What is the Neodymium (Nd-Fe-B) Magnet Market Size?

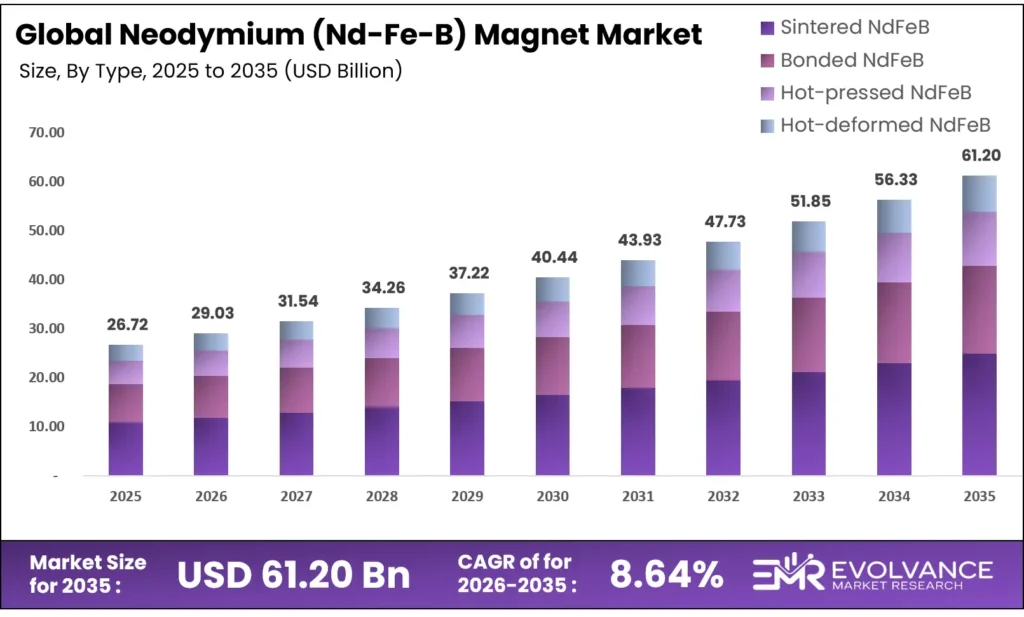

The Global Neodymium (Nd-Fe-B) Magnet Market size will be worth around USD 61.20 Billion by 2035 from USD 26.72 Billion in 2025, growing at a CAGR of 8.64% during the forecast period 2026 to 2035. Electric vehicle motor production and offshore wind installations are pulling sintered magnet volumes faster than non-Chinese suppliers can scale. Buyers are shifting from spot procurement to long-term supply contracts as geopolitical pressure on rare earth access rises. China’s control of heavy rare earth refining remains the single largest supply-side risk limiting output expansion outside Asia.

Market Highlights

- The Global Nd-Fe-B Magnet Market will grow from USD 26.72 Billion in 2025 to USD 61.20 Billion by 2035, at a CAGR of 8.64%.

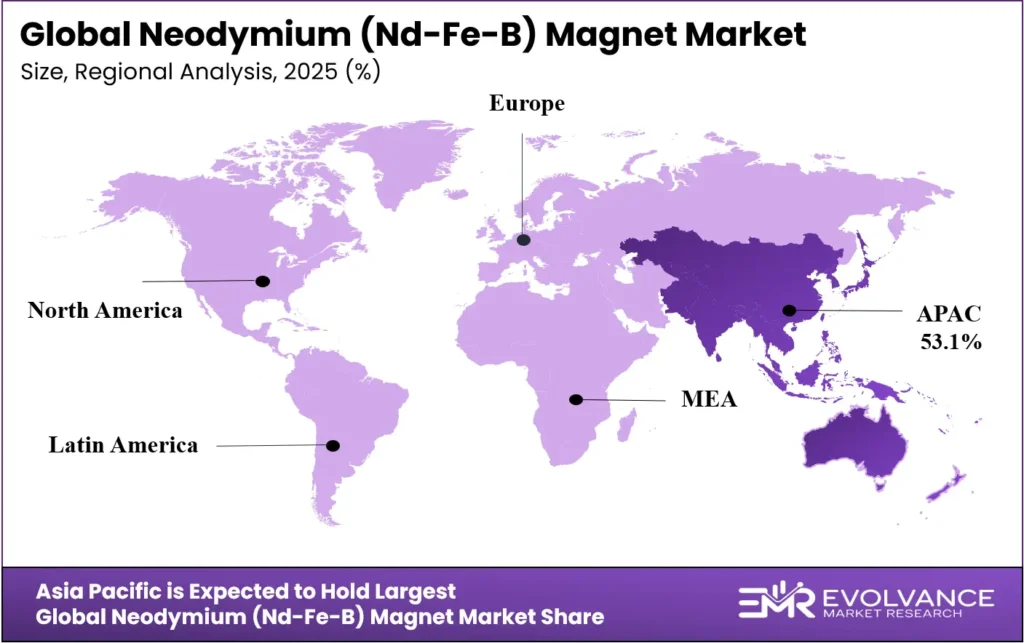

- Asia Pacific leads with a 53.1% market share, valued at USD 14.18 Billion, driven by concentrated magnet production and dominant EV manufacturing in China.

- By Type, Sintered NdFeB Magnets dominate with a 64.1% share, reflecting their superior energy density for automotive and wind applications.

- By Magnet Grade, N42 holds the top position with a 32.4% share as the preferred balance of strength and cost for motor OEMs.

- By Coating Type, Ni-Cu-Ni (Nickel-Copper-Nickel) commands 60.7% share due to its corrosion resistance in humid and high-heat environments.

- By Shape, Block/Rectangle magnets account for 45.2%, driven by high-volume motor and generator assembly requirements.

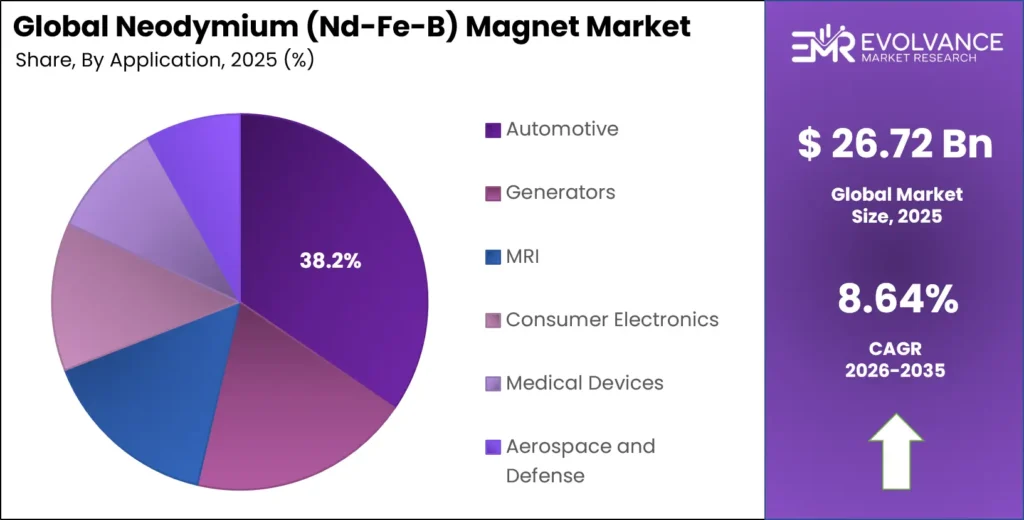

- By Application, Automotive applications dominate with 38.2% share, anchored by permanent magnet synchronous motor adoption across EV platforms.

Market Overview

Neodymium iron boron (Nd-Fe-B) permanent magnets are the highest-energy-density magnetic material available at commercial scale. They enable compact, high-torque motors in EVs, servo systems, and wind generators applications where ferrite or samarium-cobalt cannot deliver the required performance. Their properties make them structurally non-substitutable in most high-value end-uses today.

However, every Nd-Fe-B magnet depends on rare earth elements mined and refined in a highly concentrated supply chain. This concentration creates systemic risk for buyers outside China. The result is a market where demand is technically robust but supply is politically fragile — a tension that is now driving industrial policy responses across North America, Europe, and India.

Government action is reshaping the supply chain faster than organic market forces would. In June 2026, the U.S. Department of Commerce’s CHIPS Program finalized a definitive agreement awarding USA Rare Earth up to $277 million in direct incentives and up to a $1.3 billion federal loan to build domestic mine-to-magnet production capability. This signals that governments now treat Nd-Fe-B magnets as defense and energy-security infrastructure, not just industrial commodities.

As reported by the IEA, cumulative planned production capacity for downstream magnet alloys and finished permanent magnets outside China stood at just 18 kilotonnes in early 2026. This represents roughly one-third of diversified upstream mining capacity — exposing a severe processing bottleneck. For investors, this gap signals that midstream processing assets will attract premium valuations as non-Chinese governments fund supply chain self-sufficiency programs.

Type Insights

Sintered NdFeB Magnet dominates with 64.1% due to superior energy density for motor and generator use.

In 2025, Sintered NdFeB Magnet held a dominant market position in the By Type segment of the Neodymium (Nd-Fe-B) Magnet Market, with a 64.1% share. Sintered magnets are produced through powder metallurgy, yielding near-theoretical magnetic performance that bonded or hot-pressed variants cannot match.

EV traction motors and multi-megawatt wind generators require this energy density ceiling. Proterial’s NMX-F1SH-HF sintered magnet, validated in 2025, achieved a residual magnetic flux density of 1.40 T without heavy rare earth additions — directly answering OEM demand for supply-chain-clean, high-performance magnet grades.

Bonded NdFeB Magnet serves precision miniaturization markets where net-shape forming and isotropy outweigh peak magnetic performance. Bonded grades are injection-molded directly into complex geometries, eliminating secondary machining costs. Demand comes from hard disk drives, small cooling fans, and wearable medical devices — segments where dimensional tolerance matters more than flux density. Though a smaller share of total volume, bonded magnets command margin premiums from medical and consumer electronics OEMs seeking integrated component solutions.

Hot-pressed NdFeB Magnet occupies a niche between sintered and bonded grades, offering isotropic properties with finer grain structures suited to miniaturized high-frequency motor applications. Production volumes remain limited because the hot-pressing process is energy-intensive and difficult to scale. Adoption is concentrated in advanced servo actuators and implantable medical devices where the combination of compact form factor and thermal stability justifies higher unit cost. Growth in this sub-segment tracks collaborative robotics capex cycles.

Magnet Grade Insights

N42 dominates with 32.4% due to its balance of cost efficiency and performance for mainstream motor platforms.

In 2025, N42 held a dominant market position in the By Magnet Grade segment of the Neodymium (Nd-Fe-B) Magnet Market, with a 32.4% share. N42 sits at the performance-cost sweet spot that most commercial EV traction motor and HVAC compressor platforms target. It delivers adequate flux density for standard operating temperatures without requiring the premium dysprosium additions that higher grades demand. Motor OEMs standardize on N42 to simplify procurement and hold down material cost per unit, which concentrates volume strongly in this grade.

N35 serves cost-sensitive applications where magnetic performance requirements are modest and unit price matters most. Consumer electronics accessories, small actuators, and low-power sensor assemblies absorb N35 volumes. Buyers in these segments face intense end-product price competition, so they trade off peak flux density for lower magnet cost per kilogram. N35’s price advantage over mid-tier grades keeps it relevant in high-unit-count, low-margin production environments across Asia.

N48, N50, and N52 grades serve the top tier of performance-critical applications including MRI gradient coil assemblies, aerospace actuators, and high-speed spindle motors. These grades require tighter process control during sintering and higher dysprosium content, both of which compress margins and limit qualified suppliers. Buyers accept premium pricing because these grades unlock system-level design advantages — smaller motor envelopes, lighter aircraft structures, or faster MRI scan times — that no lower grade can replicate.

Coating Type Insights

Ni-Cu-Ni (Nickel-Copper-Nickel) dominates with 60.7% due to broad corrosion resistance across humid and high-temperature environments.

In 2025, Ni-Cu-Ni (Nickel-Copper-Nickel) held a dominant market position in the By Coating Type segment of the Neodymium (Nd-Fe-B) Magnet Market, with a 60.7% share. The three-layer structure provides both oxidation resistance from the outer nickel and adhesion durability from the copper interlayer. EV motor and industrial servo motor OEMs specify Ni-Cu-Ni as the default because it survives thermal cycling, vibration, and coolant exposure without delamination. Its long-established qualification in automotive supply chains reduces the switching risk that buyers would face with alternative coatings.

Zinc coating serves cost-sensitive outdoor and industrial applications where exposure to moisture demands protection but budget constraints eliminate premium options. Galvanic zinc is applied electrochemically at lower process cost than nickel-based stacks. It is common in wind turbine generator magnets where large surface areas make coating cost a material line item. Zinc’s moderate corrosion resistance is sufficient for sealed nacelle environments, which sustains its use in utility-scale wind applications despite its lower performance ceiling.

Epoxy coating addresses applications requiring electrical isolation in addition to corrosion protection. It is applied as a thin polymer layer, adding negligible dimensional change while blocking conductive pathways between adjacent magnets in stacked or segmented rotor assemblies. Medical device and aerospace applications particularly value epoxy for its biocompatibility and resistance to aggressive sterilization chemicals. As medical magnet demand grows, epoxy-coated grades gain share in premium application segments.

Shape Insights

Block/Rectangle dominates with 45.2% due to its compatibility with high-volume motor and generator assembly lines.

In 2025, Block/Rectangle held a dominant market position in the By Shape segment of the Neodymium (Nd-Fe-B) Magnet Market, with a 45.2% share. Rectangular blocks are the default output geometry from sintered magnet slicing operations, minimizing finishing cost per unit. Motor assembly lines built around block magnets benefit from standardized handling fixtures and automated placement systems.

High-volume EV traction motor production locked in rectangular formats years ago, and retooling to alternative geometries would require capital expenditure that OEMs are reluctant to authorize mid-program.

Ring magnets suit axial-flux motor designs and sensor assemblies where a single annular piece replaces multiple arc segments. Axial-flux architectures are gaining traction in in-wheel EV motors and direct-drive generators because they enable flatter, lighter drivetrains. As axial-flux motor volumes grow, ring magnet demand follows — representing one of the faster-growing shape sub-segments despite its current smaller share relative to block formats.

Application Insights

Automotive dominates with 38.2% due to mandatory permanent magnet synchronous motor deployment across major EV platforms.

In 2025, Automotive held a dominant market position in the By Application segment of the Neodymium (Nd-Fe-B) Magnet Market, with a 38.2% share. Global battery EV production surpassing 10 million units annually has made permanent magnet synchronous motors the de facto standard across most OEM platforms. Each EV drivetrain requires multiple kilograms of sintered Nd-Fe-B magnets, and auxiliary systems — power steering, HVAC compressors, braking — add further volume per vehicle. Automotive’s dominance will deepen as EV penetration rates rise in Europe, North America, and Southeast Asia.

Generators represent the second large demand pool, anchored by offshore wind turbines using direct-drive architectures. Direct-drive generators eliminate the gearbox, improving reliability in salt-spray environments, but they require large-format Nd-Fe-B magnet assemblies weighing several tonnes per turbine. Offshore wind capacity additions accelerating toward 30 GW annually convert directly into multi-year magnet order commitments for qualified suppliers, creating long-term revenue visibility that most other application segments do not offer.

MRI systems use Nd-Fe-B permanent magnets in open-field configurations where superconducting coils are not practical. Permanent magnet MRI units are lower-field-strength but far less costly to operate, making them viable in emerging market hospitals and point-of-care settings. As healthcare infrastructure expands across Southeast Asia, Africa, and Latin America, permanent magnet MRI demand grows independent of EV or wind cycles — providing diversification value for magnet suppliers serving multiple end markets.

Consumer Electronics rely on Nd-Fe-B in hard disk drive voice coil motors, premium headphone drivers, and smartphone haptic actuators. Miniaturization pressure continuously pushes engineers toward higher energy density grades to deliver equivalent acoustic or haptic performance from smaller components. Medical Devices include implantable drug delivery systems and surgical robotic end effectors, where extreme size and weight constraints make Nd-Fe-B the only viable permanent magnet option. Aerospace and Defense applications cover electromechanical actuators, radar systems, and directed-energy weapon power systems requiring magnets qualified to military environmental standards.

Market Segments Covered in the Report

By Type

- Sintered NdFeB Magnet

- Bonded NdFeB Magnet

- Hot-pressed NdFeB Magnet

- Hot-deformed NdFeB Magnet

By Magnet Grade

- N42

- N35

- N38

- N45

- N48

- N50

- N52

By Coating Type

- Ni-Cu-Ni (Nickel-Copper-Nickel)

- Zinc

- Epoxy

- Gold

- Silver

- PTFE

By Shape

- Block/Rectangle

- Ring

- Disc

- Arc/Segment

- Sphere/Ball

By Application

- Automotive

- Generators

- MRI

- Consumer Electronics

- Medical Devices

- Aerospace and Defense

Regional Insights

Asia Pacific Dominates the Neodymium (Nd-Fe-B) Magnet Market with a Market Share of 53.1%, Valued at USD 14.18 Billion

Asia Pacific holds 53.1% share, valued at USD 14.18 Billion, because China commands both the upstream rare earth supply chain and the downstream sintered magnet manufacturing base. Chinese producers benefit from vertically integrated processing, below-market rare earth feedstock access, and decades of process scale advantages. Japan and South Korea add high-grade magnet capacity through companies like Shin-Etsu and TDK. This structural concentration means Asia Pacific’s lead will persist even as Western reshoring programs ramp up through 2030.

North America Market Trends

North America is transitioning from a magnet import dependency toward active domestic production investment. Federal policy has become the primary growth engine, with the IRA and CHIPS Program directing capital toward mine-to-magnet supply chains. The region’s EV assembly base and defense procurement requirements create guaranteed demand volumes that justify the economics of new domestic magnet capacity now being built in Texas and other states.

Europe Market Trends

Europe’s Nd-Fe-B market is shaped by offshore wind buildout targets and automotive OEM electrification commitments. The EU Critical Raw Materials Act designates rare earth permanent magnets as strategic, triggering new domestic processing investments and import diversification mandates. University-led recycling programs — such as the Birmingham facility launched in early 2026 — signal Europe’s intent to build secondary supply loops rather than depend entirely on primary Chinese feedstocks.

Latin America Market Trends

Latin America holds meaningful rare earth mineral reserves, particularly in Brazil, but lacks the downstream processing and magnet manufacturing infrastructure to convert geology into market position. The region’s magnet consumption grows in step with EV assembly investments by global OEMs entering Brazilian and Mexican markets. Regional supply chain development depends on foreign direct investment and technology transfer agreements rather than organic industrial build-up in the near term.

Middle East and Africa Market Trends

The Middle East and Africa consume Nd-Fe-B magnets primarily through industrial automation, oil and gas equipment, and imported consumer electronics. Local magnet production is negligible. However, Gulf sovereign wealth funds are beginning to explore rare earth value chain investments as part of economic diversification strategies. Africa’s rare earth mining potential — especially in Tanzania, Namibia, and South Africa — positions the continent as a future upstream contributor rather than a finished magnet producer in the near term.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

On 26 November 2025, the Government of India approved a ₹7,280 crore scheme to build sintered NdFeB permanent magnet manufacturing capacity. The scheme targets 6,000 MTPA of integrated domestic output. It offers a capital subsidy of ₹750 crore per facility and ₹6,450 crore in sales-linked incentives. Each approved project must operate between 600 and 1,200 MTPA. This positions India as an emerging non-Chinese supply node backed by direct state funding.

In the United States, the Inflation Reduction Act and the CHIPS and Science Act together fund domestic critical mineral processing and magnet production. These laws require recipient manufacturers to meet domestic content thresholds, creating demand floors for U.S.-produced Nd-Fe-B magnets in EV and defense procurement. The regulatory framework converts government purchasing power into production volume guarantees, which reduces investor risk for new magnet factories operating outside the Chinese supply chain.

The EU Critical Raw Materials Act, which came into force in 2024, classifies neodymium, dysprosium, and praseodymium as strategic raw materials subject to domestic production and recycling benchmarks. Member states must establish national stockpile plans and report import dependency levels to the European Commission. This compliance obligation pushes European magnet buyers to qualify non-Chinese sources, directly expanding the addressable customer base for Western and Indian magnet producers.

Drivers

EV Motor Mandates and Wind Energy Expansion Pull Nd-Fe-B Volumes Beyond Alternative Magnet Capabilities

Battery EV production surpassing 10 million units annually forces permanent magnet synchronous motor adoption across nearly all major OEM platforms. Each vehicle requires kilogram-scale sintered magnet loads in the traction motor alone. Auxiliary electrified systems multiply per-vehicle magnet consumption further. No ferrite or samarium-cobalt alternative meets the torque density requirements within the packaging constraints set by current EV platform architectures.

Offshore wind direct-drive turbines add a second large pull on sintered magnet supply. Multi-megawatt nacelles using gearbox-free architectures require tonne-scale Nd-Fe-B assemblies per unit. In February 2026, MP Materials announced a long-term supply agreement with Apple for rare earth magnets made from recycled materials — showing that even consumer electronics OEMs are now securing dedicated supply chains, reflecting how demand pressure has spread well beyond automotive and wind.

Moreover, industrial automation investment in servo motors and collaborative robotics adds a third demand vector that operates independently of EV or energy cycles. Factory electrification programs across Europe and North America are specifying high-torque-density servo actuators that depend on Nd-Fe-B rotor assemblies. This multi-axis demand structure means any single end-market slowdown is unlikely to meaningfully reduce total magnet volume growth over the forecast horizon.

Restraints

Chinese Control of Heavy Rare Earth Refining Creates Structural Supply Concentration Risk for Non-Chinese Producers

Chinese state-controlled infrastructure processes over 85% of global heavy rare earth refining capacity. Dysprosium and terbium — critical coercivity-enhancing additives for high-temperature Nd-Fe-B grades — pass almost entirely through Chinese facilities. Non-Chinese magnet manufacturers have no viable alternative refining pathway at scale today. This is not a temporary market condition — it reflects decades of deliberate industrial policy investment that cannot be replicated quickly elsewhere.

The consequence for buyers is direct: any geopolitical disruption to Chinese rare earth exports immediately threatens magnet production schedules outside China. Western automotive OEMs building EV platforms on multi-year schedules face supply chain risk they cannot fully hedge through inventory alone. The IEA estimates that maintaining a strategic one-year stockpile of magnet rare earth materials for non-Chinese countries would cost approximately $200 million annually — a significant but finite insurance premium that few governments have yet authorized.

Additionally, rare earth mining and solvent extraction in primary production regions generates severe environmental legacies. New mine permitting in regions that could diversify supply — including parts of Africa and Central Asia — faces stringent environmental review timelines and community opposition. ESG-driven investment mandates further restrict capital flows to projects without credible environmental remediation plans. These constraints slow the pace at which new non-Chinese supply can enter the market even when government funding is available.

Growth Factors

Magnet Recycling Loops and Western Government Investment Create New Supply Pathways Outside China

Commercial-scale recycling of end-of-life Nd-Fe-B from EV drivetrains and wind turbine nacelles can bypass virgin rare earth oxide price volatility. An EU-funded electrochemical recycling project for recovering rare earths from end-of-life NdFeB magnets concluded its 24-month operational reporting cycle in April 2025, validating an environmentally cleaner recovery route. As EV fleets age and first-generation offshore wind turbines reach end of life, secondary rare earth feedstocks will grow from negligible to material volumes by the early 2030s.

Furthermore, MP Materials selected Northlake, Texas for a new $1.25 billion rare earth magnet manufacturing campus designed to produce up to 10,000 metric tons of NdFeB magnets per year. This investment is backed by long-term customer commitments, demonstrating that demand guarantees from major OEMs are now sufficient to finance Western magnet plants at commercial scale. Facilities of this size create anchor capacity that can attract additional investment from downstream motor manufacturers seeking proximity to magnet supply.

Strategic licensing of grain boundary diffusion technology to mid-tier magnet producers can reduce dysprosium content by 40–60% without sacrificing high-temperature coercivity. Lower heavy rare earth consumption per magnet directly reduces exposure to Chinese refining bottlenecks. For producers outside China, licensing this process technology removes the most critical raw material cost and supply risk simultaneously — improving both margin structure and supply chain resilience in a single step.

Emerging Trends

Rare Earth Onshoring Policy and Digital Traceability Platforms Reshape the Nd-Fe-B Supply Chain Structure

Rapid onshoring of rare earth separation and alloy production across North America and Europe is converting government policy into physical industrial capacity. The IRA and EU Critical Raw Materials Act provide funding triggers that are now producing final investment decisions rather than feasibility studies. This shift — from policy intent to capital deployment — means non-Chinese magnet supply capacity will begin to scale meaningfully within the forecast period, altering competitive dynamics for established Asian producers.

Automotive OEMs are migrating toward dual-sourcing and buffer inventory strategies for sintered Nd-Fe-B grades. Single-source dependency on Chinese magnets is increasingly flagged as an unacceptable procurement risk by OEM supply chain boards. Dual qualification processes are expensive and time-consuming, but their completion creates a more resilient supply base. Suppliers who receive dual-source qualification from major OEMs gain a structural advantage that is difficult for new entrants to displace once quality records are established.

Additionally, digital material passports and blockchain-based rare earth traceability systems are moving from pilot to standard requirement among EU-facing supply chains. These tools satisfy tightening EU conflict minerals and supply chain due diligence rules. For magnet producers, investing early in traceability platforms creates a qualification differentiator in European customer tenders. Research into iron nitride and manganese-based rare-earth-free permanent magnets also signals long-term substitution awareness — though commercial viability remains a decade away for most high-performance applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

This report covers the global Neodymium (Nd-Fe-B) permanent magnet market, defined as all commercially produced sintered, bonded, hot-pressed, and hot-deformed NdFeB magnet products sold for end-use in automotive drivetrains, wind generators, MRI systems, consumer electronics, medical devices, and aerospace and defense applications.

The market is valued in constant USD using 2025 as the base year to eliminate currency fluctuation effects across the ten-year forecast period. Revenue is measured at the point of finished magnet sale, covering all grades from N35 through N52 and all coating types including Ni-Cu-Ni, zinc, epoxy, gold, silver, and PTFE, across all standard commercial shapes.

The scope excludes soft magnetic materials, ferrite magnets, samarium-cobalt magnets, and electromagnetic coil assemblies not incorporating permanent NdFeB elements. Software-only magnet design tools, rare earth mining extraction operations upstream of alloy production, and rare earth oxide trading are outside the study boundary. Market sizing does not include captive production consumed internally by vertically integrated magnet manufacturers where no commercial transaction occurs.

Regional analysis covers North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa, with country-level granularity for the US, Canada, Germany, France, the UK, Spain, Italy, China, Japan, South Korea, India, Australia, Brazil, Mexico, GCC states, and South Africa.

Key Companies Insights

Neo Performance Materials Inc. operates one of the few rare earth processing and sintered magnet manufacturing platforms outside China with production assets in Europe and Estonia. Their geographic position directly addresses Western OEM demand for non-Chinese supply chain qualification. Neo’s ability to source mixed rare earth carbonate from diverse geographic origins and process it into finished magnets gives them a structural advantage as dual-sourcing mandates from automotive and defense buyers become standard procurement requirements through the forecast period.

JL MAG Rare-Earth Co., Ltd. is among China’s largest sintered NdFeB magnet producers, supplying EV motor OEMs, wind turbine builders, and industrial automation customers across Asia and Europe. Their scale in sintered magnet production enables cost efficiency that smaller Western producers cannot yet match. However, their China-headquartered production base increasingly faces qualification barriers from European and North American buyers under new supply chain due diligence and domestic content rules, limiting growth in regulated Western procurement channels.

Vacuumschmelze GmbH & Co. KG is a premium European magnet producer with deep expertise in high-grade sintered and bonded NdFeB grades for demanding applications in medical devices, aerospace, and precision automation. In June 2026, Energy Fuels Inc. announced a definitive agreement to acquire Vacuumschmelze for $1.9 billion, combining upstream U.S. rare earth processing with Vacuumschmelze’s European manufacturing capability. This transaction, if completed, would create one of the first fully integrated Western mine-to-magnet platforms at commercial scale.

Shin-Etsu Chemical Co., Ltd. is Japan’s largest NdFeB magnet producer and one of the world’s most technically advanced suppliers, holding foundational grain boundary diffusion patents that enable high-coercivity magnets with reduced dysprosium content. Their intellectual property position gives them licensing leverage over mid-tier producers globally. Shin-Etsu’s established customer relationships with Toyota, Honda, and European automotive OEMs provide stable long-term volume commitments that smaller competitors building new Western capacity must work years to replicate.

Key Companies

- Neo Performance Materials Inc.

- JL MAG Rare-Earth Co., Ltd.

- Vacuumschmelze GmbH & Co. KG

- Shin-Etsu Chemical Co., Ltd.

- TDK Corporation

- Proterial, Ltd.

- Daido Steel Co., Ltd.

- Ningbo Yunsheng Co., Ltd.

- Beijing Zhong Ke San Huan High-Tech Co., Ltd.

- Yantai Zhenghai Magnetic Material Co., Ltd.

- Innuovo Technology Co., Ltd.

- Galaxy Magnetics Co., Ltd.

- Adams Magnetic Products Co.

- Electron Energy Corporation

- Arnold Magnetic Technologies

- Goudsmit Magnetics

- Advanced Technology & Materials Co., Ltd. (AT&M)

- Earth-Panda Advance Magnetic Material Co., Ltd.

- Tianhe (Baotou) Advanced Tech Magnet Co., Ltd.

Recent Industry Developments

- In January 2026, the University of Birmingham launched a commercial-scale rare earth magnet recycling facility in the West Midlands with a capacity of 100 tonnes per year for producing sintered NdFeB magnets from recycled feeds, establishing Europe’s first dedicated secondary magnet production unit.

- In November 2025, the Government of India approved a ₹7,280 crore scheme to support domestic NdFeB permanent magnet manufacturing, targeting 6,000 MTPA of integrated capacity through capital subsidies and sales-linked incentives for approved producers.

- In 2025, Proterial, Ltd. validated its fourth-generation NMX-G1NH-HF neodymium magnet, achieving a residual magnetic flux density of 1.42 T and a coercive force of ≥ 1830 kA/m with stable operation in environments above 100°C, targeting EV steering and compressor motor applications.

- In April 2025, an EU-funded project using electrochemical processing to recover rare earths from end-of-life NdFeB permanent magnets concluded its 24-month operational reporting cycle, providing verified data on a cleaner alternative recycling route for commercial scale-up consideration.

- In April 2025, the U.S. Geological Survey published its 2025 Mineral Commodity Summaries for Rare Earths, providing official U.S. and global rare earth production statistics covering 2020–2024, which serve as the authoritative federal baseline for domestic supply chain policy planning.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 26.72 Billion |

| Forecast Revenue (2035) | USD 61.20 Billion |

| CAGR (2026-2035) | 8.64% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Sintered NdFeB Magnet, Bonded NdFeB Magnet, Hot-pressed NdFeB Magnet, Hot-deformed NdFeB Magnet), By Magnet Grade (N42, N35, N38, N45, N48, N50, N52), By Coating Type (Ni-Cu-Ni, Zinc, Epoxy, Gold, Silver, PTFE), By Shape (Block/Rectangle, Ring, Disc, Arc/Segment, Sphere/Ball), By Application (Automotive, Generators, MRI, Consumer Electronics, Medical Devices, Aerospace and Defense) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Neo Performance Materials Inc., JL MAG Rare-Earth Co. Ltd., Vacuumschmelze GmbH & Co. KG, Shin-Etsu Chemical Co. Ltd., TDK Corporation, Proterial Ltd., Daido Steel Co. Ltd., Ningbo Yunsheng Co. Ltd., Beijing Zhong Ke San Huan High-Tech Co. Ltd., Yantai Zhenghai Magnetic Material Co. Ltd., Innuovo Technology Co. Ltd., Galaxy Magnetics Co. Ltd., Adams Magnetic Products Co., Electron Energy Corporation, Arnold Magnetic Technologies, Goudsmit Magnetics, Advanced Technology & Materials Co. Ltd. (AT&M), Earth-Panda Advance Magnetic Material Co. Ltd., Tianhe (Baotou) Advanced Tech Magnet Co. Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |