What is the Solid-State Battery Materials Market Size?

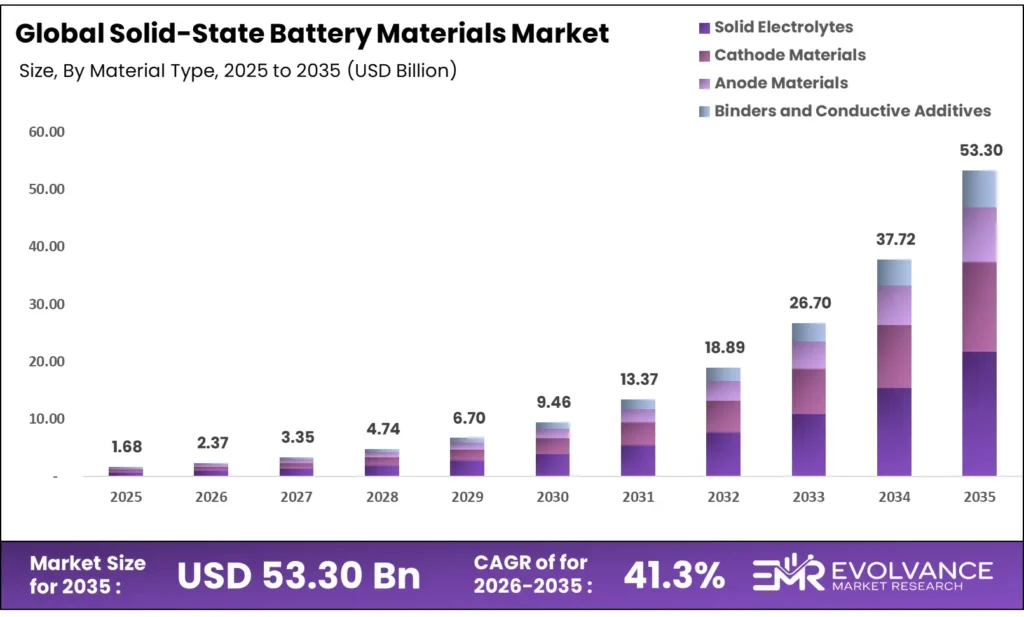

The Global Solid-State Battery Materials Market size will be worth around USD 53.30 Billion by 2035 from USD 1.68 Billion in 2025, growing at a CAGR of 41.3% during the forecast period 2026 to 2035. Automotive OEMs qualifying high-loading cathode materials and lithium-metal anodes are driving procurement shifts at a pace few material suppliers anticipated. Enterprise buyers are now locking in long-term supply contracts for sulfide electrolytes and Ni-rich cathode powders well ahead of mass-production timelines. Raw material cost pressures and sulfide electrolyte interfacial instability remain the most likely supply-side constraints as the market scales toward commercialization.

Market Highlights

- The Global Solid-State Battery Materials Market valued at USD 1.68 Billion in 2025, reaching USD 53.30 Billion by 2035 at a CAGR of 41.3%.

- Asia Pacific leads with a 47.3% market share, valued at USD 0.8 Billion in 2025.

- Solid Electrolytes dominate the By Material Type segment with a 42.1% share.

- Lithium-based Batteries lead the By Battery Type segment with a 54.2% share.

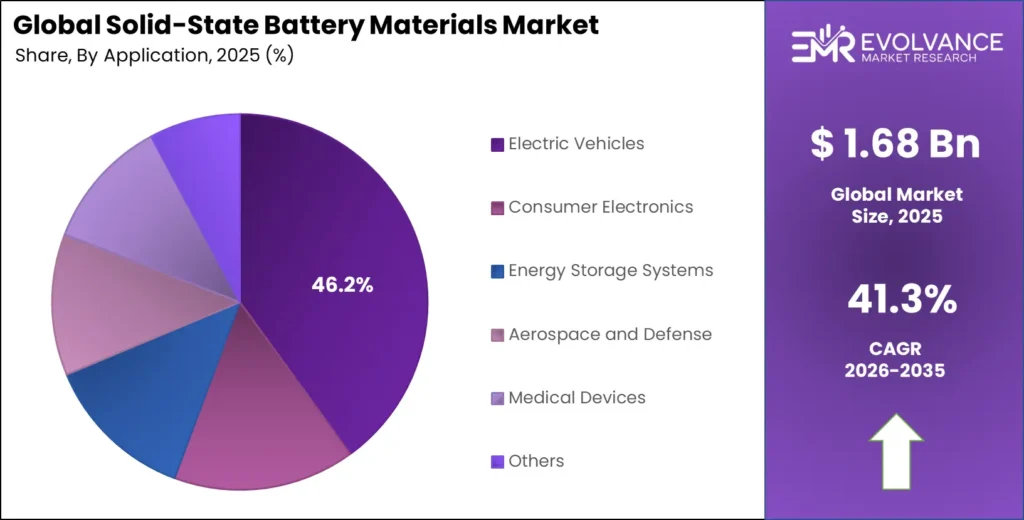

- Electric Vehicles hold the largest By Application share at 46.2%.

- Below 20 mAh capacity segment leads By Capacity with a 43.1% share.

Market Overview

The solid-state battery materials market covers the full range of functional inputs that replace liquid electrolytes in next-generation energy storage — solid electrolytes, cathode powders, anode architectures, and supporting binders. These materials are not incremental upgrades. They represent a fundamental shift in how energy is stored, enabling higher energy density, better thermal stability, and longer cycle life than conventional lithium-ion chemistry.

Material choice defines battery performance. Sulfide-based electrolytes offer the highest ionic conductivity but face interfacial stability challenges. Oxide-based materials provide better chemical stability at the cost of processing complexity. Lithium-ion and silicon-based anodes offer step-change energy density gains. Each trade-off drives distinct procurement decisions across automotive, consumer electronics, and industrial energy storage segments.

The Neodymium (Nd-Fe-B) Magnet shares strong synergies with the Solid-State Battery Materials, driven by the automotive industry’s transition toward next-generation electric vehicles. While solid-state batteries improve energy density and safety, Nd-Fe-B magnets continue to enable compact, high-performance electric motors used alongside these advanced battery technologies.

Governments in Japan, South Korea, China, and the United States are investing in solid-state battery ecosystems through both direct subsidies and national research programs. The U.S. Department of Energy selected Solid Power in September 2024 for award negotiations worth up to $50 million to expand sulfide electrolyte production — a signal that state capital is now flowing directly into material-layer infrastructure, not just cell assembly.

The Royal Society of Chemistry confirmed that sulfide-based solid electrolyte–CNF composites achieved a capacity of 204.0 mAh g⁻¹ at 1C and 82% capacity retention after 100 cycles at 0.5C. This result matters because it shows that material engineering at the electrolyte-electrode interface — not just bulk conductivity — determines commercial viability. Suppliers who solve interface degradation first will command premium pricing as OEM qualification pipelines open.

A DOE-referenced study on 2,000+ cycle testing found that solid-state batteries showed less than 5% capacity loss over that range across a −20°C to 60°C temperature range, versus a 35% capacity loss for liquid lithium-ion cells after just 1,000 cycles. That is a 4× durability advantage, and it directly changes the total cost of ownership calculation for fleet operators and grid storage buyers — shifting the argument from upfront material cost to lifetime value.

Material Type Insights

1. Solid Electrolytes

Solid Electrolytes dominate with 42.1% due to their central role in enabling cell-level performance.

In 2025, Solid Electrolytes held a dominant market position in the By Material Type segment of the Solid-State Battery Materials Market, with a 42.1% share. This leadership reflects the fact that solid electrolytes are the defining input of the entire category — without a viable solid electrolyte, no other material change delivers the promised performance gains. Automotive buyers qualifying cells for next-generation EV platforms are specifying electrolyte chemistry first, then building cathode and anode choices around it.

Sulfide-based Electrolytes offer the highest known ionic conductivity among solid electrolyte classes, making them the leading choice for high-power automotive applications. A 2026 composite solid electrolyte achieved ionic conductivity of 10.2 mS/cm at 25°C while maintaining stable electrode contact — a benchmark that narrows the performance gap with liquid electrolytes. However, moisture sensitivity and interfacial degradation during cycling remain barriers that material suppliers must resolve before mass production becomes viable.

2. Cathode Materials

In 2025, NMC (Nickel Manganese Cobalt) held a dominant market position in the By Cathode Materials segment of the Solid-State Battery Materials Market. NMC cathodes pair well with lithium-metal anodes — the architecture that is emerging as the preferred route for achieving over 500,000 km battery lifespan targets set by leading OEMs. Validated β-Li₃N all-solid-state lithium metal batteries retained 92.5% capacity after 3,500 cycles at 1.0C using an NCM83 cathode — a result that directly supports automotive warranty and lifecycle cost cases for NMC-based solid-state designs.

LFP (Lithium Iron Phosphate) cathodes bring cost and safety advantages that NMC cannot match. Their thermal stability and cobalt-free chemistry reduce supply chain risk, which is a material consideration for OEMs sourcing at scale. While LFP delivers lower energy density than NMC, that gap narrows when paired with lithium-metal anodes — making LFP a credible candidate for solid-state EV applications where long cycle life and lower cost outweigh maximum range performance.

3. Anode Materials

In 2025, Lithium Metal held a dominant market position in the By Anode Materials segment of the Solid-State Battery Materials Market. The lithium-metal architecture is the structural enabler of the industry’s most ambitious performance targets. Stellantis and Factorial Energy validated 77 Ah automotive-sized FEST solid-state battery cells achieving an energy density of 375 Wh/kg, with discharge rates up to 4C under real-world conditions — proving that lithium-metal anodes at scale can meet automotive qualification standards, not just laboratory benchmarks.

Silicon-based Anodes are gaining traction as a near-term bridge between graphite and full lithium-metal architectures. Their ability to enable 10-minute EV fast charging and deliver up to 50% higher energy density than graphite is drawing design-in activity from OEMs who need performance gains within existing production timelines. An areal capacity of 12.7 mAh/cm² has been demonstrated in laboratory settings with normalized energy densities of 1,300 mAh/cm³ in silicon/graphite hybrid configurations — signals that silicon-rich anode performance is advancing faster than scale-up costs are falling.

4. Binders and Conductive Additives

Binders and Conductive Additives are the enabling layer that holds solid-state electrode architectures together during cycling. Unlike in liquid-electrolyte cells, binder choice in solid-state designs directly affects ionic transport pathways — a poorly chosen binder raises internal resistance and degrades the performance gains that the active materials deliver. This functional criticality is elevating binder and additive suppliers from commodity vendors to qualified material partners in OEM supply chains.

Capacity Insights

Below 20 mAh capacity dominates with 43.1% due to strong demand from miniaturized electronics and wearable applications.

In 2025, the Below 20 mAh segment held a dominant market position in the By Capacity segment of the Solid-State Battery Materials Market, with a 43.1% share. This leadership is driven by the rapid expansion of wearables, hearables, and medical implants — devices where form factor is the primary design constraint and energy density per unit volume matters far more than absolute capacity. Oxide-based and thin-film solid electrolyte materials are the dominant inputs for this segment, and their qualification processes are shorter than automotive-grade materials, enabling faster revenue cycles for material suppliers.

Above 500 mAh batteries represent the highest-value, lowest-volume segment today — and the largest future opportunity. This is the automotive and grid storage arena, where CATL has begun pilot production targeting an energy density of 500 Wh/kg, nearly double the 200–300 Wh/kg of current commercial lithium-ion batteries. Material suppliers serving this segment face the longest qualification cycles and highest technical specifications, but the contract values and switching costs once qualified create durable competitive positions.

Battery Type Insights

Lithium-based Batteries dominate with 54.2% because lithium chemistry offers the highest energy density and has the deepest industrial development history.

In 2025, Lithium-based Batteries held a dominant market position in the By Battery Type segment of the Solid-State Battery Materials Market, with a 54.2% share. The commercial momentum behind lithium-metal solid-state architectures is reinforced by every major OEM qualification milestone — including QuantumScape’s Alpha-2 cell shipments in March 2024 featuring higher-loading cathodes, and PowerCo’s confirmation in January 2024 that QuantumScape’s solid-state cell exceeded 1,000 charging cycles while retaining more than 95% capacity. These milestones set the material specification bar that suppliers must meet to enter the automotive supply chain.

Sodium-based Batteries likes sodium-ion offer a materials cost advantage that matters in cost-sensitive energy storage applications. Sodium’s natural abundance removes the lithium supply concentration risk that is increasingly factored into EV platform planning by Western OEMs. A 2025 RSC sodium solid-state electrolyte cell retained 80% capacity after 800 cycles at a 3C charge/discharge rate — a performance level that, while below leading lithium-metal results, is reaching practical thresholds for stationary energy storage buyers who prioritize cost per cycle over maximum energy density.

Thin-film Batteries serve the most constrained applications — implantable medical devices, RFID tags, and micro-sensors where battery dimensions are measured in microns. Oxide-based electrolytes deposited by sputtering are the dominant material route for thin-film solid-state designs. Their market is small by volume but large by margin, and the technical barriers to entry are high enough that qualified suppliers face limited competition once they achieve design-in status with a device manufacturer.

Application Insights

Electric Vehicles dominate with 46.2% as automotive OEMs accelerate solid-state battery qualification programs at a pace that is pulling material demand forward.

In 2025, Electric Vehicles held a dominant market position in the By Application segment of the Solid-State Battery Materials Market, with a 46.2% share. Volkswagen’s PowerCo signed a licensing agreement with QuantumScape in July 2024, enabling production of up to 40 GWh annually — expandable to 80 GWh — of solid-state battery cells. The material procurement volumes for sulfide electrolytes, high-nickel cathodes, and lithium-metal anodes shift from pilot quantities to industrial supply contracts, creating the demand anchor that justifies manufacturing capacity investment by material suppliers.

Consumer Electronics represents the near-term revenue base for solid-state material suppliers because cell qualification cycles are shorter and production volumes are already established. Mercedes-Benz’s solid-state EQS prototype achieving 1,205 km on a single charge — with 137 km of remaining range after completing the drive — demonstrates what higher energy density means at the system level. That performance narrative accelerates consumer pull for solid-state-powered devices in premium electronics segments.

Energy Storage Systems are a growing application area as grid operators seek batteries that maintain performance across wide temperature ranges and thousands of cycles. Solid-state materials that enable less than 5% capacity loss over 2,000+ cycles across −20°C to 60°C — versus 35% loss in liquid cells after 1,000 cycles — directly address the total cost of ownership arguments that grid procurement teams use to justify capital allocation decisions.

Aerospace and Defense buyers apply different evaluation criteria than commercial markets. Safety, reliability under extreme conditions, and performance in compressed form factors outweigh cost considerations. Solid Power’s sulfide-based cells demonstrating structural integrity at temperatures up to 130°C with no thermal runaway events — versus 3 events recorded in liquid battery thermal cycling — create a strong safety case for defense procurement officers who manage liability and mission-critical reliability requirements.

Market Segments Covered in the Report

By Material Type

- Solid Electrolytes

- Sulfide-based Electrolytes

- Oxide-based Electrolytes

- Polymer-based Electrolytes

- Composite / Hybrid Electrolytes

- Cathode Materials

- NMC (Nickel Manganese Cobalt)

- LFP (Lithium Iron Phosphate)

- High-Nickel Cathodes

- LNMO and Advanced Cathodes

- Others

- Anode Materials

- Lithium Metal

- Silicon-based Anodes

- Graphite-based Anodes

- Composite Anodes

- Binders and Conductive Additives

By Capacity

- Below 20 mAh

- 20–500 mAh

- Above 500 mAh

By Battery Type

- Lithium-based Batteries

- Sodium-based Batteries

- Thin-film Batteries

- Others

By Application

- Electric Vehicles

- Consumer Electronics

- Energy Storage Systems

- Aerospace and Defense

- Medical Devices

- Others

Regional Insights

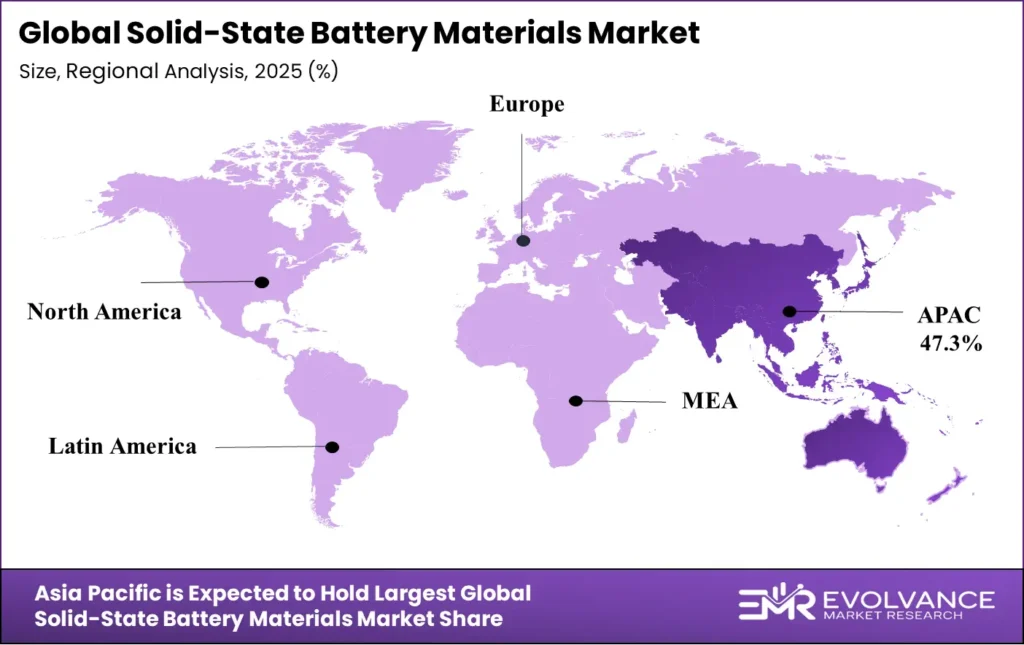

Asia Pacific Dominates the Solid-State Battery Materials Market with a Market Share of 47.3%, Valued at USD 0.8 Billion

Asia Pacific holds a 47.3% share — valued at USD 0.8 Billion in 2025 — because Japan, South Korea, and China are home to the deepest concentration of solid-state battery R&D infrastructure and the most advanced OEM qualification programs globally. Toyota’s 2027–2028 commercialization targets, Honda’s pilot production line in Sakura City unveiled in November 2024, and Korean battery manufacturers’ patent activity around sulfide electrolytes collectively create a material demand concentration that no other region can match in the near term.

North America Solid-State Battery Materials Market Trends

North America is the second-largest regional market, anchored by U.S. government investment in domestic solid electrolyte production. The DOE’s up to $50 million award negotiation with Solid Power in September 2024 signals that federal industrial policy is targeting the material layer — not just cell assembly — as a strategic supply chain priority. QuantumScape’s Alpha-2 shipments and PowerCo’s licensing payment of $130 million confirm that North America is at the center of the global solid-state technology licensing market.

Europe Solid-State Battery Materials Market Trends

Europe’s market position is defined by Volkswagen’s commitment to solid-state battery industrialization through its PowerCo subsidiary and the QuantumScape licensing agreement covering up to 80 GWh of annual production capacity. Stellantis and Factorial Energy’s validation of 375 Wh/kg FEST cells with more than 600 charge cycles shows that European automotive OEMs are moving beyond feasibility studies into active cell qualification — a shift that creates near-term demand for qualified cathode and electrolyte material suppliers.

Latin America Solid-State Battery Materials Market Trends

Latin America’s solid-state battery materials market is at an early stage relative to Asia Pacific, North America, and Europe. The region’s primary strategic relevance is as a source of battery raw materials — particularly lithium from Argentina, Bolivia, and Chile — rather than as a downstream cell or material processing hub. As global OEM supply chains for solid-state materials mature and demand scales, regional processing capacity for lithium feedstock will become an increasingly valued asset.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The U.S. Department of Energy’s Battery Materials Processing and Manufacturing Program — active through 2024 and 2025 — sets compliance and reporting standards for companies receiving federal awards to produce solid electrolyte materials at scale. Solid Power’s award negotiation for up to $50 million in September 2024 falls under this program. Suppliers receiving DOE funding must meet domestic content requirements and performance reporting obligations that affect their production planning and supply agreements.

The European Battery Regulation (EU) 2023/1542, which began phased enforcement in 2024, establishes carbon footprint declaration requirements and supply chain due diligence standards for batteries sold in the EU market. By 2026, solid-state battery cells supplied to European automotive OEMs must carry verified lifecycle carbon data. This regulation directly affects cathode material suppliers sourcing nickel and cobalt, raising compliance costs and favoring suppliers with traceable, low-carbon feedstock chains.

Japan’s Green Innovation Fund, administered through NEDO, continued to channel funding into solid-state battery material development partnerships through 2024 and 2025. Honda’s Sakura City pilot production line and Toyota’s material qualification programs operate under funding frameworks that include technology milestone reporting requirements. These conditions shape the pace and public disclosure of solid-state material development in Japan’s automotive supply chain.

China’s Ministry of Industry and Information Technology updated its New Energy Vehicle industry development guidelines in 2024, explicitly prioritizing solid-state battery technology as a strategic objective for the 2025–2030 period. CATL’s pilot production at 500 Wh/kg energy density targets aligns with these national performance benchmarks. Suppliers entering the Chinese market face both regulatory opportunity — through preferential procurement policies — and competitive pressure from state-backed material producers operating under the same framework.

Drivers

Automotive OEM Qualification Programs Pull Advanced Cathode and Electrolyte Materials Into Industrial-Scale Demand

Automotive OEMs are now validating solid-state cells at formats and performance levels that require industrial material supply — not lab quantities. Volkswagen’s PowerCo secured licensing rights to manufacture up to 40 GWh annually of solid-state cells under its July 2024 agreement with QuantumScape, with a pre-payment of $130 million. That financial commitment means cathode and electrolyte material suppliers serving PowerCo face real production scale-up requirements, not future hypotheticals.

PowerCo’s own laboratory testing confirmed that QuantumScape’s solid-state cell exceeded 1,000 charging cycles while retaining more than 95% capacity in January 2024. These endurance results set the material specification bar — suppliers must now demonstrate that their cathode powders, sulfide electrolytes, and anode materials can sustain that cycle performance at production quality, not just in hand-selected samples. The qualification bar is rising faster than most material suppliers anticipated.

Moreover, QuantumScape’s Cobra separator heat-treatment process achieved approximately 25× manufacturing speed improvement over the previous process generation. That throughput gain compresses the timeline from prototype validation to production-rate material demand, giving material suppliers a shorter window to build inventory and quality systems before automotive customers begin pulling at volume. Speed of qualification now matters as much as technical performance.

Restraints

Sulfide Electrolyte Interfacial Instability and High Processing Costs Delay Mass-Market Solid-State Battery Material Adoption

Persistent interfacial instability between sulfide solid electrolytes and both cathode and anode materials remains the primary technical barrier to commercialization. Sulfide electrolytes react with moisture during processing and form resistive interphases at electrode boundaries during cycling — degradation modes that require complex surface coating and cell assembly conditions that add cost and reduce manufacturing yield at scale.

Research published in OAE in April 2026 confirmed that solid-state electrolyte and lithium composites exhibit thermal runaway onset within a narrow window of approximately 270–350°C, while ultra-high-energy-density designs may generate temperatures exceeding 1,600°C under short-circuit conditions. This thermal behavior profile defines new safety engineering requirements for cell manufacturers — and new material qualification standards that suppliers must meet before OEMs will approve their inputs for vehicle-grade applications.

Additionally, Toyota’s 2027–2028 commercialization targets for EV solid-state batteries signal that the mass-production window for cathode and electrolyte materials at automotive scale remains two to three years away. That gap creates a financing challenge for material suppliers who must invest in production capacity now — at current low volumes and high unit costs — to be positioned when OEM demand scales. Companies without strong balance sheets or strategic partners face real execution risk in that window.

Growth Factors

Miniaturized Electronics Demand and Automotive Supply Chain Partnerships Unlock New Material Revenue Streams

TDK’s advances in oxide-based solid-state battery materials for wearables and miniaturized electronics open a near-term revenue channel that does not require automotive qualification timelines. The wearable electronics market — which includes hearables, smartwatches, AR glasses, and health monitoring patches — needs high energy density in sub-20 mAh form factors. Oxide electrolyte and thin-film material suppliers serving this segment can build revenue and manufacturing experience well ahead of the automotive volume ramp.

Toyota and Sumitomo Metal’s advances toward practical EV solid-state battery use are specifically focused on scaling demand for high-durability cathode powders and sulfide electrolytes at production quality. KERI’s nano-tin interlayer development in April 2026 enabled all-solid-state batteries to achieve greater than 350 Wh/kg energy density while operating at a low pressure of only 2 MPa — a result that reduces the mechanical compression requirements for cell assembly and directly lowers manufacturing cost at scale for cathode and electrolyte input suppliers.

Furthermore, LG Energy Solution and General Motors expanded their joint battery chemistry development partnership in December 2024, creating a significant commercial signal for prismatic solid-state battery material suppliers. Joint OEM chemistry development programs pull material suppliers into co-development agreements that provide both near-term revenue and long-term supply exclusivity. Suppliers who secure co-development positions in these partnerships build technical switching costs that protect their margins through the qualification process and into early production.

Emerging Trends

Lithium-Metal Anode Architectures and Silicon-Rich Composites Redefine Performance Benchmarks for Solid-State Material Suppliers

The industry is shifting toward lithium-metal anode architectures as the structural route to achieving over 500,000 km battery lifespan and more than 1,000 charging cycles — performance levels that justify solid-state premium pricing relative to lithium-ion. Factorial Energy’s FEST cells achieved fast charging from 15% to over 90% in just 18 minutes at room temperature. That charging speed, combined with the energy density and cycle life data, changes the total value proposition for automotive buyers — and consequently changes the material specification requirements that electrolyte and cathode suppliers must meet.

Silicon-dominant and silicon-graphene composite anode materials are advancing from research tools to production-relevant architectures. The ability to enable 10-minute EV fast charging and up to 50% higher energy density than graphite is driving design-in activity across multiple OEM platforms simultaneously. KERI’s large-area pouch cells using the nano-tin interlayer retained more than 81% capacity after 500 charge-discharge cycles even under the ultra-low pressure of 2 MPa — showing that advanced interlayer engineering is solving the pressure sensitivity challenge that previously made silicon-rich anodes impractical for large-format cells.

Accelerating global collaboration between material suppliers, automotive OEMs, and governments through dedicated solid-state battery ecosystem partnerships in Japan and South Korea is concentrating R&D spending and supply chain development in ways that favor established regional players. Huawei, Toyota, and Korean battery manufacturers are filing patents around sulfide-based solid electrolytes at an accelerating rate. Early movers who secure intellectual property positions in key material formulations will have structural advantages in licensing and supply negotiations as the market scales through 2030.

Key Companies Insights

Hitachi Zosen Corporation brings heavy industrial manufacturing expertise to solid-state battery material development — a background that matters when the market challenge shifts from chemistry to production engineering. Their experience in precision machinery and process equipment gives them an advantage in developing the high-tolerance production environments that sulfide and oxide electrolyte processing requires. As OEM customers move from prototype qualification to production-rate purchasing, suppliers with demonstrated process scale-up capability will command preferred vendor status over pure chemistry-focused competitors.

Ampcera positions itself at the electrolyte materials layer with a focus on scalable solid electrolyte synthesis — the bottleneck that separates lab-scale performance results from commercially viable production economics. Their approach targets the cost and throughput barriers that are slowing sulfide electrolyte adoption across automotive supply chains. In a market where electrolyte material quality and consistency define cell-level performance, suppliers who demonstrate tight process control across production batches will differentiate on yield and qualification speed rather than just on chemistry.

Ilika Ltd. focuses on thin-film and miniaturized solid-state battery materials — a market segment where their Stereax technology addresses the medical device and industrial IoT applications that require solid-state performance in the smallest possible form factors. These applications carry the shortest qualification timelines in the solid-state materials market and the highest margin structures. Ilika’s specialization in sub-20 mAh form factors gives them a focused commercial position that avoids direct competition with automotive-grade material suppliers while building revenue ahead of the EV volume ramp.

Solid Power operates across both cell development and solid electrolyte material supply — a dual-position strategy that gives it both application knowledge and upstream material credibility. Their September 2024 selection by the U.S. Department of Energy for award negotiations worth up to $50 million for sulfide electrolyte production at their Thornton, Colorado facility validates their manufacturing readiness. Solid Power’s structural integrity data — cells maintaining performance at temperatures up to 130°C with no thermal runaway — is the kind of safety evidence that automotive and aerospace qualification programs require before approving material suppliers.

Key Companies

- Hitachi Zosen Corporation

- Ampcera

- Ilika Ltd.

- Solid Power

- STMicroelectronics

- BrightVolt Solid-State Batteries

- Ion Storage Systems

- Blue Solutions

- Samsung SDI Co., Ltd.

- Panasonic Energy Co., Ltd.

- QuantumScape Corporation

- Toyota Motor Corporation

- ProLogium Technology CO., Ltd.

Recent Development

- In April 2025, Stellantis and Factorial Energy validated 77 Ah automotive-sized FEST solid-state battery cells achieving an energy density of 375 Wh/kg with discharge rates up to 4C under real-world conditions — a milestone for large-format lithium-metal solid-state batteries. The validated cells charged from 15% to over 90% in 18 minutes at room temperature, advancing the cells toward automotive qualification.

- In April 2026, KERI (Korea Electrotechnology Research Institute) developed a nano-tin interlayer enabling all-solid-state batteries to achieve greater than 350 Wh/kg energy density while operating at a low pressure of only 2 MPa. KERI’s large-area pouch cells using this interlayer retained more than 81% capacity after 500 charge-discharge cycles at that ultra-low pressure.

- In March 2026, CATL began pilot production of solid-state batteries targeting an energy density of 500 Wh/kg — nearly double the 200–300 Wh/kg of current commercial lithium-ion batteries, marking a significant advance toward mass-market production readiness.

- In July 2024, QuantumScape disclosed that Volkswagen battery subsidiary PowerCo would pre-pay an initial royalty fee of $130 million under a licensing agreement to industrialize QuantumScape’s solid-state battery technology, with PowerCo licensed to manufacture up to 40 GWh annually — expandable to 80 GWh.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.68 Billion |

| Forecast Revenue (2035) | USD 53.30 Billion |

| CAGR (2026-2035) | 41.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Material Type (Solid Electrolytes, Cathode Materials, Anode Materials, Binders and Conductive Additives), By Capacity (Below 20 mAh, 20–500 mAh, Above 500 mAh), By Battery Type (Lithium-based Batteries, Sodium-based Batteries, Thin-film Batteries, Others), By Application (Electric Vehicles, Consumer Electronics, Energy Storage Systems, Aerospace and Defense, Medical Devices, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Hitachi Zosen Corporation, Ampcera, Ilika Ltd., Solid Power, STMicroelectronics, BrightVolt Solid-State Batteries, Ion Storage Systems, Blue Solutions, Samsung SDI Co., Ltd., Panasonic Energy Co., Ltd., QuantumScape Corporation, Toyota Motor Corporation, ProLogium Technology CO., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |