What is Content Creator Economy Market Size?

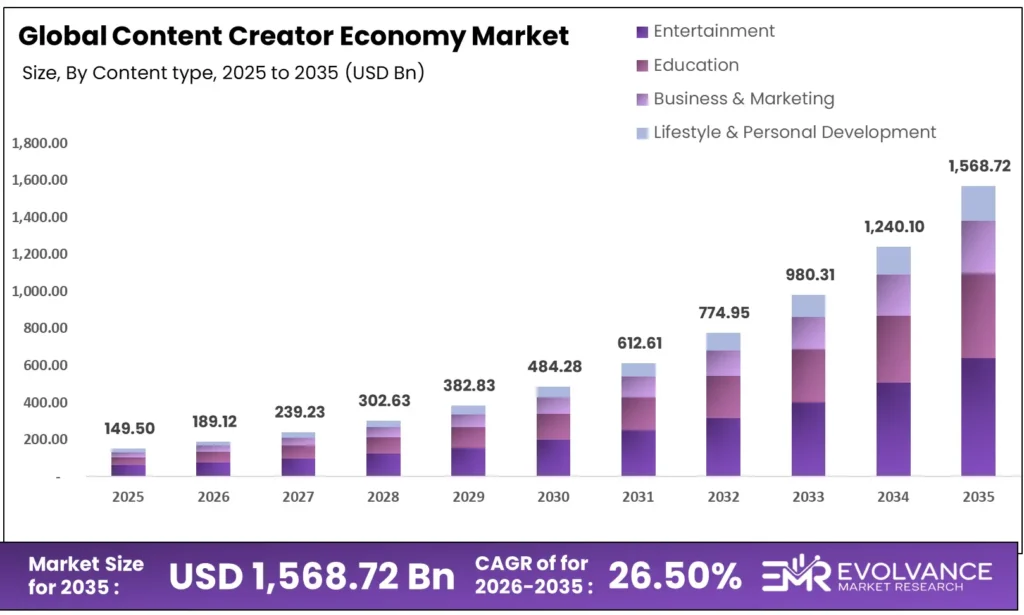

The Global Content Creator Economy market size is estimated at USD 149.50 billion in 2025 and is projected to grow from USD 189.12 billion in 2026 to approximately USD 1,568.72 billion by 2035, expanding at a CAGR of 26.50% during the forecast period from 2025 to 2034. The content creator economy has emerged as a high-growth digital ecosystem, encompassing influencers, streamers, educators, digital entrepreneurs, and independent creators, alongside the platforms and tools that enable audience development and revenue monetization.

The Content Creator Economy Market is witnessing rapid expansion driven by the rise of digital platforms, influencer monetization, and direct-to-consumer engagement models. Demand for specialized niches continues to grow, enabling diversified revenue streams. This market is strongly interconnected with the Creator Economy, as well as emerging technologies in the AI Podcast Creation Platforms and Digital Comics, which empower creators with new content formats. Furthermore, AI-driven tools from the Agentic AI for Customer Support Automation are enhancing audience engagement and automation capabilities.

Market Highlights

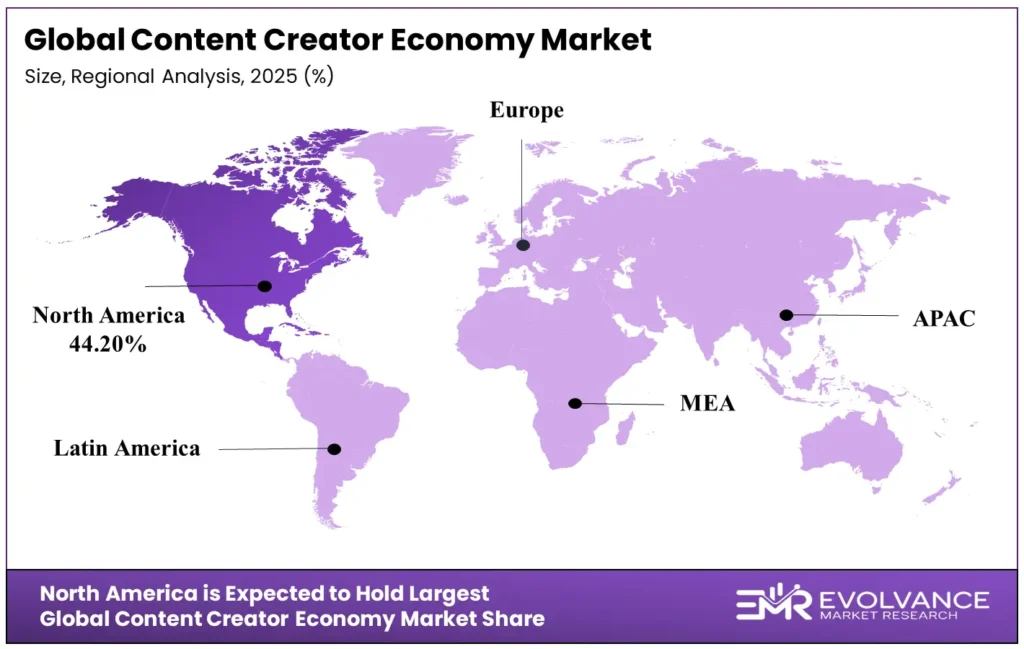

- By region, North America dominated the market, holding largest share of 44.20% in the market during 2025.

- By region, Asia Pacific is expected to expand at the fastest CAGR of 23.70% between 2026 and 2035.

- By Content Type, the Entertainment Content segment contributed the market share of 52.24% in 2025.

- By Platform Type, video-based platforms segment held the major market share of 48.80% in 2025.

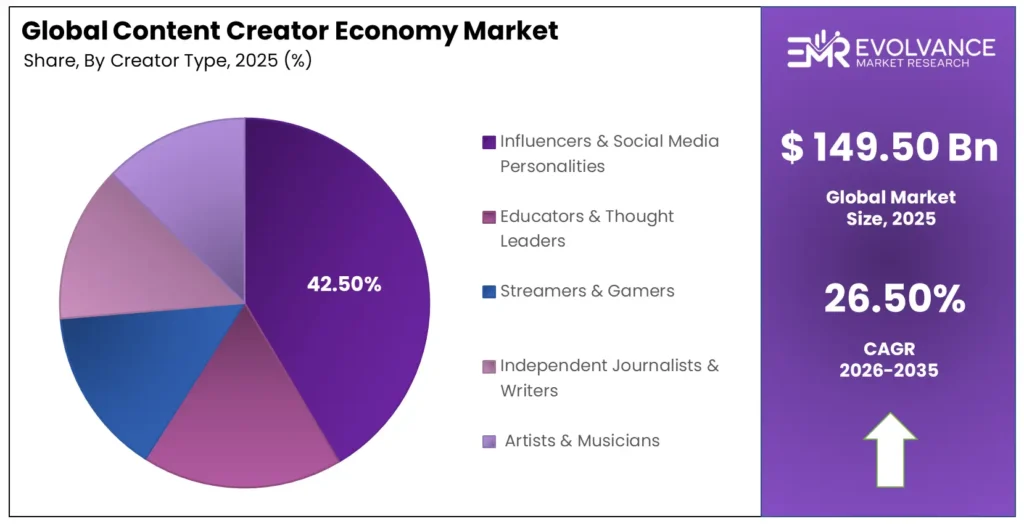

- By Creator Type, the Influencers and Social Media Personalities segment captured the highest market share of 42.80% in 2025.

U.S. Content Creator Economy Market Size and Growth 2026 to 2035

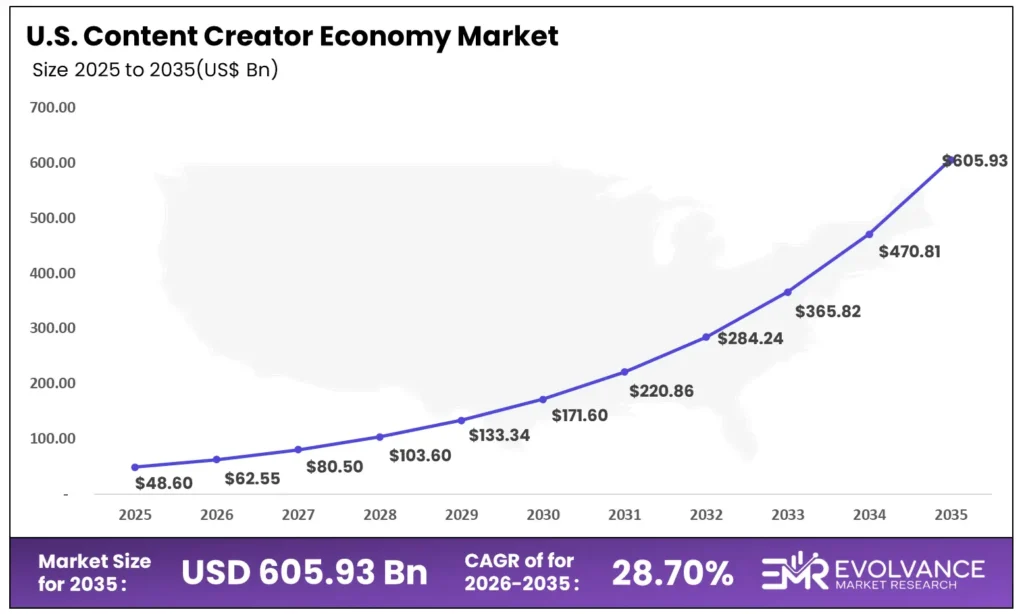

The U.S. content creator economy continues its rapid expansion, with the market size estimated at USD 62.55 billion in 2026 and projected to reach approximately USD 605.93 billion by 2035, reflecting a strong compound annual growth rate (CAGR) of 28.70% from 2026 to 2035. This growth is anchored in deep social media penetration, where more than 78% of the U.S. population regularly engages with creator-driven content across video, audio, and written formats.

Brands are increasingly shifting marketing spend to creator collaborations, with an estimated 30–40% of digital budgets now allocated to influencer and creator partnerships due to higher engagement and measurable ROI. The widespread adoption of AI-powered tools for content creation, real-time analytics, and automated editing has boosted creator productivity and earnings potential.

Demand for specialized niches — especially in education, gaming, finance, wellness, and lifestyle — continues to grow, fueling diversified revenue streams. Additionally, robust digital payment systems and subscription-based monetization models are strengthening creator income stability, positioning the U.S. market as a global leader in creator economy growth over the next decade

Market Size and Forecast

- Market Size in 2025: USD 149.50 Billion

- Market Size in 2026: USD 189.12 Billion

- Forecasted Market Size by 2035: USD 1,568.72 Billion

- CAGR (2026-2035): 26.50%

- Largest Market in 2025: North America

- Fastest Growing Market: Asia Pacific

What Is the Content Creator Economy?

The content creator economy is a rapidly expanding digital ecosystem where individuals build personal brands and earn directly from audiences. Over 50 million people identify as creators, with nearly 2–3 million earning full-time income. Unlike traditional media, where 80% of revenue was controlled by corporations, digital platforms empower independent voices. Platforms like YouTube, Instagram, and TikTok drive over 70% of creator content consumption, while short-form video contributes nearly 40% of engagement time.

Advertising generates 30–35% of income, brand partnerships 25–30%, subscriptions and digital products 20–25%, and affiliate sales 10–15%. Creators with multiple revenue streams earn 2.5x more. Around 65–70% of consumers trust creators more than traditional ads, delivering 3–4x higher engagement. Spending on creator-focused tools is growing at 25%+ annually, reshaping global media and commerce.

Content Type Insights

Why Entertainment Content segment Is Dominating the Content Creator Economy Market?

In 2025, the Entertainment Content segment led the global content creator economy, capturing over 52.24% of total market share, driven by strong audience demand, platform investments, and preference for visually engaging formats. Streaming platforms such as Netflix, Amazon Prime Video, and Disney+ continue expanding original entertainment libraries to retain subscribers. For instance, Netflix launched over 150 original shows in 2024, while in 2025 TikTok further strengthened its creator funding programs to support short-form entertainment creators globally.

Consumer behavior reinforces this dominance, with rising consumption of comedy clips, music videos, gaming streams, and short-form videos. Platforms like YouTube Shorts, Instagram Reels, TikTok, and Twitch consistently record higher engagement for entertainment categories. Notably, YouTube Shorts accounted for over 15% of total watch time in 2024, and engagement momentum continued rising in 2025.

Advancements in AI-based editing, cloud production tools, and affordable high-resolution devices further empower independent creators, making entertainment content scalable, monetizable, and central to sustained creator economy growth.

Platform Insights

Why the Video-Based Platforms segment Is Dominating the Content Creator Economy Market?

In 2025, the video-based platforms segment maintained a leading position in the global content creator economy, accounting for over 48.80% of total market share. This dominance is driven by technological innovation, evolving consumer behavior, and sustained platform investments prioritizing video-centric consumption. Growing preference for video as a primary format, supported by widespread smartphone usage and high-speed internet access, has embedded on-demand and short-form video into daily digital habits.

Leading platforms such as YouTube, TikTok, and Instagram continue strengthening their ecosystems through algorithm-driven recommendations, short-form formats, live streaming, and interactive engagement tools that expand creator reach and user interaction. For instance, in 2024, YouTube expanded its Shorts monetization program, offering higher revenue shares for high-performing videos, and TikTok increased creator payouts for trending content, attracting more video creators globally.

Simultaneously, investments in original and exclusive video content intensify competition for viewer attention, improving retention and monetization via advertising, subscriptions, and brand partnerships. Advances in AI-assisted editing, mobile-first production tools, and user-friendly software further lower entry barriers, reinforcing sustained leadership.

Creator Type Insights

Why Influencers & Social Media Personalities segment Is Dominating the Creator Economy Market?

The Influencers and Social Media Personalities segment remains the leading force in the global creator economy, accounting for approximately 42.50% of total market share in 2025. This dominance stems from expansive audience reach, strong engagement rates, and efficient monetization models supported by growing brand reliance on influencer-led campaigns.

Influencers build authenticity and trust, delivering seamless content integration and driving 8–11x higher ROI than traditional digital advertising. Platforms including Instagram, TikTok, YouTube, and X (formerly Twitter) continue enhancing monetization through ad revenue sharing, subscriptions, live gifting, and affiliate tools. In 2024, Instagram expanded its creator marketplace globally, and in 2025 introduced enhanced AI-powered brand matching tools, while TikTok further increased payouts under its Creativity Program.

Influencer marketing adoption is accelerating, with over 70% of global brands increasing spend in 2024, a trend continuing into 2025. Growth of micro and nano influencers, combined with advanced analytics optimization, ensures sustained leadership and scalable expansion.

Segments Covered in the Report

By Content Type

- Entertainment Content

- Educational Content

- Business & Marketing Content

- Lifestyle & Personal Development

- Others

By Platform

- Video-Based Platforms

- Subscription & Direct Support Platforms

- Text & Blogging Platforms

- Audio & Podcasting Platforms

- Social Media & Micro-Content Platforms

- Creator Tools & NFT Marketplaces

- Others

By Creator Type

- Influencers & Social Media Personalities

- Educators & Thought Leaders

- Streamers & Gamers

- Independent Journalists & Writers

- Artists & Musicians

- Others

Regional Insights

Why Is North America Leading the Content Creator Economy Market?

North America leads the global content creator economy due to advanced digital infrastructure, strong platform presence, and early adoption of monetization models. In 2025, the region accounted for over 44.20% of global market share, making it the largest contributor worldwide.

A major driver is high social media penetration, with more than 85% of the population in the U.S. and Canada actively using digital platforms. The region hosts major platforms including YouTube, Instagram (Meta), TikTok, Twitch, Patreon, and Substack, which continuously expand creator tools and revenue-sharing programs.

North America also represents nearly 45% of global influencer marketing expenditure, reflecting strong brand investment in creator-led campaigns. Influencer-driven campaigns generate 8–10x higher engagement than traditional digital ads. Strong e-commerce integration, high consumer purchasing power, advanced analytics tools, and widespread high-speed internet further strengthen monetization opportunities, positioning North America as the most mature and revenue-driven creator economy market.

Canadian Model in the Content Creator Economy Market

Canada holds a strategic position in the global content creator economy, supported by strong digital infrastructure, high internet penetration, and a growing creator workforce. In 2025, it accounted for approximately 44.20% of the North American creator economy. Over 90% of Canadian internet users actively engage with social media, providing a robust audience for creators.

Government-backed digital innovation programs and favorable policies for small digital businesses support creator growth. Canadian creators benefit from proximity to U.S. platforms while reaching global audiences. Professional content creators are growing at over 20% annually, especially in video, gaming, and education. Strong brand participation, bilingual content, and cross-border collaborations reinforce Canada as a scalable, stable contributor to the global creator economy.

Why Is the Asia Pacific Leading the Charge in the Content Creator Economy Market?

The Asia Pacific (APAC) region is emerging as a major driver of the global content creator economy, capturing approximately 23.70% of the global market share in 2025. Rapid smartphone adoption, expanding internet penetration, and a young, digitally savvy population are fueling growth. Over 70% of internet users in APAC actively engage with social media and content-sharing platforms, creating a large audience for creators.

Platforms like TikTok, Kuaishou, Bilibili, YouTube, and Instagram drive this growth through monetization tools, live-streaming features, and creator funds. Short-form video, gaming, and live commerce account for over 40% of regional content consumption. Brand collaborations and e-commerce integration are expanding rapidly, with influencer marketing expenditure in APAC rising 25–28% year-over-year.

High engagement, accessible technology, and strong monetization opportunities position APAC as a global hub for content creation, innovation, and sustainable creator-driven growth.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- ASEAN Countries

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of MEA

Content Creator Economy Market Outlook

- Industry Growth Overview: The content creator economy shows strong sustained growth driven by internet penetration, smartphone adoption, and rising digital consumption. Brands shift budgets to creator-led marketing for higher engagement. Short-form video, live streaming, AI editing tools, and analytics lower barriers and accelerate global expansion.

- Sustainability Trends: Sustainability focuses on long-term income stability beyond short-term virality. Creators diversify through subscriptions, memberships, digital products, and communities to reduce algorithm dependence. Platforms introduce transparent revenue-sharing and protection policies, while automation, analytics, and niche engagement strategies support creator longevity and balanced growth.

- Major Investors: Major investors including Google, Meta, Amazon, and Microsoft fund creator platforms, analytics tools, and monetization ecosystems. Venture capital and private equity accelerate innovation in AI-powered tools, Web3 ownership models, and creator funds, strengthening infrastructure and expanding scalable global opportunities.

- Startup Economy: The startup economy is expanding through creator-centric tools like AI editing, audience analytics, fintech payments, influencer marketplaces, and community platforms. Entrepreneurs leverage low entry barriers and scalable infrastructure, differentiating via personalization, transparency, and creator-friendly revenue models to drive innovation and employment.

Key Market Trends

- Expansion of 5G-enabled live and low-latency formats that increase high-quality livestream commerce and interactive shows.

- Rapid adoption of AI-assisted content tooling (script assistants, video editing, audio clean-up) that compress production time and raise output quality.

- Creator commerce maturation — embedded storefronts, direct drops, and white-label merch + fulfilment reduce friction from content → purchase.

- Subscription & community monetization replaces one-off creator income with predictable recurring revenue (tiered memberships, private communities).

- Platform revenue-share & policy evolution — creators negotiate for better splits and transparent policies; alternative models (cooperatives, creator-owned platforms) emerge.

- Regionalization of influencer markets — local creators capture culturally relevant audiences; brands invest regionally rather than only global stars.

- Professionalization & talent infrastructure — specialized agencies, creator accounting, legal support and brand strategy become standard offerings.

- Attention to creator welfare & rights — mental health, contract fairness, and IP ownership create new service opportunities and regulatory scrutiny.

- Live Streaming & Real-Time Engagement – Interactive live streaming, real-time shopping, and community chats are strengthening audience relationships while unlocking new monetization opportunities.

Market Scope

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | US$ 149.50 Billion |

| Market Size in 2026 | US$ 189.12 Billion |

| Market Size by 2035 | US$ 1,568.72 Billion |

| Market Growth Rate from 2025 to 2035 | CAGR of 26.50% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Content Type (Entertainment, Education, Business & Marketing, Lifestyle & Personal Development), By Platform (video-based platforms, Subscription & Direct Support Platforms, Text & Blogging Platforms, Audio & Podcasting Platforms, Social Media & Micro-Content Platforms, Creator Tools & NFT Marketplaces), and By Creator Type (Influencers & Social Media Personalities, Educators & Thought Leaders, Streamers & Gamers, Independent Journalists & Writers, Artists & Musicians) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC Countries, South Africa, North Africa, and Rest of MEA |

Market Value Chain Analysis in Content Creator Economy

- Content Inputs: The creator economy depends on a steady supply of digital assets such as videos, images, podcasts, music, livestreams, and written content. Smartphones, cameras, and user-friendly software make content creation accessible, enabling both amateur and professional creators to generate vast amounts of material, supporting continuous ecosystem growth.

- Technology Infrastructure: The backbone of the market includes AI-powered editing tools, recommendation algorithms, cloud storage, livestreaming platforms, and secure payment gateways. These technologies improve content quality, optimize audience reach, and provide diverse monetization opportunities across advertising, subscriptions, and e-commerce.

- Investor Funding Venture capital, private equity, and corporate investments are rapidly flowing into social media platforms, influencer marketing startups, creator management tools, and SaaS solutions designed for content creators. Funding from both tech giants and startups drives innovation and strengthens market scalability, making the creator economy one of the fastest-growing segments in digital business.

- AI & Automation: Artificial intelligence is transforming creator workflows with automated video editing, transcription, smart captions, predictive analytics, and personalized content recommendations. These innovations enhance productivity, increase viewer engagement, and unlock higher monetization potential, positioning AI as a central growth engine for the global content creator market.

Top Content Creator Economy Market Companies

- YouTube (Google): YouTube is the world’s largest long-form video platform, with over 2.5 billion monthly active users, offering monetization through ads, channel memberships, Super Chats, and Shorts. Advertising contributes 55–60% of creator earnings. YouTube Shorts records over 70 billion daily views, and consistent uploads can drive up to 3× higher subscriber growth annually, making it a top platform for creator income.

- TikTok (ByteDance) – TikTok is a leading short-form video platform with over 1.6 billion active users, offering monetization through Creator Funds, brand collaborations, affiliate links, live gifts, and in-app commerce. Live streaming contributes 25–30% of top creator earnings. 60% of viral videos come from accounts under one year old, and brand content drives 4–5× higher engagement, influencing over 40% of Gen Z purchases.

- Instagram (Meta) – Instagram has over 2 billion monthly active users and supports creators via Reels bonuses, branded content, subscriptions, affiliate marketing, and in-app shopping. Reels account for nearly 50% of total time spent, while influencer marketing drives 35–40% of global campaigns. Instagram Shopping boosts conversion rates up to 30%, and subscription-based creator models grow 20%+ annually.

- Patreon – Patreon is a subscription-based creator platform hosting over 250,000 active creators and more than 8 million paying members. Subscription revenue accounts for nearly 90% of creator earnings, with creators earning 2–4× more stable income than on ad-based platforms. Over 70% of creators rely on Patreon as a primary or secondary income source.

Top Key Players in the Market

- ByteDance Ltd. (TikTok)

- Twitch Interactive, Inc.

- Meta Platforms, Inc. (Facebook, Instagram)

- Patreon, Inc.

- Publisherr, Inc. (Buy Me a Coffee)

- Fenix International Ltd. (OnlyFans)

- Spotify Technology S.A.

- Apple Inc.

- Substack, Inc.

- Pinterest, Inc.

- Google LLC (YouTube)

- Snap Inc. (Snapchat)

- LinkedIn Corporation (Microsoft Corporation)

- Adobe Inc.

- SoundCloud Global Limited & Co. KG

- Shopify Inc.

- Discord Inc.

- X Corp. (formerly Twitter)

- Amazon.com, Inc. (Twitch, Prime Video)

- Microsoft Corporation

- Others

Recent Developments

- January 2025 – TikTok expanded its Creator Fund globally, introducing higher payouts for short-form videos with high engagement, encouraging creators to produce more diverse and interactive content.

- June 2025 – YouTube launched AI-assisted Shorts editing tools, enabling creators to generate professional-quality short-form videos faster, reducing production time and increasing monetization efficiency.

- October 2025 – Instagram introduced advanced subscription features, allowing creators to offer exclusive content and personalized interactions, strengthening direct-to-audience revenue streams.

- February 2026 – Twitch rolled out interactive live commerce integrations, allowing streamers to sell merchandise and digital products in real-time, enhancing audience engagement and diversified monetization opportunities.