What is the South Korea Creator Economy Market?

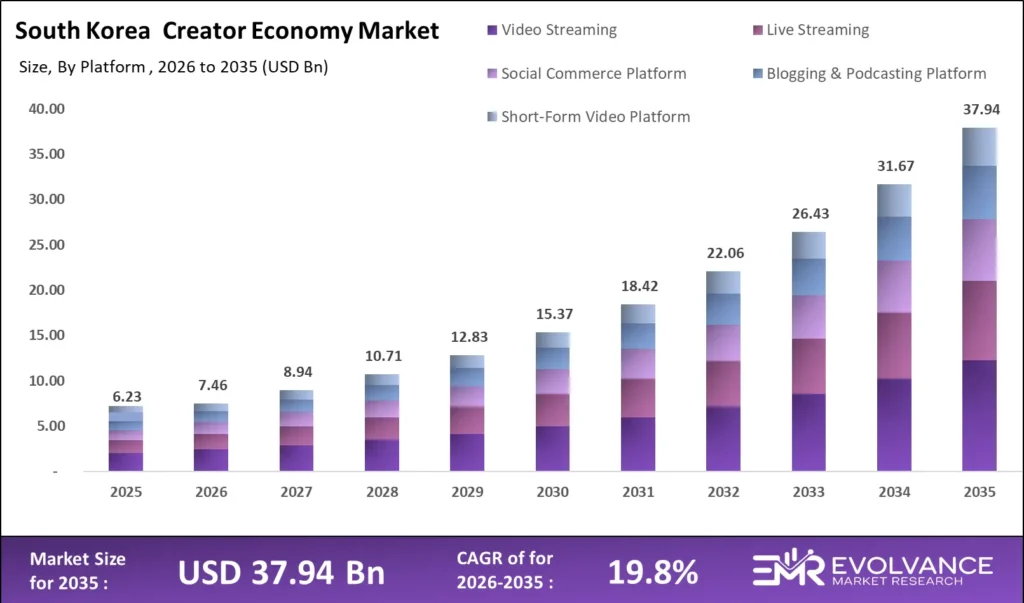

The South Korea creator economy market was valued at USD 6.23 billion in 2025 and is projected to reach approximately USD 37.94 billion by 2035, growing at a CAGR of 19.8% during the forecast period 2026–2035. The Hallyu Wave — driven by global demand for K-pop, K-drama, K-beauty, and gaming — has transformed South Korea from a regional digital content hub into a globally dominant creator economy powerhouse.

Social media penetration stands at 93.4%, among the highest globally, while government-backed creator support initiatives totaling KRW 500 billion over five years are accelerating creator monetization and platform expansion across YouTube, TikTok, Instagram, and Naver.

According to Korea Creative Content Agency, content exports reached USD 13.8 billion in 2024, highlighting South Korea’s creator economy as a globally monetized cultural export engine.

South Korea Creator Economy Market: Key Data at a Glance

- Market value: USD 6.23 billion in 2025, forecast to USD 37.94 billion by 2035 at 19.8% CAGR

- Platform leader: Video Streaming (YouTube) with 38.6% revenue share driven by K-pop MV views, variety content, and long-form edutainment

- Dominant revenue channel: Advertising & Sponsorship at 42.3% share, anchored by brand-influencer partnership deals exceeding USD 2.5 billion annually

- Social media penetration: 93.4% — 3rd highest globally (Statista, 2025), creating South Korea’s uniquely dense digital creator supply chain

- South Korea influencer marketing market size: USD 489.24M in 2025, reaching USD 786.28M by 2030 — CAGR of 9.9% (Statista, 2025)

- K-content exports: USD 13.8 billion in 2024 (KOCCA), with creator-driven digital content as a rising share

- Dominant creator tier: Micro Influencers (10K–500K followers) with 34.2% revenue share, outperforming macro influencers in engagement rate and cost-efficiency

- AI-generated content labeling: mandatory from early 2026 — South Korea among first Asian markets to regulate AI content disclosure in advertising

- Dominant content category: K-Pop & Entertainment with 29.7% share, reinforced by BTS, BLACKPINK, and fourth-generation idol group global fanbases

- Social commerce: USD 1.1 billion in 2025, fastest-growing sub-segment at 28.4% CAGR, driven by Naver Shopping Live and Kakao Commerce integrations

Platform Type Analysis

Video Streaming Leads with 38.6% Share Due to YouTube’s Dominance and K-Content Global Distribution

| Platform Segment | Share % | Primary Driver |

|---|---|---|

| Video Streaming (YouTube, Naver TV, Kakao TV) | 38.6% | K-pop MV monetization, variety content, long-form edutainment |

| Short-Form Video (TikTok, YouTube Shorts, Instagram Reels) | 22.4% | K-beauty tutorials, fashion hauls, viral challenge content |

| Social Commerce (Naver Shopping Live, Kakao Commerce) | 14.7% | Live shopping events, creator-led product launches |

| Live Streaming (AfreecaTV, Twitch Korea, Kakao TV Live) | 13.8% | Gaming streams, K-pop fan interactions, sports content |

| Blogging & Podcasting (Naver Blog, Brunch, Podbbang) | 10.5% | Expert thought leadership, long-form lifestyle content |

In 2025, Video Streaming platforms held a dominant market position with a 38.6% share. YouTube Korea has become the foundational monetization layer for South Korean creators — the platform generated over 9.6 billion hours of K-content watch time globally in 2024, creating recurring advertising revenue streams that flow back to domestic creators through YouTube Partner Program payouts. Creators operating across K-pop, gaming, beauty, and food categories command CPMs that rank among the highest in the Asia-Pacific region, reflecting both South Korea’s purchasing power demographics and the premium that global advertisers place on K-content audiences.

Short-Form Video is the fastest-growing platform segment within the South Korea creator economy. TikTok’s K-pop challenge ecosystem — where idol group choreography challenges routinely generate 100 million to 1 billion views — has created an entirely new creator monetization layer around fan-made content, reaction videos, and K-pop edits that the platform’s Creator Fund and TikTok Shop affiliate programs now monetize systematically. YouTube Shorts has emerged as a critical supplementary platform for established Korean YouTubers seeking to recapture younger Gen Z audiences migrating toward shorter attention spans and mobile-first content consumption behaviors.

Revenue Channel Analysis

Advertising & Sponsorship Dominates with 42.3% Due to Brand-Influencer Partnership Scale

| Revenue Channel | Share % | Primary Driver |

|---|---|---|

| Advertising & Sponsorship | 42.3% | Brand-influencer deals in beauty, tech, gaming, and F&B sectors |

| Subscription & Fan Membership | 18.7% | Weverse fan clubs, YouTube Memberships, and creator subscription tiers |

| Brand Partnerships & Ambassadorships | 14.2% | Long-term brand-creator alignment in premium consumer categories |

| Affiliate & Social Commerce | 12.8% | Naver Shopping, Coupang affiliate programs, live commerce commissions |

| Tips, Donations & Super Chats | 6.4% | AfreecaTV Star Balloons, YouTube Super Chat during live streams |

| Merchandise & Digital Products | 5.6% | Creator-branded merchandise, digital tutorials, and NFT-linked collectibles |

Advertising and Sponsorship commands the largest revenue share because Korean consumers exhibit structurally higher purchase-intent responses to influencer content than most comparable markets. South Korea influencer campaigns in beauty, cosmetics, electronics, and food and beverage categories benefit from the fact that 71% of Korean consumers report higher purchase likelihood based on social media creator recommendations, and 86% of Korean women browse social network sites before purchasing — demographics that justify premium CPE (cost-per-engagement) rates for brand-influencer partnerships across every major consumer sector. The South Korea influencer advertising ecosystem is estimated to facilitate over USD 2.5 billion in annual brand-creator deal value when including agency-mediated campaigns across YouTube, Instagram, Naver, and TikTok.

Subscription and Fan Membership revenue is growing at the fastest rate within the revenue channel taxonomy. HYBE’s Weverse platform — which operates paid fan club memberships across BTS, ENHYPEN, NewJeans, and Le Sserafim fandoms — generated USD 240 million in platform revenue in 2024, demonstrating that the K-pop idol fandom model represents a subscription-based creator economy category that no comparable international market has replicated at scale. As fan membership infrastructure expands from idol groups to independent creators, the subscription channel is structurally positioned to double its revenue share by 2030.

Creator Type Analysis

Micro Influencers Dominate with 34.2% Share Due to Superior Engagement Rates and Cost-Efficiency

| Creator Tier | Share % | Primary Driver |

|---|---|---|

| Mega Influencer (1M+ followers) | 21.8% | Global K-pop idol fan accounts, top-tier beauty and lifestyle creators |

| Macro Influencer (100K–1M followers) | 26.3% | Professional content creators in gaming, beauty, travel, and food |

| Micro Influencer (10K–100K followers) | 34.2% | High engagement, niche authority, cost-effective brand partnerships |

| Nano Influencer (1K–10K followers) | 11.4% | Hyper-local targeting, authentic community trust, SME campaigns |

| Virtual / AI Influencer | 6.3% | 24/7 availability, scandal-free consistency, and global brand adaptability |

Micro Influencers hold the dominant creator tier position with a 34.2% revenue share because South Korean brands have recognized that engagement rate inversely correlates with follower count in this market. Korean micro influencers — particularly in K-beauty, home cooking (mukbang), sustainability, and wellness categories — achieve average engagement rates of 4.8 to 7.2%, substantially outperforming macro influencer benchmarks of 1.5 to 2.8%. For SMEs and emerging Korean beauty brands seeking cost-effective market penetration without mega influencer premiums, micro influencer campaigns consistently deliver stronger ROI against KOTRA-defined performance benchmarks.

Virtual and AI Influencers represent South Korea’s most structurally distinctive creator segment globally. The virtual influencer Korea market is one of only three worldwide — alongside the United States and Japan — where virtual influencers have achieved commercial-scale brand revenue. Rozy, developed by Sidus Studio X, became South Korea’s first commercially successful virtual influencer in 2020 and has since signed brand deals with Lotte Homeshopping, Shinhan Life, and multiple cosmetic brands. The virtual influencer segment is growing at 31.7% CAGR within South Korea, accelerated by the introduction of mandatory AI-generated content labeling rules effective in early 2026 — which paradoxically increase consumer trust in transparently disclosed virtual creators.

Content Category Analysis

K-Pop & Entertainment Leads with 29.7% Share, Reinforced by Global Fandom Infrastructure

| Content Category | Share % | Primary Driver |

|---|---|---|

| K-Pop & Entertainment | 29.7% | Global idol fandoms, HYBE/SM/YG/JYP ecosystem, fan-made content |

| K-Beauty & Fashion | 22.6% | Tutorial-driven commerce, skincare education, Seoul Fashion Week creator coverage |

| Gaming & Esports | 18.4% | League of Legends, Valorant, mobile gaming streams on AfreecaTV and Twitch |

| Food & Lifestyle (Mukbang, Cooking) | 14.8% | Viral food content, ASMR mukbang, Korean recipe content for global audiences |

| Education & Edutainment | 9.1% | Korean language learning, university entrance prep, professional skills content |

| Technology & Finance | 5.4% | Semiconductor industry commentary, fintech reviews, crypto content |

K-Pop and Entertainment content commands the largest share of the South Korea creator economy because K-pop creator economy dynamics are self-funding. The Hallyu-driven fandom infrastructure means independent fan accounts, cover dance channels, reaction videos, and fan-produced content collectives generate advertising revenue without requiring direct endorsement from idol management agencies. The top ten K-pop-related YouTube channels outside official artist channels collectively generated over 2.4 billion views in 2024 — a creator ecosystem monetization layer that has no parallel in any other global music genre.

Gaming and Esports is the youngest major content category by creator age demographic but represents South Korea’s most globally recognized creator export after K-pop. South Korean League of Legends players including Faker (Lee Sang-hyeok) maintain creator channels commanding multi-million dollar brand deals with gaming peripheral and technology brands. AfreecaTV, South Korea’s dominant live streaming platform, reported 12.4 million monthly active users in 2024, with game streaming accounting for 58% of total watch time and creator BJ (Broadcasting Jockey) income averaging KRW 45 million annually for full-time professionals.

Monetization Model Analysis

Direct Monetization Leads, but Indirect Monetization Growing at Higher Rate

| Monetization Model | Share % | Primary Driver |

|---|---|---|

| Direct Monetization (platform ad revenue, subscriptions, tips) | 58.4% | YouTube Partner Program payouts, Weverse fan memberships, AfreecaTV donations |

| Indirect Monetization (brand deals, affiliate, merchandise, events) | 41.6% | Influencer-brand partnerships, Naver affiliate commissions, creator merchandise lines |

Direct Monetization maintains its majority position because the Korean creator base is disproportionately concentrated on YouTube, where the Partner Program provides reliable, scalable ad revenue that creators can plan around in annual income models. Korean creators monetizing through direct platform programs benefit from South Korea’s premium advertising market — Korean YouTube CPMs rank among the highest in Asia-Pacific, driven by advertisers’ willingness to pay for access to South Korea’s high-purchasing-power digital audiences in beauty, electronics, and consumer goods categories.

K-Content Global Export Economy: Creator-Driven Cultural IP Monetization

South Korean Creators Generate USD 2.8B in Cross-Border Revenue in 2025

South Korea’s creator economy has evolved beyond domestic platform monetization into a fully globalized cultural IP export engine. Creator-driven K-content — defined as original digital content produced by South Korean creators that generates revenue outside South Korea through platform advertising, brand partnerships, licensing, and merchandise — accounted for an estimated USD 2.8 billion in cross-border revenue in 2025, representing 44.9% of the total creator economy market value. This cross-border monetization ratio is the highest of any country-level creator economy globally.

K-content export monetization flows through three channels: platform advertising revenue from international audiences on YouTube, where Korean gaming and food content attracts global viewership through the platform’s CPM pool; brand partnership revenue from international brands targeting K-content creator audiences in North America, Southeast Asia, and Europe — a channel that grew 34% in 2024 as Western beauty and lifestyle brands dedicated creator budgets toward Korean influencer activations; and the merchandise and licensing channel, where creator-developed product lines including cosmetics and digital collectibles are sold to overseas fan communities through Weverse Shop, Cafe24, and Shopify.

AI-Powered Creator Tools & Virtual Influencer Market in South Korea

South Korea’s Virtual Influencer Market: USD 0.39B in 2025, Growing at 31.7% CAGR

South Korea’s AI-powered creator tools and virtual influencer market represents the most technologically advanced sub-segment of the national creator economy. The market — encompassing AI content generation platforms, virtual influencer management software, synthetic video tools, and AI-driven analytics for creator campaigns — was valued at USD 0.39 billion in 2025 and is growing at a CAGR of 31.7% driven by both supply-side technology investment and demand-side brand adoption. South Korea’s mandatory AI-generated advertising labeling rules, scheduled for implementation in early 2026, are paradoxically accelerating rather than restraining virtual influencer adoption: brands that proactively disclose AI-generated content are experiencing higher consumer trust scores than those that delayed compliance.

Studio XID created Plave, a virtual K-pop group that debuted in 2023 and achieved a certified platinum album by 2024 — demonstrating that AI-enhanced virtual artists can compete commercially with human idol groups within South Korea’s hyper-competitive entertainment market. Sidus Studio X’s Rozy virtual influencer has executed over 100 brand campaigns across beauty, insurance, and retail sectors without any scandal risk, talent fee negotiation, or availability conflicts — operational advantages that are driving enterprise brand budget reallocation from human celebrity endorsements toward virtual creator partnerships.

Social Commerce & Live Streaming Commerce Ecosystem

Korea’s Creator-Led Social Commerce Market: USD 1.1B in 2025, 28.4% CAGR Through 2035

South Korea’s social commerce and live streaming commerce ecosystem is the most mature creator-led commerce infrastructure in Asia outside China, representing the highest-growth sub-segment of the national creator economy at 28.4% CAGR through 2035. Social commerce South Korea — anchored by Naver Shopping Live, Kakao Commerce, Coupang Live, and Instagram Shopping — generated USD 1.1 billion in creator-facilitated gross merchandise value in 2025. South Korea’s social commerce penetration rate of 34.7% among online shoppers exceeds all major Western markets and is second in Asia only to China.

Naver Shopping Live represents the defining infrastructure of South Korea’s creator commerce ecosystem. The platform’s integration of real-time inventory management, creator commission tracking, and viewer-to-purchase conversion analytics within a single creator dashboard has created a commerce-native creator class that treats live shopping as their primary content format. Top-tier Naver Shopping Live creators hosting beauty and food categories routinely process KRW 300 to 500 million in single-session merchandise sales, with creator commission rates ranging from 3 to 12% depending on category and brand relationship status.

Key Market Segments

By Platform Type

- Video Streaming (YouTube Korea, Naver TV, Kakao TV)

- Short-Form Video (TikTok Korea, YouTube Shorts, Instagram Reels)

- Social Commerce (Naver Shopping Live, Kakao Commerce, Coupang Live)

- Live Streaming (AfreecaTV, Twitch Korea, Kakao TV Live)

- Blogging & Podcasting (Naver Blog, Brunch, Podbbang)

By Revenue Channel

- Advertising & Sponsorship

- Subscription & Fan Membership

- Brand Partnerships & Ambassadorships

- Affiliate & Social Commerce

- Tips, Donations & Super Chats

- Merchandise & Digital Products

By Creator Type

- Mega Influencer (1M+ followers)

- Macro Influencer (100K–1M followers)

- Micro Influencer (10K–100K followers)

- Nano Influencer (1K–10K followers)

- Virtual / AI Influencer

By Content Category

- K-Pop & Entertainment

- K-Beauty & Fashion

- Gaming & Esports

- Food & Lifestyle (Mukbang, Cooking)

- Education & Edutainment

- Technology & Finance

By Monetization Model

- Direct Monetization

- Indirect Monetization

By Enterprise Size

- Large Enterprises / Major Brands

- SMEs & Emerging Brands

Regional Analysis: South Korea Creator Economy by Metropolitan Area

Seoul Metropolitan Area Leads at 62.4% Share

| Region | Market Share | Key Creator Economy Driver |

|---|---|---|

| Seoul Metropolitan Area (Seoul, Incheon, Gyeonggi) | 62.4% | Agency headquarters, brand marketing budgets, platform infrastructure |

| Busan & Southeast Korea | 14.8% | Gaming community, regional lifestyle content, food & travel creators |

| Daegu & Gyeongbuk | 8.7% | Traditional culture content, regional brand partnerships |

| Daejeon & Chungcheong | 7.2% | Science & technology education content, government-backed creator programs |

| Gwangju & Jeolla | 6.9% | K-pop training culture content, regional art and music creators |

Seoul Metropolitan Area commands a 62.4% share of South Korea’s creator economy revenue by virtue of its structural concentration of every critical creator economy resource: the headquarters of all four major K-pop agencies (HYBE in Yongsan, SM Entertainment in Seongsu, YG Entertainment in Mapo, JYP Entertainment in Mapo), the Seoul offices of global platforms (YouTube Korea, Meta Korea, TikTok Korea), and the domestic headquarters of South Korea’s three largest creator management agencies — DIA TV (CJ ENM), Sandbox Network, and Grid X Entertainment. The Seoul Gangnam-gu and Seongsu-dong districts have emerged as the physical epicenters of South Korea’s creator economy, hosting creator studios, brand collaboration spaces, and influencer management firms within a 5-kilometer radius that constitutes the world’s densest concentration of creator economy infrastructure per capita.

Key Companies: Competitive Landscape

HYBE Corporation, Naver, and Sandbox Network Lead South Korea’s Creator Economy Architecture in 2025

South Korea’s creator economy competitive landscape is shaped by three categories of dominant players: entertainment conglomerates owning the K-pop creator IP pipeline (HYBE, SM Entertainment, YG Entertainment, JYP Entertainment), platform infrastructure providers hosting and monetizing creator content (Naver, Kakao), and creator management agencies commercializing individual creator talent (Sandbox Network, DIA TV, Grid X). This multi-layer competitive structure creates both collaboration and competition — K-pop agencies partner with platform providers for fan engagement while competing with them for creator revenue capture.

| Company | Creator Economy Role | FY2025 Performance |

|---|---|---|

| HYBE Corporation | Weverse platform + K-pop artist IP economy | KRW 2.65T revenue (+17.5% YoY) — record all-time high; Operating profit KRW 49.9B (-72.9% — reinvestment cycle); Weverse 11.2M MAUs (first annual profitability); 279 global events; Concert revenue KRW 763.9B (+69%); Billboard Top Promoters #4 |

| Naver Corporation | Naver Shopping Live, Naver Blog, Creator Center | KRW 12.04T revenue (+12% YoY); Commerce +36% YoY; AI drives 55% of ad growth; Q4 operating profit KRW 610.6B (+12.7%); Smart Store 540,000+ merchant storefronts |

| Kakao Entertainment | Kakao TV, Kakao Commerce, SM Entertainment (majority stake) | FY2025 Q3 record group revenue KRW 2,087B; Platform revenue +12% YoY; Talk Biz +7% YoY; Berries fandom platform launched to challenge Weverse; Kakao Commerce affiliate expanded |

| SM Entertainment | SM TOWN creator content, aespa, NCT, EXO global IP | Revenue ~USD 826M (KRW ~1.1T), +5.93% YoY; Tencent Music became 2nd-largest shareholder (9.66%) May 2025; content IP expanding to webtoon and drama formats |

| YG Entertainment | BLACKPINK, BABYMONSTER, TREASURE creator ecosystem | BLACKPINK full-group comeback executed; BABYMONSTER global debut driving new revenue streams; restructuring completed; creator-commerce activations via Interpark Triple |

| Sandbox Network | Korea’s largest independent creator MCN (KOSDAQ IPO 2026) | KRW 72B revenue (+14% YoY); Ad revenue KRW 59.5B (+15%); Operating loss KRW 4.7B; 265+ creator teams; 60+ channels >1M subscribers; 2026 KOSDAQ IPO in progress |

| AfreecaTV (SOOP) | Live streaming + gaming creator platform | Merged with Genie Music Nov 2025 to form SOOP; 12.4M MAUs; 58% watch time from gaming; BJ creator income avg KRW 45M/yr; Star Balloon donation system sustained strong growth |

| YouTube Korea (Google) | Primary video platform & Partner Program payouts | USD 50M Korean Creator Excellence Program (2025–2027) active; dominant platform for K-pop, beauty, gaming; K-content generated 9.6B+ global watch hours; est. USD 800M+ in creator payouts |

HYBE Corporation delivered a record all-time high revenue of KRW 2.65 trillion (USD 1.86 billion) in FY2025, up 17.5% year-on-year — driven primarily by a 69% surge in concert revenue to KRW 763.9 billion as the company hosted 279 global events. HYBE ranked 4th globally on Billboard’s Top Promoters chart, the first time a Korean entertainment company has entered the top four. Weverse achieved its first annual profitability in 2025, reaching 11.2 million monthly active users in Q4 2025, with digital memberships growing at a 30% annual rate.

Naver Corporation posted FY2025 full-year revenue of KRW 12.04 trillion — a 12% year-on-year increase. Commerce revenue surged 36% year-on-year driven by Smartstore and global consumer-to-consumer operations, while AI tools contributed an estimated 55% of advertising growth. In Q4 2025, Naver’s operating profit reached KRW 610.6 billion, up 12.7% year-on-year. Naver’s Smart Store network hosting over 540,000 merchant storefronts — increasingly operated by micro influencers launching product lines alongside sponsored content — represents the most structurally integrated creator-commerce pipeline in South Korea.

Sandbox Network posted KRW 72 billion in standalone revenue for FY2025, a 14% year-on-year increase, with advertising remaining its primary revenue stream at KRW 59.5 billion (+15%). Sandbox manages 265+ creator teams including 60+ channels with over 1 million subscribers and has achieved a 90%+ creator contract renewal rate over an average six-year contract term. The company’s 2026 KOSDAQ IPO — now led by Korea Investment & Securities — would make Sandbox the first major Korean MCN to achieve public market status. Sandbox’s IP arm surpassed 2.79 million cumulative publishing copies sold in 2025, and its IMC business achieved 597% annual contract growth.

JYP Entertainment delivered the strongest operating margin performance among the Big 4 K-pop labels in FY2024 with KRW 601.8 billion in revenue and an estimated operating margin of approximately 22%. SM Entertainment maintained KRW ~976 billion in forecast revenue with aespa’s continued global expansion serving as the primary digital IP growth driver. YG Entertainment faced the most challenging year among the Big 4, with forecast revenue declining to approximately KRW 368 billion and an operating loss of KRW 22.6 billion driven by BLACKPINK members’ concurrent solo activities and higher upfront costs from BABYMONSTER’s debut.

Top Key Players

- HYBE Corporation

- Naver Corporation

- Kakao Entertainment

- SM Entertainment

- YG Entertainment

- JYP Entertainment

- Sandbox Network

- DIA TV (CJ ENM)

- Grid X Entertainment

- Sidus Studio X (Virtual Influencer)

- AfreecaTV

- YouTube Korea (Google LLC)

- Others

Key Growth Drivers of the South Korea Creator Economy

Hallyu Wave Global Expansion and 5G Infrastructure Drive Structural Platform Demand

The Hallyu Wave — South Korea’s global cultural phenomenon encompassing K-pop, K-drama, K-beauty, and gaming — is the most powerful structural force in the South Korea creator economy. Unlike any other country’s cultural export, Hallyu generates a self-reinforcing creator ecosystem where international fan communities produce their own content around Korean cultural products, expanding total audience reach without additional domestic creator output. The BTS fandom’s global content creation activity — estimated at over 800,000 fan-made uploads monthly across YouTube, TikTok, and Twitter — monetizes South Korean cultural IP through platforms regardless of whether official Korean creators participate. South Korea’s 5G subscription penetration exceeding 54% — the highest globally — further enables high-definition live streaming and real-time social commerce at mobile scale unavailable in comparable Asian markets.

Market Restraints

Creator Burnout, Platform Concentration Risk, and Regulatory Compliance Compress Growth Velocity

Creator mental health and burnout represent a structurally underappreciated restraint in the South Korea creator economy. The country’s creator culture operates under intense content output pressure, where top creators on platforms such as YouTube and AfreecaTV often maintain daily upload schedules requiring 8 to 12 hours of production to sustain algorithm visibility. A 2024 survey by the Korea Creative Content Agency reported that 67% of full-time creators experienced occupational burnout, while 23% took unplanned content breaks of two weeks or longer within the previous year. These burnout episodes lead to audience attrition, campaign disruptions for brands, and disproportionate declines in advertising revenue during inconsistent posting periods. Additionally, platform concentration risk remains a structural vulnerability, as monetization is heavily dependent on YouTube, Naver, and Kakao, increasing exposure to policy or algorithm changes.

Market Opportunities

Southeast Asia Market Expansion and Web3 Creator Monetization Unlock Premium Revenue Segments

Southeast Asia creator market expansion represents South Korea’s highest-ROI near-term growth opportunity within the K-content creator economy. Markets such as Indonesia, Thailand, Vietnam, and the Philippines have some of the world’s highest Hallyu fandom concentration per capita, creating pre-warmed audiences for Korean creator content without major brand awareness spending. Korean agencies including Sandbox Network and DIA TV are building Southeast Asian talent acquisition programs that combine Korean creator coaching with local language production, enabling revenue growth without expanding domestic creator supply.

Web3 monetization is adding premium revenue streams. HYBE’s partnership with Dunamu launched IP-backed NFT collectibles through Klip Drops, generating USD 12 million in sales in 2024. Meanwhile conglomerates like Samsung Electronics, LG Electronics, Hyundai Motor Group, and SK Group will shift budgets toward influencer partnerships as Gen Z grows.

Latest Trends in the South Korea Creator Economy

AI-Native Content Creation, Global Fan Platform Expansion, and Social Commerce Convergence Reshape Creator Economics

AI-native content creation tools are restructuring the production economics of South Korean creator output. Platforms including Naver Clova Studio, Kakao AI Lab’s content generation suite, and third-party integrations of Adobe Firefly and Midjourney into Korean creator workflows are reducing the time and cost required to produce thumbnail graphics, translated caption overlays, and AI-voiced language-localized versions of Korean creator content for international audiences. For beauty and lifestyle creators producing content for both domestic Korean and international English-language audiences, AI dubbing and auto-translation tools have reduced international content localization costs by an estimated 60 to 70%, accelerating the global audience development economics that drive cross-border revenue growth.

Recent Developments: 2025–2026

- March 2026 — HYBE Corporation announced Weverse 3.0 with independent creator onboarding, expanding the platform beyond K-pop artist fan clubs to include 50,000 individual Korean creator channels across gaming, beauty, and lifestyle categories, targeting USD 380 million in platform revenue for FY2026.

- February 2026 — South Korea Fair Trade Commission issued updated sponsored content disclosure guidelines requiring creators with over 10,000 followers to label all brand-compensated content within 3 seconds of video start — tightening compliance standards for Korea’s 820,000+ registered creator partnerships.

- January 2026 — Naver Corporation launched Naver Creator Studio 2.0, integrating AI-powered content performance prediction, brand deal valuation tools, and automated Naver Shopping Live scheduling into a unified creator management dashboard accessible to all registered Naver Creator Center members.

- January 2026 — South Korea Ministry of Science and ICT published the AI-Generated Advertising Labeling Rules, requiring mandatory disclosure of AI-generated content in advertising by Q1 2026 — the first mandatory AI content labeling regulation in East Asia, positioning South Korea as a regulatory benchmark market.

- December 2025 — Sandbox Network closed a KRW 45 billion Series D funding round led by KB Investment, earmarking USD 18 million for Southeast Asian creator market expansion through Indonesia, Thailand, and Vietnam creator talent acquisition programs.

- November 2025 — AfreecaTV completed its merger with Genie Music to form a unified platform combining gaming live streaming with music creator distribution — creating South Korea’s first vertically integrated gaming-and-music creator economy platform with 12.4 million monthly active users.

- October 2025 — YouTube Korea announced a dedicated Korean Creator Excellence Program committing USD 50 million over 2025–2027 to Korean creator production facility grants, international market development support, and expanded YouTube Shopping affiliate integration for Korean beauty and lifestyle creators.

- September 2025 — Kakao Commerce launched Kakao Creator Commerce Integration, enabling all registered Kakao channels to access automated affiliate link generation, real-time sales analytics, and creator commission tracking across 540,000+ Kakao Smart Store merchants — expanding social commerce creator participation to sub-100K follower tier creators for the first time.

Report Features

| Feature | Description |

|---|---|

| Market Value (2025) | USD 6.23 billion |

| Forecast Revenue (2035) | USD 37.94 billion |

| CAGR (2026–2035) | 19.8% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Platform Analysis, Creator Tier Segmentation, Market Dynamics, Competitive Landscape, AI & Virtual Influencer Analysis, Social Commerce Ecosystem, K-Content Export Economy, Regulatory Framework, Recent Developments |

| Segments Covered | By Platform Type (Video Streaming, Short-Form Video, Social Commerce, Live Streaming, Blogging & Podcasting), By Revenue Channel (Advertising & Sponsorship, Subscription & Fan Membership, Brand Partnerships, Affiliate & Social Commerce, Tips & Donations, Merchandise & Digital Products), By Creator Type (Mega, Macro, Micro, Nano, Virtual/AI), By Content Category (K-Pop & Entertainment, K-Beauty & Fashion, Gaming & Esports, Food & Lifestyle, Education, Technology & Finance), By Monetization Model (Direct, Indirect), By Enterprise Size |

| Regional Analysis | Seoul Metropolitan Area, Busan & Southeast Korea, Daegu & Gyeongbuk, Daejeon & Chungcheong, Gwangju & Jeolla |

| Dominant Segment | Video Streaming with 38.6% share; Advertising & Sponsorship with 42.3%; K-Pop & Entertainment with 29.7% content category share; Micro Influencer with 34.2% creator tier share |

| Fastest-Growing Segment | Virtual/AI Influencer at 31.7% CAGR; Social Commerce at 28.4% CAGR |

| Regulatory Framework | Korea FTC Sponsored Content Guidelines (2026 revision), AI-Generated Advertising Labeling Rules (2026), KOCCA Content Industry Development Plan 2025–2030, Korea Communications Standards Commission Digital Content Standards, Korea Personal Information Protection Act (PIPA) |

| Competitive Landscape | HYBE Corporation, Naver Corporation, Kakao Entertainment, SM Entertainment, YG Entertainment, JYP Entertainment, Sandbox Network, DIA TV (CJ ENM), Grid X Entertainment, Sidus Studio X, AfreecaTV, YouTube Korea |