What is the Security Analytics Market Size?

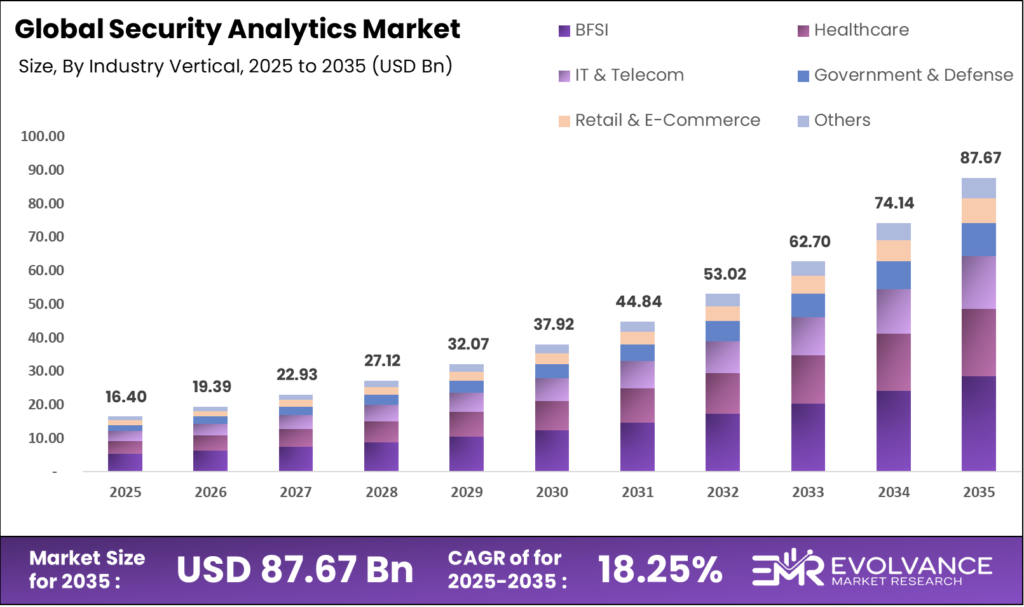

The Global Security Analytics Market was valued at approximately USD 16.40 billion in 2025 and is projected to grow from USD 19.39 billion in 2026 to nearly USD 87.67 billion by 2035, registering a compound annual growth rate (CAGR) of approximately 18.25% from 2026 to 2035. Market expansion is primarily driven by the rising frequency of sophisticated cyberattacks, rapid cloud migration, growing adoption of AI-powered threat detection, and increasing regulatory compliance requirements across BFSI, healthcare, government, and IT sectors worldwide.

The Security Analytics Market is experiencing strong growth as organizations increasingly rely on data-driven approaches to detect and respond to cyber threats. The use of advanced analytics and AI is improving threat intelligence capabilities. This market is closely interconnected with the Internet Security and Quantum-Safe Cybersecurity, ensuring comprehensive protection frameworks. Additionally, its role in supporting secure operations across the Cloud FinOps and Secure Semiconductor Supply Chain is becoming increasingly critical.

Market Highlights

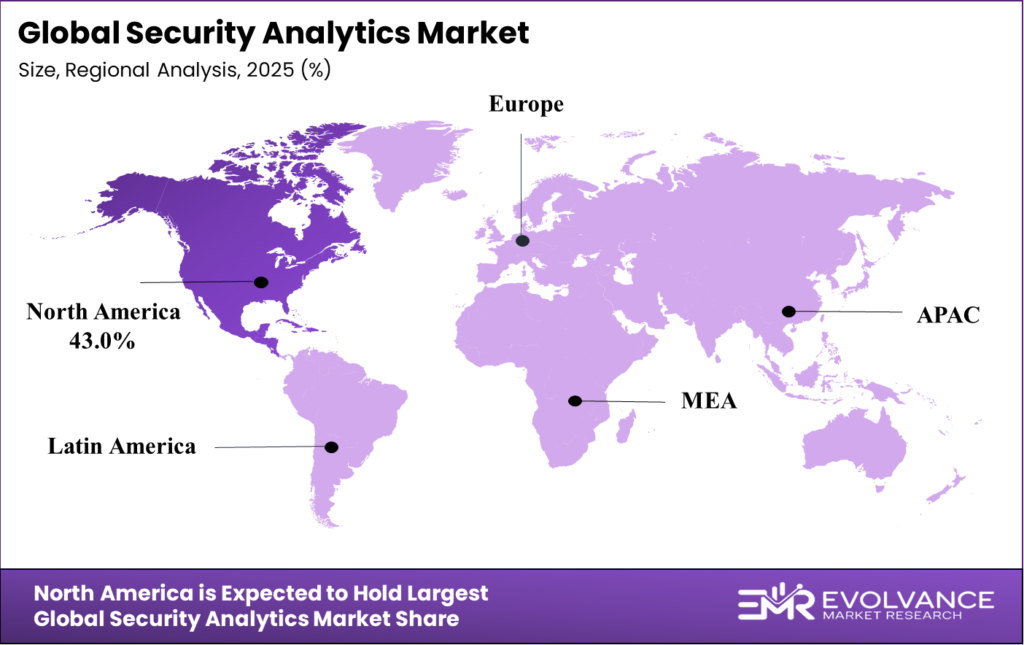

- By region, North America dominated the market, holding the largest share of 43% in the market during 2025.

- By region, Asia Pacific is expected to expand at the fastest CAGR of 19.40% between 2026 and 2035.

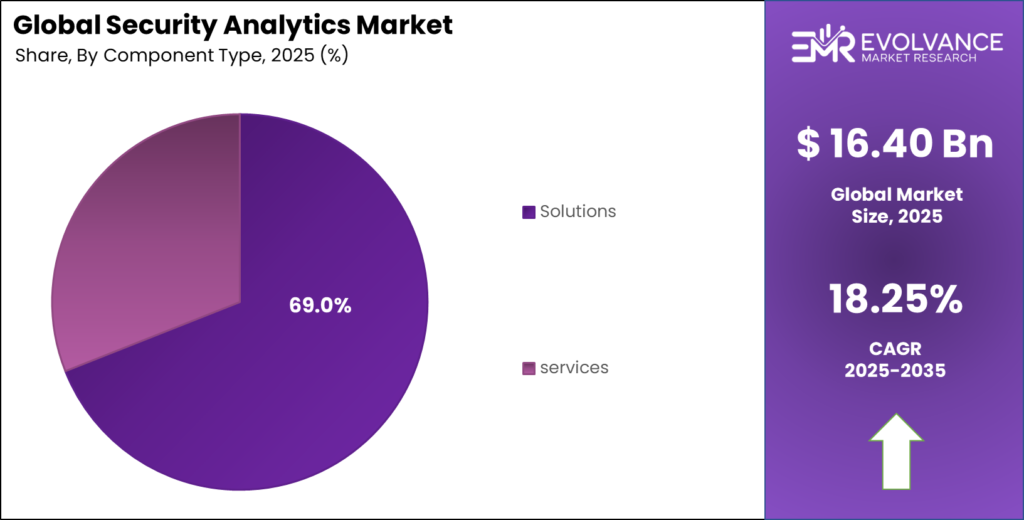

- By Component type, the solutions segment contributed the biggest market share of 69.0% in 2025.

- By Component type, the services segment is expected to grow at a remarkable CAGR of 19% between 2025 and 2035.

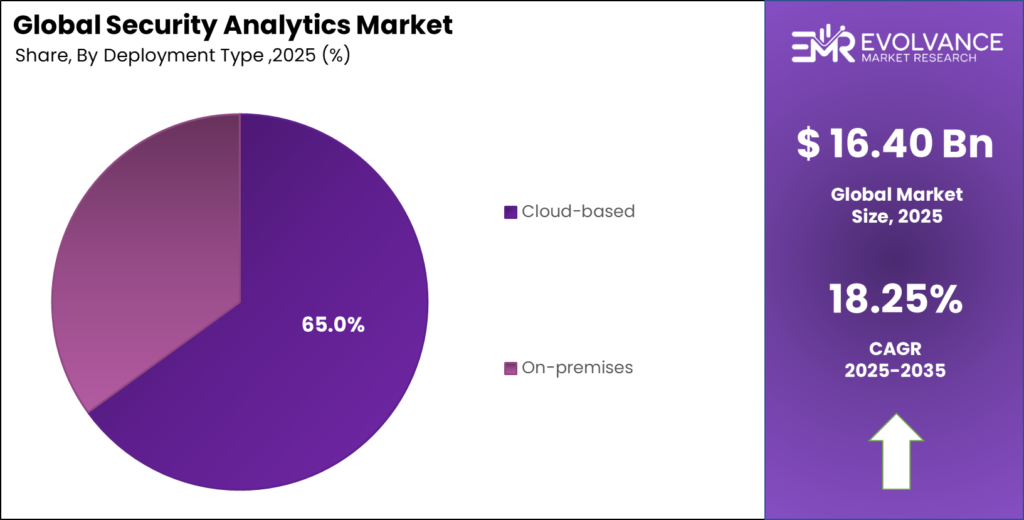

- By Deployment type, cloud-base segment held the major market share of 65.0% in 2025.

- By Deployment type, on-premises is projected to grow at a remarkable CAGR of 15% between 2025 and 2035.

- By Application type, the network security analytics segment captured the highest market share of 37.50% in 2025.

- By Application type, the cloud security segment is growing at a remarkable CAGR of 17% between 2025 and 2035.

- By Industry type, the BFSI segment held the largest market share of 32% in 2025.

- By Industry type, the healthcare segment is expanding at a strong of 19% CAGR between 2025 and 2035.

What Is the Security Analytics?

Security Analytics refers to the systematic process of collecting, monitoring, analyzing, and interpreting security-related data to detect, prevent, and respond to cyber threats in real time. It leverages big data analytics, artificial intelligence (AI), machine learning (ML), behavioral analysis, and threat intelligence to identify vulnerabilities and anomalies. By analyzing network, endpoint, cloud, and user activity data, organizations gain actionable insights, automate incident response, reduce risks, and strengthen overall cybersecurity posture.

U.S. Security Analytics Market Size and Growth 2026 to 2035

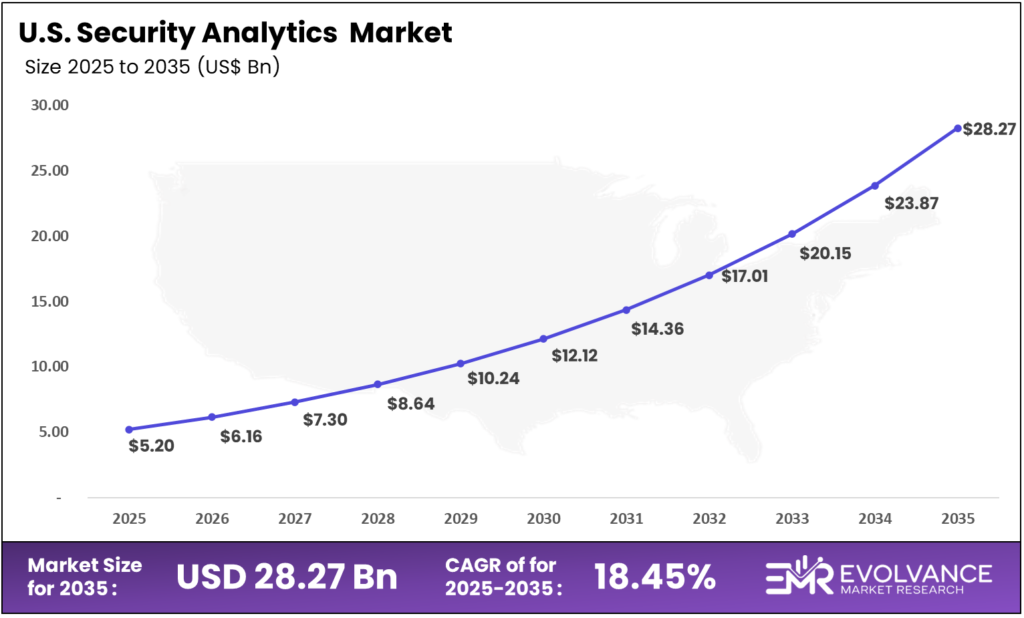

The U.S. Security Analytics Market was valued at approximately USD 5.20 billion in 2025 and is projected to grow from USD 6.16 billion in 2026 to nearly USD 28.27 billion by 2035, registering a CAGR of around 18.45% during 2026–2035. Growth is driven by rising cybersecurity investments across federal agencies, BFSI, healthcare, and large enterprises addressing ransomware and advanced threats. Strong cloud penetration, early zero-trust adoption, and strict compliance mandates support demand. Increasing integration of SIEM, XDR, behavioral analytics, cloud-native platforms, managed security services, AI-driven automation, and critical infrastructure cybersecurity initiatives continues to accelerate market expansion.

Market Size and Forecast

- Market Size in 2025: USD 16.40 Billion

- Market Size in 2026: USD 19.39 Billion

- Forecasted Market Size by 2035: USD 87.67 Billion

- CAGR (2026-2035): 18.25%

- Largest Market in 2025: North America

- Fastest Growing Market: Asia Pacific

Component Type Insight

Why Is the Solutions Segment Dominating the Security Analytics Market?

The Solutions segment is dominating the Security Analytics Market primarily due to its direct role in delivering core threat detection, monitoring, and risk management capabilities. In 2025, the solutions segment accounted for approximately 69% of the total market revenue share, driven by strong enterprise demand for advanced analytics platforms such as SIEM, XDR, UEBA, and AI-powered threat intelligence systems.

Organizations prioritize comprehensive security solutions to address rising ransomware attacks, insider threats, and multi-vector cyber risks. Solutions offer scalable, real-time data processing and centralized visibility across network, endpoint, application, and cloud environments, making them critical for large enterprises and government institutions. Additionally, increasing adoption of cloud-native and AI-integrated analytics platforms has strengthened solution-based deployments over standalone services.

While the solutions segment currently leads in revenue contribution, the services segment is projected to expand at the highest CAGR of approximately 19% during the forecast period (2026–2035). Growth in services is supported by rising demand for managed security services, consulting, integration, and incident response expertise, particularly among small and mid-sized enterprises lacking in-house cybersecurity capabilities.

Deployment Type Insight

Why Is the Cloud-Based Segment Dominating the Security Analytics Market?

The cloud-based segment is dominating the Security Analytics Market due to its scalability, cost efficiency, and ability to deliver real-time threat intelligence across distributed digital environments. In 2025, cloud-based deployments accounted for nearly 65% of the total market revenue, reflecting strong enterprise preference for flexible, subscription-based security models. Organizations are shifting workloads to public and hybrid cloud infrastructures, increasing demand for platforms that monitor multi-cloud environments, remote endpoints, and SaaS applications centrally.

Cloud-based solutions enable faster deployment, automatic updates, and seamless AI-driven detection integration, reducing operational complexity. Remote work expansion and digital transformation initiatives are accelerating cloud security investments across BFSI, healthcare, IT, and e-commerce sectors.

Additionally, cloud platforms support behavioral analytics, automated incident response, and scalable processing without high capital costs. Meanwhile, the on-premises segment is projected to grow at a CAGR of around 15% between 2026 and 2035, driven by regulatory and data sovereignty requirements.

Application Type Insight

Why Is the Network Security Analytics Segment Dominating the Security Analytics Market?

The Network Security Analytics segment is dominating the Security Analytics Market due to its critical role in monitoring and analyzing network traffic to detect malicious activities, data breaches, and unauthorized access attempts. In 2025, the network security analytics segment accounted for approximately 37.50% of the total market revenue, making it the largest application category. Organizations prioritize network-level visibility as it serves as the first line of defense against cyber threats targeting enterprise infrastructure.

The rapid increase in sophisticated ransomware attacks, distributed denial-of-service (DDoS) incidents, and lateral movement within corporate networks has intensified the need for advanced traffic inspection, anomaly detection, and real-time threat intelligence. Enterprises are investing heavily in solutions that provide deep packet inspection, behavioral monitoring, and AI-driven network analytics to identify both external and internal threats.

Furthermore, the expansion of hybrid IT environments and connected devices has increased network complexity, further driving adoption.

While network security analytics leads in revenue contribution, the cloud security analytics segment is expected to expand at the highest CAGR of approximately 17% from 2026 to 2035, supported by growing cloud migration and increased focus on securing cloud-native applications and workloads.

Industry Type Insight

Why Is the BFSI Segment Dominating the Security Analytics Market?

The BFSI (Banking, Financial Services & Insurance) segment is dominating the Security Analytics Market due to high exposure to financial fraud, cyberattacks, and strict regulatory compliance requirements. In 2025, the BFSI segment accounted for approximately 32% of the total market revenue, making it the leading industry vertical. Financial institutions manage large volumes of sensitive customer data, digital transactions, and real-time payment systems, making them prime targets for ransomware, phishing, insider threats, and advanced persistent attacks.

To mitigate risks, BFSI organizations invest in AI-powered fraud detection, behavioral analytics, transaction monitoring, and real-time threat intelligence. Regulatory mandates related to data protection and AML compliance further accelerate adoption.

While BFSI leads in overall revenue share, the healthcare segment is expected to expand at the highest CAGR of approximately 19% from 2026 to 2035, driven by rising cyberattacks on patient data, growing digital health records adoption, and increasing regulatory oversight in healthcare data security.

Segments Covered in the Report

By Component

- Solutions

- Services

By Deployment Mode

- Cloud-based

- On-premises

By Application Type

- Network Security Analytics

- Endpoint Security Analytics

- Application Security Analytics

- Web Security Analytics

- Cloud Security Analytics

By Industry Vertical

- Banking, Financial Services & Insurance (BFSI)

- Healthcare

- IT & Telecom

- Government & Defense

- Retail & E-commerce / Others

Regional Insights

Why Is North America Leading the Security Analytics Market?

North America led the security analytics market with the largest share of 43% in the global market in 2025. The region’s dominance is driven by advanced digital infrastructure, strong cybersecurity awareness, and early adoption of artificial intelligence, machine learning, and big data analytics. Organizations across the United States and Canada are increasing investments in proactive threat detection and real-time monitoring to address ransomware and data breaches. The presence of leading vendors, mature cloud ecosystems, and hybrid infrastructure adoption supports demand. Strict regulatory frameworks, zero-trust architectures, XDR platforms, venture capital funding, and federal cybersecurity initiatives continue accelerating regional market growth.

Why is Asia Pacific the Fastest Growing Region in the Security Analytics Market?

Asia Pacific is expected to expand at the fastest CAGR of 19.40% between 2026 and 2035. Asia Pacific is the fastest-growing region in the Security Analytics Market due to rapid digital transformation, expanding internet penetration, and increasing adoption of cloud computing across emerging economies such as China, India, Japan, and Southeast Asian countries. Organizations are accelerating investments in cybersecurity infrastructure as cyber threats, ransomware attacks, and data breaches become more frequent and sophisticated.

The region’s growing fintech ecosystem, expanding e-commerce sector, and government-led digital initiatives are significantly increasing the volume of sensitive data, driving demand for advanced security analytics solutions. Additionally, rising awareness of regulatory compliance and data protection laws is encouraging enterprises to implement real-time monitoring and AI-driven threat detection systems. Increasing SME adoption and managed security services further contribute to the region’s strong double-digit growth outlook.

Latin America – Security Analytics Market

Latin America’s security analytics market is growing due to increasing cyberattacks, digital transformation, and cloud adoption. Organizations in Brazil and Mexico are investing in real-time monitoring, AI-driven threat detection, and managed security services to strengthen defenses and address data protection and regulatory requirements.

Europe – Security Analytics Market

Europe’s market is expanding with strong GDPR-driven compliance, rising cyber incidents, and public sector investments. Enterprises are deploying AI-enabled analytics, SIEM, and XDR solutions, particularly in the UK, Germany, and France, to enhance visibility, reduce risk, and support hybrid cloud security initiatives.

MEA – Security Analytics Market

In the Middle East and Africa, rapid digital adoption, government cybersecurity programs, and rising awareness are driving security analytics demand. Key sectors like oil & gas, BFSI, and government are prioritizing analytics-driven threat detection and incident response capabilities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- ASEAN Countries

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of MEA

Market Value Chain Analysis in Security Analytics

- Technology Providers and Infrastructure Vendors: The value chain begins with cloud providers, data infrastructure vendors, and cybersecurity technology developers supplying AI engines, data storage systems, and network monitoring tools that form the foundation of security analytics platforms.

- Security Analytics Solution Developers: Software companies design and integrate SIEM, XDR, UEBA, and AI-based analytics platforms, transforming raw security data into actionable insights through advanced algorithms, threat intelligence, and real-time monitoring capabilities.

- System Integrators and Managed Service Providers: Implementation partners and managed security service providers (MSSPs) deploy, customize, and manage analytics solutions, ensuring seamless integration with enterprise infrastructure while offering continuous monitoring and incident response support.

- End-Use Industries and Enterprises: Banks, healthcare institutions, governments, telecom operators, and retail companies utilize security analytics solutions to strengthen cybersecurity posture, maintain regulatory compliance, protect sensitive data, and mitigate operational risks.

Top Security Analytics Market Companies

IBM Security: IBM Security offers advanced analytics solutions with strong AI and machine learning capabilities. Its platform delivers real-time threat detection, behavioral analytics, and automated response. IBM’s global presence and hybrid cloud support help enterprises strengthen their cybersecurity posture across industries.

Cisco Systems: Cisco provides integrated security analytics through network-centric solutions that monitor traffic, endpoints, and cloud environments. Its analytics tools enhance visibility, reduce response times, and support scalable deployments for large enterprises and service providers worldwide.

Palo Alto Networks: Palo Alto Networks focuses on AI-powered analytics and threat intelligence, combining network, endpoint, and cloud security data. Its platforms improve predictive threat detection, reduce breaches, and support zero-trust frameworks across enterprise environments.

Splunk Inc.: Splunk delivers robust security analytics with powerful log management, SIEM capabilities, and user behavior insights. Its real-time monitoring and customizable dashboards help organizations detect anomalies quickly and improve incident response efficiency.

Top Key Players in the Market

- IBM

- Cisco Systems

- Palo Alto Networks

- Splunk, Microsoft

- Fortinet, Broadcom

- LogRhythm

- FireEye (Trellix)

- Elastic

- Rapid7

- Sumo Logic

- Other Major Players

Security Analytics Market Outlook

- Rising Cyber Threat Complexity: Increasingly sophisticated ransomware, phishing attacks, and advanced persistent threats are driving demand for intelligent security analytics platforms focused on proactive detection, real-time monitoring, and predictive risk mitigation.

- Rapid Cloud and Digital Transformation: Expanding adoption of cloud computing, hybrid infrastructure, IoT devices, and remote work models is increasing enterprise attack surfaces, accelerating investment in scalable, cloud-native security analytics solutions.

- Integration of AI and Automation: Artificial intelligence, machine learning, and automation are enhancing behavioral analytics, anomaly detection, and automated incident response, improving detection accuracy while reducing response time and operational costs.

- Regulatory Compliance and Industry Adoption: Strict data protection regulations across BFSI, healthcare, government, and IT sectors are driving deployment of security analytics tools to ensure compliance, protect sensitive data, and strengthen cybersecurity resilience.

Key Market Trends

- AI-Driven Threat Intelligence: Growing integration of artificial intelligence and machine learning to enhance predictive threat detection, anomaly identification, and automated decision-making across enterprise security infrastructures.

- Cloud-Native Security Platforms: Rising deployment of cloud-based analytics solutions to secure hybrid and multi-cloud environments with scalable, centralized, and real-time monitoring capabilities.

- Zero-Trust Security Adoption: Increasing implementation of zero-trust frameworks requiring continuous authentication, behavioral monitoring, and advanced analytics for access control and risk mitigation.

- Extended Detection and Response (XDR): Expansion of unified XDR platforms combining network, endpoint, cloud, and application security data for holistic threat visibility and faster incident response.

- Real-Time Security Monitoring: Growing demand for real-time analytics engines capable of processing high-volume security events to reduce response times and operational disruption.

- Automation and SOAR Integration: Adoption of security orchestration, automation, and response solutions to streamline workflows, reduce manual intervention, and improve operational efficiency.

- Industry-Specific Security Solutions: Development of customized analytics platforms tailored for BFSI, healthcare, government, and retail sectors to address sector-specific compliance requirements.

Recent Developments

- October 2025 – Several leading security analytics vendors enhanced AI-driven threat prediction modules to improve detection accuracy against polymorphic malware, reducing false positives and enriching automated incident response workflows for enterprise customers.

- December 2025 – A major cloud service provider expanded its security analytics platform with cross-cloud visibility capabilities, enabling customers to unify telemetry from multi-cloud environments and accelerate threat hunting across hybrid IT landscapes.

- January 2026 – Collaborative partnerships between security analytics providers and telecom operators were announced to integrate real-time network analytics into 5G security frameworks, addressing rising mobile and IoT attack surfaces.

- February 2026 – Several enterprises began deploying next-generation security analytics with built-in behavioral biometrics, enhancing user anomaly detection to prevent insider threats and credential abuse in remote and hybrid work environments.

Market Scope

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | US$ 16.40 Billion |

| Market Size in 2026 | US$ 19.39 Billion |

| Market Size by 2035 | US$ 87.67 Billion |

| Market Growth Rate from 2025 to 2035 | CAGR of 18.25% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2025 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component Type (Solutions, Services), Deployment Mode (Cloud-Based, On-Premises), By Application Type (Network, Endpoint, Application, Web, And Cloud Security Analytics), And By Industry Vertical (BFSI, Healthcare, IT & Telecom, Government & Defense, Retail & E-Commerce, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC Countries, South Africa, North Africa, and Rest of MEA |