What is the Sodium-ion Battery Market Size?

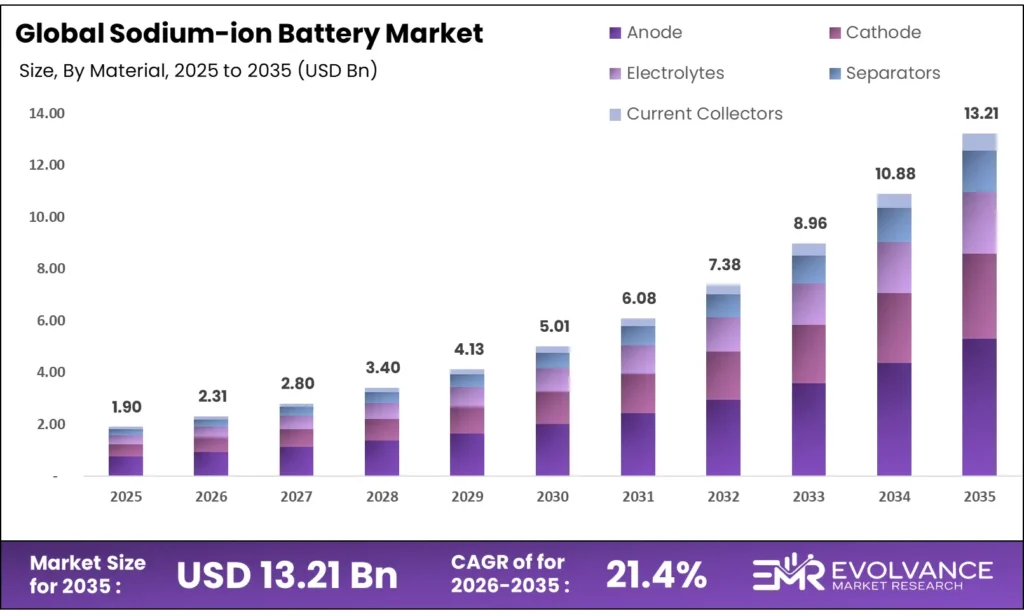

The Global Sodium-ion Battery Market size will be worth around USD 13.21 Billion by 2035 from USD 1.90 Billion in 2025, growing at a CAGR of 21.4% during the forecast period 2026 to 2035. Lithium price instability in 2024 pushed automotive OEMs and grid operators to actively test sodium-based chemistries as cost-stable alternatives. Buyers in the Electric Vehicles and stationary storage segments are now shifting procurement timelines rather than waiting for full commercial parity with lithium iron phosphate. Supply-side risks remain real: energy density gaps and a heavily China-concentrated production base expose non-Chinese buyers to geopolitical supply chain risk.

Market Highlights

- The Global Sodium-ion Battery Market size grows from USD 1.90 Billion in 2025 to USD 13.21 Billion by 2035, at a CAGR of 21.4%

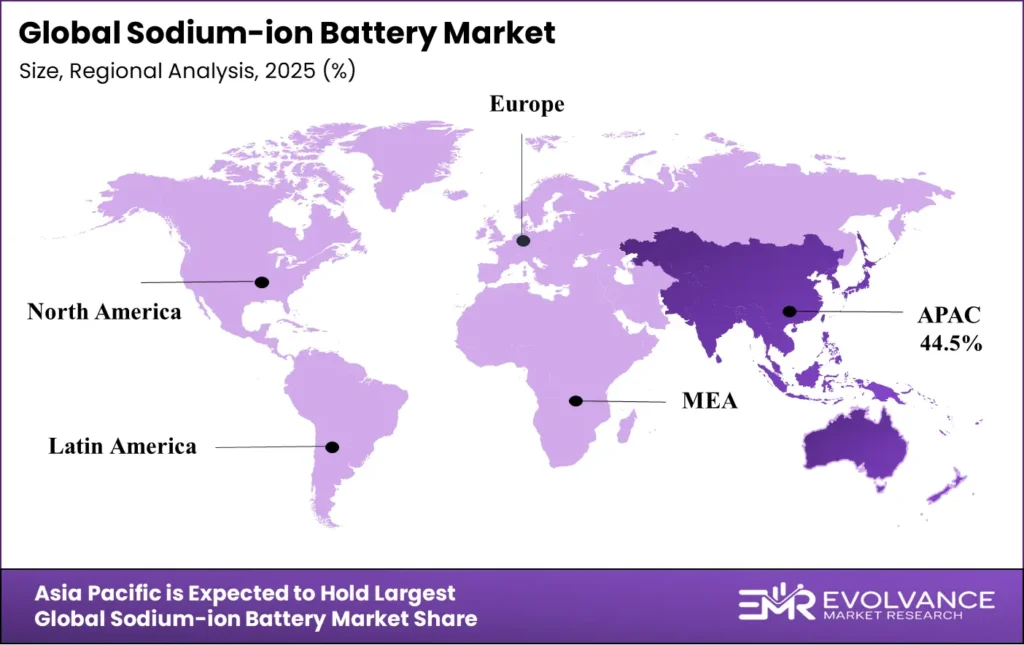

- Asia Pacific leads with a 44.5% market share, valued at USD 846 Million

- Electric Vehicles dominate the By Application segment with a 51.2% share

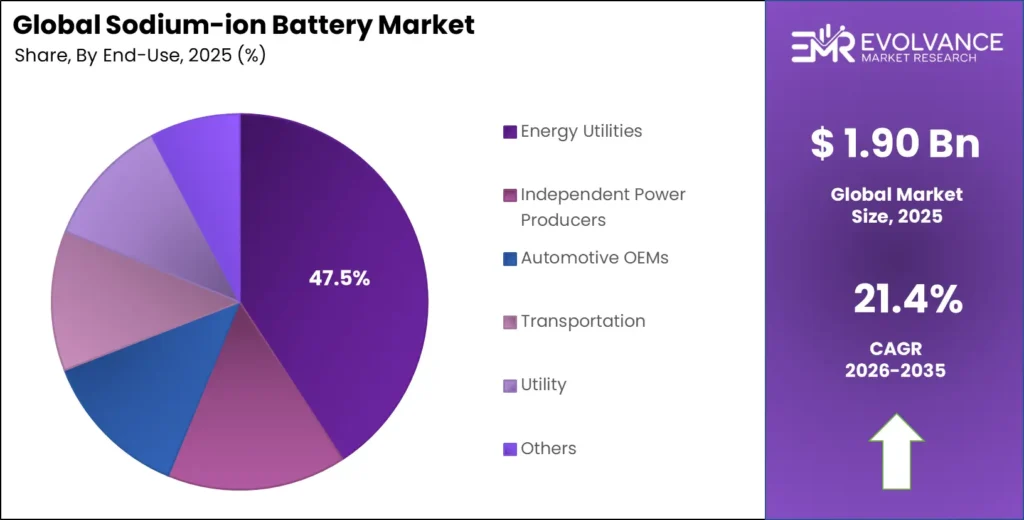

- Energy Utilities lead the By End User segment with a 47.5% share

- Sodium Sulfur Battery leads the By Product Type segment with a 37.4% share

- Anode Materials lead the By Material Type segment with a 42.3% share

Market Overview

Sodium-ion batteries store electrical energy using sodium ions moving between anode and cathode materials. Unlike lithium-ion cells, they use abundant sodium salts instead of lithium carbonate. This difference makes them structurally cheaper to produce at scale and less exposed to the supply chain pressures that raised lithium prices sharply in 2022 and 2024.

The technology spans several distinct chemistries — from high-temperature sodium-sulfur systems used in grid storage to room-temperature hard-carbon anode cells targeting EVs. Each chemistry trades off energy density, cycle life, and temperature range. This creates a market where no single product wins all applications, leaving room for specialized vendors to build durable positions in focused niches.

Government policy is accelerating commercial adoption. China’s 2024 policy cycle funded dozens of demonstration projects for sodium-ion grid storage. In Europe, the EU’s Critical Minerals Act and battery regulation are pushing manufacturers to develop lithium-free alternatives. In the US, ARPA-E’s SCALEUP program provided USD 19.8 million to support first-of-kind domestic sodium-ion production. In July 2024, Peak Energy closed a USD 55 million Series A round — led by Temasek’s Xora Innovation — signaling that institutional capital is now backing sodium-ion at scale outside China.

According to IRENA, global sodium-ion production capacity will reach 70 GWh per year by late 2025, rising to nearly 400 GWh annually by end of the decade. That sevenfold expansion in five years signals that vendors are building ahead of confirmed demand — a pattern that historically compresses margins during the ramp phase but rewards early movers who lock in offtake agreements before the market consolidates.

As per Benchmark Mineral Intelligence, China controls 96% of global sodium-ion production capacity in 2025. This concentration means Western buyers seeking to diversify away from lithium supply risks may find themselves trading one geographic dependency for another. Investors and procurement teams outside China should factor this into their vendor qualification strategies now, before commercial volumes make renegotiation difficult.

Product Type Insights

Sodium Sulfur Battery dominates with 37.4% due to proven grid-scale deployment history.

In 2025, Sodium Sulfur Battery held a dominant market position in the By Product Type segment of the Sodium-ion Battery Market, with a 37.4% share. This leadership reflects over two decades of commercial deployment in utility-scale grid storage, where the technology’s high energy density at the system level and long discharge duration have made it the reference choice for load-leveling applications.

However, Japan’s NGK Insulators — the world’s only commercial-scale producer — resolved in November 2025 to permanently exit this market after installing over 720 MW / 5,000 MWh across more than 250 global sites, recording estimated extraordinary losses of USD 117 million. The segment’s future rests on whether a successor manufacturer enters before buyers redirect procurement to room-temperature alternatives.

Non-Aqueous Sodium-Ion Batteries represent the primary pathway for EV and consumer electronics adoption. These cells operate at room temperature using organic electrolytes, enabling the compact form factors EV manufacturers need. CATL’s Naxtra sodium-ion battery — achieving 175 Wh/kg energy density with a temperature range of -40°C to +70°C and over 10,000 cycles — shows this sub-segment is closing the performance gap with lithium iron phosphate faster than most buyers anticipated. TIAMAT (France) secured EUR 30 million in funding to build a 5 GWh sodium-ion gigafactory in Amiens, with construction of the first 0.7 GWh phase beginning in Q1 2024, reinforcing Europe’s bet on non-aqueous chemistry for industrial applications.

Aqueous Sodium-Ion Batteries serve stationary and low-power applications where safety and cycle life outweigh energy density. The water-based electrolyte eliminates flammability risk, making this chemistry well-suited to indoor commercial installations and grid support systems where thermal management is constrained.

Sodium-Oxygen (Sodium Air) Batteries remain at the research stage. Theoretical energy density far exceeds any commercial sodium-ion chemistry, but air electrode degradation and sodium dendrite formation have not yet been solved at the cell level. This sub-segment represents a long-cycle R&D bet rather than a near-term revenue opportunity.

Solid-State Sodium-Ion Batteries combine the safety profile of solid electrolytes with sodium’s cost advantage. Eliminating liquid electrolytes removes the primary flammability risk in sodium-ion cells. Several European and Asian research programs are funding prototype development, but commercial production lines are not expected before 2028.

Carbon-Based Sodium-Ion Batteries use hard carbon anodes derived from biomass or synthetic precursors. This sub-segment benefits directly from sodium-ion’s avoidance of graphite — a material subject to the same geographic supply concentration as lithium. Hard carbon anode supply chains are actively being developed in China, with one 2024 contract covering a 50,000-ton cathode and anode material production base for sodium-ion applications.

Transition Metal Oxide Sodium-Ion Batteries use layered oxide cathodes that can be tuned for voltage, capacity, and cycle life by varying the transition metal composition. Chinese manufacturers have filed a rising share of global patents in this cathode class, reflecting their strategy to own the IP layer before the market scales.

Graphite Anode Sodium-Ion Batteries represent a transitional chemistry. Standard graphite does not intercalate sodium efficiently, so true sodium-ion cells use hard carbon or titanate anodes. Products marketed under this label typically use hybrid or modified electrode designs. The sub-segment serves buyers who need sodium-ion economics with familiar manufacturing processes.

Layered Oxide Cathode Sodium-Ion Batteries are among the most commercially advanced cathode architectures. China’s patent filings in this category rose sharply through 2024, and multiple commercial products use layered oxide cathodes in grid storage deployments. Based on data from China Energy Storage Alliance, 37 new sodium-ion capacity projects totaling 179.5 GWh were recorded in China alone during January to September 2025 — with six projects each exceeding 10 GWh — and layered oxide cathode designs underpin the majority of these installations.

Material Type Insights

Anode Materials dominate with 42.3% due to hard carbon’s central role in commercial cell design.

In 2025, Anode Materials held a dominant market position in the By Material Type segment of the Sodium-ion Battery Market, with a 42.3% share. Hard carbon — derived from biomass pyrolysis or synthetic precursors — is the standard anode material for commercial sodium-ion cells because sodium ions cannot intercalate into graphite the way lithium ions do. This forces a completely different supply chain from lithium-ion, which is a structural advantage for countries seeking to reduce graphite import exposure. The anode material segment captures the highest share because cell manufacturers must solve the anode first before the full chemistry becomes viable at scale.

Metal Oxides serve as an alternative anode material in specific high-power applications. Titanate-based oxides offer faster charge rates than hard carbon, making them attractive for grid frequency regulation where response speed matters more than energy capacity. The trade-off is lower energy density, which limits their use in mobile or portable applications.

Porous Hard Carbon is the refined variant of standard hard carbon with engineered porosity to maximize sodium ion storage sites. Producers in China and Europe are investing in controlled porosity processes to improve first-cycle efficiency — a known weakness of hard carbon anodes that directly reduces usable cell capacity in the first charge cycle.

Cathode Materials determine the cell’s voltage, capacity, and cycle life, making cathode chemistry the primary differentiator between competing sodium-ion products. The cathode material sub-segment is where IP competition is most intense: 2024 saw a sharp rise in patent filings covering Prussian Blue Analogues and layered oxides in both China and Europe.

Layered Metal Oxides are the leading cathode material class for commercial sodium-ion cells. Their layered crystal structure allows sodium ions to insert and extract repeatedly without significant structural degradation, supporting the long cycle lives needed for grid applications. CATL’s Naxtra battery uses a layered oxide cathode, anchoring this material class as the commercial reference point for the industry.

Phosphate-based Polyanionic cathodes offer excellent thermal stability and a flat discharge voltage profile. These properties make them well-suited to stationary storage and backup power applications where consistent voltage delivery is more important than maximum energy density. The chemistry is also more chemically stable than oxide-based cathodes at elevated temperatures.

Prussian Blue Analogues (PBAs) are low-cost cathode materials made from iron, carbon, and nitrogen — elements with no supply concentration risk. Altris AB (Sweden) has built its commercial strategy around PBA cathode materials, securing strategic investment from Volvo Cars Tech Fund and Clarios, and targeting up to 350 tonnes of annual cathode active material output from its Czech Republic production facility backed by a EUR 19.3 million in-kind investment from Draslovka.

Electrolytes in sodium-ion cells use sodium salt dissolved in organic solvents or water. The electrolyte formulation directly controls ionic conductivity, temperature performance, and safety. Natron Energy’s sodium-ion cells used an aqueous electrolyte, enabling non-flammable operation — a design choice that supported their target market in data center UPS and industrial backup power before the company ceased operations in September 2025.

Separators in sodium-ion cells must accommodate larger sodium ions than lithium-ion separators, requiring modified pore structures. This creates a distinct separator supply chain that is still being established outside China. Early-stage separator producers in Japan and South Korea are actively qualifying sodium-ion-specific separator products.

Current Collectors in sodium-ion cells can use aluminum for both anode and cathode — unlike lithium-ion, which requires copper for the anode. This single material simplification reduces cell cost and eliminates one commodity supply chain dependency, a structural cost advantage that manufacturers increasingly highlight in procurement discussions.

Application Insights

Electric Vehicles dominate with 51.2% due to OEM demand for cost-stable lithium-free supply chains.

In 2025, Electric Vehicles held a dominant market position in the By Application segment of the Sodium-ion Battery Market, with a 51.2% share. Chinese automakers integrating CATL’s Naxtra battery began commercial passenger EV deliveries using sodium-ion packs in April 2024 — a milestone that shifted sodium-ion from a demonstration technology to an OEM-qualified product. China’s planned sodium-ion projects in 2024 alone totaled 48 projects with a combined capacity of 254.7 GWh and investment of CNY 126.77 billion, confirming that EV demand is driving the majority of capacity investment decisions.

Consumer Electronics represent a secondary application where sodium-ion’s cost advantage matters but energy density constraints are more acute. Portable devices require high energy density in a small form factor — a specification where sodium-ion currently trails lithium-ion. Until energy density reaches commercial parity, this sub-segment will remain a niche opportunity for low-power devices and specific price-sensitive product lines.

Stationary Energy Storage is the second-largest application and the one most aligned with sodium-ion’s current technical strengths. HiNa Battery Technology supplied the world’s first 100 MWh sodium-ion energy storage project in June 2024 — a 50 MW / 100 MWh facility for Datang Group in Hubei Province — proving that sodium-ion can operate reliably at utility scale. CATL’s energy storage battery systems revenue grew 34.32% year-over-year to RMB 57.29 billion in FY2024, with global energy storage market share reaching 36.5%, driven partly by sodium-ion product integration.

Residential Energy Storage is an application where sodium-ion’s non-toxicity and thermal stability create a safety advantage over high-temperature chemistries. However, residential buyers prioritize compact size and long warranty periods. Sodium-ion residential products are entering this market at the lower price end, targeting cost-conscious buyers in markets where grid reliability is poor.

Emergency Backup and UPS was the core target market for Natron Energy’s sodium-ion cells before the company halted operations. Aqueous sodium-ion chemistry’s non-flammability made it ideal for indoor data center and industrial UPS applications. The exit of Natron — which had committed over USD 363 million in total cumulative funding — signals that the backup power segment requires more application-specific sales effort than initially modeled by early entrants.

Telecommunications Systems require reliable, temperature-stable backup power for tower sites and exchange facilities. Sodium-ion cells operating reliably from -40°C to +70°C — as demonstrated by CATL’s Naxtra chemistry — are technically well-matched to outdoor telecom base stations in extreme climate environments. This sub-segment is still in early commercial evaluation and has not yet produced large volume contracts.

End User Insights

Energy Utilities dominate with 47.5% due to grid-scale procurement scale and long-duration storage mandates.

In 2025, Energy Utilities held a dominant market position in the By End User segment of the Sodium-ion Battery Market, with a 47.5% share. Utilities procure battery storage in bulk under multi-year programs tied to grid reliability mandates and renewable integration targets. Their procurement volumes dwarf other buyer categories, which is why even a modest share of utility spend moves market revenue significantly. China’s Datang Group and grid-connected demonstration projects funded in the 2024 policy cycle both point to utilities as the anchor buyer class for the next phase of market scaling.

Independent Power Producers (IPPs) are increasingly evaluating sodium-ion for behind-the-meter and co-located renewable storage projects. Peak Energy’s USD 500+ million multi-year supply agreement with Jupiter Power for up to 4.75 GWh of sodium-ion storage between 2027 and 2030 is the clearest signal that IPPs are moving from evaluation to contracted procurement. This deal — the largest single US sodium-ion deployment announced — demonstrates that non-utility commercial buyers are now writing long-term supply agreements rather than waiting for further cost reductions.

Automotive OEMs are qualifying sodium-ion cells primarily for lower-range urban EVs and two- and three-wheeler vehicles in Asia, where price sensitivity is acute and range requirements are modest. CATL’s plan to integrate Naxtra sodium-ion batteries into over 3,000 Choco-Swap battery swap stations across 140 cities positions automotive OEMs to access sodium-ion economics through a shared mobility model, reducing per-vehicle cost exposure while building volume for the supply chain.

Transportation buyers beyond passenger EVs — including light commercial vehicles, micro-mobility, and low-speed industrial vehicles — represent a volume market where sodium-ion’s cost-per-kWh advantage over LFP is most commercially compelling. India and Southeast Asia are the primary target geographies for this sub-segment, where two- and three-wheeler electrification programs in 2024 and 2025 are actively evaluating sodium-ion packs.

Utility buyers overlap with Energy Utilities in practice, but this sub-segment specifically includes municipal and co-operative utility operators procuring smaller-scale community storage. These buyers often operate under tighter capital budgets than large grid operators, making sodium-ion’s lower upfront cost a more decisive purchase driver than it is for large utilities with established LFP procurement frameworks.

Market Segments Covered in the Report

By Product Type

- Sodium Sulfur Battery

- Non-Aqueous Sodium-Ion Batteries

- Aqueous Sodium-Ion Batteries

- Sodium-Oxygen (Sodium Air) Batteries

- Solid-State Sodium-Ion Batteries

- Carbon-Based Sodium-Ion Batteries

- Transition Metal Oxide Sodium-Ion Batteries

- Graphite Anode Sodium-Ion Batteries

- Layered Oxide Cathode Sodium-Ion Batteries

By Material Type

- Anode Materials

- Metal Oxides

- Porous Hard Carbon

- Cathode Materials

- Layered Metal Oxides

- Phosphate-based Polyanionic

- Prussian Blue Analogues

- Electrolytes

- Separators

- Current Collectors

By Application

- Electric Vehicles

- Consumer Electronics

- Stationary Energy Storage

- Residential Energy Storage

- Emergency Backup and UPS

- Telecommunications Systems

By End User

- Energy Utilities

- Independent Power Producers

- Automotive OEMs

- Transportation

- Utility

- Others

Sodium-ion Battery Market Regional Insights

Asia Pacific Dominates the Sodium-ion Battery Market with a Market Share of 44.5%, Valued at USD 846 Million

Asia Pacific holds 44.5% of the global sodium-ion battery market, valued at USD 846 million in 2025. China’s combination of state-backed manufacturing scale, active policy support, and a mature EV supply chain gives it structural control over this market. China commands 96% of global sodium-ion production capacity in 2025, meaning Asia Pacific’s regional dominance reflects a near-monopoly production position that no other region can credibly challenge before 2030.

North America Sodium-ion Battery Market Trends

North America is at an early but decisive moment in its sodium-ion development. The US commissioned its first grid-scale sodium-ion installation — a 3.5 MWh system at SolarTAC, Colorado — in September 2025. Natron Energy’s exit from its Holland, Michigan facility after committing over USD 363 million signals that domestic production economics remain challenging without sustained demand commitments from large industrial or utility buyers.

Europe Sodium-ion Battery Market Trends

Europe is investing in sodium-ion as a strategic response to critical mineral supply risk. Sweden’s Altris AB raised approximately USD 40 million in cumulative funding to develop Prussian Blue Analogue cathode materials. France’s TIAMAT is building a 5 GWh gigafactory in Amiens backed by over EUR 500 million in total investment. The EU’s battery regulation, which mandates supply chain transparency, is accelerating interest in lithium-free chemistries among European manufacturers.

Latin America Sodium-ion Battery Market Trends

Latin America’s sodium-ion activity is limited but growing alongside broader energy storage mandates. Brazil and Mexico — both expanding their renewable energy grids — are evaluating sodium-ion for stationary storage where lithium supply chain costs are high. India-based Reliance New Energy’s acquisition of Faradion for GBP 100 million (completed October 2024) may accelerate technology transfer to lower-cost manufacturing regions that serve Latin American buyers.

Middle East & Africa Sodium-ion Battery Market Trends

The Middle East and Africa region is at the earliest stage of sodium-ion engagement. Gulf Cooperation Council nations investing in renewable energy targets — particularly Saudi Arabia’s Vision 2030 grid diversification programs — are evaluating sodium-ion for utility-scale storage. High ambient temperatures in the region align well with sodium-ion chemistries that have demonstrated stable performance up to +70°C in commercial testing.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

China’s Ministry of Industry and Information Technology (MIIT) updated its battery industry standards in 2024 to include sodium-ion electrochemical performance criteria, covering cycle life, thermal safety, and capacity retention benchmarks. This formal inclusion accelerated OEM qualification timelines, allowing automotive manufacturers to use sodium-ion cells in type-approved vehicles without separate regulatory waivers.

The European Union’s Battery Regulation (EU) 2023/1542, which came into full enforcement in early 2024, mandates carbon footprint declarations and supply chain due diligence for batteries sold in the EU market. Sodium-ion chemistries that avoid cobalt, lithium, and conflict-prone minerals gain a compliance advantage under these rules, giving EU-focused vendors a regulatory reason to accelerate sodium-ion product development.

The US Department of Energy’s ARPA-E SCALEUP program provided USD 19.8 million in funding to Natron Energy’s sodium-ion production facility in Holland, Michigan — the first US regulatory and financial framework explicitly supporting domestic sodium-ion manufacturing at commercial scale. Though Natron later ceased operations, the program established a precedent for federal backing of sodium-ion production assets.

India’s FAME III electric vehicle subsidy framework, under development through 2024 and 2025, is expected to include sodium-ion battery packs as eligible for EV purchase incentives, removing a cost barrier for OEMs seeking to deploy sodium-ion cells in two- and three-wheeler vehicles. This regulatory inclusion would directly support Reliance Industries’ Faradion technology deployment plan at its Jamnagar gigafactory.

Drivers

CATL’s Mass-Producible Naxtra Battery and OEM Diversification Push Accelerate Sodium-Ion Commercialization

CATL’s launch of the Naxtra sodium-ion battery — reaching 175 Wh/kg energy density with operation from -40°C to +70°C and over 10,000 cycles — converted a research milestone into a production-ready product. Chinese automakers began commercial passenger EV deliveries using Naxtra packs in April 2024. This single event changed the market’s risk profile: OEMs could now specify sodium-ion without betting on unproven technology.

Rising lithium carbonate price instability in 2024 pushed automotive and storage procurement teams to actively test sodium-based supply alternatives. PRET, one of China’s most active sodium-ion suppliers to the two-wheel EV and storage markets, reported revenue of CNY 8.709 billion in 2023 — a 28.87% year-on-year gain — with net profit up 130.23%, showing that buyers were already redirecting spend before CATL’s full commercial launch. This profit surge shows sodium-ion is not just a backup option: it is becoming a primary procurement strategy for cost-conscious OEMs.

LG Chem and Sinopec jointly project China’s sodium-ion market to grow from 10 GWh in 2025 to 292 GWh by 2034. That 29x expansion in under a decade reflects not just technical adoption but a structural shift in battery procurement strategy across Asia. BYD reinforced this shift by launching construction of a 30 GWh annual-capacity sodium-ion factory in Xuzhou in January 2024, investing CNY 10 billion (USD 1.4 billion) — a capital commitment that signals BYD views sodium-ion as a core long-term product line, not an experimental hedge.

Restraints

Energy Density Gap Below LFP Benchmarks Limits Sodium-Ion’s Addressable EV Market

Commercial sodium-ion cells in 2024 remain below 200 Wh/kg, while advanced lithium iron phosphate (LFP) cells reach 240–260 Wh/kg. This gap directly limits the range achievable in a given vehicle weight budget. For passenger EVs targeting ranges above 400 km, sodium-ion requires a larger, heavier pack — adding cost that offsets the chemistry’s per-kWh price advantage. The technology is currently best suited to shorter-range urban vehicles and fixed storage where weight is not a constraint.

The energy density gap also affects grid storage economics. A sodium-ion system storing the same energy as an LFP system requires more physical space and more structural support. For constrained urban or rooftop deployments, this imposes a real estate cost premium. Vendors who cannot close the density gap to within 10–15% of LFP will find their addressable market limited to applications where space is not a constraint.

The collapse of Natron Energy’s US gigafactory plans underlines how commercial pressure can unwind even well-funded sodium-ion ventures. Natron abandoned its original USD 1.4 billion / 24 GWh North Carolina gigafactory and later ceased operations at its Michigan facility despite raising over USD 363 million in total funding. The company’s exit shows that technical feasibility alone does not create a viable business: sodium-ion vendors need committed offtake agreements before committing to large-scale production capex, not after.

Growth Factors

Grid-Scale Stationary Storage and Two-Wheeler EV Targets Open Near-Term Revenue Channels for Sodium-Ion Vendors

Grid-scale renewable integration projects in 2024 are using sodium-ion’s low-temperature stability and long cycle life to serve storage applications that LFP handles poorly. China’s 2024 policy cycle generated 37 new sodium-ion capacity construction projects totaling 179.5 GWh in just the first nine months of 2025 — already exceeding 70% of the full-year 2024 total — confirming that grid-connected demand is arriving faster than most market forecasts assumed. Each commissioned project also creates reference installations that reduce procurement risk for the next buyer.

India’s and Southeast Asia’s two- and three-wheeler EV markets are a structurally large and near-term opportunity. These vehicles require packs in the 1–5 kWh range, where sodium-ion’s cost advantage per kWh is most visible and range limitations are least important. Altris AB raised SEK 150 million (USD 14.5 million) in its Series B1 round in October 2024, with strategic investors Clarios and Maersk Growth specifically targeting low-cost EV and stationary storage applications — a clear signal that European capital is following demand toward the two-wheeler segment.

CATL’s R&D investment reached RMB 18.607 billion in FY2024, with cumulative R&D spending exceeding RMB 80 billion over the past decade and 43,354 patents and patent applications held worldwide as of end-2024. This IP base gives CATL the ability to shape the sodium-ion technology roadmap and lock competitors into licensing discussions. For vendors entering the sodium-ion market, competing directly against CATL’s IP portfolio requires either differentiated chemistry or a geographically protected market position.

Emerging Trends

Patent Race in Cathode Materials and Chinese Automaker Integration Signal Where Sodium-Ion Wins First

Increased 2024 patent filings in sodium-ion cathode materials — specifically Prussian Blue Analogues and layered oxides — in both China and Europe signal that the IP battleground is shifting from cell-level to material-level competition. Vendors who own the cathode IP own the cost structure. European players like Altris AB with its Prussian Blue cathode focus are pursuing a deliberate strategy to build defensible IP outside China’s manufacturing dominance. This trend will determine which companies can sustain margins as the market scales.

Chinese automakers integrating sodium-ion cells into commercial passenger EV models — announced in April 2024 — moved the technology from fleet pilots to mass-market products in a single announcement. CATL’s plan to deploy Naxtra cells across over 3,000 Choco-Swap battery swap stations in 140 cities creates a recurring replacement demand stream independent of new vehicle sales. Battery swap creates a captive installed base that drives stable revenue even in a competitive new vehicle market.

MWh-scale sodium-ion demonstration projects expanded rapidly across China during the 2024 policy cycle. China’s Nanning sodium-ion energy storage station — commissioned in May 2024 — distributed 10,000 kWh on its first operational day and cumulatively stored and released over 1.3 million kWh of green electricity by October 2025. Each completed installation becomes a reference site that shortens the procurement evaluation cycle for the next grid operator, compressing the timeline from demonstration to standard practice.

Sodium-ion Battery Market Key Companies Insights

Contemporary Amperex Technology Co. Limited (CATL) holds a structurally dominant position in this market. Its total revenue reached RMB 362 billion (~USD 52 billion) in FY2024, with net profit rising 15.01% year-over-year to RMB 50.745 billion (~USD 7 billion) — a profit gain driven partly by the shift toward higher-margin sodium-ion products. With 646 GWh of annual global production capacity, 13 production bases, and a February 2025 Hong Kong IPO filing targeting over USD 5 billion to fund overseas expansion, CATL can sustain sodium-ion R&D investment that no competitor outside China can match at equivalent scale.

Faradion Limited operates as a wholly-owned subsidiary of Reliance New Energy (India) following Reliance’s GBP 100 million (USD 135 million) acquisition, with completion of 100% ownership confirmed in October 2024. Reliance’s ownership gives Faradion access to one of India’s largest industrial capital bases, backing a planned 5 GWh annual sodium-ion cell-to-pack facility at the Dhirubhai Ambani Green Energy Giga Complex in Jamnagar, Gujarat. This positions Faradion as the primary non-Chinese sodium-ion manufacturer targeting India’s fast-growing EV and storage demand.

HiNa Battery Technology Co., Ltd delivered the world’s first 100 MWh sodium-ion energy storage project in June 2024 for Datang Group in Hubei Province. This installation — comprising 42 battery containers capable of storing 100,000 kWh in a single charge — established HiNa as the reference provider for utility-scale sodium-ion storage. The company also signed a 2024 contract to build a 50,000-ton cathode and anode material production base and plans a 10 GWh battery production expansion in 2025, positioning it to move from pilot supplier to volume manufacturer within two years.

Altris AB has raised approximately USD 40 million in total cumulative funding and secured strategic investment from Volvo Cars Tech Fund, Clarios, and Maersk Growth — investors with deep EV and commercial vehicle supply chain relationships. Its Prussian Blue Analogue cathode approach is a deliberate differentiation from China’s layered oxide and phosphate mainstream, targeting buyers who need a lithium-free AND cobalt-free AND China-independent supply chain. An additional 80.75 MSEK (~EUR 7.3 million) follow-on in early 2025 extended the company’s runway toward pilot production in Uppsala.

Key Companies

- Aquion Energy

- Faradion Limited

- HiNa Battery Technology Co., Ltd

- Ben’an Energy Technology (Shanghai) Co., Ltd

- AMTE Power plc

- Natron Energy, Inc.

- Tiamat Energy

- Jiangsu Zhongna Energy Technology Co., Ltd.

- Contemporary Amperex Technology Co. Limited (CATL)

- Li-FUN Technology Corporation Limited

- BLUETTI Power Inc.

- Indigenous Energy Storage Technologies Pvt. Ltd. (Indi Energy)

- Altris AB

- NEI Corporation

- Blackstone Technology GmbH

Recent Development

- November 2025 — Peak Energy signed a multi-year supply agreement with Jupiter Power covering up to 4.75 GWh of sodium-ion storage systems valued at potentially more than USD 500 million between 2027 and 2030, with the first phase delivering approximately 720 MWh in 2027 — the largest single US sodium-ion deployment announced to date.

- November 2025 — China’s Guangde Qingna Technology Co. signed an agreement for a 20 GWh sodium-ion battery production facility in Sichuan Province with a total investment of CNY 6 billion (USD 835.98 million), reinforcing Sichuan as a major hub for sodium-ion industrial development.

- February 2025 — CATL filed for a Hong Kong IPO aiming to raise over USD 5 billion (HKD 36.5 billion) to fund overseas factory expansion in Hungary and Spain; cornerstone investors included Sinopec, Kuwait Investment Authority, and Hillhouse Investment.

- April 2024 / September 2025 — Natron Energy raised USD 189 million in its Series F round in January 2024 and commenced commercial sodium-ion production at its Holland, Michigan facility — the first in the US — before ceasing all operations in September 2025; total cumulative funding exceeded USD 363 million.

- October 2024 — Reliance New Energy confirmed 100% ownership of Faradion Limited, incorporating the UK sodium-ion pioneer as a wholly-owned subsidiary following the original GBP 100 million acquisition; the integration positions Faradion’s technology for deployment at Reliance’s Jamnagar gigafactory.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.90 Billion |

| Forecast Revenue (2035) | USD 13.21 Billion |

| CAGR (2026-2035) | 21.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Sodium Sulfur Battery, Non-Aqueous Sodium-Ion Batteries, Aqueous Sodium-Ion Batteries, Sodium-Oxygen Batteries, Solid-State Sodium-Ion Batteries, Carbon-Based Sodium-Ion Batteries, Transition Metal Oxide Sodium-Ion Batteries, Graphite Anode Sodium-Ion Batteries, Layered Oxide Cathode Sodium-Ion Batteries), By Material Type (Anode Materials, Cathode Materials, Electrolytes, Separators, Current Collectors), By Application (Electric Vehicles, Consumer Electronics, Stationary Energy Storage, Residential Energy Storage, Emergency Backup and UPS, Telecommunications Systems), By End User (Energy Utilities, Independent Power Producers, Automotive OEMs, Transportation, Utility, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Aquion Energy, Faradion Limited, HiNa Battery Technology Co. Ltd, Ben’an Energy Technology (Shanghai) Co. Ltd, AMTE Power plc, Natron Energy Inc., Tiamat Energy, Jiangsu Zhongna Energy Technology Co. Ltd., Contemporary Amperex Technology Co. Limited (CATL), Li-FUN Technology Corporation Limited, BLUETTI Power Inc., Indigenous Energy Storage Technologies Pvt. Ltd. (Indi Energy), Altris AB, NEI Corporation, Blackstone Technology GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |