Report Overview

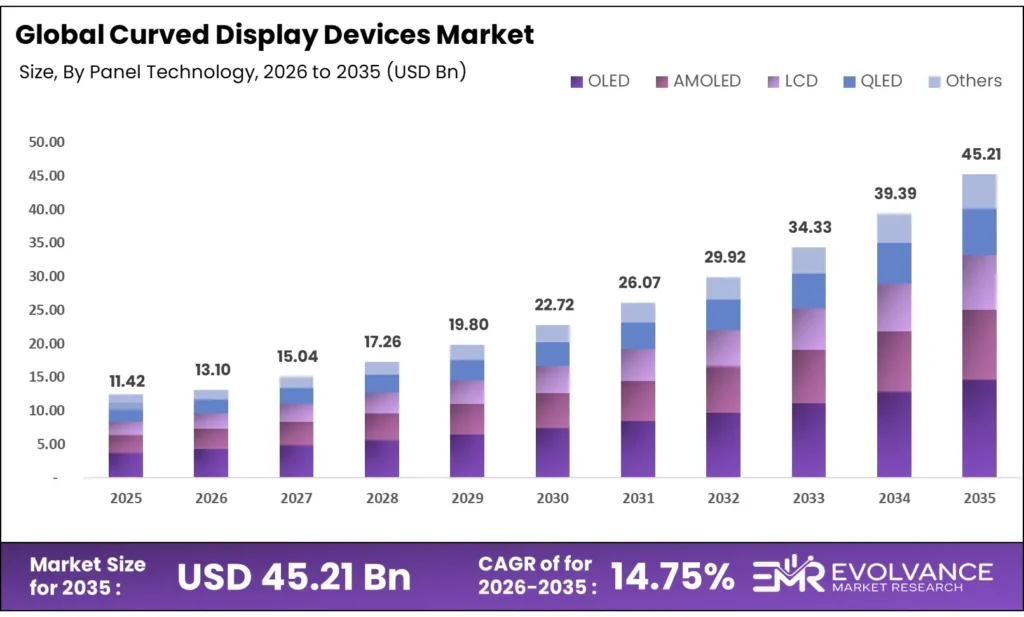

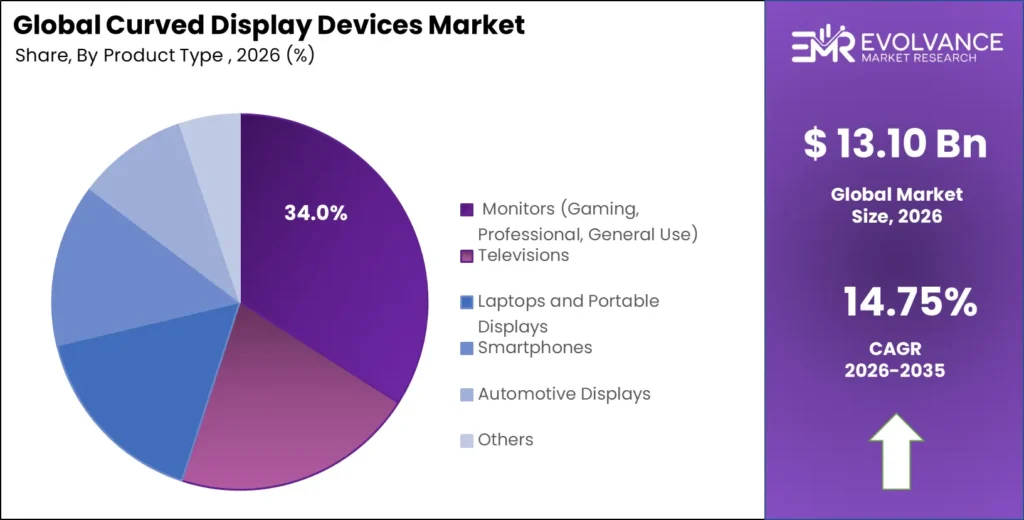

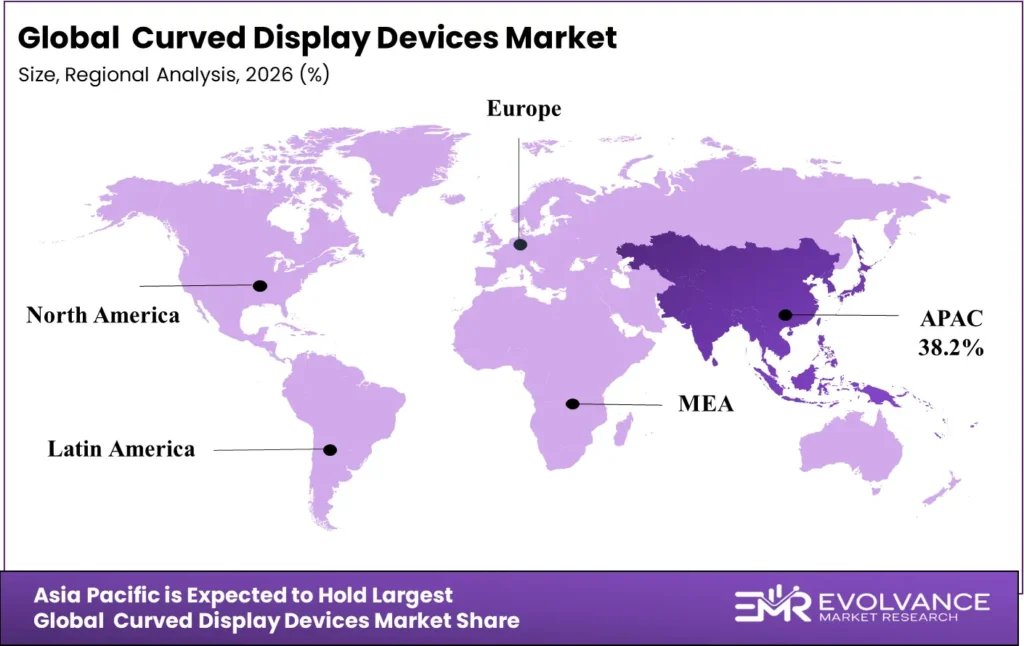

The global Curved Display Devices Market was valued at USD 11.42 billion in 2025 and is projected to reach USD 45.21 billion by 2035, growing at a CAGR of 14.75%. Asia Pacific leads with a 38.2% revenue share, while North America is the fastest-growing premium segment. The OLED panel segment dominates with 44.5% market share, and monitors hold 47.6% of total product revenue.

Gaming and consumer electronics together account for over 58% of total application demand. Key growth drivers include rising immersive gaming and entertainment demand, rapid OLED and AMOLED technology adoption, automotive cockpit display integration, growing work-from-home monitor upgrades, and expanding commercial digital signage installations worldwide.

The Curved Display Devices Market is witnessing growth driven by advancements in flexible display technologies and increasing demand for immersive user experiences. Applications across consumer electronics and gaming are fueling adoption. This trend is interconnected with the Digital Comics, where enhanced visual experiences drive engagement, and the Content Creator Economy, where high-quality display technologies support content production. Additionally, integration with simulation technologies from the Digital Twin for Telecom Network Simulation is enabling improved design and performance testing.

What Is the Curved Display Devices Market Size?

The global Curved Display Devices Market was valued at approximately USD 11.42 billion in 2025 and is projected to grow from USD 13.10 billion in 2026 to nearly USD 45.21 billion by 2035, registering a compound annual growth rate (CAGR) of around 14.75% during 2026–2035. The year 2026 represents a strategic acceleration phase as consumer demand shifts toward ultra-wide and super-ultrawide curved monitors, OLED panel proliferation intensifies across consumer and commercial applications, and automotive OEMs integrate curved cockpit displays as standard features.

Curved display technology delivers superior immersive experiences, wider field-of-view coverage, reduced eye strain during extended use, and enhanced depth perception compared to flat-panel alternatives. Market expansion is supported by rising consumer electronics spending, gaming industry growth, commercial digital signage adoption, automotive infotainment innovation, and increasing healthcare visualization requirements across global markets.

Market Highlights

- Asia Pacific dominated the market, holding the largest share of 38.2% in 2025.

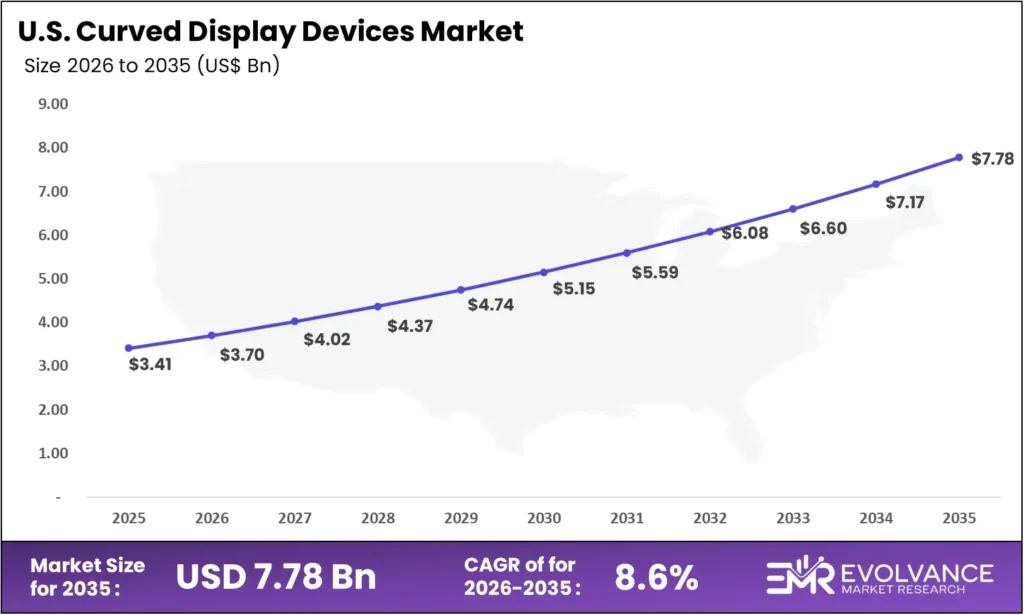

- North America is expected to expand at the fastest premium CAGR of 8.6% during 2026–2035.

- By panel technology, the OLED segment accounted for the biggest market share of 44.5% in 2025.

- By panel technology, the AMOLED segment is expected to grow at the fastest CAGR of 9.8% during 2026–2035.

- By product type, the monitors segment contributed the highest market share of 47.6% in 2025.

- By product type, the automotive displays segment is expected to expand at the fastest CAGR of 11.2% during 2026–2035.

- By application, the consumer electronics segment captured the highest market share of 41.3% in 2025.

- By application, the gaming segment is expected to expand at the fastest CAGR of 10.5% during 2026–2035.

- By end-user, the residential segment held the major market share of 52.4% in 2025.

- By end-user, the commercial segment is expected to expand at the fastest CAGR of 8.9% during 2026–2035.

U.S. Curved Display Devices Market Size and Growth 2026 to 2035

The U.S. Curved Display Devices Market size is estimated at USD 3.41 billion in 2025 and is projected to reach approximately USD 3.70 billion in 2026, reflecting strong consumer demand for immersive monitor and television upgrades. The market is expected to grow at a strong CAGR of 8.6% from 2026 to 2035, driven by robust demand for ultra-wide gaming monitors, premium home theater curved TVs, and professional-grade workstation displays. Increasing remote and hybrid work adoption has accelerated multi-monitor setups incorporating curved screens for expanded productivity.

Organizations and consumers in the United States are investing in curved OLED and VA panel displays across gaming, creative professional, and home entertainment applications to enhance immersion, improve decision-making environments, and gain productivity advantages. Growing investments in gaming infrastructure, commercial digital signage, and automotive display integration further support long-term market growth.

What Are Curved Display Devices?

Curved display devices are screens manufactured with a concave curvature along the horizontal axis, designed to wrap partially around the viewer’s field of vision to create a more immersive, cinema-like viewing experience. Unlike flat-panel displays, curved screens use precise radius of curvature measurements — typically expressed in millimeters (e.g., 1800R, 3000R, 4000R) — to determine the degree of bend and optimize the viewing distance for each application.

By leveraging advanced panel technologies including OLED, AMOLED, quantum dot LCD, and VA matrix displays, curved screens deliver superior color uniformity at peripheral viewing angles, reduced image distortion at screen edges, enhanced depth perception, and minimized ambient light reflection compared to flat alternatives.

Applications span consumer electronics including monitors, televisions, laptops, and smartphones; automotive cockpit and infotainment displays; healthcare diagnostic imaging; commercial digital signage; and professional visualization environments across broadcast, design, and financial services industries.

Curved Display Devices Market Outlook

- Rising Demand for Immersive Consumer Experiences: Growing demand for immersive gaming and entertainment is driving curved display adoption. With over 3.3 billion gamers globally, consumers prefer curved ultra-wide monitors and TVs for wider viewing angles, smoother visuals, and enhanced cinematic experiences.

- Automotive Display Integration and Cockpit Transformation: Automakers are integrating curved panoramic displays across vehicle dashboards to combine instrument clusters, infotainment, and driver assistance interfaces. Rising EV production and premium in-car experiences are accelerating curved display adoption beyond luxury vehicles into mainstream automotive models.

- OLED and AMOLED Technology Proliferation: Advancements in OLED and AMOLED technologies enable thinner, flexible panels with superior contrast and color accuracy, making them ideal for curved displays. Falling production costs and investments from major manufacturers are expanding curved display usage across smartphones, laptops, and automotive systems.

- Commercial Digital Signage and Enterprise Adoption: Curved displays are gaining traction in retail, broadcasting studios, control rooms, and healthcare imaging due to better viewing angles and visual impact. Businesses use curved digital signage and video walls to attract attention and improve data visualization in professional environments.

Key Market Trends

- Ultra-Wide and Super-Ultrawide Monitor Expansion: Increasing adoption of 21:9 and 32:9 curved monitors among gamers and professionals is replacing multi-monitor setups by providing wider workspace, seamless viewing, and improved productivity with reduced screen distortion.

- Mini-LED Backlit Curved LCD Innovation: Mini-LED backlighting combined with curved LCD panels improves contrast, HDR performance, and local dimming precision, offering OLED-like visual quality at lower prices across mid-range monitors and televisions.

- Rollable and Flexible OLED Development: Advances in flexible and rollable OLED displays allow adjustable screen curvature based on usage, enabling flat viewing for work tasks and deeper curvature for gaming or immersive entertainment.

- Gaming Monitor Premium Segment Growth: Manufacturers are launching high-refresh-rate curved gaming monitors featuring adaptive sync technologies and refresh rates above 240Hz, targeting esports players and gamers seeking premium immersive display performance.

- Automotive Panoramic Cockpit Display Systems: Automotive companies are developing panoramic curved dashboard displays integrating instrument clusters and infotainment systems into seamless panels, improving driver information visibility and enhancing modern vehicle interior aesthetics.

- Sustainable Display Manufacturing Initiatives: Display manufacturers are focusing on eco-friendly production by reducing energy consumption, removing hazardous materials, improving recyclability, and designing longer-lasting panels to support sustainability and circular economy goals.

Market Scope

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | USD 11.42 Billion |

| Market Size in 2026 | USD 13.10 Billion |

| Forecasted Market Size by 2035 | USD 45.21 Billion |

| Market Growth Rate (2026–2035) | CAGR of 14.75% |

| Base Year | 2025 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Largest Market | Asia Pacific |

| Fastest Growing Market | North America (Premium Segment) |

| Segments Covered | Product Type, Panel Technology, Application, End-User, Region |

| Regional Coverage | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Panel Technology Insights

The OLED segment dominated the Curved Display Devices Market with the largest share of 44.5% in 2025, driven by its superior contrast performance, ultra-thin panel profiles, wide color gamut, and inherently flexible substrate characteristics that enable precise curvature manufacturing without backlight uniformity compromises.

OLED panels deliver true black reproduction, instant pixel response times below 0.1ms, and vibrant color saturation across the full visible spectrum, making them the preferred choice for premium curved monitors, luxury televisions, and flagship smartphones. The elimination of backlighting requirements enables OLED panels to achieve thinner, lighter display profiles ideal for curved form factor applications.

The AMOLED segment is expected to grow at the fastest CAGR of 9.8% during 2026–2035. AMOLED technology combines active matrix TFT backplane control with OLED emissive layers to deliver faster pixel switching, superior brightness levels, and enhanced power efficiency. Growing AMOLED adoption across mid-range smartphones, automotive applications, wearables, and foldable devices is driving manufacturing scale-up at major panel producers, progressively reducing costs and enabling curved AMOLED integration across broader product categories beyond premium segments.

Product Type Insights

The monitors segment contributed the highest market share of 47.6% in 2025, establishing itself as the dominant curved display product category driven by explosive growth in gaming monitors, work-from-home productivity upgrades, and professional workstation deployments. Ultra-wide curved monitors ranging from 27 to 49 inches with resolutions spanning Full HD to 5K provide expansive digital canvas areas for content creators, financial analysts, and software developers.

The convergence of high refresh rates, HDR support, wide color gamut coverage, and competitive pricing has made curved monitors the preferred choice for enthusiast consumers and enterprise buyers seeking premium display experiences without the space requirements of multi-monitor configurations.

The automotive displays segment is expected to expand at the fastest CAGR of 11.2% during 2026–2035, driven by accelerating integration of curved panoramic cockpit display systems across premium and mid-range vehicle platforms. Curved television displays represent a significant revenue segment supported by consumer demand for immersive home theater experiences, with 55-inch to 85-inch curved 4K and 8K TVs attracting premium household spending. Curved smartphone displays maintain strong demand in flagship models where edge-to-edge curved glass aesthetics command premium retail pricing, while curved laptop displays are gaining traction among gaming laptop and professional portable workstation segments.

Application Insights

The consumer electronics segment captured the highest market share of 41.3% in 2025, encompassing curved monitors, televisions, smartphones, and laptops purchased for home entertainment, gaming, and personal productivity. Rising disposable incomes in developing markets, increasing display replacement frequency, and premiumization trends sustain robust demand for curved display form factors across residential end-users globally. The gaming segment is expected to expand at the fastest CAGR of 10.5% during 2026–2035, as global esports industry growth, increasing streaming platform viewership, and cloud gaming adoption collectively drive demand for immersive high-performance curved gaming displays.

End-User Insights

The residential segment held the major market share of 52.4% in 2025, driven by consumer investments in home entertainment systems, gaming setups, and home office workstation upgrades incorporating curved monitors and televisions. Post-pandemic hybrid work patterns have permanently elevated household display budgets, with consumers prioritizing ergonomic large-format curved monitors for extended productivity use. The commercial segment is expected to expand at the fastest CAGR of 8.9% during 2026–2035, driven by retail, hospitality, broadcasting, financial services, and healthcare enterprises adopting curved displays for customer engagement, operational visualization, and brand differentiation across physical touchpoints.

Segments Covered in the Report

By Panel Technology

- OLED (Organic LED)

- AMOLED (Active Matrix OLED)

- LCD (VA and IPS)

- Quantum Dot LED (QLED/QD-OLED)

- Others

By Product Type

- Monitors (Gaming, Professional, General Use)

- Televisions

- Laptops and Portable Displays

- Smartphones

- Automotive Displays

- Others

By Application

- Consumer Electronics

- Gaming and Esports

- Automotive and Transportation

- Healthcare and Medical Imaging

- Commercial Digital Signage

- Others

By End-User

- Residential

- Commercial

- Industrial and Institutional

Regional Insights

Asia Pacific — Leading the Market

Asia Pacific dominated the curved display devices market with the largest share of 38.2% in 2025. The region’s leadership is underpinned by the concentration of global display panel manufacturing infrastructure in South Korea, China, Japan, and Taiwan, enabling domestic market access to advanced curved display technologies at competitive price points.

Samsung Electronics and LG Electronics in South Korea drive global curved TV and monitor market standards, while Chinese panel manufacturers BOE Technology, CSOT, and Tianma are rapidly scaling AMOLED and curved LCD production capacity. Growing middle-class consumer spending in China, India, and Southeast Asian nations, combined with a thriving gaming culture and rapidly expanding automotive sector, sustains robust curved display demand across the region.

North America — Fastest Growing Premium Segment

North America is expected to register the fastest premium segment CAGR of 8.6% during 2026–2035, driven by high consumer spending power, mature gaming and esports ecosystems, strong enterprise technology investments, and robust demand for premium home entertainment systems. U.S. consumers demonstrate above-average willingness to invest in premium curved gaming monitors, luxury curved OLED televisions, and ergonomic workstation displays.

The region’s leadership in cloud gaming platform development, content streaming services, and remote work technology adoption further amplifies curved display demand. Commercial applications including financial trading floors, broadcasting studios, command and control centers, and corporate headquarters are driving institutional curved display procurement at scale.

Europe — Significant Market Position

Europe holds a significant position in the curved display devices market, driven by strong consumer electronics spending across Germany, the United Kingdom, France, and the Nordic nations. European consumers show strong preference for premium display technologies with particular emphasis on energy efficiency, environmental compliance, and design aesthetics — attributes well-served by modern curved OLED and QLED display products.

The European automotive industry, home to BMW, Mercedes-Benz, Volkswagen, Audi, and Stellantis, represents a major demand driver for automotive curved display systems as manufacturers accelerate electrification and cockpit technology differentiation. EU sustainability regulations and eco-design directives are influencing curved display product development toward lower power consumption and longer operational lifetimes.

Latin America — Emerging Opportunities

Latin America’s curved display devices market is growing steadily, driven by increasing digital transformation across retail, banking, and consumer electronics sectors. Brazil and Mexico represent the largest markets in the region, with consumers investing in curved monitors and televisions as the middle class expands and e-commerce channels improve product accessibility.

The rapid expansion of gaming communities, growing e-commerce adoption, and new commercial digital signage deployments across retail and transportation infrastructure are compelling manufacturers to strengthen regional distribution and accelerate curved display market penetration.

Middle East & Africa — Growing Demand

The Middle East and Africa region presents expanding opportunities for curved display devices, driven by government-led digital infrastructure investments, rapid smart city development, and rising consumer electronics demand across Gulf Cooperation Council nations. Countries including the UAE, Saudi Arabia, and South Africa lead regional market development, supported by national digitization strategies such as Saudi Vision 2030.

Key sectors including retail, hospitality, gaming, automotive, and government command centers are prioritizing curved display adoption for immersive consumer experiences and operational visualization, with luxury consumer electronics demand among affluent urban populations further sustaining premium segment growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- ASEAN Countries

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of MEA

Curved Display Devices vs. Flat-Panel Displays

Curved display devices deliver a fundamentally different visual experience from conventional flat-panel screens by wrapping the image around the viewer’s natural field of vision, reducing geometric distortion at screen peripheries, minimizing ambient light reflections, and creating enhanced depth perception that increases immersion for entertainment, gaming, and creative content applications.

Flat-panel displays, on the other hand, present a linear, uniform image plane optimized for multi-viewer environments, wall-mounted commercial applications, and shared workspaces where a single optimal viewing position is not guaranteed. While flat displays offer simplicity in mounting, wider viewing angles for group viewing, and lower entry-level pricing, they cannot replicate the peripheral immersion and ergonomic depth cues delivered by well-engineered curved panel designs.

| Feature | Curved Display Devices | Flat-Panel Displays |

|---|---|---|

| Immersion Level | Superior – wider FOV coverage | Standard – linear visual plane |

| Eye Strain | Reduced in extended use sessions | Higher in wide-format use |

| Optimal Viewing | Single-viewer optimized | Multi-viewer optimized |

| Peripheral Distortion | Minimal at matched viewing distance | Noticeable at screen edges |

| Wall Mounting | Requires curved wall or standoff mounts | Standard flat-wall mounting |

| Price Premium | 10–40% above flat equivalents | Baseline pricing tier |

| Best Use Cases | Gaming, cinema, workstations, automotive | Office, retail signage, multi-viewer |

| Form Factor | Fixed or variable curvature radius | Rigid flat substrate |

| OLED Compatibility | Naturally compatible with flexible OLED | Compatible with rigid OLED/LCD |

Market Value Chain Analysis

- Raw Materials and Substrate Suppliers: Glass substrate manufacturers, chemical precursor suppliers for OLED organic compounds, rare earth element providers for phosphors and quantum dot materials, and flexible polymer substrate producers forming the foundational input layer for curved display panel manufacturing across OLED, AMOLED, and LCD technology platforms.

- Panel Technology Developers and Manufacturers: Display panel producers including Samsung Display, LG Display, BOE Technology, CSOT, and Japan Display design and manufacture curved OLED, AMOLED, and LCD panels incorporating precise curvature engineering, advanced backplane architectures, and proprietary pixel arrangement technologies that define the core visual performance characteristics of finished curved display products.

- Display Component Suppliers: Semiconductor manufacturers providing display driver ICs, timing controllers, and image processing chips; backlighting system producers for Mini-LED and QLED curved LCD panels; touch sensor and digitizer manufacturers; and optical film and polarizer suppliers that complete the component ecosystem enabling high-performance curved display assembly.

- System Integrators and OEM Manufacturers: Consumer electronics brands, automotive display system integrators, commercial display solution providers, and industrial display manufacturers assembling curved panel components with mechanical enclosures, mounting systems, connectivity interfaces, and firmware to create finished curved display products for consumer, enterprise, and automotive end-markets.

Top Curved Display Devices Market Companies

Samsung Electronics

Samsung Electronics leads the curved display market with Odyssey gaming monitors, QLED/Neo QLED TVs, and Galaxy curved-edge smartphones. Strong vertical integration in display manufacturing enables cost advantages while supplying curved panels for automotive, commercial, and global consumer electronics markets.

LG Electronics

LG Electronics is a major player in curved OLED displays with UltraWide monitors, OLED Evo TVs, and flexible panels for automotive systems. Its UltraGear gaming monitors target professionals and gamers needing high refresh rates and color accuracy.

Dell Technologies

Dell Technologies focuses on enterprise and professional curved monitors through the UltraSharp series for designers and analysts requiring color precision. Its Alienware curved gaming monitors deliver high refresh rates, HDR performance, and adaptive sync technologies.

Acer

Acer Inc. offers curved displays through Predator and Nitro gaming monitor lines along with affordable productivity models. Its portfolio ranges from 24–49 inches, targeting gamers, home offices, education, and commercial digital signage markets.

Other key players include ASUS (ROG and ProArt curved displays), AOC, MSI, ViewSonic, Philips (MMD), HP, BenQ, Huawei, TCL, Hisense, Panasonic, Continental (automotive displays), Bosch, Visteon, Innolux, and AU Optronics.

Recent Developments

- February 2026 — Samsung Display announced mass production of 500R ultra-tight curvature OLED panels targeting the next generation of immersive gaming monitor applications, enabling new form factor designs previously impractical with conventional glass substrate manufacturing.

- January 2026 — LG Electronics unveiled its 2026 OLED Evo curved television lineup featuring enhanced brightness processing and a new anti-reflection surface coating delivering superior ambient light rejection for curved TV installations in bright living room environments.

- December 2025 — Multiple automotive OEMs announced adoption of 48-inch curved panoramic cockpit displays integrating instrument cluster, infotainment, passenger screen, and ambient lighting control into unified curved glass assemblies for 2026–2027 model year vehicles.

- October 2025 — BOE Technology commenced large-scale production of cost-optimized AMOLED curved panels targeting mid-range smartphone manufacturers in China, India, and Southeast Asia, accelerating AMOLED curved display democratization beyond flagship device tiers.

Future Outlook 2030–2035

Between 2030 and 2035, curved display devices are expected to evolve beyond fixed-curvature panels toward dynamically adjustable and rollable display architectures. As OLED and Micro-LED manufacturing matures, curved display technology will permeate mid-market consumer electronics price segments while simultaneously advancing into next-generation applications including transparent curved automotive windshield displays, wearable near-eye curved panels, and architectural curved display installations.

The convergence of curved display technology with spatial computing, extended reality hardware, and AI-driven adaptive display optimization will redefine immersive visual experiences across consumer, enterprise, and mobility applications, supporting the projected expansion to USD 28.96 billion by 2035.