What is the Climate-Resilient Construction Materials Market Size?

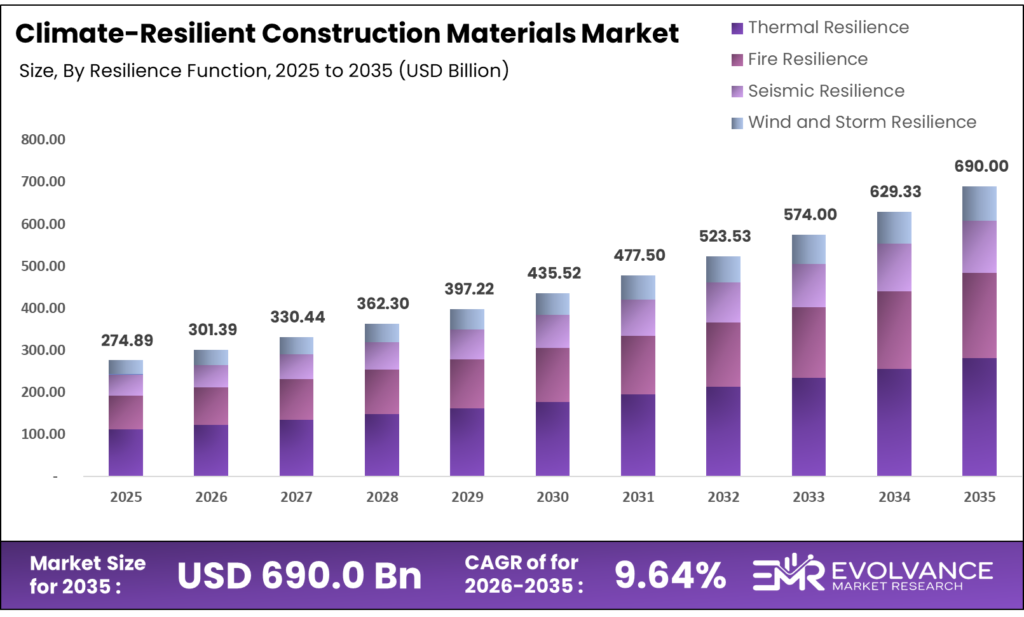

The Global Climate-Resilient Construction Materials Market size will be worth around USD 690.0 Billion by 2035 from USD 274.89 Billion in 2025, growing at a CAGR of 9.64% during the forecast period 2026 to 2035. Government mandates requiring low-carbon materials in public builds are compressing procurement timelines for certified suppliers. Enterprise buyers are shifting capital toward performance-rated concrete, insulation, and bio-based systems ahead of tightening carbon rules. Supply-side capacity for ultra-low-carbon cement remains thin, creating a near-term bottleneck as demand outpaces certified production volume.

Market Highlights

- The Global Climate-Resilient Construction Materials Market will grow from USD 274.89 Billion in 2025 to USD 690.0 Billion by 2035, at a CAGR of 9.64%.

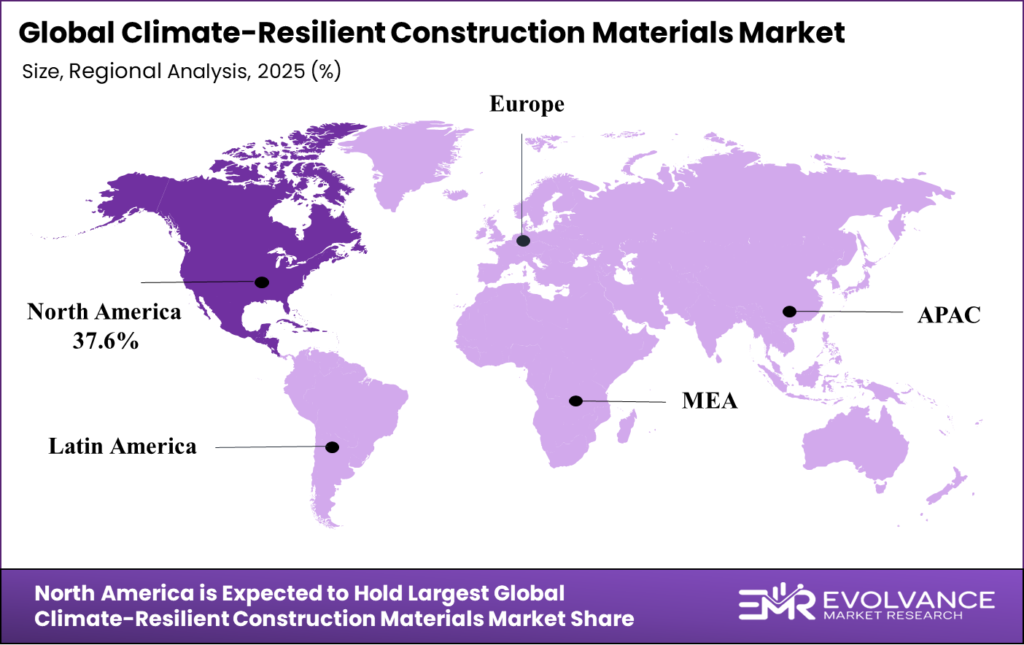

- North America leads all regions with a 37.6% share, valued at USD 103.36 Billion.

- High-performance Concrete and Cementitious Materials holds the top material segment at 32.7%.

- New Construction leads by installation method with 64.1% of market share.

- Thermal Resilience is the leading resilience function segment at 34.3%.

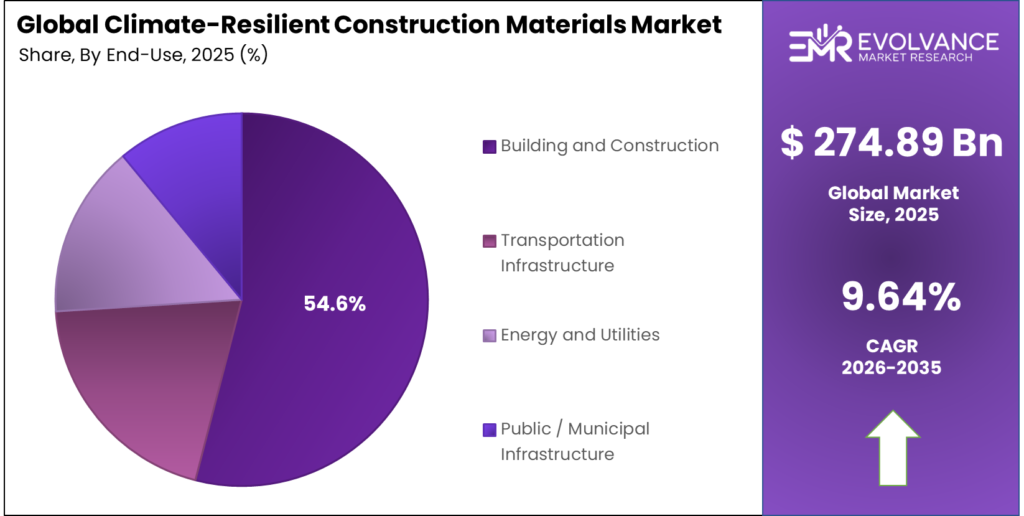

- Building and Construction drives end-use demand with a 54.6% share.

Market Overview

The climate-resilient construction materials market covers products engineered to maintain structural performance under extreme heat, flooding, high winds, fire, and seismic stress. These include advanced concrete systems, thermal envelope materials, bio-based building products, cool roofing, and moisture-resistant composites. As climate events intensify, builders and developers can no longer treat durability and carbon performance as separate considerations.

Procurement is shifting from standard-grade to performance-rated materials across all major build categories. Government bodies, corporate buyers, and infrastructure agencies now factor embodied carbon and climate stress ratings into contractor selection. This means material suppliers who hold certified product data gain a structural advantage in public and commercial tenders over those who do not.

Regulatory action is pulling capital into this space at speed. Ireland’s 30% clinker-replacement rule for public construction projects, effective September 2024, set a direct precedent for procurement-linked carbon controls. Similar mandates are now being drafted or adopted across Western Europe and parts of Asia Pacific, signaling that compliance-led purchasing will be a long-term structural feature of this market, not a short-cycle trend.

Climate-Resilient Construction Materials are designed to withstand extreme weather events, rising temperatures, and shifting environmental conditions. As climate risks intensify, architects and engineers are prioritizing materials that ensure long-term structural integrity. Integrating these materials alongside Low-Carbon Construction Materials and Carbon Neutral Construction Materials ensures buildings are not only built to last but built responsibly.

According to U.S. Department of Energy research, cool roofs can stay more than 50°F (28°C) cooler than conventional roofing surfaces on peak summer days. This temperature gap directly reduces building cooling loads, cutting energy costs and lowering urban heat island effects — a measurable business case for real estate developers and infrastructure owners facing tightening energy codes.

Furthermore, SCG launched its Low Carbon Super Cement in Vietnam in 2024 to directly support net-zero construction targets in Southeast Asia. This move illustrates how commercial players are racing ahead of regulation rather than waiting for it. Vendors who build certified, performance-rated portfolios now will be far better positioned when government mandates force broader market adoption.

Material Type Insights

High-performance Concrete and Cementitious Materials dominates with 32.7% due to widespread code mandates and proven structural data.

In 2025, High-performance Concrete and Cementitious Materials held a dominant market position in the By Material Type segment of the Climate-Resilient Construction Materials Market, with a 32.7% share. Its leadership reflects a structural procurement bias: engineers and public agencies default to concrete systems because they carry decades of performance data, established testing standards, and compatibility with existing build codes. No other category matches this institutional trust at scale.

Insulation and Thermal Envelope Materials represent the fastest-adopted category among retrofit projects, where energy efficiency upgrades account for a large share of spending. Buildings retrofitted with high-performance insulation can cut heating and cooling loads substantially, making this segment the primary entry point for climate upgrades in existing built stock rather than new construction pipelines.

Bio-based and Low-Carbon Materials are gaining traction as buyers seek alternatives with lower lifecycle emissions. Limestone calcined clay cement (LC3) emits up to 40% less CO₂ than conventional Portland cement and costs 25% less to produce while delivering comparable strength. These figures make LC3 one of the few climate-resilient options that simultaneously cuts both carbon and cost, removing the price-premium objection that has historically slowed bio-based adoption. NTPC’s 2024 ‘Sukh’ Eco-House, built with 80% fly ash materials and assembled in just 15–20 days, proves this segment’s potential for speed-optimized, low-carbon housing at scale.

Cool Roofing and Reflective Materials deliver measurable performance gains in high-temperature urban environments. An Arizona pilot showed cool pavements running 10–16°F cooler than conventional asphalt, which reached 152°F at midday. For commercial property owners and municipal infrastructure managers, this temperature reduction translates directly into lower cooling energy costs and longer pavement service life.

Installation Method Insights

New Construction dominates with 64.1% due to greenfield project volume and mandated specification standards.

In 2025, New Construction held a dominant market position in the By Installation Method segment of the Climate-Resilient Construction Materials Market, with a 64.1% share. New builds allow architects and engineers to specify climate-resilient materials from the design stage, eliminating the compatibility constraints that complicate retrofit projects. Government-backed infrastructure programs have further reinforced this dominance by requiring certified low-carbon and climate-adaptive materials in public contracts.

Retrofit and Renovation is the faster-growing installation channel as building owners face tightening carbon disclosure rules for existing assets. Energy performance certificates and corporate net-zero pledges are driving owners to upgrade aging building envelopes, cooling systems, and structural elements. This segment is also cost-competitive: a University of Washington adaptive-reuse project achieved 77% lower cradle-to-gate embodied carbon and 46% lower cost versus demolishing and rebuilding, making the financial case for retrofit investment hard to ignore.

Resilience Function Insights

Thermal Resilience dominates with 34.3% due to direct energy cost savings and near-universal building relevance.

In 2025, Thermal Resilience held a dominant market position in the By Resilience Function segment of the Climate-Resilient Construction Materials Market, with a 34.3% share. Unlike flood or seismic resilience, thermal performance applies to virtually every structure in every climate zone. Energy codes now tie thermal envelope performance to certificate issuance, making thermal-grade materials a non-negotiable line item in most major markets rather than a premium option.

Fire Resilience materials are seeing specification increases in wildfire-prone regions, particularly across the western United States, southern Europe, and parts of Australia. As insurers tighten coverage terms for fire-risk zones, building owners face direct financial incentives to upgrade structural fire resistance — driving demand for fire-rated assemblies across both residential and commercial segments.

End-Use Industry Insights

Building and Construction dominates with 54.6% due to direct exposure to carbon mandates and climate-grade specification requirements.

In 2025, Building and Construction held a dominant market position in the By End-Use Industry segment of the Climate-Resilient Construction Materials Market, with a 54.6% share. This sector bears the most direct regulatory exposure — from embodied carbon limits to energy performance certificates — making climate-resilient materials a procurement requirement rather than a preference.

Transportation Infrastructure is the second-largest end-use segment, with roads, bridges, and rail systems facing direct climate-stress exposure. Heat-resistant pavements, flood-proof bridge decks, and wind-stabilized structures are moving from pilot specification to standard procurement across OECD economies following the body’s 2024 global disaster-resilient infrastructure recommendations for G20 nations.

Energy and Utilities buyers are specifying climate-resilient materials for power plants, grid infrastructure, and renewable energy facilities, where structural failure from extreme weather carries operational and financial penalties far exceeding the incremental cost of upgraded materials. This risk calculus is accelerating adoption across the utilities segment.

Market Segments Covered in the Report

By Material Type

- High-performance Concrete and Cementitious Materials

- Insulation and Thermal Envelope Materials

- Bio-based / Low-Carbon Materials

- Cool Roofing and Reflective Materials

- Flood and Moisture-resistant Materials

By Installation Method

- New Construction

- Retrofit / Renovation

By Resilience Function

- Thermal Resilience

- Fire Resilience

- Seismic Resilience

- Wind and Storm Resilience

By End-Use Industry

- Building and Construction

- Transportation Infrastructure

- Energy and Utilities

- Public / Municipal Infrastructure

Regional Insights

North America Dominates the Climate-Resilient Construction Materials Market with a Market Share of 37.6%, Valued at USD 103.36 Billion

North America holds a 37.6% share worth USD 103.36 Billion, built on a foundation of mature procurement rules, early carbon mandates, and large government infrastructure budgets. Federal programs like the U.S. EPA’s 2024 sustainability funding streams have directly accelerated adoption of embodied-carbon measurement standards. This regulatory infrastructure gives certified material suppliers a clear and durable demand signal that most other regions cannot yet match.

Europe Climate-Resilient Construction Materials Market Trends

Europe is the second-most active region, driven by the EU Green Deal, national carbon-reduction laws, and growing adoption of Environmental Product Declarations in public tenders. The British Standards Institution’s September 2024 publication of new lower-carbon structural concrete standards is a key example of how European regulators are embedding climate-grade specifications directly into building codes, pulling demand forward across the region.

Asia Pacific Climate-Resilient Construction Materials Market Trends

Asia Pacific is the highest-volume growth region, led by construction spending in China, India, and Southeast Asia. India’s Build Ahead Coalition, formed by GCCA India and Xynteo in 2024, is setting new green cement standards that will reshape procurement across one of the world’s largest construction markets. SCG’s commercial launch of low-carbon cement in Vietnam shows that private-sector supply is scaling to meet this demand.

Latin America Climate-Resilient Construction Materials Market Trends

Latin America is an early-stage but structurally important market, where climate vulnerability is high and infrastructure investment is growing. Brazil and Mexico are the primary demand centers, driven by government housing programs and post-disaster rebuild activity. As OECD disaster-resilience recommendations from 2024 filter into national procurement policy, the region’s formal market for certified climate-resilient materials will grow more rapidly than current spend levels suggest.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

Ireland’s Department of Housing issued a 30% clinker-replacement mandate for public construction contracts, effective September 2024. This rule directly links procurement eligibility to material carbon content, forcing suppliers without compliant cementitious products out of the public tender pool. For material vendors, it creates a hard revenue barrier that only certified low-carbon producers can clear.

The British Standards Institution published new standards for lower-carbon structural concrete in September 2024, covering alkali-activated and supplementary cementitious material binders. These standards give engineers and specifiers a formal compliance pathway for cement-free concrete systems. Without this BSI backing, many alternative binder products remained locked out of regulated project categories regardless of technical performance.

The U.S. EPA rolled out sustainability funding programs in 2024 that tied capital access to embodied-carbon measurement and Environmental Product Declaration adoption. This policy design accelerates EPD uptake across the U.S. supply chain by making compliance a precondition for grants rather than a voluntary signal. Suppliers who move quickly to meet EPD requirements gain a direct funding advantage over those who delay.

Drivers

Government Procurement Mandates Compress Supplier Timelines and Lock Out Non-Compliant Material Producers

Governments are no longer merely encouraging low-carbon materials — they are requiring them as a condition of public contract eligibility. Ireland’s 30% clinker-replacement rule for public builds, effective September 2024, is a leading example. Once a government sets a carbon threshold for procurement, the market structure shifts overnight: compliant suppliers gain protected access while non-compliant ones face forced reformulation or exit.

Moreover, Sublime Systems secured additional U.S. Department of Energy support in March 2025 for its electrochemical low-carbon cement program targeting near-zero process emissions. Government co-investment of this kind de-risks early-stage production scaling for climate-resilient material startups, accelerating the point at which these technologies can compete on volume and price with conventional cement producers.

Heidelberg’s Brevik CCS plant can capture approximately 400,000 metric tons of CO₂ per year — roughly 50% of that facility’s total emissions. This demonstrates that large-scale carbon capture is operationally viable in cement production today. Buyers who specify materials from CCS-enabled plants can document scope-3 carbon reductions, a growing requirement for corporate sustainability disclosures across Europe and North America.

Restraints

Slow Building-Code Adoption Leaves High-Performance Alternative Binders Commercially Stranded in Major Markets

Many cement-free and alkali-activated binder systems deliver strong performance data but cannot enter regulated project categories because building codes have not yet recognized them as approved structural materials. This code lag is not a technical problem — it is a governance problem. Until standards bodies formally approve alternative systems, engineers face professional liability risks that stop them from specifying products their clients would otherwise accept.

Additionally, Environmental Product Declaration preparation and third-party certification costs create a meaningful financial burden for smaller material producers. These costs can reach tens of thousands of dollars per product per market, effectively pricing small and mid-sized climate-resilient material companies out of government procurement programs that require EPD compliance. This concentrates certified supply among large players and slows the overall pace of market entry.

Research data shows that climate-resilience measures in residential construction change product-stage embodied carbon by just 0–19% per measure against a pre-existing residential benchmark. This narrow range signals that some performance measures provide modest differentiation, making it harder for buyers to justify premium material pricing when the carbon benefit falls at the lower end of that band. Vendors must clearly communicate the upper-bound performance cases to avoid being commoditized.

Growth Factors

Commercial Scaling of Bio-Based and Ash-Based Systems Opens a Cost-Competitive, High-Speed Build Category

India’s Build Ahead Coalition, formed by GCCA India and Xynteo in 2024, is developing a national green cement taxonomy that will set formal standards for low-carbon construction materials across one of the world’s largest build markets. Once this taxonomy is in place, certified suppliers gain access to a procurement system covering hundreds of millions of square meters of annual construction activity — a scale that few other single-market opportunities can match.

A Skanska and RMI mass-timber design option delivered 78% lower embodied carbon versus comparable steel construction, with only a 1.25% increase in upfront cost. This data point matters because it breaks the assumption that deep carbon reduction requires a significant cost premium. For developers facing carbon reporting obligations, a near-cost-neutral path to major emissions reduction changes the investment calculation entirely.

Furthermore, the OECD’s 2024 global disaster-resilient infrastructure guidance for G20 economies creates a policy pull for climate-adaptive spending across multiple national budgets simultaneously. Countries aligning procurement with these recommendations will direct new capital toward certified climate-resilient materials, creating a multi-market demand wave that benefits suppliers with broad geographic certification coverage rather than single-country approvals.

Emerging Trends

Corporate Procurement Alliances and Startup Funding Cycles Are Reshaping Who Sets Market Standards

The formation of the Sustainable Concrete Buyers Alliance by RMI and the Center for Green Market Activation in 2025, joined by Amazon, Meta, Prologis, and other major corporations, marks a structural shift in how low-carbon concrete standards are set. When buyers of this scale align on a common procurement framework, they effectively create a private standard that suppliers must meet to access major commercial construction programs — without waiting for government regulation to catch up.

Geopolymer and alkali-activated concrete solutions are entering Asian construction markets through companies including Betolar and SCG, signaling that cement-free technologies have crossed the commercialization threshold. These products are no longer research-stage alternatives — they are now competing on live project specifications. Vendors who can deliver certified geopolymer systems at scale will capture share in Asian markets ahead of the next regulatory cycle.

Additionally, the construction technology sector attracted USD 4.4 Billion in global startup funding in Q3 2025 alone. This capital concentration signals that institutional investors see near-term commercial returns in climate-resilient building technologies, not just long-term ESG alignment. Established material producers who do not invest in R&D partnerships or startup acquisitions risk being outpaced by better-funded challengers within this decade.

Key Companies Insights

Sublime Systems is building a differentiated position in electrochemical cement production, targeting near-zero process emissions at a point in the supply chain where most producers still rely on fossil-fuel-intensive kilns. Their March 2025 additional U.S. Department of Energy support extends their runway to commercial scale, and the government co-investment signals credibility that helps Sublime win supply agreements with buyers who require performance-certified, low-carbon cement with documented production provenance.

CRH Ventures is taking a portfolio approach to climate-resilient materials by running a dedicated Sustainable Building Materials Accelerator in 2025, targeting startups working on emissions reduction, circularity, and resource efficiency. This strategy allows CRH to scout and optionally acquire commercially validated technologies before they reach market maturity — lowering its own R&D risk while building a pipeline of differentiated products to defend share as carbon mandates tighten across its core markets in North America and Europe.

Cemex Ventures is actively shaping the startup ecosystem around sustainable construction through its Construction Startup Competition 2025, spotlighting companies including Hyperion Robotics and Alithic. By embedding itself in the commercialization pipeline of these innovators, Cemex gains early-mover visibility into technologies that may disrupt conventional concrete production — and positions itself to partner, license, or acquire before competitors can. This model turns external innovation into a supply-chain hedge.

Heidelberg Materials operates the Brevik CCS cement plant, which can capture about 400,000 metric tons of CO₂ each year — approximately 50% of that plant’s total emissions. This puts Heidelberg in a rare commercial position: it can supply verifiably low-carbon cement with documented capture data to buyers seeking scope-3 reductions for ESG reporting. As corporate and government buyers raise their carbon accounting requirements, Heidelberg’s CCS-backed product line becomes a premium, defensible category that is structurally hard for non-CCS competitors to replicate.

Key Companies

- Sublime Systems

- CRH Ventures

- Cemex Ventures

- Heidelberg Materials

- SCG (Siam Cement Group)

- Betolar

- NTPC Limited

- Skanska

- Hyperion Robotics

- Alithic

Recent Development

- In 2025, Construction technology and sustainable built-environment startups attracted USD 4.4 Billion in global venture funding. This capital surge shows that investors now view climate-resilient materials as a near-term commercial opportunity, not just a long-range ESG bet.

- In March 2025, Sublime Systems secured additional U.S. Department of Energy support for its low-carbon cement commercialization program aimed at scaling electrochemical cement production with near-zero process emissions

- In 2025, CRH Ventures shortlisted multiple sustainable building material startups through its Sustainable Building Materials Accelerator targeting emissions reduction, circularity, and resource efficiency technologies

- In 2025, Cemex Ventures and partners highlighted sustainable construction startups including Hyperion Robotics and Alithic through the Construction Startup Competition 2025 investment and commercialization ecosystem

- In 2025, Amazon, Meta, Prologis, and other corporations joined the Sustainable Concrete Buyers Alliance launched by RMI and the Center for Green Market Activation to accelerate procurement of low-carbon concrete materials

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 274.89 Billion |

| Forecast Revenue (2035) | USD 690.0 Billion |

| CAGR (2026-2035) | 9.64% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (High-performance Concrete and Cementitious Materials, Insulation and Thermal Envelope Materials, Bio-based / Low-Carbon Materials, Cool Roofing and Reflective Materials, Flood and Moisture-resistant Materials), By Installation Method (New Construction, Retrofit / Renovation), By Resilience Function (Thermal Resilience, Fire Resilience, Seismic Resilience, Wind and Storm Resilience), By End-Use Industry (Building and Construction, Transportation Infrastructure, Energy and Utilities, Public / Municipal Infrastructure) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Sublime Systems, CRH Ventures, Cemex Ventures, Heidelberg Materials, SCG (Siam Cement Group), Betolar, NTPC Limited, Skanska, Hyperion Robotics, Alithic |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |