What is the Organic Hair Care Market Size?

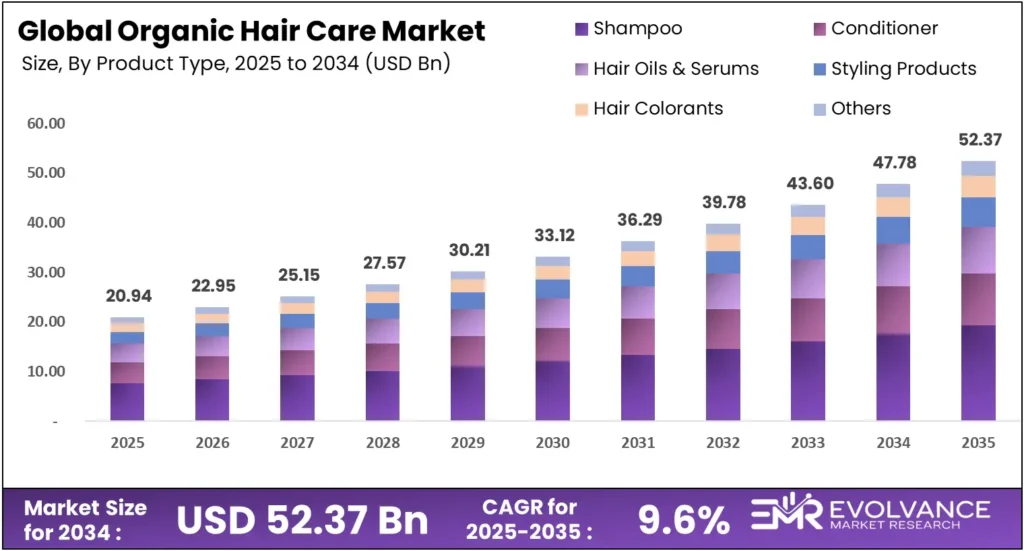

The global organic hair care market will reach USD 57.40 billion by 2035 from USD 20.94 billion in 2025, growing at a CAGR of 9.6% during the forecast period 2026 to 2035. Consumer rejection of synthetic sulfates, parabens, and silicones is pushing certified plant-based formulations into mainstream retail at speed. Scalp health positioning and biotech-infused organic formats are pulling category value upward across both mass and prestige channels.

Market Highlights

- The global organic hair care market reached USD 20.94 billion in 2025, forecast to hit USD 57.40 billion by 2035 at a CAGR of 9.6%.

- Shampoo leads the By Product Type segment with 36.80% revenue share, driven by sulfate-free reformulation momentum and daily-use certified organic demand.

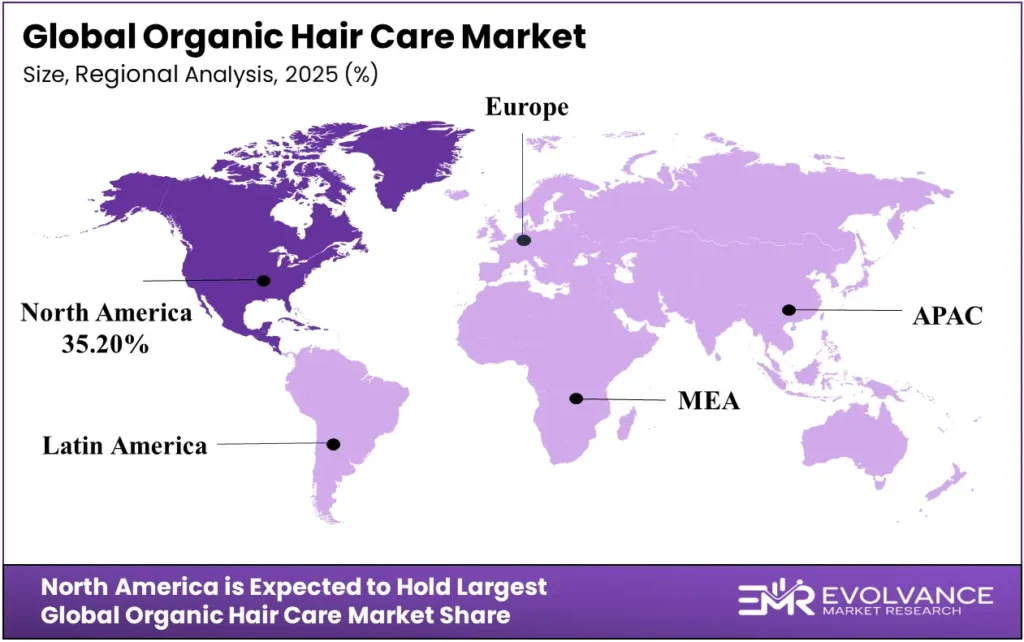

- North America dominates the global organic hair care market with 35.20% revenue share, valued at USD 7.31 billion in 2025.

- Women account for 71.4% of end-use revenue, reflecting stronger purchase intent and higher willingness to pay premium prices for certified plant-based formulations.

- Offline distribution retains 70.08% revenue share as pharmacies, specialty stores, and supermarkets remain the primary trial and repurchase channels for organic hair care brands.

- Anti-Dandruff leads the By Scalp Concern segment with 50% revenue share, capturing consumers switching from zinc pyrithione-based standard formulations to certified natural alternatives.

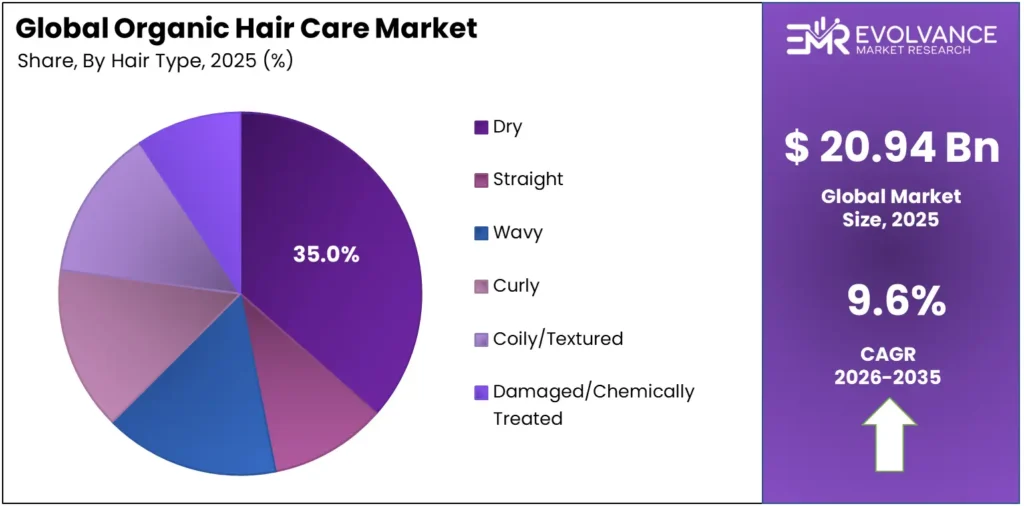

- Dry hair types account for 35% of organic hair care revenue, reflecting strong alignment between moisture-deficient hair needs and organic oil-rich botanical formulations.

Market Overview

The organic hair care market covers shampoos, conditioners, hair oils, serums, styling products, colorants, and emerging waterless formats made with certified plant-based or naturally derived ingredients. This organic hair care market analysis includes individual consumers, wellness-focused buyers, professional salon channels, and specialty retailers across mass-market and prestige tiers globally.

This analysis draws on primary survey data, trade channel interviews, and company filing reviews across key markets. Evolvance market research analysts found consistent certification-driven switching behavior across 5 regions and 7 segment groups, combining bottom-up volume modeling with analyst validation to produce a forecast grounded in original fieldwork — not aggregated public sources.

What separates organic hair care from the broader hair care product is the certification layer — USDA Organic, ECOCERT, and GMP standards governing formulation, sourcing, and labeling. Buyers here include natural and specialty retailers, procurement teams at wellness brands, and investors evaluating the organic supply chain across mass, premium, and certified-organic specialist tiers.

Organic hair care consumer behavior is shifting toward multi-concern certified formats. According to EuroConsumers 2024 research, 35% of consumers distrust brand environmental claims — a finding that pushes certified origin labeling and third-party verification up the brand priority list across all organic hair care channels. 48% of cosmetic importers showed FDA non-compliance in 2024, according to Registrar Corp, confirming that certification gaps create both brand risk and competitive opportunity for compliant players.

Product Type Analysis

Shampoo dominates with 36.80% due to high purchase frequency and sulfate-free reformulation momentum.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Shampoo | 36.80% | Daily use, sulfate-free reformulation demand |

| Conditioner | — | Complement purchase with organic shampoo |

| Hair Oils & Serums | — | Scalp treatment and Ayurvedic heritage |

| Styling Products | — | Hold-without-chemicals consumer shift |

| Hair Colorants | — | Chemical-free color, high CAGR sub-segment |

| Waterless Shampoo Bars | — | Eco-packaging and concentrated formats |

| Concentrated Powder Formulations | — | Waste reduction, travel-friendly formats |

In 2025, Shampoo held a dominant market position in the By Product Type segment of the Organic Hair Care Market, with a 36.80% share. Sodium lauryl sulfate sensitivity is the primary switching trigger among standard shampoo buyers — consumers who reject sulfates in their cleansing step logically extend certified organic requirements to conditioners and serums in subsequent purchases. Daily-use frequency gives certified organic shampoo brands disproportionate repeat-purchase revenue compared to lower-frequency product categories like colorants or styling products.

Conditioner functions as the natural complement purchase to organic shampoo, benefiting from co-formulation logic — brands that win shampoo placement typically secure conditioner shelf space in the same retail cycle. This pairing dynamic means organic shampoo growth structurally pulls conditioner revenue upward without requiring independent demand-generation investment.

Hair oils and serums are growing fastest within the non-shampoo sub-segments, powered by Ayurvedic heritage formulations gaining mainstream certification and scalp microbiome positioning in specialty retail across North America and Europe.

Organic hair colorants represent one of the fastest-growing product sub-segments in this market, driven by consumer rejection of ammonia, resorcinol, and p-phenylenediamine found in standard color formulations. Plant-based henna, indigo, and biotech-derived pigment systems are gaining certification and shelf placement as brands respond to the color category’s historically high chemical load.

Waterless shampoo bars and concentrated powder formulations address both the shelf-life challenges of water-based organic products and eco-packaging demand — two converging consumer priorities that make concentrated formats the most structurally distinct innovation archetype in the organic hair care pipeline.

End-Use Analysis

Women dominate with 71.4% due to higher ingredient literacy and stronger premium price acceptance.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Women | 71.4% | Ingredient awareness, premium willingness |

| Men | — | Fastest-growing end-use, clean grooming shift |

| Kids | — | Parental safety concerns, sensitive formulas |

| Gender-Neutral/Non-Binary | — | Inclusive branding, multi-use formats |

In 2025, Women held a dominant market position in the By End-Use segment of the Organic Hair Care Market, with a 71.4% share. Female buyers show higher ingredient literacy — reading INCI lists, cross-referencing certifications, and switching brands on formulation grounds more readily than other demographic groups. This behavior drives higher average order values and stronger brand loyalty in specialty and online organic hair care channels, making women the most commercially valuable acquisition target for certified organic brands at every price tier.

Men’s organic hair care is the fastest-growing end-use segment, as clean grooming culture — driven by ingredient awareness migrating from skin care — reaches shampoo, conditioner, and scalp treatment categories. Brands targeting men with certified organic formulations are finding strong DTC conversion rates, particularly in scalp health sub-segments where clinical credibility pairs with clean-label positioning. The men’s organic shelf environment remains significantly less saturated than women’s, meaning early entrants with certified formulations face lower brand loyalty barriers to overcome at point of purchase.

Kids’ formulations attract parental safety-driven spend, with sulfate-free and fragrance-free certifications serving as primary purchase triggers for household switching from standard to organic products. This sub-segment performs strongest in India, the Philippines, and Western Europe, where baby hair care is a culturally embedded practice combined with rising parental ingredient scrutiny.

Gender-neutral and non-binary positioning is the preferred go-to-market strategy for DTC and clean beauty brands that want to maximize addressable market without investing in gender-differentiated formulation, packaging, or messaging — a format growing fastest in North America and Western Europe.

Hair Type Analysis

Dry hair leads with 35% due to natural alignment between moisture-deficit needs and oil-rich organic botanical formulations.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Dry | 35% | Oil-rich botanicals, moisture retention |

| Straight | — | Lightweight organic serums and protectants |

| Wavy | — | Frizz control without silicones |

| Curly | — | Define-and-hold without sulfates |

| Coily/Textured | — | Deep moisture, shea and babassu butters |

| Damaged/Chemically Treated | — | Bond repair, protein-free alternatives |

In 2025, consumers with dry hair held a dominant position in the By Hair Type segment of the Organic Hair Care Market at 35% of revenue. Dry hair’s moisture deficit aligns naturally with organic ingredient strengths — argan oil, babassu butter, and fermented plant extracts deliver conditioning results that synthetic silicones replicate but certified-organic buyers actively reject on formulation grounds. This structural alignment means dry hair consumers show higher organic conversion rates than any other hair type segment at equivalent price points.

Coily and textured hair types are gaining outsized momentum within the organic segment, driven by ingredient innovations like shea butter and micro-algae extracts targeting curl definition without synthetic polymers. This sub-segment is culturally significant in the US, UK, and West African markets, where natural hair movements have created strong organic brand loyalty among textured hair consumers who actively research formulation ingredients before purchase.

Damaged and chemically treated hair buyers represent a high-value sub-segment — they convert from standard bond-repair treatments to organic alternatives driven by concerns over synthetic protein overload, and their purchase urgency generates higher trial-to-repurchase conversion rates than preventative-use segments.

Distribution Channel Analysis

Offline channels dominate with 70.08% due to trial-driven purchase behavior and in-store certification discovery.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Offline (total) | 70.08% | Trial, certification discovery, in-store education |

| Specialty Stores | — | Curated organic assortment, staff expertise |

| Supermarkets/Hypermarkets | — | Mass organic shelf expansion |

| Pharmacies/Drug Stores | — | Scalp health and therapeutic positioning |

| Online Stores | — | Subscription models, DTC brand growth |

In 2025, offline channels held a dominant market position in the By Distribution Channel segment of the Organic Hair Care Market, with a 70.08% share. Physical retail drives organic hair care’s first purchase — buyers routinely verify certification marks and assess formulations in-store before committing. Specialty stores and pharmacies carry disproportionate influence because staff education on organic claims directly converts trial into loyalty, making in-store interaction the most cost-effective customer acquisition channel for certified organic brands at premium price points.

Online stores are the fastest-growing distribution sub-channel, with DTC subscription models and ingredient-transparent product pages accelerating repeat-purchase rates beyond what physical retail achieves. Social platform discovery converts directly to search and purchase on Amazon, Nykaa, and brand DTC sites — a pattern that rewards brands with agile digital shelf management and ingredient storytelling capability.

Specialty stores maintain the highest average transaction value per organic hair care visit, as curated assortments and staff expertise reduce price resistance among premium certified-organic buyers who arrive with high purchase intent but require formulation validation before committing.

Scalp Concern Analysis

Anti-Dandruff leads with 50% due to crossover appeal between therapeutic efficacy and clean-label demand.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Anti-Dandruff | 50% | Therapeutic efficacy, zinc-free natural alternatives |

| Hair Loss & Thinning | — | Scalp microbiome repair, caffeine and rosemary actives |

| Sensitive Scalp | — | Fragrance-free, hypoallergenic certifications |

| Scalp Microbiome Balancing | — | Skinification, probiotic and prebiotic formulations |

In 2025, anti-dandruff solutions held a dominant market position in the By Scalp Concern segment of the Organic Hair Care Market, with a 50% revenue share. Standard anti-dandruff formulas rely on zinc pyrithione and coal tar that scalp-health-conscious buyers actively reject. Organic alternatives using willow bark salicylic acid and tea tree oil capture this switching demand at premium price points — a positioning that combines therapeutic credibility with certified clean-label claims, attracting both efficacy-first and ethics-first buyer segments simultaneously.

Hair loss and thinning treatments are the highest-growth sub-segment within scalp concern, with caffeine, rosemary oil, and copper tripeptide-1 formulations accumulating clinical evidence while staying within certified organic ingredient frameworks. This convergence of efficacy data and clean-label positioning is shifting consumers away from standard treatments toward organic scalp systems that address thinning preventatively rather than reactively — a behavioral shift that extends usage frequency and increases annual spend per buyer.

Scalp microbiome balancing is the newest positioning frontier, with probiotic and prebiotic formulations bridging the gap between the skinification trend and scalp treatment efficacy in prestige and specialty channels.

Key Market Segments

By Product Type

- Shampoo

- Conditioner

- Hair Oils & Serums

- Styling Products

- Hair Colorants

- Waterless Shampoo Bars

- Concentrated Powder Formulations

By End-Use

- Women

- Men

- Kids

- Gender-Neutral/Non-Binary

By Hair Type

- Dry

- Straight

- Wavy

- Curly

- Coily/Textured

- Damaged/Chemically Treated

By Distribution Channel

- Offline

- Online Stores

- Specialty Stores

- Supermarkets/Hypermarkets

- Pharmacies/Drug Stores

By Scalp Concern

- Anti-Dandruff

- Hair Loss & Thinning

- Sensitive Scalp

- Scalp Microbiome Balancing

By Ingredient Source

- Upcycled Botanical Ingredients

- Fermented Plant Extracts

- Ancient Ayurvedic Formulations

- Micro-Algae Extracts

By Personalization Level

- AI-Driven Custom Blends

- Subscription-Based Targeted Kits

- DNA-Based Hair Health Analysis

Organic Hair Care Market Regional Insights

North America Holds 35.2% Share at USD 7.31 Billion

North America leads the global organic hair care market with 35.20% revenue share, valued at USD 7.31 billion in 2025. USDA Organic certification infrastructure, strong specialty retail penetration, and a consumer base where clean-label hair care has moved from niche to mainstream premium anchor this leadership position. L’Oréal, Procter & Gamble, and Unilever hold structural shelf advantages in this region that newer certified-organic entrants cannot replicate at equivalent speed or cost.

| Region / Country | Market Value (2025) | Share % | CAGR (2026–2035) |

|---|---|---|---|

| North America | USD 7.31 Billion | 35.20% | — |

| United States | USD 6.78 Billion | 31.5% | 8.50% |

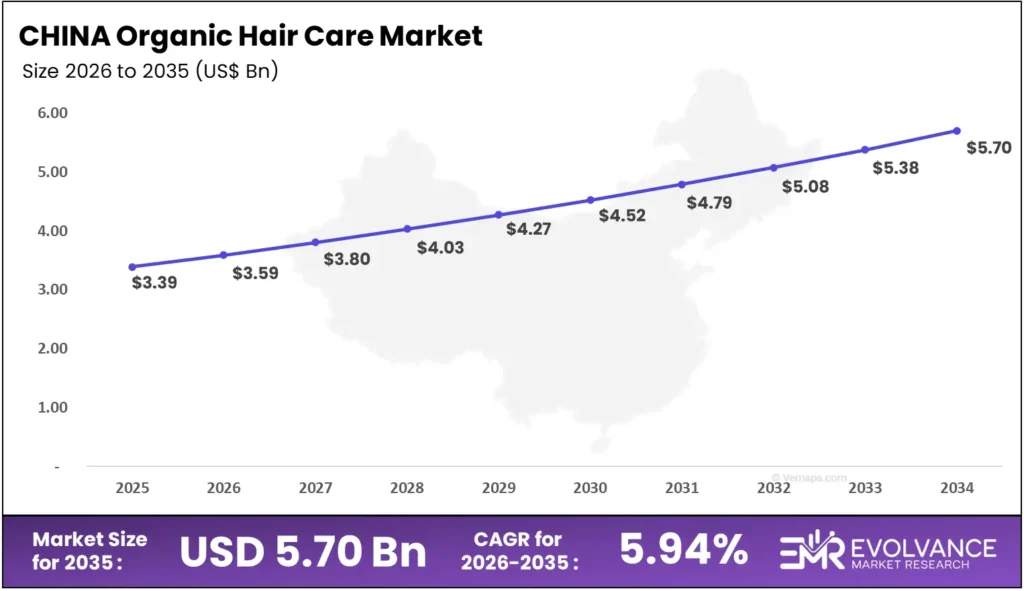

| China | USD 3.39 Billion | — | 5.94% |

| Asia Pacific | — | — | Fastest growing |

| Europe | — | — | — |

| Latin America | — | — | — |

| Middle East & Africa | — | — | — |

North America’s dominance means any brand targeting the global organic hair care market must establish a certified position in the US first. The retail systems — Whole Foods, Target clean beauty aisles, and specialty platforms — built here transfer directly to other developed markets in Europe and Australia, making the United States at USD 6.78 billion in 2025 the most strategically leveraged market entry point in the category.

Asia Pacific Organic Hair Care Market Trends

Asia Pacific posts the fastest organic hair care growth of any region, with China generating USD 3.39 billion in 2025 at a 5.94% CAGR — reflecting mass-market price sensitivity and limited ECOCERT shelf penetration across standard retail channels.

According to Unilever’s 2024 annual report, urban Asia-Pacific underlying sales grew 4.1% in 2024, signaling accelerating organic demand across the broader region beyond China’s established base. India represents the most structurally distinctive organic hair care market within Asia Pacific, where Ayurvedic ingredient heritage gives domestic brands a certified-natural formulation edge that global multinationals cannot authentically replicate through reformulation alone.

Europe Organic Hair Care Market Trends

Europe’s organic hair care market benefits from EU Cosmos certification, which sets a higher ingredient-origin threshold than USDA Organic and drives formulation premiumization across Germany, France, and the UK. According to P&G’s FY2025 annual report, hair care organic volume grew 1% in FY2025, with positive European performance confirming certified premium absorption in regional retail. The EU Green Claims Directive adds a compliance layer requiring substantiated environmental claims — a development that benefits established certified organic brands over greenwashing competitors.

Latin America Organic Hair Care Market Trends

Latin America’s organic hair care market faces a structural supply tension — the region produces key organic ingredients including argan, quinoa protein, and Amazonian botanicals, yet domestic certification systems remain underdeveloped relative to export demand.

Brands sourcing from Andean and Brazilian suppliers face El Niño-driven yield variability that creates input cost volatility without proportionate regional retail revenue to absorb it. High humidity, growing middle-class personal care spending, and strong local ingredient heritage position Latin America as a volume growth market for organic brands with established supply chain resilience.

Middle East and Africa Organic Hair Care Trends

Middle East and Africa represent an emerging organic hair care frontier, where argan oil heritage in Morocco and growing urban wellness spending in Gulf Cooperation Council markets are creating initial demand signals for certified clean formulations.

Premium international brands entering MEA are positioning certified organic variants alongside standard lines to test price acceptance before committing to full regional certification compliance rollouts. Low unit prices and high population density across sub-Saharan Africa make this a volume-over-margin priority market for organic brands with mass-accessible certified formulations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The European Commission’s EU Green Claims Directive — advancing through legislative stages in 2024–2025 — requires brands making organic or natural claims to provide substantiated, independently verified evidence. This applies directly to organic hair care products sold across Germany, France, and the UK, raising the compliance threshold for ECOCERT and EU Cosmos claims beyond self-certification. Brands without third-party audit trails face retail delisting as the directive moves toward enforcement.

In the United States, the Modernization of Cosmetics Regulation Act — MoCRA — introduced mandatory safety substantiation requirements for cosmetic products from 2024 onward. According to Registrar Corp’s 2024 data, 48% of cosmetic importers showed FDA non-compliance, confirming that MoCRA implementation is creating a structural divide between compliant certified-organic brands and non-compliant conventional competitors. Organic hair care brands with existing third-party certification systems are positioned to absorb MoCRA requirements with lower incremental compliance costs than uncertified peers.

India’s Food Safety and Standards Authority — FSSAI — and the Bureau of Indian Standards tightened Ayurvedic hair care product labeling and ingredient origin documentation requirements in 2024, directly affecting the Herbal/Ayurvedic formulation sub-segment. This regulatory tightening raises compliance costs for smaller domestic producers while creating export credibility advantages for established certified Ayurvedic brands expanding into the UAE, USA, and UK diaspora markets, where documentation standards are even more rigorous.

Drivers

Clean Formulation Demand Reshapes Organic Hair Care Shelves

Consumer rejection of synthetic sulfates, parabens, and silicones is the primary structural driver of organic hair care growth in 2025. This shift reflects documented changes in beauty purchase criteria — ingredient safety now outranks price for a growing share of premium hair care buyers across North America and Europe. Brands without third-party certification are actively losing shelf position to certified alternatives, and the reformulation investment required to achieve USDA Organic or ECOCERT status has become a baseline competitive requirement rather than a differentiator in specialty and pharmacy channels.

In our view, scalp skinification — applying facial-grade active ingredients to the scalp — is the single most commercially significant force reshaping organic hair care formulation in 2025. Consumers now understand that scalp condition directly determines hair quality, elevating scalp health from a therapeutic niche to mainstream positioning. Brands using hyaluronic acid and antioxidants in certified organic formulations command premiums that standard scalp products cannot reach — creating a category growth premium of more than double the standard nourishment rate for brands that make the skinification transition within certified frameworks.

Beyond natural demand, strategic acquisitions are expanding the certified organic competitive set faster than internal R&D alone. According to Meridian IB’s 2024 M&A data, personal care multiples reached 2.3x EV/Revenue in H1 2024 — confirming that acquirers pay significant premiums for organic hair care scale. L’Oréal’s Color Wow acquisition in June 2025 targeted professional hair care innovation that internal R&D could not deliver at an equivalent speed, signaling that acquisition-led organic scale is now a mainstream strategic option for multinationals.

Restraints

Organic Certification Gaps Limit Brand Scale in 2025

Inconsistent access to USDA Organic, ECOCERT, and EU Cosmos certification limits organic hair care brand growth in 2025. Certification requires supply chain traceability to ingredient origin — documentation systems that most small-to-mid-sized brands lack at scale. Brands that cannot certify are locked out of the premium retail shelf positions that generate this category’s highest-margin revenue, while the compliance cost of achieving certification creates a structural barrier that consolidates market power among established players.

Higher costs for certified botanical ingredients and biodegradable packaging are compressing organic hair care margins across the forecast period. El Niño-driven agricultural disruptions caused argan output losses exceeding 20% across Andean production zones in 2024, per IMF regional data. These input cost spikes cannot be absorbed by brands locked into fixed retail pricing structures — operators without multi-source ingredient contracts or price hedging arrangements face the sharpest margin exposure as weather volatility continues through the forecast period.

Greenwashing scrutiny represents a third structural restraint, compounded by documented consumer distrust. According to research, 35% of consumers distrust brand environmental claims — a distrust level that undermines uncertified organic positioning and forces brands toward expensive third-party verification to maintain credibility. Brands that invest in open-source formulation disclosure and certified origin labeling are outperforming peers on conversion rate and customer retention, but the investment required to achieve this credibility level raises the minimum viable brand-building cost for new organic hair care entrants.

Growth Factors

Personalized Organic Hair Solutions Open Significant Revenue

Personalized and science-backed organic hair care — AI diagnostics, DNA analysis, and targeted subscription kits — is the most significant revenue expansion opportunity in this category through 2026. Individualized outcomes command LTV multiples unavailable at the mass organic tier, justifying premium pricing and subscription retention investments that standard organic brands cannot access. According to Sky Organics’ 2025 launch data, certified organic scalp products targeting specific hair types launched in April 2025, confirming retail readiness for targeted organic solutions at accessible price points.

Waterless and refillable organic hair care formats are creating a distinct innovation avenue in 2025, addressing eco-conscious demand and the shelf-life challenges of water-based organic products simultaneously. Concentrated formats remove water as a filler ingredient — improving certified organic content percentage and environmental footprint in a single reformulation decision. Brands launching waterless shampoo bars and powder concentrate lines are achieving lower unit production costs and reduced retail return rates among clean beauty buyers, making waterless formats the most capital-efficient innovation archetype available to organic brands at both mass and premium price points.

Biotech and fermented ingredients are expanding organic hair care performance credibility across the forecast period, closing the efficacy gap that historically limited certified organic adoption among performance-first buyers. Fermentation technology lowers the cost of high-potency plant actives, enabling clinical performance benchmarks within full certification compliance. Operators entering the biotech-organic space are positioning their products as performance equivalents to standard premium formulations — not merely ethical alternatives — unlocking buyer segments that previously rejected organic on efficacy grounds alone.

Emerging Trends

Skinification Makes Scalp the New Face of Organic Hair Care

Scalp skinification — treating the scalp as an extension of the facial routine — is the defining trend reshaping organic hair care product development in 2025–2026. Rising consumer understanding of scalp microbiome science drives this shift from cosmetic to therapeutic positioning, with certified organic brands uniquely positioned because prebiotics, botanical antioxidants, and fermented actives satisfy both skinification and clean-label purchase requirements simultaneously. Products leading with scalp microbiome and follicle activation claims are growing at significantly faster rates than standard nourishment oils across all prestige channels.

Green chemistry and biodegradable ingredients have become baseline expectations in premium organic hair care channel placement in 2025 — no longer differentiators. Brands entering on certification credentials alone now face full lifecycle sustainability scrutiny from retail buyers, covering ingredient sourcing through packaging end-of-life. Operators with closed-loop sourcing and refill systems are building structural competitive advantages that certification-only competitors cannot match, as premium retail gatekeepers add lifecycle documentation requirements to their organic brand assessment criteria.

Preventative hair wellness is rising across the organic hair care category as scalp resilience replaces reactive damage treatment as the primary consumer motivation in 2025–2026. Consumers now buy scalp microbiome products before visible damage occurs — extending organic usage frequency and annual spend per buyer beyond what reactive treatment positioning achieves. Brands positioning organic hair care as preventative health rather than cosmetic maintenance are achieving stronger LTV and lower subscription churn, confirming that the preventative wellness positioning is a structural revenue upgrade from standard organic category framing.

Key Companies Insights

L’Oréal leads the organic hair care premium segment with EUR 44.05 billion in group sales in 2025, growing 4.0% like-for-like, according to L’Oréal’s 2025 annual results. Its Professional Products division — home to Kérastase — posted 5.7% growth, the strongest of any L’Oréal division, confirming salon-channel organic premiumization as its primary competitive lever. The Color Wow acquisition in June 2025 targeted professional hair care innovation that internal R&D could not deliver at equivalent speed.

| Company | Revenue / Sales | Growth Rate | Year Reported |

|---|---|---|---|

| L’Oréal Group | EUR 44.05 Billion | +4.0% like-for-like | FY2025 |

| L’Oréal Professional Products | EUR 5.16 Billion | +5.7% | FY2025 |

| L’Oréal (Operating Profit) | EUR 8.89 Billion | 20.2% margin | FY2025 |

| Procter & Gamble (total) | USD 84.3 Billion | +2% organic | FY2025 |

| P&G Beauty Segment | USD 14.96 Billion | -2% | FY2025 |

| Unilever (total) | EUR 50.5 Billion | +3.5% underlying | FY2025 |

| Unilever Personal Care | EUR 13.2 Billion | +4.7% underlying | FY2025 |

| Estée Lauder (total) | USD 14.33 Billion | -8% | FY2025 |

| Estée Lauder Hair Care | USD 565 Million | -10% | FY2025 |

| Henkel Hair Area | EUR 3.26 Billion | +6.9% organic | FY2024 |

Our forecast suggests the certified-organic mass-channel tier — anchored by Procter & Gamble — holds the deepest structural distribution advantage for scale. According to P&G’s FY2025 results, its Beauty segment generated USD 14.96 billion, down 2% on SK-II weakness in Greater China, while R&D spending of USD 2.1 billion backs continued scalp technology development. No other player matches P&G’s certified-product shelf presence across North American food, drug, and mass channels — a distribution system that organic specialist brands cannot replicate at comparable speed or cost.

Unilever’s personal care division generated EUR 13.2 billion in 2025 at 4.7% underlying growth — its strongest personal care performance — led by premium organic-adjacent lines and the K18 biotech hair repair integration, according to Unilever’s Q4 2025 results. Emerging market distribution depth across India, Southeast Asia, and Latin America gives Unilever certified-organic reach no other multinational replicates at scale. K18 delivered double-digit growth in 2024, validating biotech-organic as Unilever’s premium hair care growth formula.

The Estée Lauder Companies reported hair care net sales of USD 565 million in FY2025, down 10%, yet hair care operating income recovered from -USD 52 million to +USD 41 million in the same period, according to Estée Lauder’s FY2025 results. This margin recovery confirms that organic prestige repositioning is rebuilding profitability before volume. Aveda anchors its certified organic portfolio in the premium salon channel, sustaining price premiums that protect margin even as total category volume contracts.

Key Companies

- Procter & Gamble

- The Estée Lauder Companies Inc.

- L’Oréal

- Unilever

- Kao Corporation

- Hain Celestial Group

- Honasa Consumer Limited (Mamaearth)

- Davines S.p.A.

- John Masters Organics

- Rahua Beauty

Recent Developments

- January 2026 — Jes + Lou launched Happy Hair Hydrating Shampoo and Calm Balm Hydrating Conditioner, expanding performance-focused clean hair care with sulfate- and silicone-free formulas using plant-derived oils and butters, targeting the hydration-focused organic buyer in specialty and DTC channels.

- September 2025 — Blu & Green expanded with Daily Shampoo and Conditioner Concentrates, building on its 2024 tablet-format launch — emphasizing plastic-free and aerosol-free concentrated formats that reduce packaging waste and carbon impact in premium clean beauty retail.

- June 2025 — L’Oréal closed its acquisition of Color Wow, targeting professional hair care innovation without disclosed value, aimed at accelerating entry into premium certified-organic salon segments versus building equivalent capability through internal R&D alone.

- April 2025 — EVERSOFT launched its Nature’s Therapy shampoo range across the Southeast Asia region, extending its Organic Haircare line with targeted results-driven products positioned at the intersection of nature-inspired therapy and mass-market accessibility in the APAC growth corridor.

- April 2025 — Sky Organics expanded its certified organic hair care collection with two new scalp care products — Shea & Babassu Moisture Butter and Castor Oil with Rosemary — formulated for curly hair, potent plant-based ingredients, and sustainability.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 20.94 Billion |

| Forecast Revenue (2035) | USD 57.40 Billion |

| CAGR (2026–2035) | 9.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Shampoo, Conditioner, Hair Oils & Serums, Styling Products, Hair Colorants, Waterless Shampoo Bars, Concentrated Powder Formulations), By End-Use (Women, Men, Kids, Gender-Neutral/Non-Binary), By Hair Type (Dry, Straight, Wavy, Curly, Coily/Textured, Damaged/Chemically Treated), By Distribution Channel (Offline, Online Stores, Specialty Stores, Supermarkets/Hypermarkets, Pharmacies/Drug Stores), By Scalp Concern, By Ingredient Source, By Personalization Level |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Dominant Segment | Shampoo with 36.80% share |

| Dominant Region | North America with 35.20% share, valued at USD 7.31 billion |

| Dominant End-Use | Women with 71.4% revenue share |

| Dominant Distribution Channel | Offline with 70.08% revenue share |

| Competitive Landscape | Procter & Gamble, The Estée Lauder Companies Inc., L’Oréal, Unilever, Kao Corporation, Hain Celestial Group, Honasa Consumer Limited (Mamaearth), Davines S.p.A., John Masters Organics, Rahua Beauty |

| Regulatory Framework | USDA Organic, ECOCERT, EU Cosmos, FDA MoCRA, EU Green Claims Directive, India FSSAI/BIS Ayurvedic Standards |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Sources

- EuroConsumers — 35% of consumers distrust brand environmental claims; survey of 16,000 people across 16 countries on green claims and certification trust, 2024

- Meridian IB — Personal care M&A multiples reached 2.3x EV/Revenue in H1 2024; market update on acquisition activity in organic personal care

- L’Oréal Finance — FY2025 annual results: group sales EUR 44.05 billion (+4.0% like-for-like), Professional Products division EUR 5.16 billion (+5.7%), operating profit EUR 8.89 billion (20.2% margin)

- L’Oréal Finance — Agreement to acquire Color Wow professional haircare brand, June 2025

- Procter & Gamble — FY2025 results: total net sales USD 84.3 billion (+2% organic), Beauty segment USD 14.96 billion (-2%), R&D spending USD 2.1 billion

- Procter & Gamble — FY2025 Annual Report: hair care organic volume growth of 1% in Europe, certified premium absorption in regional retail

- Unilever — Q4 2025 full announcement: Personal Care division EUR 13.2 billion (+4.7% underlying), urban Asia-Pacific underlying sales grew 4.1% in 2024, K18 double-digit growth

- Estée Lauder Companies — FY2025 results: hair care net sales USD 565 million (-10%), operating income recovered from -USD 52 million to +USD 41 million

- Sky Organics (via Yahoo Finance / PR Newswire) — Launch of certified organic scalp care products (Shea & Babassu Moisture Butter and Castor Oil with Rosemary) for curly hair, April 2025