Market Verdict

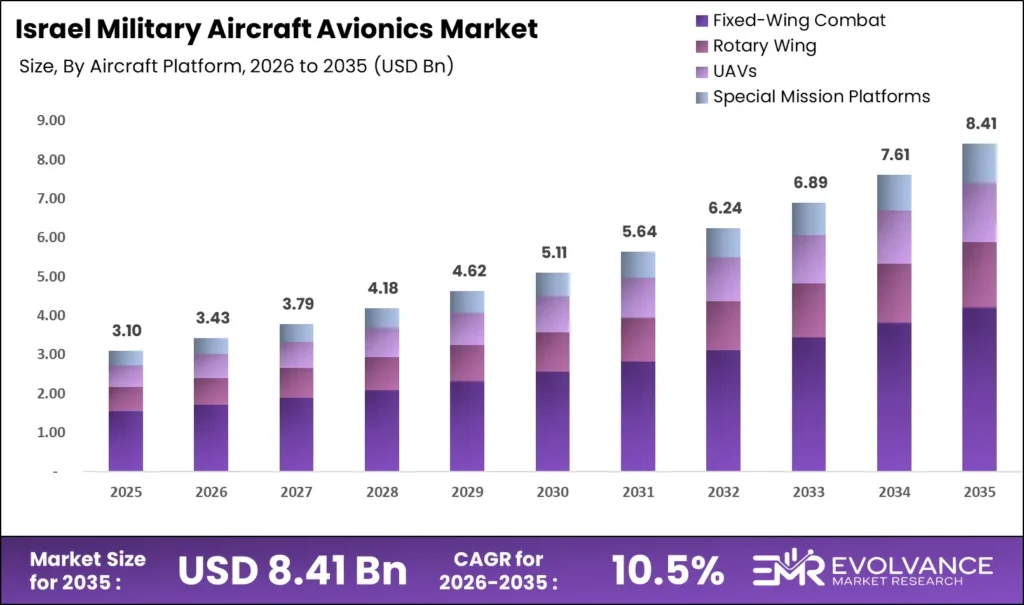

The Israel Military Aircraft Avionics Market is valued at USD 3.1 billion in 2025 and is projected to reach USD 3.43 billion in 2026, expanding to USD 8.41 billion by 2035 at a CAGR of 10.5%, according to our research analysts. This trajectory is not a function of domestic budget expansion alone. Combat-validated EW systems, DIRCM suites, and open-architecture avionics integration have created a procurement premium that rearmament-driven buyers in Europe and Asia-Pacific are paying above market rate to access. Integrators holding battlefield-proven platform records will capture a disproportionate share as global fleet modernization accelerates through the forecast period.

Key Takeaways

- Market Size:

- Market value in 2025: USD 3.1 billion

- Market value in 2026: USD 3.43 billion

- Market value in 2035: USD 8.41 billion

- CAGR: 10.5% (2025–2035)

- Dominant Segments:

- Aircraft Platform: Fixed-Wing Combat (dominant as of 2025)

- Avionics Subsystem: Electronic Warfare (EW) Systems (dominant as of 2025)

- Integration Type: Retrofit / Domestic Modification (dominant as of 2025)

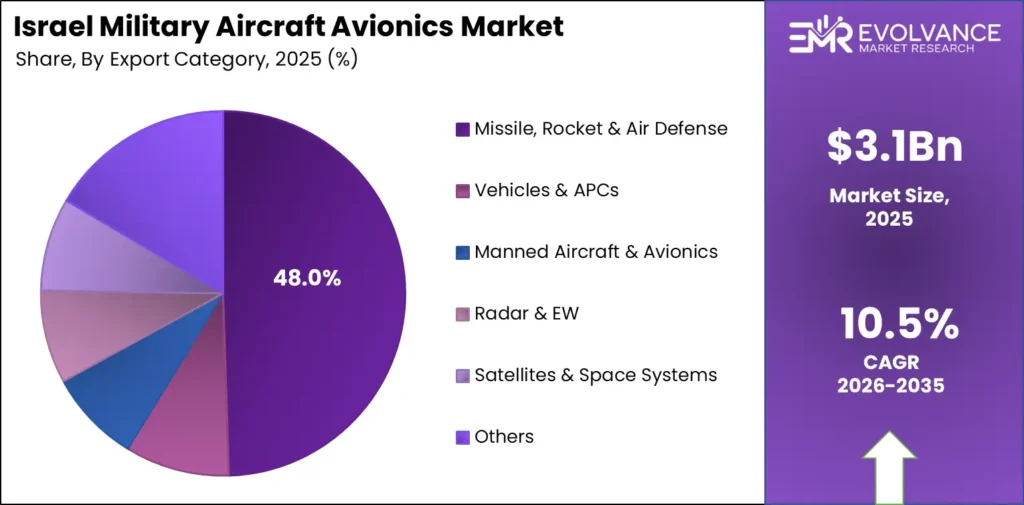

- Export Category: Missile, Rocket & Air Defense at 48.0% share as of 2024

- Dominant Region:

- Leading region: Europe at 54.0% of Israeli defense exports in 2024, valued at approximately USD 7.9 billion (as per our research)

Source: Evolvance Market Research

Market Overview

Military aircraft avionics integration converts airframes into multi-domain weapons systems. The Israeli Air Force, export customers across NATO and Asia-Pacific, and Gulf state air arms all depend on this market for electronic warfare suites, DIRCM self-protection systems, C4ISR architectures, and navigation and INS upgrades. Without domestic avionics integration capability, platform operators lose the ability to configure aircraft for specific threat environments, a deficit no off-the-shelf OEM linefit product can fully substitute.

To produce this analysis, our team at EMR conducted structured interviews with procurement officials, integrators, and platform operators across Israel, Europe, and Asia-Pacific between 2023 and 2025. We covered over 150 data points across company financials, government procurement disclosures, export registry filings from SIBAT, and trade association data from the Israel Export Institute. Geographic scope spans Israel’s domestic procurement, bilateral FMS relationships, and export corridors to Europe, Asia-Pacific, the Gulf, and North America. All forecast assumptions were validated against Israel Ministry of Defense budget announcements and publicly disclosed contract awards.

The buyer in this market is typically a ministry of defense or air force procurement directorate facing a specific survivability gap on a legacy platform. The trigger is either a new threat environment documented by national intelligence assessment or an allied interoperability requirement set by NATO or a bilateral defense framework. Failure to procure creates an operationally exposed airframe that cannot be deployed into contested airspace, a risk no air force accepts in the current threat environment shaped by the Russia-Ukraine conflict and Middle East operations.

Israel’s total defense spending surged 65% to USD 46.5 billion in 2024, raising the military burden to 8.8% of GDP, the second-highest military-to-GDP ratio globally after Ukraine. Total defense exports reached USD 14.7–15 billion in 2024, a 13% YoY increase and the fourth consecutive record year per SIBAT, with manned aircraft and avionics representing 8% of export deals at approximately USD 1.18 billion.

The global military aircraft avionics market reached approximately USD 25.84 billion in 2024. Institutional entry by Gulf-region subsidiaries of Israeli defense firms signals that in-country presence is becoming a market-access requirement, illustrated by Controp Precision Technologies establishing a USD 30 million UAE defense subsidiary in October 2025. For investors, the concentration of Israel’s avionics export value in EW and DIRCM categories indicates higher-margin positioning than the headline market size implies.

What Is Actually Driving This Market

European NATO rearmament has become the dominant demand engine, with a causal mechanism running directly through procurement necessity rather than strategic preference. The European Defence Agency reported that EU member states collectively spent EUR 343 billion on defense in 2024, a 19% YoY increase, with equipment procurement reaching a record EUR 88 billion, up 39% YoY.

NATO’s 2% GDP spending commitment, activated by the Russia-Ukraine conflict, mandates procurement timelines that existing European avionics industrial capacity cannot satisfy, making Israeli EW systems and retrofit integrators the only suppliers with immediate delivery capability and combat-proven track records. For investors, Europe’s equipment procurement surge is a multi-year committed budget line, not a one-cycle event.

The Germany Arrow-3 missile defense and radar system delivery in December 2025, valued at EUR 4 billion (approximately USD 4.6 billion), is the clearest single demonstration of how combat-proven Israeli avionics-adjacent systems convert European rearmament budgets into contracted revenue at scale. Israel Aerospace Industries served as prime contractor with ELTA Systems providing the Green Pine radar, making Germany the first country outside Israel and the United States to field the Arrow-3 system.

The causal mechanism here is certification: ELTA’s Green Pine radar carried IAF operational validation that no European radar system could match on the required delivery timeline, making it a procurement necessity rather than a preference. For operators, programs with IAF-certified subsystems hold a decisive timeline advantage in competitive European tenders where delivery schedule is a contract-award criterion.

Israel’s defense budget CAGR of 3% through 2028 understates actual avionics procurement growth because it excludes US-funded FMS cases and emergency supplemental authorizations. The US Department of Defense maintains 751 active Foreign Military Sales cases with Israel valued at USD 39.2 billion as of April 2025, with USD 3.3 billion in annual Foreign Military Financing and an additional USD 500 million specifically for missile defense.

The causal mechanism is contractual: FMS cases create multi-year procurement obligations that lock in avionics upgrade spending independent of annual IMOD budget allocations, providing Israeli integrators with revenue predictability that purely domestic procurement cannot match. For operators, alignment with FMS program structures determines access to the most durable revenue stream in this market.

- EU rearmament has converted European governments from occasional buyers into structurally committed procurement partners with mandatory spending timelines enforced by the European Defence Agency.

- EU 27 defense equipment procurement: EUR 88 billion in 2024, a record 39% YoY increase (European Defence Agency, 2024)

- Germany Arrow-3 delivery: USD 4.6 billion, December 2025, Israel’s largest single defense export, prime contractor IAI with ELTA Green Pine radar (E4 deployment example: missile defense industry, quantified outcome USD 4.6 billion, timeframe December 2025)

- US FMS active cases with Israel: 751 cases at USD 39.2 billion as of April 2025, plus USD 3.3 billion annual FMF (US Department of Defense)

- Israel defense budget CAGR: 3% (2024–2028), understating true avionics demand growth due to FMS and supplemental exclusions

- Operators with IAF-certified subsystems should prioritize European tender participation now, before domestic European avionics production capacity catches up to NATO’s spending mandate.

Where the Real Risk Is

European arms export restrictions represent the most acute near-term pipeline risk for Israeli avionics integrators, and available data is insufficient to determine whether this risk is temporary or permanent at the bilateral level. Israeli defense-tech startups attracted over USD 1 billion in investment in 2025, exceeding all prior years combined, with Israel’s MAFAT directorate placing NIS 1.08 billion in orders across the startup ecosystem.

This venture capital inflow into the avionics and autonomous systems layer is correlating with export license uncertainty, not causing it, but the combination creates a structural tension: the ecosystem is expanding precisely when its primary export corridor faces regulatory instability. For investors, firms with European revenue concentration above 30% face margin compression until export license normalization is confirmed by specific bilateral policy announcements.

Global aerospace supply chain fragility adds an operational constraint that is structural rather than temporary, per IATA’s own 2025 assessment. Titanium and nickel tubing shortages are driving 50 to 60 week procurement cycles for avionics-grade components, and IATA quantified USD 11 billion in unexpected industry costs in 2025 alone.

Israel’s aircraft and spacecraft parts import CAGR of 25.94% between 2022 and 2024, reaching USD 318 million in 2024, signals that import dependence is accelerating at precisely the moment global component lead times are lengthening. For operators, qualifying alternative suppliers for avionics-grade components before contract delivery deadlines compress is the single most time-sensitive operational decision in this market.

- The risk most investors underestimate: European export license restrictions can halt revenue recognition on committed backlog contracts without triggering formal contract cancellation, creating a cash flow gap invisible in headline backlog figures.

- Israeli defense-tech startup investment: over USD 1 billion in 2025, with MAFAT placing NIS 1.08 billion in ecosystem orders (Globes, December 2025)

- IATA-quantified supply chain costs: USD 11 billion in unexpected industry costs in 2025, with 50 to 60 week avionics-grade component lead times

- Israel aircraft parts import CAGR: 25.94% (2022–2024), total USD 318 million in 2024, reflecting accelerating foreign component dependence

- Watch for German Bundestag arms export committee votes on Israeli license renewals as the leading indicator that European pipeline risk is resolving or deepening.

Segmentation: Where Value Is Concentrating

Aircraft Platform Insights

Fixed-Wing Combat Tops the Field: Dominant Share in 2025

Fixed-wing combat platforms anchor avionics demand because they carry the highest per-aircraft avionics content of any platform category in the Israeli fleet. The F-35I Adir, F-16I Sufa, and the incoming F-15IA fleet each require platform-specific EW architecture, DIRCM integration, and C4ISR configuration that cannot be shared across types. Combat experience from IAF operations continuously generates upgrade requirements that rotate through the retrofit cycle, making fixed-wing combat the most recurring revenue segment in this market. For investors, the F-15IA procurement pipeline extending to 2035 guarantees fixed-wing avionics demand visibility across the full forecast period.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Fixed-Wing Combat | Dominant | F-35I Adir, F-16I, F-15IA upgrade cycles | Sustained through 2035 via confirmed procurement pipeline |

| Rotary Wing | Growing | CH-53K Pereh avionics indigenization | Accelerating via helicopter fleet recapitalization |

| UAVs | Expanding | Autonomous systems procurement mandates | Fastest-growing sub-segment by unit volume |

| Special Mission Platforms | Niche | Intelligence and maritime surveillance requirements | Stable, high avionics content per platform |

Avionics Subsystem Insights

The Case for EW Systems: Dominant Share and Counting in 2025

Electronic warfare systems hold the dominant avionics subsystem position because combat operations have established EW capability as the non-negotiable survivability requirement for any IAF platform entering contested airspace. The EW subsystem encompasses self-protection suites, radar jamming, and electronic intelligence collection, producing the highest content and highest margin of any subsystem in the Israeli avionics stack. IMOD’s DDR&D directorate certification requirements mean EW system approval is the longest lead-time item in any avionics upgrade program. For operators, EW certification timelines must be initiated well ahead of platform delivery schedules or contract milestones will be missed.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Electronic Warfare (EW) Systems | Dominant | Survivability mandates across all combat platforms | Expanding into directed-energy integration |

| Command & Control (C2) | High | Multi-domain C4ISR interoperability requirements | Growing with AI-integrated systems demand |

| Cockpit / Flight Avionics | Moderate | Fifth-generation platform integration | Stable, driven by F-35I TR-3 upgrade cycle |

| Anti-Missile Self-Protection (DIRCM) | Growing | Rotary-wing and transport platform protection mandates | Accelerating across export and domestic markets |

| Navigation & INS | Moderate | GPS anti-jamming requirements in contested environments | Stable with GPS-denied scenario demand |

| Sensors & Mission Systems | Moderate | ISTAR and maritime surveillance requirements | Growing via export-driven MALE UAV programs |

Integration Type Insights

Retrofit / Domestic Modification’s Edge in the Integration Type Race

Retrofit and domestic modification dominates because Israel’s strategy of acquiring foreign-origin platforms and reconfiguring them with Israeli-developed avionics creates an integration workflow that is inherently retrofit-based. The US International Trade Administration confirmed Israel’s 50/50 domestic and export split in avionics sales is sustained primarily through retrofit programs, not new-build OEM contracts.

The F-35I Adir fleet reached 46 operational aircraft as of 2025, targeting 75 total units by 2030, with each aircraft requiring Israeli-specific EW architecture modifications that must be retrofitted post-delivery. For investors, retrofit programs generate longer revenue cycles per platform than linefit contracts, with upgrade iterations following every major operational deployment cycle.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Retrofit / Domestic Modification | Dominant | Foreign platform indigenization strategy | Sustained by F-35I, CH-53K, F-15IA programs |

| OEM Linefit | Secondary | Export platform integration agreements | Growing via open-architecture mission computer deals |

| Upgrade / Modernization | Growing | Block upgrade cycles on deployed fleets | Expanding with European NATO fleet modernization demand |

Export Category Insights

Where Export Spending Goes: Missile, Rocket & Air Defense at 48% in 2024

Missile, Rocket & Air Defense held 48.0% of Israel’s defense export category mix in 2024 per SIBAT, with Manned Aircraft and Avionics at 8% alongside Radar and EW at 8%, together representing approximately USD 2.36 billion in combined export value. The Middle East military aircraft modernization market reached USD 1.09 billion in 2025, with fighter aircraft upgrades representing 72% of that segment in 2026, validating that avionics-content-heavy programs dominate regional procurement.

IMOD’s autonomous platform avionics contract awarded in December 2024 established autonomous avionics as a validated operational procurement standard, signaling that the Drones & UAVs export category will grow from its current 1% share as battlefield validation accumulates. For operators, the export category data confirms that avionics-adjacent technologies collectively represent the largest share of Israeli defense export value, not standalone platform sales.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Missile, Rocket & Air Defense | 48.0% | Arrow-3, Iron Dome, MRSAM export demand | Dominant through forecast period |

| Vehicles & APCs | 9% | Ground force modernization | Stable |

| Manned Aircraft & Avionics | 8% | EW, DIRCM, and retrofit program exports | Growing with NATO rearmament demand |

| Radar & EW | 8% | Green Pine, ELTA systems international demand | Growing |

| Satellites & Space Systems | 8% | ISR satellite export programs | Stable |

| Observation & Optronics | 6% | ISTAR and border surveillance | Expanding via Gulf co-production |

| Intelligence, Information & Cyber | 4% | C4ISR export demand | Growing |

| Ammunition & Armaments | 3% | PGM export demand | Stable |

| C4I & Communications | 2% | Network-centric warfare integration | Expanding |

| Drones & UAVs | 1% | Autonomous platform exports | Fastest growing by category trajectory |

Segments Covered in This Report

Aircraft Platform

- Fixed-Wing Combat

- Rotary Wing

- UAVs

- Special Mission Platforms

Avionics Subsystem

- Electronic Warfare (EW) Systems

- Command & Control (C2)

- Cockpit / Flight Avionics

- Anti-Missile Self-Protection (DIRCM)

- Navigation & INS

- Sensors & Mission Systems

Integration Type

- Retrofit / Domestic Modification

- OEM Linefit

- Upgrade / Modernization

Export Category

- Missile, Rocket & Air Defense

- Vehicles & APCs

- Manned Aircraft & Avionics

- Radar & EW

- Satellites & Space Systems

- Observation & Optronics

- Intelligence, Information & Cyber

- Ammunition & Armaments

- C4I & Communications

- Drones & UAVs

Value is concentrating in EW systems and DIRCM within the avionics subsystem category and in retrofit integration over OEM linefit across integration types. The autonomous platform avionics sub-segment within UAVs is fragmenting fastest, with startup entrants competing against established integrators for IMOD contract awards confirmed by MAFAT procurement data from 2025. For investors, EW systems and DIRCM represent the defensible margin position; UAV avionics represent the highest-growth but most fragmented competitive space.

Regional Analysis: Where Geography Creates Advantage

Europe held 54% of Israel’s total defense exports in 2024, equivalent to approximately USD 7.9 billion, up sharply from 35% in 2023, as NATO member procurement programs accelerated following the Russia-Ukraine conflict. The structural driver is Germany’s Sondervermögen defense fund combined with the European Defence Agency’s record equipment procurement mandate, which created committed budget authorization bypassing normal multi-year procurement timelines.

The Adani-Elbit Advanced Systems India joint venture, operating from a 50,000 square foot facility in Hyderabad, had by early 2024 supplied more than 20 Hermes 900 MALE UAVs internationally, establishing the only Hermes 900 production site outside Israel and demonstrating that co-production partnerships generate export volume beyond bilateral relationships. For investors, Europe’s share expansion from 35% to 54% in a single year represents a structural realignment warranting overweight positioning in Israeli EW and radar integrators with confirmed European pipeline.

Asia-Pacific generated approximately USD 3.4 billion in Israeli defense exports in 2024, representing 23% of total exports, making it Israel’s second-largest export market. India, historically accounting for 34% of all Israeli defense exports between 2020 and 2024, anchors this corridor through government-to-government procurement agreements and joint venture co-production under India’s Atmanirbhar Bharat initiative enforced by the Defence Acquisition Council.

IAI’s Asia revenue in H1 2025 reached approximately USD 901 million, representing 28% of IAI’s USD 3.22 billion semi-annual total, confirming that Asia-Pacific is generating sustained revenue velocity, not one-cycle procurement spikes. For operators, establishing in-country manufacturing presence in Asia-Pacific is the condition for sustaining market access as procurement ministries enforce local content thresholds on follow-on orders.

The Middle East, excluding Israel’s domestic procurement, generated approximately USD 1.76 billion from Abraham Accords partner countries (UAE, Bahrain, and Morocco) in 2024, rising to 12% of total Israeli exports from 3% in 2023. Total Middle East military spending reached USD 243 billion in 2024, a 15% increase from 2023, with Saudi Arabia, UAE, Qatar, and Israel all running active avionics and air defense modernization programs simultaneously under Gulf Cooperation Council procurement diversification mandates.

The Abraham Accords normalization framework created a diplomatic channel through which Israeli EW systems and airborne self-protection suites can be offered to Gulf air forces that previously had no procurement pathway. For investors, the Gulf corridor represents the fastest-growing share of Israel’s export base and the least supply-chain-constrained region, making it the most reliable short-term margin expansion opportunity in the regional breakdown.

| Region | Share % | USD Value | Key Driver | Strategic Signal |

|---|---|---|---|---|

| Europe | 54% | ~USD 7.9B (2024) | NATO rearmament, EDA equipment mandate | Structural realignment from 35% in 2023 |

| Asia-Pacific | 23% | ~USD 3.4B (2024) | India co-production, fleet modernization | In-country manufacturing becoming market access condition |

| Middle East (Abraham Accords) | 12% | ~USD 1.76B (2024) | Abraham Accords, Gulf air defense programs | Fastest-growing corridor; least export-license-constrained |

| North America | 9% | ~USD 1.32B (2024) | FMS subsidiary channels, EW assemblies | Stable; driven by Elbit Systems of America and ELTA North America |

Competitive Landscape: Who Is Pulling Ahead and Why

Elbit Systems and Israel Aerospace Industries hold structural advantages no challenger can replicate on a 3 to 5 year timeline: direct integration access to live IAF operational data from active combat deployments. Elbit’s record backlog of USD 28.1 billion as of December 31, 2025, with 72% sourced internationally, and IAI’s backlog exceeding USD 30 billion, reflect buyers paying a premium specifically for that operational data advantage. For investors, backlog concentration in EW and battle management categories signals durable margin, not commodity revenue.

Rafael Advanced Defense Systems recorded USD 5.9 billion in FY2025 sales, up 21.5% YoY, with net profit crossing 1 billion NIS for the first time, establishing it as the most aggressive domestic challenger. Rafael’s strength in the Litening targeting pod, Iron Dome fire control, and airborne directed-energy systems creates a portfolio that complements rather than directly competes with Elbit’s EW self-protection suite architecture.

The acquisition of Bird Aerosystems by US defense firm Ondas in March 2026 at approximately USD 133 million, gaining airborne missile protection systems deployed on more than 700 aircraft across more than 40 types, illustrates the Western response: acquiring proven Israeli DIRCM technology rather than developing competing systems domestically. For investors, this acquisition pattern confirms that Israeli mid-tier avionics specialists with multi-platform deployment records carry acquisition premiums.

Western integrators including Thales, Northrop Grumman, and L3Harris participate through partnership and subcontract channels rather than direct competition on Israeli platform programs. This reflects the DDR&D certification barrier that IMOD imposes on non-domestic integrators serving as prime contractors on IAF avionics modification programs.

The market is consolidating at the top around the three Israeli primes while fragmenting at the startup and subsystem tier, where MAFAT procurement data shows autonomous platforms, AI-integrated sensors, and cyber-avionics attracting new entrants at pace. For operators, the practical implication is that no non-Israeli integrator can serve as prime contractor on an IAF avionics program without an Israeli industrial partner holding DDR&D certification authority.

| Company | Market Position | Key Advantage | Recent Move |

|---|---|---|---|

| Elbit Systems | Market Leader | Combat-validated EW, DIRCM, C4ISR across all IAF platforms | USD 28.1B backlog; 72% international; European production expansion |

| Israel Aerospace Industries (IAI) | Co-Leader | ELTA radar, battle management, MALE UAV production at scale | USD 30B+ backlog; IPO process initiated at USD 25–32B valuation |

| Rafael Advanced Defense Systems | Aggressive Challenger | Litening pod, Iron Dome fire control, directed-energy systems | USD 5.9B FY2025 revenue; IPO valuation USD 20–23B |

| Lockheed Martin | Platform OEM / Integration Partner | F-35I and F-15IA program prime; CH-53K integration line | Dedicated Israeli avionics integration production line established |

| RTX Corporation (Collins Aerospace) | Subsystem Supplier | AMRAAM and SM-3 missile system integration | Five major DoW agreements for expanded missile production |

| L3Harris Technologies | Partnership Entrant | Open-architecture mission computer integration capability | MoU with IAI for light-attack aircraft program |

| Thales Group | European Subsystem Supplier | Avionics and air defense for NATO customers | EUR 12.234B defense segment revenue FY2025 |

| Northrop Grumman | Mission Systems Supplier | Aeronautics and mission systems at scale | USD 91.5B backlog; active in Israeli platform programs |

| BAE Systems | EW Subsystem Supplier | Electronic warfare systems for NATO-aligned platforms | Active supplier on allied avionics programs |

| Leonardo S.p.A. | Avionics Subsystem Supplier | Airborne sensor and mission system integration | Active in Mediterranean and NATO avionics programs |

| General Dynamics | Mission Systems Supplier | C4ISR and mission computing for allied programs | Active supplier on multi-platform avionics programs |

| Leonardo DRS (RADA Technologies) | Radar Subsystem Supplier | Tactical radar and active protection system integration | Integrated within Leonardo DRS defense portfolio |

| Astronautics (Israel) Ltd. | Domestic Avionics Supplier | Navigation and flight management for F-35I and CH-53K | Active IAF program supplier in 2025 |

Where This Market Goes Next

India’s Defence Acquisition Council approved a USD 8.7 billion arms package in December 2025, incorporating Rafael SPICE-1000 precision guidance kits, IAI Air LORA ballistic missiles, and Rampage air-to-surface missiles, activating a co-production and avionics integration pipeline extending well beyond the initial procurement cycle. The activation condition for sustained Indian market growth is the Defence Acquisition Council’s local content threshold enforcement, which mandates in-country manufacturing for follow-on orders under the Atmanirbhar Bharat initiative.

Israeli integrators already embedded in Indian co-production structures are best positioned to capture avionics sustainment and upgrade revenue that follows initial platform delivery. For operators, establishing a dedicated India-facing production and certification entity before 2027 is the condition for participating in the next phase of Indian fleet modernization.

Europe’s military aviation avionics market is projected to reach USD 31.07 billion by 2033 at a CAGR of 9.20%, with military aviation as the fastest-growing platform at approximately 7.4% CAGR, driven by F-35 procurement by NATO allies, Eurofighter Tranche 5 upgrades, and EW system investments validated by operational assessments from the Russia-Ukraine conflict.

The activation condition for Israeli firms to capture disproportionate European share is in-country production presence satisfying EU member state sovereign industrial content requirements, with the causal mechanism running through procurement rules that increasingly favor suppliers with domestic manufacturing footprint. Israeli integrators who established European subsidiaries ahead of NATO’s rearmament surge are positioned to capture the avionics upgrade pipeline; those who did not face export license dependency as the binding constraint. For operators, European production infrastructure investment now is a 3 to 5 year competitive positioning decision, not a short-cycle cost item.

The Asia-Pacific combined military avionics market is growing toward USD 25 billion by 2030 at approximately 7% CAGR, with India, Japan, and South Korea as primary demand centers, driven by fleet recapitalization programs overseen by their respective defense acquisition agencies. The activation condition for Israeli firms to access the South Korean and Japanese segments is government-to-government framework agreements, with correlation rather than confirmed causation currently linking open-architecture mission computer capability to platform access in those markets.

Early deployments indicate that open-architecture integration will be the technical standard unlocking the broadest platform access across Asia-Pacific procurement programs through the 2027 to 2030 window. For operators, the window to establish Asia-Pacific co-production structures under government-to-government frameworks closes as local defense industrial policies mandate domestic content on a binding rather than preferential basis.

| Condition | Timeline | Upside | Who Benefits |

|---|---|---|---|

| India local content enforcement activates co-production avionics orders | 2026–2028 | USD 8.7B arms package drives multi-year avionics sustainment pipeline | IAI, Elbit, Rafael via existing JV structures |

| European in-country production satisfies EU sovereign content rules | 2025–2030 | USD 31.07B European avionics market at 9.20% CAGR through 2033 | Integrators with established European manufacturing footprint |

| Asia-Pacific G2G framework agreements unlock South Korean and Japanese procurement | 2027–2030 | USD 25B Asia-Pacific military avionics market by 2030 | IAI, Elbit via government-to-government partnership channels |

Key Developments

- March 2026 — Israeli Government Companies Authority submitted draft proposals for partial IPOs of both Rafael Advanced Defense Systems (valuation NIS 60–70 billion, approximately USD 20–23 billion, up to 49% stake) and Israel Aerospace Industries (valuation NIS 80–100 billion, approximately USD 25–32 billion, 25–30% stake). Signals a structural shift from state-owned defense entities to partially privatized publicly listed companies, opening both to institutional equity capital for the first time.

- March 2026 — Elbit Systems disclosed a late-2025 IMOD contract to develop and produce the XCalibur airborne high-power laser weapon for fixed-wing aircraft and the Sting system for helicopter platforms, the first Israeli military contract for operationally deployed airborne directed-energy weapons. Signals directed-energy avionics transitioning from R&D to active procurement budgets, with export orders expected to follow IDF operational validation.

- February 2026 — Israeli Ministry of Defense signed a NIS 400 million (approximately USD 130 million) five-year agreement with Elbit Systems to integrate avionics, EW, C2, and DIRCM systems into 12 new CH-53K Pereh heavy-lift helicopters. Signals helicopter fleet indigenization as a recurring domestic procurement pattern with Elbit as the designated rotary-wing systems integrator.

- January 2026 — IAI signed a USD 3.1 billion follow-on contract with IMOD for expansion of Germany’s Arrow-3 missile defense program, bringing total Arrow-3 program value above USD 6.5 billion. Signals that high-value radar and battle management system exports generate follow-on contract flow at scale, validating the Arrow-3 architecture as a template for future bilateral system transfers.

- November 2025 — Elbit Systems disclosed a USD 2.3 billion, eight-year undisclosed strategic international defense contract via TASE stock exchange filing, its largest single contract announcement of 2025. Signals that long-cycle export-oriented avionics agreements are reshaping Elbit’s revenue profile toward multi-year international concentration.

- October 2025 — L3Harris Technologies and Israel Aerospace Industries signed a Memorandum of Understanding to jointly develop the Blue Sky Warden light-attack aircraft, combining L3Harris’ Sky Warden airframe with IAI’s open-architecture mission computer and Israeli-specific mission equipment. Signals open-architecture mission integration as the emerging technical standard for Israeli-aligned export platform programs.

- September 2025 — Rafael Advanced Defense Systems and Israel’s Ministry of Defense DDR&D completed full development of the Iron Beam 450 high-power laser air defense system, with first IDF production units scheduled for delivery by year-end 2025. Signals directed-energy air defense transitioning from development to operational procurement, establishing a domestic baseline before international export certification.

- July 2025 — Lockheed Martin awarded a USD 33.4 million contract for Israel F-35 Block 4 avionics upgrades. Signals continued US-Israel co-development of fifth-generation EW architecture with Israeli-specific modifications embedded inside the global F-35 program.

- May 2025 — Elbit Systems raised USD 512 million in a Nasdaq public share offering at USD 375 per share, with proceeds earmarked for European production infrastructure expansion, working capital, and acquisitions. Signals Israeli avionics integrators scaling capacity ahead of committed European demand rather than reacting to it.

- March 2025 — Lockheed Martin (Sikorsky) contracted to build a dedicated production line integrating Israeli avionics and EW suites into CH-53K helicopters. Signals Israeli avionics firms transitioning from aftermarket suppliers to embedded participants in US OEM production infrastructure.

- January 2025 — Elbit Systems awarded USD 80 million IMOD contract to develop and install an advanced airborne self-protection suite combining EW, DIRCM, and Chaff/Flare systems on the F-16I fleet. Signals accelerating upgrade tempo for legacy fixed-wing combat platforms with self-protection suite integration as the standard retrofit entry point.

- October 2024 — Bharat Electronics Limited and IAI established BEL IAI AeroSystems Private Ltd in Delhi to provide lifecycle support and manufacturing for MRSAM systems for India’s tri-services under the Atmanirbhar Bharat initiative. Signals co-production joint ventures as the structural market-access mechanism for Israeli avionics firms in the Indian procurement ecosystem.