What is the Hydrogen Hubs Market Size?

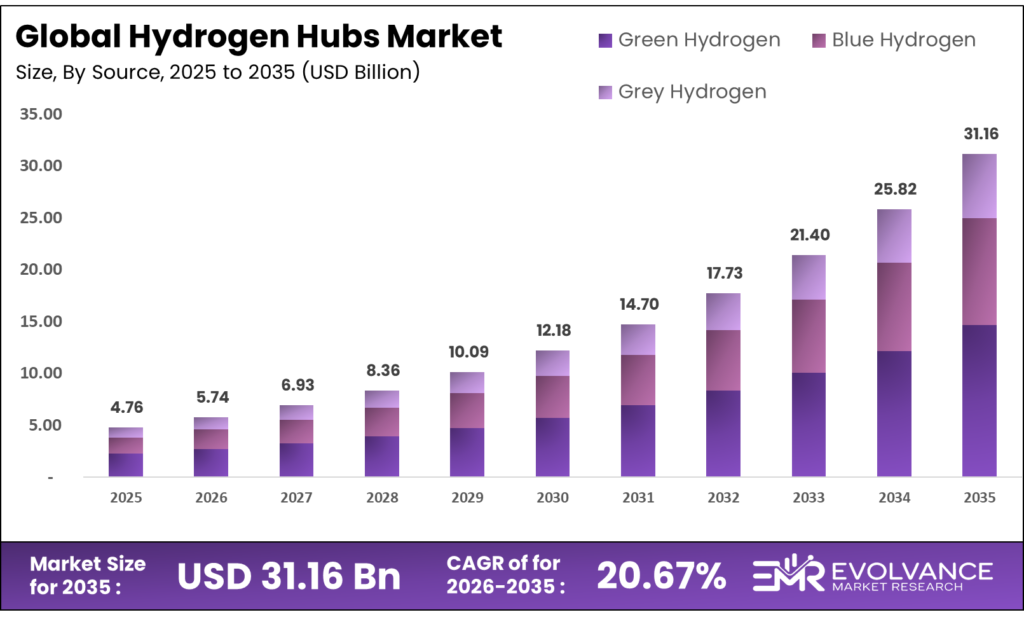

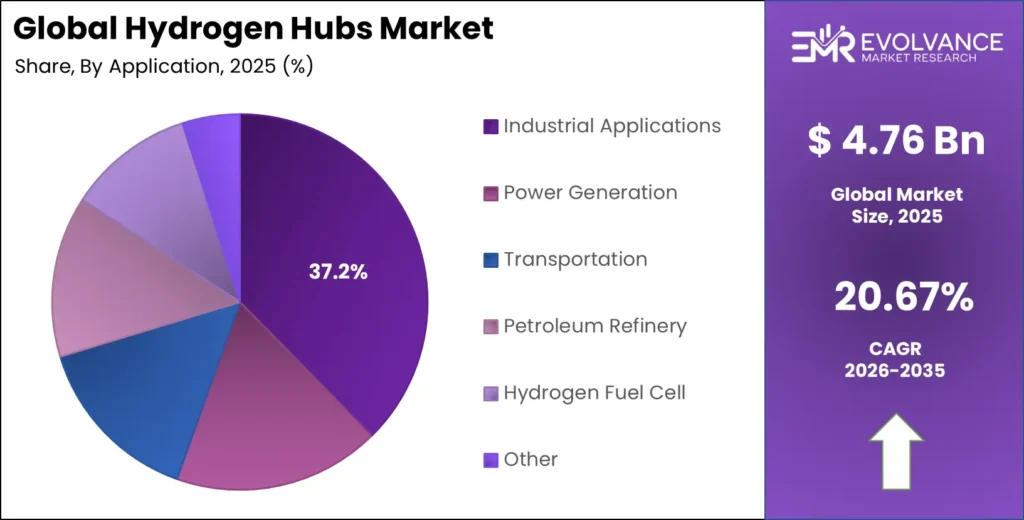

The Global Hydrogen Hubs Market size will be worth around USD 31.16 Billion by 2035 from USD 4.76 Billion in 2025, growing at a CAGR of 20.67% during the forecast period 2026 to 2035. This pace reflects government-backed funding programs that are pulling projects out of planning and into active build — compressing timelines vendors once assumed would be far longer. Buyers are locking in long-term offtake agreements ahead of supply availability, signaling that demand-side confidence is outpacing infrastructure readiness. On the supply side, hydrogen electrolyzer cost uncertainty and delayed final investment decisions remain the primary bottleneck constraining faster hub deployment.

Market Highlights

- The Hydrogen Hubs Market will grow from USD 4.76 Billion in 2025 to USD 31.16 Billion by 2035, at a CAGR of 20.67%.

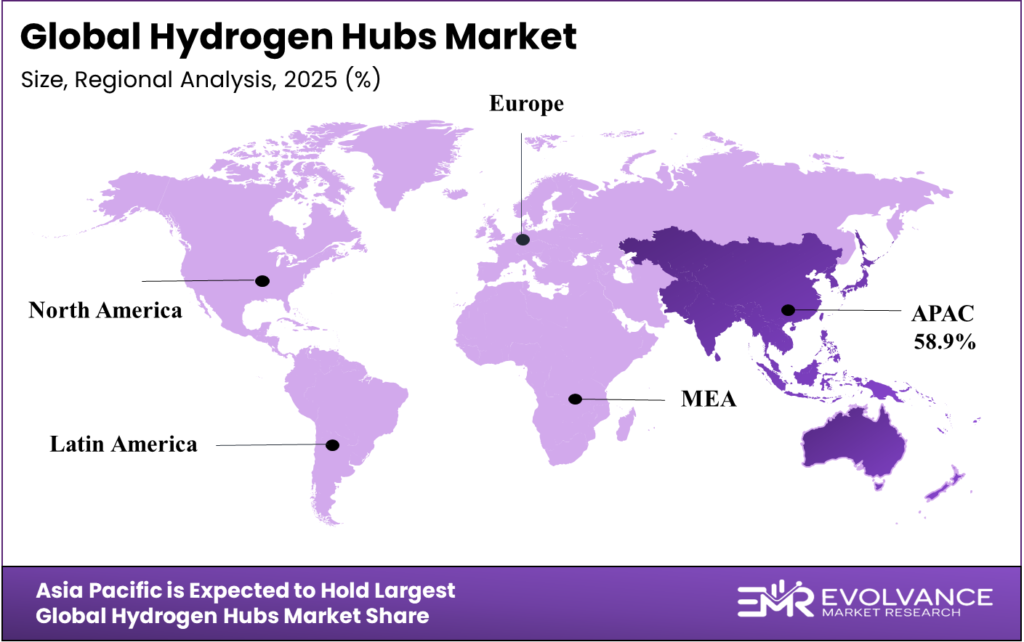

- Asia-Pacific leads all regions with a 58.9% share, valued at USD 2.80 Billion in 2025.

- Green Hydrogen dominates the By Source segment with a 45.7% share in 2025.

- Electrolysis-Based technology holds a 43.1% share in the By Technology segment.

- Industrial Applications leads the By Application segment with a 37.2% share.

- Cylinder distribution holds a 54.8% share in the By Distribution Channel segment.

- Electrolyzers dominate the By Infrastructure Component segment with a 46.2% share.

- Ammonia Production leads the By Offtake Sector segment with a 41.9% share.

- Salt Cavern Storage dominates the By Storage Method segment with a 63.7% share.

- Operational Hubs lead the By Hub Development Stage segment with a 67.2% share.

- Publicly Funded Hubs dominate the By Funding Model segment with a 58.3% share.

Market Overview

Hydrogen hubs are large-scale, co-located networks that link hydrogen production, storage, transport, and industrial end-use within a single geographic zone. They differ from standalone hydrogen projects because they serve multiple offtakers and sectors simultaneously, creating shared infrastructure economics. This shared model lowers per-unit costs and reduces the financing risk that has historically blocked single-buyer projects from reaching final investment decisions.

The market spans a wide set of production pathways — from green hydrogen made via electrolysis powered by renewables, to blue hydrogen from natural gas with carbon capture, to grey hydrogen from conventional steam reforming. Each pathway serves different cost points and decarbonization targets. The mix of technologies within a single hub is increasingly the norm, as developers seek to match supply volumes to buyer timelines regardless of feedstock.

The European Union’s Hydrogen Bank pilot auction attracted 132 project bids across 17 countries, representing 8.5 GW of planned electrolyzer capacity. This signals that developers across multiple geographies see hub-scale renewable hydrogen as commercially viable with the right revenue support — and that competition for public funding is already intense.

European hydrogen IPCEI programs combined €1.4 Billion in public funding with €3.3 Billion in additional private investment across 13 hydrogen projects in 2024. This leverage ratio — roughly 2.4x private capital per euro of public support — shows that public mechanisms are successfully unlocking private capital at scale, a structural shift that directly supports faster hub deployment timelines.

Source Insights

Green Hydrogen dominates with 45.7% due to policy mandates and renewable cost declines.

In 2025, Green Hydrogen held a dominant market position in the By Source segment of the Hydrogen Hubs Market, with a 45.7% share. Buyers in steel, chemicals, and ammonia sectors are committing to green hydrogen to meet net-zero targets that cannot be satisfied with fossil-derived alternatives. Public funding programs explicitly require green hydrogen qualification, which locks out grey and blue variants from the largest government-backed hub awards.

Blue Hydrogen serves as a near-term bridge for industrial buyers that need large hydrogen volumes before green supply scales up. Its cost advantage over green hydrogen narrows as electrolyzer manufacturing grows, but for hubs in carbon-intensive regions with access to natural gas and sequestration sites, blue hydrogen remains the commercially rational entry point. Several major hub programs explicitly include blue hydrogen in their early phases to secure offtake volumes before transitioning.

Grey Hydrogen retains a role inside existing industrial facilities where hydrogen was already produced from steam methane reforming without carbon capture. As hub infrastructure connects these facilities to new supply networks, grey hydrogen volumes can be displaced over time. The speed of that displacement depends on how quickly hub developers can bring green or blue alternatives online at competitive delivered costs.

Technology Insights

Electrolysis-Based technology dominates with 43.1% due to policy alignment and clean hydrogen mandates.

In 2025, Electrolysis-Based technology held a dominant market position in the By Technology segment of the Hydrogen Hubs Market, with a 43.1% share. Government funding programs in the U.S. and Europe tie clean hydrogen eligibility directly to electrolysis-based production from renewable power.

Electric Hydrogen secured a US$46.3 Million DOE grant in March 2024 to scale electrolyzer output — a clear signal that domestic manufacturing capacity is becoming a policy priority as well as a commercial one. As electrolyzer costs fall and manufacturing scales, electrolysis-based hubs will gain further cost competitiveness against fossil-derived pathways.

Steam Methane Reforming (SMR) is the most widely deployed hydrogen production method inside existing industrial complexes. Within hub architectures, SMR units are typically integrated with carbon capture systems to qualify for blue hydrogen status. The capital cost of retrofitting SMR with capture is a known quantity for buyers, which makes it a lower-risk transition technology compared to building electrolysis capacity from scratch.

Partial Oxidation (POX) and Auto Thermal Reforming offer higher feedstock flexibility than SMR, making them relevant for hubs that process heavy hydrocarbons or need to handle variable feedstock quality. These technologies are less common in greenfield hubs but appear in industrial clusters tied to refinery and petrochemical complexes.

Application Insights

Industrial Applications dominates with 37.2% due to established hydrogen demand and decarbonization pressure.

In 2025, Industrial Applications held a dominant market position in the By Application segment of the Hydrogen Hubs Market, with a 37.2% share. Industrial buyers — particularly in chemicals, steel, and refining — already consume hydrogen at scale and are converting existing grey hydrogen demand into green or blue supply through hub offtake agreements.

The Gulf Coast Hydrogen Hub alone is expected to create approximately 45,000 direct jobs over its lifetime, reflecting the scale of industrial integration planned across its end-user network. This existing demand base makes industrial applications the lowest-risk anchor segment for hub developers seeking bankable offtake commitments.

Power Generation as a hub application is emerging where hydrogen is co-fired in gas turbines or used in fuel cells to provide grid-balancing services. The economics are currently challenging compared to direct industrial use, but hubs that produce surplus hydrogen during periods of low power demand are increasingly evaluating power generation as a flexible offtake pathway.

Distribution Channel Insights

Cylinder distribution dominates with 54.8% due to established last-mile logistics and broad end-user reach.

In 2025, Cylinder distribution held a dominant market position in the By Distribution Channel segment of the Hydrogen Hubs Market, with a 54.8% share. Cylinders provide the lowest-barrier entry point for buyers who cannot access pipeline networks or do not have the volume to justify tube trailer delivery. This is particularly true for smaller industrial and fuel cell buyers who are adopting hydrogen for the first time.

Pipeline distribution is the most cost-efficient channel at scale and is the preferred infrastructure for large industrial clusters within hub zones. New hydrogen pipeline networks are under development in Europe and the United States, with projects like H2MED linking production zones to demand centers across national borders. Pipeline economics improve sharply as throughput increases, making them the long-term backbone of hub supply chains.

Infrastructure Component Insights

Electrolyzers dominate with 46.2% due to policy-mandated green hydrogen production requirements.

In 2025, Electrolyzers held a dominant market position in the By Infrastructure Component segment of the Hydrogen Hubs Market, with a 46.2% share. Electrolyzer procurement is the first critical milestone in hub construction because equipment lead times — currently 18 to 36 months for large systems — determine overall project schedules. Hub developers that secure electrolyzer supply early gain a structural schedule advantage over competitors.

Pipelines and Transport Networks are the connective tissue of hub operations, linking production assets to storage and end-use facilities. Their capital intensity and long permitting timelines make them a gating factor for hub completion. In regions where gas pipeline repurposing is feasible, hydrogen can share existing rights-of-way, significantly reducing buildout costs and timelines.

Offtake Sector Insights

Ammonia Production dominates with 41.9% due to established export markets and long-term supply agreements.

In 2025, Ammonia Production held a dominant market position in the By Offtake Sector segment of the Hydrogen Hubs Market, with a 41.9% share. Ammonia is the preferred hydrogen carrier for export because it can be liquefied at moderate conditions and has an established global shipping and storage infrastructure.

Long-term offtake agreements — such as EnBW’s contract for 100,000 tons of green ammonia annually beginning in 2027 — demonstrate that import buyers in Europe are already locking in supply, giving hub developers the demand certainty they need to reach final investment decisions.

Steel Manufacturing is the fastest-growing offtake sector by ambition. Direct-reduced iron production using green hydrogen instead of coking coal requires large, stable hydrogen supply — exactly what hub infrastructure is designed to deliver. Several European steel producers have staked their decarbonization plans on hub supply availability, creating a strong demand pull that governments are responding to with dedicated funding.

Storage Method Insights

Salt Cavern Storage dominates with 63.7% due to large-scale capacity and low operational cost.

In 2025, Salt Cavern Storage held a dominant market position in the By Storage Method segment of the Hydrogen Hubs Market, with a 63.7% share. Salt caverns provide the highest-volume, lowest-cost hydrogen storage available and are geologically proven through decades of natural gas storage operations.

Compressed Hydrogen Storage is the dominant option for hubs located away from salt cavern geology. It serves medium-term buffer storage needs and is widely used at refueling stations and industrial supply points. Its higher per-kilogram cost relative to cavern storage limits its role to operational balancing rather than strategic reserve functions.

Hub Development Stage Insights

Operational Hubs dominate with 67.2% due to mature infrastructure and proven offtake relationships.

In 2025, Operational Hubs held a dominant market position in the By Hub Development Stage segment of the Hydrogen Hubs Market, with a 67.2% share. These are facilities that have moved through permitting, construction, and commissioning and are now delivering hydrogen to customers. Their dominance reflects the legacy of industrial hydrogen production complexes — primarily grey hydrogen sites — that qualify as hubs by virtue of their co-located production, storage, and distribution assets.

Planned Hubs are the largest segment by project count but the least certain by volume. More than 90% of global electrolyzer developments remain in early-stage planning due to offtake uncertainty and capital cost risk, meaning the gap between planned ambition and bankable projects remains wide. The hubs that can demonstrate contracted offtake volumes will move from planned to under construction first — and will define the market’s actual growth trajectory.

Funding Model Insights

Publicly Funded Hubs dominate with 58.3% due to government de-risking programs that attract early-stage capital.

In 2025, Publicly Funded Hubs held a dominant market position in the By Funding Model segment of the Hydrogen Hubs Market, with a 58.3% share. Public funding is the primary enabler of hub development at this stage because private capital alone cannot absorb the technology, offtake, and policy risks that characterize first-mover projects.

The U.S. hydrogen hub strategy operates under a broader US$7 Billion federal grants framework, and European programs have committed comparable sums through IPCEI and Hydrogen Bank mechanisms. This public funding dominance is a feature of the current market cycle, not a permanent structure — as projects prove out and offtake markets deepen, privately funded hubs will gain share.

Public-Private Partnership Hubs represent the next stage in funding model maturity. They combine public grants or loan guarantees with equity and debt from private investors, distributing risk across both sectors. The HyVelocity Gulf Coast Hydrogen Hub exemplifies this model, with six major industrial partners — AES, Air Liquide, Chevron, ExxonMobil, Mitsubishi Heavy Industries, and Ørsted — alongside federal funding of up to US$1.2 Billion.

Market Segments Covered in the Report

By Source

- Green Hydrogen

- Blue Hydrogen

- Grey Hydrogen

By Technology

- Electrolysis-Based

- Alkaline Electrolysis

- PEM Electrolysis

- Solid Oxide Electrolysis

- Steam Methane Reforming (SMR)

- Partial Oxidation (POX)

- Auto Thermal Reforming

- Coal Gasification

By Application

- Industrial Applications

- Power Generation

- Transportation

- Petroleum Refinery

- Hydrogen Fuel Cell

- Methanol Production

- Export Terminals

By Distribution Channel

- Cylinder

- Pipeline

- Tube Trailer

By Infrastructure Component

- Electrolyzers

- Pipelines & Transport Networks

- Refueling Infrastructure

By Offtake Sector

- Ammonia Production

- Steel Manufacturing

- Cement Industry

- Aviation Fuel Production

By Storage Method

- Salt Cavern Storage

- Compressed Hydrogen Storage

- Liquid Hydrogen Storage

By Hub Development Stage

- Operational Hubs

- Under Construction Hubs

- Planned Hubs

By Funding Model

- Publicly Funded Hubs

- Public-Private Partnership Hubs

- Privately Funded Hubs

Regional Insights

Asia-Pacific Dominates the Hydrogen Hubs Market with a Market Share of 58.9%, Valued at USD 2.80 Billion

Asia-Pacific holds 58.9% of the global Hydrogen Hubs Market, valued at USD 2.80 Billion in 2025. This dominance reflects the region’s large existing industrial hydrogen demand — primarily from refining, ammonia, and steel — combined with government-led clean energy transition programs in China, Japan, South Korea, and India. Asian hub development is largely driven by energy security goals rather than purely climate targets, giving these projects strong political backing that accelerates funding and permitting.

North America Market Trends

North America is the most active hub funding market globally, with the U.S. government committing up to US$2.2 Billion for Gulf Coast and Midwest hubs in November 2024 as part of a broader US$7 Billion federal hub grants program. This level of committed federal capital creates a durable pipeline of large-scale projects that private investors can co-invest in with lower risk. The U.S. strategy targets 50 million metric tons of clean hydrogen production annually by 2050, establishing clear long-term demand signals for hub developers and equipment suppliers.

Europe Market Trends

Europe’s hub market is advancing through two parallel mechanisms: the Hydrogen Bank auction — which attracted 132 bids from 17 countries in 2024 — and the IPCEI framework, which combined €4.7 Billion in public and private capital across 13 projects. The H2MED Trans-European Hydrogen Corridor, backed by Spain’s €3.2 Billion infrastructure commitment through 2030, will link Iberian green hydrogen production with industrial demand centers in France and Germany.

Latin America Market Trends

Latin America’s hub market is at an early stage but holds structural advantages. Chile and Brazil have large renewable energy resources and deep-water port access suited to green hydrogen export. National strategies in both countries target ammonia and liquid hydrogen export as primary hub use cases.

Middle East & Africa Market Trends

The Middle East is positioning itself as a low-cost green hydrogen export zone, with projects in Saudi Arabia, the UAE, and Oman targeting European and Asian import markets. Existing petrochemical and ammonia infrastructure provides a partial conversion pathway for blue hydrogen production.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The U.S. Department of Energy operates the Regional Clean Hydrogen Hubs program under the Infrastructure Investment and Jobs Act, which established a US$7 Billion grants framework for hub development. Phase 1 funding tranches released in November 2024 for the Gulf Coast and Midwest hubs formalized federal cost-share obligations, creating binding project development milestones that hub operators must meet to access subsequent funding. This structure ties regulatory compliance directly to capital access, making milestone adherence a commercial necessity.

India’s National Green Hydrogen Mission, supported by government budget allocations from 2024 onward, establishes a framework for certifying green hydrogen production and mandating green hydrogen use in specific industrial sectors. The Mission’s hub provisions target at least two renewable hydrogen hubs, with INR 2 Billion (approximately USD 24 Million) allocated in 2024 for their establishment. Compliance with Mission standards will be required to access production incentives under the scheme.

The European IPCEI hydrogen framework, approved by the European Commission in 2024, governs the €1.4 Billion public funding package across 13 hydrogen projects in seven member states. IPCEI approval requires projects to demonstrate cross-border spillover effects, technology innovation, and additionality relative to market-only outcomes. These criteria effectively require hub projects to demonstrate system-level integration — linking multiple countries, sectors, and technologies — rather than standalone production assets.

Drivers

Large Federal Capital Commitments Accelerate Hub Construction Timelines in the U.S. and Europe

The U.S. Department of Energy committed up to US$2.2 Billion in November 2024 across two new Regional Clean Hydrogen Hubs. This is not a pledge — it is a binding cost-share structure with milestone-linked disbursements. For hub developers, federal cost-share changes the project financing stack by providing senior capital that private lenders can sit behind, reducing the interest rate and equity returns required to make projects bankable.

The European IPCEI framework approved €1.4 Billion in public funding across 13 projects and unlocked an additional €3.3 Billion in private investment. The leverage ratio demonstrates that public capital in the hydrogen hub market is not substituting for private capital — it is activating it. This distinction matters for policymakers assessing the return on public funds and for investors tracking where co-investment opportunities are concentrated.

Moreover, the European Hydrogen Bank’s pilot auction attracted 132 bids representing 8.5 GW of planned electrolyzer capacity, far exceeding the €800 Million available budget. The oversubscription confirms that the binding constraint on hub deployment is not developer appetite — it is the pace at which public support mechanisms can disburse capital. Governments that move faster through auction cycles will shape which regions capture hub manufacturing and employment benefits.

Restraints

Offtake Uncertainty and Cost Risk Stall Final Investment Decisions Across Global Hub Pipelines

More than 90% of electrolyzer developments globally remain in early-stage planning due to unresolved offtake agreements and uncertain production costs. This figure reveals a structural gap between project announcements and bankable commitments. Hub developers can design projects and secure land, but without contracted buyers at economics that justify construction costs, lenders will not provide project finance and equity investors will not commit capital.

Electric Hydrogen received a US$46.3 Million U.S. DOE manufacturing grant in March 2024 to scale gigawatt-level electrolyzer production. This investment targets the core supply-chain bottleneck that has historically caused hub project delays — equipment lead times. A domestic manufacturing base allows hub developers to contract equipment earlier in the project cycle with greater delivery certainty than import-dependent supply chains provide.

Electric Hydrogen’s cost target of US$1 per kilogram of hydrogen production by 2031 illustrates the trajectory that domestic manufacturing investment is designed to enable. Reaching that cost threshold would make green hydrogen competitive with natural gas in many industrial applications without subsidy — fundamentally changing the offtake negotiation dynamic for hub developers and reducing their dependence on public revenue support mechanisms.

Growth Factors

Revenue Support Mechanisms and Cross-Border Corridors Create Durable Hub Investment Cases

The €1.2 Billion European Hydrogen Bank IF24 auction creates a revenue support structure for hub developers that removes the largest single obstacle to project finance — price uncertainty over a 10-year operating period. Fixed-premium contracts under the auction mechanism allow hub operators to model revenue with enough certainty to satisfy lenders and equity investors. This is the same structural logic that made offshore wind bankable, and it is now being applied to hydrogen at hub scale.

Spain’s approval of €3.2 Billion in hydrogen infrastructure investment through 2030, supporting the H2MED Trans-European Hydrogen Corridor, creates a physical offtake pathway for Iberian green hydrogen production. Cross-border corridors matter because they allow hub production to reach buyers outside the immediate geographic market, enlarging the addressable demand pool and reducing dependence on any single industrial cluster. This geographic reach is what allows large hub projects to achieve the utilization rates needed for long-term viability.

Emerging Trends

Competitive Auction Mechanisms and Multi-Sector Valley Models Define the Next Phase of Hub Development

Europe’s shift from an €800 Million pilot auction to a €1.2 Billion IF24 program signals a maturation of public support design — from exploratory grant funding to competitive, price-discovery mechanisms. Auction models select the most cost-competitive projects, ensuring public money achieves maximum production per euro. This transition will accelerate as more countries adopt auction-based hydrogen support, creating a global competitive environment for hub capital.

The integration of hydrogen hubs with maritime decarbonization strategies is creating a new class of hub use case — dedicated renewable hydrogen production for shipping fuels, supported by dedicated funding streams. Shipping companies facing IMO decarbonization mandates are signing long-term supply agreements with hub developers, providing the offtake certainty that industrial buyers in other sectors have been slower to commit. This maritime demand pull is pulling forward investment in port-adjacent hub sites.

Moreover, the multi-sector Hydrogen Valley model — linking production, storage, transport, and multiple industrial end-uses within a single regional cluster — is becoming the structural template for new hub development. Italy’s Puglia Green Hydrogen Valley and similar programs across Europe demonstrate that hubs achieve better economics and more durable offtake when they serve several sectors simultaneously rather than a single industrial buyer. This model also builds political support across a broader industrial constituency, which improves permitting and policy durability.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global hydrogen hubs market as every integrated ecosystem of co-located hydrogen production, storage, transmission, and end-use facilities that collectively operate as a centralized clean energy network. Covered categories include green and blue hydrogen production clusters, shared electrolysis and carbon capture infrastructure, centralized hydrogen storage and compression facilities, intra-hub pipeline and logistics networks, hydrogen distribution terminals, and offtake agreements with industrial, mobility, and power generation end-users.

According to our research framework, all market values are expressed in constant 2025 US dollars to eliminate currency-driven distortions and ensure consistent cross-regional and cross-project comparability.

We exclude standalone single-site hydrogen production facilities that operate without hub-level integration, isolated hydrogen refueling stations not connected to a broader hub network, downstream hydrogen-consuming industries such as steel manufacturing or chemical processing where the hub itself is not the primary subject of analysis, pre-feasibility stage concepts without committed funding or regulatory approval, and software-only hydrogen hub management platforms not tied to physical infrastructure development.

Key Companies Insights

Linde plc operates as a foundational infrastructure player across global hydrogen hubs, supplying industrial gases and managing hydrogen production and distribution assets within multiple hub zones. Linde’s existing pipeline networks and liquid hydrogen terminals position it to serve as the logistics backbone for emerging hub clusters, rather than just a commodity supplier.

Air Liquide brings both production technology and end-user relationships to hydrogen hub development, having already invested in large-scale electrolysis projects across Europe and North America. Its participation as an industrial partner in the HyVelocity Gulf Coast Hydrogen Hub alongside AES, Chevron, ExxonMobil, Mitsubishi Heavy Industries, and Ørsted places it at the center of one of the largest hub programs globally.

Air Products and Chemicals, Inc. has built its hub strategy around large-scale green and blue hydrogen production projects linked to export terminals. Its business model targets international hydrogen trade rather than purely domestic industrial supply, giving it exposure to the emerging ammonia and liquid hydrogen export market that other industrial gas companies have been slower to pursue.

Shell plc approaches hydrogen hubs as an extension of its downstream energy value chain, integrating hydrogen production within existing refinery and industrial sites to manage transition costs. Shell’s strategic positioning focuses on retaining its industrial buyer relationships while shifting the underlying energy input from fossil-derived hydrogen to green or blue alternatives.

Key Companies

- Linde plc

- Air Liquide

- Air Products and Chemicals, Inc.

- Shell plc

- BP plc

- Engie SA

- Siemens Energy

- Nel ASA

- Plug Power Inc.

- ITM Power plc

- Ballard Power Systems Inc.

- Hyundai Motor Company

- McPhy Energy

- Mitsubishi Power

- Toyota Motor Corporation

Recent Industry Developments

- In January 2025, the U.S. DOE awarded the Heartland Hydrogen Hub an initial $20 Million tranche from a total federal cost-share commitment of up to $925 Million, advancing hub development activities and unlocking the next phase of project planning.

- In July 2024, the U.S. DOE awarded the California Hydrogen Hub (ARCHES) an initial $30 Million tranche toward a total federal commitment of up to $1.2 Billion to begin Phase 1 development activities across the state’s renewable hydrogen network.

- In 2024, the Government of India allocated INR 2 Billion (approximately USD 24 Million) to establish at least two renewable hydrogen hubs under the National Green Hydrogen Mission framework, targeting domestic production and industrial supply.

- In July 2024, California officially launched the ARCHES Hydrogen Hub with a planned network of renewable hydrogen production, transport, and end-use projects aimed at reducing emissions by approximately 2 million metric tons annually across the state’s industrial and transport sectors.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.76 Billion |

| Forecast Revenue (2035) | USD 31.16 Billion |

| CAGR (2026-2035) | 20.67% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Green Hydrogen, Blue Hydrogen, Grey Hydrogen), By Technology (Electrolysis-Based, SMR, POX, Auto Thermal Reforming, Coal Gasification, Alkaline Electrolysis, PEM Electrolysis, Solid Oxide Electrolysis), By Application (Industrial Applications, Power Generation, Transportation, Petroleum Refinery, Hydrogen Fuel Cell, Methanol Production, Export Terminals), By Distribution Channel (Cylinder, Pipeline, Tube Trailer), By Infrastructure Component (Electrolyzers, Pipelines & Transport Networks, Refueling Infrastructure), By Offtake Sector (Ammonia Production, Steel Manufacturing, Cement Industry, Aviation Fuel Production), By Storage Method (Salt Cavern Storage, Compressed Hydrogen Storage, Liquid Hydrogen Storage), By Hub Development Stage (Operational Hubs, Under Construction Hubs, Planned Hubs), By Funding Model (Publicly Funded Hubs, Public-Private Partnership Hubs, Privately Funded Hubs) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Linde plc, Air Liquide, Air Products and Chemicals Inc., Shell plc, BP plc, Engie SA, Siemens Energy, Nel ASA, Plug Power Inc., ITM Power plc, Ballard Power Systems Inc., Hyundai Motor Company, McPhy Energy, Mitsubishi Power, Toyota Motor Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |