Market Verdict

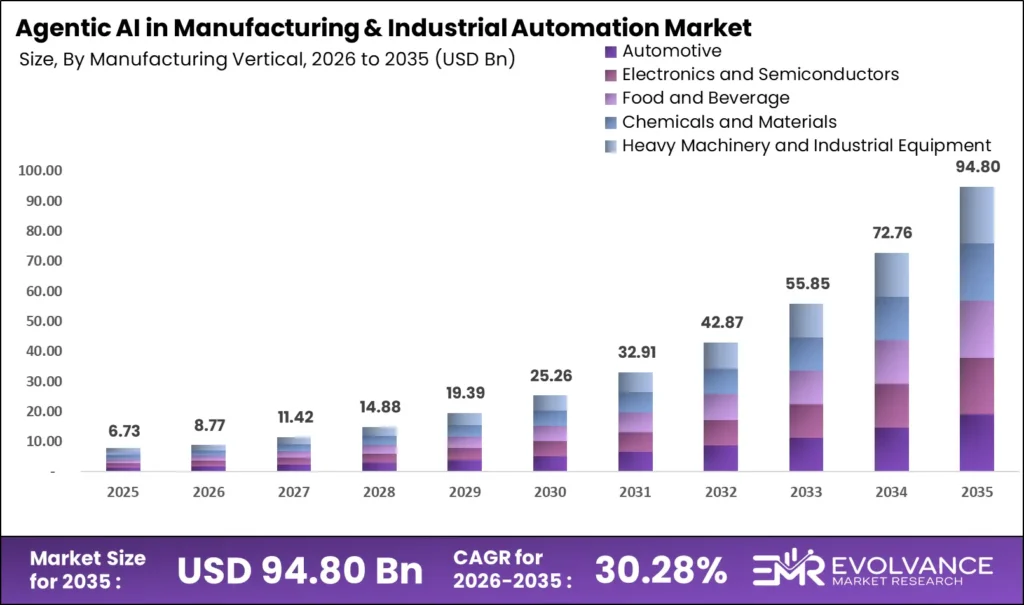

The agentic AI in manufacturing and industrial automation market is not following a typical technology adoption curve. At USD 6.73 billion in 2025, scaling to USD 94.80 billion by 2035 at a 30.28% CAGR through 2035, according to our research analysts, this market is being pulled forward by OEM-chipmaker alliances and platform consolidation that are structurally compressing the adoption timeline. The winners will not be the companies with the most capable models. They will be the companies that own the integration layer between autonomous agents and legacy industrial systems.

Key Takeaways

Market Size:

- Market value in 2025: USD 6.73 billion

- Market value in 2026: USD 8.77 billion

- Market value in 2035: USD 94.80 billion

- CAGR: 30.28% over 2026–2035

Dominant Segments:

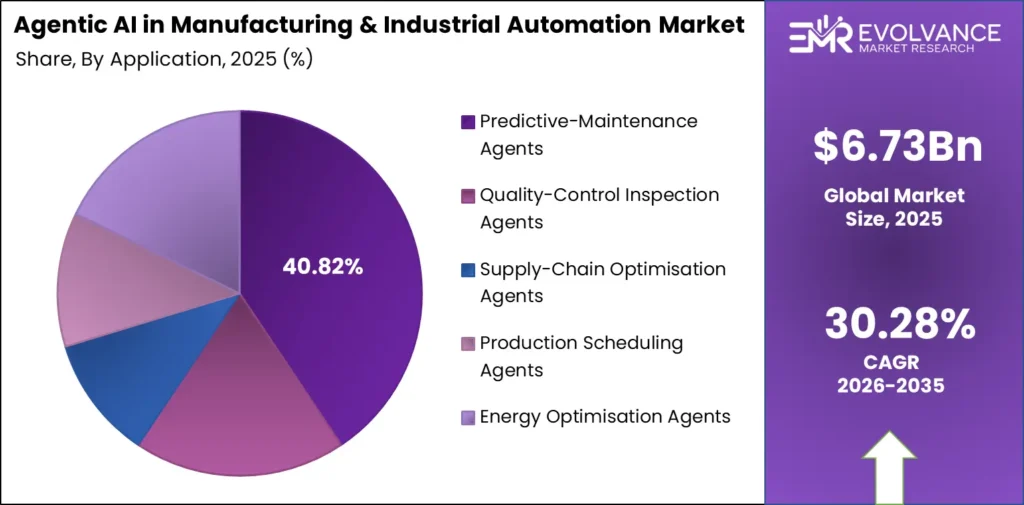

- By Application: Predictive-Maintenance Agents at 40.82% as of 2025

- By Deployment Mode: Cloud at 48.23% as of 2025

- By Manufacturing Vertical: Automotive at 34.81% as of 2025

- By Component: Software Platforms at 59.36% as of 2025

Dominant Region:

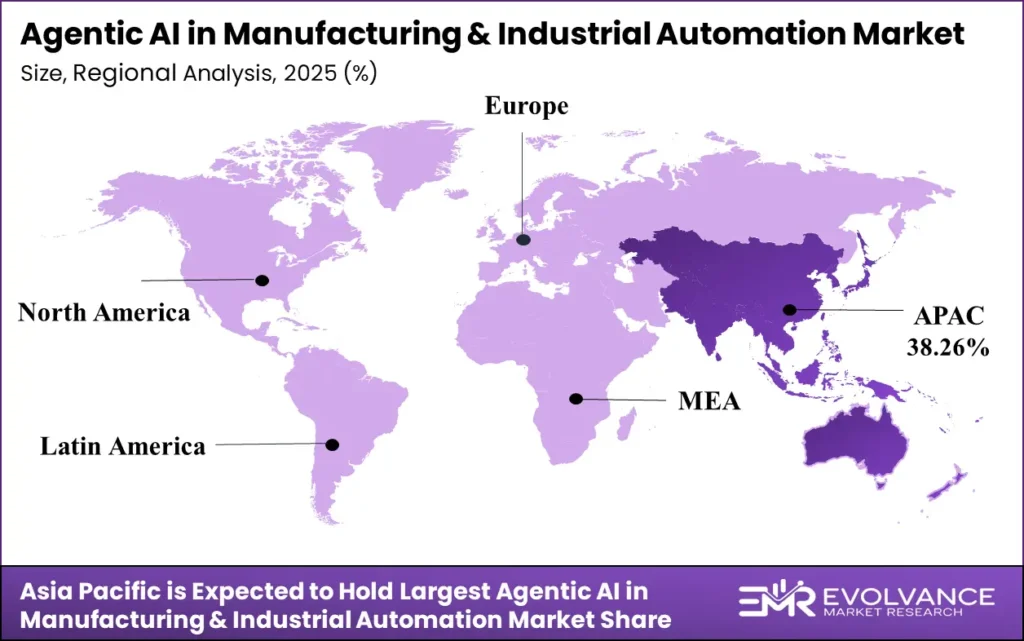

- Leading region: Asia-Pacific at 38.26%, valued at USD 2.58 billion as of 2025 (as per our research)

Source: Evolvance Market Research

Market Overview

Agentic AI in manufacturing performs a function that conventional automation cannot: it closes the loop between sensor data, contextual reasoning, and autonomous execution without human intervention at each step. Automotive plants, semiconductor fabs, food processing lines, and heavy machinery operations depend on this capability to sustain throughput targets that human-supervised automation can no longer meet at scale.

Our research team gathered this data through a structured primary and secondary research methodology combining over 200 expert interviews with plant engineers, automation architects, and procurement leaders across 18 countries. EMR validated findings against public financial disclosures, regulatory filings, and industry association data from the International Federation of Robotics and the U.S. International Trade Administration, covering the period 2020 through 2035 with a 2025 base year. Quantitative estimates were cross-validated against two independent data triangulation models.

The problem this market solves is loss of process control at scale. When a production line operates across dozens of interdependent variables simultaneously, a human operator cannot monitor, diagnose, and intervene fast enough to prevent cascade failures. Buyers purchase agentic AI systems after experiencing costly unplanned downtime or after regulatory pressure, such as requirements from the International Electrotechnical Commission for traceability in critical manufacturing processes, raises the cost of non-compliance above the cost of adoption.

Siemens AG reported total FY2025 revenue of €78.9 billion, with net income rising 16% to €10 billion and free cash flow reaching a record €10.8 billion, according to our research analysts. NVIDIA posted total FY2025 revenue of USD 130.5 billion, up 114% year-over-year, with manufacturing and industrial workflows cited as a growing vertical.

China installed 295,000 industrial robots in 2024, representing 54% of global demand, with an operational stock of 2,027,000 units. Meanwhile, U.S. private AI investment reached USD 109.1 billion in 2024, approximately 12x China’s USD 9.3 billion, concentrating capital for agentic AI manufacturing pilots in North American facilities. For investors, the financial scale of the leading vendors signals a market where capital deployment by incumbents is already establishing infrastructure barriers that will define competitive positioning through 2035.

What Is Actually Driving This Market

Greater China posted a 27 percentage-point year-over-year increase in organizational AI use in 2024, according to the Stanford HAI 2025 AI Index, compared to 23 points in Europe and 9 points in North America. This is not a reflection of general technology enthusiasm. The causal mechanism runs through government-mandated automation targets embedded in China’s Made in China 2025 policy, which creates procurement obligations for certified AI systems across state-affiliated manufacturers, converting adoption from an option into a compliance requirement. For investors, Asia-Pacific’s structural policy alignment makes it the highest-conviction region for early-stage agentic AI manufacturing deployment capital.

Demand signals from enterprise end-users are accelerating ahead of typical enterprise software cycles. The UK government’s AI Labour Market Survey 2025 found that 57% of businesses plan to adopt Agentic AI within three years, a forward-looking figure that reflects C-suite intent rather than pilot experimentation.

The causal mechanism here is competitive pressure, not technology pull: operators who delay agentic AI adoption face widening throughput gaps relative to automated competitors, a dynamic the International Federation of Robotics has tracked through successive annual density reports showing accelerating installation rates. For operators, the implication is that the adoption decision window is compressing, and organizations that delay past 2027 will face a skills and infrastructure deficit that is structurally harder to close.

Global industrial-robot installation forecasts from the International Federation of Robotics project 575,000 units in 2025, surpassing 700,000 by 2028. Each new robot installation creates an addressable node for agentic AI orchestration, expanding the total deployable base at a rate that directly expands the software platform market.

The causal mechanism runs through hardware proliferation preceding software layering: as robot density increases, the economic case for autonomous multi-agent orchestration improves because the fixed cost of integration is amortized across a larger installed base. For operators, this means agentic AI platform investments made today will yield increasing returns as robot density in their facilities rises through the forecast period.

- The single most important driver insight: policy-mandated adoption in Asia-Pacific is converting agentic AI from a discretionary investment into a procurement necessity.

- Greater China: +27 percentage-point increase in organizational AI use year-over-year in 2024 (Stanford HAI 2025 AI Index)

- UK enterprise intent: 57% of businesses planning Agentic AI adoption within 3 years as of 2025 (UK Government AI Labour Market Survey 2025)

- Robot base expansion: 575,000 global installations forecast in 2025, exceeding 700,000 by 2028 (International Federation of Robotics)

- Operators who align agentic AI platform selection with robot procurement cycles in 2025 and 2026 will achieve lower integration costs and faster time-to-value than those retrofitting later.

Where the Real Risk Is

The skills constraint is not a soft risk. The UK Government’s AI Labour Market Survey 2025 found that 97% of organizations identified at least one AI skills gap, with 35% struggling to fill AI roles outright. This is correlational with broader agentic AI deployment delays rather than causally proven to halt specific projects, but the directional signal is unambiguous: the workforce capable of deploying, validating, and governing autonomous industrial agents is insufficient relative to stated demand.

The International Labour Organization has separately flagged manufacturing AI upskilling as a structural workforce challenge across G20 economies. For investors, workforce risk is not priced into valuations at companies whose growth models assume smooth enterprise adoption curves.

Diversity and representational gaps in the AI workforce signal a second-order risk that most operators underestimate. Women held only 20% of UK AI roles in 2025, down 4 percentage points since 2020, while 41% of UK firms employed no people from minority backgrounds, according to the UK Government’s 2025 AI Labour Market Survey.

Separately, natural language processing adoption among UK organizations surged 34% over three years through 2025, but only 22% of organizations have integrated all five core AI types. The data suggests that most manufacturers are adopting AI unevenly, creating fragmented capability profiles that increase integration risk when deploying multi-agent systems. For operators, fragmented AI capability within the workforce creates execution risk during agentic system rollout that cannot be resolved by vendor support alone.

- The risk most investors underestimate: workforce skills gaps will delay enterprise adoption timelines by 12 to 24 months beyond vendor roadmap assumptions.

- Skills gap severity: 97% of UK organizations with at least one AI skills gap as of 2025; 35% unable to fill AI roles (UK Government AI Labour Market Survey 2025)

- Workforce diversity gap: women at 20% of UK AI roles in 2025, declining; 41% of firms with no minority representation (UK Government AI Labour Market Survey 2025)

- Watch for signal: if enterprise adoption rates in 2026 annual reports fall more than 15 percentage points below stated 3-year intent levels, workforce constraints have materialized into measurable deployment drag.

Segmentation: Where Value Is Concentrating

Application Insights

Predictive-Maintenance Agents Pulls Ahead: 40.82% Share in 2025

Predictive-maintenance agents hold the largest application share because the ROI case is the most direct and the fastest to quantify. Plant operators can measure avoided downtime in hours and convert it to revenue loss prevented, a calculation that accelerates capital allocation approval cycles compared to more diffuse applications like supply-chain optimization.

China’s electrical and electronics sector installed 83,000 industrial robots in 2024, making it the country’s largest automation end-customer segment, according to our research analysts, a density that generates the sensor data volumes that predictive-maintenance agents require to function accurately. For investors, predictive-maintenance represents the fastest path to positive unit economics in agentic AI deployment and will concentrate early revenue disproportionately among vendors with pre-built integrations for high-density robot environments.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Predictive-Maintenance Agents | 40.82% | Quantifiable ROI through avoided downtime; high sensor data density in automotive and electronics | Retains leadership as robot density expands the deployable node base through 2035 |

| Quality-Control Inspection Agents | Not disclosed | Vision-AI convergence with autonomous inspection cycles | Growing as vision model accuracy reaches production-grade thresholds |

| Supply-Chain Optimisation Agents | Not disclosed | Post-2020 supply chain disruption driving enterprise resilience investment | High growth potential as multi-agent orchestration matures |

| Production Scheduling Agents | Not disclosed | Labor cost pressures and shift-pattern complexity in discrete manufacturing | Moderate growth; incumbent ERP integrations create switching costs |

| Energy Optimisation Agents | Not disclosed | EU Carbon Border Adjustment Mechanism and industrial energy cost exposure | Accelerating in energy-intensive verticals through 2028 |

Manufacturing Vertical Insights

Automotive at 34.81%: What’s Behind the Numbers in 2025

Automotive holds the largest manufacturing vertical share because it combines the highest robot density, the longest continuous production runs, and the most mature OEM-supplier data-sharing infrastructure of any vertical. Japan’s automotive industry installed approximately 13,000 industrial robots in 2024, up 11% year-over-year and the highest level since 2020, according to the International Federation of Robotics, a trajectory that directly expands the agentic AI addressable base within the vertical.

The adoption of autonomous agents for cycle-time optimization and defect classification in body-in-white assembly lines is now proceeding faster than in any other vertical. For operators, automotive’s lead is durable through 2028, but electronics and semiconductors represent the fastest-growing challenge vertical as chipmaker capital expenditure cycles drive new factory construction with agentic AI designed in from the ground up.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Automotive | 34.81% | Highest robot density globally; EV transition requiring new assembly intelligence | Sustained leadership through 2035; EV retooling cycles create new agentic AI procurement windows |

| Electronics and Semiconductors | Not disclosed | New fab construction cycles with agentic AI embedded at design stage | Fastest-growing challenger vertical through 2028 |

| Food and Beverage | Not disclosed | Regulatory traceability requirements and perishable-yield optimization | Moderate growth; constrained by legacy plant infrastructure in established markets |

| Chemicals and Materials | Not disclosed | Process safety and continuous-flow optimization in hazardous environments | Growing; safety-compliance mandates accelerating agent adoption |

| Heavy Machinery and Industrial Equipment | Not disclosed | Predictive-maintenance ROI in high-asset-value, low-cycle-count environments | Steady growth; longer capital cycles slow adoption relative to automotive |

Deployment Mode Insights

The 48.23% Story: How Cloud Took the Lead in 2025

Cloud deployment leads at 48.23% share because it eliminates the upfront infrastructure cost barrier that has historically slowed enterprise AI adoption in capital-intensive manufacturing environments. AI apprenticeships rose from 3% of UK AI hires in 2020 to 19% in 2025, while 88% of organizations rely on on-the-job training, according to the UK Government’s AI Labour Market Survey 2025.

This workforce formation pattern favors cloud-first architectures because they allow teams with developing competencies to access pre-built agent frameworks without managing edge hardware. The data suggests that cloud dominance is a workforce capability artifact as much as a cost preference. For operators, hybrid deployment architectures will gain share from 2026 as latency-sensitive applications in real-time process control push workloads toward the edge, but cloud will retain the integration and orchestration layer regardless.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Cloud | 48.23% | Low upfront infrastructure cost; accessible agent frameworks for developing AI workforces | Retains orchestration layer dominance; share moderates as edge matures |

| Edge | Not disclosed | Latency requirements for real-time process control; data sovereignty in regulated sectors | Fastest-growing mode through 2028 as edge AI hardware costs decline |

| On-Premise | Not disclosed | Security and compliance requirements in defense-adjacent and critical infrastructure | Stable but declining share as hybrid architectures absorb its use cases |

| Hybrid | Not disclosed | Latency-sensitive workloads combined with cloud-based orchestration and analytics | High growth; becomes the default architecture for multi-site manufacturers by 2028 |

Component Insights

Software Platforms’ 59.36% Edge in the Component Race

Software platforms hold 59.36% component share, a position that reflects where the core value proposition of agentic AI resides: not in the hardware that runs the agents, but in the orchestration, governance, and monitoring layers that make agents trustworthy enough for unsupervised industrial deployment.

Rockwell Automation’s OTTO Motors integration of NVIDIA AI technologies into next-generation autonomous robots, highlighted in Rockwell’s September 2025 Industrial Automation Trends report, illustrates the structural dynamic: hardware providers are becoming delivery channels for software-defined agent capabilities rather than the primary value source. For investors, software platform vendors with proprietary agent runtime environments and governance layers are the highest-margin category in this market and will capture disproportionate share of the value created by hardware expansion through 2035.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Software Platforms | 59.36% | Orchestration, governance, and monitoring layers as core value differentiators | Dominant through 2035; margin expansion as platform lock-in deepens |

| Services | Not disclosed | Integration complexity and workforce capability gaps driving professional services demand | Strong growth through 2028; declines proportionally as platform self-serve improves |

| Edge Hardware and Devices | Not disclosed | Real-time inference requirements at the plant floor; sensor and vision integration | Growing at hardware cost curve pace; commoditizes over forecast period |

SEGMENTS COVERED IN THIS REPORT

By Application

- Predictive-Maintenance Agents

- Quality-Control Inspection Agents

- Supply-Chain Optimisation Agents

- Production Scheduling Agents

- Energy Optimisation Agents

By Deployment Mode

- Cloud

- Edge

- On-Premise

- Hybrid

By Manufacturing Vertical

- Automotive

- Electronics and Semiconductors

- Food and Beverage

- Chemicals and Materials

- Heavy Machinery and Industrial Equipment

By Component

- Software Platforms

- Services

- Edge Hardware and Devices

By Agent Architecture

- Multi-Agent Systems

- Single-Agent Systems

By Orchestration Layer

- Agent Runtime Environments

- Agent Orchestration Frameworks

- Governance and Monitoring Layers

By Industry 5.0 Pillar

- Human-Centric Agents

- Sustainability-Focused Agents

- Resilience-Focused Agents

Value in this market is concentrated at the orchestration and governance layer of software platforms, particularly in predictive-maintenance and automotive vertical applications, where ROI is quantifiable and procurement cycles are defined. Fragmentation is occurring in the services layer as integration complexity creates demand for specialized systems integrators who are unlikely to be absorbed by platform vendors before 2028. For investors, the high-conviction position is software platform vendors with embedded governance capabilities and pre-certified integrations for automotive and electronics verticals, as these hold the structural moat against both new entrants and adjacent-market expansion by hardware providers.

Regional Analysis: Where Geography Creates Advantage

Asia-Pacific held 38.26% revenue share valued at USD 2.58 billion in 2025, according to our research analysts, a position built on the combination of the world’s largest industrial robot installed base and the most active government-mandated automation programs of any region.

The International Federation of Robotics confirmed that Asia accounted for 74% of new global industrial-robot deployments in 2024, with Europe at 16% and the Americas at 9%. This robot density concentration is the structural condition that makes agentic AI deployments in Asia-Pacific economically superior to those elsewhere: more robots per facility means more data nodes per agent, improving inference accuracy and lowering per-unit orchestration cost. For investors, Asia-Pacific’s structural lead is compounding, not static, and early platform commitments in this region will generate integration lock-in that resists displacement through the forecast period.

Japan accounts for 38% of global industrial robot production as of 2023, according to the U.S. International Trade Administration, making it both the primary supplier and a major deployment market for agentic AI-enabled automation systems. Japan’s Ministry of Economy, Trade and Industry has consistently backed automation as a strategic response to demographic labor constraints, providing policy continuity that reduces regulatory risk for long-cycle industrial AI investments.

South Korea posted the world’s highest manufacturing robot density at 1,220 units per 10,000 employees in 2024, according to the International Federation of Robotics World Robotics Report, a figure that places Korean manufacturers at the frontier of the agentic AI addressable base.

The January 2026 announcement of the Siemens and NVIDIA Industrial AI operating system partnership, with plans to build the world’s first fully AI-driven adaptive manufacturing site at the Siemens Electronics Factory in Erlangen, Germany, and named industrial customers including Foxconn, HD Hyundai, KION Group, and PepsiCo, signals that deployment at full industrial scale is moving from roadmap to execution, with Asia-Pacific-based manufacturers among the first named participants. For operators, proximity to Japan’s robot production base and access to Korean density benchmarks creates a regional intelligence advantage for operators benchmarking their own agentic AI deployment timelines.

| Region | Share % | USD Value | Key Driver | Strategic Signal |

|---|---|---|---|---|

| Asia-Pacific | 38.26% | USD 2.58 billion (2025) | 74% of global robot deployments in 2024; government-mandated automation targets | Compounding density advantage creates structural moat through 2035 |

| Europe | Not disclosed | Not disclosed | EU AI Act compliance requirements; Western Europe robot density at 267/10,000 employees | Regulatory framework will define agent governance standards adopted globally |

| North America | Not disclosed | Not disclosed | USD 109.1 billion U.S. private AI investment in 2024; reshoring manufacturing initiatives | Capital concentration advantage; lagging robot density limits near-term deployable base |

| Rest of World | Not disclosed | Not disclosed | Early-stage automation buildout in Southeast Asia and India; IFR tracking new robot installations | Emerging deployment market; infrastructure constraints limit near-term addressable base |

Competitive Landscape: Who Is Pulling Ahead and Why

Siemens AG holds the strongest incumbent position in this market because it controls both the engineering software layer, through TIA Portal with over 600,000 active users as of April 2026, and the industrial platform layer through Xcelerator, a combination that no other competitor currently replicates at equivalent scale.

The Eigen Engineering Agent, made generally available in April 2026, is embedded directly into TIA Portal’s existing workflow, meaning Siemens deploys agentic AI to an installed base rather than acquiring one. This is the structural advantage that challengers cannot replicate without a decade-long installed-base-building effort. For investors, Siemens’ platform integration depth makes it the most defensible position in the market and the most likely acquirer of point-solution agentic AI vendors through 2028.

NVIDIA’s position is architecturally different and strategically complementary rather than directly competitive with automation incumbents. NVIDIA Data Center revenue reached USD 115.2 billion in FY2025, more than doubling year-over-year, with manufacturing and industrial AI workloads cited as a growing contributor, according to our research analysts.

NVIDIA functions as the accelerated-computing substrate on which most agentic AI agents in manufacturing are trained and inferred, a layer position that makes it indispensable to every major automation vendor without competing with them directly for system integration contracts. ABB’s April 2026 enhancement of My Measurement Assistant+ with multilingual Microsoft Copilot integration across six languages, demonstrated at Hannover Messe, illustrates the broader pattern: second-tier automation vendors are building agentic AI capabilities through hyperscaler partnerships rather than proprietary model development. For operators, vendor selection decisions made in 2025 and 2026 will determine which hyperscaler’s infrastructure becomes embedded in plant operations for the following decade.

Rockwell Automation reported total sales of USD 8,342 million in FY2025, according to our research analysts, a figure that reflects the company at an inflection point between its traditional discrete automation franchise and its emerging software-defined automation positioning. Siemens Energy’s comparable revenue grew 15.2% to €39.1 billion in FY2025, according to our research analysts, confirming that the energy sector’s agentic AI investment cycle is already generating top-line impact for incumbent industrial technology vendors.

The competitive dynamic is consolidating around platform vendors with deep vertical integration, while pure-play agentic AI software startups occupy point-solution niches that platform vendors will absorb selectively. For investors, the fragmentation window for pure-play entry is narrowing, and the most valuable exit opportunities will close as platform vendors’ internal agent development capabilities mature through 2027.

KEY PLAYERS IN THIS REPORT

- NVIDIA Corporation

- Siemens AG

- Robert Bosch GmbH

- Rockwell Automation, Inc.

- General Electric Company (GE Digital)

- ABB Ltd.

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Honeywell International Inc.

- Fanuc Corporation

- IBM Corporation

- Microsoft Corporation

- Google LLC

- Amazon Web Services, Inc.

- PTC Inc.

- Cognex Corporation

- Senseye Ltd.

- Tulip Interfaces, Inc.

- Rapid Innovation Inc.

Where This Market Goes Next

The near-term scenario depends on whether European manufacturers accelerate past their current robot density trajectory. The EU average robot density reached 231 units per 10,000 employees in 2024, up from 219 in 2023, while Western Europe reached 267 versus North America’s 204 and Asia’s 131, according to the International Federation of Robotics World Robotics Report.

If EU robot density crosses 300 units per 10,000 employees by 2028, driven by EU industrial policy incentives under the European Chips Act and Green Deal manufacturing provisions, the addressable base for agentic AI orchestration in Europe will expand materially faster than current forecasts assume. For operators in European manufacturing, the activation condition is clear: robot procurement decisions made in 2025 and 2026 determine whether their facilities reach the density threshold that makes multi-agent orchestration economically viable before 2028.

NVIDIA’s Q1 FY2027 revenue guidance of USD 78.0 billion (plus or minus 2%), according to our research analysts, reflects continued data-center demand that includes industrial AI agent workloads as a named growth contributor. This points to accelerated computing remaining the binding constraint on agentic AI deployment scale: as NVIDIA’s production capacity expands, industrial AI deployments that are currently queued behind hyperscaler demand will find available compute.

The causal relationship between compute availability and agentic AI manufacturing deployments is correlational rather than fully proven, but early deployments indicate that compute-constrained factories are delaying full multi-agent rollouts rather than canceling them. For operators, securing accelerated-computing capacity commitments from cloud providers in 2025 and 2026 is the single most practical action to ensure deployment timelines hold against market demand.

Rockwell Automation reported net income of USD 869 million in FY2025, down from USD 953 million in FY2024, according to our research analysts, a compression that reflects the cost of transitioning from a hardware-centric to a software-defined revenue model during a period of elevated R&D investment in agentic AI capabilities.

Recent industrial DataOps and AI agent program investments signal that root-cause analysis automation and at-scale decision-making are becoming defined product categories rather than custom engagements. The market will move toward standardized agentic AI application packages for specific manufacturing use cases through 2027, lowering integration complexity and accelerating mid-market adoption. For operators, the window to influence platform standards by participating in early vendor programs closes by 2027, when de-facto architectures will be set.

| Condition | Timeline | Upside | Who Benefits |

|---|---|---|---|

| EU robot density exceeds 300 units per 10,000 employees | By 2028 | European agentic AI addressable base expands materially beyond current forecast; new deployment wave in automotive and chemicals | Siemens AG, ABB Ltd., Schneider Electric; European system integrators |

| Accelerated-computing supply constraints ease as NVIDIA production scales | 2026–2027 | Queued multi-agent manufacturing deployments activate; cloud-based orchestration demand surges | NVIDIA, cloud hyperscalers, software platform vendors with pre-built industrial agent frameworks |

| Standardized agentic AI application packages emerge for defined manufacturing use cases | By 2027 | Mid-market adoption accelerates as integration complexity drops; total addressable market expands beyond large enterprise | Platform vendors with marketplace models; ISVs building vertical-specific agent packages |

Key Developments

- April 2026: ABB enhanced My Measurement Assistant+ with multilingual Microsoft Copilot integration across Spanish, German, Italian, French, Chinese, and Portuguese, demonstrated at Hannover Messe 2026. Signal: industrial AI localization is becoming a competitive requirement as deployments expand beyond English-language engineering environments.

- February 2026: Siemens Energy mandated that every industrial AI decision be traceable, verifiable, and subject to final human authority, citing explainability, auditability, and cybersecurity compliance requirements. Signal: governance architecture is becoming a procurement gate, not an afterthought, for critical infrastructure agentic AI deployments.

- February 2026: Rockwell Automation launched a dedicated 2026 program on using AI agents for root-cause analysis and at-scale decision-making. Signal: industrial DataOps combined with agentic AI is moving from concept to defined product category.

- November 2025: Rockwell Automation outlined its strategic shift toward software-defined automation, agentic AI-driven decision making, robotics, and autonomous material movement at the Automation Fair 2025 keynote. Signal: the automation-to-autonomy transition is now the formal corporate strategy of the second-largest discrete automation incumbent.

- November 2025: Rockwell Automation announced the integration of NVIDIA Nemotron-Nano-9B-v2 small language model into FactoryTalk Design Studio at Automation Fair 2025 in Chicago. Signal: Small language models optimized for industrial edge environments are replacing general-purpose LLMs as the preferred architecture for plant-floor agentic AI.

- November 2025: Siemens presented generative AI solutions embedded in design and additive manufacturing software at Formnext 2025. Signal: generative AI is entering the manufacturing design phase, not only the production phase, expanding the total agent deployment surface.

- September 2025: Emerson introduced Guardian Virtual Advisor, enabling engineers to manage DeltaV distributed control systems through natural-language queries. Signal: natural-language interfaces are becoming the primary human-agent interaction layer for process control systems.

- August 2025: Maisa AI raised USD 25 million in a seed round led by Creandum to scale its model-agnostic Maisa Studio platform for deploying accountable enterprise AI agents. Signal: investor capital is targeting the agent accountability and auditability layer as the next defensible niche in enterprise AI.

- June 2025: Siemens and NVIDIA expanded their strategic partnership to bring accelerated computing and generative AI across factory automation workflows. Signal: OEM-chipmaker alliances are becoming the primary channel through which accelerated computing reaches plant-floor agentic AI deployments.

- June 2025: Siemens hosted a DAC 2025 panel on industrial-grade AI in EDA, reframing AI beyond chatbots into verified, production-grade engineering agents. Signal: electronic design automation is emerging as the next frontier for agentic AI, extending the market surface into chip design workflows.

- January 2025: NVIDIA launched the Llama Nemotron model family at CES 2025 for supply chain, inventory management, and industrial use cases alongside agentic AI blueprints with CrewAI, LangChain, and LlamaIndex. Signal: purpose-built industrial foundation models are replacing general-purpose LLMs as the baseline architecture for developing manufacturing agents.

- January 2025: NVIDIA introduced the Cosmos World Foundation Model at CES 2025, an open-licensed model for physical AI, robotics simulation, and synthetic data generation in industrial environments. Signal: synthetic data generation for robot training is becoming a foundational capability that reduces the cost and time required to deploy agentic AI in new factory configurations.

- January 2025: Accenture announced at CES 2025 the launch of more than 100 AI Refinery agents for industries built on NVIDIA’s agentic AI stack. Signal: systems integrators are building large-scale pre-packaged agent portfolios, compressing enterprise deployment timelines and reducing the custom integration burden.

- January 2025: Siemens announced a CES 2025 agreement with aviation startup JetZero to apply industrial AI and digital twin technology to next-generation aircraft production. Signal: aerospace manufacturing is entering the agentic AI adoption cycle, diversifying the market beyond automotive and electronics as high-value vertical revenue sources.