What is the Thermal Interface Materials Market Size?

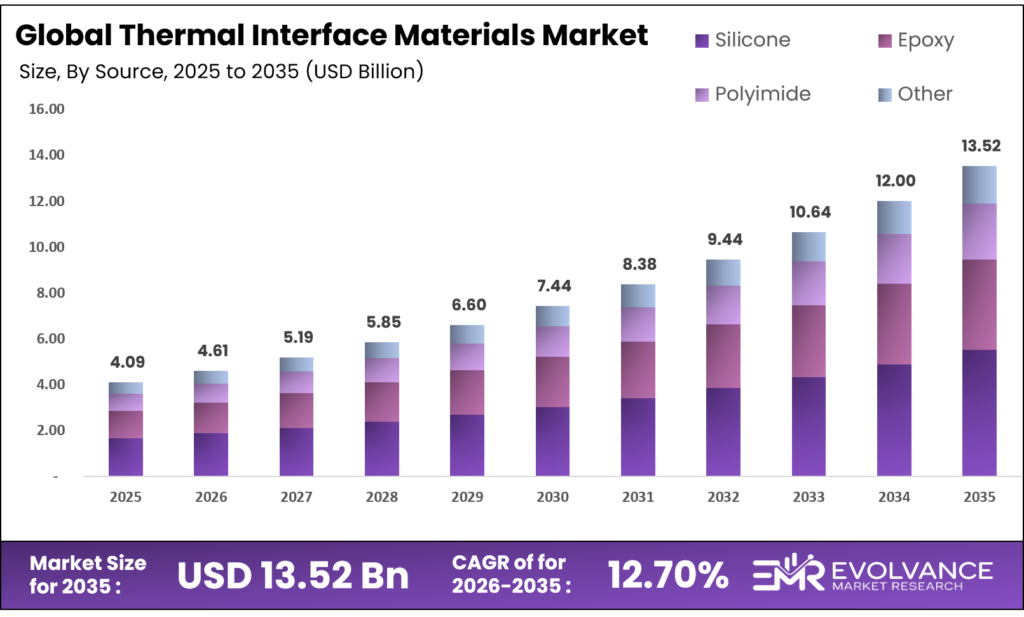

The Global Thermal Interface Materials Market will be worth around USD 13.52 Billion by 2035 from USD 4.09 Billion in 2025, growing at a CAGR of 12.70% during the forecast period 2026 to 2035. EV battery packs and AI accelerator chips are pulling the highest volumes of high-conductivity materials from formulators. Enterprise data center buyers are shifting spend from bulk greases toward precision-dispensed liquid TIMs. Raw material tightness in boron nitride and gallium feedstocks remains a margin pressure point for mid-tier suppliers.

Market Highlights

- The Thermal Interface Materials Market will grow from USD 4.09 Billion in 2025 to USD 13.52 Billion by 2035, at a CAGR of 12.70%.

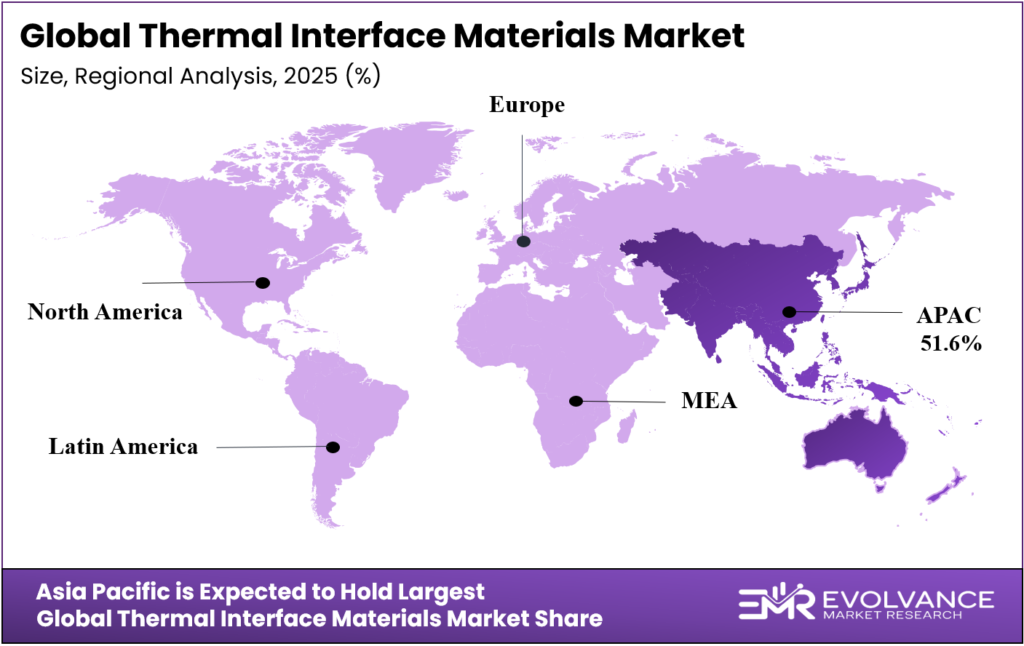

- Asia Pacific leads all regions with a 51.6% share, valued at USD 2.11 Billion.

- Greases and Adhesives dominate the By Type segment with 35.2% share.

- Silicone leads By Material at 54.7%.

- Pastes lead By Form at 41.3%.

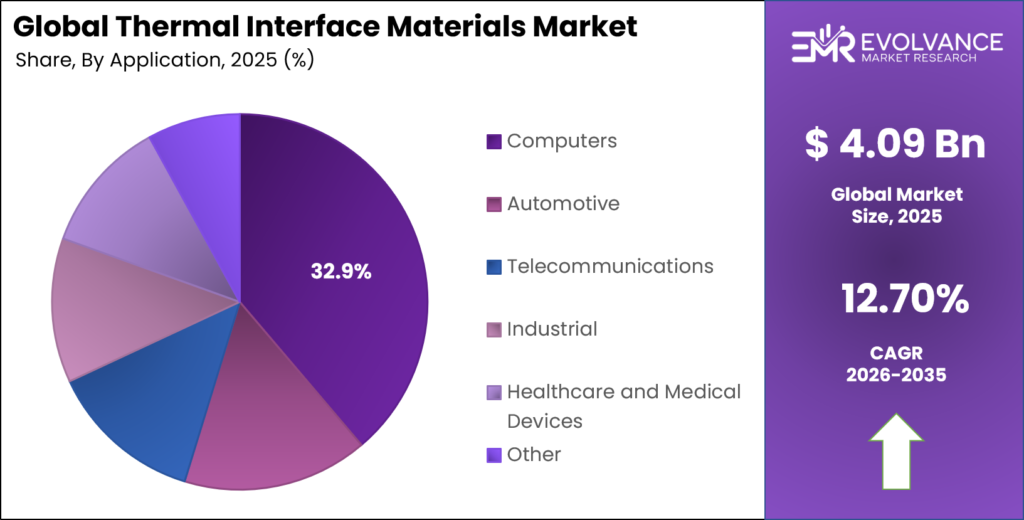

- Computers lead By Application at 32.9%.

- Direct Sales dominates By Distribution Channel at 73.6%.

Market Overview

Thermal interface materials are substances placed between heat-generating components and cooling surfaces to reduce contact resistance and move heat efficiently. They fill microscopic air gaps that act as insulators, enabling reliable thermal transfer in electronics, Electric Vehicles, aerospace, and industrial equipment. Their form, conductivity, and chemical makeup vary widely by end-use requirement.

The materials span greases, adhesives, pads, phase-change compounds, and metal-based solutions. Each form trades off between bond-line control, rework ease, and thermal performance. High-conductivity products above 5 W/m·K are now the baseline expectation in data center and EV applications, pushing formulators to upgrade filler chemistries and depart from older silicone grease standards.

Government programs and enterprise procurement are both directing capital into advanced TIM development. The U.S. DOE and NASA have funded next-generation thermal management projects that set verifiable performance benchmarks. These benchmarks, once published, become buyer specification floors which effectively bars low-performance suppliers from high-value contracts.

According to Coherent, cooling systems can account for up to 50% of a data center’s energy use. This single figure explains why hyperscalers are willing to pay premium prices for materials that cut chip temperatures. A 15°C reduction in chip temperature, as shown by Coherent’s Thermadite platform, directly cuts energy bills and extends hardware life making TIM cost a minor line item against operational savings.

Coherent’s diamond–silicon carbide composite, which achieved isotropic thermal conductivity exceeding 800 W/m·K in 2025, demonstrates that material science limits are being pushed well beyond copper benchmarks. This signals a structural shift: the TIM market is no longer competing on price per kilogram but on thermal performance per watt of cooling energy saved.

Type Insights

Greases and Adhesives dominate with 35.2% due to low cost and broad compatibility.

In 2025, Greases and Adhesives held a dominant market position in the By Type segment of the Thermal Interface Materials Market, with a 35.2% share. Their dominance reflects buyer preference for proven chemistry and low rework cost in electronics assembly. They remain the default choice for PCB-level thermal management where precision dispensing and bond-line control are achievable at scale.

Gap Fillers address uneven or tall component topographies where pastes and films cannot conform reliably. Qnity Electronics reported that the Laird Tflex SF16 gap filler provides 16 W/m·K thermal conductivity, setting a new performance bar for non-silicone formulations. This level of conductivity in a conformable pad format opens gap fillers to 5G base station and EV power module applications previously served by metal-based TIMs.

Phase Change Materials activate at a target temperature, flowing to fill surface irregularities while remaining solid during storage and handling. T-Global Technology’s TG-PCM095 delivers 9.5 W/m·K thermal conductivity among the highest in its category making it competitive against conventional greases without their pump-out and dry-out failure modes over time.

Material Insights

Silicone dominates with 54.7% due to thermal stability and chemical versatility.

In 2025, Silicone held a dominant market position in the By Material segment of the Thermal Interface Materials Market, with a 54.7% share. Silicone’s wide service temperature range, chemical inertness, and compatibility with most substrate materials make it the default carrier fluid and binder for most TIM formulations. Its dominance reflects decades of validated field performance across electronics, automotive, and aerospace environments.

Polyimide carriers are specified for high-temperature and flexible circuit applications, particularly in aerospace avionics and medical wearables. Their electrical insulation properties, combined with dimensional stability under thermal cycling, make them suitable for interfaces where both heat transfer and dielectric isolation are required in a single material layer.

Other materials include carbon-based and hybrid systems such as graphene films, diamond composites, and metal matrix compounds. These are gaining traction in ultra-high-performance applications. Coherent’s diamond–silicon carbide material, delivering 800 W/m·K and roughly 2× the thermal performance of copper, represents the leading edge of this non-silicone, non-polymer segment.

Thermal Conductivity Insights

Medium conductivity (1–5 W/m·K) dominates with 47.1% due to broad industrial fit.

In 2025, Medium (1–5 W/m·K) held a dominant market position in the By Thermal Conductivity segment of the Thermal Interface Materials Market, with a 47.1% share. This range covers most commercial electronics, standard automotive ECUs, and general industrial power supplies. It represents the balance point where thermal performance meets cost accessible to a wide buyer base without requiring exotic filler materials or precision processing.

High (>5 W/m·K) conductivity TIMs are the fastest-moving category by value. AI server operators, EV OEMs, and 5G infrastructure builders are all specifying above-5 W/m·K as a baseline. Henkel’s LOCTITE TCF 14001, launched in 2025, delivers 14.5 W/m·K under ASTM D5470 testing positioned specifically for 800G and 1.6T optical transceiver applications in next-generation AI data centers.

Form Insights

Pastes dominate with 41.3% due to versatile application and proven field performance.

In 2025, Pastes held a dominant market position in the By Form segment of the Thermal Interface Materials Market, with a 41.3% share. Pastes offer the lowest bond-line thickness in practice, maximizing thermal transfer across flat mating surfaces such as CPU heat spreaders, GPU dies, and power transistor flanges. Their compatibility with automated dispensing equipment makes them the default choice in high-volume electronics manufacturing.

Liquids including two-part dispensable TIMs such as Henkel’s LOCTITE TCF 14001 enable high-throughput robotic dispensing and precise volume control. With a 3-hour pot life at 25°C and a 180-day shelf life, TCF 14001 is designed for industrial assembly workflows where scheduling flexibility and inventory management directly affect line efficiency.

Application Insights

Computers dominate with 32.9% due to high chip power density and volume scale.

In 2025, Computers held a dominant market position in the By Application segment of the Thermal Interface Materials Market, with a 32.9% share. The scale of global PC and server production creates consistent, high-volume demand for paste and pad TIMs. AI server deployments are now the highest-value sub-segment, where TIM performance directly affects GPU junction temperatures and sustained compute throughput.

Automotive is the fastest-shifting application by material specification. EV battery management systems, SiC traction inverters, and on-board chargers all require TIMs that survive thousands of thermal cycles under vibration. DOE-funded testing at NREL showed TIM-integrated cooling modules surviving 36,000 power cycles under 100°C delta junction temperature, with thermal degradation staying below the 20% project target.

Healthcare and Medical Devices, Consumer Electronics, LED Lighting, Aerospace and Defense, and Power Electronics each represent distinct thermal management requirements. Aerospace is particularly demanding: NASA’s 2025 SmallSat guidance documents thermal contact conductance values from 0.21 W/K to 3.51 W/K for bolted interfaces, with TIM sheet thicknesses from 0.13 mm to 5 mm underscoring how tight performance tolerances are in space-grade applications.

Distribution Channel Insights

Direct Sales dominate with 73.6% due to specification complexity and volume contracts.

In 2025, Direct Sales held a dominant market position in the By Distribution Channel segment of the Thermal Interface Materials Market, with a 73.6% share. TIMs are application-specific materials that require technical validation before procurement. Buyers rely on direct supplier engagement for application engineering support, qualification testing, and supply agreements. This relationship-driven model concentrates revenue with vendors who invest in field application teams.

Distributors serve smaller buyers, MRO (maintenance, repair, and operations) demand, and markets where direct vendor coverage is thin. Their role is growing in emerging markets and in the aftermarket segment where small-batch, on-demand supply is the norm. Distributors who invest in application knowledge rather than just stocking product command better margins and stickier customer relationships in this segment.

Market Segments Covered in the Report

By Type

- Greases and Adhesives

- Tapes and Films

- Gap Fillers

- Metal-Based TIMs

- Phase Change Materials

- Elastomeric Pads

- Thermal Pads

By Material

- Silicone

- Epoxy

- Polyimide

- Other

By Thermal Conductivity

- High (>5 W/m·K)

- Medium (1–5 W/m·K)

- Low (<1 W/m·K)

By Form

- Pastes

- Films

- Gels

- Liquids

- Pads

By Application

- Computers

- Automotive

- Telecommunications

- Industrial

- Healthcare and Medical Devices

- Consumer Electronics

- LED Lighting

- Aerospace and Defense

- Power Electronics

By Distribution Channel

- Direct Sales

- Distributors

Regional Insights

Asia Pacific Dominates the Thermal Interface Materials Market with a Market Share of 51.6%, Valued at USD 2.11 Billion

Asia Pacific’s 51.6% share worth USD 2.11 Billion reflects the concentration of global electronics manufacturing in China, Japan, South Korea, and Taiwan. These countries host the world’s largest PCB, semiconductor, and consumer electronics assembly lines. This structural manufacturing density means TIM volumes in Asia Pacific are driven by production output, not just end-market demand making the region’s share structurally durable.

North America Market Trends

North America’s position in the TIM market is being reshaped by onshoring of power electronics and semiconductor production. Federal investment through the CHIPS Act and IRA is building domestic chip fab and EV drivetrain capacity. This shift creates a new domestic TIM procurement base that is actively moving away from sole-source Asia-Pacific supply chains a realignment that favors North American and European TIM formulators with local technical support.

Europe Market Trends

Europe’s TIM demand is anchored by automotive OEMs and industrial equipment makers in Germany, France, and Italy. EU Ecodesign regulations under Lot 9 are tightening specifications on server thermal materials, including recyclability requirements for pads and encapsulants. Suppliers unable to meet these requirements face exclusion from EU data center supply chains, giving eco-compliant TIM producers a near-term competitive advantage in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

In the United States, the Department of Energy’s appliance and equipment efficiency standards, updated in 2024–2025, set minimum energy performance targets for data center cooling systems. These standards indirectly mandate better thermal interface performance, as lower system energy use requires tighter chip-to-heatsink resistance. Formulators whose products enable compliance with these targets gain a specification advantage in North American data center procurement.

RoHS 3 (EU Directive 2015/863, enforcement tightened through 2024) restricts lead, mercury, cadmium, and specific phthalates in electronic equipment. Metal-based TIMs using indium or bismuth must demonstrate compliance at the substance level. This adds testing and documentation costs for suppliers costs that small formulators absorb at lower margins than the large chemical companies that already hold compliance infrastructure.

The U.S. National Aeronautics and Space Administration published updated SmallSat Thermal Control guidance in 2025, documenting performance benchmarks for bolted and TIM-assisted interfaces in spacecraft. While not a binding regulation, NASA specifications function as de facto standards in aerospace procurement globally. Any TIM used in satellite or defense electronics is benchmarked against these published values before qualification approval is granted.

Drivers

EV Drivetrain Electrification and AI Accelerator Density Force High-Performance TIM Adoption Across Both Markets

EV battery packs, SiC inverters, and on-board chargers require TIMs that withstand vibration, thermal cycling, and chemical exposure simultaneously. These conditions eliminate most standard greases and pads from the qualified supplier list. OEMs are now writing TIM performance specs not just material specs into platform sourcing agreements, locking in high-value, long-term supply contracts for qualified formulators.

AI accelerator chips generate heat flux that standard solder and grease interfaces cannot dissipate safely. Henkel’s LOCTITE TCF 14001 was designed specifically for 800G and 1.6T optical transceiver applications indicating that hyperscale buyers are specifying TIMs at the transceiver level, not just at the chip level. This signals a broader procurement shift where thermal management is a system-level specification, not an afterthought.

A U.S. Department of Energy project reported a 40% reduction in pressure drop from 12.2 kPa to 7.4 kPa using improved thermal interface strategies in inverter cooling designs. This result demonstrates that TIM optimization directly reduces hydraulic load on cooling systems. For power electronics buyers, that means smaller pumps, lower energy costs, and simpler thermal system design outcomes that justify paying a premium for validated TIM performance.

Restraints

Certification Gaps and Raw Material Price Volatility Constrain Supplier Margin and Buyer Adoption Speed

Long-term reliability certification for reusable TIMs in automotive and aerospace environments remains incomplete for many high-conductivity formulations. Automotive OEMs require TIM qualification data spanning tens of thousands of thermal cycles before approving a material for production. Suppliers without completed reliability datasets cannot enter the automotive qualification pipeline, regardless of their material’s thermal performance.

Boron nitride, aluminum oxide, and gallium are the primary fillers driving high conductivity in premium TIMs. All three face supply chain concentration risks and periodic price spikes tied to mining output and export policy. For mid-tier TIM formulators without vertical supply agreements, a 20–30% spike in filler costs can eliminate profit entirely on fixed-price contracts pushing some suppliers to substitute lower-cost, lower-performance fillers that risk failing buyer qualification.

The reliability gap is especially acute for reusable TIMs in aerospace, where NASA’s 2025 SmallSat guidance documents spacecraft TIM thicknesses from 0.13 mm to 5 mm each requiring separate qualification evidence. The range of required form factors, combined with the cost of qualification testing under vacuum and thermal cycling conditions, means only well-funded suppliers can realistically compete for space-grade contracts.

Growth Factors

Embedded TIM Solutions and Automated Dispensing Workflows Unlock New Revenue in Wearables, Power Modules, and Retrofit Markets

Medical wearable ultrasound patches require biocompatible, low-modulus TIMs that transfer heat away from skin-contact electronics without causing discomfort or irritation over long use periods. No major supplier has a fully commercialized solution for this use case. The first formulator to achieve biocompatibility certification and regulatory clearance for a skin-contact thermal material will secure a high-margin, recurring supply position in a medtech segment with few qualified competitors.

High-voltage power module assembly lines currently lack automated dispensing workflows for thermally conductive adhesives. This process gap forces manual application, which introduces variability in bond-line thickness and risks product failure under thermal stress. Suppliers who develop TIM products optimized for robotic dispensing with rheology and pot life matched to industrial equipment will gain share by solving a process engineering problem, not just a material one.

DOE testing at NREL confirmed that TIM-integrated cooling assemblies survived 36,000 power cycles under a 100°C delta junction temperature with coolant flowing at 4 L/min at 50°C and thermal degradation stayed below the 20% target. In March 2026, Coherent’s Thermadite 800 cold plates reduced chip temperatures by more than 15°C versus copper and weighed roughly 60% less. Both results expand the validated performance range buyers can confidently specify, accelerating adoption in premium segments.

Emerging Trends

Satellite Constellations, Onshoring, and EU Ecodesign Rules Are Reshaping TIM Specification and Supply Chain Strategy

Satellite mega-constellation programs are creating new TIM specifications beyond military standards. Space-grade TIMs must be vacuum-stable with minimal outgassing requirements that disqualify most silicone-based formulations used in ground electronics. NASA’s 2025 SmallSat guidance documents conductance values from 0.21 W/K to 3.51 W/K for bolted interfaces, giving satellite builders a reference range but leaving a clear gap for suppliers to develop materials that exceed these published baselines.

North American onshoring of power electronics manufacturing is actively breaking sole-source dependence on Asia-Pacific TIM supply chains. As domestic chip fab and EV battery plants come online, procurement teams are requiring qualified local or regional TIM sources to meet supply chain resilience mandates. This creates a near-term demand signal for North American and European TIM suppliers who can match the technical specs currently met only by Asian producers.

EU Ecodesign rules under Lot 9 are penalizing non-recyclable thermal pads in IT hardware sold in Europe. This regulation is forcing server OEMs to audit their TIM supply chains and replace non-compliant materials before product launch. Formulators with recyclable or halogen-free products certified under EU Ecodesign requirements have a concrete, regulation-driven specification advantage not a theoretical one in the European enterprise server market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

This report covers the global Thermal Interface Materials Market, defined as all chemical and composite materials applied between heat-generating components and cooling surfaces to reduce thermal contact resistance. Covered product categories include greases, adhesives, tapes, films, gap fillers, metal-based TIMs, phase-change materials, elastomeric pads, and thermal pads across silicone, epoxy, polyimide, and advanced composite chemistries. Market values are reported in constant USD, with 2025 as the base year, to ensure cross-period comparability and eliminate distortion from currency fluctuations. The quantitative scope spans historic data from 2020 to 2024 and a forecast period from 2026 to 2035.

This study excludes standalone active cooling hardware such as heat sinks, fans, liquid cooling loops, and vapor chambers where no interface material is the primary deliverable. It also excludes thermally conductive structural adhesives used primarily for bonding rather than heat transfer, and software-based thermal management tools. Regional and country-level analysis covers North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with primary demand-side coverage focused on electronics, automotive, aerospace, telecommunications, industrial, and healthcare end markets.

Key Companies Insights

Henkel has positioned itself as the high-performance TIM supplier for AI data center hardware through its LOCTITE product line. The LOCTITE TCF 14001 liquid TIM rated at 14.5 W/m·K, dielectric strength of 13 kV/mm, and a 180-day shelf life is purpose-built for 800G and 1.6T optical transceivers. This focus on a specific, fast-scaling hardware segment gives Henkel a specification-in advantage before competitors can qualify alternatives.

3M brings a diversified materials portfolio covering adhesive films, pads, and thermal compounds across electronics, automotive, and industrial markets. Its global manufacturing and distribution reach gives it the supply continuity advantage that large OEM buyers demand for single-source TIM qualification. In markets where supply chain reliability outweighs marginal thermal performance differences, 3M’s infrastructure is a competitive moat that pure-play TIM specialists cannot easily replicate.

Parker Hannifin approaches the TIM market through its motion and control engineering strength, serving industrial and aerospace applications where thermal management is integrated into larger fluid and motion systems. Its position in high-reliability, long-lifecycle markets including defense electronics and power conversion makes it a key vendor for customers who require materials validated for 10-plus-year operational lifetimes under demanding environmental conditions.

Dow competes through its silicone chemistry platform, supplying base polymers and finished TIM formulations across a wide conductivity range. Dow’s upstream integration into silicone monomer production gives it a cost and formulation flexibility advantage that compounders without raw material control cannot match. As high-conductivity filler costs rise, Dow’s ability to adjust silicone matrix chemistry while holding price helps it maintain margin stability where competitors are squeezed.

Key Companies

- Henkel

- 3M

- Parker Hannifin

- Dow

- Shin-Etsu Chemical

- Wacker Chemie

- Momentive

- Fujipoly

- Honeywell Electronic Materials

- Indium Corporation

- Laird Performance Materials (DuPont)

- Boyd Corporation

- Dexerials Corporation

- Sekisui Chemical

- Denka Company Limited

- Kerafol

- NeoGraf Solutions, LLC

- Panasonic

- AI Technology Inc.

- DuPont de Nemours, Inc.

Recent Industry Developments

- In 2025, Coherent introduced a diamond–silicon carbide composite TIM achieving isotropic thermal conductivity exceeding 800 W/m·K approximately 2× the performance of copper targeting AI and HPC cooling applications.

- In March 2026, Coherent announced Thermadite 800 liquid cold plates delivering 800 W/(m·K) conductivity, chip temperature reduction of more than 15°C versus copper, and roughly 60% lower density than copper cold plates.

- In October 2025, Henkel launched LOCTITE TCF 14001, a liquid TIM with 14.5 W/m·K conductivity and dielectric strength of 13 kV/mm, designed for 800G and 1.6T optical transceiver hardware in AI data centers.

- In 2025, Qnity Electronics announced the Laird Tflex SF16 gap filler providing 16 W/m·K thermal conductivity positioning it among the highest-conductivity non-silicone pad TIMs available to the market.

- In December 2025, T-Global Technology launched TG-PCM095, a phase-change TIM with 9.5 W/m·K conductivity described as among the highest values in the phase-change material category.

- In 2025, a U.S. DOE-funded project reported a 40% reduction in inverter cooling pressure drop from 12.2 kPa to 7.4 kPa and a 68.7% reduction in temperature spread between power switches, using optimized TIM-integrated cooling assemblies.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 4.09 Billion |

| Forecast Revenue (2035) | USD 13.52 Billion |

| CAGR (2026-2035) | 12.70% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Greases and Adhesives, Tapes and Films, Gap Fillers, Metal-Based TIMs, Phase Change Materials, Elastomeric Pads, Thermal Pads), By Material (Silicone, Epoxy, Polyimide, Other), By Thermal Conductivity (High >5 W/m·K, Medium 1–5 W/m·K, Low <1 W/m·K), By Form (Pastes, Films, Gels, Liquids, Pads), By Application (Computers, Automotive, Telecommunications, Industrial, Healthcare and Medical Devices, Consumer Electronics, LED Lighting, Aerospace and Defense, Power Electronics), By Distribution Channel (Direct Sales, Distributors) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Henkel, 3M, Parker Hannifin, Dow, Shin-Etsu Chemical, Wacker Chemie, Momentive, Fujipoly, Honeywell Electronic Materials, Indium Corporation, Laird Performance Materials (DuPont), Boyd Corporation, Dexerials Corporation, Sekisui Chemical, Denka Company Limited, Kerafol, NeoGraf Solutions LLC, Panasonic, AI Technology Inc., DuPont de Nemours Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |