What is the Green Building Materials Market Size?

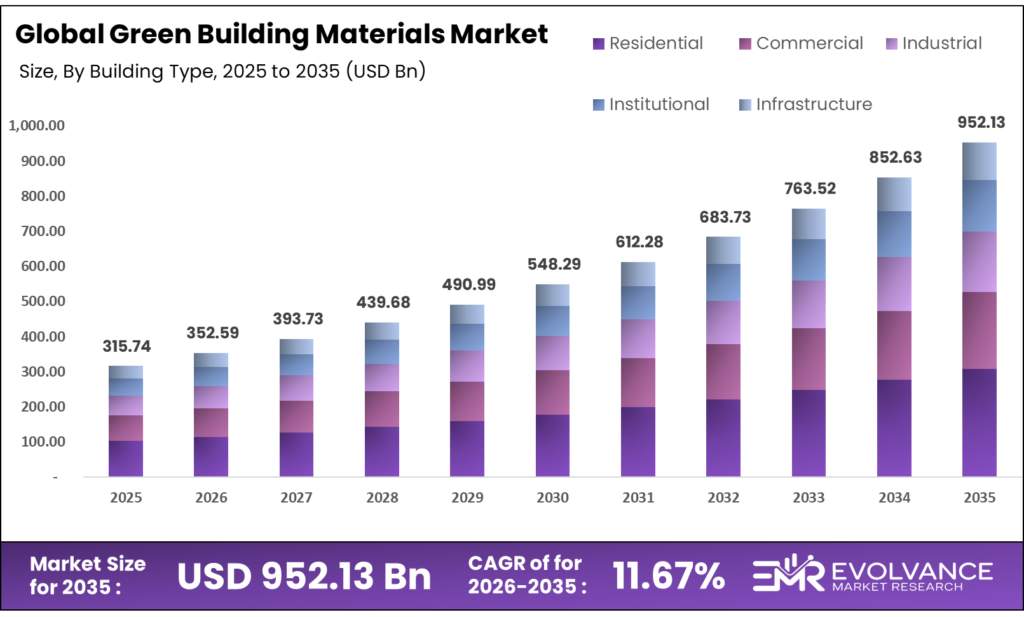

The Global Green Building Materials Market size will be worth around USD 952.13 Billion by 2035 from USD 315.74 Billion in 2025, growing at a CAGR of 11.67% during the forecast period 2026 to 2035. Federal procurement mandates and government-backed clean material programs are pulling spend away from conventional products at scale. Real estate developers and contractors are shifting budgets toward certified low-carbon materials as carbon disclosure norms tighten across major markets. Supply-side constraints remain, as large-scale carbon-capture cement plants require heavy public subsidies to reach commercial output.

Market Highlights

- The Global Green Building Materials Market size grows from USD 315.74 Billion in 2025 to USD 952.13 Billion by 2035, at a CAGR of 11.67%.

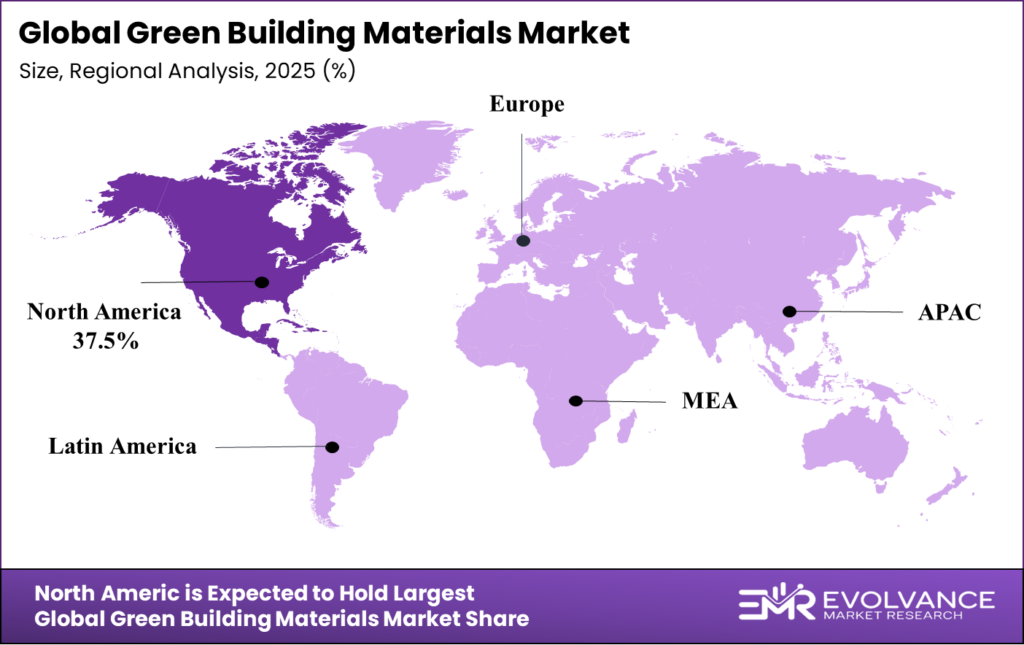

- North America leads all regions with a 37.5% share, valued at USD 118.40 Billion.

- Residential building type holds the largest segment share at 44.1%.

- LEED certification alignment dominates with 41.7% share among certification segments.

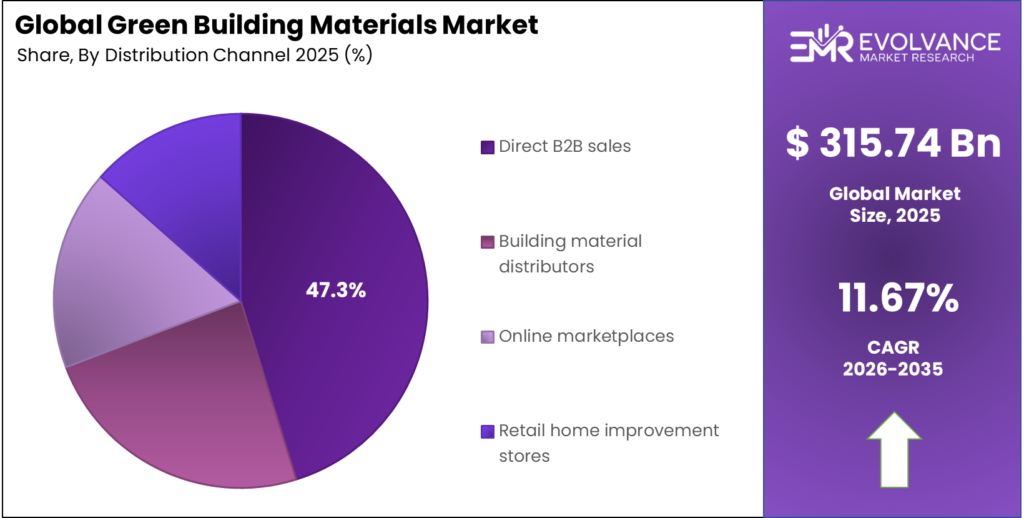

- Direct B2B sales leads distribution channels with 47.3% share.

- Real estate developers are the top buyer type at 34.6% of demand.

Market Overview

Green building materials include products that cut carbon emissions, improve energy performance, and meet environmental certification standards across construction projects. This covers low-carbon cement, mass timber, recycled aggregates, insulation systems, and certified glass and steel. These materials now sit at the center of procurement decisions for developers, government agencies, and large contractors.

The market spans four main buyer segments — residential, commercial, industrial, and institutional — with each applying different certification and performance criteria. Residential buyers focus on cost and energy savings. Commercial and institutional buyers prioritize LEED and BREEAM alignment to meet regulatory and investor-reporting needs. Industrial buyers track embodied carbon targets tied to national decarbonization commitments.

Government funding is reshaping the supply side at speed. The U.S. EPA’s July 2024 allocation of nearly $160 million to 38 clean construction material production projects shows that public capital is now actively de-risking new green material technologies. This reduces the barrier to entry for low-carbon cement, recycled content products, and next-generation aggregates entering mainstream supply chains.

The demand for Green Building Materials has surged as the construction industry seeks more sustainable alternatives to traditional resources. These materials reduce environmental impact by minimizing waste, improving energy efficiency, and lowering emissions throughout a building’s lifecycle. For projects targeting net-zero goals, pairing green materials with Carbon Neutral Construction Materials creates a powerful foundation for responsible development.

According to RICS, 46% of construction professionals do not measure carbon across projects, up from 34% in 2024. This gap between stated sustainability goals and actual tracking practice signals that demand for third-party verified green materials will accelerate as reporting norms tighten — creating a direct revenue opportunity for certified product suppliers.

Research by RMI shows that proven low-embodied-carbon building solutions can cut upfront embodied carbon by 19–46% with a cost premium of less than 1%. This cost-parity evidence removes the single biggest buyer objection — price — and positions certified green materials as the default rational choice for informed procurement teams.

Building Type Insights

Residential dominates with 44.1% due to volume scale and retrofit demand.

In 2025, Residential held a dominant market position in the By Building Type segment of the Green Building Materials Market, with a 44.1% share. Homeowner demand for energy-efficient insulation, low-emission paints, and certified timber drives consistent volume across new builds and retrofits. Government subsidy programs in North America and Europe directly target residential upgrades, keeping purchase rates high even during tighter credit cycles.

Commercial projects consume a disproportionately high value of green materials per square foot, driven by LEED and BREEAM certification requirements tied to tenant ESG commitments and lender green finance conditions. Office and retail developers face growing pressure from institutional investors to disclose embodied carbon data, making certified product sourcing a non-negotiable procurement step rather than an optional add-on.

Industrial facilities are earlier in their green material adoption curve, but the shift is accelerating. Lafarge Canada’s 2024 Alberta facility, projected to divert 120,000 tonnes of demolition waste annually while cutting plant emissions by up to 30,000 tonnes per year, demonstrates that industrial operators are now treating recycled-content building products as both a compliance tool and a cost-reduction strategy.

Certification Alignment Insights

LEED dominates with 41.7% due to global recognition and mandatory adoption in key markets.

In 2025, LEED held a dominant market position in the By Certification Alignment segment of the Green Building Materials Market, with a 41.7% share. LEED certification is embedded in green finance frameworks, corporate real estate policies, and government procurement rules across North America and parts of Asia. Developers who target LEED-certified projects face narrow approved-product lists, which concentrates spend with a smaller number of verified green material suppliers and raises their pricing power.

IGBC (Indian Green Building Council) certification drives material demand across India’s fast-growing commercial and residential construction sector. As India’s urban building stock expands and developers seek premium pricing on certified projects, IGBC-aligned products are gaining shelf space with domestic distributors who previously focused on standard-grade materials.

Buyer Type Insights

Real Estate Developers dominate with 34.6% due to volume procurement and ESG reporting pressure.

In 2025, Real Estate Developers held a dominant market position in the By Buyer Type segment of the Green Building Materials Market, with a 34.6% share. Developers control project-level specification decisions across thousands of units at a time, giving them outsized influence over material selection. As green finance conditions tied to embodied carbon scores become standard in project lending, developers are converting from opportunistic buyers of certified products to systematic ones.

Architects act as early-stage gatekeepers in material selection, embedding green product specifications into design documents before procurement teams engage. Their growing reliance on embodied-carbon tools — supported by the nearly 150,000 EC3-verified EPDs added since 2019 — means low-carbon materials are increasingly locked in before cost-optimization rounds can substitute them out.

Contractors face rising contractual obligations to meet embodied carbon targets set by developers and public clients, shifting their role from passive material buyers to active low-carbon procurement managers. This shift is creating new demand for supplier scorecards, EPD documentation, and carbon calculation tools at the field level.

Distribution Channel Insights

Direct B2B sales dominate with 47.3% due to project scale and specification-driven procurement.

In 2025, Direct B2B Sales held a dominant market position in the By Distribution Channel segment of the Green Building Materials Market, with a 47.3% share. Large developers, contractors, and government agencies purchase green materials directly from manufacturers to secure volume pricing, verified EPD documentation, and supply continuity.

Building material distributors serve as the primary access point for mid-tier contractors, architects, and smaller developers who lack direct manufacturer relationships. As green product ranges expand, distributors who invest in trained sales staff and EPD documentation libraries will capture a larger share of the specification-driven purchasing process.

Online marketplaces are beginning to disrupt traditional distribution by enabling price and carbon data comparison across competing products at scale. For commodity green materials — recycled aggregates, certified insulation, low-VOC paints — digital purchasing removes the friction that previously favored incumbent suppliers with strong distributor relationships.

Market Segments Covered in the Report

By Building Type

- Residential

- Commercial

- Industrial

- Institutional

- Infrastructure

By Certification Alignment

- LEED

- IGBC

- GRIHA

- BREEAM

By Buyer Type

- Real Estate Developers

- Architects

- Contractors

- Government Agencies

- Facility Managers

- Homeowners

By Distribution Channel

- Direct B2B Sales

- Building Material Distributors

- Online Marketplaces

- Retail Home Improvement Stores

Regional Insights

North America Dominates the Green Building Materials Market with a Market Share of 37.5%, Valued at USD 118.40 Billion

North America holds 37.5% share, valued at USD 118.40 Billion, because federal procurement mandates now set binding carbon thresholds for public construction. The GSA’s 2025 GWP limits for concrete, cement, asphalt, and glass create a mandatory floor for green material adoption in federal projects. This regulatory pull — combined with mature LEED infrastructure and active EPA grant programs — gives North American suppliers both a defined market and a funded growth pathway.

Europe Green Building Materials Market Trends

Europe’s green building material demand is shaped by EU taxonomy-aligned sustainable finance rules and mandatory BREEAM or DGNB certification requirements across institutional and commercial construction. Germany’s €5 billion industrial decarbonization support program for cement and steel signals that public capital is actively subsidizing the supply side. UK-based projects, including Heidelberg Materials’ Padeswood CCS facility designed to capture 800,000 tonnes of CO₂ per year, show that European producers are investing at scale ahead of regulatory tightening.

Asia Pacific Green Building Materials Market Trends

Asia Pacific is the fastest-expanding regional opportunity, driven by China’s green building code upgrades, India’s IGBC and GRIHA certification growth, and Southeast Asia’s net-zero policy commitments. SCG’s June 2024 launch of SCG Low Carbon Super Cement, aligned with Vietnam’s Net Zero 2050 roadmap, shows regional producers are moving to capture first-mover advantage before import competition scales. The region’s construction volume makes even a small green material share shift a large absolute revenue gain.

Latin America Green Building Materials Market Trends

Latin America’s green building market is at an earlier stage, but Brazil and Mexico are seeing growing green certification activity in commercial real estate tied to multinational tenant ESG requirements. Climate Investment Funds’ October 2024 plan to mobilize up to $1 billion for decarbonization in developing economies, including cement and steel, gives regional producers access to concessional finance that can close the cost gap on low-carbon material production at scale.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The U.S. EPA launched its “Label Program for Low Embodied Carbon Construction Materials” in August 2024, backed by a $100 million Buy Clean initiative. This program sets verified carbon thresholds for federal procurement of concrete, steel, glass, and asphalt — effectively making low-carbon material certification a prerequisite for access to U.S. federal construction contracts.

The U.S. General Services Administration (GSA) issued binding 2025 low-embodied-carbon GWP thresholds for key construction products. These include 284 kgCO₂e/m³ for 4,000 PSI concrete, 751 kgCO₂e/t for cement, 217 kgCO₂e/m³ for CMU, 55.4 kgCO₂e/t for asphalt, and 1,331 kgCO₂e/t for flat glass. Suppliers who cannot meet these thresholds lose access to a significant federal procurement pool.

In July 2024, the U.S. EPA allocated nearly $160 million to 38 clean construction material production projects. This grant program directly de-risks the capital cost of building new low-carbon material facilities, accelerating commercialization timelines that would otherwise face multi-year financing gaps. Producers with active EPA grant relationships gain a structural cost advantage over unfunded peers.

Germany activated a €5 billion industrial decarbonization support program targeting cement and steel sectors. Norway’s Longship CCS project and Heidelberg Materials’ Brevik CCS facility — designed to capture around 400,000 tonnes of CO₂ per year — operate under European regulatory frameworks that require public subsidy co-investment for large-scale carbon capture projects to reach financial close.

Drivers

Federal Procurement Mandates and EPA Grant Programs Accelerate Low-Carbon Material Adoption

The U.S. EPA’s Buy Clean initiative and its August 2024 label program for low-embodied-carbon materials have turned federal construction contracts into a performance-based market. Suppliers who meet verified carbon thresholds gain direct access to federal buyers. Those who do not are effectively excluded, creating a binary compliance requirement that forces product reformulation across the supply chain.

The EPA’s $160 million grant allocation to 38 clean construction material projects in July 2024 shows that government is not just regulating — it is funding supply-side transformation. This capital reduces the financial risk for producers investing in carbon-neutral manufacturing, which means the pipeline of compliant products entering the market will grow faster than regulatory timelines alone would suggest.

Moreover, Holcim Germany’s April 2024 Lägerdorf carbon-capture cement plant — designed to capture approximately 1.2 million tonnes of CO₂ annually — shows that large incumbent producers are committing capital ahead of regulatory mandates. This early investment by market leaders raises the performance bar for all competitors and signals that low-carbon manufacturing will become the industry standard rather than a niche offering.

Restraints

Slow Certification Processes and High Capital Costs Delay Market-Ready Low-Carbon Supply

Ecocem’s ACT cement product, which cuts clinker concentration to approximately 20% versus the traditional 35% norm, is still awaiting European technical certification and broader standards integration until at least 2026. This approval lag means a proven low-carbon product sits outside mainstream procurement for an extended period — costing producers revenue and slowing buyer access to better-performing materials.

Carbon-capture-enabled building material plants require large public subsidies to reach financial close. Norway’s Longship CCS project and Germany’s €5 billion industrial decarbonization program both demonstrate that private capital alone cannot fund these assets at the required scale. This public-finance dependency creates timing risk — if government funding cycles shift, project pipelines stall and supply growth falls behind demand.

Additionally, RICS data shows 30% of construction professionals cite insufficient knowledge and skills as a barrier to cutting embodied carbon. This skills gap slows the translation of available green materials into actual project specifications. Even when certified products are available and cost-competitive, adoption stalls when procurement teams lack the technical capacity to evaluate carbon data or navigate EPD documentation.

Growth Factors

Next-Generation Low-Carbon Cement Technologies and Industrial Waste Recycling Open New Revenue Streams

Material Evolution’s planned 150,000-ton annual production facility in Wales, announced in 2024, targets a reduction in embodied CO₂ emissions of up to 85% versus conventional cement. If this facility reaches commercial output on schedule, it positions ultra-low-carbon cement as a viable mainstream product — not just a pilot-scale experiment — which expands the addressable market for certified low-carbon materials significantly.

Lafarge Canada’s 2024 Alberta facility demonstrates that industrial-scale demolition waste recycling can simultaneously reduce cement plant emissions by up to 30,000 tonnes per year while diverting 120,000 tonnes of waste from landfill. This dual environmental and operational benefit improves the financial case for recycled-content building materials, especially in markets where waste disposal costs are rising and carbon credit mechanisms are active.

Furthermore, Heidelberg Materials pre-sold all 2025 production from its Norway-based evoZero net-zero cement facility before commercial launch. This sell-out before production starts is a rare commercial signal — it confirms that buyer demand for verified net-zero products already exceeds available supply, giving producers of ultra-low-carbon cement strong pricing power and low customer acquisition cost as they scale up capacity.

Emerging Trends

Embodied Carbon Labeling and Electrochemical Cement Startups Reshape Buyer Expectations

The EPA’s 2024 Buy Clean framework is normalizing centralized embodied-carbon registries and product labeling systems across U.S. federal construction. As EC3-verified EPDs have grown by nearly 150,000 since 2019, the infrastructure for comparing product-level carbon data at scale now exists. Buyers who previously accepted materials without carbon data will face growing internal and regulatory pressure to switch to labeled alternatives.

Startups including Sublime Systems, Fortera, and Brimstone are pursuing electrochemical and fossil-fuel-free alternatives to conventional limestone calcination — the single largest source of CO₂ in cement production. In September 2024, Sublime Systems secured a combined $75 million investment from CRH and Holcim to support its first commercial facility in Holyoke, Massachusetts. Incumbent producers co-investing in these startups signals that the next generation of cement technology is moving from lab to market faster than the industry expected.

However, RICS data shows that more than 60% of construction professionals report running carbon calculations and climate resilience assessments in fewer than half of their projects, or not at all. This measurement gap means the full market shift toward embodied-carbon-labelled products is still in early stages — giving suppliers and certification bodies a clear window to invest in tools, training, and standards that convert passive awareness into active purchasing decisions.

Key Companies Insights

Alumasc Group Plc positions itself as a specialist in building envelope and water management systems, serving commercial and residential construction across the UK and export markets. Its focus on roofing, facades, and drainage systems aligns directly with green building retrofit demand, where improving thermal performance and water management delivers measurable energy savings. Alumasc’s specialist niche insulates it from commodity pricing pressure while keeping it relevant to BREEAM-driven specification processes.

PPG Industries operates across coatings, sealants, and specialty glass — product categories that sit at the intersection of green building certification requirements and mainstream construction demand. PPG’s ability to supply low-VOC coatings and thermally efficient glass to both residential and commercial markets at scale gives it a broad footprint across certification-aligned procurement. Its global production network positions it well to respond to regional regulatory shifts, including GSA’s 2025 flat glass GWP threshold of 1,331 kgCO₂e/t.

BASF SE supplies insulation materials, concrete admixtures, and performance chemicals that directly enable green building product formulation across the supply chain. Its investment in Vateris — a technology that converts flue-gas CO₂ into a calcium-based concrete additive that can improve strength and cut cement use — reflects a strategy of building green material technology ownership rather than relying solely on product sales. This positions BASF as both a supplier and an IP holder in the low-carbon construction materials space.

DuPont brings advanced material science to building applications through its line of high-performance insulation films, vapor barriers, and construction membranes. Its products are embedded in high-specification residential and commercial envelopes where energy performance targets drive material selection. DuPont’s ability to demonstrate quantifiable energy reduction outcomes for architects and developers makes it a preferred specification choice in markets where building performance certifications carry financial value for developers.

Key Companies

- Alumasc Group Plc

- PPG Industries

- BASF SE

- DuPont

- Interface, Inc.

- Bauder Ltd

- BSW GROUP

- HOLCIM

- Owens Corning

- RedBuilt, LLC

- Forbo Group

- Kingspan Group plc

- CertainTeed Corporation

Recent Development

- In September 2024, Sublime Systems secured a combined $75 million investment from CRH and Holcim to accelerate its “true-zero” cement technology. The funding supports its first commercial facility in Holyoke, Massachusetts.

- In August 2024, Fortera raised $85 million in Series C funding to scale its ReAct low-carbon cement technology. The capital will expand operations beyond its California ReCarb plant.

- In October 2024, Climate Investment Funds announced plans to mobilize up to $1 billion for decarbonization technologies in cement, steel, and chemicals. The program targets developing economies where clean material production capacity is most constrained.

- In July 2024, CRH completed its acquisition of a majority stake in Australian building materials company Adbri, acquiring the remaining 57% of shares not held by Barro Group. The deal expands CRH’s low-carbon materials footprint into the Asia Pacific region.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 315.74 Billion |

| Forecast Revenue (2035) | USD 952.13 Billion |

| CAGR (2026-2035) | 11.67% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Building Type (Residential, Commercial, Industrial, Institutional, Infrastructure), By Certification Alignment (LEED, IGBC, GRIHA, BREEAM), By Buyer Type (Real Estate Developers, Architects, Contractors, Government Agencies, Facility Managers, Homeowners), By Distribution Channel (Direct B2B Sales, Building Material Distributors, Online Marketplaces, Retail Home Improvement Stores) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Alumasc Group Plc, PPG Industries, BASF SE, DuPont, Interface Inc., Bauder Ltd, BSW GROUP, HOLCIM, Owens Corning, RedBuilt LLC, Forbo Group, Kingspan Group plc, CertainTeed Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |