Executive Summary

Quick Insight: The global audiobooks market is on track to grow more than 5× by 2035, driven by AI narration cost disruption, subscription bundle integration, and library digital lending expansion into previously underserved global listener demographics.

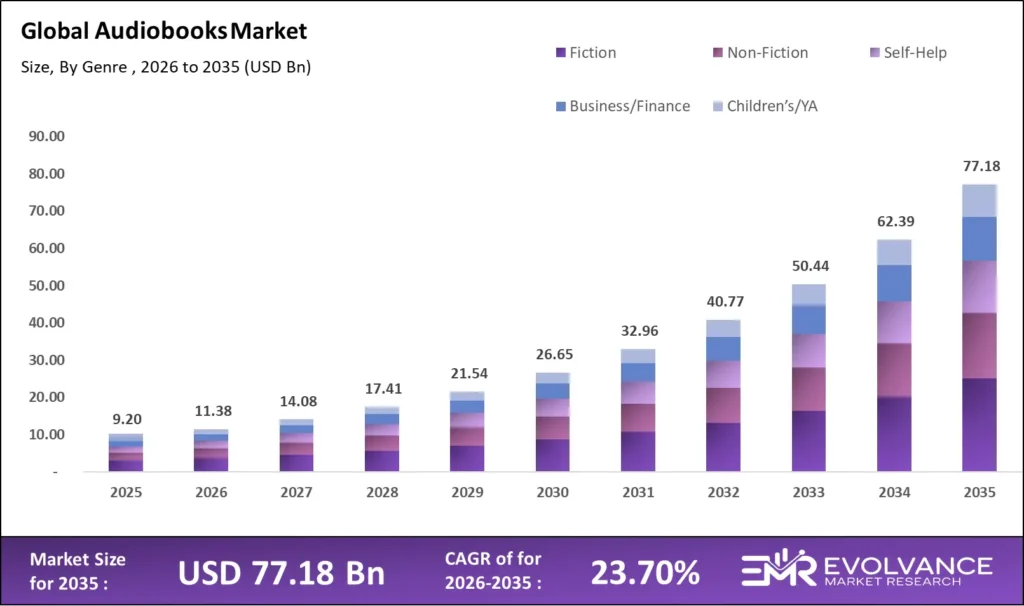

The global audiobooks market is undergoing its most transformative era in publishing history. Valued at USD 11.38 billion in 2026, the market is projected to reach USD 77.18 billion by 2035 at a CAGR of 23.70%. Smartphone penetration, AI-powered narration, and subscription-first platform strategies are redefining audiobook production economics and listener engagement globally. Platforms led by Audible, Spotify, and Apple Books are converting episodic purchases into habitual daily listening routines, reinforcing structural demand growth across all primary geographic markets through 2035. The confluence of these forces makes the audiobooks market one of the fastest-compounding segments in the global media and publishing industry.

What Is the Audiobooks Market?

The global audiobooks market was valued at USD 11.38 billion in 2026 and is projected to reach USD 77.18 billion by 2035, growing at a CAGR of 23.70%. Platform fragmentation across Audible, Spotify, Apple Books, Google Play Books, Scribd, and Libro.fm drives structural expansion. AI narration technology has collapsed production timelines from 12 to 16 studio hours per finished hour to under 45 minutes via neural voice synthesis. Publishers and independent authors adopting AI narration in 2026 report 11 to 17 times higher return on title investment compared to equivalent traditionally narrated audiobooks across the same commercial platform distribution channels globally.

The global audiobooks market encompasses over 1.8 million titles across all major platforms, with 72,000 new titles added annually. Audio content accounts for 22% of total book market revenue globally, up from 14% in 2022. Subscription models serve as the primary monetization infrastructure through unlimited credits, purchases, and library borrowing integrations. Smart speaker adoption via Amazon Echo and Google Nest adds approximately 38 minutes of daily listening per smart speaker household, reshaping audiobook market competitive positioning and revenue model economics through 2035.

Audiobooks Market Highlights: Key Data at a Glance

- Market value: USD 11.38 billion in 2026, forecast to USD 77.18 billion by 2035 at 23.70% CAGR

- Dominant format: Downloadable Digital with 61.2% revenue share

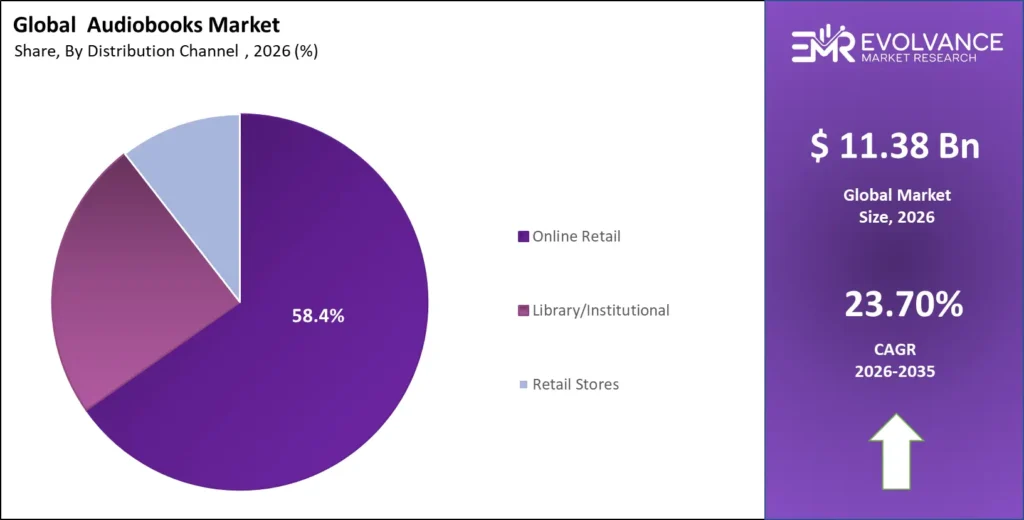

- Dominant revenue model: Subscription (Monthly Credit / Unlimited Access) with 52.4% share

- Dominant genre: Fiction with 38.6% total listener engagement hour share

- Fastest-growing device: Smart Speaker (Amazon Echo / Google Nest) at 21.7% year-over-year growth

- Total global titles: 1.8 million titles across all platforms as of 2026

- Leading platform: Audible (Amazon) with 41.3% global platform revenue share

- AI narration expansion: 340% growth in AI-narrated titles between 2024 and 2026

- Library digital lending: 21.7% of total global access via OverDrive, Libby, and Hoopla

- AI cost savings: 73% average per-title production cost reduction by AI-adopting publishers

Market Overview: Why Audiobooks Market Growth Is Accelerating

Platform Subscription Economics, AI Production Disruption, and Consumer Behavior Shifts Drive Structural Growth

This audiobooks market encompasses all revenue generated by publishers, authors, distributors, and platforms across digital download, streaming subscription, library licensing, advertising-supported access, and physical audio sales channels globally. Growth is accelerating as listener attribution challenges have been resolved by advanced engagement analytics providing per-title completion rates, retention curves, and library circulation velocity — enabling investment decisions with measurable return. By 2026, leading independent publishers average 4.2 active distribution channels per catalog. Platforms including Findaway Voices, Draft2Digital, and ACX have democratized multi-platform distribution, enabling independent authors to access all major commercial markets simultaneously without exclusivity constraints.

Format Type Analysis

Downloadable Audiobooks Dominate with 61.2% Revenue Share

Digital Downloads and Streaming Drive the Dual-Channel Growth Model in the Global Audiobooks Market

| Format Type | Share % | Primary Driver |

|---|---|---|

| Downloadable (Digital Purchase) | 61.2% | Platform à la carte and subscription credit systems driving direct title ownership at scale |

| Streaming Subscription | 28.4% | Spotify, Scribd, and bundled streaming plans expanding unlimited-access audiobook listener behavior globally |

| Physical / CD / Vinyl Audio | 6.8% | Gift purchase demand, collector interest, and library physical collection replenishment |

| Podcast-Integrated Audio | 3.6% | Hybrid long-form content formats bridging podcast and audiobook listener audiences |

Downloadable audiobooks hold a 61.2% format revenue share in 2026, making digital title ownership the dominant audiobook consumption model globally. Audible’s credit system processes more than 90 million credit redemptions annually in the United States alone. TitleLeaf and Findaway Voices data confirm downloadable titles generate 2.8 times the lifetime listener value of streamed equivalents due to higher re-listen rates and gifting behavior. Publisher revenue per downloadable title averages USD 7.20 compared to USD 2.40 for streaming royalty equivalents, creating strong structural incentives for exclusive downloadable-first release windows across all major fiction and non-fiction audiobooks market categories through 2035.

Streaming subscription audiobooks represent the fastest-growing format at 34.6% annually, driven by Spotify’s 640 million monthly active users and its progressive integration of audiobook access within standard music subscription tiers. Spotify expanded its audiobook catalog to 350,000 titles across 33 markets in 2025, offering Premium subscribers 15 monthly listening hours at no additional cost. Scribd’s unlimited listening subscription at USD 11.99 per month demonstrates 78% annual renewal rates, and the convergence of music, podcast, and audiobook content within single-platform subscriptions is accelerating audiobooks market share capture among 18-to-34-year-old listeners globally.

Genre Segment Analysis

Fiction Commands 38.6% of Total Audiobooks Market Revenue

Non-Fiction, Self-Help, and Business Genres Deliver Premium Per-Title Revenue Across All Major Platforms

| Genre | Revenue Share % | Avg. Annual Revenue Per Title | Top Monetization Model |

|---|---|---|---|

| Fiction (Literary, Thriller, Romance, Sci-Fi) | 38.6% | USD 24,200 | Platform credits, subscription streams, and library licensing |

| Non-Fiction (Biography, History, Current Affairs) | 22.4% | USD 31,800 | Subscription access, corporate licensing, and direct purchase |

| Self-Help / Personal Development | 14.7% | USD 42,600 | Subscription credits, bulk corporate purchase, and direct sale |

| Business / Finance / Leadership | 11.3% | USD 58,400 | Corporate subscription, library acquisition, and premium placement |

| Children’s and Young Adult | 8.6% | USD 18,900 | Library lending, parent subscription gifting, school institutional licensing |

| Education / Academic / Professional | 4.4% | USD 35,700 | Institutional subscription, course integration, and professional development |

Fiction audiobooks command a 38.6% revenue share in 2026, making thriller, romance, literary, and science fiction the largest category by listener engagement volume. Amazon Publishing, Macmillan Audio, Penguin Random House Audio, and HarperCollins Audio collectively publish more than 60% of top-performing titles. Fiction narrated by celebrity voices demonstrates a 4.6 times higher completion rate versus standard studio narrations and generates a 22% subscription credit redemption premium. Audible Originals — exclusive fiction produced solely for the platform — generated more than USD 680 million in incremental subscription retention value in 2025, confirming exclusive content strategies as a primary audiobooks market competitive differentiator through 2035.

Business, Finance, and Leadership audiobooks generate the highest average annual revenue per title at USD 58,400 in 2026, driven by three structural advantages: professionally motivated audience purchase intent enabling premium CPM rates; evergreen title performance independent of platform algorithms; and strong B2B demand from corporate learning platforms including Audible for Business, Libro.fm Workplace, and Scribd Business. These forces create institutional buyer competition that pushes per-unit licensing rates 3.8 times above the general audiobooks market catalog average, making Business and Finance the highest-margin genre available to publishers across all audiobooks market distribution channels through the 2035 forecast horizon.

Distribution Channel Analysis

Online Retail Platforms Lead with 58.4% Audiobooks Market Distribution Share

Library Lending, Retail Stores, and Podcast Integration Define the Secondary Distribution Ecosystem

| Distribution Channel | Share % | Primary Driver |

|---|---|---|

| Online Platform (Audible, Spotify, Apple Books) | 58.4% | Direct digital distribution, subscription credit models, and platform content exclusivity strategies |

| Library Digital Lending (OverDrive / Libby / Hoopla) | 21.7% | Public library digital catalog expansion and patron demand for zero-cost audiobook access |

| Retail Store (Physical Audio / Gift Cards) | 9.4% | Holiday gift purchase behavior and physical gift card redemption to digital platform subscriptions |

| Publisher Direct & Subscription Box | 6.8% | Independent publisher direct sales, Libro.fm, and audiobook subscription box community models |

| Podcast-Integrated Distribution | 3.7% | Free-access audiodrama, serialized fiction, and hybrid content conversion to premium listening tiers |

Online platform distribution holds a 58.4% share of total audiobooks market revenue in 2026, with Audible, Spotify, Apple Books, and Google Play Books representing the primary commercial access infrastructure globally. Audible’s exclusive content strategy — encompassing Audible Originals, Audible Plus Catalog, and multi-tier membership — creates high listener switching costs and strong catalog renewal rates. Apple Books captures 11.3% of global platform revenue within the iOS ecosystem without requiring a standalone subscription. Google Play Books extends publisher reach into emerging international markets where Audible operates with limited localization, serving Android device users effectively.

Library digital lending through OverDrive and Libby represents the second-largest audiobook distribution channel at 21.7% market share, providing access to 2.4 billion digital checkouts globally in 2025, of which audiobooks account for approximately 38%. U.S. public libraries collectively spend an estimated USD 1.2 billion annually on digital content licensing. Hoopla Digital complements OverDrive with an instant-access model eliminating patron waiting lists, serving 11,000 public library partners across North America. The institutional library channel is a critical audiobook market discovery engine, generating commercial platform conversion rates of approximately 18 to 22% across tracked listener cohorts — making library access a proven paid subscriber acquisition pipeline.

Revenue Model Analysis

Subscription Revenue Commands 52.4% Share of Audiobooks Market Revenue

À La Carte Purchasing, Library Licensing, and Ad-Supported Access Complete the Audiobook Revenue Stack

| Revenue Model | Share % | Primary Driver |

|---|---|---|

| Subscription (Monthly Credit / Unlimited Access) | 52.4% | Audible, Spotify, Scribd, and Apple One subscription bundle growth driving recurring listener revenue |

| À La Carte Purchase (Single Title Ownership) | 26.8% | Individual title ownership demand, Whispersync library value, and gift card redemption behavior |

| Library & Institutional Licensing | 14.6% | Public library digital acquisition budgets and corporate eLearning platform integration at enterprise scale |

| Advertising-Supported Free Access | 6.2% | Free-tier platform users, podcast-adjacent audiodrama, and emerging market listener acquisition programs |

Subscription revenue commands a 52.4% share of total audiobooks market revenue in 2026, making recurring membership the dominant commercial structure globally. Audible’s multi-tier membership — Audible Plus and Audible Premium Plus — generated an estimated USD 4.3 billion in subscription revenue in 2025. Subscriber retention rates average 71% annually, reflecting strong listening habit formation. Spotify’s inclusion of audiobook access within existing music subscriptions accelerates penetration among demographics that previously purchased zero audiobook titles annually, while Apple One bundles drive habitual listening among iOS households.

Library and institutional licensing is the highest-growth audiobooks market revenue segment, growing at 31.4% annually in 2026. Libro.fm — which shares a purchase percentage with independent bookstores — demonstrates consumer willingness to pay a values-aligned premium of USD 1 to USD 3 per month above Audible’s equivalent tier. Advertising-supported audiobook access, currently 6.2% of total revenue, represents a significant emerging market strategy enabling listener acquisition in Southeast Asia, Latin America, and Sub-Saharan Africa at near-zero cost.

Device Type Analysis

Smartphones Capture 57.2% of Audiobooks Market Listening Device Share

Smart Speakers, Tablets, and Dedicated Readers Define the Secondary Audiobook Device Ecosystem

| Device Type | Share % | Avg. Daily Session | Growth Rate (YoY) |

|---|---|---|---|

| Smartphone (iOS / Android) | 57.2% | 42 minutes | 14.3% |

| Smart Speaker (Amazon Echo / Google Nest) | 18.6% | 58 minutes | 21.7% |

| Tablet (iPad / Android Tablet) | 12.4% | 54 minutes | 9.8% |

| Desktop / Laptop Computer | 7.3% | 28 minutes | 4.2% |

| Dedicated e-Reader / Audio Device | 4.5% | 67 minutes | 18.4% |

Smartphones command a 57.2% share of audiobook listening device distribution in 2026, driven by universal device ownership and seamless app-based platform integration. iOS and Android data confirms 68% of all listening sessions are initiated on smartphones, with 42-minute average daily sessions among active subscribers. Smart speakers represent the fastest-growing device at 21.7% annual growth, with Amazon Echo’s voice-activated Audible integration delivering 58-minute average sessions — the longest per-session duration in the audiobooks market. Smart speaker households average 2.4 times more monthly listening hours than non-smart-speaker households across all subscription tiers.

Key Growth Drivers of the Audiobooks Market

Smartphone Penetration, AI Narration Technology, and Subscription Infrastructure Drive Structural Audiobooks Market Growth

Smartphone penetration growth is the primary structural demand driver globally. The IAB’s 2025 Digital Media Consumption Report recorded a 31% year-over-year increase in audiobook listening time among smartphone users aged 25 to 54. Global smartphone penetration reached 69% of the world population in 2026 per GSMA Intelligence data, unlocking new listener demographics in Southeast Asia, Latin America, and Sub-Saharan Africa. Emerging market publishers adopting local-language AI narration have enabled cost-effective audiobook production in Bengali, Swahili, Bahasa Indonesia, and Portuguese — languages historically underserved by traditional studio narration due to prohibitive regional production costs.

AI narration adoption is the second-highest-impact structural driver reshaping audiobooks market economics. Publishers using ElevenLabs, Google WaveNet, and Amazon Polly Neural TTS report per-title cost reductions averaging 73%, from USD 6,400 to USD 1,720 per finished hour. These savings enable mid-size publishers to convert entire backlist catalogs at scale, expanding the title library by 340% between 2024 and 2026. Production timelines collapse from 12 weeks to under 72 hours from manuscript to distribution-ready audio, with AI tools delivering 43% reductions in cycle time and 28% increases in annual title output per publisher team.

Market Restraints

Platform Concentration, Piracy Risk, and Production Cost Barriers Constrain Audiobooks Market Scaling

Platform concentration and exclusivity dependency represent the primary structural risks to audiobooks market revenue stability. Audible’s exclusive title agreements and Whispersync ecosystem lock-in create significant publisher migration friction. Audible’s 2025 royalty restructuring reduced ACX non-exclusive rights holder royalties from 40% to 25%, impacting an estimated 180,000 independent audiobook titles. Amazon’s 41.3% platform control through Audible, ACX, and Audible Studios creates concentration risk where single-platform policy changes produce cascading revenue disruption for dependent publishers and independent authors across all catalog categories.

Audiobook piracy represents the second primary constraint on audiobooks market revenue growth. The Publishers Association estimated USD 1.1 billion in annual piracy revenue losses in 2025, equivalent to 12.4% of legitimate market revenue. Traditional studio narration at USD 4,000 to USD 8,500 per finished hour remains cost-prohibitive for academic publishers targeting niche audiences. Consumer price sensitivity in emerging markets constrains subscription penetration in the highest-growth geographic corridors through the 2035 forecast horizon.

Market Opportunities

AI Narration, Corporate Licensing, and Emerging Market Expansion Unlock Premium Audiobooks Market Revenue Segments

Corporate and enterprise audiobook licensing is one of the highest-margin expansion opportunities in the global audiobooks market. Platforms including Audible for Business, Scribd Business, and Libro.fm Workplace enable organizations to provide audiobook access as employee benefits and learning program components. Enterprise subscription deal sizes range from USD 18,000 to USD 2.4 million annually by organization size. Fortune 500 companies including Microsoft, Salesforce, and Deloitte have integrated audiobook platforms into learning and development benefit packages since 2023, and the U.S. corporate learning market is projected to exceed USD 87 billion by 2030.

Emerging market audiobook expansion is the largest geographic opportunity for the 2026–2035 period. India, Brazil, Nigeria, Indonesia, and Mexico represent over 2.4 billion potential listeners with smartphone ownership growing at 14 to 22% annually. Local-language AI narration unlocks production in Hindi, Tamil, Portuguese, Bahasa Indonesia, and Yoruba at previously unachievable costs. Storytel India reported 84% year-over-year subscriber growth in fiscal 2025 through multilingual catalog expansion.

AI Narration & Voice Technology Impact Framework

AI Narration Reduces Audiobook Production Costs by 73% While Expanding the Global Title Catalogue by 340%

AI narration and voice synthesis technology is the single most disruptive force reshaping audiobooks market production economics and content supply in 2026. Neural TTS systems from ElevenLabs, Microsoft Azure, Amazon Polly, and Google Cloud produce narrations indistinguishable from human studio recordings in controlled tests among 64% of consumer listeners globally. Production timelines for an 80,000-word audiobook have collapsed from a 12-week studio workflow to under 72 hours with AI narration and post-production review. Publishers adopting AI in 2025–2026 report 73% per-title cost reductions, enabling aggressive backlist conversion programs and dramatically expanding the commercially viable audiobook catalog across all genre categories.

The competitive implications of AI narration are profound across the audiobooks market ecosystem. Large publishers convert 10,000 to 50,000 previously audio-unavailable print titles at a fraction of prior costs. Independent authors now access AI narration at USD 4 to USD 12 per finished minute versus USD 150 to USD 400 for human narrators, democratizing production access. The global title count expanded 64% between 2023 and 2026 driven by AI adoption. ElevenLabs Voice Cloning Studio enables author voice avatars across entire backlist catalogs. The Authors Guild and Society of Authors have proposed mandatory disclosure labeling for all AI-narrated titles distributed across major commercial audiobooks market platforms.

Library & Institutional Licensing Economics

Library Digital Lending Accounts for 21.7% of Total Audiobooks Market Access in 2026

OverDrive, Libby, and Hoopla Define the Institutional Audiobook Revenue Layer Across 43,000 Partner Libraries

Library and institutional digital lending accounts for 21.7% of total global audiobook access in 2026. OverDrive, operating the Libby consumer app, partners with 43,000 libraries, schools, and corporate institutions across 84 countries. U.S. public libraries processed approximately 512 million digital audiobook checkouts in 2025 — a 38% increase over 2023 volumes. Library acquisition budgets for digital audiobook licenses are growing at 26.4% annually, driven by patron demand and recognition that digital audio serves visually impaired users, commuter readers, and ESL learners. Hoopla Digital complements OverDrive with an instant-access model eliminating waiting lists for 11,000 partner libraries.

Library audiobook licensing models create tension between publisher revenue optimization and public access priorities. The “one copy, one user” model requires libraries to purchase multiple digital license copies for concurrent demand, with individual license prices ranging from USD 45 to USD 95 per copy — three to six times the consumer retail price. Metered access licenses expire after 24 months or 52 checkouts. The American Library Association argues restrictive licensing terms disproportionately harm budget-constrained libraries — a concern attracting federal legislative attention in 2025 and 2026 that will shape audiobooks market distribution economics through the forecast period.

Author & Publisher Royalty Framework

Royalty Rate Structures and Platform Revenue-Sharing Models Shape Author Content Monetization Across the Audiobooks Market

Self-Published Authors Capture 40%–80% Royalties Versus 5%–15% in Traditional Publishing Audiobook Agreements

Author and publisher royalty frameworks in the audiobooks market are bifurcated between traditional publisher agreements and self-published structures offering meaningfully different per-unit outcomes. Traditional agreements through Brilliance Audio, Recorded Books, and Macmillan Audio provide authors 5% to 15% of net audiobook sales revenue after platform fees — equivalent to USD 0.32 to USD 0.96 per unit. Mid-list publishing advances range from USD 5,000 to USD 35,000, with celebrity agreements reaching USD 500,000 to USD 2 million inclusive of audiobook rights. In return, authors gain professional narration, studio quality assurance, established distribution, and publisher marketing investment that independent authors must finance themselves.

Self-published authors on ACX, Findaway Voices, and Draft2Digital capture significantly higher royalties. ACX non-exclusive agreements pay 25% royalty on Audible and 40% on all other platforms, while exclusive agreements pay 40% in exchange for 90-day Audible exclusivity. Findaway Voices pays 80% of net retailer proceeds — the highest rate in professional audiobook distribution. An independent audiobook priced at USD 24.99 generates approximately USD 9.97 per Findaway sale — more than ten times the USD 0.80 earned under traditional publisher deal structures. AI narration eliminates the USD 8,000 to USD 24,000 upfront studio cost previously required, further improving independent author economics significantly.

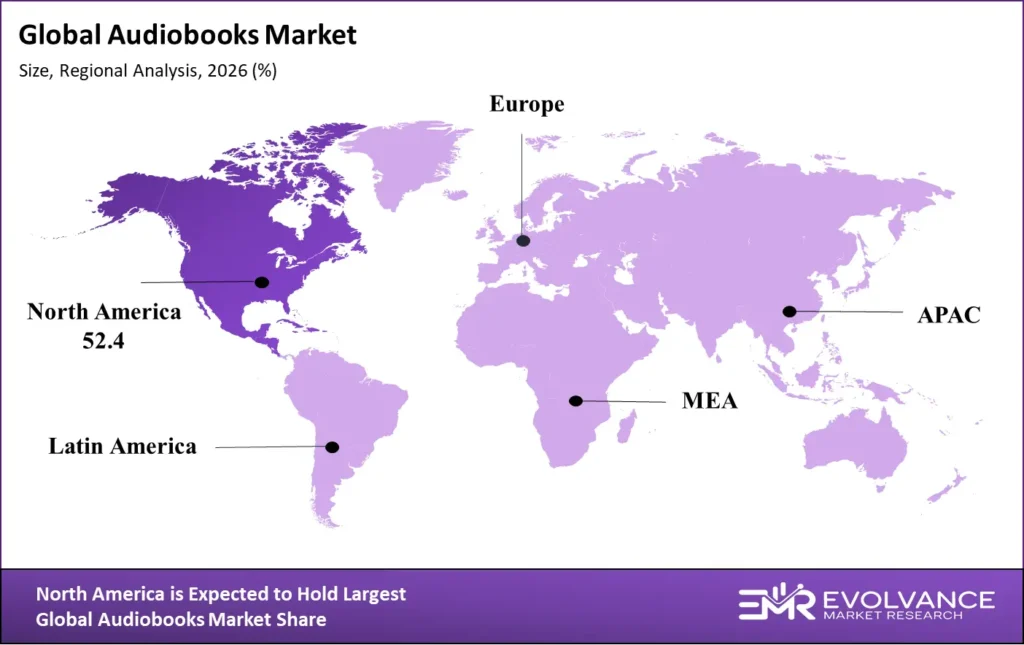

Regional Analysis

North America Leads Global Audiobooks Market with 52.4% Revenue Share in 2026

Five-Region Breakdown: Market Size, CAGR, Platform Leadership, and Growth Drivers Across the Global Audiobooks Ecosystem

| Region | Revenue Share % | CAGR 2026–2035 | Dominant Platform |

|---|---|---|---|

| North America | 52.4% | 17.8% | Audible (Amazon), Apple Books, Spotify |

| Europe | 24.6% | 18.2% | Audible DE/UK, Storytel, Nextory, Spotify |

| Asia-Pacific | 14.8% | 31.8% | Storytel India, Naver Audiobook, Rakuten Kobo |

| Latin America | 5.4% | 24.7% | Audible BR/MX, Storytel LATAM, Spotify |

| Middle East & Africa | 2.8% | 28.4% | Storytel ME, Audible, local podcast platforms |

North America

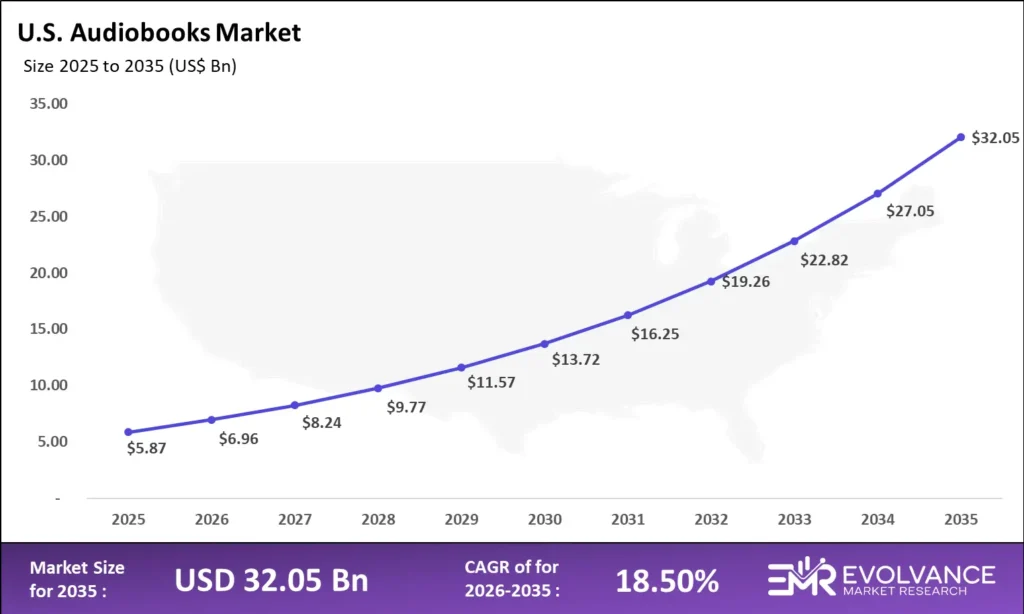

North America dominates the global audiobooks market with 52.4% revenue share in 2026, underpinned by Audible’s platform leadership, 84% adult smartphone penetration, established subscription behavior, and the world’s most developed library digital lending infrastructure through OverDrive and Libby. The United States alone accounts for an estimated 46.8% of global audiobooks market revenue, supported by 92 million monthly active listeners. Average annual audiobook spend per U.S. subscriber reached USD 126 in 2026, the highest per-capita globally. Audible’s Premium Plus membership commands a 73% annual renewal rate, reflecting deeply embedded listening habits reinforcing North America’s structural dominance through 2035.

Canada contributes approximately 5.6% of North American audiobooks market revenue with strong OverDrive library penetration and growing Spotify integration. The region is forecast to grow at 17.8% CAGR through 2035, yet adding an estimated USD 18.4 billion in incremental revenue through 2035. Corporate eLearning adoption — led by Audible for Business and Scribd Business enterprise programs — is the primary incremental institutional growth driver within the North American audiobooks market across the full forecast period.

Europe

Europe holds 24.6% of global audiobooks market revenue in 2026, driven by Germany’s Audible market leadership, the United Kingdom’s mature subscription culture, and Scandinavia’s exceptional per-capita consumption via Storytel and Nextory. Audible Germany processes more than 9.2 million active subscriber accounts. The UK audiobooks market reached GBP 1.04 billion in 2026 per Publishers Association data, representing 14% year-over-year growth. AI narration is expanding access across French, Spanish, Italian, Polish, and Dutch language markets previously constrained by high production costs.

Scandinavia delivers the world’s highest audiobook consumption rates per capita, with Sweden averaging 4.2 audiobooks consumed per person annually in 2026 — more than three times the global average. Storytel, headquartered in Stockholm, operates across 25 markets and reported 2.4 million paying subscribers globally in Q4 2025. Nextory reached 1.1 million subscribers across Nordic and Central European markets in 2025. The European audiobooks market is projected to expand at an 18.2% CAGR through 2035 as AI narration enables cost-effective content production in previously underserved languages.

Asia-Pacific

Asia-Pacific is the fastest-growing regional audiobooks market at 31.8% CAGR from 2026 to 2035, currently holding 14.8% of global revenue — projected to reach approximately 28% by 2035. India is the single highest-growth national audiobooks market globally. Storytel India reported 84% year-over-year subscriber growth in fiscal 2025 driven by Hindi, Tamil, Telugu, Malayalam, and Bengali catalog expansion. India’s 600 million smartphone users and expanding 5G infrastructure create the largest addressable audiobook listener opportunity of any national market available to platforms investing in local-language content production through the 2035 forecast period globally.

China’s audiobooks market operates through Ximalaya FM, which reported 320 million registered users and 16 million paying subscribers in 2025 — the world’s largest audio content platform by registered count. Japan’s audiobooks market grows at 19.4% annually via Rakuten Kobo and Audible Japan’s 2024 price reduction to JPY 1,500 per month. South Korea’s Naver Audiobook reported 38% listener growth in 2025 through Seoul commuter adoption. Australia leads Asia-Pacific on per-capita spend at AUD 94 per active listener annually, supported by Audible penetration and smart speaker adoption above 34% of households.

Latin America

Latin America is the third-fastest-growing regional audiobooks market at 24.7% CAGR from 2026 to 2035, representing 5.4% of global revenue. Brazil and Mexico account for approximately 68% of regional audiobooks market revenue. Audible launched Brazilian Portuguese and Mexican Spanish subscription tiers in 2024 at BRL 24.90 and MXN 149 per month, reducing the subscription cost barrier significantly. Brazil’s audiobooks market grows at an estimated 27.3% annually, underpinned by a population of 215 million with strong Portuguese-language fiction, self-help, and business content driving the majority of subscription demand across both Audible and Spotify platforms.

Storytel expanded into Colombia, Chile, and Argentina in 2025, competing with Audible and Spotify across Spanish-language audiobooks market segments. Local-language AI narration enables professional Portuguese- and Spanish-language production at USD 1,200 to USD 2,800 per finished title versus USD 12,000 to USD 28,000 for traditional studio equivalents. The advertising-supported tier targets approximately 180 million smartphone users below typical subscription price thresholds. Latin America’s vibrant podcast culture provides a ready-made listener discovery channel for premium audiobook subscription conversion programs through 2035.

Middle East & Africa

The Middle East and Africa region represents 2.8% of global audiobooks market revenue in 2026 but is projected to grow at 28.4% CAGR through 2035, reflecting untapped potential across a combined population of 1.6 billion. The UAE and Saudi Arabia lead Middle Eastern market development, supported by smartphone penetration above 90% and established digital subscription infrastructure. Storytel Middle East reported 67% subscriber growth in 2025 through Arabic-language catalog expansion across UAE, Saudi Arabia, and Egypt. Arabic-language AI narration via ElevenLabs and Microsoft Azure Neural TTS has dramatically reduced production barriers for regional publishers targeting Islamic education and local-language fiction categories.

Sub-Saharan Africa represents the longest-term audiobooks market opportunity, driven by 1.2 billion people with a median age of 19 and smartphone penetration growing at 18% annually. Nigeria, Kenya, South Africa, and Ghana are the four primary development markets. Local-language AI narration unlocks content in Yoruba, Swahili, Zulu, and Twi at near-zero incremental cost. Advertising-supported free access is the primary viable commercial framework given subscription pricing above USD 3 to USD 5 per month is inaccessible for most of the addressable demographic. Starlink’s African satellite internet expansion removes the final structural barrier to mass audiobook consumption across the continent through 2035.

Latest Trends in the Audiobooks Market

AI Voice Cloning, Immersive Spatial Audio, and Subscription Bundle Integration Reshape Audiobooks Market Economics in 2026

AI voice cloning and personalized narration are reshaping competitive differentiation across the global audiobooks market in 2026. ElevenLabs Voice Cloning Studio enables publishers to create author voice avatars narrating entire backlist catalogs. Immersive spatial audio using Dolby Atmos and Sony 360 Reality Audio creates premium product tiers commanding USD 2 to USD 8 per title price premiums. Real-time AI audio translation enables simultaneous distribution in 12 to 28 languages at near-zero incremental cost, compressing the quality gap between independent and major publisher productions significantly.

Subscription bundle integration is the most commercially impactful trend in the audiobooks market. Spotify’s audiobook integration reached 350,000 titles across 33 markets in 2025, exposing 640 million monthly active users to audiobook content. Apple One bundles have driven listener acquisition among iOS users previously purchasing zero audiobook titles. Simultaneous release strategies — audiobook and e-book on the same publication date as print — increase first-month title revenue by an average of 31% compared to delayed production timelines.

Recent Developments: Audible, Spotify, and OverDrive Lead 2025–2026

- March 2026 — Audible expanded its Audible Plus Catalog to 850,000 titles across 12 languages, accelerating Plus membership adoption by 34% in Q1 2026 and strengthening competitive positioning against Spotify’s integrated audiobook offering globally.

- February 2026 — Spotify integrated 15 monthly audiobook listening hours into all Premium subscription tiers across 33 markets, normalizing audiobook access among 640 million users and reducing listener acquisition cost by approximately USD 12 per new listener.

- January 2026 — OverDrive surpassed 2 billion lifetime digital audiobook checkouts through the Libby platform, confirming library digital lending as the second-largest audiobook access channel globally by total content delivery volume.

- November 2025 — ElevenLabs raised USD 80 million in Series C funding to expand its AI voice synthesis and audiobook narration platform, validating AI narration as a standalone commercial opportunity within audiobooks market infrastructure.

- September 2025 — Penguin Random House Audio announced a global partnership with Findaway Voices to distribute its full 22,000-title backlist across all major non-Audible platforms, reducing single-platform revenue concentration risk by an estimated 18%.

Competitive Landscape

Market Concentration, Platform Power, and Publisher Dynamics Define the Audiobooks Market in 2026

The global audiobooks market competitive landscape is defined by platform concentration at the distribution layer and meaningful fragmentation across production technology, library services, and self-publishing infrastructure. Amazon’s Audible controls approximately 41.3% of global platform revenue, giving it disproportionate influence over content access, author royalties, and listener acquisition. Spotify, Apple Books, and Google Play Books account for an additional 31.4% of platform revenue, with Spotify’s subscription bundle strategy posing the most significant challenge to Audible’s dominance. Scribd, OverDrive, Libro.fm, and Hoopla maintain steady competitive pressure on Audible’s pricing and catalog exclusivity terms through 2035.

Key Market Segments

By Format Type

- Downloadable (Digital Purchase / Credit Redemption)

- Streaming Subscription (Unlimited Access)

- Physical / CD / Vinyl Audio

- Podcast-Integrated Audio (Hybrid Content)

By Genre

- Fiction (Literary, Thriller, Romance, Science Fiction)

- Non-Fiction (Biography, History, Current Affairs)

- Self-Help / Personal Development

- Business / Finance / Leadership

- Children’s and Young Adult

- Education / Academic / Professional

By Distribution Channel

- Online Platform (Audible, Spotify, Apple Books, Google Play Books)

- Library Digital Lending (OverDrive, Libby, Hoopla)

- Retail Store (Physical Audio, Gift Cards)

- Publisher Direct & Subscription Box

- Podcast-Integrated Distribution

By Revenue Model

- Subscription (Monthly Credit / Unlimited Catalog Access)

- À La Carte Purchase (Single Title Ownership)

- Library & Institutional Licensing

- Advertising-Supported Free Access

By Device Type

- Smartphone (iOS / Android)

- Smart Speaker (Amazon Echo / Google Nest / Apple HomePod)

- Tablet (iPad / Android Tablet)

- Desktop / Laptop Computer

- Dedicated e-Reader / Portable Audio Device

By Region

- North America (United States, Canada)

- Europe (Germany, United Kingdom, Scandinavia, France, Rest of Europe)

- Asia-Pacific (India, China, Japan, South Korea, Australia, Rest of APAC)

- Latin America (Brazil, Mexico, Rest of Latin America)

- Middle East & Africa

Report Features

| Feature | Description |

|---|---|

| Market Value (2026) | USD 11.38 billion |

| Forecast Revenue (2035) | USD 77.18 billion |

| CAGR (2026–2035) | 23.70% |

| Base Year for Estimation | 2026 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Format Type Analysis, Genre Deep Dive, Distribution Channel Economics, Revenue Model Breakdown, Device Type Analysis, AI Narration Impact Framework, Library Licensing Economics, Author Royalty Structure, Regional Analysis, Competitive Intelligence, SWOT Analysis |

| Segments Covered | By Format, By Genre, By Distribution Channel, By Revenue Model, By Device Type, By Region |

| Regional Analysis | North America (52.4%), Europe (24.6%), Asia-Pacific (14.8%), Latin America (5.4%), Middle East & Africa (2.8%) — country-level platform, CAGR, and listener data |

| Dominant Format | Downloadable Digital with 61.2% revenue share |

| Dominant Revenue Model | Subscription (Monthly Credit / Unlimited Access) with 52.4% share |

| Competitive Landscape | Audible (Amazon), Spotify, Apple Books, Google Play Books, Scribd, OverDrive, Hoopla, ElevenLabs, ACX, Findaway Voices, Libro.fm, Draft2Digital, Storytel |