What is the Smart Power Distribution Systems Market Size?

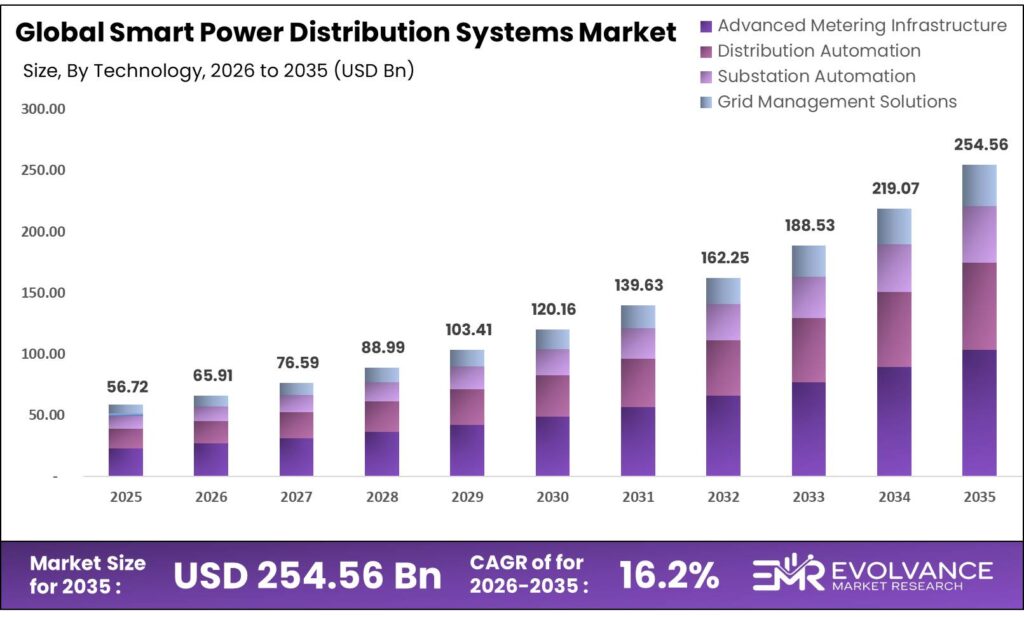

The Global Smart Power Distribution Systems Market size will be worth around USD 254.56 Billion by 2035 from USD 56.72 Billion in 2025, growing at a CAGR of 16.20% during the forecast period 2026 to 2035. National grid upgrade programs and utility-scale smart metering rollouts are the two sharpest demand engines pulling spend forward. Buyers are shifting from reactive maintenance models to digital monitoring contracts as grid reliability standards tighten globally. Supply-side pressure from transformer shortages and long equipment lead times could slow deployment timelines for large-scale projects.

Market Highlights

- The Smart Power Distribution Systems Market will grow from USD 56.72 Billion in 2025 to USD 254.56 Billion by 2035, at a CAGR of 16.20%

- North America leads with a 42.3% market share, valued at USD 24.90 Billion

- Advanced Metering Infrastructure (AMI) dominates the Technology Type segment with a 47.2% share

- On-Premise deployment holds a 67.4% share of the Deployment segment

- Hardware leads the Component segment with a 54.6% share

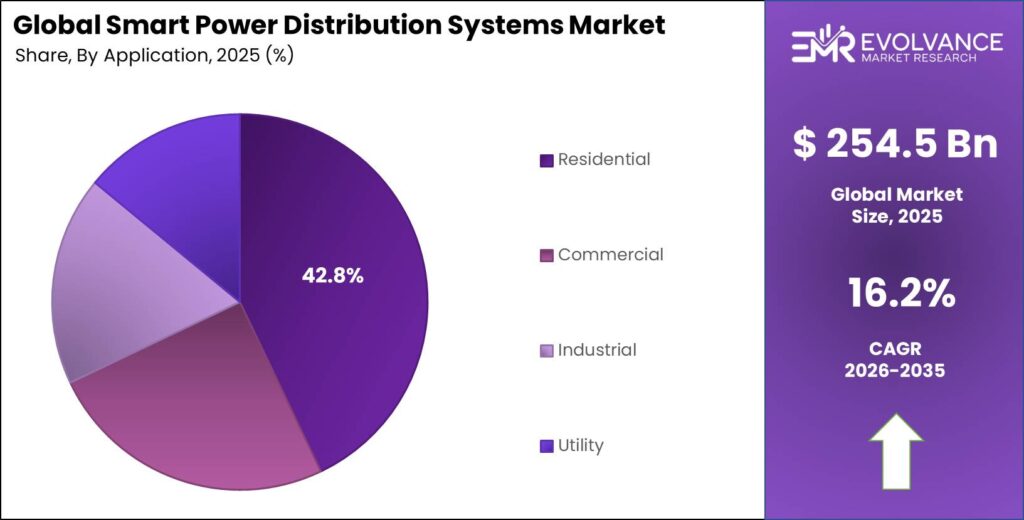

- Residential applications hold a 42.8% share of the Application segment

- Energy and Utilities is the top end-use vertical with a 39.7% share

Market Overview

Smart power distribution systems replace traditional analog grid infrastructure with digital monitoring, automated control, and real-time data analytics. These systems include smart meters, automated substations, sensors, distribution management software, and remote control units. Utilities and grid operators use them to reduce power losses, detect faults faster, and manage distributed energy sources more efficiently.

The core value proposition is control. Utilities that deploy these systems can monitor grid conditions at a granular level, respond to faults within minutes rather than hours, and integrate variable renewable energy without destabilizing supply. This shift from passive to active grid management is not incremental — it changes the operating model of distribution utilities from infrastructure managers to data-driven service providers.

Government investment is the primary demand accelerant for this market. India launched a ₹3.03 trillion ($36.8 billion) national power distribution upgrade scheme to strengthen grid networks and deploy smart meters across utilities nationwide. China allocated $442 billion for grid infrastructure in the 2021–2025 period. Japan created a ¥20 trillion fund for power grid upgrades. These are not pilot programs — they are structural commitments that create sustained multi-year procurement pipelines for vendors.

According to the International Energy Agency, approximately 75% of all digital grid spending globally targets electricity distribution systems through smart meters, sensors, automated substations, and digital monitoring tools. This concentration means that vendors serving the distribution layer — not transmission — are capturing the majority of global grid digitalization budgets. The implication is clear: distribution-focused product portfolios carry a structural revenue advantage over transmission-only players.

The IEA and industry trackers, global investment in electricity grids reached $359 billion in 2024, a 14% rise over the 2022–2023 average as governments scaled smart grid build-outs to absorb renewable energy capacity. This spending trajectory confirms that grid modernization is no longer discretionary. Utilities that delay smart distribution upgrades now face higher integration costs later as renewable penetration rises and legacy grid limits become binding constraints on energy system performance.

Technology Type Insights

Advanced Metering Infrastructure (AMI) dominates with 47.2% due to mass national meter rollout programs.

In 2025, Advanced Metering Infrastructure (AMI) held a dominant market position in the By Technology Type segment of the Smart Power Distribution Systems Market, with a 47.2% share. AMI leads because national governments have made smart metering a policy priority, not an option. India’s program targets deployment of approximately 250 million smart meters nationwide by 2025 to improve digital monitoring and distribution efficiency — a procurement scale that no other technology sub-segment can match. Utilities investing in AMI gain the data foundation needed to run demand forecasting, revenue loss detection, and dynamic pricing programs.

Distribution Automation serves utilities that need to isolate faults, reroute power, and restore supply without manual field intervention. The push for shorter outage durations — driven by regulatory penalties and customer pressure — is making automated switching and remote fault isolation commercially essential rather than optional upgrades. Utilities operating aging overhead networks are the primary buyers, particularly in North America and South Asia.

Substation Automation delivers the digital command layer that connects field devices to central control systems. Utilities modernizing high-voltage substations are integrating protection relays, communication gateways, and supervisory control systems to cut maintenance costs and enable remote operation. This sub-segment benefits directly from the trend toward centralized command control centers replacing manual substation staffing.

Grid Management Solutions sit at the software and analytics end of the technology stack. These platforms process meter data, outage reports, and sensor feeds to give operators a real-time operating picture of the distribution network. As smart meter deployments scale, the volume of distribution data grows faster than human operators can process manually — making grid management software a compulsory investment for any utility running a large AMI estate.

Deployment Insights

On-Premise dominates with 67.4% due to security and control requirements in critical infrastructure.

In 2025, On-Premise held a dominant market position in the By Deployment segment of the Smart Power Distribution Systems Market, with a 67.4% share. Utilities treat grid control systems as critical national infrastructure, and most regulatory frameworks require that operational data stay within utility-controlled environments. U.S. utilities alone spent $50.9 billion on electricity distribution infrastructure in 2023 — much of it hardware-intensive on-premise systems — confirming that capital-heavy, site-controlled deployments remain the industry standard. The cybersecurity risks associated with cloud-hosted operational technology reinforce this preference.

Cloud-Based deployment is gaining ground in analytics, billing, and customer-facing applications where real-time control is not required. Utilities and energy retailers are moving meter data management, demand forecasting, and revenue analytics to cloud platforms to reduce IT overhead and access scalable processing power. This creates a hybrid architecture — on-premise for control, cloud for analytics — that vendors able to serve both layers are best positioned to capture.

Component Insights

Hardware dominates with 54.6% due to large-scale physical grid equipment replacement cycles.

In 2025, Hardware held a dominant market position in the By Component segment of the Smart Power Distribution Systems Market, with a 54.6% share. Physical equipment — meters, sensors, controllers, and distribution boards — forms the foundation of every smart grid project. U.S. utilities invested $5.1 billion in smart meters and customer-side distribution equipment in 2023, a 25% increase compared with 2022, reflecting the pace at which analog devices are being replaced. Without hardware at the network edge, software and services have nothing to run on.

Circuit Monitors give operators real-time visibility into current, voltage, and power quality at panel and feeder level. They are the first device class utilities install when transitioning from manual reading to continuous grid monitoring. Their low unit cost and easy retrofit profile make them a high-volume, recurring product category across both new installations and system upgrades.

Smart Meters are the data collection endpoint for every AMI deployment. Beyond billing, they feed load profiles, tamper alerts, and outage notifications back to utility control systems. The scale of national meter programs in India, the U.S., and Europe means smart meter manufacturing capacity and supply chain logistics are now active bottlenecks shaping deployment timelines for utility programs.

Software covers the control logic, metering platforms, and analytics engines that process data from hardware deployments. The software layer creates recurring revenue through licensing and subscription contracts, which is why major vendors are pushing software attach rates on every hardware sale. Utilities that standardize on a single vendor’s software stack create significant switching costs — giving incumbent vendors strong revenue retention across upgrade cycles.

Protection and Control Software governs how the distribution network responds to faults, overloads, and switching commands. These systems operate at millisecond response times and directly affect grid reliability scores that regulators track. Utilities face financial penalties for exceeding outage duration limits, making protection software a non-discretionary purchase tied to compliance requirements.

Sensor and Analytics Software turns raw field data into operational insights — fault predictions, load forecasts, and asset health scores. This is where AI and machine learning are creating a competitive gap. Vendors embedding predictive analytics into their sensor platforms can demonstrate measurable reductions in outage frequency and maintenance costs, creating a clear return-on-investment case that accelerates procurement decisions.

Services in this market include consulting, installation, and ongoing maintenance contracts. As smart distribution systems grow in complexity, utilities increasingly rely on vendor-led services to manage rollouts and sustain system performance. This creates a recurring revenue stream that balances hardware’s lumpy capital cycle — and it is why major players like Siemens, Schneider, and ABB are building out managed services divisions alongside their product businesses.

Maintenance and Support contracts provide utilities with the technical resources to sustain smart distribution systems over their operational life. As these systems become embedded in grid operations, downtime carries regulatory and reputational risk — making multi-year maintenance contracts a standard procurement element rather than an optional add-on.

Application Insights

Residential dominates with 42.8% due to mass-scale national smart metering programs targeting household consumers.

In 2025, Residential held a dominant market position in the By Application segment of the Smart Power Distribution Systems Market, with a 42.8% share. National smart meter mandates are the structural driver here. When a government targets 250 million household meters or a utility deploys 4.3 million meters in a single city, the residential segment absorbs the majority of procurement volume. This segment’s dominance is policy-driven — not demand-led — which makes it more predictable but also more sensitive to changes in government program timelines.

Commercial applications cover office buildings, retail facilities, hotels, and data centers where energy cost management and power quality directly affect operating margins. Building managers are deploying smart distribution systems to monitor energy consumption at circuit level, identify waste, and meet corporate sustainability reporting requirements. This segment is growing as energy cost pressures and ESG disclosure rules create internal business cases independent of utility-mandated programs.

Industrial applications span manufacturing plants, refineries, and heavy processing facilities where power reliability is directly tied to production output. Industrial buyers prioritize fault detection speed and harmonic filtering — power quality problems that can damage sensitive equipment and halt production lines. Their procurement decisions are driven by downtime cost calculations, not energy efficiency targets, which means they tolerate higher upfront costs for proven system reliability.

Utility applications represent distribution network operators deploying smart systems across their entire grid footprint — from primary substations down to low-voltage network ends. This segment drives the highest average contract values because utility-scale deployments involve integrated system contracts covering hardware, software, communication networks, and multi-year support. A single national utility program can represent a billion-dollar procurement commitment.

End-use Insights

Energy and Utilities dominates with 39.7% due to regulatory mandates and national grid upgrade programs.

In 2025, Energy and Utilities held a dominant market position in the By End-use segment of the Smart Power Distribution Systems Market, with a 39.7% share. Power distribution operators face dual pressure: regulators demand higher reliability metrics while governments mandate smart meter deployment at national scale. This combination forces capital allocation into smart distribution upgrades regardless of internal financial priorities. The segment’s dominant share reflects this structural spending obligation — utilities are not choosing to invest, they are required to.

Manufacturing end-users are deploying smart distribution systems to cut energy costs, reduce unplanned downtime, and meet industrial energy efficiency standards. Modern manufacturing facilities run energy-intensive equipment on tight production schedules — any power quality event or unplanned outage translates directly into lost output and penalty costs. Smart distribution investments in this segment are justified on productivity grounds, not sustainability rhetoric.

Telecommunications operators depend on uninterrupted power for network infrastructure. Smart distribution systems protect critical loads, enable predictive maintenance on power supply units, and provide the real-time monitoring needed to meet network uptime commitments. As 5G infrastructure rolls out globally, the density and complexity of telecom power systems increases — expanding the addressable market for smart distribution solutions in this vertical.

Healthcare facilities prioritize power quality and continuity above all other facility systems. Hospitals and diagnostic centers run life-critical equipment on circuits that cannot tolerate voltage fluctuations or interruptions. Smart distribution systems with automatic load transfer and fault isolation are moving from optional upgrades to mandatory infrastructure investments as healthcare facility standards tighten globally.

Automotive end-users — particularly EV production plants and battery assembly facilities — require high-power, high-precision distribution systems capable of managing rapid load changes from robotic manufacturing equipment and high-voltage charging infrastructure. Smart distribution is becoming a core facility requirement for new automotive manufacturing investments, especially as EV production capacity expands globally.

Transportation infrastructure including rail networks, airports, and port facilities requires smart power distribution to manage complex multi-load systems across large geographic footprints. Electrification of rail and port operations is driving new procurement of smart distribution equipment capable of handling traction power, station loads, and electric vehicle charging simultaneously from a single integrated control platform.

Electronics manufacturing facilities operate high-sensitivity production processes that are vulnerable to power quality events. Semiconductor fabs, display panel plants, and PCB assembly lines invest in premium smart distribution systems with harmonic filtering and microsecond fault response. Power quality failures in these facilities cause product defects that cost multiples of the smart distribution investment required to prevent them.

Market Segments Covered in the Report

By Technology Type

- Advanced Metering Infrastructure (AMI)

- Distribution Automation

- Substation Automation

- Grid Management Solutions

By Deployment

- On-Premise

- Cloud-Based

By Component

- Hardware

- Circuit Monitor

- Smart Meters

- Sensors and Controllers

- Distribution Boards

- Others

- Software

- Protection & Control Software

- Programmable Logic Controllers (PLC)

- AMI Metering Software

- Sensor & Analytics Software

- Services

- Consulting

- Installation

- Maintenance & Support

By Application

- Residential

- Commercial

- Industrial

- Utility

By End-use

- Energy and Utilities

- Manufacturing

- Telecommunications

- Healthcare

- Automotive

- Transportation

- Electronics

- Others

Smart Power Distribution Systems Market Regional Insights

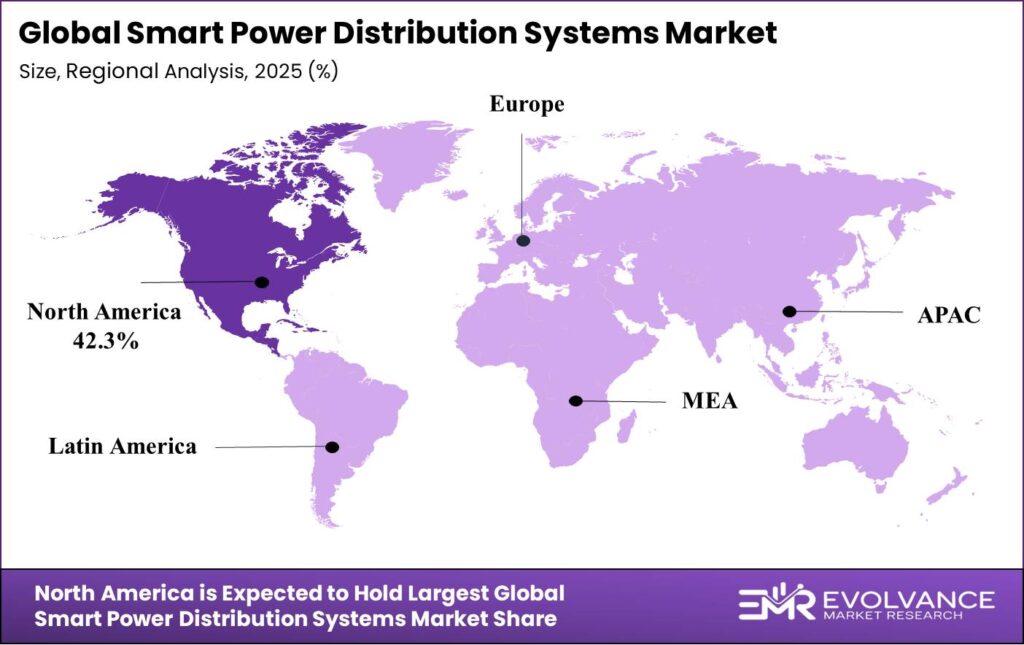

North America Dominates the Smart Power Distribution Systems Market with a Market Share of 42.3%, Valued at USD 24.90 Billion

North America holds 42.3% of the global market, valued at USD 24.90 Billion, because federal funding programs have made grid modernization a policy mandate backed by committed capital. The U.S. Department of Energy allocated $10.5 billion for grid upgrade programs including $3 billion for smart grid tech and $5 billion for grid innovation. This level of public investment creates a procurement environment that private utilities then match with their own capital spending — compounding the regional demand signal beyond what any single government program generates alone.

Europe Market Trends

Europe is advancing smart grid deployment through binding renewable energy targets and EU-mandated smart metering directives that require utilities to offer smart meters to all consumers. Western European utilities — particularly in Germany, France, and the UK — are running large-scale distribution automation programs to manage the high penetration of rooftop solar and wind generation across low-voltage networks. Regulatory penalties for poor reliability metrics and carbon reduction commitments jointly drive capital allocation decisions.

Asia Pacific Market Trends

Asia Pacific is the fastest-scaling region due to the sheer volume of national grid investment programs running concurrently across China, India, and Japan. China’s $442 billion grid infrastructure plan and India’s $36.8 billion distribution modernization scheme represent the two largest national smart grid commitments globally. The region’s growth is deployment-volume-driven — adding more smart meters, automated substations, and distribution sensors in absolute terms than any other region on the planet.

Latin America Market Trends

Latin America faces a dual challenge of expanding distribution access in underserved areas while modernizing legacy grid infrastructure in urban centers. Brazil and Mexico are the two primary markets, with utility regulators pushing smart metering pilots and distribution loss reduction programs. High technical and commercial distribution losses — in some markets exceeding 15% — create an economic case for smart distribution investments that reduces wasted energy and improves revenue recovery for utilities.

Middle East & Africa Market Trends

The Middle East is investing in smart grid infrastructure as part of broader national energy diversification programs. Gulf states are modernizing distribution networks to support solar energy integration and manage growing electricity demand from cooling, desalination, and urban development. Africa’s market is earlier stage, with investment concentrated in South Africa and selected national utility modernization programs in Nigeria, Kenya, and Egypt where grid reliability gaps create the sharpest investment case.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The U.S. Infrastructure Investment and Jobs Act directed $10.5 billion to electricity grid programs, with the Department of Energy administering smart grid, resilience, and grid innovation funding streams. By 2024, disbursements to utilities were accelerating, creating a formal compliance and procurement pipeline for smart distribution vendors tied to federal grant conditions including cybersecurity standards and interoperability requirements.

The European Union’s Energy Efficiency Directive, updated in 2023, requires member states to deploy smart meters to at least 80% of consumers by set national deadlines. EU network codes governing electricity distribution require utilities to meet defined reliability and power quality standards — creating a regulatory floor that makes smart distribution investments a compliance cost, not a discretionary choice for European network operators.

India’s Revamped Distribution Sector Scheme (RDSS), launched under the Ministry of Power in 2021 and actively funded through 2025, sets binding targets for smart prepaid meter installation, feeder separation, and distribution loss reduction. States must meet quarterly performance milestones to access central government grants — meaning utilities that delay smart distribution upgrades lose access to the ₹3.03 trillion funding pool that underpins India’s national grid modernization program.

China’s National Energy Administration issued smart grid standards in 2024 covering communication protocols, cybersecurity requirements, and interoperability specifications for distribution automation equipment. These standards effectively require foreign vendors entering the Chinese market to comply with domestic technical norms — raising barriers for non-compliant products while creating clear specifications that accelerate procurement decisions for compliant local and international suppliers.

Smart Power Distribution Systems Market Dynamics

Drivers

Government-Funded Smart Grid Programs Are Accelerating Distribution Digitalization at Scale

National governments are committing capital to smart grid programs at a pace that forces utility procurement cycles to accelerate. The U.S. Department of Energy allocated $10.5 billion for grid upgrade programs — including $3 billion for smart grid technologies and $5 billion for grid innovation — creating a federal demand signal that private utilities match with their own capital budgets. Vendors with proven deployments and federal procurement certifications have a structural advantage in this environment.

India’s National Smart Grid Mission is installing 1.69 lakh smart meters across pilot projects, building the operational template for the country’s full national rollout. In parallel, Tata Power Delhi Distribution deployed over 4.3 million smart meters integrated with GIS and SCADA systems — demonstrating at commercial scale that large urban utilities can absorb high-volume smart meter deployments without disrupting ongoing service. These reference cases reduce procurement risk for other utilities evaluating similar programs.

The Rajasthan Government allocated ₹700 crore for AMI deployment, GIS mapping, and AI analytics upgrades — representing one state’s contribution to India’s broader national distribution modernization effort. Moreover, this type of state-level spending is being replicated across multiple Indian states, creating a distributed procurement market that rewards vendors with the ability to service diverse regional utility requirements simultaneously rather than relying on a single large national contract.

Restraints

High Capital Costs and Technical Complexity Slow Smart Distribution Adoption Among Smaller Utilities

The full cost of reinforcing electricity distribution networks for large-scale electrification is estimated at between $320 billion and $720 billion in the United States alone. This scale of investment is accessible only to large, creditworthy utilities backed by regulatory rate recovery mechanisms. Smaller distribution companies and state-owned utilities in emerging markets face capital constraints that push smart grid upgrades down their priority list — limiting market penetration beyond the largest utility accounts.

Technical integration complexity adds a second barrier layer. Smart distribution deployments require simultaneous management of hardware installation, communication network build-out, software integration, and workforce training. Utilities that lack internal technical depth rely heavily on vendor-led services, which adds cost and creates implementation risk when rollout timelines slip. For smaller programs, this complexity can push total project costs well beyond initial budget estimates, leading to scope reduction or project delays.

Persistent technical and commercial power distribution losses across utility networks in developing markets further constrain investment capacity. Utilities with high loss rates generate lower revenue per unit of energy distributed — eroding the financial headroom needed to fund smart distribution capital programs. Until loss rates are brought under control through better billing and network management, the internal funding case for smart grid investment remains difficult to make at board level in many emerging market utilities.

Growth Factors

AI-Driven Grid Monitoring and Smart Electrification Technologies Are Opening New Revenue Streams

The integration of EV smart charging, heat pumps, and distributed solar into distribution networks is creating demand for advanced grid control that legacy systems cannot provide. Research shows that full electrification of U.S. housing and vehicles could require up to 544 gigawatts of additional distribution capacity nationally. Utilities that deploy smart distribution systems now are building the control infrastructure needed to manage this load growth — positioning themselves to avoid the most expensive grid reinforcement scenarios through active demand management.

Andhra Pradesh’s EPDCL deployed AI servers to detect faulty power poles using smartphone images captured by field technicians — a practical, low-cost application of computer vision that reduces inspection labor costs and catches faults before they cause outages. Additionally, the U.S. Department of Energy funded a $7.5 million program in 2024 to develop advanced grid analytics and sensor technologies for distribution reliability. These real-world deployments validate the commercial case for AI in distribution operations and signal growing utility willingness to fund AI-specific procurement programs.

Distribution automation components — ring main units, fault passage indicators, and remote terminal units — are being deployed in urban and semi-urban grids to enable section-level fault isolation without full feeder shutdowns. Utilities that deploy these components reduce customer outage minutes per year, directly improving regulatory performance scores. Vendors that bundle automation hardware with analytics software platforms can demonstrate compliance value alongside operational savings, strengthening their position in competitive procurement processes.

Emerging Trends

AI-Enabled Asset Inspection and Large-Scale Underground Cabling Are Reshaping Distribution Operations

AI-enabled distribution asset inspection using field images and sensor data has moved from research to operational deployment in Indian DISCOM networks since 2025. Utilities using these systems can identify equipment degradation, vegetation encroachment, and structural failures at scale without proportional increases in field staffing. This represents a shift in how distribution operators manage asset lifecycles — from scheduled inspection cycles to continuous condition monitoring driven by data rather than calendar.

GE Vernova recorded total orders of $44.1 billion in 2024, a 7% organic rise led by demand for power and electrification equipment. This order volume signals that the pipeline for grid equipment — including smart distribution hardware — extends well beyond the current fiscal year, giving vendors and supply chain partners the forward visibility needed to scale production. Consequently, companies able to secure long-term supply agreements with leading OEMs are better positioned to capture share as delivery timelines lengthen across the industry.

Large-scale programs for underground cabling in disaster-prone regions are building distribution networks that are structurally more resilient and operationally more compatible with digital monitoring systems. Underground cables are easier to instrument with sensors and more amenable to automated fault location than overhead lines. DGVCL’s expansion of underground high-tension cables to 6,906 km and ring main units to 1,698 units demonstrates that large utilities are committing to buried network architectures that inherently favor smart distribution system integration over legacy overhead infrastructure.

Key Companies Insights

Siemens competes in this market through its Smart Infrastructure division, offering integrated smart grid solutions covering substation automation, distribution management systems, and advanced metering platforms. Siemens’ strength is its end-to-end system capability — hardware, software, and services delivered under a single contract. This full-stack positioning gives it an advantage in large utility tenders where integration risk is a primary procurement concern for buyers evaluating multiple vendors.

Schneider Electric generated €2.5 billion ($2.7 billion) in revenue from its India operations alone in 2024, representing about 7% of the company’s global revenue and supported by 31 manufacturing facilities in the country. This local production scale gives Schneider a cost and delivery advantage in one of the world’s fastest-growing smart distribution markets. Its EcoStruxure grid management platform provides utilities with a software layer that connects physical grid assets to analytics and control applications — creating a recurring revenue stream on top of hardware sales.

ABB focuses on grid automation and electrification products including protection relays, switchgear, and distribution automation systems deployed by transmission and distribution utilities worldwide. ABB’s Ability platform integrates operational data from grid assets with predictive analytics — helping utilities move from reactive fault response to condition-based maintenance. Its global manufacturing footprint and established utility relationships make it a default shortlist participant in large national grid modernization tenders.

Eaton serves the smart distribution market through power management hardware and electrical systems targeting commercial, industrial, and utility customers. Its strength lies in the commercial and industrial segments where power quality, load management, and energy efficiency drive procurement decisions. The U.S. Department of Energy funded a $2.4 million project led by Southern Company Services to develop advanced communication and control technologies for distribution systems — reflecting the type of utility innovation program that creates new technology procurement cycles Eaton is well positioned to serve.

Key Companies

- Siemens

- Schneider Electric

- ABB

- Eaton

- Honeywell International Inc.

- Mitsubishi Electric Europe B.V.

- General Electric

- Itron Inc.

- Oracle

- Rockwell Automation

- Cisco Systems, Inc.

- Emerson Electric Co.

- Tech Mahindra Limited

- Landis+Gyr

- Hubbell

- Delta Electronics, Inc.

- Huawei Technologies Co., Ltd.

Recent Development

- March 2024 – India’s National Smart Grid Mission installed 1.69 lakh smart meters across pilot project sites, providing field-tested operational data to support the design of the country’s full national rollout program targeting hundreds of millions of meters.

- In 2024 – The U.S. Department of Energy invested $7.5 million in a program to develop advanced grid analytics and sensor technologies, targeting measurable improvements in electricity distribution system reliability and resilience through data-driven operations.

- In 2024 – GE Vernova recorded total orders of $44.1 billion, a 7% organic increase driven by strong demand for power and electrification equipment, signaling a multi-year forward pipeline for smart grid and distribution hardware across global markets.

- In 2026 – South Gujarat utility network expansion projects for underground cabling in disaster-prone regions are progressing through 2026, building buried distribution infrastructure that is structurally suited to sensor deployment and digital fault monitoring systems.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 56.72 Billion |

| Forecast Revenue (2035) | USD 254.56 Billion |

| CAGR (2026-2035) | 16.20% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology Type (Advanced Metering Infrastructure, Distribution Automation, Substation Automation, Grid Management Solutions), By Deployment (On-Premise, Cloud-Based), By Component (Hardware, Software, Services), By Application (Residential, Commercial, Industrial, Utility), By End-use (Energy and Utilities, Manufacturing, Telecommunications, Healthcare, Automotive, Transportation, Electronics, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Siemens, Schneider Electric, ABB, Eaton, Honeywell International Inc., Mitsubishi Electric Europe B.V., General Electric, Itron Inc., Oracle, Rockwell Automation, Cisco Systems, Inc., Emerson Electric Co., Tech Mahindra Limited, Landis+Gyr, Hubbell, Delta Electronics, Inc., Huawei Technologies Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |