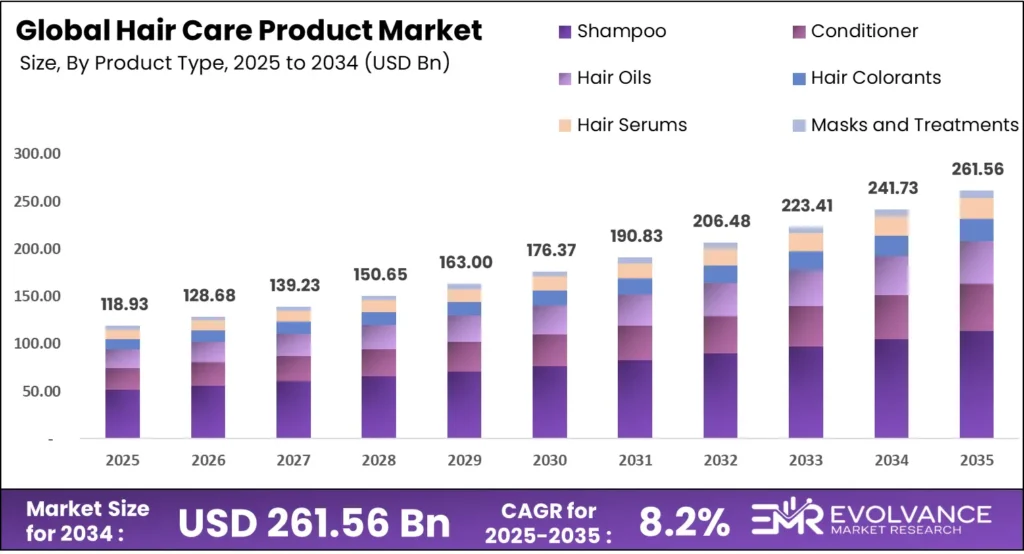

Hair Care Product Market: USD 118.93B to USD 261.56Bn by 2035

The global hair care product market will reach USD 261.56 billion by 2035 from USD 118.93 billion in 2025, growing at a CAGR of 8.2% during the forecast period 2026 to 2035. Premium formulation demand, scalp-first consumer routines, and e-commerce channel expansion are the structural forces widening this gap between base and forecast value.

Investors entering this market face two compounding pressures on margins: input cost volatility in natural ingredients and rising regulatory compliance costs under expanded FDA oversight. As per data from argan-oil.ma, argan seed prices in Agadir reached 225 dirhams per kilogram in March 2024, contributing to sustained raw material cost pressure for premium hair oil and serum formulators. Operators building natural ingredient portfolios must price this supply volatility into five-year investment models.

Hair Care Product Market Highlights: Key Data at a Glance

- Market value: USD 118.93 billion in 2025, forecast to USD 261.56 billion by 2035 at 8.2% CAGR

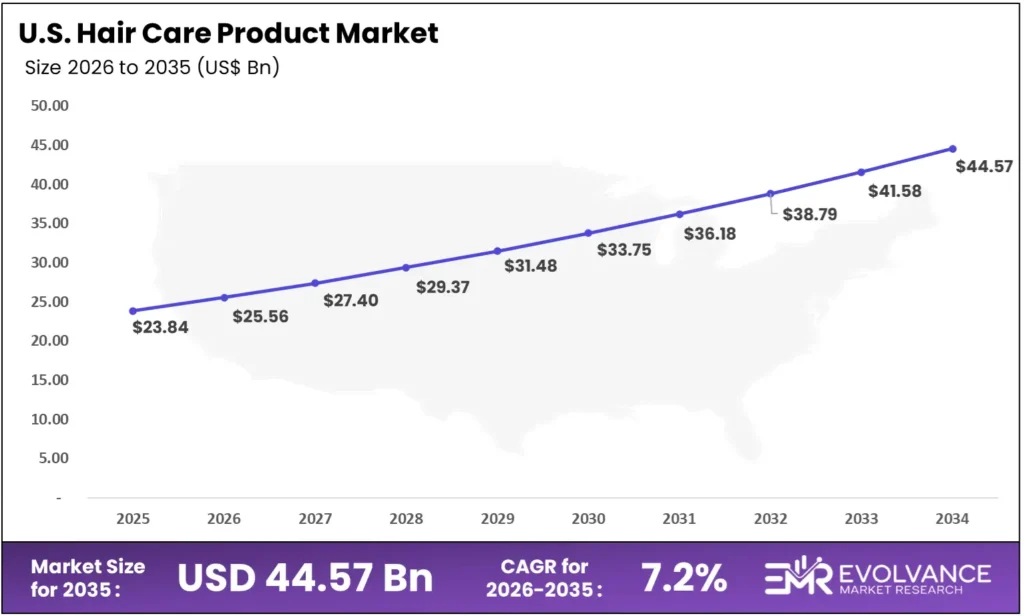

- US market: USD 23.84 billion in 2025, forecast to USD 44.57 billion by 2035 at 7.2% CAGR

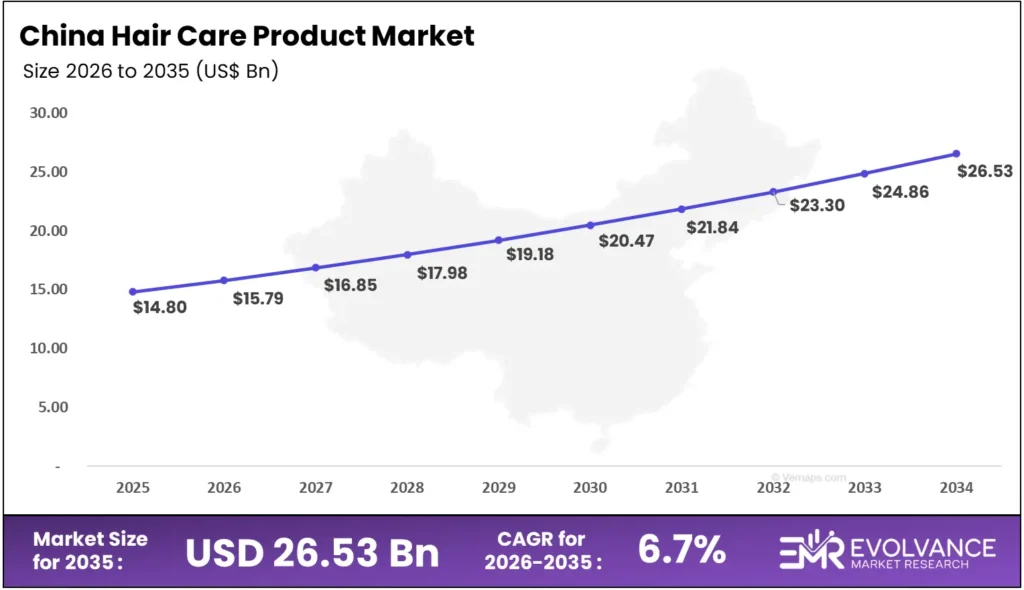

- China market: USD 14.8 billion in 2025, forecast to USD 26.53 billion by 2035 at 6.7% CAGR

- Dominant product segment: Shampoo with 43.5% revenue share, driven by daily repurchase frequency and broadest retail distribution

- Dominant end-use segment: Women with 66.89% revenue share, anchoring mass and premium formulation strategies

- Dominant concern segment: Dry and Damaged Hair with 28.44% revenue share, fueling bond-repair technology adoption

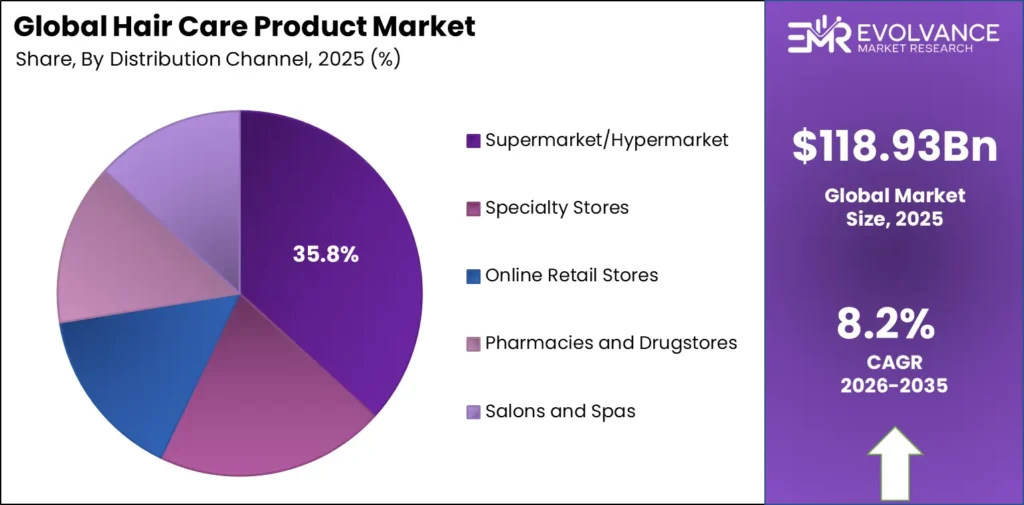

- Dominant distribution channel: Supermarket/Hypermarket with 35.82% revenue share

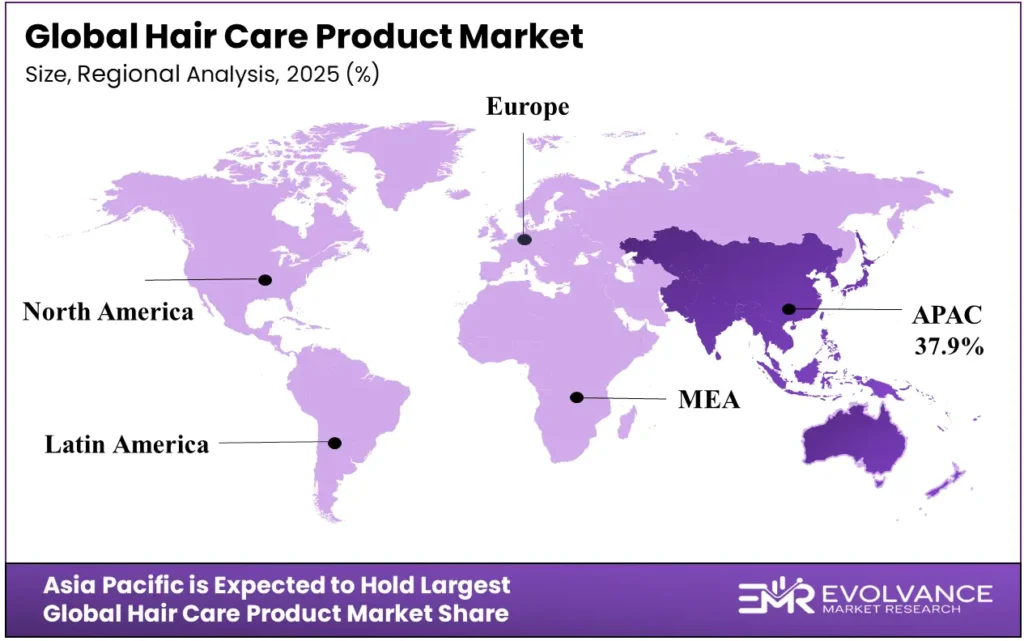

- Asia-Pacific: Largest regional share at 37.9%, valued at USD 45.07 billion, and fastest-growing region globally

- Dominant hair type segment: Straight hair with 35.99% revenue share

- Dominant technology: Bond Repair Technology leads all formulation investment categories

US Hair Care Market: USD 23.84B to USD 44.57B by 2035

The US hair care market will reach USD 44.57 billion by 2035 from USD 23.84 billion in 2025, growing at a CAGR of 7.2%. This growth rate sits below the global average of 8.2% — reflecting a mature market where volume growth is moderate but value expansion through premiumization is structurally embedded. Premium hair care products already hold 39% revenue share in North America as of 2024, up 500 basis points since 2019, confirming that the US market grows through trading up rather than new buyer acquisition.

MoCRA compliance requirements effective July 2024 are reshaping competitive dynamics in US distribution. Facility registration, adverse event reporting, and safety substantiation mandates raise baseline operating costs for all brands — but disproportionately burden undercapitalized indie operators who lack compliance infrastructure. For investors, this regulatory shift is functioning as a consolidation catalyst — well-resourced incumbents like L’Oréal, P&G, and Unilever absorb compliance costs while acquiring MoCRA-stressed indie brands at favorable valuations.

China Hair Care Market: USD 14.8B to USD 26.53B by 2035

The China hair care market will reach USD 26.53 billion by 2035 from USD 14.8 billion in 2025, growing at a CAGR of 6.7%. China’s growth rate is the most conservative among major individual markets — reflecting both macroeconomic softness and P&G’s reported volume declines in Greater China in FY2025. However, the absolute market size trajectory still adds over USD 15 billion in value through the forecast period, making it a strategically significant expansion target for operators with established local distribution infrastructure.

Anti-pollution scalp health positioning is the dominant product development angle for China-specific formulations. Urban consumers in tier-one cities face sustained environmental particulate exposure that drives demand for scalp detox treatments, clarifying shampoos, and microbiome-protecting serums — a formulation need that generic global SKUs do not address. Consequently, operators who localize product claims and active ingredient profiles for Chinese consumers outperform those deploying global portfolio formats without adaptation.

Market Overview: Why Hair Care Spending Is Structurally Resilient

The hair care product market covers shampoos, conditioners, hair oils, colorants, serums, masks, styling products, and dry shampoos sold across retail, professional salon, and direct-to-consumer channels. It excludes hair extensions, wigs, and equipment. Buyers comparing figures across research reports must confirm scope before drawing conclusions, as products-only scopes produce figures meaningfully lower than those bundling services.

This analysis draws on company filings, regulatory disclosures, and trade body data. Evolvance Market Research analysts cross-referenced segment share percentages against reported revenues from L’Oréal, Unilever, Procter & Gamble, and Henkel across 5 regions and 8 product categories — combining fiscal disclosures with distribution channel data to produce a forecast grounded in verifiable corporate performance rather than aggregated estimates alone.

Consumer motivation in this market has shifted from hygiene to performance and identity expression. Products targeting specific hair types, scalp conditions, and molecular-level repair now occupy shelf space that mass cleansers held five years ago. This structural shift means average selling prices are rising even within mass retail channels — a dynamic operators must model when projecting category revenue growth.

Buyer behavior spans three distinct procurement profiles. Individual consumers drive volume through mass and mid-tier channels. Professional salons source premium salon-only brands through distributor networks. Institutional buyers — hotels, airlines, gyms — source standardized formulations through B2B wholesale. Each profile responds to different price signals, brand cues, and product claims, which means a single channel or brand strategy cannot serve all three simultaneously.

Product Type Analysis

Shampoo Dominates with 43.5% Due to Daily Repurchase Frequency

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Shampoo | 43.5% | Daily use and widest retail distribution |

| Conditioner | — | Routine bundling with shampoo |

| Hair Oils | — | Premiumization and ingredient science |

| Hair Colorants | — | Ageing population and self-coloring trend |

| Hair Serums | — | Skinification driving serum adoption |

| Masks and Treatments | — | Bond-repair technology and scalp routines |

| Hair Styling Products | — | Social media-driven styling experimentation |

| Dry Shampoos | — | Convenience and hair health interval extension |

In 2025, Shampoo held a dominant market position in the By Product Type segment of the Hair Care Product Market, with a 43.5% share. No other segment achieves the same repurchase cycle across all income tiers simultaneously. For brand operators, shampoo functions as both a revenue anchor and a consumer acquisition vehicle — buyers who adopt a brand’s shampoo convert into conditioner, serum, and treatment buyers at measurably higher rates than those entering via other product types.

Conditioner operates as the natural complement to shampoo in multi-step routines. Its growth is structurally linked to shampoo category expansion — as sulfate-free and scalp-focused shampoo formats grow, conditioner formulas follow with matching active ingredients like ceramides and peptides. This co-development dynamic creates cross-sell opportunities for brands operating across both formats.

Hair Oils represent the fastest premiumizing sub-segment within the product type category. Argan, coconut, and rosehip formulations targeting dry and damaged hair command significant price premiums over commodity oil formats. Supply volatility in argan — with forests in Morocco shrinking by 40% since 2000 per AP News — creates a structural margin risk for oil-heavy portfolios that operators must actively hedge.

Hair Colorants benefit from two converging demand sources: an ageing population seeking grey coverage and a younger demographic using color as self-expression. The self-coloring trend, accelerated by salon access disruptions in 2020–2021, created lasting behavioral change — consumers who colored at home retained the habit even after salons reopened.

Hair Serums are the direct product of the skinification trend. Consumers now evaluate serums on the same ingredient science framework they use for facial skincare — seeking peptides, niacinamide, and hyaluronic acid in hair formats. This reformulation imperative is not optional for brands with mass retail ambitions — shelf adjacency to skincare-credentialed products has raised the ingredient expectation baseline across all channels.

Masks and Treatments anchor the bond-repair technology investment cycle. Olaplex’s patent validation of clinical-grade at-home treatment created consumer willingness to pay dermatology-adjacent prices for scalable formats. Every major player from L’Oréal to Henkel has since invested in competing bond-repair platforms, making this sub-segment the primary formulation battleground through the forecast period.

Hair Styling Products benefit from social media-driven styling experimentation, particularly on TikTok where tutorial content drives product discovery for heat protectants, curl creams, and edge control formats. This channel advantage disproportionately rewards brands with strong visual identity and influencer partnerships over those relying on traditional retail shelf placement alone.

Dry Shampoos serve a dual function: convenience for consumers extending wash intervals and hair health positioning for those reducing thermal damage frequency. The category’s growth is supported by the scalp health trend — dry shampoo brands repositioning around scalp microbiome protection rather than simple oil absorption command higher price points and better shelf placement.

End-Use Analysis

Women Dominate with 66.89% Due to Multi-Step Routine Complexity

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Women | 66.89% | Multi-step routines and premium product adoption |

| Men | — | Grooming culture expansion and hair loss awareness |

| Unisex | — | Scalp health and clean label positioning |

In 2025, Women held a dominant position in the By End-Use segment of the Hair Care Product Market, with a 66.89% share. Female hair care routines encompass the highest number of distinct product categories — shampoo, conditioner, serum, treatment mask, and styling product usage in a single week is standard. This breadth drives average basket size, retention, and sensitivity to trend cycles across all price tiers.

The Men’s hair care segment is growing faster than any other end-use group. According to Sally Beauty data, Gen Z online beauty purchases totaled 45% in 2024/2025, the highest rate of any demographic — and male Gen Z consumers are leading adoption of scalp treatment and hair loss products. Brands entering men’s via clinical positioning face lower brand loyalty barriers than the saturated women’s segment, creating lower acquisition cost opportunities for well-positioned entrants.

Unisex positioning captures scalp health and clean label demand from consumers who reject gender-coded marketing. This format favors transparent ingredient lists, clinical claims, and minimalist packaging — a positioning strategy that travels well across both DTC and pharmacy channels where clinical adjacency drives purchase decisions.

Hair Type Analysis

Straight Hair Dominates with 35.99% Due to Largest Global Consumer Base

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Straight | 35.99% | Largest global consumer base by hair type |

| Wavy | — | Routine expansion from straight to textured care |

| Curly | — | Hair intellectualism and type-specific formulation |

| Coily | — | Natural hair movement and bond-repair demand |

| Sensitive Scalp | — | Microbiome awareness and dermatologist-adjacent claims |

In 2025, Straight hair held a dominant position in the By Hair Type segment, with a 35.99% share. East Asian markets — particularly China and Japan — anchor this segment’s volume, and K-beauty formulation influence shapes product development across the global straight hair category. For operators planning Asia-Pacific expansion, straight hair-specific claims and formats are table-stakes positioning.

Curly and Coily hair segments represent the highest-growth opportunity within hair type segmentation. Consumers with Type 2–4C hair now buy specifically for curl pattern, porosity level, and protein tolerance — creating demand for formulation specificity that generic moisturizing claims cannot satisfy. This consumer sophistication rewards brands with deep ingredient expertise and penalizes those treating textured hair as a niche extension of straight hair formulas.

Sensitive Scalp positioning bridges the hair type and hair concern segments. Products targeting scalp microbiome balance, fragrance-free formulations, and dermatologist-tested claims capture consumers who experience scalp conditions across all hair types. This cross-segment appeal makes Sensitive Scalp one of the most commercially flexible positioning strategies available to brands across mass, mid-tier, and premium price tiers.

Distribution Channel Analysis

Supermarket/Hypermarket Dominates with 35.82% Due to Mass Shopper Reach

| Channel | Share % | Primary Driver |

|---|---|---|

| Supermarket/Hypermarket | 35.82% | Impulse purchase and broadest shopper reach |

| Specialty Stores | — | Expert consultation and premium SKU discovery |

| Online Retail Stores | — | DTC and marketplace convenience with personalization |

| Pharmacies and Drugstores | — | Clinical credibility for treatment products |

| Salons and Spas | — | Professional endorsement and premium brand trial |

In 2025, Supermarket/Hypermarket held the dominant distribution position with a 35.82% share. This channel dominance masks a structural shift in revenue quality — products sold through supermarkets skew toward mass price tiers, while margin-rich premium and luxury tiers migrate to online and specialty channels. Operators managing multi-channel portfolios must model this bifurcation explicitly when setting channel investment priorities.

Online Retail Stores represent the fastest-rising channel by revenue quality. The personalized recommendation algorithms that online platforms deploy at scale drive conversion into higher-priced serums, scalp treatments, and bundled routines that physical shelf space cannot replicate. This channel advantage disproportionately rewards brands that invest in digital content — ingredient explanation, diagnostic tools, and tutorial formats — that converts discovery into purchase.

Salons and Spas function as the professional endorsement layer that validates premium brand positioning across retail channels. When salon professionals recommend a brand, it moves units in both physical and online retail — a flywheel that requires consistent R&D investment to sustain but generates compounding returns for operators who commit to professional channel relationships over the long term.

Concern Analysis

Dry and Damaged Hair Dominates with 28.44% Due to Bond-Repair Technology Demand

| Concern Segment | Share % | Primary Driver |

|---|---|---|

| Dry and Damaged Hair | 28.44% | Bond-repair technology and heat styling damage |

| Dandruff and Flaky Scalp | — | OTC active ingredient credibility |

| Oily and Greasy Scalp | — | Scalp microbiome awareness growth |

| Hair Loss and Thinning | — | Clinical product pipeline expansion |

| White and Grey Hair | — | Ageing demographic and toning product demand |

| Scalp Microbiome Imbalance | — | Probiotic and prebiotic formulation adoption |

In 2025, Dry and Damaged Hair led concern segments with a 28.44% share. This segment maps directly to the largest formulation investment category in hair care — bond-repair technology. Consumers experiencing measurable results from bond-repair treatments demonstrate the highest brand loyalty and highest tolerance for price increases of any concern sub-segment, making this the most valuable consumer relationship in the category.

Hair Loss and Thinning is transitioning from cosmetically positioned to clinically validated. Investment activity — including Pelage Pharmaceuticals’ USD 120 million Series B in October 2025 for Phase 3 trials — signals that pharmaceutical capital is entering at clinical-stage scale. Cosmetically positioned hair loss brands face a credibility challenge as clinical competitors advance through regulatory pipelines with efficacy data that topical cosmetics cannot match.

Scalp Microbiome Imbalance represents the newest concern segment entering commercial viability. Probiotic and prebiotic formulations targeting scalp microbiome balance command mid-tier to premium pricing while creating routine expansion — consumers adding a scalp probiotic serum consistently add additional product steps within six months. This upsell dynamic makes microbiome positioning one of the highest-LTV entry points in the concern category.

Price Tier Analysis

Mass Tier Dominates Due to Volume Leadership Across All Channels

| Price Tier | Share % | Primary Driver |

|---|---|---|

| Mass | Dominant | Broadest channel reach and highest purchase frequency |

| Mid-Tier | — | Trade-up from mass with accessible premium positioning |

| Premium / Luxury | — | Fastest-growing tier by revenue value |

The Mass tier leads overall revenue through sheer purchase frequency and channel breadth — every supermarket, pharmacy, and convenience store carries mass hair care. However, the strategic growth story belongs to Premium/Luxury. As reported by Lincoln International, premium hair care products’ revenue share in North America reached 39% in 2024, up 500 basis points since 2019 — confirming that the value mix is shifting upward even as mass volume holds.

The Premium/Luxury tier is the fastest-growing by revenue value. This growth is not limited to prestige retail — premium formats are expanding into mass retail channels through sulfate-free shampoo positioning, clean beauty credentials, and clinical claims that command a 15–30% price premium over standard formulations while remaining within mass retail price bands.

Technology / Method Analysis

Bond Repair Technology Dominates Due to Clinical Validation and Patent Moat

| Technology | Share % | Primary Driver |

|---|---|---|

| Bond Repair Technology | Dominant | Clinical validation and Olaplex patent moat |

| AI-Driven Diagnostics | — | Personalization and DTC conversion optimization |

| Water-Activated Formulations | — | Sustainability and packaging reduction |

| Bio-Diffusion Technology | — | Peptide delivery into hair cortex |

Bond Repair Technology leads all formulation investment categories. Olaplex’s Bis-Aminopropyl Diglycol Dimaleate patent demonstrated consumer willingness to pay dermatology-adjacent prices for at-home molecular repair. Every major player — L’Oréal through Kérastase, Henkel through Schwarzkopf’s BC Fibre Clinix, Unilever through K18’s peptide bio-diffusion mechanism — has since invested in competing platforms. For investors, bond-repair competitive intensity signals category maturity — the next differentiation wave will come from scalp microbiome and AI diagnostic platforms layered on top.

AI-Driven Diagnostics is changing the DTC acquisition cost equation. Based on data from Revieve, Gen Z engagement with beauty personalization tools reached 85% in 2025, driving 35% of web traffic for brands deploying diagnostic quizzes and AI recommendation engines. This tool engagement reduces paid social dependency while improving product match accuracy — directly lifting repeat purchase rates for operators who invest in diagnostic infrastructure.

Key Market Segments

By Product Type

- Shampoo

- Conditioner

- Hair Oils

- Hair Colorants

- Hair Serums

- Masks and Treatments

- Hair Styling Products

- Dry Shampoos

By End-Use

- Women

- Men

- Unisex

By Hair Type

- Straight

- Wavy

- Curly

- Coily

- Sensitive Scalp

By Distribution Channel

- Supermarket/Hypermarket

- Specialty Stores

- Online Retail Stores

- Pharmacies and Drugstores

- Salons and Spas

By Concern

- Dry and Damaged Hair

- Dandruff and Flaky Scalp

- Oily and Greasy Scalp

- Hair Loss and Thinning

- White and Grey Hair

- Scalp Microbiome Imbalance

By Price Tier

- Mass

- Mid-Tier

- Premium / Luxury

By Technology / Method

- Bond Repair Technology

- AI-Driven Diagnostics

- Water-Activated Formulations

- Bio-Diffusion Technology

Regional Analysis: Asia-Pacific Leads at 37.9% Share

| Region | Market Value | Share % | Year |

|---|---|---|---|

| Asia-Pacific | USD 45.07 billion | 37.9% | 2025 |

| North America (US) | USD 23.84 billion | Leading developed market | 2025 |

| China | USD 14.8 billion | Part of Asia-Pacific | 2025 |

| Europe | €18.1 billion | Second major region | 2024 |

Asia-Pacific holds 37.9% of global hair care revenue at USD 45.07 billion in 2025 — both the largest and fastest-growing major region. Its structural advantage lies in demographic scale combined with rising per-capita beauty spending. China, Japan, India, and South Korea each represent distinct consumer behavior profiles that collectively generate more product volume than any other regional combination.

North America Hair Care Market: Premium Tier Reaches 39% Share

The US hair care market, valued at USD 23.84 billion in 2025, will reach USD 44.57 billion by 2035 at a CAGR of 7.2%. Premium hair care products’ revenue share in North America reached 39% in 2024, up 500 basis points since 2019, confirming that American consumers are trading up into personalized and biotech-positioned products. MoCRA compliance costs are creating structural advantages for well-capitalized incumbents — facility registration and adverse event reporting requirements raise entry barriers for undercapitalized indie brands.

Europe Hair Care Market Trends

According to Cosmetics Europe, Europe’s hair care products market reached €18.1 billion in 2024, part of €104 billion in total cosmetics retail sales. Germany anchors European hair care through Henkel’s dual-brand strategy across Schwarzkopf Professional salon and Syoss mass retail. The IFRA 51st amendment restricting 48 fragrance materials is raising reformulation costs for all brands operating in European distribution, compressing margins on fragrance-forward styling and treatment products.

Asia Pacific Hair Care Market: Fastest-Growing Region Globally

Asia-Pacific’s growth is driven by three distinct country-level engines. According to South Korea’s Ministry of Trade, South Korea cosmetics exports reached USD 10.2 billion in 2024, a record high, with SME exports at USD 8.3 billion — demonstrating how Korean formulation innovation travels globally through the K-beauty distribution network. China at USD 14.8 billion grows through anti-pollution scalp health positioning. Japan leads UV protection extension from skincare into hair care through Kao Corporation’s domestic portfolio.

India Hair Care Products Market Size and Growth

India represents one of the highest-growth opportunities within Asia-Pacific. According to YouGov data, 28% of Indian consumers are willing to pay up to 10% more for sustainable cosmetics — a meaningful premium tolerance for an emerging market. Ayurvedic ingredient fusion with peptide technology — combining neem, turmeric, and amla with clinically validated actives — is the dominant formulation strategy for capturing dual demand in this market.

Middle East & Africa Hair Care Market Trends

The Middle East and Africa region is underpenetrated but structurally promising for premium and natural hair care. GCC consumers index highly on luxury beauty spending. Saudi Arabia’s Vision 2030 economic diversification has expanded modern retail infrastructure supporting specialty and premium hair care distribution. South Africa serves as the primary sub-Saharan gateway for textured hair care products, with naturals-focused brands gaining distribution across supermarket and specialty channels.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Companies: Three Players Define the Competitive Landscape

Three companies — L’Oréal S.A., Unilever PLC, and Procter & Gamble — dominate global hair care revenue through brand portfolio breadth, manufacturing scale, and acquisition-led access to high-growth sub-segments. This concentration creates high entry barriers in mass retail but leaves premium DTC, clinical, and textured hair segments meaningfully open for challengers operating with different cost structures.

| Company | Revenue / Sales | Growth Rate | Year Reported |

|---|---|---|---|

| L’Oréal S.A. (Group) | €44.05 billion | +1.3% | FY2025 |

| L’Oréal Professional Products | €5.163 billion | +5.7% | FY2025 |

| L’Oréal Consumer Products | €16.09 billion | +0.7% (haircare double digits) | FY2025 |

| Procter & Gamble (Group) | USD 84.3 billion | Flat (organic +2%) | FY2025 |

| P&G Beauty Segment | USD 15.22 billion | +1.4% | FY2024 |

| Henkel Group | €21.586 billion | +0.3% nominal (+2.6% organic) | FY2024 |

| Henkel Consumer Brands | €10.467 billion | +3.0% organic | FY2024 |

According to L’Oréal’s 2025 annual results, L’Oréal Professional Products division reached €5.163 billion in 2025, up 5.7% — outperforming the group’s overall 1.3% growth. This bimodal distribution advantage through Kérastase in both physical salon and e-commerce channels simultaneously is difficult for competitors to replicate quickly, and it explains why L’Oréal’s operating gross margin expanded to 74.3% in 2025.

As reported by P&G investor relations, P&G hair care organic sales were flat in FY2025, with innovation-driven growth in Latin America and Europe offset by volume declines in North America and Greater China. This divergence signals that P&G’s core Pantene and Head & Shoulders brands face premiumization pressure in developed markets while holding volume in emerging ones. The acquisition of Pattern Beauty in Q1 2025 represents P&G’s direct response — building multicultural hair credibility its existing portfolio lacked.

We believe Henkel presents the most underappreciated competitive narrative among the three. Its Hair business area drove organic Consumer Brands growth of 3.0% in FY2024, led by Hair Styling and Hair Colorants — two sub-categories where Schwarzkopf Professional holds stronger salon channel relationships than either P&G or Unilever. Henkel’s adjusted EBIT grew 20.9% to €3.089 billion in FY2024, suggesting pricing discipline is generating margin expansion that its revenue growth rate does not fully reflect.

Based on data from Unilever’s 2024 annual report, Unilever hair care underlying sales grew mid-single digits in 2024, with K18 posting double-digit growth post-integration. The January 2025 acquisition of Nutrafol for ingestible supplements positions Unilever as the only major conglomerate with credible ownership in both topical bond-repair technology and ingestible hair health — a combined positioning no competitor has yet matched.

Kao Corporation anchors Asia-Pacific competitive dynamics through deep Japan domestic penetration and a UV protection hair care platform extending the brand’s skincare credibility into hair. In June 2025, L’Oréal signed an agreement to acquire Color Wow, a fast-growing professional haircare brand with proven humidity-blocking technology — its clearest signal yet that it targets brands with DTC or salon credibility in specific technical benefit categories before integrating them into its global distribution infrastructure.

Top Key Players

- L’Oréal S.A.

- Unilever PLC

- The Procter & Gamble Company

- Henkel AG & Co. KGaA

- Coty Inc.

- Kao Corporation

- John Paul Mitchell Systems

- Revlon, Inc.

- Shiseido Co., Ltd.

- The Estée Lauder Companies Inc.

- Mielle Organics

Related Markets: 5 Segments Shaping Hair Care

Five adjacent markets intersect directly with the hair care product market. Each carries distinct growth dynamics, regulatory exposure, and buyer profiles — but all share the same upstream supplier network and many of the same retail distribution channels. Operators building multi-category beauty portfolios need visibility across all five to avoid concentration risk and identify white-space entry points.

The Hair Oil Market is valued at USD 25.26 billion in 2025 and will reach USD 58.30 billion by 2035 at a CAGR of 7.9%. Its structural advantage is high repurchase frequency paired with premiumization — consumers trading up from commodity oils to clinically positioned serums as ingredient science awareness rises. Supply volatility in argan remains the primary margin risk for operators in this sub-market.

The Organic Hair Care Market is valued at USD 20.94 billion in 2025, forecast to USD 57.40 billion by 2035 at a CAGR of 9.6% — the fastest growth rate among all five cluster markets. The structural challenge is ingredient sourcing cost, which compresses margins at the mass organic price tier while rewarding brands with COSMOS, USDA Organic, and Leaping Bunny certifications in premium channels.

The Men’s Hair Care Market is valued at USD 36.76 billion in 2025, forecast to USD 80.62 billion by 2035 at a CAGR of 7.4%. This market warrants a dedicated investment thesis separate from the women’s segment — male consumers enter via scalp health and hair loss rather than styling, creating a clinical positioning entry point that generic mass brands cannot easily replicate.

The Hair Loss Treatment Market is valued at USD 7.61 billion in 2025, forecast to USD 19.44 billion by 2035 at a CAGR of 8.9%. Investment activity accelerated sharply in late 2025 with Pelage Pharmaceuticals and Veradermics raising a combined USD 345 million — signaling pharmaceutical capital entering at clinical-stage scale with implications for cosmetically positioned hair loss products.

The Shampoo Market is valued at USD 38.23 billion in 2025, forecast to USD 71.82 billion by 2035 at a CAGR of 5.9%. Shampoo anchors the entire hair care category with 43.5% revenue share globally. The US shampoo sub-market warrants separate tracking due to concentration of MoCRA compliance investment and the shift from sulfate-based to sulfate-free formulations commanding meaningful price premiums.

Drivers

Premium Formulation Demand and Professional Channel Growth Drive Margin Expansion

Premium and performance-oriented demand is the single most powerful structural force in this market. Procter & Gamble and Unilever both report resilient hair care sales despite broader economic pressures — confirming that consumers are not trading down. They are either staying premium or waiting for the right innovation to trade up, which narrows the competitive window for mass-only operators to hold volume without margin sacrifice.

The professional salon channel amplifies this premium dynamic. Figures from L’Oréal’s 2025 annual results confirm that the Professional Products division reached €5.163 billion at +5.7% growth — outperforming the group’s overall rate. When salon professionals recommend Kérastase, the brand moves units in both physical and online retail simultaneously. This flywheel generates compounding returns for operators who invest consistently in professional channel relationships and R&D to sustain recommendation credibility.

In our view, bond-repair technology is the formulation driver most structurally embedded in this growth story. L’Oréal’s Consumer Products division reported haircare advancing in double digits within a division that grew only 0.7% overall in FY2025 — a divergence that points directly to bond-repair and scalp-positioned SKUs outperforming the broader mass portfolio. Operators who have not built a credible bond-repair or scalp-science platform are already behind the formulation baseline the market expects.

Restraints

MoCRA Compliance and Input Cost Inflation Compress Margins for Indie Brands

The FDA Modernization of Cosmetics Regulation Act (MoCRA), effective July 2024, has materially raised compliance costs for hair care manufacturers in US distribution. Facility registration, mandatory adverse event reporting, and safety substantiation requirements now apply to all brands — including indie and DTC operators who previously had minimal FDA interaction. For undercapitalized brands, MoCRA is functioning as a consolidation catalyst — creating acquisition targets for well-resourced buyers who can absorb compliance infrastructure costs.

Input cost inflation compounds the regulatory burden. As per AP News data, argan forests in Morocco shrunk by 40% since 2000, reducing fruit yield and exacerbating price volatility for natural hair care ingredients. Brands relying on argan as a hero ingredient face a structurally higher cost base with no short-term supply relief — an asymmetric competitive disadvantage that erodes margin regardless of how strong demand-side momentum is.

Consumer economic caution in key markets adds a third layer of margin pressure. Beauty retailers including Douglas have tempered forecasts amid reduced premium spending on personal care. This demand softness does not affect the premium tier uniformly — it disproportionately impacts mid-tier brands caught between mass price points they cannot match and premium credentials they have not established. Operators without clear tier positioning face the highest churn risk in a cautious consumer environment.

Opportunities

Scalp Health Positioning and E-Commerce Personalization Unlock Premium Revenue

Scalp-first product positioning unlocks the highest average selling price expansion of any current opportunity in the category. Scalp serums, exfoliators, and microbiome-balancing treatments command mid-tier to premium pricing while driving routine expansion. According to Sally Beauty financial data, global e-commerce accounted for 10.7–11.1% of net sales in beauty retail — and scalp care leads online discovery because ingredient explanation converts best in long-form digital content that physical retail cannot replicate.

Investment in hair loss therapy is accelerating market potential. In October 2025, KilgourMD closed a USD 5 million funding round targeting menopausal hair loss — confirming that sub-segment specificity is attracting capital even at early stage. In December 2025, yuv secured USD 12 million in Series A for smart salon hair color technology. These funding signals define where adjacent white space still exists for operators building specialist brand portfolios within the broader category.

E-commerce channel economics offer a structural advantage over traditional wholesale for brands with strong digital content. Based on data from Phoenix Strategy Group, referral programs delivered customer acquisition costs of $150 for B2B in 2025, outperforming paid social at $230 and organic search at $290. For hair care DTC operators, referral and loyalty-driven acquisition models generate higher LTV:CAC ratios — with top performers reaching 4:1 to 6:1 — than wholesale channel economics allow.

Trends

Skinification and AI Personalization Reshape Hair Care Formulation Economics

The skinification of hair care means consumers now evaluate hair care products on the same ingredient science framework they use for skincare — reading INCI labels for peptides, niacinamide, hyaluronic acid, probiotics, and ceramides. This is a formulation investment imperative, not a marketing trend. Brands that have not reformulated core lines to include at least one clinically recognized skincare active risk losing shelf position to K18, Vichy Dercos, and CeraVe-adjacent hair care extensions that the same consumer already trusts in facial routines.

AI personalization is changing the acquisition cost structure across DTC hair care. As per Kyra research, Gen Z beauty purchases were 37% driven by trend recreation in 2024/2025, with 39% discovering products via TikTok — creating a viral discovery dynamic that AI recommendation engines then convert into recurring purchase behavior. L’Oréal’s Beauty Genius AI tool achieved a 28% share of beauty influence in advocated media in 2024 post-ModiFace integration. For operators, AI diagnostics reduce paid social dependency while lifting repeat purchase rates.

Sustainability credentials are moving from positioning tool to purchase requirement in developed markets. As per PwC survey data, global consumers’ willingness to pay a premium for sustainable beauty products averaged 9.7% in 2024. In late 2025, Dyson expanded into consumable hair care products — frizz-busting and shine-boosting items — building on patented technologies from its Airwrap tool. This move signals that hardware-to-consumables models are entering hair care as a distinct growth strategy, creating a new competitive dimension for traditional formulation-only brands to address.

Recent Developments: L’Oréal and Funding Activity Lead 2025–2026

- January 2026 — L’Oréal introduced the Light Straight + Multi-styler at CES 2026, using patented infrared light technology to style hair at lower temperatures for better hair health protection — recognized as a CES 2026 Innovation Award honoree with global launch planned for 2027.

- January 2026 — &Done (haircare brand) raised USD 3 million in Series A funding led by RTP Global at a post-money valuation of INR 125 crore to scale R&D, expand product portfolio, and widen salon network.

- December 2025 — Veradermics raised USD 75 million in Series B financing to support initiation of Phase 2/3 trials for its oral hair loss therapeutic targeting regulatory submission pathways.

- October 2025 — Pelage Pharmaceuticals closed a USD 120 million Series B co-led by ARCH Venture Partners and GV (Google Ventures) to advance PP405, a topical small molecule for reactivating dormant hair follicle stem cells, with Phase 3 trials planned for 2026.

- October 2025 — Veradermics raised USD 150 million in an oversubscribed Series C round to advance its oral therapeutic for hair regrowth through regulatory submissions.

- September 2025 — Blackstone agreed to make a significant investment in South Korean premium hair care brand Juno to boost growth and support global expansion infrastructure for the K-beauty brand.

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 118.93 billion |

| Forecast Revenue (2035) | USD 261.56 billion |

| CAGR (2026–2035) | 8.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Shampoo, Conditioner, Hair Oils, Hair Colorants, Hair Serums, Masks and Treatments, Hair Styling Products, Dry Shampoos), By End-Use (Women, Men, Unisex), By Hair Type (Straight, Wavy, Curly, Coily, Sensitive Scalp), By Distribution Channel (Supermarket/Hypermarket, Specialty Stores, Online Retail Stores, Pharmacies and Drugstores, Salons and Spas), By Concern (Dry and Damaged Hair, Dandruff and Flaky Scalp, Oily and Greasy Scalp, Hair Loss and Thinning, White and Grey Hair, Scalp Microbiome Imbalance), By Price Tier (Mass, Mid-Tier, Premium/Luxury), By Technology (Bond Repair Technology, AI-Driven Diagnostics, Water-Activated Formulations, Bio-Diffusion Technology) |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Dominant Segment | Shampoo with 43.5% revenue share; Women with 66.89% end-use share |

| Dominant Region | Asia-Pacific with 37.9% share valued at USD 45.07 billion |

| Dominant Technology | Bond Repair Technology |

| Regulatory Framework | FDA MoCRA (effective July 2024), EU Cosmetics Regulation EC No 1223/2009, IFRA 51st Amendment, ISO 22716, COSMOS, REACH |

| Competitive Landscape | L’Oréal S.A., Unilever PLC, The Procter & Gamble Company, Henkel AG & Co. KGaA, Coty Inc., Kao Corporation, John Paul Mitchell Systems, Revlon Inc., Shiseido Co. Ltd., The Estée Lauder Companies Inc., Mielle Organics |

Sources

- Argan-Oil.ma — Argan seed price per kilogram in Agadir, March 2024, and year-over-year price volatility data

- Lincoln International — Premium hair care revenue share in North America, 2024 and 2019 comparison

- Personal Care Insights / Kyra Research — Gen Z online beauty purchase rate, TikTok discovery rate, and trend recreation purchase drivers, 2024/2025

- Revieve — Gen Z engagement with beauty personalization tools and web traffic contribution, 2025

- L’Oréal Finance — L’Oréal Group annual sales, operating profit, gross margin, Professional Products and Consumer Products division performance, FY2025

- Procter & Gamble Investor Relations — P&G net sales, core EPS, hair care organic sales performance by region, FY2025

- Unilever Annual Report 2024 — Hair care underlying sales growth, K18 post-acquisition performance, Latin America underlying sales, productivity savings

- Henkel — Group sales, adjusted EBIT, Consumer Brands organic growth, Hair business area performance, FY2024

- South Korea Ministry of Trade, Industry and Energy — South Korea cosmetics export value and SME export share, 2024

- Cosmetics Europe — Europe hair care products market value and total cosmetics retail sales, 2024

- YouGov — Indian consumer willingness to pay premium for sustainable cosmetics, 2024

- China Briefing / PwC — Global consumer willingness to pay premium for sustainable beauty products, 2024

- Phoenix Strategy Group — Customer acquisition cost benchmarks by channel including referral, paid social, and organic search, 2025

- AP News — Argan forest shrinkage in Morocco since 2000 and impact on natural hair care ingredient supply, 2025

- Pelage Pharmaceuticals — USD 120 million Series B financing details, PP405 program, and Phase 3 trial plans, October 2025

- Veradermics — USD 150 million Series C financing for oral hair regrowth therapeutic, October 2025

- Veradermics — USD 75 million Series B financing for Phase 2/3 trial initiation, December 2025

- WWD — KilgourMD USD 5 million funding round for menopausal hair loss product development, October 2025

- Vestbee — yuv USD 12 million Series A for smart salon hair color technology, December 2025

- Blackstone — Investment in South Korean premium hair care brand Juno for global expansion, September 2025

- L’Oréal — Light Straight + Multi-styler launch at CES 2026, infrared light technology and Innovation Award recognition, January 2026

- L’Oréal Finance — Agreement to acquire Color Wow professional haircare brand, June 2025

- Entrepreneur India — &Done haircare brand USD 3 million Series A funding, valuation, and growth plans, January 2026

- Procter & Gamble Annual Report 2024 — Beauty segment net sales, hair care organic growth, Latin America performance, FY2024

- Mexico Business News — L’Oréal USD 80 million Mexico production investment across San Luis Potosí and Mexico City plants

- Cincinnati Business Journal — P&G USD 450 million Mason campus expansion for manufacturing capacity, 2025

- Unilever — £80 million UK fragrance facility investment at Port Sunlight supporting TRESemmé and hair care innovation, 2025

- Procter & Gamble Annual Report 2025 — Operating cash flow and reinvestment capacity for hair care innovation, FY2025

- Dyson — Expansion into consumable hair care products building on Airwrap patented technologies, late 2025