What is the Digital Twin in Aerospace Manufacturing Market size?

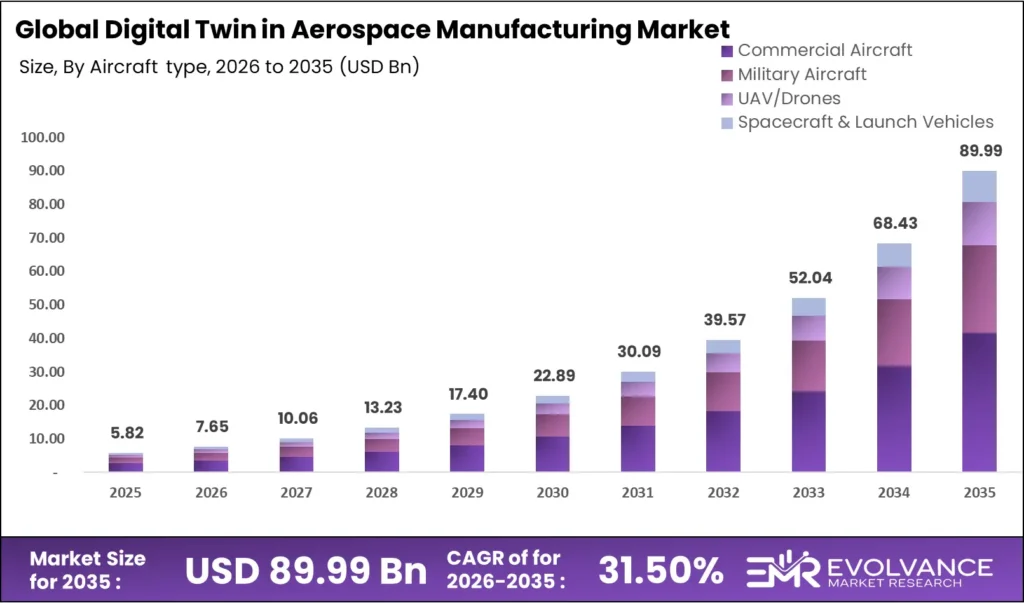

The global Digital Twin in Aerospace Manufacturing Market was valued at USD 5.82 billion in 2025 and is projected to reach approximately USD 89.99 billion by 2035, growing at a CAGR of 31.50% during the forecast period 2026 to 2035. The convergence of AI-powered simulation, IoT-enabled real-time sensor integration, and next-generation aircraft development programs — including the Boeing 777X, Airbus A321XLR, and multiple next-gen fighter programs — are the structural investment forces compressing the time between design conception and physical production in aerospace environments.

Aerospace manufacturers deploying digital twin in aerospace manufacturing platforms face two simultaneous pressures: legacy PLM integration debt from decades of CAD toolchain development, and a shortage of engineers capable of operating AI-driven simulation environments at production scale. According to the AIA, the US aerospace sector will require over 340,000 additional engineers by 2028. A growing share of Aerospace Program Capital & Digital Twin for Telecom Network Simulation is directed toward digital twin aerospace manufacturing tools that reduce certification risk before metal is cut.

The Digital Twin in Aerospace Manufacturing Market is growing due to increasing adoption of simulation and predictive maintenance technologies in aircraft production. These solutions improve operational efficiency and reduce costs across the lifecycle. The market is closely connected with the Secure Semiconductor Supply Chain, ensuring reliable hardware components, and the Security Analytics for data monitoring. Additionally, cloud integration through the Cloud FinOps supports scalable deployment of digital twin solutions.

Digital Twin in Aerospace Manufacturing Market Highlights: Key Data at a Glance

- Market value: USD 5.82 billion in 2025, forecast to USD 89.99 billion by 2035 at 31.50% CAGR

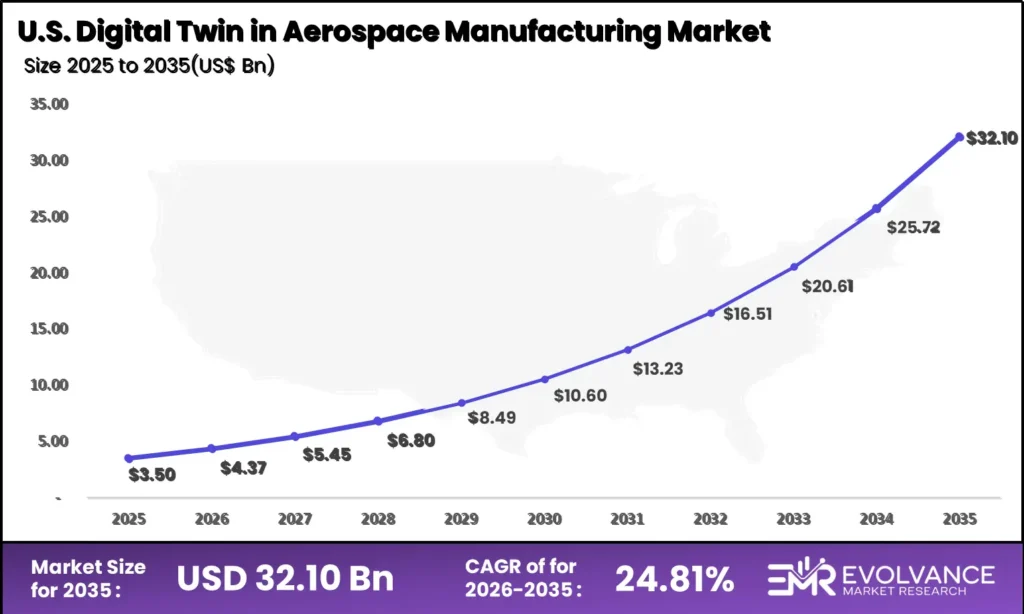

- US market: USD 3.50 billion in 2025, forecast to USD 32.10 billion by 2035 at 24.81% CAGR

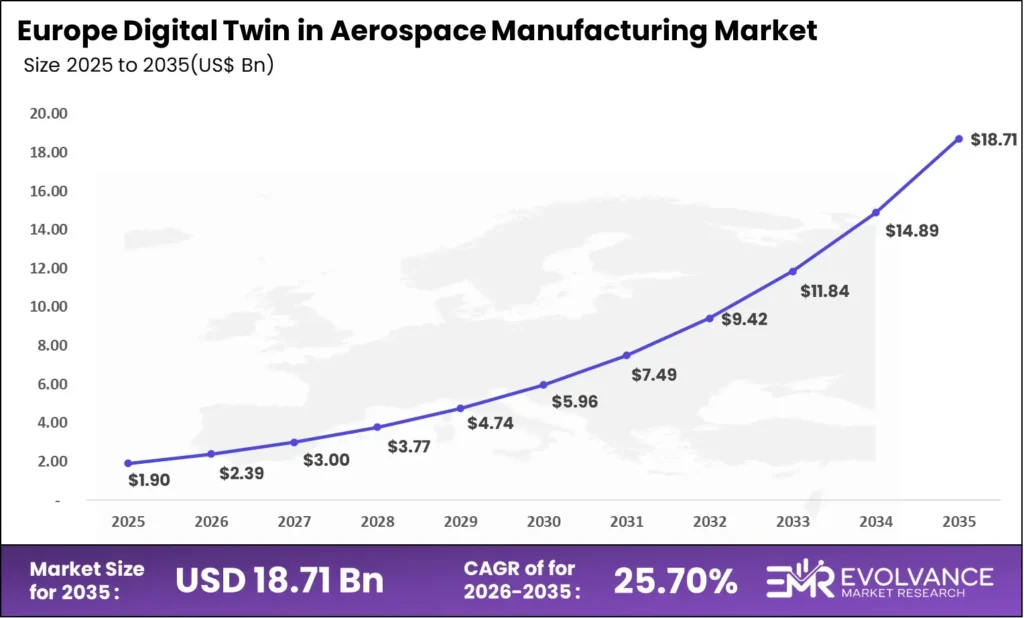

- Europe market: USD 1.90 billion in 2025, forecast to USD 18.71 billion by 2035 at 25.7% CAGR

- Dominant component segment: Software/Platform with 68.9% revenue share, driven by SaaS adoption, simulation-as-a-service models, and recurring license economics tied to aircraft program lifecycles

- Dominant application: Design & Engineering Simulation with 34.2% revenue share, anchoring pre-production digital validation workflows

- Dominant deployment mode: Cloud-Based with 59.4% revenue share, enabling multi-site collaborative simulation across global OEM supply chains

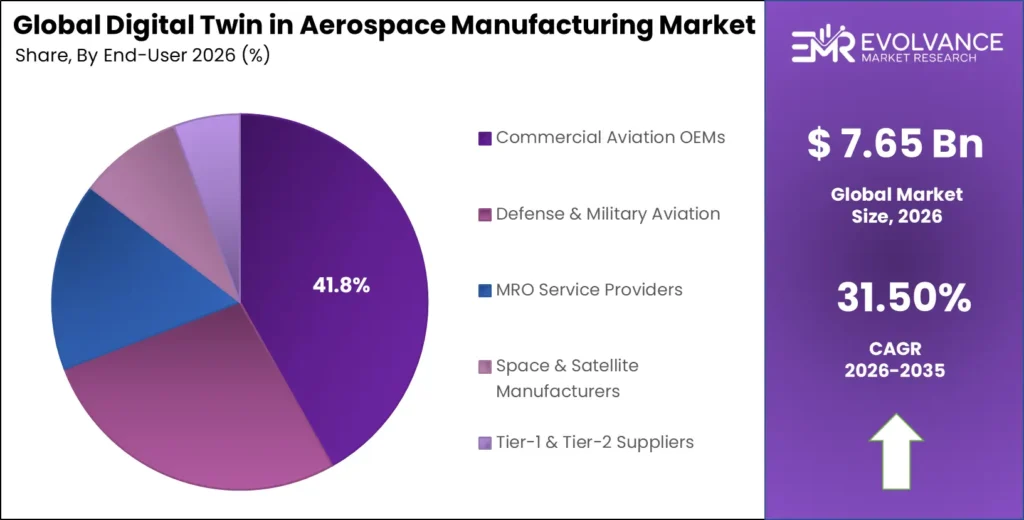

- Dominant end-user: Commercial Aviation OEMs with 41.8% revenue share, driven by aircraft development program digital thread mandates

- Dominant technology: AI-Driven Digital Twin leads all technology investment categories

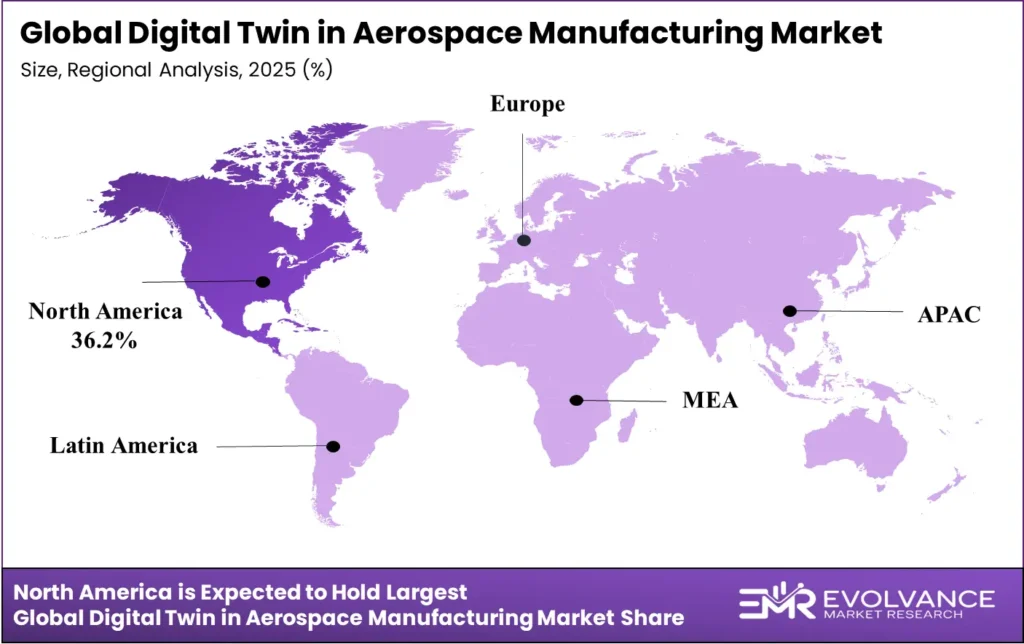

- North America: Largest regional share at 36.2%, valued at USD 2.11 billion in 2025

- Asia-Pacific: Fastest-growing region globally at 25.1% CAGR

US Digital Twin Aerospace Manufacturing Market

The US digital twin in aerospace manufacturing market will reach USD 32.10 billion by 2035 from USD 3.50 billion in 2025, growing at a CAGR of 24.81%. This growth rate sits slightly below the global average, reflecting a market where enterprise-grade platform adoption by Boeing, Lockheed Martin, and Northrop Grumman is already well underway, but where legacy MBD (model-based definition) integration and FAA digital certification pathway development are slowing net-new deployment velocity at Tier-2 and Tier-3 supplier levels.

The Department of Defense’s Digital Engineering Strategy — mandating digital twin-based design authority for all major defense acquisition programs — and the FAA’s ARAC digital airworthiness pilot initiatives are reshaping competitive dynamics in US aerospace simulation. Digital thread mandates now require contractors to validate component performance through simulation before any physical certification submission, compressing evaluation cycles that previously extended 18–24 months. NASA’s Digital Twin initiative is channeling additional federal capital into simulation-led design, targeting autonomous system certification — a segment with no physical-test alternative.

Europe Digital Twin Aerospace Manufacturing Market

The Europe digital twin in aerospace manufacturing market will reach USD 18.71 billion by 2035 from USD 1.90 billion in 2025, growing at a CAGR of 25.7%. Europe’s growth trajectory is underpinned by Airbus’s Skywise digital platform expansion, Safran’s manufacturing intelligence investments, and the European Commission’s Horizon Europe funding for digital manufacturing transformation across aerospace industrial clusters in France, Germany, the UK, and Spain.\

Airbus’s Digital Continuity across the A320 Family — linking design, tooling, assembly, and in-service data in a continuous digital thread — is the largest active digital twin aerospace deployment outside the US. The EU’s Clean Aviation Joint Undertaking, with EUR 4 billion in funding through 2030, requires digital twin validation as a co-investment condition. GDPR data residency requirements sustain demand for on-premises and EU-cloud-hosted simulation environments.

Market Overview: Why Aerospace Manufacturing Digital Twin Investment Is Structurally Accelerating

The digital twin in aerospace manufacturing market covers software platforms, AI-driven simulation tools, IoT integration middleware, and professional services that create real-time virtual replicas of aircraft components, manufacturing systems, production lines, and maintenance environments for design validation, production optimization, quality assurance, and predictive maintenance. The digital twin in aerospace manufacturing scope excludes general-purpose CAD and CAE software not specifically architected for aerospace-grade operation, and physical test infrastructure.

This analysis draws on aerospace OEM capital program disclosures, defense acquisition documentation, vendor earnings reports, and regulatory filings. Evolvance Market Research analysts cross-referenced digital twin in aerospace manufacturing segment shares against reported revenues from Boeing Digital Aviation, Airbus Digital, Siemens Digital Industries, PTC Inc., and Ansys Inc. across five regions and seven application categories.

Aerospace manufacturer motivation has shifted from post-production quality sampling to continuous digital-thread-enabled validation across the full product lifecycle. Digital twin in aerospace manufacturing platforms enabling real-time process state replication now occupy capital budget lines that traditional quality management software held five years ago, as aerospace manufacturing digital twin scope expands from individual component modeling to full aircraft system integration.

Component Analysis

Software/Platform Dominates with 68.9% Due to SaaS Adoption and Aircraft Program Lifecycle Economics

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Software/Platform | 68.9% | SaaS deployment, simulation-as-a-service, and recurring license economics tied to 10–25 year aircraft program lifecycles |

| Services | 31.1% | Integration complexity, PLM migration, and managed digital thread operations demand |

In 2025, Software/Platform held a dominant market position in the By Component segment of the digital twin in aerospace manufacturing market with a 68.9% share. No other segment achieves the same compounding revenue dynamic — aerospace manufacturing digital twin simulation platforms generate recurring license revenue while expanding usage-based billing as scope grows from single-component to full-aircraft system integration. Switching costs rise sharply once digital twin models are calibrated to OEM-specific aircraft geometry, material databases, and production process parameters accumulated over multi-year deployments. Aircraft program lifecycles of 25–40 years mean that once an aerospace digital twin platform is embedded in a commercial aircraft program’s design authority, it retains revenue through the entire production run and into the in-service phase — creating LTV multiples unavailable in shorter-cycle manufacturing digital twin markets.

Services operate as the integration layer converting digital twin in aerospace manufacturing platform licenses into certified operational value. PLM migration, digital thread architecture, sensor network integration, and AI model training services are growing alongside aerospace manufacturing digital twin deployments — particularly at Tier-2 and Tier-3 suppliers lacking internal talent to operate aerospace-grade simulation at program scale. The services segment generates lower margin than platform software but creates deeper customer relationships and cross-sell pathways into adjacent manufacturing intelligence and in-service data analytics contracts.

Application Analysis

Design & Engineering Simulation Dominates with 34.2% Due to Pre-Certification Digital Validation Mandates

| Application Segment | Share % | Primary Driver |

|---|---|---|

| Design & Engineering Simulation | 34.2% | Pre-certification digital validation mandates and aerodynamic/structural simulation integration |

| Predictive Maintenance & MRO | 24.7% | AOG cost reduction, prognostic health management, and fleet-wide sensor data integration |

| Production Process Optimization | 19.3% | Assembly line digital thread, robotic welding simulation, and composite layup optimization |

| Quality Assurance & Inspection | 13.1% | Automated optical inspection twin, CMM digital twin, and zero-defect manufacturing programs |

| Supply Chain & Logistics Simulation | 8.7% | Critical parts availability simulation and multi-tier supplier digital thread integration |

In 2025, Design & Engineering Simulation led digital twin in aerospace manufacturing application segments with a 34.2% share. This segment maps directly to the highest-value capital allocation decision in aerospace manufacturing — structural sizing, aerodynamic performance validation, and propulsion system integration for new aircraft programs where design errors carry correction costs in the hundreds of millions of dollars. OEMs using aerospace manufacturing digital twin-validated design models before physical prototype fabrication consistently report 20–35% reductions in engineering change order cycles, translating into measurable savings on tooling rework, certification test campaigns, and program schedule compression.

Predictive Maintenance and MRO is the fastest-growing aerospace digital twin application segment by revenue trajectory. AI models trained on digital twin in aerospace manufacturing-generated component degradation simulations identify failure precursors — turbine blade thermal fatigue signatures, landing gear actuator wear patterns, and avionics thermal cycling anomalies — before they manifest as airworthiness events. MRO operators with mature aerospace manufacturing digital twin deployments report unscheduled maintenance event reductions of 25–40% versus time-based scheduling. Each avoided AOG event at a major hub carries direct cost avoidance of USD 150,000–500,000 per incident, creating ROI frameworks that justify premium MRO digital twin platform investments.

Production Process Optimization benefits from the convergence of digital twin platforms and robotics in aerospace assembly. Airbus’s synchronized digital twins across A320 final assembly lines — where robotic drilling, fastening, and inspection are validated against physical assembly state — demonstrates the capability multiplier production digital twins provide over legacy CNC programming. For Tier-1 composite structures suppliers, aerospace manufacturing digital twin platforms reduce autoclave programming cycles and out-of-autoclave validation time, compressing part production lead times.

Quality Assurance and Inspection digital twins are transitioning to primary certification evidence generators. The FAA’s continued airworthiness directive framework increasingly accepts digital twin-validated design authority data as equivalent to physical test evidence for defined structural analysis categories — a regulatory evolution Boeing, Airbus, and their Tier-1 partners have co-developed through EASA and FAA technical standards bodies, directly reducing program test campaign costs.

Deployment Mode Analysis

Cloud-Based Dominates with 59.4% Due to Multi-Site Collaboration and OEM Supply Chain Connectivity

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Cloud-Based | 59.4% | Elastic compute scalability for large-model simulation and multi-site OEM/supplier collaboration |

| On-Premises | 28.3% | Classified program data sovereignty, export control compliance, and ITAR/EAR requirements |

| Hybrid | 12.3% | Regulated program data separation with cloud-scale compute access for unclassified workloads |

In 2025, Cloud-Based deployment held a dominant position in the digital twin in aerospace manufacturing deployment mode segment with a 59.4% share. Cloud platforms enable aerospace OEMs to scale simulation compute resources elastically during peak design campaign phases — full-aircraft CFD simulations requiring millions of CPU-core hours during aerodynamic optimization cycles — without sustaining year-round HPC infrastructure costs. AWS GovCloud, Microsoft Azure Government, and Google Cloud’s Aerospace vertical all offer export-controlled cloud regions with ITAR-compliant data handling, reducing the regulatory barriers that previously confined aerospace manufacturing digital twin simulation to on-premises environments.

On-Premises retains structural necessity for classified defense programs where ITAR, EAR, and classification requirements prohibit cloud-hosted simulation. These deployments command significant premiums — on-premises aerospace digital twin contracts average 2.8x the total contract value of equivalent cloud deployments due to air-gapped network architecture and dedicated program support. ITAR registration and DFARS compliance function as market access credentials for DoD prime contractor programs.

Hybrid deployment is growing as the preferred architecture for OEMs managing both classified and unclassified programs. Boeing’s hybrid digital twin architecture separates classified defense data in on-premises environments while leveraging Azure cloud for commercial aircraft simulation — providing both regulatory compliance and commercial simulation scalability. This pattern is propagating through the supply chain as Tier-1 suppliers adopt the same architecture to serve both commercial and defense OEM requirements.

End-User Analysis

Commercial Aviation OEMs Dominate with 41.8% Due to Digital Thread Program Mandates

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Commercial Aviation OEMs | 41.8% | Aircraft program digital thread mandates and multi-decade lifecycle simulation economics |

| Defense & Military Aviation | 27.4% | DoD Digital Engineering Strategy and classified platform digital authority requirements |

| MRO Service Providers | 16.2% | Predictive maintenance ROI, AOG reduction, and fleet health management SLA commitments |

| Space & Satellite Manufacturers | 8.9% | Launch vehicle simulation, satellite on-orbit twin, and reusable rocket refurbishment digital twin |

| Tier-1 & Tier-2 Suppliers | 5.7% | OEM-mandated digital thread participation and component design authority digital validation |

In 2025, Commercial Aviation OEMs held a dominant position in the By End-User segment with a 41.8% share. Boeing’s Digital Aviation Solutions, Airbus’s Skywise platform, and broad OEM adoption of MBSE are driving procurement of digital twin platforms spanning the full product development lifecycle. OEMs managing multi-generation aircraft coexistence — A320ceo/neo/XLR, B737 MAX/NG, B787 — face simulation complexity that legacy PLM tools cannot efficiently manage, with digital twin platforms delivering measurable program risk reductions quantifiable in reduced design freeze delays and lower certification costs.

Defense and Military Aviation procurement commands the highest average contract values. Major combat aircraft programs — including the F-35, FCAS, and GCAP — require dedicated digital twin environments maintaining design authority for classified aircraft systems across multi-decade lifecycles. The US Air Force’s ABMS and the UK’s Digital Backbone program both embed digital twin requirements as program entry criteria, creating recurring simulation revenue for vendors with ITAR registration and NISPOM compliance credentials.

Space and Satellite Manufacturers are the fastest-growing end-user segment by CAGR. SpaceX’s digital twins across Merlin and Raptor engine manufacturing, and commercial space entrants including Rocket Lab and Blue Origin, are expanding the addressable market for space-qualified aerospace manufacturing digital twin platforms. Reusable launch vehicle programs require digital twin models accumulating flight history data across multiple missions — a new category of in-service propulsion digital twin with no equivalent in commercial aviation.

Technology Analysis

AI-Driven Digital Twin Dominates Due to Autonomous Manufacturing Intelligence Investment Cycle

| Technology | Share % | Primary Driver |

|---|---|---|

| AI-Driven Digital Twin | Dominant | Generative AI for design optimization, autonomous anomaly detection, and predictive failure modeling |

| IoT-Integrated Digital Twin | — | Real-time sensor fusion from manufacturing equipment, tooling, and in-service aircraft components |

| AR/VR-Enhanced Digital Twin | — | Immersive assembly guidance, maintenance technician training, and remote expert collaboration |

| Physics-Based Simulation Twin | — | High-fidelity FEA/CFD certification evidence and validated structural analysis across load cases |

AI-Driven Digital Twin leads all technology investment categories. The combination of generative AI for design space exploration — generating and evaluating thousands of structural topology variants in hours rather than weeks — and machine learning for anomaly detection across manufacturing process sensor streams is creating a simulation-first design paradigm. Lockheed Martin’s AI-augmented digital twin program for F-35 component manufacturing integrates real-time machining process data with AI anomaly detection, demonstrating a 30% reduction in non-conformance escapes versus previous statistical process control approaches.

IoT-Integrated Digital Twin is transforming data fidelity for production floor digital twins. Sensor networks across CNC machining centers, composite layup equipment, autoclaves, and robotic assembly cells provide real-time process state data that elevates digital twins from static models to live manufacturing intelligence environments. Boeing’s 777X composite wing facility in Everett captures over 10 million sensor data points per day, feeding real-time updates into digital twin models that detect composite layup deviations before autoclave cycle initiation.

Physics-Based Simulation Twin remains the foundational technology layer for certification evidence generation. High-fidelity FEA and CFD digital twins, validated against physical test data across multiple load cases, are increasingly accepted by airworthiness authorities as primary or supplementary certification evidence. The FAA’s Advisory Circular AC 20-193 on CFD acceptance and EASA’s CS-25 digital modeling guidance have both expanded the scope of physics-based simulation accepted as equivalent to physical test evidence — directly expanding the certification value proposition of aerospace digital twin platforms.

Aircraft Type Analysis

Commercial Aircraft Dominates Due to Fleet Scale and Recurring In-Service Digital Twin Demand

| Aircraft Type | Share % | Primary Driver |

|---|---|---|

| Commercial Aircraft | 46.3% | Fleet-scale MRO digital twin and new aircraft program digital thread investment |

| Military Aircraft | 29.1% | Defense acquisition digital engineering mandates and classified platform sustainment |

| UAV/Drones | 14.2% | Autonomous system certification frameworks and high-volume manufacturing digital twin requirements |

| Spacecraft & Launch Vehicles | 10.4% | Reusable vehicle refurbishment digital twin and satellite constellation manufacturing optimization |

Commercial Aircraft holds the largest aircraft type segment share at 46.3%, driven by simultaneous demand for new program digital twins — covering the A321XLR, B777X, B737 MAX-10, and emerging narrowbody replacements — and in-service fleet digital twins serving airlines’ predictive maintenance requirements. The global commercial fleet of approximately 26,000 active aircraft, each generating continuous sensor data over a 25–30 year service life, creates a massive recurring market for aerospace manufacturing digital twin platforms.

UAV and Drone digital twins represent the highest-growth aircraft type sub-segment. The FAA’s UAM integration framework, military SUAS modernization programs, and commercial drone delivery expansion are creating demand for digital twin platforms supporting high-volume UAV manufacturing optimization and autonomous system certification. Joby Aviation, Archer, and Wisk are investing in digital twin-based certification strategies because physical test campaigns for novel eVTOL configurations would be prohibitively expensive without computational pre-validation.

Enterprise Size Analysis

Large Enterprises Dominate Due to Program Scale and PLM Integration Requirements

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Large Enterprises | Dominant | Aerospace program capital scale and complex PLM/ERP/MES integration requirements |

| SMEs | — | SaaS adoption and OEM-mandated digital thread supply chain participation |

Large Enterprises lead overall revenue — Tier-1 primes like Boeing, Airbus, Lockheed Martin, and Northrop Grumman deploy digital twin in aerospace manufacturing environments across full aircraft program scope, creating nine-to-ten-figure platform commitments over multi-decade contracts. Cloud-native aerospace manufacturing digital twin platforms on consumption-based pricing are progressively making simulation accessible to Tier-2 and Tier-3 suppliers, MRO independents, and UAM startups who previously lacked capital for enterprise-grade PLM-integrated deployments.

OEM digital thread mandates are the primary SME adoption accelerator. Boeing’s SQMS and Airbus’s Supply Chain Management 4.0 both require suppliers to demonstrate digital twin capability as a condition of long-term agreement qualification — mandating supplier investment as a procurement prerequisite and creating a top-down market development dynamic that reduces SME sales cycle friction.

Key Market Segments

By Component

- Software/Platform

- Services

By Application

- Design & Engineering Simulation

- Predictive Maintenance & MRO

- Production Process Optimization

- Quality Assurance & Inspection

- Supply Chain & Logistics Simulation

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By End-User

- Commercial Aviation OEMs

- Defense & Military Aviation

- Space & Satellite Manufacturers

- MRO Service Providers

- Tier-1 & Tier-2 Suppliers

By Technology

- AI-Driven Digital Twin

- IoT-Integrated Digital Twin

- AR/VR-Enhanced Digital Twin

- Physics-Based Simulation Twin

By Aircraft Type

- Commercial Aircraft

- Military Aircraft

- UAV/Drones

- Spacecraft & Launch Vehicles

By Enterprise Size

- Large Enterprises

- SMEs

Regional Analysis of Digital Twin Aerospace Manufacturing Market

North America Leads at 36.2% Share

| Region | Market Value (2025) | Share % | CAGR |

|---|---|---|---|

| North America (US) | USD 2.11 billion | 36.2% | 22.8% |

| Europe | USD 1.34 billion | 23.0% | 21.7% |

| Asia-Pacific | USD 1.16 billion | 19.9% | 25.1% (fastest) |

| China | USD 0.47 billion | Part of Asia-Pacific | 24.3% |

| Latin America | USD 0.52 billion | 9.0% | 20.1% |

| Middle East & Africa | USD 0.69 billion | 11.9% | 23.4% |

North America holds 36.2% of global digital twin in aerospace manufacturing revenue at USD 2.11 billion in 2025. Its structural advantage lies in the concentration of the world’s largest aerospace prime contractors — Boeing, Lockheed Martin, Northrop Grumman, RTX, and General Dynamics — combined with the DoD’s Digital Engineering Strategy mandating aerospace manufacturing digital twin adoption across every major defense acquisition program. The US accounts for approximately 38% of global aerospace and defense revenue, providing a demand foundation no other single market can match for digital twin in aerospace manufacturing vendors.

North America Digital Twin Aerospace Market: DoD Digital Engineering Mandates Drive Procurement

The US digital twin in aerospace manufacturing market, valued at USD 1.76 billion in 2025, will reach USD 13.84 billion by 2035 at 22.8% CAGR. The DoD’s Digital Engineering Strategy mandates digital twin-based design authority for all ACAT I programs, creating non-discretionary procurement requirements across all prime contractors. The US Air Force’s CBM+ mandate extends digital twin requirements into aircraft sustainment, creating recurring platform revenue independent of new aircraft production cycles.

Europe Digital Twin Aerospace Market Trends

Europe’s digital twin in aerospace manufacturing market reached USD 1.34 billion in 2025, driven by Airbus program digital thread expansion, MBDA missile system digital validation, and Eurofighter Typhoon mid-life upgrade simulation requirements. The EU’s Clean Aviation Joint Undertaking — with EUR 4 billion through 2030 — requires digital twin validation as a co-investment condition. Germany’s Hamburg hub, France’s Toulouse cluster, and the UK’s Farnborough and Bristol sectors represent concentrated procurement corridors that Siemens, Dassault Systèmes, and PTC are actively targeting.

Asia-Pacific Digital Twin Aerospace Manufacturing Market: Fastest-Growing Region

Asia-Pacific’s 25.1% CAGR makes it the fastest-growing major region for digital twin aerospace manufacturing. Four country-level growth engines drive this trajectory. China’s COMAC is deploying digital twin platforms across C919 and CR929 widebody programs — with a domestic vendor preference architecture that creates opportunities for Siemens, PTC, and ANSYS in joint-venture structures. Japan’s Kawasaki Heavy Industries H3 rocket and Mitsubishi SpaceJet program revival are creating demand for aerospace-grade digital twin platforms meeting JAXA and METI requirements. India’s HAL TEJAS MkII fighter and ATL simulation infrastructure expansion represent the largest single defense aerospace digital twin procurement opportunity in South Asia.

Middle East & Africa Digital Twin Aerospace Market Trends

The Middle East and Africa region presents a structurally distinctive growth opportunity driven by sovereign aerospace capability investment. Saudi Arabia’s Vision 2030 aviation localization mandate — targeting 60% domestic MRO capability for SAUDIA by 2030 — is driving investment in MRO digital twin platforms as the technical foundation of domestic capability development. The UAE’s Strata Manufacturing facility in Abu Dhabi, producing A320 Family wing components under Airbus direction, is deploying production digital twin platforms as part of its manufacturing excellence program. Emirates Engineering’s fleet health management digital twin investment — targeting predictive maintenance across its 260+ aircraft widebody fleet — represents one of the largest single MRO digital twin procurement opportunities outside North America and Europe.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Rest of Europe

Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Companies: Three Players Define the Aerospace Digital Twin Competitive Landscape

Three companies — Siemens AG, PTC Inc., and Dassault Systèmes SE — dominate global digital twin in aerospace manufacturing revenue through platform breadth, aerospace-specific PLM integration credentials, and OEM relationship depth accumulated over multi-decade program partnerships. This concentration in the aerospace manufacturing digital twin competitive landscape creates high entry barriers in Tier-1 OEM accounts but leaves AI-native, cloud-first, and domain-specific simulation segments meaningfully open for challengers with differentiated technology architectures.

| Company | Revenue / Segment | Growth Rate | Year Reported |

|---|---|---|---|

| Siemens AG (Digital Industries) | EUR 9.8 billion | -7% nominal (+3% organic) | FY2024 |

| Siemens Xcelerator Platform | Part of Digital Industries | +12% organic | FY2024 |

| PTC Inc. | USD 2.31 billion | +12% | FY2024 |

| Dassault Systèmes SE | EUR 6.02 billion | +8% | FY2024 |

| Ansys Inc. (now Synopsys) | USD 2.47 billion | +10% | FY2024 |

| Boeing Digital Aviation Solutions | Part of BDS segment | Embedded | FY2024 |

According to Siemens FY2024 results, its Xcelerator cloud platform — including Teamcenter PLM, NX CAD, and Simcenter simulation as core aerospace digital twin components — achieved 12% organic growth. Siemens’ aerospace customers include Airbus, Embraer, and Spirit AeroSystems. Its installed base of Teamcenter PLM across hundreds of aerospace supplier organizations creates a structural cross-sell advantage for digital twin upgrades that cloud-native competitors cannot easily replicate.

PTC’s FY2024 ARR grew 12% to USD 2.09 billion, with aerospace representing one of its highest-growth verticals. PTC’s Windchill PLM and Vuforia AR platforms are deployed across Lockheed Martin, GE Aerospace, and RTX for design engineering and AR-guided assembly use cases. PTC’s ServiceMax acquisition extends its platform value from new production into the multi-decade MRO lifecycle representing the largest total addressable digital twin revenue pool in commercial aviation.

Dassault Systèmes reported EUR 6.02 billion in FY2024 at +8% growth, with aerospace at approximately 25% of group revenue. Its 3DEXPERIENCE platform — deployed across Airbus’s Digital Continuity, Boeing’s 777X, and Embraer’s E-Jet E2 — is the most broadly deployed aerospace manufacturing digital twin architecture in commercial aviation, with SIMULIA FEA and CATIA digital manufacturing creating a vertically integrated environment spanning aerodynamic design through factory process optimization.

Microsoft is the most strategically significant competitive entrant from outside traditional aerospace PLM. Through Azure Digital Twins, Azure HPC, and its deepening Boeing partnership, Microsoft is positioning Azure as the compute and data infrastructure layer for digital twin in aerospace manufacturing platforms from multiple ISV vendors — creating both a cloud distribution channel and a competitive threat in the platform integration layer.

Top Key Players

- Siemens AG

- PTC Inc.

- Dassault Systèmes SE

- Ansys, Inc. (Synopsys)

- Boeing Digital Aviation Solutions

- Airbus (Skywise / Digital Continuity)

- GE Aerospace (Digital Solutions)

- Microsoft Corporation

- Hexagon AB

- Rockwell Collins (RTX)

- Cognite AS

- Altair Engineering

- Others

Related Markets: 5 Segments Shaping Digital Twin Aerospace Manufacturing

Five adjacent markets intersect directly with the digital twin in aerospace manufacturing market. Each carries distinct growth dynamics, regulatory exposure, and buyer profiles — but all share the same upstream technology stack (cloud HPC, AI/ML frameworks, IoT sensor platforms, and PLM data architectures) and many of the same aerospace OEM and defense contractor procurement channels as the digital twin in aerospace manufacturing segment.

- Aerospace Simulation & Modeling Software Market: Valued at USD 4.18 billion in 2025, forecast to reach USD 18.94 billion by 2035 at a CAGR of 16.3%. The aerospace simulation software market growth is driven by the increasing acceptance of computational evidence in FAA and EASA certification frameworks. Digital twin platforms growing 23.7% annually are outpacing the broader simulation software category, driven by their real-time data integration and lifecycle continuity capabilities.

- Aerospace AI Market: Valued at USD 3.24 billion in 2025, forecast to reach USD 21.87 billion by 2035 at a CAGR of 21.1%. The aerospace AI market growth is driven by the compounding relationship between AI model performance and digital twin-generated synthetic training data. OEMs investing in digital twin platforms accelerate AI-driven design optimization and autonomous manufacturing capabilities compared to competitors with limited simulation data pipelines.

- Industrial IoT in Aerospace Market: Valued at USD 5.67 billion in 2025, forecast to reach USD 32.14 billion by 2035 at a CAGR of 18.9%. The industrial IoT aerospace market growth directly enables digital twin data fidelity improvements, as sensor network density across manufacturing equipment and in-service aircraft components provides the real-time state data that elevates digital twins from static simulation models to continuous manufacturing intelligence environments.

- Aerospace MRO Market: Valued at USD 102.3 billion in 2025, forecast to exceed USD 178 billion by 2035 at a CAGR of 5.7%. While the MRO market grows at a lower overall rate, digital twin penetration within MRO is accelerating at 24%+ annually as predictive maintenance platforms demonstrate AOG cost reductions that justify premium platform investments, creating a high-value growth layer within the larger MRO addressable market.

- Aerospace 3D Printing & Additive Manufacturing Market: Valued at USD 4.89 billion in 2025, forecast to reach USD 22.46 billion by 2035 at a CAGR of 16.5%. The additive manufacturing aerospace growth is tightly coupled with digital twin investment, as qualified additive manufacturing processes require digital twin-enabled process validation to achieve FAA 14 CFR Part 21 production approval — making digital twin platforms a certification prerequisite for aerospace AM adoption.

Key Growth Drivers of Digital Twin Aerospace Manufacturing Market

Next-Generation Aircraft Programs and Digital Engineering Mandates Drive Structural Platform Demand

Next-generation aircraft program investment is the single most powerful structural force driving digital twin in aerospace manufacturing market growth. The combined development investment for programs including the Boeing 777X, Airbus A321XLR, next-generation narrowbody replacements, and multiple next-generation fighter and bomber programs represents over USD 150 billion in active aerospace R&D spending that flows through aerospace manufacturing digital twin platforms as a foundational enabling technology. Current and next-generation programs are designed with simulation-first validation philosophies — the 777X completed over 2 million hours of structural simulation before the first physical test article was fabricated. Unlike previous aircraft generations where physical prototype fabrication was the primary validation mechanism, digital twin in aerospace manufacturing-enabled design review now precedes metal cutting on every major program.

The DoD’s Digital Engineering Strategy creates the most structurally compelling regulatory demand driver for digital twin in aerospace manufacturing adoption. Published by the Office of the Under Secretary of Defense for Research and Engineering, this strategy mandates authoritative digital models as the primary design and manufacturing product for all ACAT I defense acquisition programs. For prime contractors including Lockheed Martin, Northrop Grumman, and RTX, compliance is not optional — aerospace manufacturing digital twin platforms are now program entry requirements rather than discretionary investments. This mandate creates demand floors across the defense aerospace segment that persist regardless of discretionary digital transformation budget cycles.

Sustainability-driven design optimization is a high-value digital twin in aerospace manufacturing use case in commercial aviation. The industry’s net-zero CO2 commitment by 2050 under IATA’s resolution — requiring structural weight reduction, aerodynamic efficiency improvement, and SAF compatibility across the entire commercial fleet — creates continuous demand for aerospace digital twin-based design optimization across every new aircraft development cycle. Airbus’s ZEROe hydrogen propulsion program and Boeing’s ecoDemonstrator both use digital twin simulation as the primary tool for evaluating novel propulsion concepts that cannot be physically tested at full program scale during the research phase.

Restraints

PLM Integration Debt and Aerospace Simulation Talent Scarcity Compress Deployment Velocity

Legacy PLM and CAE system integration is the primary deployment barrier for digital twin in aerospace manufacturing platform adoption in incumbent Tier-1 manufacturers. Product lifecycle management environments built over 30+ years of CATIA, NX, and Pro/E CAD data accumulation contain geometric data model inconsistencies, material property database gaps, and manufacturing process parameter incompatibilities that prevent aerospace manufacturing digital twin platforms from achieving the simulation fidelity their business cases require. Integration projects scoped at 12–18 months routinely extend to 30–36 months when legacy data quality issues are fully surfaced — compressing the IRR that program offices modeled at platform procurement approval.

Aerospace simulation talent scarcity compounds the integration challenge for digital twin in aerospace manufacturing deployments. These platforms require engineers who understand both ML model architecture and aerospace-specific physics — structural dynamics, aeroelasticity, propulsion thermodynamics, and manufacturing process metallurgy. According to the AIA, the US aerospace industry faces a shortage of 340,000 engineers and technicians by 2028, with advanced simulation and digital engineering specialties representing the most acute shortage categories.

Certification framework maturity for aerospace manufacturing digital twin evidence presents a third constraint layer. While FAA and EASA digital twin in aerospace manufacturing acceptance frameworks are progressing, regulatory guidance development trails technology adoption rates. Aerospace OEMs cannot deploy digital twin platforms as primary certification evidence tools in categories where guidance is still under development — limiting financial return on platform investment until equivalency acceptance criteria are formally published. This pacing constraint is most acute for eVTOL and hydrogen propulsion programs where both the technology and certification framework are simultaneously under development.

Opportunities

Commercial Space Economy and AI-Driven Design Optimization Unlock Premium Revenue Segments

The commercial space economy expansion is creating the highest-growth new end-user segment for digital twin in aerospace manufacturing platforms. SpaceX’s Starship production ramp, Amazon Project Kuiper’s satellite constellation manufacturing scale-up, and NASA’s CLPS program are creating demand for space-grade aerospace manufacturing digital twin platforms that handle both launch vehicle manufacturing optimization and on-orbit satellite health management. Per Morgan Stanley estimates, the space economy will reach USD 1 trillion by 2040, with digital twin in aerospace manufacturing investment growing proportionally to commercial space vehicle production rates.

AI-driven generative design integration represents the highest near-term ROI opportunity for aerospace digital twin in manufacturing platform vendors. Generative AI tools producing novel structural topology variants — validated through integrated aerospace manufacturing digital twin simulation before physical fabrication — are compressing aerospace structural design cycles from months to days for specific component categories. Airbus’s generative-design-enabled cabin partition structures demonstrated a 45% weight reduction while maintaining certification equivalency, creating premium pricing power for digital twin platforms with embedded AI design optimization capabilities.

Sustainable Aviation Fuel and hydrogen propulsion certification represents a white-space digital twin in aerospace manufacturing opportunity with no physical-test alternative at program scale. Aircraft manufacturers developing hydrogen combustion propulsion systems cannot validate engine, fuel system, and airframe integration performance exclusively through physical test campaigns — the cost and timescale are incompatible with commercial program development schedules. Aerospace manufacturing digital twin platforms modeling hydrogen fuel system thermodynamics and combustion dynamics across the full flight envelope create a pre-certification validation capability that physical testing cannot economically replicate, establishing premium pricing power independent of cost-reduction value arguments.

Latest Trends in Aerospace Manufacturing Digital Twin Market

Generative AI Design Twins and Digital Thread Standardization Reshape Platform Economics

Generative AI-native digital twins — where large language models and diffusion models collaborate with physics-based simulation engines to simultaneously explore design space and validate certification compliance — are redefining the value proposition of aerospace digital twin platforms beyond visualization and process monitoring toward autonomous design authority. NVIDIA’s Omniverse platform, extended with Modulus physics-informed neural networks for aerospace structural simulation, has demonstrated design optimization cycle acceleration of 15–50x versus traditional FEA-based parametric design studies — a capability multiplier that is pulling GPU computing infrastructure investment into aerospace engineering environments previously dominated by CPU-based HPC clusters.

Digital thread standardization through AS9100, LOTAR International, and AP242 STEP file format evolution are transforming interoperability across aerospace digital twin deployments. LOTAR International’s archiving standards — co-developed by Airbus, Boeing, Safran, MTU, and major defense contractors — define the data formats and metadata structures that digital twin platforms must support for multi-decade program data continuity. Vendors with native LOTAR-compliant data archiving and AP242 3D annotation support hold a structural procurement advantage in commercial aviation OEM selections where 30-year data accessibility is non-negotiable.

Quantum computing integration for aerospace optimization is emerging as a longer-horizon trend with near-term simulation implications. IBM’s Quantum Network and IonQ’s aerospace partnerships are exploring quantum optimization algorithms for structural topology, airspace routing, and composite layup sequencing problems that exceed classical computing capacity at full-aircraft scale. Aerospace OEMs establishing quantum-digital twin research programs in 2025–2026 are positioning for a computational advantage window in the 2029–2033 timeframe that Airbus, Boeing, and Lockheed Martin are actively scoping in long-range technology roadmaps.

Recent Developments: Siemens, PTC, and Dassault Systèmes Lead 2025–2026

- February 2026 — Siemens launched Xcelerator for Aerospace & Defense 2026, integrating generative AI-assisted structural topology optimization within the Simcenter simulation environment, validated against Airbus A320 Family component weight reduction targets and qualified for EASA CS-25 supplemental structural analysis.

- January 2026 — PTC announced its Windchill 22.0 platform update embedding real-time IoT sensor data fusion for production floor digital twins, with Boeing 737 MAX production line deployment as the reference implementation, targeting a 15% reduction in quality escape rates during fuselage panel assembly.

- December 2025 — Dassault Systèmes launched its 3DEXPERIENCE.Cloud Aerospace Edition with integrated SIMULIA AI-driven fatigue life prediction, enabling airframe structural digital twins to generate supplementary certification evidence for FAA AC 25.571 damage tolerance analysis without separate physical coupon test campaigns.

- November 2025 — Ansys (Synopsys) released Ansys SimAI 2.0 for aerospace applications, extending its physics-informed neural network simulation platform with validated hypersonic aerodynamics and propulsion thermal modeling capabilities, attracting procurement commitments from three US Air Force Research Laboratory programs.

- October 2025 — GE Aerospace launched its FlightPulse+ predictive maintenance digital twin platform for commercial operators, integrating real-time LEAP and GE9X engine sensor data with physics-based degradation models, targeting 40% reduction in unscheduled engine removal events for launch airline customers.

- September 2025 — Airbus Digital expanded its Skywise Health Monitoring platform to cover full A350 structural health monitoring data integration, with a digital twin of the A350 composite wing structure processing 800,000 flight data parameters per flight to generate predictive maintenance intelligence for airline operators.

Report Features

| Feature | Description |

|---|---|

| Market Value (2025) | USD 5.82 billion |

| Forecast Revenue (2035) | USD 89.99 billion |

| CAGR (2026–2035) | 31.50% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Software/Platform, Services), By Application (Design & Engineering Simulation, Predictive Maintenance & MRO, Production Process Optimization, Quality Assurance & Inspection, Supply Chain & Logistics Simulation), By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By End-User (Commercial Aviation OEMs, Defense & Military Aviation, Space & Satellite Manufacturers, MRO Service Providers, Tier-1 & Tier-2 Suppliers), By Technology (AI-Driven Digital Twin, IoT-Integrated, AR/VR-Enhanced, Physics-Based Simulation), By Aircraft Type (Commercial, Military, UAV/Drones, Spacecraft), By Enterprise Size (Large Enterprises, SMEs) |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Dominant Segment | Software/Platform with 68.9%; Commercial Aviation OEMs with 41.8%; Design & Engineering Simulation with 34.2% |

| Dominant Region | North America with 36.2%; Asia-Pacific fastest-growing at 25.1% CAGR |

| Dominant Technology | AI-Driven Digital Twin |

| Regulatory Framework | FAA AC 20-193, EASA CS-25, DoD Digital Engineering Strategy, AS9100 Rev D, LOTAR International, ITAR/EAR, DFARS Clause 252.204-7012, 3GPP (UAM), FAA Part 107/135 UAS |

| Competitive Landscape | Siemens AG, PTC Inc., Dassault Systèmes SE, Ansys Inc. (Synopsys), Boeing Digital Aviation Solutions, Airbus Skywise, GE Aerospace Digital Solutions, Microsoft Corporation, Hexagon AB, Rockwell Collins (RTX), Cognite AS, Altair Engineering |

Sources

- Aerospace Industries Association (AIA) — Aerospace & Defense Workforce Study 2025 | https://www.aia-aerospace.org

- US Department of Defense — Digital Engineering Strategy | https://ac.cto.mil/digital-engineering/

- FAA — Advisory Circular AC 20-193 (CFD Acceptance for Certification) | https://www.faa.gov/regulations_policies/advisory_circulars

- EASA — CS-25 Amendment 28 Digital Modeling Guidance | https://www.easa.europa.eu/en/document-library/certification-specifications

- Siemens AG — Annual Report 2024 | https://www.siemens.com/global/en/company/investor-relations

- PTC Inc. — FY2024 Annual Report & Earnings | https://investor.ptc.com

- Dassault Systèmes SE — FY2024 Financial Results | https://investor.3ds.com

- Ansys Inc. — FY2024 Annual Report | https://investors.ansys.com

- IATA — Net-Zero 2050 Commitment and SAF Roadmap | https://www.iata.org/en/programs/environment/flyzero

- EU Clean Aviation Joint Undertaking — Work Programme 2024-2027 | https://www.clean-aviation.eu

- Boeing — 2024 Annual Report & Digital Aviation Solutions | https://investors.boeing.com

- Airbus — Digital and Innovation Report 2024 | https://www.airbus.com/en/innovation

- GE Aerospace — 2024 Annual Report | https://www.geaerospace.com/investors

- NASA — Digital Twin Initiative Overview | https://www.nasa.gov/digital-twin

- LOTAR International — Long Term Archiving and Retrieval Standards | https://www.lotar-international.org

- Morgan Stanley — Space Economy Research Report 2024 | https://www.morganstanley.com/ideas/investing-in-space