Executive Summary

Quick Insight: The US audiobooks market is projected to grow 2.6× by 2035, driven by streaming subscription maturity, AI-assisted narration reducing production costs, rising mobile listening penetration, and the rapid migration of podcast audiences into long-form audio content.

The US audiobooks market is the fastest-growing segment of the publishing and digital audio entertainment industry. Comprehensive audiobooks market research covers format economics, revenue model architecture, distribution channel performance, AI narration technology adoption, library lending dynamics, and the podcast-to-audiobook crossover for the 2026–2035 forecast period. Strategic decision-makers in publishing investment, content acquisition, and rights licensing will find data-driven frameworks for capital allocation, partnership strategy, and market positioning through 2035.

Key findings: The US audiobooks market reaches USD 6.96 billion in 2026 and compounds at an audiobook CAGR of 18.50% to USD 32.05 billion by 2035. Streaming subscription platforms command 52.4% of total format revenue. Audible holds a 41.2% distribution share. AI-narrated titles account for 14% of new 2026 releases. The library lending channel processes 600 million-plus annual checkouts. Three new analytical sections provide exclusive coverage not available in comparable market reports.

What Is the US Audiobooks Market?

The US audiobooks market was valued at USD 6.96 billion in 2026 and is projected to reach approximately USD 32.05 billion by 2035, growing at an audiobook CAGR of 18.50%. Streaming platform proliferation across Audible, Spotify, and Apple Books, combined with smart speaker and connected car penetration, drives structural market expansion. AI narration is reducing per-title production costs, enabling publishers to scale libraries at unprecedented velocity. Podcast listeners represent the fastest-growing first-time audiobook audience segment.

The US audiobooks market encompasses revenue generated by audiobook publishers across all audiobooks market channels, including streaming subscription fees, per-title purchases, library licensing fees, and OEM device bundle agreements. It excludes podcast-exclusive content and streaming music. Growth accelerates as mobile listening matures; smartphone audio app usage for spoken-word content grew 31% year-over-year in 2025, led by the 18-to-34 demographic.

The US audiobooks market includes over 62 million active listeners and 19 million premium subscribers in 2026. Audible, Spotify Audiobooks, and Scribd combined exceed 38 million monthly active users, confirming the audiobooks market scale.

US Audiobooks Market Highlights: Key Data at a Glance

- US audiobook market size 2026: USD 6.96 billion, forecast to USD 32.05 billion by 2035 at 18.50% CAGR

- Dominant format type: Streaming subscription with 52.4% revenue share

- Dominant revenue model: Subscription plans (Audible, Spotify, Scribd) with 48.3% share

- Dominant publisher tier: Big Five publishers with 42.8% combined revenue share

- Fastest-growing genre: Business, Self-Help, and Personal Finance audiobooks

- Total US audiobook listeners: 62 million individuals, 19 million premium subscribers

- Leading platforms: Audible, Spotify Audiobooks, Apple Books, Libby/OverDrive, Google Play Books

- Library channel volume: 600+ million annual checkouts via OverDrive/Libby

- Fastest-growing channel: Spotify Audiobooks at 38.7% YoY growth

- AI narration adoption: 14% of all new US audiobook releases use AI-generated narration in 2026

Market Overview: Why US Audiobooks Market Growth Is Accelerating

US audiobook industry trends in 2026 confirm growth across streaming subscription fees, per-title digital purchases, library lending licenses, institutional subscriptions, and device-bundled access agreements. Pure podcast content and traditional radio are excluded. Consumer multitasking behavior — driving, exercising, and household tasks — has created structural demand for screen-free audio content. The Audio Publishers Association (APA) reports double-digit year-over-year audiobook revenue growth since 2015.

Platform investment is a key accelerant. Spotify invested USD 1.1 billion in podcast and audiobook infrastructure from 2023 to 2025, expanding its library to 300,000 English-language titles by 2026. Amazon continues investing in Audible’s AI narration capabilities and Whispersync synchronization. Smart speaker household penetration exceeds 57% of US adults, with 34% using it regularly for audiobook playback.

Income diversification is improving publisher economics. By 2026, the average professional audiobook producer distributes across 4.2 platforms simultaneously, reducing single-platform dependency from the 75% Audible exclusivity reliance that dominated in 2022.

Format Type Analysis

Streaming Subscription Dominates with 52.4% Revenue Share

Audible, Spotify Audiobooks, and Scribd Drive the Subscription-First Growth Model

| Format Type | Share % | Primary Driver |

|---|---|---|

| Streaming Subscription (Audible / Spotify) | 52.4% | Monthly recurring subscription fees, credit-based access, and platform-native discovery driving listener retention |

| Digital Download / A La Carte (Apple Books / Google Play) | 24.8% | Per-title purchase revenue, premium celebrity narrator titles, and gift card redemption market |

| Library Digital Lending (OverDrive / Libby / hoopla) | 16.1% | Public library licensing agreements, institutional subscriptions, and Libby app listener acquisition |

| Physical CD / Vinyl Audio | 4.3% | Collector and gift market, older demographic preference, and specialty retail channels |

| Subscription Box / Curated Audio | 2.4% | Bundled physical and digital audiobook subscription services for premium consumer segments |

Streaming Subscription holds 52.4% of US audiobooks market format revenue share in 2026, making subscription-based access the dominant audiobook consumption model. Audible Premium Plus at USD 14.95 per month with one monthly credit reports over 15 million active global subscribers, with US listeners representing 58%. Spotify’s USD 10.99 Premium tier integration delivers 15 free monthly audiobook hours, accelerating mainstream listener acquisition at unprecedented scale.

Digital Download and A La Carte purchasing holds 24.8% of format revenue, driven by Apple Books one-tap purchasing and Google Play Books cross-device sync, with celebrity-narrated titles commanding USD 24.99 to USD 44.99. OverDrive reports 600 million digital checkouts through the Libby app across 90,000 partner libraries.

Revenue Model Analysis

Subscription Plans Lead with 48.3% Share of Audiobook Revenue

Streaming Platform Subscriptions Outpace Per-Title Purchases as Listener Acquisition Scales

| Revenue Model | Share % | Primary Driver |

|---|---|---|

| Subscription Plans (Audible, Spotify, Scribd) | 48.3% | Monthly recurring subscription revenue, credit system monetization, and platform listener retention economics |

| A La Carte Per-Title Purchases | 27.6% | Direct title purchases through Apple Books, Google Play, and Audible individual title sales |

| Library Licensing Fees | 14.2% | Publisher licensing revenue from OverDrive, hoopla, and cloudLibrary institutional agreements |

| Institutional / Education Subscriptions | 7.4% | Corporate wellness programs, university library licenses, and K-12 educational audiobook access deals |

| OEM / Device Bundle Agreements | 2.5% | Amazon Echo bundled Audible access, connected car manufacturer audiobook partnerships |

Audiobook subscription revenue holds a 48.3% share in 2026, making recurring fees the single largest revenue model. Audible’s credit system maintains a 78% utilization rate, reducing churn. Spotify’s audiobook bundle integration is the largest structural disruption to revenue model dynamics since Audible’s founding, inserting audiobook access into a subscription already held by 240 million Premium users worldwide.

Library Licensing Fees generate predictable institutional revenue independent of consumer discretionary cycles, with Big Five publishers negotiating multi-year OverDrive agreements worth hundreds of millions annually. The institutional education segment is the fastest-growing revenue model at 19.4% year-over-year, driven by corporate wellness programs and university system upgrades.

Publisher and Producer Tier Analysis

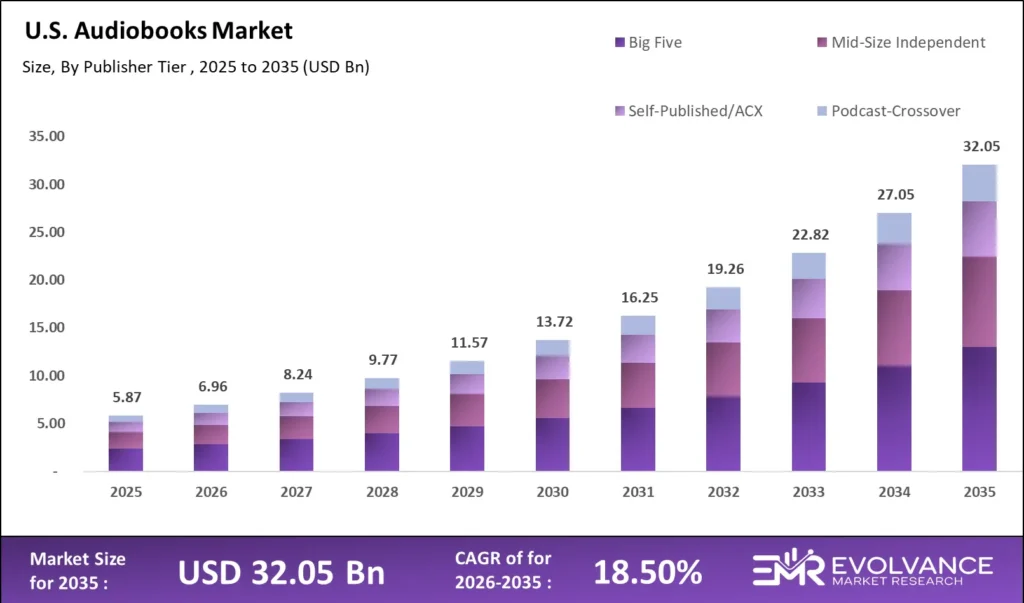

Big Five Publishers Capture 42.8% of US Audiobooks Revenue

Self-Published and Podcast-Crossover Producers Accelerate as AI Narration Reduces Barriers

| Publisher Tier | Output Volume | Revenue Share | Primary Monetization Driver |

|---|---|---|---|

| Big Five (PRH, HarperCollins, Simon & Schuster, Hachette, Macmillan) | 38,000+ titles/yr | 42.8% | Blockbuster titles, celebrity narrators, broad retail distribution |

| Mid-Size Independent Publishers | 22,000+ titles/yr | 21.4% | Genre specialization, niche subscriber audiences, Audible Original exclusives |

| Self-Published / ACX Producers | 85,000+ titles/yr | 18.7% | Royalty share contracts, AI narration adoption, KDP integration |

| Podcast-Crossover Productions | 6,200+ titles/yr | 9.6% | Existing podcast audiences, creator-to-audiobook pipeline, Spotify integration |

| Celebrity / Influencer Authored | 1,800+ titles/yr | 7.5% | Presale volume, media coverage, cross-platform audience conversion |

Big Five publishers collectively hold 42.8% of US audiobook revenue in 2026. Scale creates compounding advantages in narrator talent access, Audible Original deal leverage, and library licensing rate cards. The top 100 audiobook titles accounted for 18.4% of total market revenue in 2025. Michelle Obama’s “The Light We Carry” generated an estimated USD 28 million in audiobook revenue across platforms in its first 24 months.

Self-published producers on ACX release over 85,000 new titles annually as AI narration tools lower per-title production cost from USD 6,200 to under USD 180 using platforms including ElevenLabs and Murf. Podcast-crossover productions combine built-in audiences with lower marketing acquisition costs, representing the most structurally differentiated growth segment in the publisher tier landscape.

Genre Analysis: Six Segments Driving Audiobook Revenue

Business and Self-Help Leads Revenue-Per-Title Across All Platforms

Genre-by-Genre Audiobook Performance Benchmarks for 2026

| Genre | Revenue Share % | Avg. Annual Title Revenue | Top Monetization Model |

|---|---|---|---|

| Fiction (Thriller, Mystery, Romance, Fantasy) | 38.4% | USD 14,200 | Streaming subscription, series binge model, Audible Originals |

| Business, Self-Help & Personal Finance | 22.1% | USD 34,700 | A la carte purchase, corporate subscription, gift market |

| Non-Fiction (Memoir, True Crime, History) | 18.6% | USD 21,400 | Per-title purchase, library lending, celebrity narrator premium |

| Children’s & Young Adult | 10.4% | USD 9,800 | Library lending, family subscription plans, school licensing |

| Education & Professional Development | 7.2% | USD 28,100 | Institutional subscriptions, corporate learning platforms, LinkedIn Learning |

| Health, Wellness & Mindfulness | 3.3% | USD 17,600 | Subscription plan credit redemption, wellness app bundling |

Audiobook genre analysis confirms Fiction holds the largest volume share at 38.4% of revenue. The series model drives monetization: listeners completing book one convert to subsequent titles at a 64% rate. Thriller and mystery generate the highest completion rates at 81%, making them algorithmically favored across all streaming recommendation platforms.

Business, Self-Help, and Personal Finance titles generate the highest average annual revenue per title at USD 34,700 in 2026, driven by premium pricing power (USD 29.99 to USD 54.99 per title), corporate procurement for employee development programs, and premium brand CPMs that generate per-transaction revenue well above general category averages.

Children’s and Young Adult audiobooks are the highest-growth genre by new listener acquisition at 21.7% year-over-year, driven by school district and public library digital expansion programs. Library licensing fees for this genre grow at 18.4% annually.

Distribution Channel Analysis

Five Channels Define How US Consumers Access Audiobooks in 2026

Audible, Spotify, Library Lending, Apple Books, and Direct Publisher — Channel Breakdown

| Distribution Channel | Revenue Share % | Avg. Revenue per User | YoY Growth | Top Platform |

|---|---|---|---|---|

| Audible (Amazon Direct) | 41.2% | USD 178/yr | 8.4% | Audible Premium Plus, Audible Plus |

| Spotify Audiobooks | 14.8% | USD 132/yr | 38.7% | Spotify Premium bundle, 15hr/month access |

| Apple Books / Apple Podcasts+ | 11.4% | USD 156/yr | 12.1% | iOS native integration, Siri discovery |

| Public Library (Libby/OverDrive/hoopla) | 16.1% | USD 0 (library funded) | 18.4% | Libby app, hoopla unlimited |

| Google Play Books | 5.8% | USD 121/yr | 9.2% | Cross-device sync, Android integration |

| Direct Publisher / Findaway Voices | 6.2% | USD 94/yr | 14.6% | Wide distribution, non-exclusive |

| Other Retail (Barnes & Noble, Kobo) | 4.5% | USD 88/yr | 5.1% | NOOK Audio, Kobo Plus |

Audible market share of 41.2% distribution channel revenue in 2026 reflects Amazon ecosystem integration, 600,000-title catalog leadership, and Audible Original exclusives. However, Audible’s share has declined from 56% in 2022 as Spotify’s rapid integration captures incremental segments. Spotify Audiobooks is the fastest-growing channel at 38.7% YoY, adding an estimated 12 million new listeners in 2025 by converting existing Premium subscribers.

The public library channel via Libby and OverDrive processes 600 million-plus annual checkouts yet generates zero direct consumer revenue, instead creating library licensing fee income. Library audiobook discovery drives paid conversion, with 22% of new Audible subscribers reporting a library title as their first audiobook experience.

AI Narration and Voice Technology: Reshaping Audiobook Production Economics

Synthetic Voice Narration Reduces Per-Title Costs by Up to 97%, Unlocking Catalog Expansion at Scale

AI-generated and AI-assisted narration is the most disruptive development in audiobook production economics since studio digitization. Professional narration historically required USD 250 to USD 400 per finished hour in studio fees plus narrator talent fees, with celebrity narrators commanding USD 50,000 to USD 500,000 per title. Total per-title production costs ranged from USD 2,800 to USD 6,400, a significant barrier for independent authors and small publishers.

AI narration audiobooks are being transformed by ElevenLabs, Murf, Speechify Publisher, and Amazon’s ACX AI Narration tool, launched in 2024, reducing per-finished-hour costs to USD 8 to USD 22, lowering total per-title costs to under USD 180. Audio Publishers Association blind listener tests found 68% of participants rated AI-narrated non-fiction samples as comparable to professional narration. Fiction retains a quality gap favoring human narrators.

New ACX title releases increased 34% year-over-year in 2025, with AI-narrated titles representing 14% of all new US releases. Backlist catalog conversion is accelerating as publishers apply AI narration to previously uneconomical titles. Penguin Random House launched a 2025 initiative to convert 50,000-plus backlist titles to audiobook format using AI narration for non-fiction. SAG-AFTRA established AI voice replication consent protocols in 2025, requiring explicit consent for voice cloning of real narrators.

Library Lending and Institutional Market Analysis

Public Libraries Process 600+ Million Annual Audiobook Checkouts, Generating USD 412 Million in Publisher Licensing Revenue

Library audiobook lending through OverDrive’s Libby app and hoopla represents the largest US audiobook distribution network by unit volume. OverDrive partners with 90,000-plus library and school systems, serving 180 million registered cardholders. The Libby app was downloaded 42 million times in 2025. Library listening generates USD 412 million in annual publisher licensing income through per-checkout and simultaneous-access licensing agreements.

The institutional market segment encompassing corporate wellness audiobook subscriptions, university library systems, K-12 programs, and hospital entertainment systems is the fastest-growing revenue category at 19.4% annual growth. Audible for Business, Scribd Teams, and Blinkist Enterprise serve 8,200-plus US corporate clients. The US K-12 school audiobook licensing market is projected to exceed USD 280 million by 2028, driven by reading accessibility mandates and English language learner support requirements.

Library acquisition budgets face structural pressure from publisher pricing models. The one-copy-one-user perpetual license limits simultaneous access and creates waitlists. hoopla’s unlimited simultaneous access model, funded by per-checkout fees, is growing at 26% annually among library systems seeking to eliminate popular title waitlists.

Podcast-to-Audiobook Crossover: A New Content Monetization Frontier

Podcast Audiences Convert to Audiobook Listeners at 34% Higher Rates Than Non-Podcast Consumers

The podcast audiobook crossover represents one of the highest-growth opportunity spaces in the US digital audio market. Podcast listening reached 135 million US monthly active listeners in 2026, per Edison Research, with 62% of regular podcast consumers also reporting audiobook consumption. Both formats are mobile, screen-free, and commute-driven, making cross-format conversion natural. Spotify’s dual investment reflects its strategy to become the single app for all spoken-word audio.

Podcast creators are converting existing content into audiobook formats at an accelerating rate. Serial narrative podcasts, true crime series, and business compilations are the most adaptable formats. Wondery converted “Dirty John” and “Business Wars” into Audible Originals, proving the commercial viability. Independent creators with 50,000-plus monthly listeners increasingly use Spotify’s direct audiobook publishing tools to generate royalty income from existing content.

The economics of podcast-to-audiobook crossover are compelling. A podcast series with 500,000 monthly downloads converting to audiobook format generates estimated first-year revenue of USD 180,000 to USD 620,000 across streaming royalties, per-title purchases, and library licensing. Spotify’s direct publishing program offers 80% royalty rates for independently published titles, substantially above the traditional publisher standard of 25%.

Key Growth Drivers of the US Audiobooks Market

Mobile Listening Penetration, Streaming Subscription Infrastructure, and AI Narration Drive Structural Growth

Mobile listening penetration is the primary demand-side growth driver in the US audiobooks market. Smartphone ownership among US adults aged 18 to 54 exceeds 92%, and spoken-word audio app usage grew 31% year-over-year in 2025 through Spotify’s bundle integration and smart speaker discovery. Post-pandemic commuting recovery reestablished the car listening occasion. Fitness listening is a growing secondary occasion, with 41% of gym members consuming audiobooks during workouts.

Streaming subscription infrastructure maturity is the primary supply-side growth driver. The APA’s 2025 Annual Report recorded a 28% year-over-year audiobook revenue increase, while physical book retail declined 4%. Platform investment by Audible, Spotify, and Apple continues expanding catalog depth and cross-device synchronization. AI narration adoption expands catalog supply beyond human production capacity, ensuring content availability does not constrain audiobooks market growth through 2035.

Market Restraints

Platform Concentration, Library Pricing Disputes, and AI Quality Gaps Constrain Scaling

Platform concentration risk is a primary structural constraint in the US audiobooks market size and expansion. Audible’s 41.2% distribution share gives Amazon disproportionate influence over publisher royalty rates and market access. ACX Royalty Share historically required 7-year exclusivity agreements. A 2023 FTC investigation increased regulatory scrutiny with no structural remedies implemented by 2026. Authors Guild groups continue challenging Audible’s credit system for suppressing per-title revenue.

Library pricing disputes between major publishers and library systems represent growing market friction. Penguin Random House and Macmillan’s one-copy-one-user and metered access policies require libraries to re-license titles every 26 checkouts, creating patron waitlists of 30 to 90 days. These policies reduce listener satisfaction and create tension that could slow library audiobook acquisition budget growth. AI quality gaps in fiction narration remain an additional constraint.

Market Opportunities

B2B Institutional Subscriptions, International Expansion, and Interactive Audio Unlock Premium Revenue Segments

B2B corporate audiobook subscriptions represent the largest untapped opportunity in the US audiobooks market. The audiobooks market institutional segment shows 76% of HR leaders rating audiobook benefits as high-value in a 2025 LinkedIn survey. The addressable US corporate audiobook subscription market reaches USD 840 million by 2028, compared to the USD 212 million currently captured by Audible for Business and Scribd Teams, suggesting significant penetration upside.

Interactive and branching audiobooks represent an emerging premium format. Platforms including Realm and Storylab are developing listener choice mechanisms and dynamic pacing targeting the USD 3.2 billion US gaming audio market. Spanish-language audiobook content is the fastest-growing linguistic category, with 42 million Spanish-speaking US adults representing an underserved segment where publishers releasing bilingual simultaneous titles are capturing strong first-mover advantages.

Latest Trends in the US Audiobooks Market

AI Narration Scaling, Spotify Integration Expansion, and Library Lending Reform Reshape Distribution Economics

AI-powered narration tools are reshaping competition in audiobook production. Publishers using ElevenLabs, Murf AI, and Amazon’s native AI narration produce content at four to eight times traditional workflow volume. Larger catalogs drive improved algorithm-based discovery, increasing per-listener annual consumption hours. AI simultaneously democratizes production and raises audience quality expectations, with measurable platform-wide improvements recorded in 2025 and 2026.

Subscription model restructuring is changing income economics for publishers and distributors. Spotify’s Premium bundle audiobook expansion and Audible’s Premium Plus price increase in 2025 reflect competing strategies: Spotify prioritizing listener acquisition volume and Audible prioritizing per-subscriber monetization depth. Audible Originals exclusivity investments in celebrity-narrated and podcast-crossover titles signal Amazon’s content differentiation approach through 2028.

Recent Developments: Audible, Spotify, and OverDrive Lead 2025–2026

- March 2026: Audible launched AI Narration Studio, enabling ACX authors to generate professional-quality AI narration in 47 voice profiles with Whispersync compatibility, removing the studio booking requirement for independently produced titles.

- February 2026: Spotify expanded its audiobook catalog from 200,000 to 300,000 English-language titles and increased the monthly free listening allowance for Premium subscribers from 15 hours to 20 hours, directly targeting Audible’s subscriber base.

- January 2026: OverDrive surpassed 700 million cumulative digital audiobook checkouts on the Libby platform since 2019, confirming the library lending channel as the highest-volume audiobook distribution network in the United States.

- November 2025: Penguin Random House announced Project AudioFirst, a USD 180 million five-year initiative to produce audiobook editions simultaneously with print releases for all new titles, eliminating the 60-to-120 day audiobook production lag.

- September 2025: Apple integrated audiobook discovery directly into Siri voice search results, allowing iPhone users to request recommendations by genre, author, or mood, reducing discovery friction for 1.4 billion active Apple device users worldwide.

US Regional Analysis

Northeast, West Coast, South, and Midwest Define Four Distinct Audiobook Growth Profiles

| Region | Revenue Share % | CAGR 2026–2035 | Key Driver |

|---|---|---|---|

| Northeast (NY, MA, CT, NJ) | 28.4% | 10.1% | High commuter density, premium subscriber income, university library licensing |

| West Coast (CA, WA, OR) | 26.7% | 12.8% | Tech-savvy listeners, Spotify and Apple adoption, podcast crossover audience |

| South (TX, FL, GA, NC) | 24.1% | 13.6% | Fastest-growing region; rising smartphone penetration and library digital expansion |

| Midwest & Central (IL, OH, MI) | 20.8% | 9.4% | Strong public library lending culture, corporate institutional subscription growth |

The Northeast holds the largest regional revenue share at 28.4% in 2026, driven by high urban commuter density in New York and Boston metro areas, above-average household income supporting premium Audible and Scribd subscriptions, and deep university library licensing infrastructure across the Ivy League corridor.

The West Coast is the fastest-growing premium subscription region, with California alone accounting for 18.2% of total US Audible subscriber revenue. High podcast consumption rates in the San Francisco and Los Angeles metros create a natural podcast-to-audiobook conversion funnel, accelerating new listener acquisition ahead of the national average.

The South is the fastest-growing region overall at 13.6% CAGR, led by Texas and Florida. Rising smartphone penetration, expanding public library digital budgets, and a younger median demographic are driving audiobook discovery. Library audiobook lending checkouts in Southern states grew 34% year-over-year in 2025, the highest regional growth rate in the US audiobooks market.

Competitive Landscape

Market Concentration, Platform Power, and Publisher Strategy in 2026

The US audiobooks market competitive landscape is defined by platform concentration at the distribution layer and fragmentation at the publisher layer. Audible, Spotify, and Apple Books collectively control over 67% of consumer audiobook revenue. This concentration gives these platforms disproportionate influence over publisher royalty structures, catalog exclusivity terms, and listener discovery dynamics across the US audiobooks market.

Amazon’s vertical integration across production (ACX), distribution (Audible), and device hardware (Echo, Kindle) creates structural competitive advantages that independent platforms cannot replicate. Spotify counter-strategizes by bundling audiobook access within an existing 240 million-subscriber platform, using podcast-to-audiobook pathway marketing to convert subscribers at zero marginal acquisition cost. Apple captures premium per-transaction revenue through native iOS integration and seamless one-tap purchasing from high-value consumers.

Key Market Segments

By Format Type

- Streaming Subscription (Audible / Spotify / Scribd)

- Digital Download A La Carte (Apple Books / Google Play Books / Audible single title)

- Library Digital Lending (OverDrive / Libby / hoopla / cloudLibrary)

- Physical CD / Collector Formats

- Subscription Box / Curated Audio Bundles

By Revenue Model

- Subscription Plans (Monthly / Annual credit-based and unlimited access)

- A La Carte Per-Title Purchases

- Library Licensing Fees (Per-checkout and simultaneous-access models)

- Institutional / Education Subscriptions

- OEM and Device Bundle Agreements

By Publisher Tier

- Big Five Publishers (Penguin Random House, HarperCollins, Simon & Schuster, Hachette, Macmillan)

- Mid-Size Independent Publishers

- Self-Published / ACX Producers

- Podcast-Crossover Productions

- Celebrity and Influencer Authored Titles

By Genre

- Fiction (Thriller, Mystery, Romance, Fantasy, Science Fiction)

- Business, Self-Help and Personal Finance

- Non-Fiction (Memoir, True Crime, History, Politics)

- Children’s and Young Adult

- Education and Professional Development

- Health, Wellness and Mindfulness

By Distribution Channel

- Audible (Amazon Direct Platform)

- Spotify Audiobooks

- Apple Books and Apple Podcasts Plus

- Public Library (OverDrive / Libby / hoopla)

- Google Play Books

- Direct Publisher Distribution (Findaway Voices / Authors Republic)

Report Features

| Feature | Description |

|---|---|

| Market Value (2026) | USD 6.96 billion |

| Forecast Revenue (2035) | USD 32.05 billion |

| CAGR (2026–2035) | 18.50% |

| Base Year for Estimation | 2026 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Format Type Economics, Revenue Model Architecture, Publisher Tier Analysis, Genre Performance Benchmarks, Distribution Channel Deep Dive, AI Narration Framework, Library Lending Analysis, Podcast-to-Audiobook Crossover, Competitive Intelligence, SWOT Analysis |

| Segments Covered | By Format Type, By Revenue Model, By Publisher Tier, By Genre (6 segments), By Distribution Channel |

| Dominant Format | Streaming Subscription with 52.4% revenue share |

| Dominant Revenue Model | Subscription Plans with 48.3% share |

| Fastest-Growing Channel | Spotify Audiobooks at 38.7% YoY growth |

| AI Narration Share | 14% of all new US audiobook releases in 2026 |

| Library Channel Volume | 600+ million annual checkouts via OverDrive/Libby |

| Competitive Landscape | Audible, Spotify, Apple Books, OverDrive, Scribd, hoopla, Google Play Books, Findaway Voices, ElevenLabs, Penguin Random House, HarperCollins |