Market Verdict

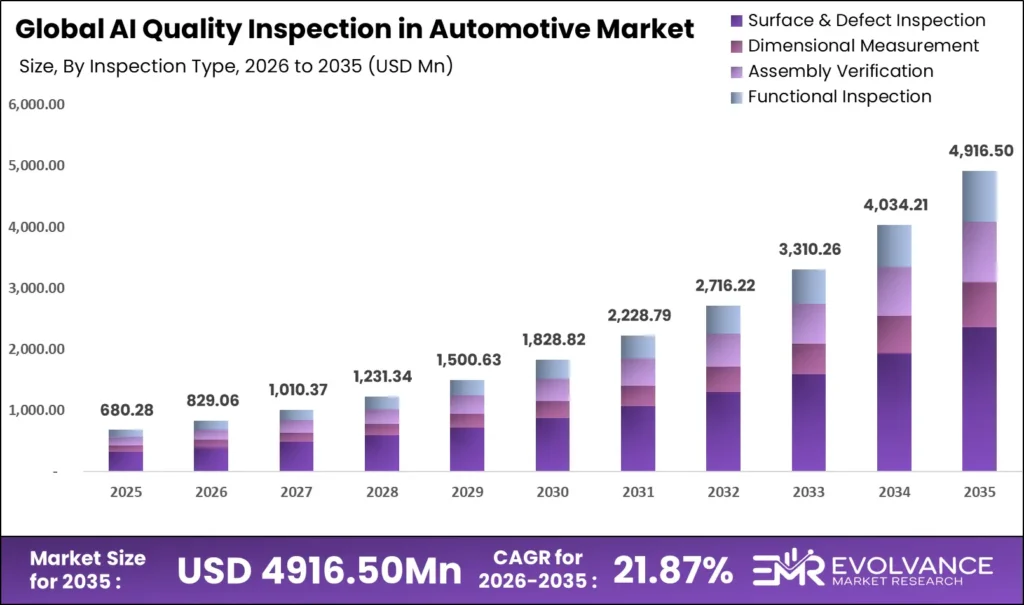

At USD 829.06 million in 2026, the AI quality inspection in automotive market is not a nascent experiment. It is a consolidating industrial segment where capital has already moved, and production lines are already rewired, according to our research analysts. The market reaches USD 4,916.50 million by 2035 at a CAGR of 21.87%, a pace that reflects mandatory quality mandates in OEM contracts and the structural impossibility of meeting sub-200ms cycle time requirements through manual inspection. Asia Pacific leads with 43.5% revenue share, valued at USD 360.64 million as of 2026 per our research, and the region that controls volume production controls the inspection investment cycle.

Key Takeaways

- Market Size:

- Market value 2026: USD 829.06 million

- Market value 2035: USD 4,916.50 million

- CAGR 2026 to 2035: 21.87%

- Dominant Segments:

- Component: Hardware at 77.62% revenue share as of 2025

- Vehicle Type: Passenger Cars at 78.84% revenue share as of 2025

- End Use: OEM at 68.93% revenue share as of 2025

- Deployment Mode: On-Premises at 69.18% revenue share as of 2025

- Technology: Computer Vision at 41.58% revenue share as of 2025

- Inspection Type: Surface & Defect Inspection at 47.18% revenue share as of 2025

- Application: Body-in-White Inspection at 42.4% revenue share as of 2025

- Dominant Region:

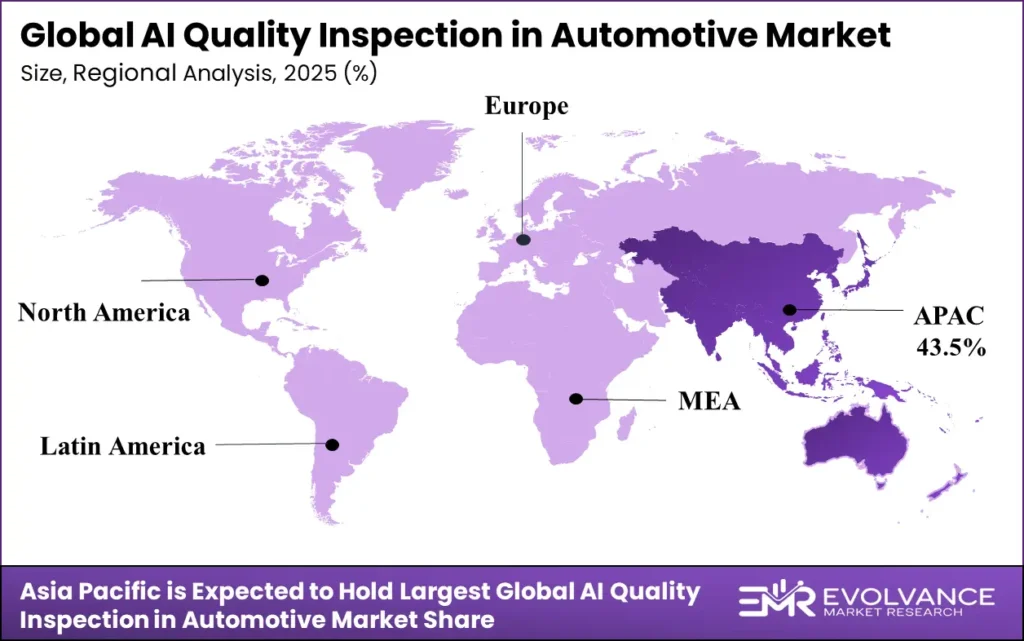

- Leading region: Asia Pacific at 43.5%, valued at USD 360.64 million as of 2026 (as per our research)

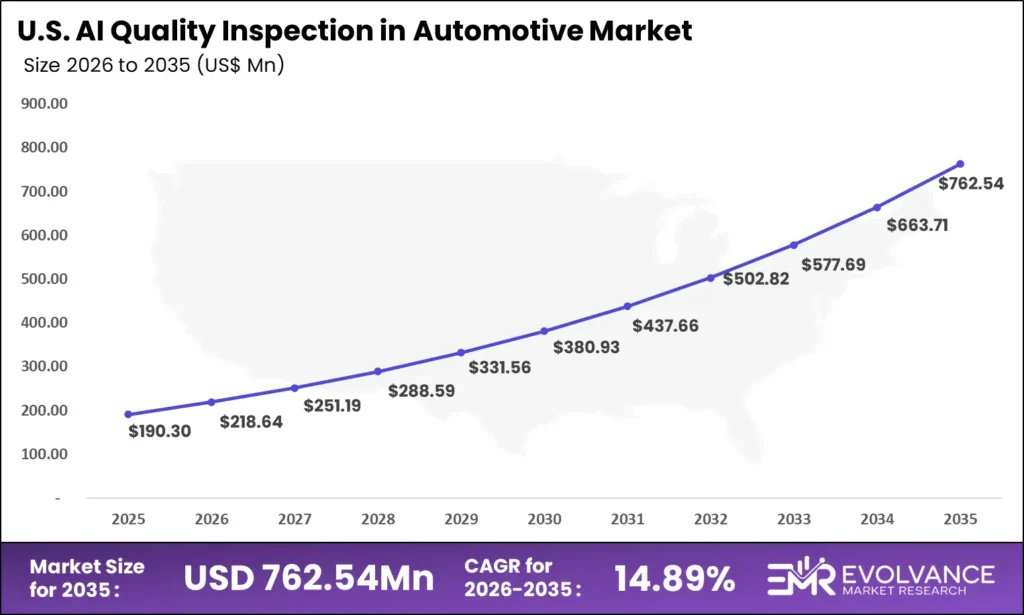

- Leading country: United States at USD 218.64 million as of 2026 (as per our research)

Source: Evolvance Market Research

Market Overview

AI quality inspection in the automotive sector replaces or augments manual and legacy camera-based visual checks across every stage of vehicle production, from stamping and body shop welding through paint application and final assembly verification. Tier-1 suppliers, OEMs, and dealer reconditioning networks depend on these systems to enforce zero-defect mandates, sustain high-throughput cycle times, and satisfy quality management standards including IATF 16949. Without automated inline inspection, production throughput and defect escape rates move in opposite directions.

Our research team built this analysis using a combination of primary interviews with production engineering and quality leadership at OEM and Tier-1 facilities, secondary source triangulation across regulatory filings, trade association publications from bodies including the Verband der Automobilindustrie (VDA) and the Japan Automobile Manufacturers Association (JAMA), and financial disclosures from publicly traded inspection equipment suppliers. Evolvance Market Research validated final estimates through cross-referencing against machine-vision industry billing data from the German VDMA and against regional production output from CAAM, SIAM, and INEGI. The study covers the 2020 to 2035 window with 2025 as the base year and encompasses seven geographic regions.

The core buyer problem is defect escape. An undetected surface flaw in a body panel that reaches final assembly triggers rework costs, recall exposure, and warranty liability that far exceed the cost of inline detection. OEMs trigger AI inspection procurement when legacy systems produce unacceptable pseudo-defect false positive rates that throttle throughput, or when new EV and hybrid platform launches demand inspection configurations that fixed-parameter camera systems cannot provide. Buyers who delay face line downtime, contract non-conformance exposure, and quality audit failure under IATF 16949 certification.

The United States market stood at USD 218.64 million in 2025 and is projected to reach USD 762.54 million by 2035 at a CAGR of 14.89%, according to our research analysts. OEMs held 68.93% end-use share as of 2025, confirming that the primary procurement decision sits at the assembly plant level rather than the aftermarket or service channel. BMW Group’s deployment of real-time AI image-comparison for sheet-metal parts at its Dingolfing facility in February 2025, with millisecond-scale comparison against reference libraries in press-shop inspection, illustrates the production-stage specificity that is driving Tier-1 and OEM procurement decisions today. For investors, the US sub-market’s slower CAGR relative to the global rate signals that Asia Pacific is where incremental dollars produce higher growth multiples.

What Is Actually Driving This Market

Zero-defect manufacturing mandates are the primary structural driver, and the causal mechanism runs directly through OEM supplier contract requirements rather than through general quality aspiration. When an OEM inserts sub-ppm defect escape clauses into Tier-1 supply agreements and requires IATF 16949 conformance documentation, inline AI inspection shifts from optional to contractually necessary. Body-in-White Inspection held 42.4% application share as of 2025, according to our research, because body structure is where weld and dimensional deviations create the most costly downstream rework. For operators, the implication is that inspection investment is not discretionary capital expenditure. It is a condition of contract retention.

Deep learning CNN architectures have crossed a performance threshold that legacy rule-based vision systems cannot match, and the timing is specific. Sensors Journal’s January 2026 documentation of live-production defect detection accuracy at 95 to 100% reflects a capability step-change that became available to production environments between 2023 and 2025 as GPU inference hardware reached sub-200ms latency at affordable price points.

The causal link runs from GPU cost-per-inference falling below the labor cost of manual re-inspection, which makes the ROI calculation favor AI deployment at scale. Named bodies including the VDMA and JAMA both confirm sustained machine-vision investment across their respective markets as production volumes hold. For investors, the maturation of CNN accuracy into the 95-to-100% range closes the performance argument against AI adoption and concentrates competition on integration speed and line-adaptive retraining capability rather than detection capability.

Body shop and paint shop automation is pulling AI inspection into stages of production that legacy systems could not economically serve. Surface & Defect Inspection captured 47.18% of inspection type share as of 2025, per our research analysts, because painted-surface quality is both highly visible to end customers and difficult to evaluate at speed without computer vision.

BMW Group’s CNN-based deployments across Dingolfing and Munich plants reduced painted-surface defects by nearly 40%, a quantified outcome that translates directly into rework labor cost reduction, paint material waste reduction, and warranty claim avoidance. The causal mechanism here is cost avoidance rather than revenue uplift. For operators, paint shop AI inspection delivers measurable P&L impact within 12 to 18 months of full-line deployment, making it the highest near-term ROI application in the inspection stack.

The single most important driver insight: AI inspection is contractually mandated, not aspirationally adopted, and the performance threshold justifying that mandate was crossed in production environments between 2023 and 2025.

- Body-in-White Inspection: 42.4% application share as of 2025, driven by weld and dimensional defect exposure in OEM supply contracts (our research)

- Surface & Defect Inspection: 47.18% inspection type share as of 2025, anchored in paint shop and body panel quality mandates (our research)

- CNN accuracy: 95 to 100% live-production defect detection, documented by Sensors Journal, January 2026

- BMW Group painted-surface defect reduction: nearly 40% through CNN deployments at Dingolfing and Munich, 2025

For investors, capital targeting paint shop and body shop inspection integrators captures the segment where ROI is most defensible and OEM contract mandates create the most durable demand.

Where the Real Risk Is

Pseudo-defect false positives remain the most misunderstood operational risk in this market. The problem is not that AI systems fail to detect real defects. It is that systems not yet calibrated to a specific production environment flag non-faults at rates that disrupt throughput. BMW Group’s Dingolfing plant documented exactly this failure mode with prior camera-based systems before AI retraining corrected accuracy in 2025, per BMW’s press office. This restraint is temporary in facilities with retraining infrastructure, but it is effectively permanent in plants lacking the data engineering capability to run continuous-learning pipelines. For operators, deploying AI inspection without a retraining protocol is the root cause of throughput disruption, not the AI system itself.

Integration complexity with legacy IATF 16949 quality workflows is the structural barrier most likely to slow rollout across mixed EV and ICE production lines. The Capgemini World Quality Report 2025, surveying 1,775 senior quality engineering leaders, found that while organizations deploying AI in quality engineering reported average productivity gains of approximately 19%, one-third reported minimal gains.

The Deloitte 2025 Smart Manufacturing survey found that only 45% of manufacturers had leveraged enterprise standards to manage scaled AI deployments as of 2025. The causal relationship between governance maturity and AI inspection ROI is correlational in the current data, not proven causal. For investors, this gap between adopters and non-adopters suggests the market will bifurcate: high-governance OEMs and Tier-1s will scale quickly, while mid-tier suppliers will lag by two to three years.

The risk most investors underestimate: pseudo-defect false positives are a deployment governance problem, not a technology problem, and the differentiation between vendors will be retraining infrastructure, not detection accuracy.

- Capgemini World Quality Report 2025 (1,775 QE leaders surveyed): one-third of AI quality deployments reported minimal productivity gains as of 2025

- Deloitte 2025 Smart Manufacturing: only 45% of manufacturers had enterprise AI governance standards in place as of 2025

- BMW Dingolfing: prior camera systems produced pseudo-defect false positives before AI retraining, documented by BMW press office, 2025

Watch AI inspection vendor churn rates at Tier-1 suppliers as the signal that false positive rates are materializing as line downtime rather than isolated calibration events.

Segmentation: Where Value Is Concentrating

Component Insights

Hardware commanded 77.62% component share as of 2025, according to our research analysts, because inline AI inspection requires purpose-built industrial cameras, lighting arrays, and edge inference hardware that cannot be substituted by software alone at production line speeds. The industrial imaging supply base, anchored by suppliers certified to automotive production environmental standards, has no consumer-grade equivalent. For investors, hardware lock-in at the component level creates durable margin for integrated inspection system vendors and a structural barrier against software-only entrants.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Hardware | 77.62% | Production-grade imaging and edge inference requirements | Dominant through 2035; software-defined lighting expanding hardware complexity |

| Software | Remainder | CNN model licensing and retraining platforms | Fastest growing as line-adaptive AI commands premium pricing |

| Services | Remainder | Integration, calibration, and retraining support | Growing as governance complexity drives managed service demand |

Deployment Mode Insights

On-Premises deployment held 69.18% share as of 2025, per our research, driven by OEM and Tier-1 data sovereignty requirements and the latency constraints of sub-200ms inline inspection that cloud round-trip times cannot satisfy. IATF 16949 quality record retention requirements further anchor inspection data on-premises. For operators, cloud migration in this segment is constrained by physics and compliance, not preference, and any vendor roadmap promising a cloud-first architecture for inline inspection deserves scrutiny against cycle time specifications.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| On-Premises | 69.18% | Latency constraints, data sovereignty, IATF 16949 compliance | Dominant; hybrid edge-cloud gaining share in non-real-time analytics |

| Cloud-Based | Remainder | Predictive analytics, model retraining pipelines | Growing in ancillary use cases; limited for inline inspection |

Technology Insights

Computer Vision held 41.58% technology share as of 2025, according to our research analysts, because it is the foundational layer on which Deep Learning and Edge AI applications are built. No AI inspection deployment operates without an imaging and feature-extraction pipeline, which anchors Computer Vision as the largest single technology category regardless of the CNN or 3D Vision capabilities layered above it. For investors, companies that own the Computer Vision infrastructure layer hold a structural position that persists even as CNN and Edge AI capture incremental growth.

| Sub-segment | Share % | Primary Driver | Outlook |

|---|---|---|---|

| Computer Vision | 41.58% | Foundation layer for all AI inspection pipelines | Stable; platform for Deep Learning and Edge AI growth |

| Machine Learning | Remainder | Defect classification and pattern recognition | Mature; differentiation shifting to retraining speed |

| Deep Learning | Remainder | CNN-based accuracy gains at production speed | Fastest growing technology sub-segment through 2027 |

| 3D Vision | Remainder | Dimensional measurement in stamping and assembly | Growing as EV platform complexity increases tolerance requirements |

| Edge AI | Remainder | Sub-200ms latency requirements at line speed | High growth; hardware cost reduction accelerating deployment |

SEGMENTS COVERED IN THIS REPORT

By Component

- Hardware

- Software

- Services

By Vehicle

- Passenger Cars

- Commercial Vehicles

By End Use

- OEM

- Tier-1 Suppliers

By Deployment Mode

- On-Premises

- Cloud-Based

By Technology

- Computer Vision

- Machine Learning

- Deep Learning

- 3D Vision

- Edge AI

By Inspection Type

- Surface & Defect Inspection

- Dimensional Measurement

- Assembly Verification

- Functional Inspection

By Application

- Body-in-White Inspection

- Paint & Coating Inspection

- Powertrain Inspection

- Interior & Exterior Inspection

- Final Assembly Inspection

By Manufacturing Stage

- Stamping/Body Panel Inspection

- Welding/Body Shop Inspection

- Paint Shop Inspection

- Assembly Line Inspection

By Defect Type

- Surface Defects

- Dimensional Deviations

- Assembly Errors

- Contamination

Value is concentrated in hardware-anchored, on-premises deployments for body shop and paint shop applications, where OEM contract mandates create non-discretionary demand. Fragmentation is occurring in software, Edge AI, and cloud-adjacent analytics layers, where no single vendor has established a dominant position and retraining platform differentiation is still being determined. For investors, the hardware and Computer Vision foundation layers offer a defensible margin today. The software and Edge AI layers offer higher growth but require a longer hold to capture consolidation value.

Regional Analysis: Where Geography Creates Advantage

Asia Pacific commanded 43.5% revenue share, valued at USD 360.64 million as of 2026, per our emr research analysts, a position structurally anchored in the region’s concentration of high-volume OEM production. China, the region’s dominant production economy, recorded total auto output of 34.531 million units in 2025, up 10.4% year-over-year per the China Association of Automobile Manufacturers (CAAM), sustaining the inspection volume that underpins regional market leadership.

India added production momentum, with total vehicle output rising 8.1% year-over-year in August 2025 per the Society of Indian Automobile Manufacturers (SIAM). For investors, Asia Pacific is where inspection deployment scale drives the steepest unit-cost curves downward, which creates a compounding cost-of-inspection advantage for regional OEMs relative to Western competitors.

North America, led by the United States, holds a structurally distinct position. BMW Manufacturing Co. was the largest US automotive exporter by value in 2025, shipping nearly 200,000 BMW X-model vehicles worth USD 9 million per US Department of Commerce data. Mexico contributed 3,953,494 light vehicle units in 2025 per official INEGI records, with 78.4% of exports directed to the United States, confirming the tightly integrated North American production corridor that drives cross-border inspection standard alignment.

UVeye’s deployment of its drive-thru scanner platform across US dealership networks in 2025 signals that North American AI inspection demand is expanding beyond OEM production floors into dealer reconditioning channels. For operators in North America, the dealer and aftermarket channel represents the most accessible new deployment front, with lower integration complexity than inline OEM inspection.

Europe’s production base is navigating structural headwinds, but the underlying inspection demand remains durable. Germany produced 4,148,836 passenger cars in 2025, a 2.0% increase over 2024, per Verband der Automobilindustrie (VDA) official figures. Electric passenger car production reached 1.67 million units in 2025, up 23% year-over-year, including 1.22 million BEVs, per the same VDA data.

New EV platform launches require fresh inspection parameter libraries and expanded dimensional measurement capability, driving incremental inspection system investment even as overall production volumes grow modestly. For operators in Europe, EV line launch cycles are the primary procurement trigger for AI inspection upgrades, and the 23% BEV production growth rate in Germany signals that this trigger is firing now.

Japan’s production trajectory shows a recovery pattern that sustains inspection investment. Motor vehicle output contracted 8.5% in 2024 per JAMA, but January-to-August 2025 production grew 4.2% year-over-year to 5,458,386 units, confirming a production floor and recovery trend.

Japan’s 2024 AACN-equipped vehicle base reached 8.6 million units, reflecting deep integration of computer-vision-adjacent sensor systems that create a receptive OEM environment for AI inspection upgrades. For investors, Japan’s recovery from the 2024 contraction, combined with an established ADAS sensor ecosystem, positions it as a secondary growth market where AI inspection penetration lags the technology readiness of the OEM base.

| Region | Share % | USD Value (2025) | Key Driver | Strategic Signal |

|---|---|---|---|---|

| Asia Pacific | 43.5% | USD 292.52M | China and India volume production: CAAM 34.5M units in 2025 | Scale-driven cost curve compression; dominant through 2035 |

| North America | Second largest | US: USD 190.30M | OEM export platforms; Mexico-US corridor; dealer channel expansion | Aftermarket channel opening as a secondary demand source |

| Europe | Third position | Estimated contributor | Germany BEV production up 23% YoY (VDA, 2025); EV line launches | EV platform cycles driving inspection hardware refresh |

| Japan | Secondary Asia | Recovery phase | Production recovery Jan-Aug 2025 +4.2% YoY (JAMA); AACN base 8.6M | Inspection technology adoption is lagging OEM readiness |

Competitive Landscape: Who Is Pulling Ahead and Why

The leaders in this market hold advantages built on three compounding factors: deep integration with OEM quality management systems, proprietary training data sets accumulated across multiple production lines, and hardware-software stack control that prevents substitution at the component level.

Cognex Corporation reported Q1 2025 revenue of USD 216 million, up 2% year-over-year from USD 211 million, even as automotive end-market weakness persisted, which the data suggests reflects the non-discretionary nature of inspection system maintenance and calibration contracts rather than new deployment momentum.

Basler AG’s Q1 2025 revenue of EUR 59.5 million grew 37% year-over-year, with incoming orders of EUR 52.1 million up 18%, signaling accelerating downstream demand for industrial imaging hardware. For investors, companies with OEM-embedded contract positions are more defensible than those dependent on new project wins.

The most aggressive challengers are pure-play AI inspection vendors that have built automotive-specific CNN model libraries and are competing on retraining speed and line-adaptive capability rather than hardware. Basler AG’s H1 2025 revenue grew 20% year-over-year against a German VDMA machine-vision market where billings grew 9%, but bookings contracted 4%, suggesting Basler is taking share within a market where total order momentum is softening.

UVeye has secured significant strategic backing from an automotive OEM growth fund, positioning it as the dominant player in the dealer and aftermarket inspection channel, a segment that established industrial inspection vendors have not prioritized. For operators, the vendor selection decision now involves evaluating both production-line integration capability and aftermarket channel ambitions, which are served by structurally different supplier types.

The market is consolidating around integrated stack players at the OEM production level while fragmenting at the dealer and aftermarket level. New entrants face a genuine barrier in the form of OEM qualification timelines, which run 18 to 24 months minimum for inline production inspection systems and require demonstrated accuracy in the customer’s specific production environment.

Omron Corporation’s Industrial Automation Business reported FY2024 operating income growth of 68.8% year-over-year to JPY 36.3 million through structural cost reforms, even as net sales contracted 8.3%, which the data suggests reflects margin discipline in a hardware business facing near-term volume softness. For investors, the consolidation dynamic at the OEM level favors established multi-product automation vendors with existing plant relationships over single-application AI inspection specialists.

| Company | Market Position | Key Advantage | Recent Move |

|---|---|---|---|

| Cognex | Market leader, industrial vision | Embedded OEM contracts; multi-sector vision platform | Q1 2025 revenue USD 216M; automotive softness offset by contract base |

| Basler AG | Industrial imaging hardware leader | Automotive-grade camera systems; VDMA-tracked billing growth | Q1 2025 revenue +37% YoY; H1 2025 +20% YoY; outpacing market billings |

| Omron Corporation | Automation systems integrator | Multi-product plant relationships; cost reform-driven margin recovery | FY2024 operating income +68.8% YoY; VT-X950 CT X-ray system launched Dec 2024 |

| UVeye | Dealer channel AI inspection leader | OEM growth fund backing; drive-thru scanner platform for dealerships | Significant strategic investment secured; dealer network deployment scaling |

| Siemens | Smart factory integration incumbent | Enterprise MES and quality workflow integration | Cited as customer in AI inspection ecosystem deployments |

| Keyence | Sensor and vision system specialist | Proprietary sensor stack; direct sales model | Established inline inspection presence across Asian OEM facilities |

| FANUC | Robotics and automation platform | Robot-integrated inspection; OEM-embedded automation contracts | Inspection capability integrated into robotic assembly cells |

| ZEISS Group | Precision metrology leader | Dimensional measurement accuracy; metrology certification | Expanding into AI-assisted coordinate measurement |

| Hexagon AB | Metrology and smart manufacturing | End-to-end quality software and measurement hardware | Predictive quality analytics platform development |

| Nvidia | AI compute infrastructure | GPU inference hardware; edge AI platform | Edge AI inference driving sub-200ms inspection deployments |

| Landing AI | AI inspection software specialist | Industry-specific CNN model libraries | Manufacturing inspection platform expanding automotive coverage |

| Intel Corporation | Edge compute platform | OpenVINO inference optimization for vision workloads | Embedded in inspection system compute stacks |

| SICK AG | Industrial sensor specialist | 3D vision and sensor fusion capability | Expanding dimensional measurement portfolio |

| ISRA Vision | Surface inspection specialist | Paint and surface defect detection depth | Integrated into ZEISS Group portfolio |

| Teledyne Technologies | Industrial imaging systems | High-resolution imaging for dimensional and surface inspection | Expanding automotive-certified imaging product line |

| Tractable | AI claims and damage assessment | Insurance and aftermarket damage AI | Expanding automotive damage assessment platform |

| Ravin.AI | AI vehicle damage inspection | Post-collision inspection AI; insurance channel integration | Partnership with insurance platform expanding claims automation |

| DeGould | Vehicle condition imaging | Automated vehicle imaging for remarketing and fleet | Fleet and remarketing channel expansion |

| Monk.AI | Vehicle damage detection | Mobile-first damage detection for fleet and rental | Fleet operator channel development |

| Pave AI | Vehicle condition AI | Dealer-facing vehicle assessment platform | Dealer channel integration |

| Inspektlabs | AI vehicle inspection | Remote inspection automation for insurance and fleet | Insurance and fleet channel scaling |

| Bdeo | Visual intelligence for insurance | AI claims and inspection for insurance carriers | European insurance market expansion |

| Claim Genius | AI claims automation | Damage assessment AI for insurance claims workflows | US insurance market integration |

| WeProov | Vehicle condition documentation | Digital vehicle inspection for leasing and fleet | European leasing channel development |

| Rockwell Automation | Industrial automation platform | FactoryTalk quality integration; OEM plant relationships | AI inspection integration into connected enterprise platform |

Where This Market Goes Next

EV and hybrid platform proliferation is the most structurally certain growth activator. Germany’s BEV production growth of 23% year-over-year to 1.67 million units in 2025 per VDA confirms that new platform launches requiring fresh inspection parameter libraries are firing at scale.

Each new EV model launch requires a complete inspection configuration rebuild for body structure, battery housing, and powertrain, because the defect profiles, tolerances, and assembly sequences differ materially from ICE equivalents. This is not a correlational relationship. It is causal: new platform, new inspection system. For operators, EV line conversion is the single most time-sensitive trigger for AI inspection procurement, and the 18-to-24-month OEM qualification timeline means procurement decisions must precede line launch by two years.

Japan’s production recovery trajectory, with January-to-August 2025 output up 4.2% per JAMA-adjacent reporting, combined with an established AACN-equipped vehicle base of 8.6 million units, positions Japan as a market where AI inspection penetration is running below what the technology readiness of the OEM base can absorb. The activation condition is OEM capital expenditure cycle alignment, which the data suggests is tracking with the broader production recovery.

Software-defined lighting and 2.5D imaging, exemplified by the UnitX FleX platform launched in December 2025 with up to 2^32 programmable lighting patterns at sub-200ms cycle times, signal that hardware capability is no longer the constraint. For operators, the constraint is integration talent and retraining infrastructure, and closing that gap is where the near-term competitive differentiation will be determined.

Predictive quality analytics linking inline defect data to upstream process parameters is the direction that converts AI inspection from a defect detection tool into a process control input. When defect data captured at the paint shop feeds back into stamping parameter adjustments three process stages earlier, the inspection system’s value proposition expands from detection to prevention. This shift is correlational in the current data, with early-stage evidence from smart-factory deployments tracked by Automotive Manufacturing Solutions in March 2026, but the causal mechanism is well-defined: real-time defect-to-parameter correlation reduces root-cause investigation time and accelerates corrective action. For operators, investing in the data architecture that connects inspection outputs to process control systems now positions them to capture process prevention ROI rather than detection ROI alone.

| Condition | Timeline | Upside | Who Benefits |

|---|---|---|---|

| EV platform launch cycles drive inspection reconfiguration demand across BEV and PHEV lines | 2025 to 2028 | Inspection system replacement in every converted OEM facility | Integrated stack vendors with EV-specific CNN libraries |

| Japan OEM capex recovery aligns with AI inspection deployment cycles | 2026 to 2028 | Underpenetrated market absorbs inspection investment as production recovery holds | Asia-capable inspection system vendors; JAMA-affiliated OEM Tier-1 suppliers |

| Predictive quality analytics links defect detection to upstream process parameters | 2027 to 2030 | Inspection system repositioned as process control input, commanding premium pricing | Software-layer vendors with MES and process control integration capability |

Key Developments

- January 2025: UVeye secured a USD 191 million funding extension led by Woven Capital (Toyota’s growth fund) with UMC Capital, MyBerg, and a USD 150 million debt facility from Trinity Capital, bringing total funding to USD 380.5 million; approximately 700 systems targeted for deployment in 2025; customers include Amazon and CarMax. Signal: Toyota’s strategic capital signals OEM-level conviction that dealer-channel AI inspection is a durable market, not a niche application.

- February 2025: Self Inspection raised a USD 3 million seed round co-led by Costanoa Ventures and DVx Ventures with Westlake Financial; customers include Avis and CarOffer. Signal: Early-stage capital entering the consumer-facing vehicle inspection channel confirms that aftermarket AI inspection is attracting venture attention beyond the OEM production floor.

- February 2025: RAVIN AI and Five Sigma announced a partnership integrating DeepDetect into Five Sigma’s Claims Management Platform and Clive AI Claims Adjuster in Sydney, Australia, with a reported 50% reduction in claim cycle times. Signal: AI inspection ROI quantification in insurance claims workflows provides a template for justifying deployment cost in adjacent automotive service channels.

- May 2024: EthonAI raised a USD 16.5 million Series A led by Index Ventures with General Catalyst, Earlybird, and Founderful; customers include Siemens Smart Infrastructure and Lindt & Sprüngli. Signal: Index Ventures’ commitment to a manufacturing AI inspection specialist confirms that the industrial AI quality sector is attracting top-tier venture capital beyond automotive-specific applications.

- October 2025: RAVIN AI and ROLLiN’ (IAG) launched a strategic partnership to digitise post-collision inspections in Australia. Signal: Insurance-channel AI inspection deployments are moving from pilot to scaled partnership agreements, expanding the addressable market beyond production-floor applications.