What is the Carbon Dioxide Removal Market Size?

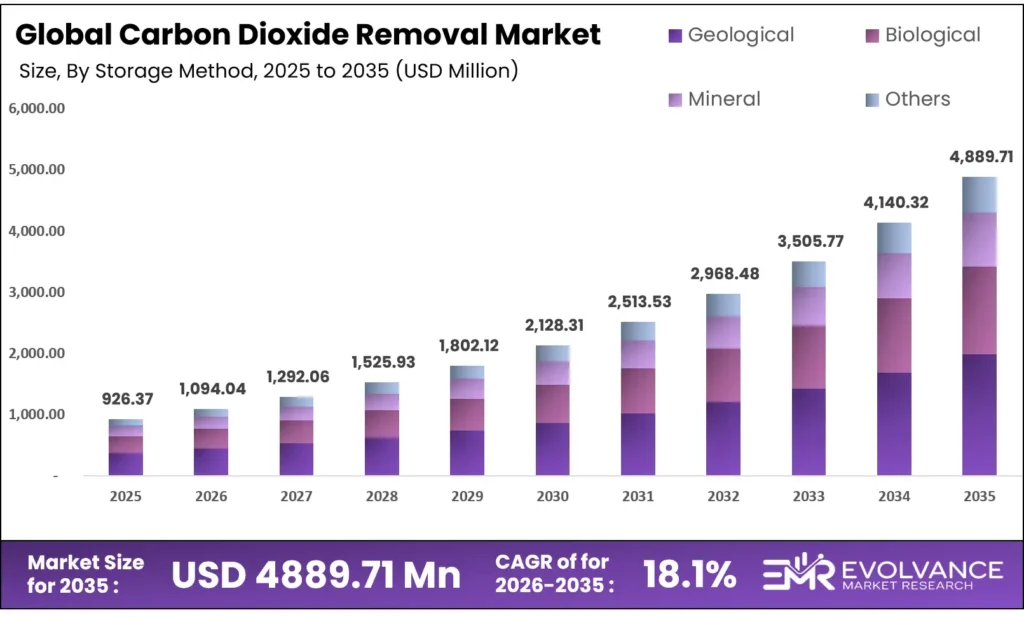

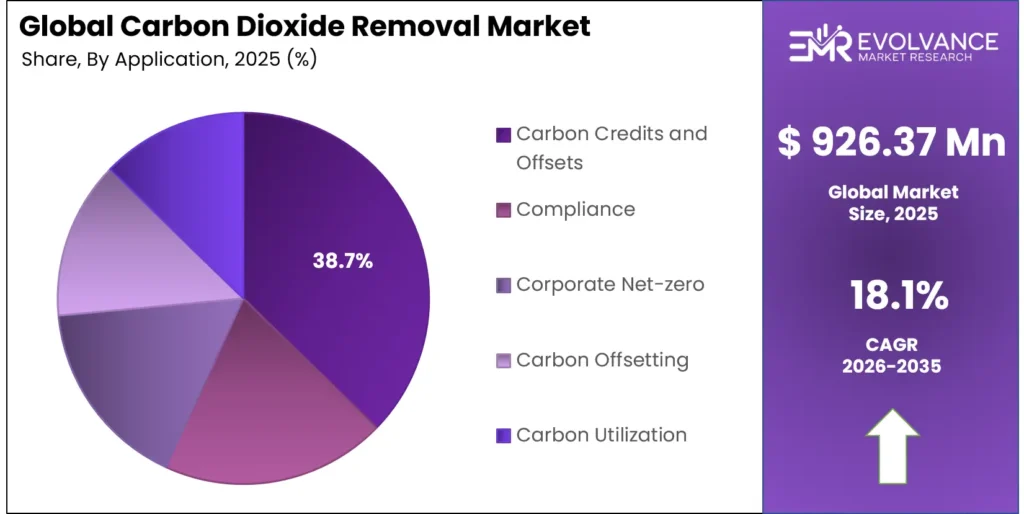

The Global Carbon Dioxide Removal Market size will be worth around USD 4889.71 Million by 2035 from USD 926.37 Million in 2025, growing at a CAGR of 18.1% during the forecast period 2026 to 2035. This pace reflects Fortune 500 buyers signing multi-year offtake contracts, pulling capital into engineered removal at an accelerating rate. Corporate net-zero timelines are compressing procurement cycles, shifting buyer behavior from spot purchases toward long-dated forward contracts. On the supply side, high per-tonne costs for Direct Air Capture and thin CO₂ transport infrastructure remain the most concrete bottlenecks to bankable project pipelines.

Market Highlights

- The Carbon Dioxide Removal Market will grow from USD 926.37 Million in 2025 to USD 4889.71 Million by 2035, at a CAGR of 18.1%.

- North America leads all regions with a 39.4% market share, valued at USD 364.98 Million in 2025.

- By Technology Type, Direct Air Capture holds the dominant position with a 34.2% share.

- By Application, Carbon Credits and Offsets commands the largest share at 38.7%.

- By Storage Method, Geological storage leads with a 41.3% share.

- By End-Use Industry, Energy and Power Generation holds the top position at 46.3%.

Market Overview

Carbon dioxide removal (CDR) covers a set of methods that extract CO₂ directly from the atmosphere and store it in durable geological, biological, or mineral sinks. The market spans engineered approaches such as Direct Air Capture and Bioenergy with Carbon Capture and Storage alongside nature-based methods including afforestation, soil carbon, and enhanced weathering. Each method differs in cost, permanence, and the infrastructure needed to scale.

CDR’s commercial relevance has shifted from niche climate science into a procurement category with real contract volume. Technology firms, financial institutions, and energy producers now treat carbon removal credits as a compliance and reputational asset. This demand is no longer aspirational it is backed by signed offtake deals, with delivery windows stretching to 2039 and beyond.

Government policy is reinforcing private demand. The U.S. IRA’s 45Q tax credit and the DOE’s Carbon Negative Shot program directly reduce the financial risk of first-of-kind projects. The EU’s Carbon Removal and Carbon Farming Regulation (CRCF) is building a formal certification architecture that positions European CDR projects for compliance market integration. These are structural demand signals, not temporary subsidies.

According to the United Nations Environment Programme’s 2025 Emissions Gap Report, global annual emissions must fall by 35% relative to 2019 levels by 2035 to stay on a 2°C pathway. This gap cannot close through efficiency measures alone residual emissions from hard-to-abate sectors require CDR at scale. That constraint creates a structural floor beneath demand that cannot be negotiated away.

As reported by the U.S. Department of Energy in its January 2025 Multi-Year Program Plan, CDR must reach gigaton-scale annual removal to support climate pathways. The DOE sets a minimum reporting threshold of more than 1 ktCO₂e per year for pilot projects used in cost benchmarking. That threshold signals where the agency is focusing on projects with real removal scale, not demonstration-only activity.

Technology Type Insights

Direct Air Capture (DAC) dominates with 34.2% due to engineered permanence and policy-backed cost reduction pathways.

In 2025, Direct Air Capture (DAC) held a dominant market position in the By Technology Type segment of the Carbon Dioxide Removal Market, with a 34.2% share. DAC’s lead reflects its verifiable permanence geological storage timescales exceeding thousands of years satisfy buyer requirements that nature-based methods cannot reliably meet.

According to IATA, solid sorbent DAC has reached Technology Readiness Level (TRL) 9, meaning the technology is commercially deployable today. Climeworks reported facilitating more than 450,000 tonnes of certified removals in 2025, accounting for over 40% of all platform-based durable-removal transactions confirming DAC’s structural lead in high-integrity credit supply.

Bioenergy with Carbon Capture and Storage (BECCS) combines biomass combustion with geological CO₂ storage, producing energy while generating negative emissions. This dual-output model makes BECCS attractive for energy utilities seeking to monetize both electricity output and carbon credits. The Stockholm Exergi BECCS project has emerged as a replicable template for blended public-private finance, offering CDR developers in emerging markets a proven project structure to adapt.

Ocean-based CDR methods including alkalinity enhancement and direct ocean removal are at early commercial stages. Their scaling potential is large given ocean surface area, but regulatory pathways, ecological monitoring requirements, and liability frameworks are still under development. Buyers treat ocean-based credits as experimental positions rather than core portfolio holdings at this stage.

Carbon Mineralization permanently binds CO₂ into solid carbonate rock, offering near-irreversible storage. The approach is technically validated Carbfix in Iceland operates a commercial-scale mineralization system but application is constrained to geologies with appropriate basaltic formations. That geographic limitation caps its near-term addressable market.

Application Insights

Carbon Credits and Offsets dominates with 38.7% due to forward contract demand from large corporate buyers.

In 2025, Carbon Credits and Offsets held a dominant market position in the By Application segment of the Carbon Dioxide Removal Market, with a 38.7% share. Large technology firms are signing multi-year offtake contracts that lock in removal delivery years in advance. Climeworks announced in September 2025 that Schneider Electric agreed to remove 31,000 tonnes of CO₂ through a contract running until 2039. These long-dated agreements reflect buyers’ need to secure supply before high-integrity credit availability tightens further.

Compliance applications are gaining share as regulatory frameworks formalize CDR’s role in national emission accounting. The EU CRCF and Article 6 of the Paris Agreement are creating enforceable pathways for CDR credits to count toward sovereign and corporate compliance obligations. This regulatory legitimacy is the primary reason compliance demand is accelerating beyond voluntary market activity.

Corporate Net-zero commitments from Fortune 500 buyers are generating multi-billion-dollar long-term CDR offtake contracts. Technology and financial sector companies face reputational and regulatory pressure to move beyond emissions avoidance toward actual removal. This shift is pulling purchase decisions earlier in the corporate planning cycle, compressing timelines between commitment and contract signing.

Carbon Offsetting serves buyers seeking cost-effective short-term neutralization of residual emissions. As durability requirements tighten in voluntary markets, offsetting is losing ground to removal in high-value contract positions. Buyers who relied on forestry-based offsets are now being pressured by stakeholders and standards bodies to add at least a portion of durable engineered removal to their portfolios.

Carbon Utilization converts captured CO₂ into materials such as concrete, fuels, and chemicals. Companies like CarbonCure Technologies embed CO₂ into concrete production, turning waste carbon into a material strength additive. Utilization provides near-term revenue to CDR projects while storage markets mature, though permanence varies by end use concrete storage is durable, while fuel combustion re-releases CO₂ quickly.

Storage Method Insights

Geological dominates with 41.3% due to verified permanence and alignment with compliance-grade durability standards.

In 2025, Geological storage held a dominant market position in the By Storage Method segment of the Carbon Dioxide Removal Market, with a 41.3% share. Injecting CO₂ into deep saline aquifers or depleted hydrocarbon reservoirs produces storage that is effectively permanent on human timescales. This permanence profile directly matches the durability requirements now embedded in institutional buyer contracts and emerging compliance frameworks.

Biological storage methods including forests, wetlands, and soil offer lower costs and co-benefits such as biodiversity and watershed protection. However, reversal risk from fire, drought, and land-use change creates credit integrity concerns for buyers who need guaranteed delivery. Biological storage retains relevance as a high-volume, lower-price tier within CDR portfolios, particularly for corporate buyers seeking balance between cost and permanence.

Mineral storage permanently converts CO₂ into carbonate rock through reactions with silicate minerals. Carbfix has demonstrated this at scale in Iceland, achieving full mineralization within two years of injection. However, suitable geology is geographically constrained, and the process is energy-intensive, which limits replication to specific locations with both the right rock formation and access to low-carbon energy.

End-Use Industry Insights

Energy and Power Generation dominates with 46.3% due to compliance exposure and BECCS integration opportunities.

In 2025, Energy and Power Generation held a dominant market position in the By End-Use Industry segment of the Carbon Dioxide Removal Market, with a 46.3% share. Power producers face the most direct regulatory exposure to carbon pricing in the EU, ETS-regulated power and industrial facilities have already cut emissions by approximately 47% below 2005 levels, according to European Commission data. The remaining reductions require CDR for residual emissions that efficiency measures cannot eliminate. BECCS is particularly attractive for this sector because it generates both electricity and carbon removal credits from a single asset.

Enhanced Oil Recovery (EOR) uses injected CO₂ to increase hydrocarbon extraction from mature reservoirs, while storing carbon underground. EOR represents a hybrid use case it generates revenue from oil production while achieving geological CO₂ storage. The net removal benefit depends on whether the CO₂ injected exceeds the CO₂ released from the incremental oil produced, a calculation that varies by field and buyer accountability standards.

Market Segments Covered in the Report

By Technology Type

- Direct Air Capture (DAC)

- Bioenergy with Carbon Capture and Storage (BECCS)

- Afforestation & Reforestation

- Soil Carbon Sequestration

- Ocean-based CDR

- Enhanced Weathering

- Carbon Mineralization

- Biochar

By Application

- Carbon Credits and Offsets

- Compliance

- Corporate Net-zero

- Carbon Offsetting

- Carbon Utilization

- Permanent Storage

- Industrial

- Energy Production

- Agricultural

By Storage Method

- Geological

- Biological

- Mineral

- Other

By End-Use Industry

- Energy and Power Generation

- Agriculture

- Construction Materials

- Manufacturing & Heavy Industry

- Enhanced Oil Recovery (EOR)

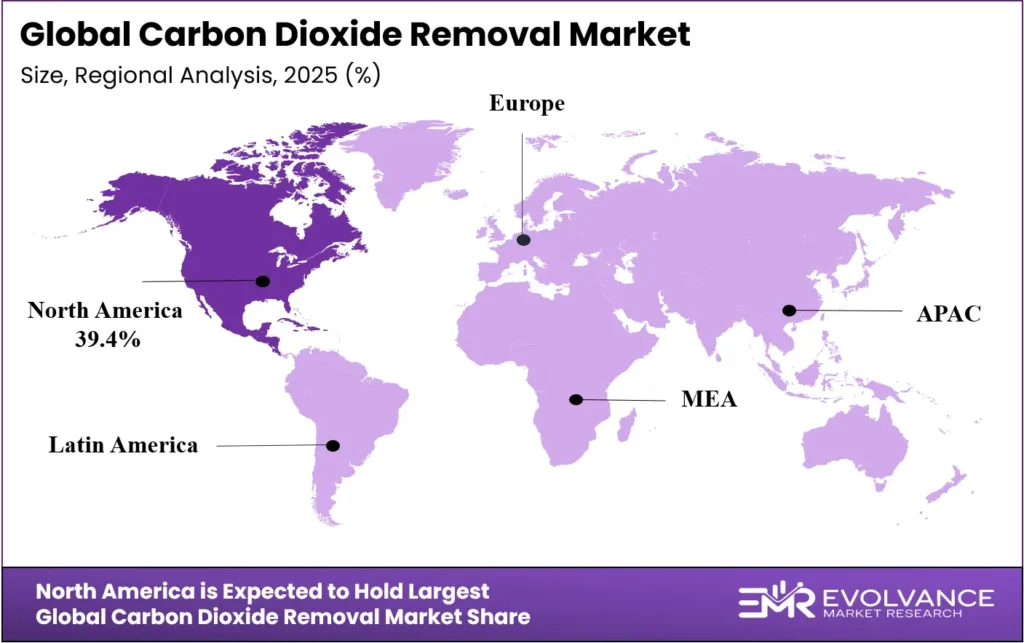

Regional Insights

North America Dominates the Carbon Dioxide Removal Market with a Market Share of 39.4%, Valued at USD 364.98 Million

North America leads with a 39.4% share valued at USD 364.98 Million in 2025. The IRA’s 45Q tax credit and the DOE’s Carbon Negative Shot program have structurally de-risked first-of-kind DAC and BECCS projects by reducing the cost gap between current prices and bankable economics. The U.S. procurement infrastructure with standardized offtake contracting, deep capital markets, and established MRV practices allows projects to reach financial close faster than in any other region. Canada is also emerging as a hub, as evidenced by the Deep Sky Alpha carbon removal facility becoming operational in August 2025.

Europe Market Trends

Europe is building the world’s most formal CDR compliance architecture. The EU’s CRCF (Regulation EU 2024/3012) entered into force in 2025 and adopted its first permanent carbon removal certification methodologies in February 2026. The EU ETS already covers approximately 45% of EU greenhouse gas emissions and has cut regulated sector emissions by roughly 47% below 2005 levels. The remaining residual emissions create a structural CDR demand that the CRCF is designed to channel. This regulatory clarity is positioning Europe to challenge North America for CDR market leadership over the next five years.

Asia Pacific Market Trends

Asia Pacific is entering CDR through national policy frameworks rather than corporate procurement. India launched its national R&D roadmap for carbon capture and storage on 4 December 2025, signaling government commitment to building domestic CDR capacity. China’s compliance carbon market is expanding sector coverage and tightening caps. Japan and South Korea are incorporating CDR into their national carbon neutrality strategies. These are early-stage signals Asia Pacific’s CDR market volume remains below North America and Europe, but its long-term potential is the largest given the region’s emission base.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The EU’s Carbon Removal and Carbon Farming Regulation formally Regulation (EU) 2024/3012 entered into force during 2025 as the world’s first statutory CDR certification framework. It establishes rules for permanence, additionality, and monitoring across both engineered and nature-based removal activities. The regulation gives CDR operators a defined path to certification that compliance buyers and carbon market platforms can recognize.

The European Commission adopted the first permanent carbon removal certification methodologies in February 2026 under this framework. These methodologies define how CDR project operators calculate, monitor, and report net removal volumes for certification purposes. Their adoption removes a key ambiguity that had delayed project development across Europe by giving developers a clear technical standard to design against.

In the United States, the Inflation Reduction Act’s Section 45Q tax credit remains the primary CDR policy instrument, providing direct per-tonne payments for DAC and BECCS projects meeting verified removal thresholds. The DOE’s Carbon Negative Shot program, outlined in its January 2025 Multi-Year Program Plan, targets reductions in DAC costs toward USD 100 per tonne or below. These programs directly shape project economics by de-risking capital deployment into first-of-kind facilities.

Drivers

Corporate Net-Zero Commitments and IRA Policy Architecture Create Durable CDR Demand With Signed Contract Evidence

Fortune 500 technology and financial sector buyers are converting net-zero pledges into binding offtake contracts. In June 2025, SAP committed to purchasing 37,000 tonnes of carbon removal credits from Climeworks through a portfolio spanning DAC, biochar, and enhanced rock weathering, with deliveries extending through 2034. These multi-year contracts create predictable revenue streams that CDR project developers can use to secure project financing.

The IRA’s 45Q tax credit and the DOE Carbon Negative Shot program are systematically lowering the financial risk of first-of-kind DAC and BECCS projects. By attaching a per-tonne government payment to verified removals, these instruments reduce the effective cost gap between current market prices and the level needed for project bankability. This policy architecture is the single most important reason new CDR projects are reaching financial close in the U.S. at all.

The IPCC’s scenario consensus is also a structural driver. Residual emissions from hard-to-abate sectors steel, cement, aviation, shipping cannot reach net-zero through efficiency measures alone. According to UNEP’s 2025 Emissions Gap Report, global emissions must fall by 55% relative to 2019 levels by 2035 to align with a 1.5°C pathway. That requirement creates a floor beneath CDR demand that grows larger as efficiency measures exhaust their potential.

Restraints

High Engineered CDR Costs and Underdeveloped Storage Infrastructure Block Bankable Project Pipelines at Scale

Direct Air Capture faces a hard cost floor that limits its addressable buyer base. According to the International Energy Agency’s assessment cited by IATA, the levelized cost of DACCS ranges from USD 134 to USD 342 per tonne of CO₂ captured. At those levels, DAC credits are accessible only to large technology buyers with dedicated CDR budgets the mass of mid-market corporate buyers remains entirely priced out.

The energy intensity of DAC compounds the cost problem. IATA data shows that DAC systems processing atmospheric air which contains just 0.04% CO₂ by volume need approximately 2–4 times more energy than conventional flue-gas capture systems processing gas with 3–14% CO₂ concentration. This energy disadvantage means DAC cost reductions require both technology learning and access to low-cost renewable power simultaneously, a combination that is rare outside a few geographies.

Beyond cost, fragmented MRV standards across permanence, additionality, and leakage accounting are undermining institutional buyer confidence. When buyers cannot verify that a credit represents a genuine, permanent, additional removal, they reduce purchase volumes or add conservative buffers to their net-zero accounting. This uncertainty is not a future risk it is currently reducing the volume of contracts that CDR project developers can sign with confidence.

Growth Factors

Hard-to-Abate Sectors and Low-Cost CDR Pathways Open New Buyer Classes and Geographies

Maritime and aviation sectors are entering multi-year CDR offtake agreements as Scope 3 residual emission obligations tighten. These sectors cannot decarbonize through fuel switching alone within current technology timelines. Their entry into CDR procurement adds a new class of large, recurring buyers distinct from the technology sector that broadens the market’s demand base beyond its current concentration.

Agricultural enhanced rock weathering can scale through existing farming supply chains at costs well below engineered alternatives. Tropical and subtropical markets Brazil, India, and Sub-Saharan Africa offer the fastest weathering reaction rates due to high rainfall, which accelerates the CO₂ mineralization process. Deploying CDR through supply chains that already reach millions of farming operations reduces infrastructure investment requirements and lowers per-tonne costs below those of any engineered approach.

Blended public-private finance structures modeled on the Stockholm Exergi BECCS project are creating a replicable template for CDR developers in emerging markets. GE Vernova’s DAC system deployed at Deep Sky Alpha in Canada, which became operational in August 2025, has a designed capture capacity of up to 1,500 tonnes of CO₂ per year. This cross-technology hub demonstrates that multi-method CDR facilities can reach commercial operation, reducing investor uncertainty about project execution risk.

Emerging Trends

Forward Contracting, Big Tech Buyer Concentration, and Voluntary-Compliance Market Convergence Reshape CDR Procurement Structure

Forward offtake contracting is displacing spot market transactions as the dominant CDR procurement model across 2026–2030 vintage windows. Buyers who wait for spot availability face both supply scarcity and pricing disadvantages as high-integrity credit supply is locked into long-dated contracts by early movers. This shift rewards first-mover buyers and creates a structural disadvantage for procurement teams that have not yet established CDR supplier relationships.

Big tech buyer concentration is already compressing available supply. Microsoft’s 2025 portfolio of 45 million tonnes of CDR commitments represents a buyer position so large that it tightens supply available to all other buyers. This concentration effect means that mid-market corporate buyers face a market where high-integrity credits are structurally scarce not because of technical limitations, but because a small number of large buyers have secured most of the near-term supply.

Voluntary and compliance carbon markets are converging on durability and permanence as non-negotiable credit quality thresholds. India’s national CCUS roadmap, launched in December 2025, signals that even emerging economies are embedding permanence requirements into their CDR policy frameworks. For CDR developers and credit standards bodies, this convergence simplifies the quality benchmark but raises the bar for nature-based methods that struggle to demonstrate multi-century storage assurance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

This report covers the global Carbon Dioxide Removal (CDR) market, defined as all commercial and pre-commercial methods that extract CO₂ directly from the atmosphere or ocean and store it in geological, biological, or mineral sinks. Covered categories include Direct Air Capture (DAC), Bioenergy with Carbon Capture and Storage (BECCS), afforestation and reforestation, soil carbon sequestration, ocean-based CDR, enhanced weathering, carbon mineralization, and biochar. Market values are expressed in constant U.S. dollars to eliminate currency fluctuation effects on year-on-year comparisons. The base year is 2025, with historical data from 2020 to 2024 and forecasts extending through 2035.

This report excludes emissions avoidance and reduction credits that do not involve active CO₂ removal from the atmosphere. It does not cover carbon capture from industrial point sources that lacks a CDR component such as standalone flue-gas capture without permanent storage nor unrelated climate services such as energy efficiency consulting or renewable energy certificates. Software-only carbon accounting platforms without a physical removal component are also excluded from scope.

Key Companies Insights

Climeworks holds the most advanced commercial DAC position of any operator globally. The company secured an additional USD 162 million in equity financing in 2025, bringing cumulative funding above USD 1 billion capital that funds both technology scale-up and cost reduction. Climeworks opened its DAC Innovation Center in December 2025, consolidating more than 50 engineers, chemists, and technology specialists. This concentration of technical talent signals a deliberate strategy to compress the cost curve faster than competitors, widening the gap between Climeworks and earlier-stage DAC developers.

Heirloom uses a mineral-based DAC approach that relies on limestone’s natural CO₂ absorption cycle, accelerated through controlled heating and spreading. This method operates at lower energy inputs than sorbent-based DAC, which directly addresses the energy cost problem constraining most engineered removal approaches. Heirloom’s technology position makes it a meaningful alternative to liquid- and solid-sorbent DAC for buyers seeking verifiable permanence without the full energy cost burden of conventional DAC systems.

Global Thermostat deploys solid sorbent DAC using low-grade industrial waste heat to drive the CO₂ desorption cycle, significantly reducing electricity requirements relative to systems that rely entirely on grid power. This energy sourcing strategy lowers operating costs per tonne and opens deployment options at industrial sites where waste heat is available a structural cost advantage that sorbent-only competitors cannot replicate without co-location with industrial heat sources.

Charm Industrial converts waste biomass into bio-oil through fast pyrolysis and injects it into deep geological wells, achieving permanent carbon storage at costs below those of most DAC systems. This approach bridges biological and geological storage in a single process flow, sidestepping the need for pipeline-quality CO₂ compression and transport infrastructure. Charm’s bio-oil injection model appeals to corporate buyers seeking durable removal at price points closer to biochar than DAC, making it a competitive option in the mid-market segment.

Key Companies

- Climeworks

- Heirloom

- Global Thermostat

- Charm Industrial

- CarbonCapture Inc.

- Carbyon

- Mission Zero Technologies

- AirCapture

- Avnos

- LanzaTech

- Twelve

- CarbonCure Technologies

- Blue Planet Systems

- CarbiCrete

- CarbonFree

- Carbfix

- Neustark

- Cella Mineral Storage

- Ebb Carbon

- 1PointFive Inc.

- Arca Climate

- Carbofex Oy

- Lithos Carbon Inc.

- Novocarbo GmbH

- Noya Inc.

- Planetary Technologies, Inc.

- Prometheus Fuels

- Skytree

- Verdox, Inc.

- Wakefield BioChar

Recent Industry Developments

- In August 2025, Deep Sky Alpha became operational in Canada as the world’s first cross-technology carbon removal hub, hosting multiple CDR methods at a single facility and demonstrating that multi-method removal operations can reach commercial scale.

- In September 2025, GE Vernova announced its DAC system selected for Deep Sky Alpha would have a designed capture capacity of up to 1,500 tonnes of CO₂ per year, with full operations planned for late 2026.

- In September 2025, Climeworks and Schneider Electric signed a long-term carbon removal agreement covering 31,000 tonnes of CO₂, with delivery commitments running until 2039, extending forward-contract visibility further than most prior industry agreements.

- In June 2025, SAP committed to purchasing 37,000 tonnes of CDR credits from Climeworks through a portfolio of DAC, biochar, and enhanced rock weathering, with deliveries scheduled through 2034.

- In 2025, Climeworks secured an additional USD 162 million in equity financing, bringing the company’s total cumulative funding to more than USD 1 billion the first DAC developer to cross this capital threshold.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 926.37 Million |

| Forecast Revenue (2035) | USD 4889.71 Million |

| CAGR (2026-2035) | 18.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology Type (Direct Air Capture, BECCS, Afforestation & Reforestation, Soil Carbon Sequestration, Ocean-based CDR, Enhanced Weathering, Carbon Mineralization, Biochar), By Application (Carbon Credits and Offsets, Carbon Utilization, Permanent Storage), By Storage Method (Geological, Biological, Mineral, Other), By End-Use Industry (Energy and Power Generation, Agriculture, Construction Materials, Manufacturing & Heavy Industry, Enhanced Oil Recovery) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Climeworks, Heirloom, Global Thermostat, Charm Industrial, CarbonCapture Inc., Carbyon, Mission Zero Technologies, AirCapture, Avnos, LanzaTech, Twelve, CarbonCure Technologies, Blue Planet Systems, CarbiCrete, CarbonFree, Carbfix, Neustark, Cella Mineral Storage, Ebb Carbon, 1PointFive Inc., Arca Climate, Carbofex Oy, Lithos Carbon Inc., Novocarbo GmbH, Noya Inc., Planetary Technologies Inc., Prometheus Fuels, Skytree, Verdox Inc., Wakefield BioChar |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |