What is the Fluorochemicals Market Size?

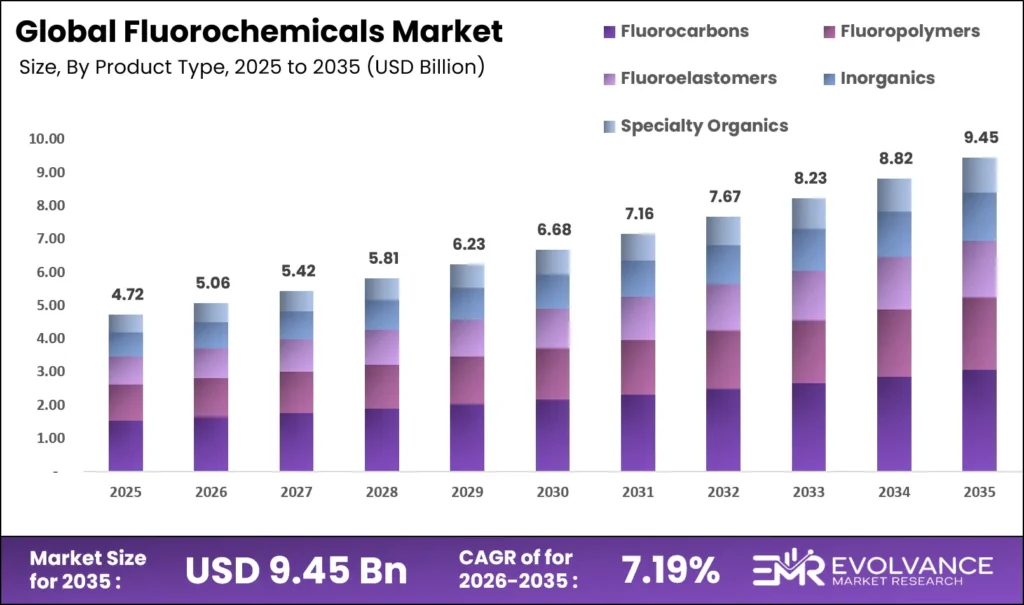

The Global Fluorochemicals Market size will be worth around USD 9.45 Billion by 2035 from USD 4.72 Billion in 2025, growing at a CAGR of 7.19% during the forecast period 2026 to 2035. The Kigali Amendment’s HFC phasedown mandate and battery gigafactory buildouts are pulling demand for next-generation fluorinated compounds faster than most suppliers had planned. Enterprise buyers across HVAC, semiconductor, and flywheel energy storage sectors are shifting procurement toward lower-GWP and high-purity specialty grades. Geopolitically concentrated fluorspar supply chains, with China controlling most downstream processing, introduce real cost and availability risks for non-integrated producers.

Market Highlights

- The Global Fluorochemicals Market will grow from USD 4.72 Billion in 2025 to USD 9.45 Billion by 2035, at a CAGR of 7.19%.

- Asia Pacific leads with a 53.7% market share, valued at USD 2.53 Billion, driven by dense manufacturing output and raw material access.

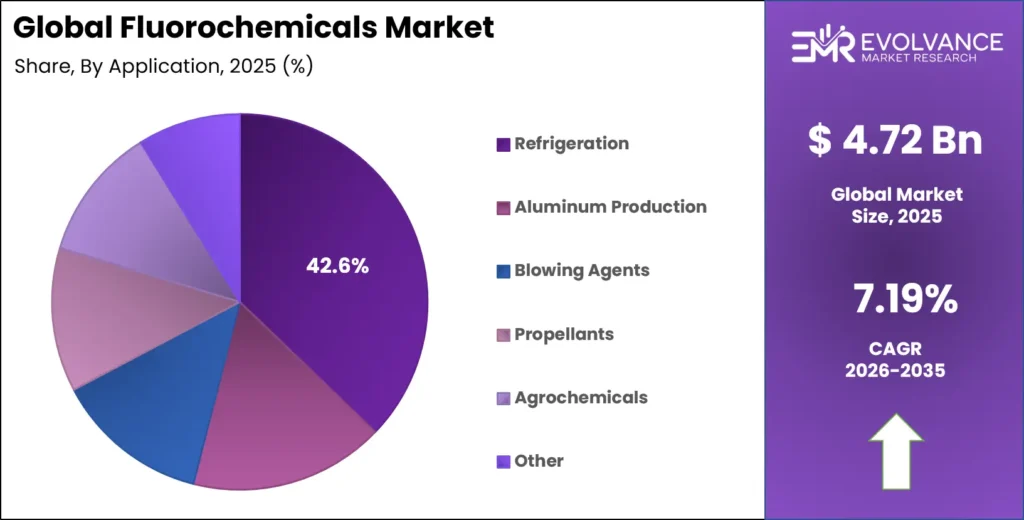

- Fluorocarbons dominate the By Product Type segment with a 53.2% share, while Refrigeration leads By Application at 42.6%.

- Emulsion holds a 43.6% share in the By Form segment; Anionic Fluorochemicals lead By Ionic Nature at 39.2%.

- Fluorosurfactants command 48.1% in By Specialized Additive Function; HFCs lead By Compound Type at 34.7%.

- Chemical Vapor Deposition leads By Technology at 41.3%; Chemical and Petrochemicals leads By End-Use Industry at 31.8%.

Market Overview

The fluorochemicals market covers a broad set of fluorine-based compounds used across refrigeration, semiconductors, energy storage, pharmaceuticals, and specialty coatings. These compounds — including fluorocarbons, fluoropolymers, fluoroelastomers, and fluorinated gases — deliver thermal stability and chemical resistance that standard materials cannot match. Their technical performance makes them difficult to replace in critical industrial and consumer applications.

The market spans products ranging from high-volume refrigerant gases and PTFE materials to precision fluorinated electrolytes and etching agents for chip production. This diversity means demand is not tied to a single sector cycle. When refrigerant demand dips due to seasonal shifts, semiconductor and battery segments typically absorb the slack — creating a more resilient revenue base for diversified producers.

Policy is reshaping this market’s structure as much as technology is. The Kigali Amendment mandates a global phase-down of high-GWP HFCs, forcing manufacturers, distributors, and end-users to switch to next-generation low-GWP blends on a fixed schedule. This is not optional compliance — it is a timed transition that forces procurement changes across HVAC, automotive, and commercial refrigeration industries simultaneously.

According to India’s National Green Tribunal, one fluorochemical facility in India alone holds an installed capacity of approximately 39,300 tonnes per annum for refrigerant gases, PTFE, and related compounds. This scale signals that domestic producers in growth markets are building industrial-grade infrastructure to meet regional self-sufficiency targets, reducing import dependence and reshaping global supply flows.

The European Environment Agency published its 2025 F-gas compliance dataset covering fluorinated greenhouse gas production, imports, exports, and destruction for the 2024 reporting year. This data infrastructure makes non-compliance in Europe increasingly visible and enforceable — a condition that will accelerate the exit of high-GWP products from EU supply chains and lift demand for compliant alternatives.

Product Type Insights

Fluorocarbons dominate with 53.2% due to broad refrigerant and industrial gas demand.

In 2025, Fluorocarbons held a dominant market position in the By Product Type segment of the Fluorochemicals Market, with a 53.2% share. Their dominance reflects decades of embedded use in HVAC systems, industrial refrigeration, and aerosol propellants. Buyers across these sectors have long procurement cycles, and transitioning away from established fluorocarbon chemistries involves significant re-certification costs — giving this sub-segment structural staying power even as regulations tighten.

Fluoropolymers serve as the backbone for high-performance coatings, wire insulation, and membrane systems across semiconductor, energy, and chemical processing applications. Demand is rising as green hydrogen, hydrogen electrolyzer plants require fluoropolymer ion-exchange membranes and as EV battery production scales. Producers who can deliver consistent purity and volume will benefit from the long-term supply agreements these sectors typically prefer.

Fluoroelastomers target sealing, gasket, and tubing applications in environments with extreme heat, chemical exposure, or pressure. Pharmaceutical continuous manufacturing and oil and gas processing are core demand pockets. These applications prioritize lifecycle reliability over unit cost, making fluoroelastomers a margin-rich sub-segment for producers with proven material certifications.

Specialty Organics cover high-value fluorinated intermediates and active molecules used in agrochemicals, pharmaceuticals, and specialty coatings. These products carry higher margins than commodity fluorocarbons but require more complex synthesis and tighter regulatory clearance. Producers entering this space gain pricing power but face longer development timelines.

Form Insights

Emulsion dominates with 43.6% due to versatile processing and coating compatibility.

In 2025, Emulsion held a dominant market position in the By Form segment of the Fluorochemicals Market, with a 43.6% share. Emulsion forms are widely used in surface treatment, textile finishing, and paper coating because they integrate easily into water-based processing lines. This compatibility with existing production systems reduces the cost of switching to fluorochemical-based solutions, making emulsions the default choice for industrial buyers scaling up surface treatment capacity.

Film forms serve lightweight glazing, photovoltaic front-sheets, and packaging applications where optical clarity and chemical resistance must coexist. Solar module manufacturers are exploring transparent recyclable fluoropolymer films as a lower-carbon alternative to traditional front-sheet materials, opening a new demand channel tied directly to solar capacity additions.

Pellet forms serve high-throughput thermoplastic processing for automotive, electrical, and construction applications. Their uniformity makes them well-suited for injection molding lines running at industrial volumes. Automotive OEMs adopting lightweight fluoropolymer components for EV platforms represent a growing demand source for pellet-form materials.

Powder forms are used in coatings, lining applications, and additive blending. Their fine particle size enables uniform dispersion in industrial coatings applied to chemical vessels, pipes, and cookware surfaces. PTFE powder benefits from the long-established global cookware and industrial coating supply chains.

Ionic Nature Insights

Anionic Fluorochemicals dominate with 39.2% due to broad surfactant and processing use.

In 2025, Anionic Fluorochemicals held a dominant market position in the By Ionic Nature segment of the Fluorochemicals Market, with a 39.2% share. These compounds provide strong surface tension reduction in aqueous systems and are widely used as fluorosurfactants in industrial coatings, firefighting foams, and textile treatments. Their performance at low concentrations makes them cost-effective for large-scale industrial applications, anchoring their share even as PFAS regulations tighten around specific long-chain variants.

Cationic Fluorochemicals carry a positive charge and find use in antimicrobial coatings, paper treatment, and textile finishing where charge interaction with substrates matters. Their niche function limits volume but supports premium pricing in applications where performance differentiation is measurable and auditable.

Non-ionic Fluorochemicals are compatible with a wider range of formulation systems because they do not carry a net charge. They are used in emulsions, wetting agents, and specialty coatings where compatibility across pH ranges is essential. R&D investment in fluorine-free and short-chain alternatives has been highest in this sub-segment, as reformulation work is technically more accessible here than in ionic chemistries.

Specialized Additive Function Insights

Fluorosurfactants dominate with 48.1% due to widespread industrial and coating use.

In 2025, Fluorosurfactants held a dominant market position in the By Specialized Additive Function segment of the Fluorochemicals Market, with a 48.1% share. They deliver extreme reduction in surface tension at low dose rates, making them effective in coatings, inks, and fire suppression systems. Regulatory pressure on PFAS-based firefighting foams is simultaneously driving demand for next-generation short-chain or fluorine-free alternatives — a reformulation cycle that keeps this sub-segment active even as specific chemistries exit the market.

Stain Resistant Additives and Sealers protect textiles, carpets, stone, and paper from oil and water-based staining. Consumer products and construction are the primary end-use channels. Long-chain PFAS restrictions in the EU and North America have forced reformulation toward short-chain alternatives — a transition that increases development costs for additive producers but also creates supplier switching opportunities for those with compliant formulations ready to deploy.

Acid Mist Suppressants reduce hazardous acid mist emissions in electroplating, metal finishing, and battery production. Tightening workplace safety regulations across all major manufacturing regions are making acid mist control a compliance requirement rather than an optional upgrade. This mandatory adoption profile creates stable, recurring demand that is relatively price-insensitive.

Application Insights

Refrigeration dominates with 42.6% due to embedded infrastructure and global HFC phasedown schedules.

In 2025, Refrigeration held a dominant market position in the By Application segment of the Fluorochemicals Market, with a 42.6% share. The Kigali Amendment’s legally binding HFC phasedown timetable is forcing every major economy to retire high-GWP refrigerants on a fixed schedule. This creates a mandated replacement cycle that guarantees demand for low-GWP fluorochemical refrigerant blends through the entire forecast period — a structural demand floor that is regulatory, not discretionary.

Aluminum Production uses fluorine-based compounds, particularly cryolite and aluminum fluoride, as electrolyte components in the Hall-Héroult smelting process. Aluminum demand from EV battery casings, lightweight vehicle structures, and construction continues to rise, keeping fluorochemical consumption in this application on a steady upward track tied to global aluminum output growth.

Propellants in metered-dose inhalers and aerosol applications use HFCs and their successor HFO compounds. The pharmaceutical propellant segment is undergoing transition as regulators mandate a shift from HFA-134a to lower-GWP alternatives such as HFA-152a and HFO-1234ze — generating both product development activity and supply chain restructuring among inhaler manufacturers globally.

Agrochemicals use fluorine chemistry in active ingredient synthesis, where fluorine atoms enhance the biological activity and metabolic stability of herbicides, fungicides, and insecticides. Fluorinated agrochemicals now account for a large and growing portion of new pesticide registrations, reflecting how deeply fluorine chemistry has embedded itself into modern crop protection science.

Compound Type Insights

Hydrofluorocarbons (HFCs) dominate with 34.7% due to established refrigerant and aerosol infrastructure.

In 2025, Hydrofluorocarbons (HFCs) held a dominant market position in the By Compound Type segment of the Fluorochemicals Market, with a 34.7% share. Their position reflects decades of installed base in commercial HVAC, automotive air conditioning, and industrial refrigeration. The Kigali Amendment’s phasedown schedule means this share will decline over the forecast period as HFOs and low-GWP blends take volume — but the transition timeline ensures HFCs remain the largest single compound type through the near term.

Hydrofluoroolefins (HFOs) are the primary replacement candidates for high-GWP HFCs across refrigeration, blowing agent, and propellant applications. Their low global warming potential and comparable performance in most HFC use cases make them the default transitional chemistry under the Kigali Amendment framework. Producers with HFO manufacturing capacity are positioned to capture incremental volume as HFC phase-out schedules accelerate in developed markets.

Perfluorocarbons (PFCs) are chemically inert, high-purity compounds used in semiconductor manufacturing, medical imaging contrast agents, and specialty heat transfer applications. AI-driven semiconductor capacity expansion and the buildout of immersion-cooled data centers are both pulling PFC demand into new use cases at meaningful volumes, adding a technology-driven growth layer to this sub-segment.

Technology Insights

Chemical Vapor Deposition (CVD) dominates with 41.3% due to semiconductor and advanced materials manufacturing demand.

In 2025, Chemical Vapor Deposition (CVD) held a dominant market position in the By Technology segment of the Fluorochemicals Market, with a 41.3% share. CVD is the standard deposition method for fluorinated thin films and dielectric layers in semiconductor device fabrication. As AI-driven fab expansions add capacity globally, CVD equipment utilization and the fluorinated precursor gases that feed it are both scaling in parallel — making CVD the segment most tightly coupled to the AI-semiconductor demand wave.

Plasma Etching uses reactive fluorinated gases to selectively remove material layers during semiconductor patterning. Tighter node geometries in advanced chip manufacturing increase the number of etch steps per wafer, directly multiplying fluorinated gas consumption per device produced. This etch-intensity trend benefits specialty gas suppliers with semiconductor-grade quality certifications.

Solution Polymerization produces fluoropolymers with controlled molecular weight and chain architecture, enabling precise tuning of mechanical and thermal properties. This technology is preferred for specialty grades of PVDF and other functional fluoropolymers used in battery binders, membranes, and medical-grade tubing. In June 2026, Arkema completed a 15% capacity expansion for its Kynar PVDF production at Calvert City, Kentucky — direct evidence that producers are investing in solution polymerization capacity ahead of confirmed battery demand.

End-Use Industry Insights

Chemical and Petrochemicals dominate with 31.8% due to deep process integration across fluorochemical supply chains.

In 2025, Chemical and Petrochemicals held a dominant market position in the By End-Use Industry segment of the Fluorochemicals Market, with a 31.8% share. Chemical plants use fluorochemicals as process solvents, catalyst components, and corrosion-resistant lining materials across reactors, piping, and heat exchangers. The sector’s demand is structural — fluorinated materials are embedded in plant design, not discretionary add-ons — making this the most stable and volume-anchored end-use category in the market.

Electrical and Electronics manufacturers rely on fluorinated materials for wire insulation, PCB coatings, connector housings, and dielectric fluids. Fluorinated dielectric heat transfer fluids for single-phase immersion cooling of AI training clusters represent a fast-scaling high-value application. Data center operators running dense GPU infrastructure need cooling solutions that perform at higher heat flux densities than traditional air cooling can manage — positioning immersion cooling fluids as a new revenue stream for fluorochemical suppliers.

Aerospace uses perfluoroelastomers and specialty fluoropolymers in engine seals, fuel system components, and hydraulic line linings where performance at temperature extremes is non-negotiable. Once a fluorochemical material earns a flight certification, it typically stays in the supply chain for the aircraft’s full service life — creating a durable, predictable demand base for qualified suppliers.

Market Segments Covered in the Report

By Product Type

- Fluorocarbons

- Fluoropolymers

- Fluoroelastomers

- Inorganics

- Specialty Organics

- Gases

By Form

- Emulsion

- Film

- Granule

- Pellet

- Powder

By Ionic Nature

- Anionic Fluorochemicals

- Cationic Fluorochemicals

- Non-ionic Fluorochemicals

- Zwitterionic Fluorochemicals

By Specialized Additive Function

- Fluorosurfactants

- Stain Resistant Additives and Sealers

- Acid Mist Suppressants

- Flame Retardant Additives

By Application

- Refrigeration

- Aluminum Production

- Blowing Agents

- Propellants

- Agrochemicals

- Solvents

- Surface Treatment

- Pharmaceuticals and Meter Dose Inhalers

By Compound Type

- Hydrofluorocarbons (HFCs)

- Hydrofluoroolefins (HFOs)

- Perfluorocarbons (PFCs)

- Nitrogen Trifluoride

- Sulfur Hexafluoride

By Technology

- Chemical Vapor Deposition (CVD)

- Plasma Etching

- Solution Polymerization

- Suspension Polymerization

By End-Use Industry

- Chemical and Petrochemicals

- Automotive

- Electrical and Electronics

- Aerospace

- Construction

- Consumer Goods

- Oil and Gas

Regional Insights

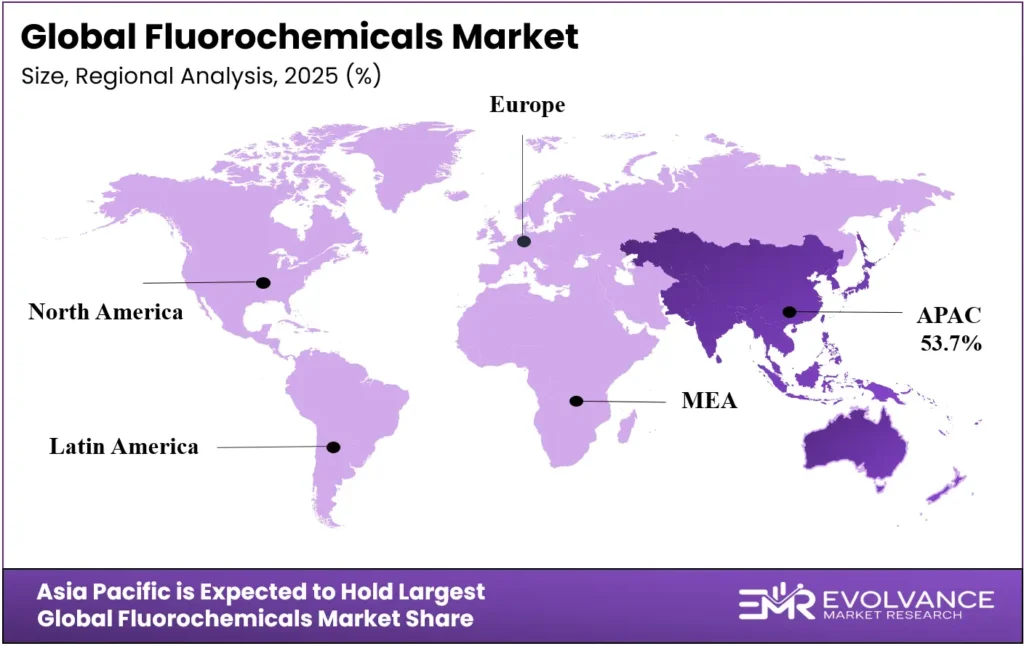

Asia Pacific Dominates the Fluorochemicals Market with a Market Share of 53.7%, Valued at USD 2.53 Billion

Asia Pacific holds 53.7% of the global fluorochemicals market, valued at USD 2.53 Billion in 2025. China’s dual position as the world’s largest fluorspar miner and its largest downstream fluorochemical processor gives the region an integrated cost advantage that no other geography can quickly replicate. India is adding production scale through domestic manufacturing investment — with individual facilities now holding capacities measured in tens of thousands of tonnes per annum for refrigerant and fluoropolymer output. These supply-side fundamentals will keep Asia Pacific’s position dominant through the forecast period.

North America Market Trends

North America is undergoing a structured transition in fluorochemicals, driven by two parallel forces. The Kigali Amendment’s HFC phasedown schedule and tightening EPA PFAS regulations are reshaping product portfolios, while battery gigafactory construction across the US is pulling demand for high-purity fluorinated electrolyte materials. In June 2026, Chemours settled with the US EPA under a Consent Decree — signaling that regulatory enforcement costs are now a permanent line item for large producers in this region, with liability obligations stretching across a fifteen-year horizon.

Europe Market Trends

Europe is the most regulation-driven fluorochemicals market globally. The EU F-gas Regulation’s phase-down schedule and broad PFAS restriction proposals under REACH are simultaneously contracting legacy product lines and forcing R&D investment into compliant alternatives. The European Environment Agency’s enforcement dataset covering the most recent reporting year has made non-compliance increasingly visible. Producers without clear PFAS transition roadmaps risk losing EU market access entirely as restriction timelines firm up.

Latin America Market Trends

Latin America’s fluorochemicals demand is anchored in refrigeration, agriculture, and light industrial applications. Brazil and Mexico are the primary consumption markets, with demand for refrigerant gases and surface treatment chemicals tied to regional HVAC and food processing sector growth. The region lacks domestic fluorochemical production at scale, making it structurally import-dependent and exposed to global supply chain disruptions and currency-driven price volatility in ways that more vertically integrated markets are not.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The Kigali Amendment to the Montreal Protocol legally mandates a global phase-down of hydrofluorocarbons across all signatory nations. Developed markets must achieve an 85% reduction in HFC consumption by 2036, while developing markets face staggered timelines extending through 2047. This framework forces end-users in HVAC, automotive air conditioning, and industrial refrigeration to retire existing HFC systems and adopt low-GWP alternatives on binding regulatory timetables.

The European Union’s revised F-gas Regulation entered a tightened phase from 2024 onward, imposing stricter HFC quotas, broader product bans, and mandatory reporting for fluorinated greenhouse gas producers and importers. This enforcement infrastructure raises compliance costs for producers and tightens market access for non-compliant chemistries across EU member states — conditions that will systematically remove high-GWP products from European supply chains.

In the United States, the EPA’s Significant New Alternatives Policy program continues to approve HFC alternatives while delisting high-GWP compounds from key end uses. Separately, the EPA’s PFAS regulatory framework — including maximum contaminant level rules finalized in 2024 — is constraining addressable markets for long-chain PFAS compounds. In June 2026, Chemours entered a Consent Decree with the US EPA and WVDEP, committing to a USD 22.5 million civil penalty and USD 90 million in environmental mitigation projects over fifteen years.

India’s National Green Tribunal actively monitors fluorochemical manufacturing compliance. Its June 2025 inspection report documented production capacity, effluent treatment capacity of 2,800 m³/day, and a captive power plant of 48 MW at a major fluorochemical site. This oversight signals that India is building regulatory enforcement capacity alongside its industrial expansion — a trend that will raise compliance costs for domestic producers but also create a more credible operating environment for foreign investment.

Drivers

Kigali Amendment HFC Phase-Down Forces Accelerated Adoption of Low-GWP Fluorochemical Blends

The Kigali Amendment’s binding HFC phase-down schedule is the single most powerful demand-creation mechanism in the fluorochemicals market today. Every major economy is legally committed to cutting HFC consumption by defined percentages on fixed timelines. HVAC manufacturers, commercial refrigeration operators, and automotive OEMs must replace their current refrigerant systems — not when convenient, but on a regulatory clock. This creates guaranteed volume for low-GWP fluorochemical blends through the entire forecast period.

Beyond refrigerants, energy efficiency building codes are tightening globally and mandating advanced low-GWP fluorochemical blowing agents in rigid foam insulation panels. Markets in Europe, North America, and key Asia Pacific economies are updating standards on overlapping timelines. This parallel policy push across two major end-use channels — refrigerants and insulation — creates a compounding demand effect that is structural and multi-year, not cyclical.

Honeywell announced in October 2025 the planned spin-off of its Advanced Materials fluorochemicals division into a standalone publicly traded company named Solstice Advanced Materials. This corporate restructuring signals that major producers see fluorochemical transition chemistry as a distinct, high-value business unit — one worth separating from diversified conglomerates to unlock dedicated capital allocation and management focus during this phase-down-driven transition window.

Restraints

PFAS Regulatory Bans and Litigation Shrink Addressable Markets for Long-Chain Fluorochemical Product Lines

Proliferating regulatory restrictions targeting broad PFAS categories are contracting the addressable market for established long-chain fluorochemical product lines across multiple geographies simultaneously. The EU’s PFAS restriction proposals under REACH, combined with US EPA maximum contaminant level rules finalized in 2024, are removing entire product categories from legal commerce. Producers with large long-chain PFAS portfolios face both revenue write-downs and stranded asset risks in manufacturing capacity built around now-restricted chemistries.

Class-action litigation in the United States has added a financial liability layer on top of the regulatory burden. The Chemours Consent Decree reached in June 2026 sets a legal precedent that other PFAS producers will likely face, raising the effective cost of operating in long-chain fluorochemical markets and accelerating the exit of marginal players who cannot absorb these liabilities. The combined civil penalty and mitigation commitment — totaling more than USD 112 million — illustrates the scale of exposure facing producers with legacy PFAS operations.

Producers dependent on long-chain PFAS revenues must now simultaneously fund litigation defense, regulatory compliance programs, and R&D investment in next-generation alternatives — all from the same balance sheet. This capital allocation pressure is most acute for mid-sized producers who lack the financial reserves of global chemical majors. The constraint narrows the field of viable competitors and concentrates market share among producers with the scale to absorb these costs while managing the transition.

Growth Factors

Battery Gigafactory Buildouts and Semiconductor Fab Expansions Create High-Purity Fluorochemical Demand at Industrial Scale

Lithium-ion battery gigafactories under construction across North America, Europe, and Asia require fluorinated electrolyte salts, PVDF binders, and separator coatings at volumes that dwarf previous specialty chemical demand in these categories. Each gigawatt-hour of cell production capacity requires a defined tonnage of fluorinated materials that must meet exacting purity specifications. As announced gigafactory capacity translates into operating production, fluorochemical suppliers with battery-grade quality systems will be first in line for long-term supply contracts.

Gujarat Fluorochemicals commissioned a 73.7 MW hybrid renewable-energy installation at its Dahej operations in FY2024-25, reporting that renewable sources accounted for 8.3% of its total energy consumption during that year. This investment signals that leading fluorochemical producers are building the energy infrastructure needed to meet sustainability procurement requirements of battery and semiconductor customers who now audit supply chain carbon intensity as a vendor qualification criterion.

AI-driven semiconductor demand is creating a parallel high-purity fluorinated gas consumption wave tied to fab utilization and expansion. Plasma etching and CVD processes each consume multiple fluorinated gases per wafer cycle, and advanced node chips require more process steps than previous generations. As AI chip production scales globally, fluorinated gas demand scales with it — giving specialty gas suppliers a direct line of sight into semiconductor capital spending plans as a leading demand indicator.

Emerging Trends

Downstream Integration and AI-Driven Molecular Screening Are Reshaping How Fluorochemical Value Is Created and Captured

Fluorochemical producers are moving downstream into precision parts fabrication to capture higher margins in aerospace, semiconductor equipment, and medical device supply chains. A raw fluoropolymer pellet sold to a converter earns commodity pricing. The same material shaped into a certified semiconductor wafer carrier or a medical-grade valve body commands application-specific pricing with margin structures that bear no relation to the underlying polymer cost. Producers who can qualify and supply these fabricated components are repositioning themselves as specialty manufacturers.

AI-driven in silico toxicology screening is compressing the early-stage discovery timeline for new fluorochemical candidates. Traditional molecular development programs commit significant synthesis and regulatory testing resources before knowing whether a candidate will face regulatory barriers. AI pre-screening can flag likely PFAS classification issues or environmental persistence risks before a single gram of material is synthesized — systematically reducing the cost and timeline of building compliant next-generation product portfolios for early adopters.

Fluoropolymer membrane-based gas separation modules for direct air capture and industrial carbon dioxide recovery are moving from pilot to pre-commercial scale at several sites globally. These systems require fluoropolymer membranes with precisely tuned permeability and durability profiles. As carbon capture infrastructure scales under policy support in the EU, US, and parts of Asia, it will create a new end-use channel for specialty fluoropolymer membrane materials — one that did not exist as a meaningful demand source five years ago.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

This report covers the global fluorochemicals market, which includes fluorocarbons, fluoropolymers, fluoroelastomers, inorganic fluorine compounds, specialty organic fluorochemicals, and fluorinated gases. The market is valued in constant US dollars using 2025 as the base year to remove the effect of currency movements from cross-period comparisons. The scope spans all major product forms — emulsion, film, granule, pellet, and powder — and covers demand across eight primary applications and seven end-use industries. All revenue figures represent manufacturer-level selling prices.

This report excludes non-fluorinated specialty chemicals, general purpose industrial gases without fluorine content, and biological or organic active pharmaceutical ingredients where fluorine plays no role in the molecular structure. Software platforms for fluorochemical process management and unrelated specialty polymer markets — including silicones, polyurethanes, and chlorinated polymers — are outside the defined scope. The analysis covers the period from 2020 through 2035, with 2020 to 2024 as the historical baseline and 2026 to 2035 as the forecast horizon.

Key Companies Insights

The Chemours Company is the global leader in fluoroproducts and titanium technologies, with its Opteon refrigerant line positioned as the primary commercial beneficiary of HFC phase-down mandates under the Kigali Amendment. However, its June 2026 Consent Decree with the US EPA signals that legacy PFAS liability will consume significant capital over the next fifteen years — constraining investment capacity just as the low-GWP transition enters its most critical growth phase and competitors race to build compliant capacity.

Arkema S.A. has positioned Kynar PVDF as a core growth platform aligned with battery, photovoltaic, and chemical processing demand. The June 2026 completion of a 15% capacity expansion at its Calvert City, Kentucky facility reflects direct capital commitment to the battery materials growth trajectory. Arkema’s strategy of investing ahead of volume, rather than waiting for confirmed orders, positions it to be the preferred supplier for battery gigafactories that need supply certainty before their own production lines go live.

Honeywell International Inc. announced in October 2025 the planned spin-off of its Advanced Materials fluorochemicals business into Solstice Advanced Materials, a standalone publicly traded entity. This structural move is designed to give fluorochemicals dedicated management focus, independent capital allocation, and a valuation multiple more reflective of specialty chemicals peers than a diversified industrial conglomerate. The spin-off is well-supported by the regulatory transition dynamics currently driving HFO demand globally.

Gujarat Fluorochemicals Limited is India’s most integrated fluorochemical producer, with operations spanning fluorspar processing, refrigerant manufacturing, PTFE production, and specialty fluoropolymers. Its Dahej renewable energy plant commissioned in FY2024-25 reduces both energy costs and supply chain carbon intensity — two criteria increasingly used by multinational customers to qualify suppliers. As India’s domestic fluorochemical ambitions grow alongside government support for import substitution, Gujarat Fluorochemicals is the clearest domestic beneficiary of that policy direction.

Key Companies

- The Chemours Company

- Arkema S.A.

- Honeywell International Inc.

- Gujarat Fluorochemicals Limited

- Daikin Industries Ltd.

- 3M Company

- Solvay S.A.

- AGC Inc.

- Navin Fluorine International Limited

- Dongyue Group

- Pelchem SOC Ltd

Recent Industry Developments

- In June 2026, Chemours agreed to a Consent Decree with the U.S. EPA and WVDEP to resolve PFAS emissions claims, committing to a USD 22.5 million civil penalty and USD 90 million in mitigation projects over 15 years.

- In March 2026, Daikin Industries announced the establishment of Daikin Chemical India Private Limited in Gurugram, India, with an initial capital of INR 600 million, marking a direct manufacturing entry into the Indian fluorochemicals market.

- In October 2025, Honeywell announced the expected spin-off of its Advanced Materials fluorochemicals business into a standalone publicly traded company named Solstice Advanced Materials, enabling dedicated capital and management focus for the division.

- In FY2024-25, Gujarat Fluorochemicals reported total renewable energy consumption of 863,183 GJ following commissioning of its hybrid renewable energy plant at the Dahej facility.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.72 Billion |

| Forecast Revenue (2035) | USD 9.45 Billion |

| CAGR (2026-2035) | 7.19% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Fluorocarbons, Fluoropolymers, Fluoroelastomers, Inorganics, Specialty Organics, Gases), By Form (Emulsion, Film, Granule, Pellet, Powder), By Ionic Nature (Anionic, Cationic, Non-ionic, Zwitterionic Fluorochemicals), By Specialized Additive Function (Fluorosurfactants, Stain Resistant Additives and Sealers, Acid Mist Suppressants, Flame Retardant Additives), By Application (Refrigeration, Aluminum Production, Blowing Agents, Propellants, Agrochemicals, Solvents, Surface Treatment, Pharmaceuticals and Meter Dose Inhalers), By Compound Type (HFCs, HFOs, PFCs, Nitrogen Trifluoride, Sulfur Hexafluoride), By Technology (CVD, Plasma Etching, Solution Polymerization, Suspension Polymerization), By End-Use Industry (Chemical and Petrochemicals, Automotive, Electrical and Electronics, Aerospace, Construction, Consumer Goods, Oil and Gas) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | The Chemours Company, Arkema S.A., Honeywell International Inc., Gujarat Fluorochemicals Limited, Daikin Industries Ltd., 3M Company, Solvay S.A., AGC Inc., Navin Fluorine International Limited, Dongyue Group, Pelchem SOC Ltd |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |