What is the Smart Coating And Surface Chemical Market Size?

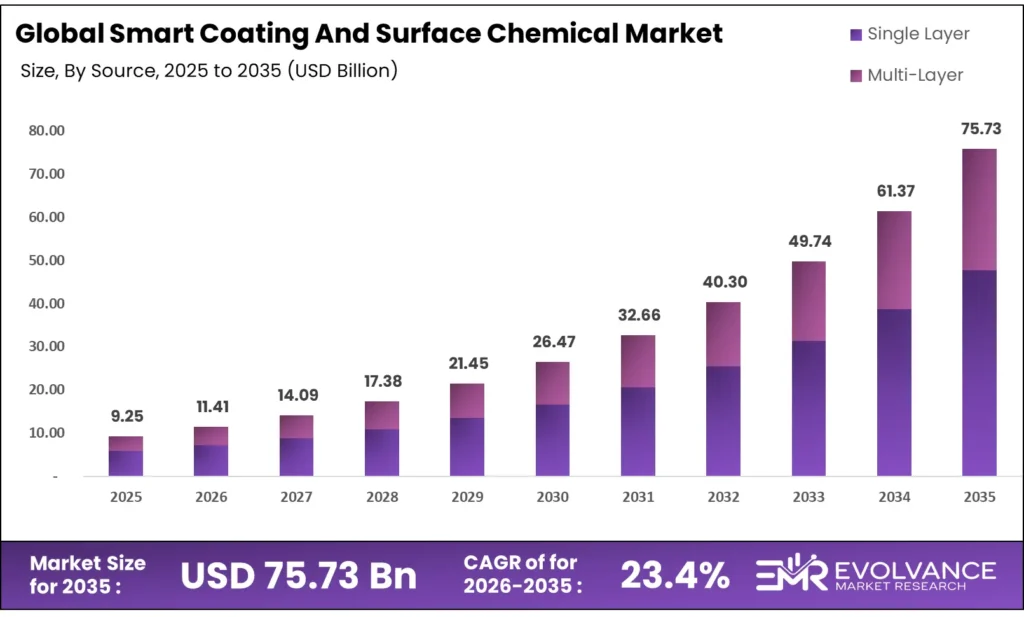

The Global Smart Coating And Surface Chemical Market size will be worth around USD 75.73 Billion by 2035 from USD 9.25 Billion in 2025, growing at a CAGR of 23.4% during the forecast period 2026 to 2035. Automotive OEM demand and defense-grade anti-corrosion needs are pulling spend into stimuli-responsive and self-healing formulations faster than most vendors planned. Enterprise buyers in construction and aerospace are shifting budget toward multi-functional coatings that cut long-term maintenance costs. Supply-side scale remains constrained by the technical complexity of nanotechnology-based formulations across diverse industrial substrates.

Market Highlights

- The Global Smart Coating And Surface Chemical Market valued at USD 9.25 Billion in 2025, reaching USD 75.73 Billion by 2035 at a CAGR of 23.4%.

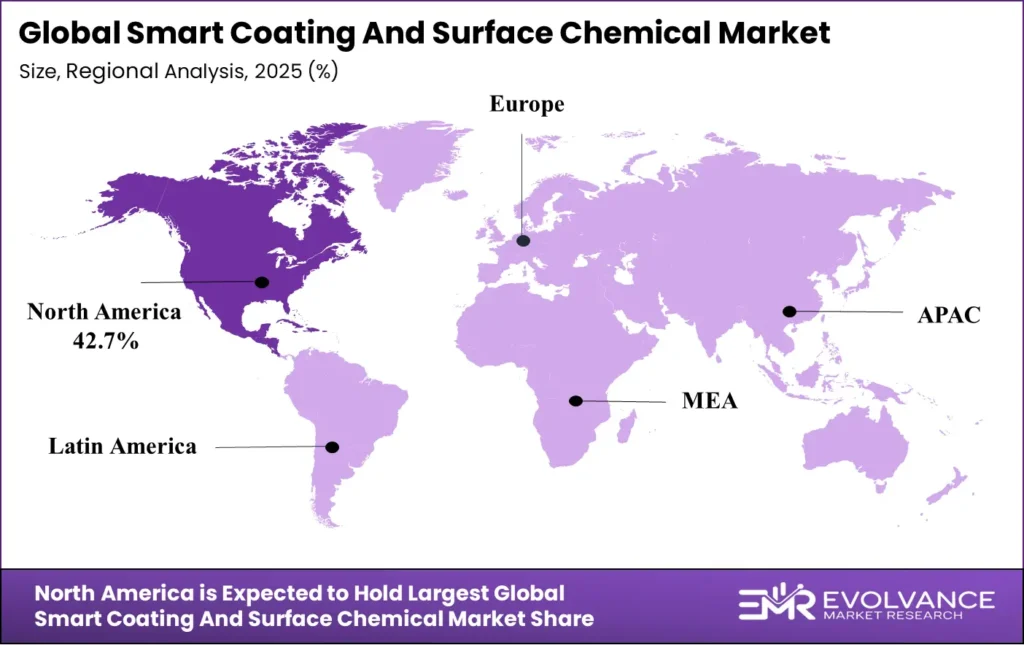

- North America leads with a 42.7% market share, valued at USD 3.9 Billion.

- By Product Type, Single Layer dominates with a 67.3% share.

- By Function, Anti-corrosion leads with a 34.1% share.

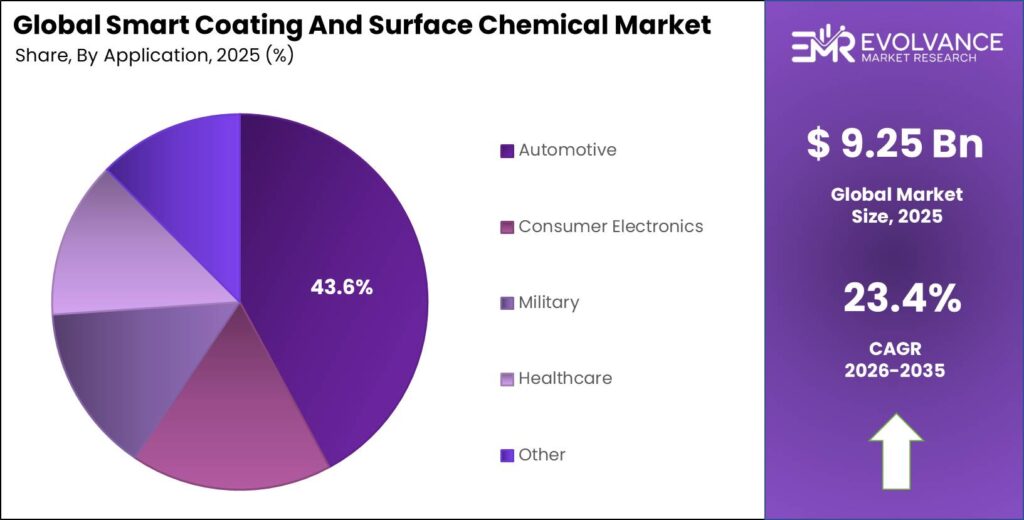

- By Application, Automotive holds a 43.6% share.

- By End-use, Building and Construction commands a 48.3% share.

Market Overview

The smart coating and surface chemical market covers advanced coatings that respond to external stimuli — heat, light, moisture, or mechanical stress — to deliver protective or functional changes on demand. These products span anti-corrosion barriers, self-cleaning films, antimicrobial surfaces, and dynamic color-shifting or electrochromic systems deployed across buildings, vehicles, ships, aircraft, and medical devices.

Unlike conventional paints, smart coatings carry engineered functionality. A self-healing automotive film recovers from scratches without manual work. A photocatalytic building facade breaks down pollutants under sunlight. This embedded intelligence is what commands price premiums and drives replacement of standard coatings in high-value assets where maintenance downtime is costly.

According to worldmetrics.org, automotive coatings accounted for 30% of global coatings demand, making it the single largest end-use segment. This confirms that automotive OEM and aftermarket channels are the primary proving grounds for smart coatings adoption — vendors who establish technical credibility there hold the strongest platform to expand into aerospace and healthcare.

Packaging coatings held a 22% share of global coatings demand. While packaging remains a volume-driven category, it signals an adjacent opportunity for antimicrobial and barrier smart coatings, particularly in food-grade and pharmaceutical supply chains where contamination risk carries regulatory penalties.

Government support is reinforcing adoption at scale. Aerospace bodies are mandating corrosion-resistant coatings to cut fleet maintenance costs. Urban infrastructure agencies in China and India are backing photocatalytic and smart road marking solutions to meet air quality targets. These regulatory and procurement signals are accelerating commercial rollout beyond the early-adopter phase in key regions.

Product Type Insights

Single Layer dominates with 67.3% due to lower cost and simpler production.

In 2025, Single Layer held a dominant market position in the By Product Type segment of the Smart Coating And Surface Chemical Market, with a 67.3% share. Single-layer systems offer manufacturers a faster path to commercialization because they require fewer deposition steps and lower capital investment per unit. Buyers across automotive and construction prefer them when a single functional property — corrosion protection or self-cleaning — is the primary requirement, making them the volume workhorse of this market.

Multi-Layer coatings serve applications where stacking two or more functional properties is non-negotiable. In high-value sectors like aerospace and marine, buyers accept the higher cost because a single coating that both blocks corrosion and resists ice accumulation reduces total system maintenance spend over an asset’s life. As nano-deposition equipment costs fall, multi-layer adoption will expand beyond premium niches into mid-tier industrial markets.

Function Insights

Anti-corrosion dominates with 34.1% due to scale of industrial infrastructure demand.

In 2025, Anti-corrosion held a dominant market position in the By Function segment of the Smart Coating And Surface Chemical Market, with a 34.1% share. Corrosion costs industrial operators billions annually in unplanned shutdowns and asset replacement. Smart anti-corrosion coatings that self-heal microcracks extend asset life without manual intervention — a direct productivity gain that justifies the premium over standard epoxy coatings. AkzoNobel’s ongoing self-healing and anti-corrosion advances for wind turbines illustrate how this segment is moving from R&D into active fleet deployment.

Anti-fouling coatings are critical for marine hulls and offshore structures where biofouling increases fuel consumption and triggers premature dry-dock cycles. As reported by worldmetrics.org, marine coatings held 7% of global coatings demand in 2022, and smart anti-fouling formulations command a disproportionately high share of value within that segment because the cost of fouling to fleet operators far exceeds the coating premium.

Color-shifting and electrochromic coatings are advancing from specialty automotive trim into functional building energy management. Miru Smart Technologies’ 2025 unveiling of a 1.5m x 1.6m dynamic electrochromic sunroof — one of the largest in the world, developed with Argotec/Mativ — shows that scale barriers are falling faster than the industry expected, opening architectural glazing as a near-term commercial channel.

Application Insights

Automotive dominates with 43.6% due to high-value asset protection and OEM mandates.

In 2025, Automotive held a dominant market position in the By Application segment of the Smart Coating And Surface Chemical Market, with a 43.6% share. OEM buyers prioritize coatings that protect high-value paint finishes while reducing dealership prep time and warranty claims. 3M’s August 2025 launch of next-generation self-healing Paint Protection Film and Performance Finish Ceramic Coating directly targets this cost pressure — giving installers a differentiated product and giving fleet operators a measurable maintenance saving.

Consumer Electronics demand surface coatings that resist fingerprints, moisture, and micro-abrasion without altering optical clarity. As device form factors shrink and display surfaces expand, coatings that maintain touch sensitivity while adding functional protection become a design constraint rather than an optional upgrade — pulling spend toward higher-performance smart formulations.

Military applications require coatings that meet stringent radar-absorbing, camouflage, and corrosion-resistance standards under extreme conditions. Defense procurement budgets are largely insulated from commercial cycle pressure, making military a stable and margin-rich channel for vendors with proven technical qualification records.

Healthcare surfaces face strict infection control standards that standard coatings cannot meet. Antimicrobial and photocatalytic smart coatings that actively neutralize pathogens — rather than just resisting adhesion — are entering hospital procurement specs as facility managers seek to reduce hospital-acquired infection rates and demonstrate regulatory compliance.

End-use Insights

Building and Construction dominates with 48.3% due to large asset base and sustainability mandates.

In 2025, Building and Construction held a dominant market position in the By End-use segment of the Smart Coating And Surface Chemical Market, with a 48.3% share. Building owners face tightening energy codes and sustainability ratings that reward facades capable of regulating heat gain, resisting pollution, and reducing maintenance cycles. Smart coatings address multiple compliance requirements in a single application, making them financially attractive versus traditional renovation approaches. Nippon Paint’s Walltron Advance thermal comfort solution in India reflects growing residential and commercial uptake in high-temperature urban markets.

Aerospace and Defense end-use covers both commercial aircraft and military platforms where coating failure carries safety consequences and regulatory consequences. PPG Industries’ 2025 presentations on total system coating solutions for aviation reinforce that large aerospace buyers are moving toward integrated smart coating programs rather than individual product purchases — a shift that favors vendors with full system capabilities.

Marine end-use spans commercial shipping, offshore energy, and naval vessels. Fuel efficiency pressure on shipping operators and environmental regulations restricting biocide use in traditional anti-fouling coatings are together creating demand for next-generation smart anti-fouling systems that combine mechanical and chemical protection without restricted substances.

Market Segments Covered in the Report

By Product Type

- Single Layer

- Multi-Layer

By Function

- Anti-corrosion

- Self-cleaning

- Anti-microbial

- Anti-fouling

- Anti-icing

- Color-shifting

- Others

By Application

- Automotive

- Consumer Electronics

- Military

- Healthcare

- Other

By End-use

- Building and Construction

- Aerospace and Defense

- Marine

- Others

Regional Insights

North America Dominates the Smart Coating And Surface Chemical Market with a Market Share of 42.7%, Valued at USD 3.9 Billion

North America holds a 42.7% share worth USD 3.9 Billion, driven by mature aerospace procurement, early EV adoption, and stringent EPA coating regulations that push OEMs toward advanced smart formulations. The U.S. defense budget consistently allocates spend for corrosion-resistant and radar-absorbing coatings, creating a stable high-margin revenue base that vendors in other regions cannot easily replicate.

Europe Market Trends

Europe is the second-largest market, driven by strong automotive OEM infrastructure in Germany and France and ambitious EU Green Deal building efficiency targets. Evolving REACH chemical regulations are pushing formulators to replace legacy solvents with low-VOC smart alternatives, creating a product upgrade cycle that benefits established chemical companies with compliant R&D pipelines already in place.

Asia Pacific Market Trends

Asia Pacific is the fastest-growing region, with China and India expanding smart infrastructure and EV production at scale. Nippon Paint’s 2024 revenue of USD 10.81 Billion reflects the depth of Asia Pacific coatings demand. Government smart city programs in China are directly funding photocatalytic and road-marking coating procurement, converting public infrastructure into a reliable commercial channel for smart coating vendors.

Latin America Market Trends

Latin America is an emerging market where construction growth in Brazil and Mexico is creating base-level demand for functional protective coatings. Smart coatings penetration remains low relative to standard paints, but rising awareness of lifecycle maintenance costs among commercial property developers is beginning to shift specification decisions toward higher-performance products in major urban centers.

Middle East & Africa Market Trends

The Middle East and Africa market is shaped by extreme climate conditions — high UV, salt spray, and sand abrasion — that accelerate asset degradation and create strong demand for corrosion-resistant and self-cleaning coatings in oil, gas, and infrastructure sectors. GCC nations investing in new smart city projects are also pulling demand for architectural smart glazing and energy-efficient facade coatings.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The U.S. Environmental Protection Agency updated its VOC emission limits for architectural coatings in 2025, tightening allowable solvent content for a broad range of product categories. These updates force reformulation across both standard and smart coating lines, creating near-term compliance costs but also accelerating the shift toward waterborne and low-VOC smart chemistries that already align with where the market is heading.

The European Union’s REACH regulation continues to restrict or evaluate dozens of coating chemicals, with new substance evaluations published through 2024 and 2025. REACH compliance now functions as a market access requirement for any coatings company selling into Europe, raising the barriers for smaller formulators and widening the competitive gap that established players with large compliance teams can exploit.

China’s Ministry of Ecology and Environment tightened VOC emission standards for industrial coatings under the 2024 industrial source pollution control framework. These rules are pushing Chinese OEM coating buyers toward smart, low-emission formulations faster than market forces alone would have driven. Vendors with compliant product lines ready at launch hold a clear first-mover advantage in China’s large automotive and construction segments.

IMO anti-fouling regulations continue to restrict biocide use in marine coatings, with the review cycle for tributyltin alternatives advancing through 2024–2025. Shipowners face mounting pressure to replace legacy anti-fouling systems with smart alternatives that meet IMO standards, creating a regulatory-driven replacement cycle across commercial and naval fleets globally.

Smart Coating And Surface Chemical Market Dynamics

Drivers

Self-Healing and Ceramic Coating Launches Push Automotive OEM Adoption of Smart Surface Systems

Automotive OEMs and aftermarket buyers are replacing standard paint protection products with smart coatings that reduce ownership costs over the vehicle’s life. 3M’s August 2025 launch of next-generation self-healing Paint Protection Film and Performance Finish Ceramic Coating targets both new vehicle finish protection and the fast-growing detailing services market, putting proven technology in front of millions of end buyers.

According to worldmetrics.org, automotive coatings accounted for 30% of global coatings demand in 2022. This baseline volume signals that even modest smart coating penetration into the automotive channel represents billions in addressable revenue. Vendors with automotive-qualified smart products hold a structurally stronger position than those relying solely on industrial channels.

Moreover, the EV platform shift is creating new coating requirements at the battery and chassis level. PPG Industries’ 2025 presentations on total system solutions for luxury EVs show that smart coatings are entering vehicle design specs — not just aftermarket add-ons — which pulls adoption much earlier in the product development cycle and locks in preferred supplier relationships with OEMs.

Restraints

High Production Costs and Technical Scale Barriers Slow Nanotechnology Coating Commercialization

Scaling nanotechnology-based and stimuli-responsive smart coatings from lab formulations to industrial volumes is technically demanding. Maintaining consistent nanoparticle dispersion, substrate adhesion, and functional response across large production runs requires precision equipment and quality controls that small and mid-size coating manufacturers cannot easily afford or staff.

Fragmented regulatory compliance across geographies compounds this cost pressure. A product that meets EPA VOC limits in the U.S. may require reformulation to satisfy EU REACH criteria or China’s 2024 industrial VOC standards. Each market-specific reformulation adds to R&D spend and delays commercialization timelines — costs that smaller players cannot absorb as easily as global majors with dedicated regulatory affairs teams.

Consequently, high technical and compliance costs are concentrating smart coating supply among a small number of well-capitalized incumbents. This market structure limits competition on price and slows the cost reduction curve that would otherwise accelerate adoption among mid-market industrial buyers who cannot yet justify smart coating premiums over standard alternatives.

Growth Factors

Electrochromic and Photocatalytic Coating Expansion Opens New Revenue Streams in Buildings and Transport

Electrochromic window coatings are entering commercial scale. Miru Smart Technologies’ 2025 commercial orders for dynamic electrochromic sunroofs — built in partnership with Argotec/Mativ — signal the transition from prototype to production. Miru’s recognition as a 2025 World Economic Forum Technology Pioneer adds institutional credibility that accelerates adoption by risk-averse architectural and automotive procurement teams.

Photocatalytic coatings for healthcare and sustainable buildings are attracting both regulatory support and corporate sustainability investment. AkzoNobel’s healthcare coating launches in 2025 and Saint-Gobain’s photocatalytic product development reflect that major players are treating antimicrobial and air-purifying coatings as a distinct growth category — not an add-on to existing lines.

Additionally, solar energy applications are emerging as a credible volume channel. SunDensity’s NSF-supported photonic smart coatings for solar panels convert surface treatment into an efficiency multiplier — a proposition that resonates with solar farm operators under pressure to maximize output per square meter. As reported by worldmetrics.org, industrial machinery coatings held 15% of the global coatings market in 2022, confirming broad industrial appetite for surface solutions with productivity benefits.

Emerging Trends

IoT-Enabled and Responsive Coatings Reframe Surface Protection as a Real-Time Data Asset

Coatings embedded with sensors or responsive chemistries are moving from research labs into pilot deployments in bridge infrastructure, pipelines, and wind turbines. These systems do not just protect — they report. A coating that signals crack formation or corrosion onset before failure gives asset owners the ability to schedule maintenance proactively, cutting unplanned shutdown costs that often exceed the coating investment many times over.

Sustainability is driving product design, not just marketing. BASF’s ChemCycling program in automotive refinish — introduced in September 2024 — uses chemically recycled feedstocks to produce coatings with the same technical performance as virgin-material products. This approach gives buyers a verified circular economy claim without the performance trade-off that has historically limited bio-based coating adoption in demanding applications.

Furthermore, self-healing polymer and ceramic systems are defining a new product standard in automotive and industrial protection. Industry focus on reducing maintenance cycles — highlighted by 3M’s 2025 PPF advancements — signals that buyers now expect coatings to recover from minor damage rather than degrade to failure. Vendors who cannot offer self-healing functionality will face increasing pressure in premium specification rounds as the technology becomes more widely qualified.

Key Companies Insights

3M anchors its smart coating position in the automotive channel through verified performance technology. Its August 2025 launch of next-generation self-healing Paint Protection Film and Performance Finish Ceramic Coating targets OEM and detailing markets with products that measurably cut maintenance costs — a concrete value proposition that resonates with fleet buyers and consumer-facing installers alike. 3M’s distribution scale and brand trust in surface protection give it a structural advantage over smaller specialty formulators entering the same channel.

BASF SE leverages its integrated chemicals platform to build smart coating formulations from proprietary raw material supply, giving it cost control that pure-play coating companies lack. BASF’s coatings division revenue reached USD 4.78 Billion in 2024. Its ChemCycling initiative in automotive refinish, launched in September 2024, directly addresses growing OEM sustainability mandates — positioning BASF as the supplier that can meet both performance specs and corporate ESG reporting requirements in a single product line.

AkzoNobel N.V. is building a dual-front smart coatings strategy covering both industrial anti-corrosion and healthcare antimicrobial segments. Its ongoing self-healing coating advances for wind turbines address the energy sector’s need to cut blade maintenance costs, while its 2025 healthcare launches target a segment where antimicrobial performance is a regulatory requirement rather than a selling point. AkzoNobel’s 2024 revenue reached USD 11.99 Billion, with the announced merger with Axalta creating a combined entity targeting USD 17 Billion in annual revenue.

PPG Industries, Inc. generates the deepest smart coating revenue exposure across automotive, aerospace, and industrial channels simultaneously. Its performance coatings segment generated USD 2.92 Billion in Q3 2024 revenue, supported by aerospace coatings demand — the channel most directly tied to smart coating premiums. PPG’s 2025 total system EV coating presentations show it is actively designing smart coating into the next generation of electric vehicle platforms rather than waiting for aftermarket pull.

Key Companies

- 3M

- BASF SE

- AkzoNobel N.V.

- Axalta Coating Systems LLC

- DuPont

- Hempel AS

- Jotun Group

- NEI Corporation

- PPG Industries, Inc.

- RPM International Inc.

- The Sherwin-Williams Company

Recent Development

- In January 2026, Mativ Holdings, Inc. announced an equity investment into Miru Smart Technologies to deepen their strategic partnership and prepare for commercial production of dynamic electrochromic window (eWindow) technology targeting automotive markets.

- In March 2025, Miru Smart Technologies and Argotec (Mativ brand) unveiled one of the world’s largest compound-curved electrochromic sunroof windows measuring 1.5 m × 1.6 m for automotive panoramic glazing applications, offering dynamic tinting, solar heat control, and enhanced energy efficiency.

- In October 2024, Miru Smart Technologies and Mativ (via Argotec brand) entered a joint development agreement to commercialize a novel lamination interlayer for dynamic electrochromic windows (eWindows) using advanced polymer films.

- In December 2025, Qlayers and Aramco signed an MoU to collaborate on deployment of next-generation coating automation (smart coating innovation) for storage tanks in the oil & gas sector, aligned with Saudi Vision 2030.

- In January 2025, Miru Smart Technologies partnered with Glaston to accelerate development and production of dynamic electrochromic eWindow technologies by integrating glass processing expertise.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 9.25 Billion |

| Forecast Revenue (2035) | USD 75.73 Billion |

| CAGR (2026-2035) | 23.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Single Layer, Multi-Layer), By Function (Anti-corrosion, Self-cleaning, Anti-microbial, Anti-fouling, Anti-icing, Color-shifting, Others), By Application (Automotive, Consumer Electronics, Military, Healthcare, Other), By End-use (Building and Construction, Aerospace and Defense, Marine, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | 3M, BASF SE, AkzoNobel N.V., Axalta Coating Systems LLC, DuPont, Hempel AS, Jotun Group, NEI Corporation, PPG Industries Inc., RPM International Inc., The Sherwin-Williams Company |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |