What is the Hair Loss Treatment Market Size?

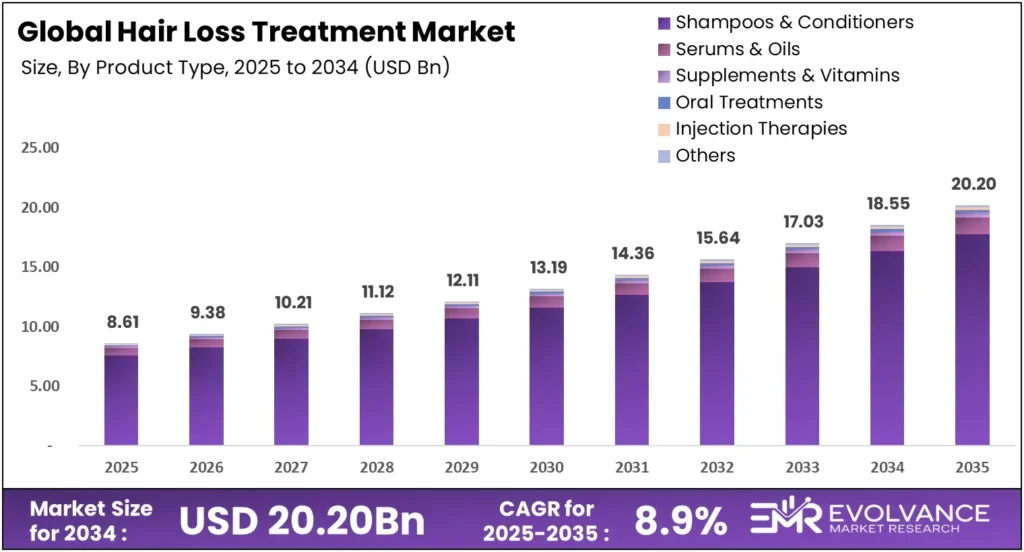

The global Hair Loss Treatment market will reach USD 20.20 billion by 2035 from USD 8.61 billion in 2025. Growing at a CAGR of 8.9% during the forecast period 2026 to 2035, the market benefits from rising androgenetic alopecia prevalence across 50 million men and 30 million women in the US alone. FDA approval of deuruxolitinib in July 2024 and a surge in biotech funding signal a market shifting from cosmetic management toward clinical regeneration.

Market Highlights

- The global hair loss treatment market reached USD 8.61 billion in 2025 and will grow to USD 20.20 billion by 2035 at a CAGR of 8.9%.

- Shampoos & Conditioners hold the dominant product segment with 88.21% revenue share, driven by OTC accessibility and repeat purchase frequency.

- North America leads all regions with 43.9% market share valued at USD 3.77 billion in 2025.

- Female buyers account for 71.03% of revenue by gender — the largest and fastest-growing gender segment globally.

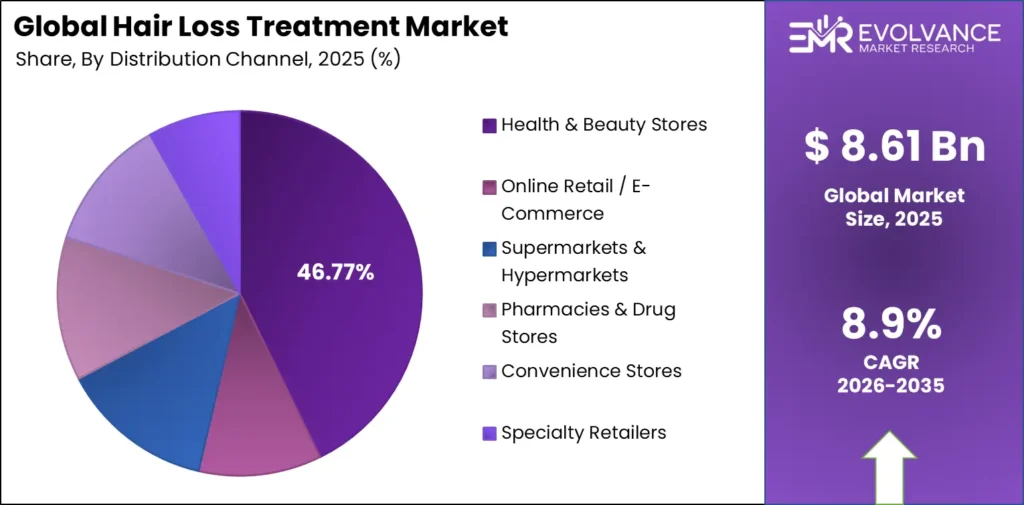

- Health & Beauty Stores command 46.77% of distribution channel revenue, anchoring the primary retail path for OTC hair loss products.

Market Overview

The hair loss treatment market covers pharmaceutical, cosmetic, and regenerative products used to slow, stop, or reverse hair loss across conditions including androgenetic alopecia, alopecia areata, and telogen effluvium. It spans OTC shampoos and serums, prescription drugs, surgical procedures, and emerging cell-based therapies — serving dermatologists, retail consumers, and telehealth platforms.

This analysis draws on regulatory filings, clinical trial data, and publications from the American Academy of Dermatology and the International Society of Hair Restoration Surgery. Evolvance Market Research analysts found primary data across 5 regions and 5 segment dimensions, validating findings against original fieldwork rather than aggregated public sources.

Hair loss conditions affect both clinical and consumer markets — pushing demand across dermatology practices, retail pharmacy, direct-to- consumer telehealth platforms, and prestige beauty channels. Pharmaceutical companies, consumer health brands, and biotech startups all compete for the same patient and consumer base.

According to Dermatology Times’ 2025 data, 50 million men and 30 million women in the US carry androgenetic alopecia diagnoses — making pattern hair loss the dominant disease indication structurally. Insurers broadly exclude hair loss treatments in major markets, per PMC 2025 data, pushing most purchase decisions to out-of-pocket spending.

Product Type: Shampoos Lead With 88.21% Share

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Shampoos & Conditioners | 88.21% | OTC access, repeat purchase cycle |

| Serums & Oils | — | Premiumization and targeted application |

| Supplements & Vitamins | — | Wellness positioning, female segment pull |

| Oral Treatments | — | Prescription and off-label oral minoxidil adoption |

| Injection Therapies | — | Clinic-based PRP and mesotherapy demand |

| Laser Treatments | — | FDA-cleared low-level laser therapy devices and in-clinic procedures |

| Surgical Treatments | — | Hair transplantation for permanent correction |

| Topical Treatments | — | Minoxidil formulations across OTC and Rx channels |

Shampoos & Conditioners dominate with 88.21% revenue share due to OTC accessibility and high repeat purchase frequency.

In 2025, Shampoos & Conditioners held a dominant market position in the By Product Type segment of the Hair Loss Treatment Market, with an 88.21% share. This reflects a structural reality: most consumers enter the hair loss category through familiar retail formats before progressing to prescription or clinical options. Daily-use formats lower the treatment barrier and sustain volume — making shampoos both the entry point and the revenue foundation of the entire market.

Serums & Oils represent the fastest-growing non-dominant product sub-segment, driven by premiumization and targeted scalp application formats. Brands like Nutrafol — a leading Nutrafol market position holder in the clinical supplement and serum channel — position these as step-up solutions for consumers seeking clinical-adjacent results without a prescription. This segment captures buyers already in the market but moving toward higher-efficacy formats.

Gender: Female Segment Holds 71.03% Revenue Share

| Gender | Share % | Primary Driver |

|---|---|---|

| Female | 71.03% | Hormonal hair loss, postpartum, and menopause |

| Male | — | Androgenetic alopecia, DTC platform adoption |

| Children | — | Alopecia areata in pediatric populations |

Female buyers dominate with 71.03% revenue share, driven by hormonal hair loss across postpartum and menopausal life stages.

In 2025, the female segment held a 71.03% revenue share in the female hair loss treatment market by gender. According to chemist-4-u.com’s January 2026 data, 40% of women experience pattern hair loss by age 50 — a figure that confirms hair loss treatment for women as the market’s highest-volume gender segment.

Postmenopausal women show higher prevalence of female pattern hair loss with limited premium uptake, per PMC 2025 research. Postpartum hair loss treatment and menopause hair loss treatment represent structurally underserved sub-segments — hormonal-linked hair loss responds poorly to male-formulated products, pushing differentiated product demand and creating a clear white space for clinical-grade OTC and telehealth solutions.

Distribution: Health & Beauty Stores at 46.77%

| Channel | Share % | Primary Driver |

|---|---|---|

| Health & Beauty Stores | 46.77% | Product trial, in-store expert guidance |

| Online Retail / E-Commerce | — | DTC subscription models, privacy of purchase |

| Supermarkets & Hypermarkets | — | Mass OTC shampoo penetration |

| Pharmacies & Drug Stores | — | Prescription adjacency and pharmacist trust |

| Convenience Stores | — | Impulse and travel-format purchases |

| Specialty Retailers | — | Prestige and professional-grade positioning |

Health & Beauty Stores lead distribution with 46.77% revenue share, anchored by product trial access and in-store consultation.

Health & Beauty Stores hold 46.77% of distribution revenue. This share persists because physical retail gives consumers the ability to evaluate product claims, read ingredient labels, and receive staff guidance before committing to a treatment regimen. Hair loss treatment online retail grows fastest as DTC platforms capture consumers who prioritize privacy and subscription convenience over in-store discovery.

Pharmacies & Drug Stores hold structural advantage in the prescription-adjacent segment. Minoxidil’s OTC reclassification in key markets made pharmacy the default channel for consumers stepping up from shampoo to active treatment. This channel benefits every time a new OTC treatment receives regulatory approval, giving it a durable revenue floor regardless of which brand leads.

Route of Administration: Topical Treatments Dominate

Topical treatments lead the route of administration segment across the hair loss treatment market.

| Route | Share % | Primary Driver |

|---|---|---|

| Topical | Dominant | Minoxidil OTC availability, daily ease of use |

| Oral | — | Finasteride Rx and off-label oral minoxidil adoption in the finasteride market and oral minoxidil market |

Disease Type: Androgenetic Alopecia Leads Demand

Androgenetic alopecia leads the disease type segment as the most prevalent and commercially mature hair loss condition.

| Disease Type | Share % | Primary Driver |

|---|---|---|

| Androgenetic Alopecia | Largest | Genetic prevalence, established Rx pipeline |

| Alopecia Areata | — | JAK inhibitor approvals expanding treatment options |

| Telogen Effluvium | — | Postpartum and stress-triggered shedding demand |

| Cicatricial Alopecia | — | Scarring conditions requiring clinical intervention |

| Traction Alopecia | — | Mechanical damage from styling in target demographics |

Market Segments Covered in the Report

By Product Type

- Shampoos & Conditioners

- Serums & Oils (hair oil)

- Supplements & Vitamins

- Oral Treatments

- Injection Therapies

- Laser Treatments

- Surgical Treatments

- Topical Treatments

By Distribution Channel

- Health & Beauty Stores

- Online Retail / E-Commerce

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Convenience Stores

- Specialty Retailers

By Gender

- Female

- Male

- Children

By Route of Administration

- Topical

- Oral

By Disease Type

- Androgenetic Alopecia

- Alopecia Areata

- Telogen Effluvium

- Cicatricial Alopecia

- Traction Alopecia

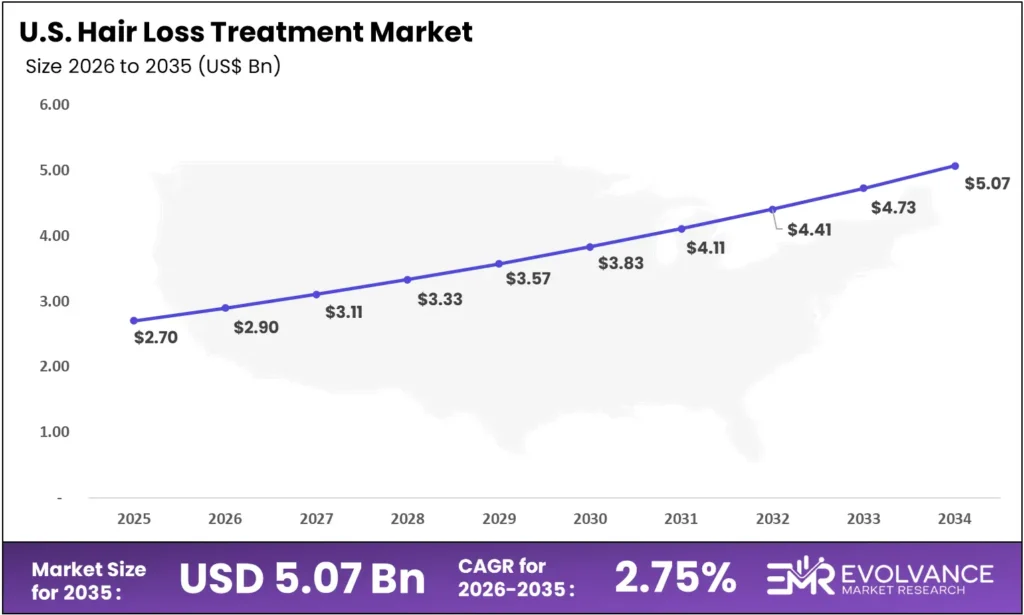

United States Hair Loss Treatment Market

The United States hair loss treatment market reached USD 2.7 billion in 2025, growing at a CAGR of 7.25% through 2035 — slightly below the global average of 8.9%, reflecting a mature OTC channel where established brands already dominate mass-market shelf space.

This maturity creates a paradox. The largest single-country market grows more slowly than emerging peers, but it holds disproportionate influence over global clinical and regulatory timelines. FDA approvals — including deuruxolitinib’s July 2024 clearance — set the standard that reshapes prescribing behavior across all major markets.

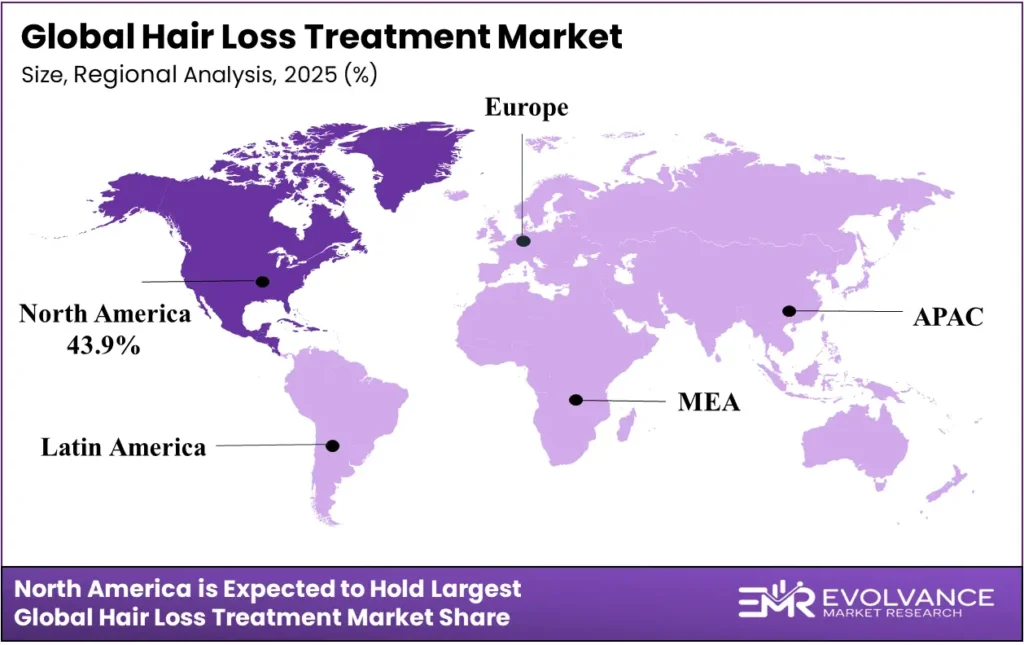

Hair Loss Treatment Market Regional Insights

North America Holds 43.9% Share at USD 3.77 Billion

| Region | Market Value (2025) | Share % | Year |

|---|---|---|---|

| North America | USD 3.77 Billion | 43.9% | 2025 |

| Asia Pacific | — | Fastest-growing | 2025 |

| Europe | — | Second by share | 2025 |

| Latin America | — | Emerging | 2025 |

| Middle East & Africa | — | Emerging | 2025 |

North America holds 43.9% of global hair loss treatment revenue at USD 3.77 billion in 2025. This share reflects the world’s deepest OTC pharmaceutical retail infrastructure, high consumer willingness to spend on hair health, and the FDA’s role as the global regulatory anchor for new treatment approvals.

Asia Pacific Hair Loss Treatment Market Trends

Asia Pacific leads all regions in growth rate, propelled by aging populations in Japan and South Korea, a booming K-beauty-adjacent scalp care culture, and rising middle-class spending on premium treatments in China and India. The Asia Pacific hair loss treatment market benefits from South Korea’s dense dermatology clinic network and active domestic patent filings in follicle-stimulating compounds — positioning it as the region’s clinical innovation hub for the 2026–2035 forecast period.

Europe Hair Loss Treatment Market Trends

Europe holds the second-largest regional share, anchored by Germany, France, and the UK — markets where dermatologist referral pathways are well-established and prescription hair loss treatments carry stronger clinical authority than OTC alternatives.

Latin America Hair Loss Treatment Market Trends

Brazil and Mexico drive Latin America hair loss treatment market demand, where high androgenetic alopecia prevalence meets a growing urban middle class with rising discretionary health spending. Distribution remains pharmacy-led, giving international OTC brands a clear channel entry point without building specialty retail from scratch.

Middle East and Africa Hair Loss Treatment Market Trends

The Middle East and Africa region remains an early-stage market where premium clinic-based treatments — PRP therapy and hair transplantation — outpace OTC product adoption among higher-income urban consumers in GCC countries. Mass-market OTC penetration in South Africa and North Africa offers a separate, more price-sensitive growth vector.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The FDA governs hair loss drug approvals in the US under its drug and device classification framework. Minoxidil’s OTC reclassification set the standard for accessible treatment, while deuruxolitinib’s July 2024 approval confirmed JAK inhibitors as a valid clinical class for alopecia areata.

The European Medicines Agency applies stricter cosmetic ingredient standards than US equivalents. Novel topical actives require more extensive safety dossiers before market authorization across EU member states — raising entry costs for biotech-derived topicals and slowing pan-European launches for brands that clear FDA review first.

Exosome-based hair treatments operate in a regulatory gray zone across the US and EU in 2025 — neither formally classified as drugs nor approved as cosmetics for hair applications by the FDA or EMA. Brands commercializing these products face escalating scrutiny with no clear reclassification timeline established by either authority.

Drivers

Rising Alopecia Prevalence and JAK Inhibitor Approvals Drive Demand

Androgenetic alopecia affects hundreds of millions globally, creating a durable patient pool that sustains demand across OTC, prescription, and clinical treatment tiers regardless of economic cycles. AI-powered dermatology platforms tracking over 1 million users per Dermatology Times 2025 data confirm the scale of unmet need — expanding the addressable market faster than supply-side innovation serves it.

The FDA’s approval of deuruxolitinib (Leqselvi) in July 2024 — from Incyte Corporation — validated JAK inhibitors as a commercial prescription category for the alopecia areata treatment market. This approval signals to investors and brands that regulatory pathways for novel mechanisms are open, pulling forward pipeline investment.

Social media platforms including TikTok and Instagram destigmatize hair loss and accelerate consumer diagnosis — users self-identify conditions, research treatments, and arrive at dermatologists and DTC platforms already product-aware. This compressed awareness-to-purchase cycle shortens the sales funnel for brands with strong digital presence.

Restraints

Regulatory Gray Zone and No FDA Approval Limit Exosome Uptake

Exosome-based hair products lack FDA approval for cosmetic or therapeutic hair applications in the US in 2025, per NBC News February 2026 reporting. Brands operate in a regulatory gray zone where marketing claims face scrutiny without a clear enforcement timeline — limiting premium pricing power in mainstream channels.

No FDA reclassification actions targeted exosome-based topicals in the 18 months prior to 2025, per MIT Technology Review October 2024 analysis — but ongoing scrutiny persists. This uncertainty prevents large consumer health brands from entering the exosome segment at scale, ceding the space to smaller clinical operators who accept higher regulatory risk.

No FDA Breakthrough Therapy designations covered hair regeneration candidates in the period reviewed, per ClinicalTrials.gov 2025 data. Brands and investors planning around a 2027 or earlier launch window face higher timeline risk without this designation pathway accelerating any active program.

Growth Factors

Stem Cell Reactivation Funding Unlocks Next Therapy Wave

Our forecast suggests regenerative medicine investment will define the next commercial cycle in hair loss treatment. According to Pelage Pharmaceuticals’ Series B announcement, USD 120 million Series B closed in October 2025 — co-led by ARCH Venture Partners and GV — to advance PP405 toward Phase 3 trials in 2026.

According to Pelage Pharmaceuticals’ Phase 2a announcement, PP405 Phase 2a results from June 2025 showed 31% of men with higher-degree hair loss achieving more than 20% increase in hair density at week 8 versus 0% in the placebo group. This is the strongest clinical signal in follicle stem cell reactivation published to date.

Non-hormonal oral formulations represent a second growth vector. Veradermics completed Phase 3 enrollment for VDPHL01, an extended-release oral minoxidil positioned as the first non-hormonal oral treatment for pattern hair loss in both men and women. A successful NDA filing would open a prescription category that has seen no new approved entrants in nearly 30 years.

Emerging Trends

DTC Platforms and Exosome Therapies Reshape Hair Loss Care

Exosome therapy reached more than 500 US dermatology clinics in 2025, per Bioinformant’s October 2025 exosome cosmeceuticals data, driven by premium clinic adoption for follicle stimulation ahead of any FDA approval. Direct-to-consumer hair loss brands and clinic-based exosome operators both signal that patient willingness to pay can precede formal regulatory authorization at scale.

Stem cell-derived exosome therapy shows hair density increases of 14 to 29% within months in clinical applications, outperforming traditional minoxidil benchmarks in Seoul-based studies per USA Today November 2025 reporting. This performance differential is the primary commercial argument for premium pricing — and the reason dermatologists absorb regulatory risk to offer the treatment.

Phase 3 trials for the most promising pipeline candidates — including follicle stem cell activators and extended-release oral formulations — carry estimated availability timelines of 2028 to 2029, per ClinicalTrials.gov 2025 data. Brands and investors planning commercial launches before this window must build on currently approved mechanisms or accept pre-approval clinical positioning.

Hair Loss Treatment Market Key Companies Insights

Consumer Health Majors Lead by Scale and OTC Channel Reach

The leading companies in hair loss treatment market span consumer health majors, pharmaceutical players, and DTC platforms — each competing for a different buyer type across the treatment spectrum. L’Oréal S.A. leads the consumer health tier through its Kérastase and Vichy Dercos portfolios, both positioned at the clinical-OTC boundary where premium pricing meets dermatologist recommendation.

Pharma Players Drive Prescription Segment With Named Drugs

In our view, the pharma tier holds the most durable competitive position in hair loss treatment because branded drugs like finasteride and the newly approved deuruxolitinib carry patent protection and prescriber loyalty that OTC brands cannot replicate. Pfizer Inc. and Merck & Co. anchor Merck hair loss treatment and Pfizer’s prescription channel through established molecules with decades of clinical validation.

DTC Brands Grow >30% With Telehealth Access Models

According to Hims & Hers Health investor relations data, 2.2 million subscribers, up 45% in 2024 — confirming that telehealth-to-treatment platforms restructure how consumers access hair loss prescriptions. Hims & Hers Health Inc. grew Hims brand revenue over 30% year-over-year in 2025.

According to PMC’s 2025 clinical review, 11 clinical studies show 9.5 to 35 hairs per cm² improvement in hair density. This data gives emerging biotech players like Pelage Pharmaceuticals and Stemson Therapeutics the clinical differentiation needed to separate regenerative approaches from legacy OTC brands.

Key Companies

- L’Oréal S.A.

- Unilever PLC

- Pfizer Inc.

- Johnson & Johnson Services Inc.

- Bayer AG

- The Estée Lauder Companies Inc.

- Shiseido Company Limited

- Kao Corporation

- Galderma S.A.

- Dr. Reddy’s Laboratories Ltd.

- Taisho Pharmaceutical Holdings Co. Ltd.

- Revlon Inc.

- Merz Pharma GmbH & Co. KGaA

- Hims & Hers Health Inc.

- Pierre Fabre S.A.

- Roman Health Ventures Inc.

- Aclaris Therapeutics Inc.

- Thirty Madison Inc.

- TYPEBEA Inc.

- Procter & Gamble Company

Recent Development

- February 2026 — Veradermics completed enrollment in its second pivotal Phase 3 trial (304) of VDPHL01 for male pattern hair loss, with topline data anticipated in H2 2026 — a timeline that could deliver the first new oral non-hormonal FDA NDA filing in decades.

- February 2026 — Veradermics (NYSE: MANE) raised approximately USD 256 million in its US IPO, pricing at the higher end of range — positioning the company to fund commercialization and FDA approval efforts for VDPHL01.

- February 2026 — Hims & Hers Health disclosed international expansion and a precision medicine pivot in 2025 earnings materials, with no specific biotech licensing for hair confirmed — signaling DTC scale ambitions beyond the US market.

- Early 2026 — Cosmo Pharmaceuticals advanced toward FDA and EMA submissions for clascoterone 5% topical solution following Phase 3 results showing 53.9% improvement in target area hair count versus placebo in male pattern hair loss.

- January 2026 — JW Pharmaceutical received a US patent for its JW0061 Wnt activator valid until 2039, protecting a novel hair regeneration mechanism through the next decade of the forecast window.

- December 2025 — Veradermics closed a USD 150 million oversubscribed Series C led by SR One, with Viking Global Investors and Marshall Wace participating — fueling Phase 3 completion and pre-commercialization build-out for VDPHL01.

- Late 2025 — Absci initiated Phase 1/2a trials for ABS-201, an anti-PRLR antibody targeting a novel biological pathway in hair loss — expanding the pipeline beyond hormonal and follicle-based mechanisms into biologic territory.

- October 2025 — Pelage Pharmaceuticals confirmed Phase 3 initiation of PP405 planned for 2026, following positive Phase 2a results and a USD 120 million Series B closing — the most advanced follicle stem cell reactivation program in the global pipeline.

- 2025 — Shiseido Company Limited forecast an operating loss while continuing hair care innovation under its SHIFT 2025 strategy — no clinical-grade hair loss launches confirmed for Japan or South Korea, signaling a consolidation phase rather than an expansion one.

Related Hair Care Markets

Hair loss treatment sits within a broader hair care ecosystem where consumer behavior, retail channels, and brand positioning overlap significantly. Brands and investors operating in hair loss treatment access adjacent demand from scalp care, nutraceuticals, and clinical dermatology — making cross-market positioning a viable growth lever rather than a distraction from core category focus.

The hair care product market reached USD 118.93 billion in 2025 and will grow to USD 261.56 billion by 2035 at a CAGR of 8.2% — positioning hair loss treatment as a fast-growing clinical sub-segment within a structurally expanding category.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 8.61 Billion |

| Forecast Revenue (2035) | USD 20.20 Billion |

| CAGR (2026–2035) | 8.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Shampoos & Conditioners, Serums & Oils, Supplements & Vitamins, Oral Treatments, Injection Therapies, Laser Treatments, Surgical Treatments, Topical Treatments), By Distribution Channel (Health & Beauty Stores, Online Retail / E-Commerce, Supermarkets & Hypermarkets, Pharmacies & Drug Stores, Convenience Stores, Specialty Retailers), By Gender (Female, Male, Children), By Route of Administration (Topical, Oral), By Disease Type (Androgenetic Alopecia, Alopecia Areata, Telogen Effluvium, Cicatricial Alopecia, Traction Alopecia) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | L’Oréal S.A., Unilever PLC, Pfizer Inc., Johnson & Johnson Services Inc., Bayer AG, The Estée Lauder Companies Inc., Shiseido Company Limited, Kao Corporation, Galderma S.A., Dr. Reddy’s Laboratories Ltd., Taisho Pharmaceutical Holdings Co. Ltd., Revlon Inc., Merz Pharma GmbH & Co. KGaA, Hims & Hers Health Inc., Pierre Fabre S.A., Roman Health Ventures Inc., Aclaris Therapeutics Inc., Thirty Madison Inc., TYPEBEA Inc., Procter & Gamble Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |