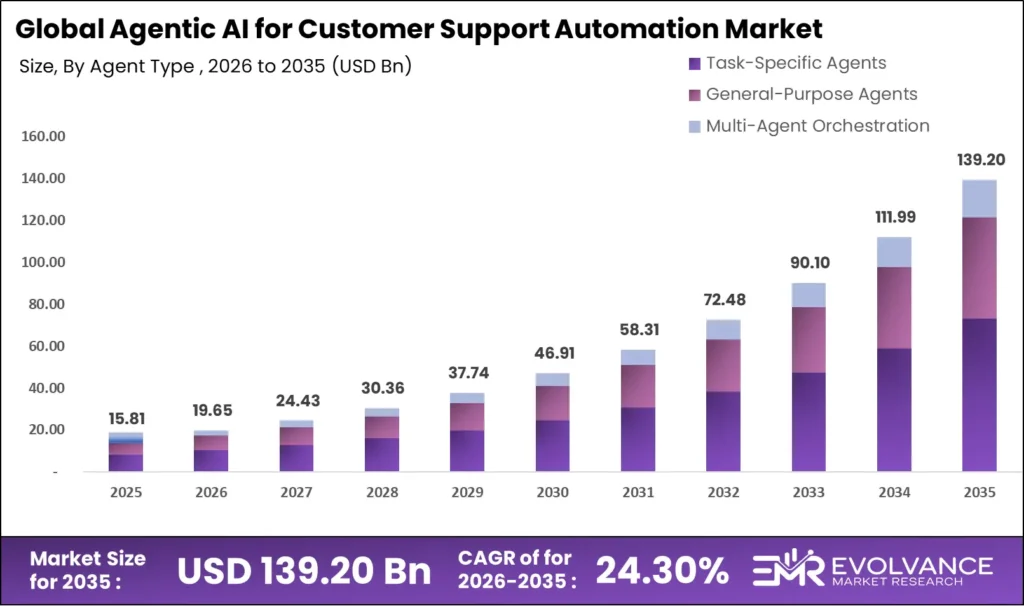

Agentic AI for Customer Support Automation Market: USD 15.81B to USD 139.20B by 2035

The Global Agentic AI for Customer Support Automation Market will reach USD 15.81 billion in 2025 and expand to USD 139.20 billion by 2035, growing at a CAGR of 24.30%. Rapid enterprise migration from rule-based chatbots to goal-directed autonomous agents, declining large language model inference costs, and rising pressure to reduce cost-per-interaction while maintaining service quality are key growth drivers. Organizations that previously deployed basic chatbot automation are now transitioning to agentic systems capable of multi-step reasoning, real-time CRM integration, and autonomous resolution of complex queries.

However, enterprises face dual challenges: integrating with legacy CRM and ticketing systems, and managing workforce resistance due to automation-led role changes. By 2027, a significant share of customer interactions is expected to involve AI agents, driving vendor demand. Successful adoption requires investment in governance frameworks, memory architecture, and supervised escalation models to maximize long-term value and operational efficiency.

The Agentic AI for Customer Support Automation Market is witnessing strong growth driven by the adoption of autonomous decision-making systems and intelligent automation across enterprises. Businesses are increasingly deploying these solutions to enhance real-time engagement and operational efficiency. The evolution of such AI-driven ecosystems is closely associated with advancements in the AI Podcast Creation Platforms and Adaptive Learning Software, where similar generative AI and personalization capabilities are being utilized. Additionally, integration with the Content Creator Economy and broader Creator Economy is enabling scalable conversational experiences and automated content-driven customer interactions.

Agentic AI for Customer Support Automation Market Highlights: Key Data at a Glance

- Market value: USD 2.47 billion in 2025, forecast to USD 139.20 billion by 2035 at 24.30% CAGR

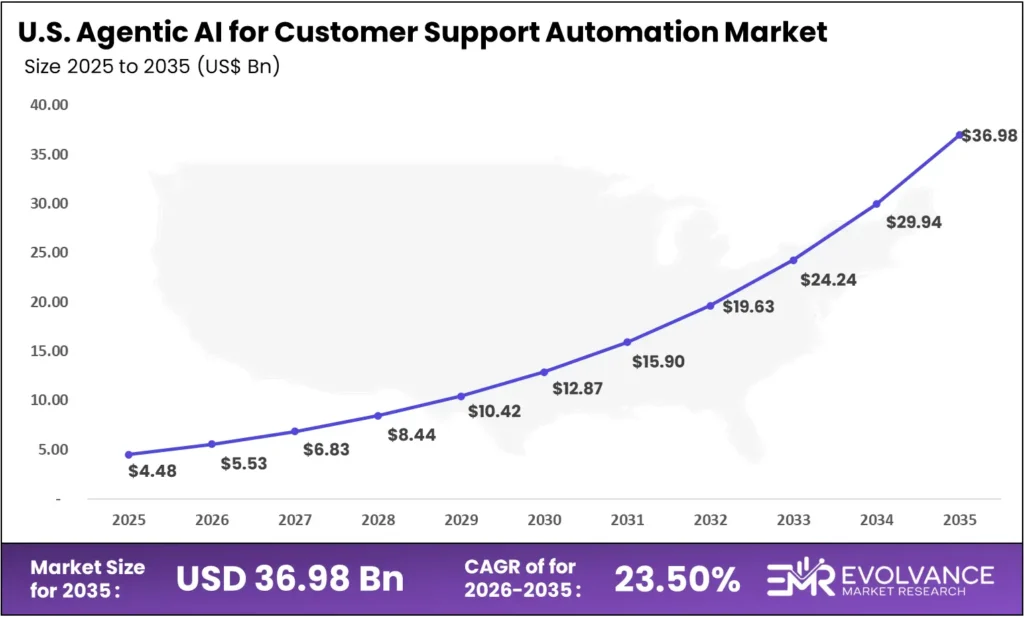

- US market: USD 4.48 billion in 2025, forecast to USD 27.04 billion by 2035 at 23.50% CAGR

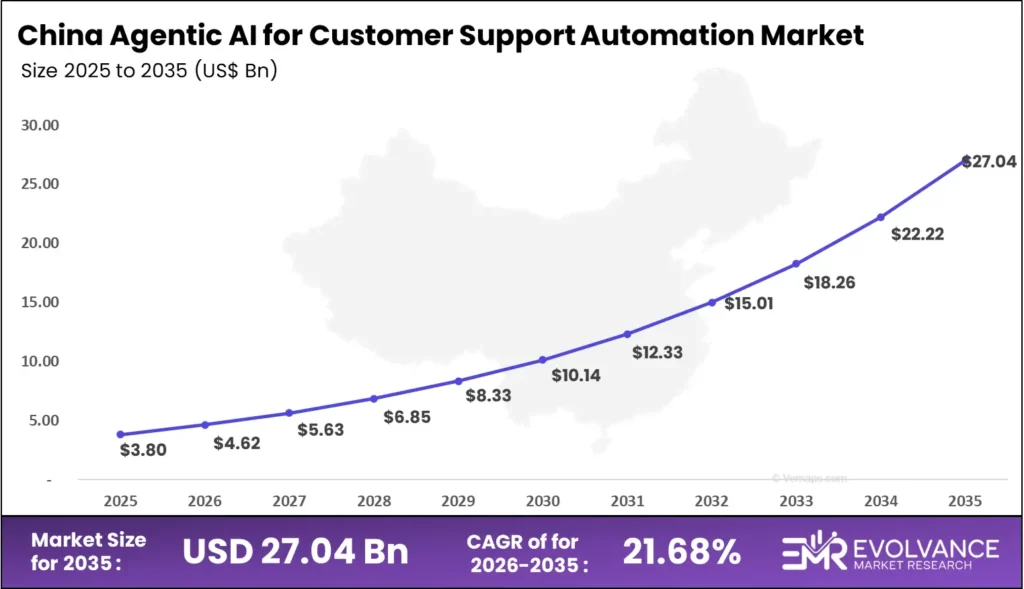

- China market: USD 3.80 billion in 2025, forecast to USD 3.18 billion by 2035 at 21.68% CAGR

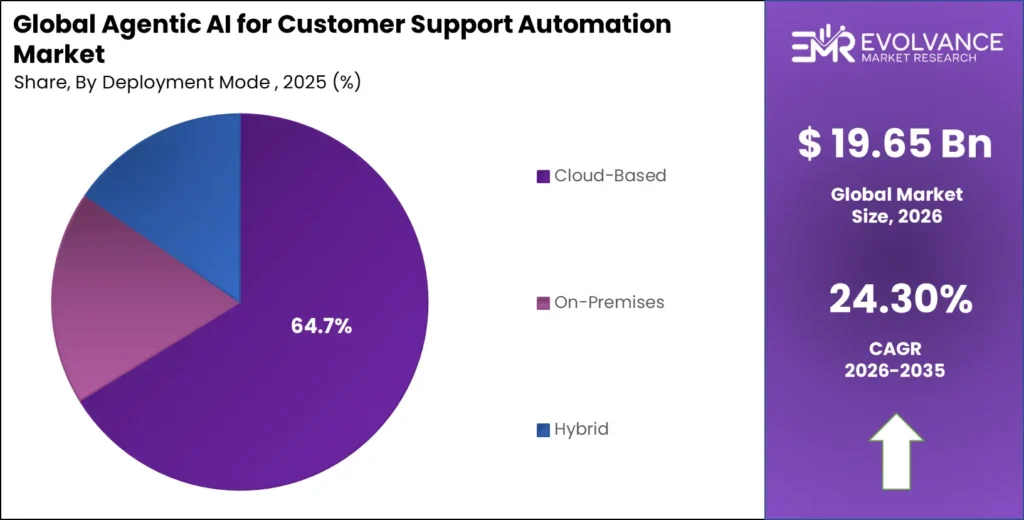

- Dominant deployment mode: Cloud-Based with 64.7% revenue share, driven by SaaS pricing models and elastic LLM inference capacity from hyperscaler platforms

- Dominant enterprise size: Large Enterprises with 71.4% revenue share, anchored by complex multi-channel customer experience orchestration requirements

- Dominant industry vertical: BFSI with 28.3% revenue share, fuelled by high-volume query resolution and regulatory compliance automation demand

- Dominant functionality: Conversational AI & Live Assistance with 33.1% revenue share, leading all functionality investment categories

- Dominant channel: Web Chat with 34.6% revenue share, the primary digital-first interface for enterprise agentic AI deployment

- Dominant agent type: Task-Specific Agents with 58.9% revenue share, reflecting enterprise preference for bounded, auditable automation architectures

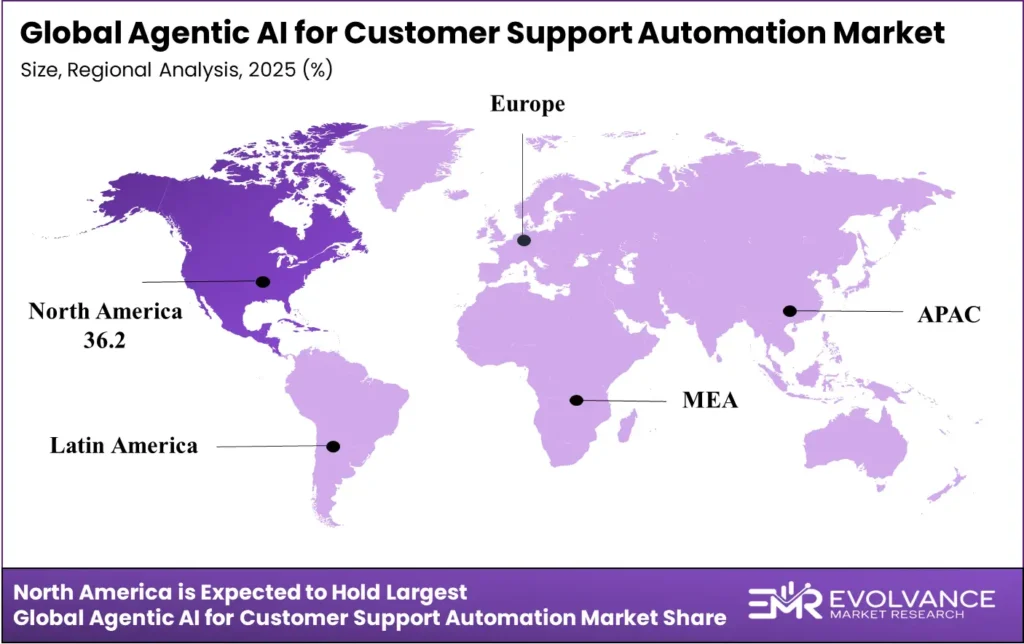

- North America: Largest regional share at 36.2%, valued at USD 0.89 billion in 2025

- Asia-Pacific: Fastest-growing region globally at 34.1% CAGR

US Agentic AI Customer Support Automation Market: USD 0.83B to USD 9.60B by 2035

The US agentic AI for customer support automation market will reach USD 36.98 billion by 2035 from USD 4.48 billion in 2025, growing at a CAGR of 23.50%. Growth is slightly below the global average due to mature enterprise adoption and slower mid-market expansion. Leading enterprises have already committed to integrating agentic AI into customer experience operations, driving structured vendor procurement.

Regulatory oversight is reshaping deployment strategies, with evolving transparency and compliance requirements increasing implementation complexity. Enterprises must build auditable decision systems and human escalation pathways to meet standards. This compliance burden favors established platform providers over smaller vendors, while also driving market consolidation and strengthening long-term investment potential in enterprise-grade solutions.

China Agentic AI Customer Support Automation Market: USD 0.31B to USD 3.18B by 2035

The China agentic AI for customer support automation market will reach USD 27.04 billion by 2035 from USD 3.80 billion in 2025, growing at a CAGR of 21.68%. Growth is driven by state-led AI industrialisation priorities, with national policies promoting customer-facing AI adoption across enterprises and state-owned organizations. This creates strong demand for locally compliant agentic AI platforms.

Domestic technology leaders are developing proprietary solutions, resulting in a bifurcated market where local providers dominate. Strict data localisation and cybersecurity regulations increase entry barriers for foreign vendors, requiring localized infrastructure deployment. As a result, enterprises entering China must align with regulatory frameworks and account for domestic vendor preference when designing long-term investment and market entry strategies.

Market Overview: Why Agentic AI Customer Support Investment Is Structurally Accelerating

The agentic AI for customer support automation market covers software platforms, orchestration frameworks, LLM-powered conversational engines, and professional services that deploy autonomous AI agents capable of planning, executing, and adapting multi-step customer resolution workflows without continuous human oversight. It excludes rule-based chatbots, static FAQ tools, and human-assisted chat systems lacking autonomous reasoning.

This analysis is based on enterprise CX procurement data, vendor financial disclosures, and AI adoption surveys. Segment shares are validated against revenues from major technology providers, combining financial reporting with procurement insights to ensure accuracy. Growth projections align with LLM cost reductions and enterprise deployment benchmarks derived from real-world implementations.

Enterprise demand is shifting from basic query handling to full-cycle autonomous resolution, including account management, order exceptions, and service coordination. Agentic platforms are increasingly replacing traditional workforce tools and BPO services, driving higher contract values even in SME segments as deployments scale across channels.

Buyer behavior varies across three segments. Large enterprises prioritize integrated, multi-year contracts with deep CRM alignment. Mid-market firms favor cloud-based, consumption pricing models for faster deployment. Meanwhile, system integrators and BPO providers adopt agentic AI to enhance service delivery efficiency and profitability.

Deployment Mode Analysis

Cloud-Based Dominates with 64.7% Due to LLM Inference Economics and Rapid Iteration Velocity

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Cloud-Based | 64.7% | Elastic LLM inference capacity and SaaS consumption pricing economics |

| On-Premises | 21.4% | Data sovereignty, regulated-industry compliance, and PII data protection requirements |

| Hybrid | 13.9% | Phased migration architecture for large enterprises with legacy CRM technology estates |

In 2025, Cloud-Based deployment held a dominant position in the By Deployment Mode segment with a 64.7% share. Cloud platforms enable enterprises to access frontier LLM inference capacity — GPT-4o, Claude 3.5, Gemini 1.5 Pro — without sustaining dedicated GPU infrastructure costs. AWS Bedrock, Microsoft Azure OpenAI Service, and Google Cloud Vertex AI all offer enterprise-grade agentic environments with SOC 2 Type II, HIPAA, and PCI-DSS compliance certifications, removing security evaluation barriers that previously delayed cloud adoption in regulated CX programmes.

On-Premises deployment retains structural relevance for financial services, government, and healthcare enterprises where data residency regulations prohibit customer interaction data from leaving controlled infrastructure perimeters. These deployments command substantial price premiums — averaging 2.7x the annual contract value of equivalent cloud deployments due to model hosting, fine-tuning compute, and dedicated support requirements. For vendors, on-premises capability is a market-access credential for regulated sectors that cannot adopt cloud alternatives regardless of cost-efficiency arguments.

Industry Vertical Analysis

BFSI Dominates with 28.3% Due to High-Volume Query Resolution and Compliance Automation

| Industry Vertical | Share % | Primary Driver |

|---|---|---|

| BFSI | 28.3% | Account query resolution, fraud alert management, and compliance workflow automation |

| Retail & E-Commerce | 22.7% | Order tracking, return processing, and proactive exception notification agents |

| Healthcare | 14.9% | Appointment scheduling, insurance pre-authorisation, and patient access automation |

| Telecom & IT | 13.8% | Technical support deflection and network troubleshooting automation workflows |

| Travel & Hospitality | 10.4% | Booking modification, refund processing, and loyalty programme query resolution |

| Others | 9.9% | Education, utilities, and government digital services adoption growth |

In 2025, BFSI held a dominant market position in the By Industry Vertical segment with a 28.3% share. Financial institutions processing millions of monthly account inquiries, fraud alert notifications, and loan status queries represent the highest-volume customer interaction environment across all industry sectors, making the per-interaction cost reduction case for agentic AI deployment uniquely compelling at board level. Major banks that have deployed agentic AI for first-contact resolution report 40–60% containment rates for structured tier-one queries, delivering payback periods of 12–18 months in large contact centre environments.

Retail & E-Commerce is the fastest-growing vertical sub-segment. Digital commerce has permanently elevated consumer expectations for real-time order visibility, instant refunds, and proactive shipping notifications. Brands deploying agentic AI consistently avoid seasonal workforce expansion costs, creating recurring ROI that compounds as interaction volumes grow.

Healthcare represents the highest near-term contract value growth opportunity within the vertical taxonomy. Patient access centres managing appointment scheduling, insurance pre-authorisation, and post-discharge follow-up workflows face chronic staffing shortages and CMS reimbursement pressure that agentic AI directly addresses. Regulatory clarity from HHS AI in healthcare guidance and CMS endorsement of AI-assisted prior authorisation is accelerating procurement cycles previously extended 18–24 months by compliance uncertainty.

Functionality Analysis

Conversational AI & Live Assistance Dominates with 33.1% Due to Direct CX Measurability

| Functionality Segment | Share % | Primary Driver |

|---|---|---|

| Conversational AI & Live Assistance | 33.1% | Real-time autonomous inbound query resolution with measurable CSAT impact |

| Ticket Routing & Triage | 22.4% | AI-driven priority classification and specialist queue assignment optimisation |

| Self-Service Automation | 18.7% | Zero-touch resolution for structured account, billing, and policy queries |

| Sentiment Analysis & Intent Detection | 14.2% | Real-time escalation triggers and CX quality scoring at 100% coverage |

| Post-Interaction Analytics | 11.6% | Agent coaching intelligence and continuous process optimisation insights |

In 2025, Conversational AI & Live Assistance led functionality segments with a 33.1% share. This segment maps directly to the highest-visibility CX metric in enterprise procurement — first-contact resolution rate — creating a direct link between platform deployment and measurable customer satisfaction improvement that procurement decision-makers can present with confidence. Enterprises deploying agentic conversational AI consistently report 20–35% improvement in CSAT scores for agent-handled interactions versus legacy IVR flows, providing CX leaders with ROI narratives that board-level technology investment review committees can quantify and approve.

Ticket Routing & Triage is the second-largest functionality segment and the lowest-risk entry point for enterprises beginning agentic AI deployment. Routing automation requires no customer-facing AI interaction, eliminating hallucination risk while delivering measurable efficiency gains through accurate priority assignment, SLA compliance optimisation, and specialist queue routing. Enterprises use routing success metrics as proof-points that justify expanded conversational AI investment, making triage a structural pipeline driver for full-stack platform vendors.

Post-Interaction Analytics represents the emerging white-space functionality gaining rapid commercial traction. Agentic AI platforms that analyse 100% of interaction transcripts — versus the 2–5% sampling rates of traditional QA programmes — generate coaching intelligence that CX leadership can act on at near-real-time velocity. Vendors offering analytics as an upsell module within conversational deployments achieve net revenue retention exceeding 125%, making it the highest-margin incremental tier within the platform stack.

Agent Type Analysis

Task-Specific Agents Dominate with 58.9% Due to Deployment Predictability and Audit Compliance

| Agent Type | Share % | Primary Driver |

|---|---|---|

| Task-Specific Agents | 58.9% | Deterministic automation with bounded failure modes and auditable decision trails |

| General-Purpose Agents | 26.3% | Open-domain query resolution for complex multi-intent customer interactions |

| Multi-Agent Orchestration | 14.8% | Enterprise-scale complex case resolution requiring collaborative agent networks |

In 2025, Task-Specific Agents held a dominant position in the By Agent Type segment with a 58.9% share. Enterprises prioritise task-specific architectures because bounded scope reduces hallucination risk, simplifies audit trail requirements, and enables incremental deployment without full CRM redesign. Order management agents, billing dispute agents, and password reset agents operate within defined tool-call boundaries — a pattern that CX leadership can monitor and refine without exposing customers to open-domain reasoning failures.

Multi-Agent Orchestration represents the highest-growth agent type segment despite its current 14.8% share. Complex cases — insurance claims requiring document verification, cross-border transactions requiring fraud and compliance checks, or healthcare referral pathways requiring eligibility verification and scheduling — exceed single-agent resolution capacity. Vendors building orchestration frameworks managing reliable agent handoffs, shared memory, and conflict resolution logic are positioning for the premium contract tier as enterprise maturity deepens through 2027.

Key Market Segments

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By Enterprise Size

- Large Enterprises

- SMEs

By Industry Vertical

- BFSI

- Retail & E-Commerce

- Healthcare

- Telecom & IT

- Travel & Hospitality

- Others

By Functionality

- Ticket Routing & Triage

- Conversational AI & Live Assistance

- Sentiment Analysis & Intent Detection

- Self-Service Automation

- Post-Interaction Analytics

By Channel

- Web Chat

- Voice / IVR

- Social Media & Messaging

- Mobile App

By Agent Type

- Task-Specific Agents

- General-Purpose Agents

- Multi-Agent Orchestration

Regional Analysis of Agentic AI Customer Support Automation Market

North America Leads at 36.2% Share

| Region | Market Value (2025) | Share % | CAGR |

|---|---|---|---|

| North America (US) | USD 0.89 billion | 36.2% | 27.7% |

| Asia-Pacific | USD 0.56 billion | 22.7% | 34.1% (fastest) |

| Europe | USD 0.52 billion | 21.1% | 23.8% |

| China | USD 0.31 billion | Part of Asia-Pacific | 26.2% |

| Latin America | USD 0.27 billion | 10.9% | 22.6% |

| Middle East & Africa | USD 0.23 billion | 9.3% | 21.4% |

North America holds 36.2% of global agentic AI for customer support automation revenue at USD 0.89 billion in 2025 — the largest region by absolute value. Its structural advantage lies in early generative AI adoption combined with the deepest concentration of cloud-native CX platform vendors, creating the largest installed base of enterprises with active agentic AI procurement programmes. NIST’s AI Risk Management Framework is establishing implementation guardrails that accelerate qualified vendor procurement by reducing enterprise governance evaluation cycle durations.

North America Agentic AI Customer Support Market: LLM Platform Maturity Drives Procurement

The US agentic AI for customer support automation market, valued at USD 0.83 billion in 2025, will reach USD 9.60 billion by 2035 at a CAGR of 27.70%. Salesforce’s Einstein and Agentforce, Microsoft’s Copilot for Service, and ServiceNow’s Now Assist — all broadly deployed within US enterprise accounts — are creating structured expansion pipelines for agentic AI capabilities embedded within existing CRM investments. Enterprises that have already adopted these platforms are expanding from co-pilot assistance to fully autonomous agent deployment, generating organic net revenue retention above 130% for platform vendors with strong agentic product upgrade paths through annual subscription cycles.

Europe Agentic AI Customer Support Market Trends

Europe’s agentic AI for customer support automation market reached an estimated USD 0.52 billion in 2025, driven by German, French, and UK enterprise digital transformation programme timelines. The EU AI Act — which classifies high-risk AI applications in financial services, insurance, and healthcare customer interactions — is creating compliance architecture requirements that favour platform vendors with built-in transparency, audit logging, and human oversight enforcement controls. GDPR data residency requirements are sustaining demand for EU-hosted deployments, with AWS EU, Azure North Europe, and Google Cloud Belgium serving as compliant inference infrastructure for enterprise agentic deployments that cannot process customer PII outside EU jurisdiction boundaries.

Asia-Pacific Agentic AI Customer Support Market: Fastest-Growing Region Globally

Asia-Pacific’s 34.1% CAGR makes it the fastest-growing major region for agentic AI customer support automation. Three distinct country-level growth engines drive this trajectory. India’s digital services sector — with over 1.5 million BPO employees managing global enterprise CX operations — is under acute automation pressure from Western enterprise clients seeking cost structure reduction, creating platform demand that no other region matches in scale or urgency. Japan’s structural labour scarcity across all service industries is accelerating AI adoption rates beyond comparable Western markets, with consumer tolerance for AI-assisted service significantly higher than European survey benchmarks indicate. Southeast Asia’s mobile-first consumer base — where over 70% of customer interactions originate from messaging applications — creates a natural deployment environment for agentic AI agents integrated within WhatsApp Business, LINE, and WeChat enterprise channels.

India Agentic AI Customer Support Market Size and Growth

India represents the single highest-velocity growth opportunity within Asia-Pacific. The NASSCOM-estimated 1.54 million active BPO and contact centre agents managing global enterprise CX operations are under unprecedented automation pressure as enterprise clients re-evaluate labour arbitrage economics against agentic AI total cost of ownership. IT services majors including Infosys, Wipro, and HCL Technologies are investing in proprietary agentic AI platforms as strategic service delivery infrastructure — creating both a competitive threat to Western pure-play vendors and a channel partnership opportunity for LLM platform providers seeking scaled India deployment.

Middle East & Africa Agentic AI Customer Support Market Trends

The Middle East and Africa region is in early-stage adoption but structurally promising. Saudi Arabia’s Vision 2030 initiative includes a dedicated AI in public services programme, with Saudi Telecom Company and stc pay commissioning agentic AI customer service environments for national-scale operations. The UAE’s Smart Dubai initiative and ADNOC’s digital CX programme are creating eight-figure procurement commitments. Africa’s earliest adoption cycle is led by MTN Group and Safaricom’s M-Pesa customer service operations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Netherlands

- Sweden

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Companies: Three Players Define the Competitive Landscape

Three companies — Salesforce, Microsoft Corporation, and ServiceNow — dominate global agentic AI for customer support automation revenue through platform breadth, enterprise CRM integration depth, and CX buyer relationship density built across decades of enterprise software sales. This concentration creates significant entry barriers in Tier-1 enterprise accounts but leaves AI-native, vertical-specialist, and mid-market SaaS segments meaningfully open for challengers with differentiated model architecture, faster deployment timelines, and purpose-built industry compliance frameworks.

| Company | Revenue / Segment | Growth Rate | Year Reported |

|---|---|---|---|

| Salesforce (Group) | USD 37.9 billion | +9% organic | FY2025 |

| Salesforce Agentforce / Service Cloud | ~USD 9.6 billion Service Cloud | +12% organic | FY2025 |

| Microsoft Corporation (Group) | USD 245.1 billion | +16% | FY2024 |

| Microsoft Azure OpenAI / Copilot for Service | Part of USD 105B Intelligent Cloud | +29% Azure OpenAI YoY | FY2024 |

| ServiceNow (Group) | USD 10.98 billion | +23% | FY2024 |

| ServiceNow Now Assist AI Agents | Part of USD 4.3B Pro+ tier | +41% AI seat growth | FY2024 |

| Google Cloud (CCAI / Vertex AI) | USD 43.2 billion | +35% | FY2024 |

According to Salesforce’s FY2025 annual results, Service Cloud reached approximately USD 9.6 billion in annual revenue with strong organic growth driven by Agentforce adoption momentum across large enterprise accounts. Salesforce’s Agentforce platform — launched in September 2024 and positioned as the industry’s first purpose-built agentic AI layer for enterprise CX — enables businesses to deploy autonomous agents across service, sales, and marketing workflows from within existing Salesforce CRM environments. The company’s installed base across over 150,000 enterprise accounts globally creates a structural cross-sell advantage for agentic AI upgrade paths that pure-play entrants cannot replicate through organic sales motion or channel partnership programmes alone.

As reported by Microsoft’s investor relations, Azure OpenAI Service grew at 29% year-on-year in FY2024, with Copilot for Service adoption accelerating meaningfully across enterprise contact centre accounts in financial services, retail, and healthcare verticals. Microsoft’s integration of GPT-4o and custom fine-tuned models within Dynamics 365 Customer Service creates a compelling full-stack agentic deployment path for enterprises already operating on Microsoft infrastructure — eliminating the vendor evaluation complexity that pure-play agentic AI vendors must navigate when entering accounts with established Microsoft enterprise agreements.

We believe Google Cloud Contact Centre AI presents the most strategically significant competitive evolution from outside the traditional CRM platform community. CCAI’s deep integration with Vertex AI Agent Builder — enabling enterprises to construct multi-agent customer service workflows using grounded Gemini models with real-time enterprise data retrieval — positions Google as the infrastructure layer for agentic CX deployments that prioritise model flexibility and multimodal capability over CRM vendor lock-in. Google’s partnerships with Accenture, Deloitte, and Cognizant for CCAI enterprise deployment accelerate market penetration through systems integrator channels that reach mid-market enterprise accounts beyond direct Google Cloud salesforce coverage boundaries.

Top Key Players

- Salesforce (Agentforce / Einstein Copilot)

- Microsoft Corporation (Copilot for Service / Azure OpenAI)

- ServiceNow (Now Assist / AI Agents)

- Google Cloud (Contact Centre AI / Vertex AI Agent Builder)

- Amazon Web Services (Amazon Connect / Amazon Bedrock)

- IBM Corporation (Watson Assistant / watsonx Orchestrate)

- Zendesk (AI Agents)

- Intercom (Fin AI Agent)

- Cognigy (Cognigy.AI)

- LivePerson (Conversational Cloud)

- Sprinklr (Unified-CXM)

- Nuance Communications (Microsoft DAX / Dragon)

Related Markets: 5 Segments Shaping Agentic AI Customer Support Automation

Five adjacent markets intersect directly with the agentic AI for customer support automation market. Each carries distinct growth dynamics, regulatory exposure, and buyer profiles — but all share the same upstream technology stack including LLM inference infrastructure, vector database retrieval systems, and orchestration frameworks. Enterprises building intelligent operations portfolios need visibility across all five to manage platform concentration risk and identify white-space investment opportunities across the full customer experience technology ecosystem.

- Conversational AI Platform Market: The Conversational AI Platform Market is valued at USD 14.8 billion in 2025 and is forecast to reach USD 78.3 billion by 2035, growing at a CAGR of 18.2%. The conversational AI platform growth is driven by LLM capability improvements that enable open-domain dialogue quality previously achievable only through extensive human-authored scripting, dramatically reducing deployment engineering cost and expanding the viable use case scope for conversational automation across enterprise segments.

- Customer Experience Management (CXM) Software Market: The CXM Software Market is valued at USD 22.6 billion in 2025 and is forecast to reach USD 61.4 billion by 2035 at a CAGR of 10.5%. CXM market growth creates the platform integration layer for agentic AI deployment — enterprises upgrading CXM infrastructure simultaneously create procurement openings for embedded agentic capabilities, making CXM platform replacement cycles the primary agentic AI co-acquisition event in enterprise technology budgets.

- AI in BPO Services Market: The AI in BPO Services Market is valued at USD 3.1 billion in 2025 and is projected to reach USD 19.8 billion by 2035 at a CAGR of 20.4%. AI in BPO market growth is driven by global enterprises re-evaluating labour arbitrage economics as agentic AI total cost of ownership falls below offshore human agent cost thresholds for structured interaction categories at scale.

- Enterprise LLM / Generative AI Platform Market: The Enterprise LLM Platform Market is valued at USD 9.4 billion in 2025 and is forecast to reach USD 89.7 billion by 2035, growing at a CAGR of 25.3%. Enterprise LLM platform market growth underpins agentic AI customer support capabilities, as foundation model reasoning quality and tool-use reliability are the primary determinants of agent resolution quality, containment rate performance, and customer satisfaction outcomes.

- Robotic Process Automation (RPA) Market: The RPA Market is valued at USD 18.2 billion in 2025 and is projected to reach USD 43.8 billion by 2035 at a CAGR of 9.2%. RPA market growth intersects with agentic AI adoption as enterprises combine deterministic process automation with agentic reasoning to build hybrid workflows handling both structured back-office process execution and unstructured customer interaction content within unified orchestration environments.

Key Growth Drivers of Agentic AI Customer Support Market

LLM Capability Maturity and Inference Cost Deflation Drive Structural Enterprise Adoption

The rapid maturation of large language model reasoning capability is the single most powerful structural force in this market. The transition from GPT-3.5-class models limited to single-turn FAQ answering to GPT-4o and Claude 3.5-class models capable of multi-step tool-calling, long-context document reasoning, and reliable structured output generation has expanded the viable autonomous resolution scope from trivial queries to complex case types requiring specialist knowledge. Simultaneously, LLM inference costs have declined by an estimated 90–95% between 2023 and 2025 per million tokens processed — destroying the economic argument for maintaining high-volume human agent workflows for structured interaction categories where agentic AI can achieve comparable resolution quality at a fraction of the operating cost.

The customer experience cost imperative is amplifying structural demand at every enterprise tier. McKinsey estimates global enterprise contact centre costs exceed USD 350 billion annually, with labour representing 60–70% of total spend. Agentic AI achieving 40–60% first-contact containment delivers payback periods of 12–18 months in large environments — a financial case resilient to macroeconomic headwinds: enterprises under cost pressure accelerate agentic AI investment rather than defer it.

The standardisation of agentic AI orchestration frameworks — including LangGraph, AutoGen, and CrewAI — is the near-term procurement acceleration catalyst most underappreciated in current market forecasts. These frameworks reduce custom engineering for enterprise deployments from months to weeks, compressing proof-of-concept timelines and enabling CX buyers to evaluate multiple vendor architectures simultaneously. Vendors aligned to these open-source standards hold a structural procurement velocity advantage over proprietary-architecture competitors.

Restraints

LLM Hallucination Risk and Data Integration Complexity Compress Enterprise Deployment Velocity

LLM hallucination and off-policy response generation is the primary enterprise adoption barrier for agentic AI customer support deployments in regulated industries. Financial services and healthcare enterprises cannot accept customer-facing AI agents that generate inaccurate account balances, incorrect policy terms, or clinically inappropriate health information — even at low occurrence rates that would be considered statistically negligible in other automation contexts. Mitigation architectures including retrieval-augmented generation, constrained tool-use frameworks, and confidence-scoring escalation triggers add significant engineering complexity to production deployments, extending timelines that vendors scope at 8–12 weeks into 20–30 week production-readiness cycles when enterprise compliance review requirements are fully incorporated.

CRM and ticketing system data fragmentation adds a compounding constraint. Agentic AI requires clean, real-time access to customer account data, interaction history, and policy documentation to generate accurate resolutions. Organisations grown through acquisitions typically operate fragmented CRM estates that cannot deliver the data completeness agentic resolution requires without CRM unification programmes that must precede agentic AI deployment. This sequencing constraint is rarely surfaced adequately before contract signature.

Workforce transformation resistance presents a third structural restraint. Customer service management communities in large enterprises are built around human agent capacity planning, QA sampling, and coaching investment — all disrupted by agentic AI at scale. Operational leaders who have built careers around human workforce metrics resist deployments that redefine what CX operations excellence means. Vendors embedding change management and workforce transition planning within deployment methodologies systematically accelerate adoption timelines by reducing the organisational resistance that delays technical approvals.

Opportunities

Vertical-Specific Agent Platforms and BPO Transformation Unlock Premium Revenue Segments

Vertical-specific agentic AI platforms purpose-built for BFSI, healthcare, and government customer operations represent the highest near-term average contract value expansion opportunity in this market. Generic LLM-powered agents lacking industry-specific knowledge bases, regulatory compliance controls, and pre-built workflow integrations face sustained enterprise procurement resistance in regulated verticals where compliance risk outweighs automation efficiency gains in procurement committee risk frameworks. Financial services agentic AI platforms with pre-certified FFIEC audit trail architectures command 3–4x contract premiums over horizontal alternatives in US community bank and regional credit union procurement cycles where regulatory examination readiness is a non-negotiable deployment prerequisite.

BPO market transformation is unlocking the largest addressable market expansion opportunity in agentic AI customer support automation. In March 2026, Concentrix announced a three-year commitment to deploy Salesforce Agentforce across 80,000 agent seats globally — signalling that Tier-1 BPO service providers are actively embedding agentic AI into service delivery infrastructure rather than deferring automation investment to protect labour model margins. In January 2026, Teleperformance expanded its Google Cloud CCAI partnership to deploy multi-agent workflows across 25 client programmes targeting financial services and healthcare verticals across Latin America and Europe. These investment signals define where agentic AI platform vendors can access large-scale enterprise deployment through BPO channel relationships, reducing direct enterprise customer acquisition cost while accelerating revenue scale.

Multilingual and voice-first agentic AI capabilities offer structural market share advantages for vendors targeting Asia-Pacific and Latin America. The shift from text chat to voice-native agentic interaction — driven by mobile-first consumer preference — creates demand for platforms combining speech recognition, LLM reasoning, and natural speech synthesis within sub-500ms latency. Vendors achieving voice-first deployment quality at scale in non-English languages will capture disproportionate regional market share through 2030.

Latest Trends in Agentic AI Customer Support Automation Market

Multi-Agent Orchestration and Memory-Augmented Architectures Reshape Platform Economics

Multi-agent orchestration architectures — where specialised agents for intent classification, policy lookup, transaction execution, and human escalation management operate collaboratively under a supervisor agent — are redefining the complexity ceiling for autonomous customer support resolution. Salesforce’s Agentforce 2.0, launched in January 2026, introduced a native multi-agent workflow builder enabling enterprises to deploy agent networks handling end-to-end complex case resolution without human touchpoints. Early enterprise deployments are reporting full case closure rates above 75% for structured financial service interactions within 60 days of deployment — a performance benchmark that fundamentally changes the economic model for human agent workforce planning at enterprise scale.

Long-term memory architectures are transforming how agentic AI platforms deliver personalised customer interactions across sessions separated by days or weeks. Persistent agent memory — storing customer preferences, prior resolution context, product usage patterns, and inferred intent signals across full interaction history — enables agents to provide service continuity that legacy IVR and stateless chatbot platforms structurally cannot deliver. Memory-augmented agents consistently achieve significantly higher CSAT scores on return-customer interactions than stateless agents responding to each query in contextual isolation, creating a measurable differentiation driver in enterprise platform evaluation processes.

Real-time enterprise knowledge graph integration is emerging as the critical infrastructure layer separating production-grade agentic deployments from proof-of-concept quality demonstrations. Agentic AI platforms querying live product catalogues, current pricing databases, and real-time inventory availability within sub-100ms tool-call latency deliver resolution accuracy that static RAG pipelines with periodic index refresh cycles cannot match. Vendors building proprietary enterprise knowledge connector libraries for Salesforce, SAP, Oracle, and ServiceNow are establishing durable competitive differentiation as enterprises discover that autonomous resolution quality is determined primarily by real-time data access architecture rather than by foundation model selection alone.

Recent Developments: Salesforce, Microsoft, and Google Lead 2025–2026

- March 2026 — Concentrix announced a three-year partnership with Salesforce to deploy Agentforce across 80,000 agent seats globally, targeting BFSI and healthcare verticals with multi-agent case resolution workflows integrated with Salesforce Data Cloud for real-time enterprise knowledge access.

- February 2026 — ServiceNow launched Now Assist for Customer Service 3.0 at Knowledge 2026, introducing proactive agentic AI capabilities that anticipate customer needs based on real-time event triggers from connected enterprise ERP and CRM systems before inbound customer contact is initiated.

- January 2026 — Salesforce released Agentforce 2.0 with native multi-agent workflow orchestration, enabling enterprises to deploy collaborating agent networks for complex case resolution workflows. Early adopters reported 75%+ automated case closure rates on structured BFSI interactions within 60 days of production deployment.

- January 2026 — Teleperformance expanded its Google Cloud CCAI partnership to deploy multi-agent workflows across 25 client programmes, targeting financial services and healthcare agentic AI deployment at scale across Latin American and European market operations.

- December 2025 — Microsoft released Copilot for Service with autonomous agent action capabilities, extending Dynamics 365 Customer Service to support fully autonomous case closure for structured query types without human review, with integrated Microsoft 365 compliance audit trail logging.

- November 2025 — Intercom launched Fin AI Agent 3.0 with multi-step reasoning and live enterprise system integration, achieving a 78% autonomous resolution rate across 500+ deployed enterprise accounts — the highest publicly disclosed containment rate for a production-scale horizontal agentic AI customer service platform.

- September 2025 — IBM expanded its watsonx Assistant enterprise programme with a financial services-specific agentic AI accelerator validated against FFIEC examination standards, targeting US regional bank and credit union accounts facing acute contact centre operating cost pressure in a higher-for-longer interest rate environment.

Report Features

| Feature | Description |

|---|---|

| Market Value (2025) | USD 15.81 billion |

| Forecast Revenue (2035) | USD 139.20 billion |

| CAGR (2026–2035) | 24.30% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Deployment Mode (Cloud-Based, On-Premises, Hybrid), By Enterprise Size (Large Enterprises, SMEs), By Industry Vertical (BFSI, Retail & E-Commerce, Healthcare, Telecom & IT, Travel & Hospitality, Others), By Functionality (Ticket Routing & Triage, Conversational AI & Live Assistance, Sentiment Analysis, Self-Service Automation, Post-Interaction Analytics), By Channel (Web Chat, Voice/IVR, Email, Social Media & Messaging, Mobile App), By Agent Type (Task-Specific Agents, General-Purpose Agents, Multi-Agent Orchestration) |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Dominant Segment | Cloud-Based 64.7%; BFSI 28.3%; Conversational AI & Live Assistance 33.1%; Task-Specific Agents 58.9% |

| Dominant Region | North America 36.2%; Asia-Pacific fastest-growing at 34.1% CAGR |

| Regulatory Framework | EU AI Act, GDPR, US NIST AI RMF, FTC AI Disclosure Rules, CFPB AI in Financial Services Guidance, HHS AI Healthcare Framework, FFIEC Examination Standards, China PIPL |

| Competitive Landscape | Salesforce, Microsoft, ServiceNow, Google Cloud, AWS, IBM, Zendesk, Intercom, Cognigy, LivePerson, Sprinklr, Nuance |

Sources

- Salesforce — FY2025 Annual Reports (Agentforce & Service Cloud)

https://investor.salesforce.com/financials/annual-reports/default.aspx - Microsoft — FY2024 Annual Report (Azure OpenAI & Copilot for Service Growth)

https://www.microsoft.com/en-us/investor/annual-reports - ServiceNow — FY2024 Annual Reports (Now Assist AI & Pro+ Tier)

https://ir.servicenow.com/financial-information/annual-reports - Google — FY2024 Annual Reports (Google Cloud / Vertex AI)

https://abc.xyz/investor/ - NASSCOM — BPO & Contact Centre Transformation Reports

https://www.nasscom.in/knowledge-center/publications - EU AI Act — Official Policy & Timeline

https://digital-strategy.ec.europa.eu/en/policies/regulatory-framework-ai - NIST — AI Risk Management Framework 1.0 (PDF)

https://www.nist.gov/system/files/documents/2023/01/26/AI%20RMF%201.0.pdf - U.S. Department of Health and Human Services — AI in Healthcare (2024)

https://www.hhs.gov/ai/index.html - Salesforce — Agentforce 2.0 Launch (Jan 2026)

https://www.salesforce.com/news/press-releases/2026/01/agentforce-2-announcement - Intercom — Fin AI Agent Benchmarks (2025)

https://www.intercom.com/blog/fin-ai-agent-resolution-rates - IBM — watsonx AI Financial Services Launch (2025)

https://newsroom.ibm.com/ - Concentrix — Investor News & Partnerships

https://ir.concentrix.com/news-releases - Teleperformance — Press Releases (CCAI Partnership)

https://www.teleperformance.com/en-us/newsroom/press-releases