevada.

- In April 2024, Holcim launched Europe’s first industrial-scale calcined clay cement plant in Saint-Pierre-La-Cour, France, capable of producing 500,000 tons annually of low-carbon ECOPlanet cement.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 18.09 Billion |

| Forecast Revenue (2035) | USD 45.24 Billion |

| CAGR (2026-2035) | 9.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Category (Structural materials, Finishing materials, Insulation materials, Envelope materials, Roofing systems, Flooring systems), By Carbon Strategy (Carbon-reducing materials, Carbon-neutral materials, Carbon-negative materials, Carbon-sequestering materials), By Building Type (Residential, Commercial, Industrial, Institutional), By Certification Alignment (LEED, IGBC, GRIHA, BREEAM, WELL), By Buyer Type (Developers, Architects, EPC contractors, Government agencies, Infrastructure companies, Green consultants), By Distribution Channel (Direct B2B procurement, Construction distributors, OEM partnerships, Online procurement platforms, Specialty sustainability suppliers), By End-Use (New construction, Retrofitting, Renovation, Prefabrication, Modular construction) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Holcim, Heidelberg Materials, CEMEX, Kingspan, Saint-Gobain, Plantd, Hempitecture, GreenJams, CarbonCure, CarbiCrete, Carbonaide, Skanska, AECOM, L&T, ArcelorMittal, Tata Steel, Nucor, Stora Enso, Mercer Mass Timber |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |