What is the Shampoo Market Size?

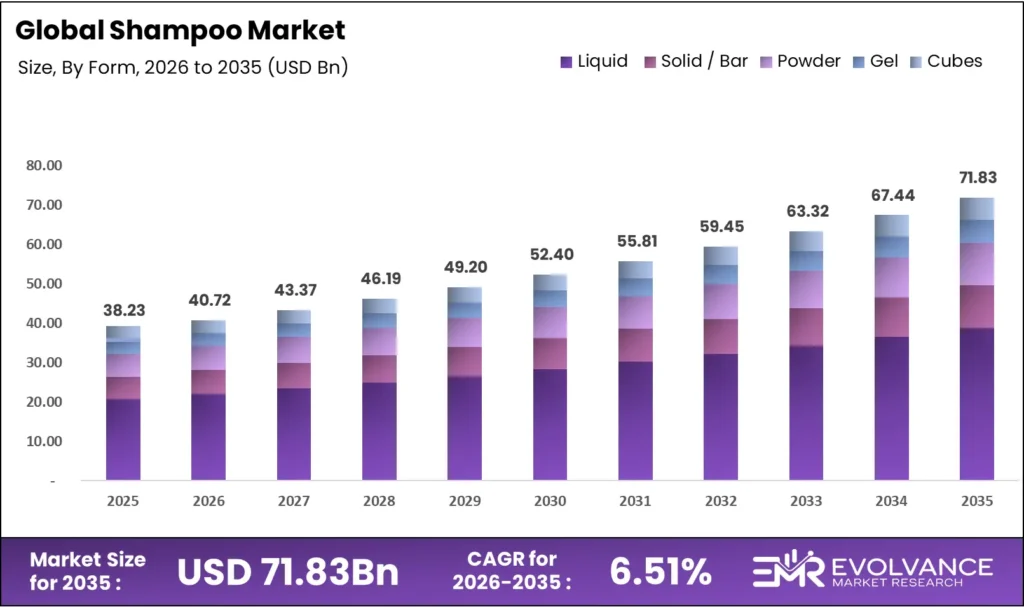

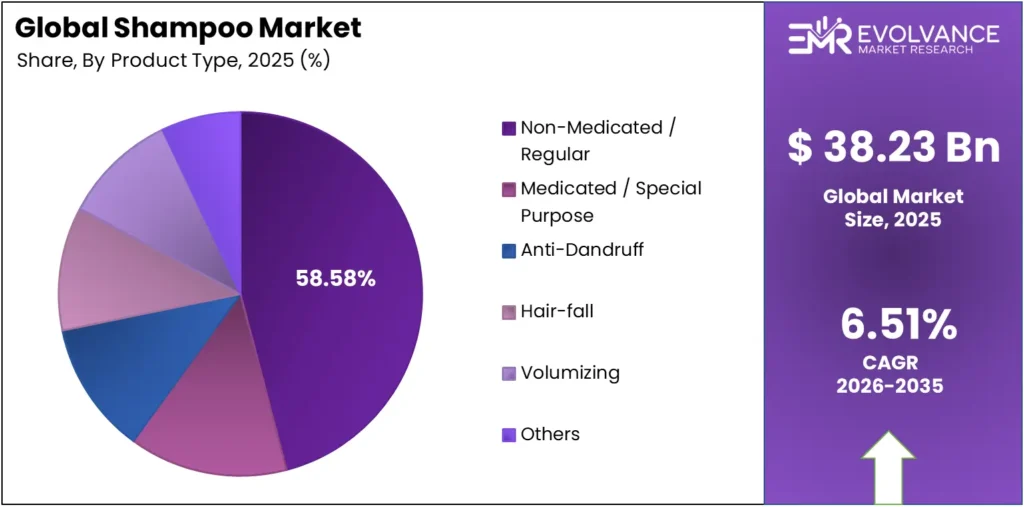

The global shampoo market will reach USD 71.83 billion by 2035 from USD 38.23 billion in 2025, growing at a CAGR of 6.51% during the forecast period 2026 to 2035. Premiumization and scalp-health innovation push mid-single-digit growth across both mass and prestige channels globally. Asia Pacific anchors demand with 39.8% revenue share, while North America and Europe sustain premium-tier consumption at above-average price points.

Market Highlights

- The global shampoo market was valued at USD 38.23 billion in 2025 and will reach USD 71.83 billion by 2035 at a CAGR of 6.51%.

- By product type, Non-Medicated / Regular shampoos hold 58.58% revenue share — driven by daily-use frequency across household and mass-market channels.

- Asia Pacific leads all regions with 39.8% revenue share and a market value of USD 15.21 billion in 2025.

- Women account for 66.89% of global shampoo revenue — the largest end-user segment by a margin that reflects both purchase frequency and basket size.

- Hypermarkets and supermarkets control 62.15% of distribution — confirming that physical retail remains the dominant shampoo purchase channel despite e-commerce expansion.

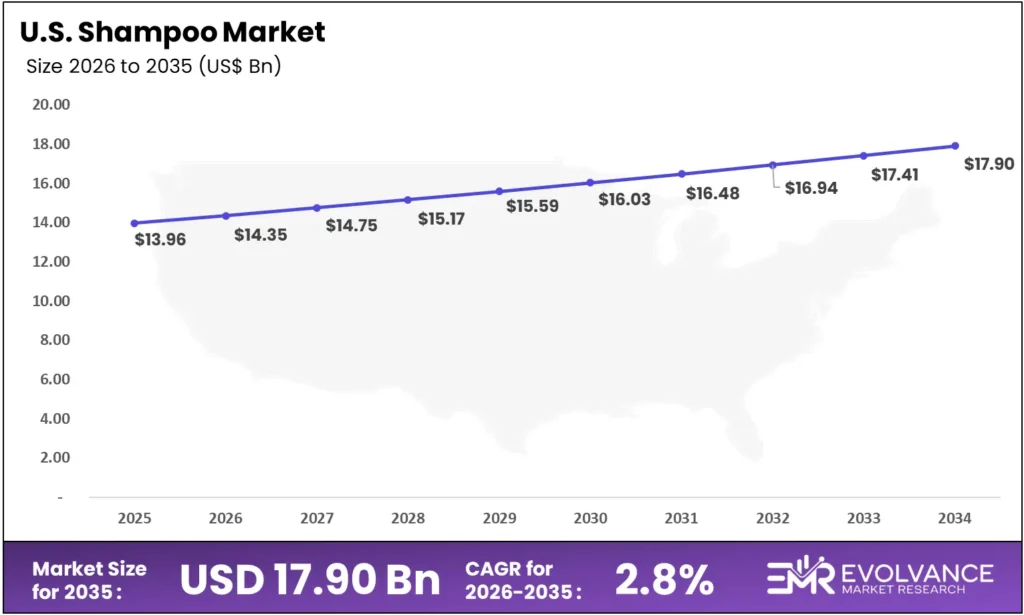

- The United States shampoo market was valued at USD 13.96 billion in 2025, growing at 2.80% CAGR to reach USD 17.90 billion by 2035.

Market Overview

The shampoo market covers all rinse-off hair cleansing products — from everyday non-medicated formulas to clinically positioned anti-dandruff, bond-repair, and scalp-treatment shampoos. The market serves household consumers, professional salon operators, and institutional buyers across hotels, spas, and health facilities in every major geography worldwide.

This analysis draws on primary data gathered from company filings, regulatory disclosures, and trade body reports across 5 global regions and 8 distinct market segments. Evolvance Market Research analysts found that data discrepancies between competing market sizing reports — ranging from USD 34.1 billion to USD 38.23 billion — stem from differing base-year scopes and segment definitions, not measurement error. Buyers using this report can rely on the USD 38.23 billion figure as the most current and scope-complete baseline available.

Shampoo addresses the universal need for scalp hygiene and hair condition maintenance — a need that does not compress during economic downturns, giving the market structural resilience few personal care categories match. Brand managers, retail category buyers, salon procurement managers, hotel supply directors, and private equity analysts tracking personal care acquisition targets all use shampoo market data to drive capital and inventory decisions.

Major FMCG operators reported strong category performance in 2025. According to L’Oréal’s 2025 annual results, L’Oréal H1 2025 operating profit reached EUR 4,740.1 million — representing 21.1% of sales, up 30 basis points versus H1 2024. Unilever posted an underlying operating margin of 20.0% in 2025, backed by EUR 670 million in cumulative productivity savings. Procter & Gamble’s core earnings per share reached USD 6.83 in fiscal 2025, up 4% year-on-year.

Product Type Analysis

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Non-Medicated / Regular | 58.58% | Daily-use frequency across household channel |

| Anti-Dandruff | — | Dermatology-positioned mass-market demand |

| Hair-fall | — | Rising consumer awareness of trichology |

| Volumizing | — | Styling outcome combined with cleanse |

| 2-in-1 | — | Convenience-driven repeat purchase |

| Anti-Frizz | — | Humidity-sensitive markets in Asia and LatAm |

| Bond Repair | — | Premium positioning via ingredient science |

| Everyday | — | Entry-level volume driver in emerging markets |

Non-Medicated / Regular shampoos dominate with 58.58% revenue share — driven by daily cleansing frequency across household and mass-market channels globally.

In 2025, Non-Medicated / Regular shampoos held a dominant market position in the By Product Type segment of the shampoo market, with a 58.58% share. This dominance reflects purchase behavior: most consumers use shampoo three to five times per week as a routine hygiene step, not a treatment decision. Mass-market brands like Head & Shoulders, Pantene, and Dove anchor this segment with hero SKUs that drive repeat purchase at accessible price points.

Medicated and special-purpose sub-segments — including Anti-Dandruff, Hair-fall, and Bond Repair — collectively represent the fastest-growing product tier within the category. Clinically positioned launches from CeraVe, Pantene Abundant & Strong, and prestige brands attract consumers willing to pay a premium for dermatology-adjacent claims, compressing the share gap with regular shampoos over the forecast period to 2035.

Form Analysis

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Liquid | 54.09% | Consumer familiarity and salon compatibility |

| Solid / Bar | — | Eco-packaging and travel convenience demand |

| Powder | — | Emerging waterless format in Asia Pacific |

| Gel | — | Styling-adjacent cleanse for men’s segment |

| Cubes | — | Novelty and D2C positioning |

Liquid shampoo dominates with 54.09% revenue share — underpinned by universal consumer familiarity and compatibility with salon dispensing systems.

In 2025, liquid shampoo held a 54.09% revenue share across the By Form segment. Liquid format benefits from decades of consumer conditioning, full compatibility with professional salon back-bar systems, and the broadest retail shelf presence across every distribution channel — advantages that solid and powder formats cannot yet match at scale despite their sustainability appeal.

Solid and bar shampoos represent the most disruptive non-liquid format, gaining shelf space at Unilever, L’Oréal, and independent D2C brands targeting organic hair care sustainability-conscious buyers. Water-activated formats like Gemz — launched by Procter & Gamble in November 2025 after 14 years of R&D — signal that formulation science is closing the performance gap between liquid and solid alternatives.

Application Analysis

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Household | 59.05% | Daily personal use and family purchase cycles |

| Commercial (Salons, Hotels, Spas) | — | Back-bar volume contracts and guest amenity supply |

| Professional Use | — | High-concentration formulas for treatment services |

Household application leads with 59.05% revenue share — reflecting the category’s foundation in daily personal use rather than institutional procurement.

In 2025, household application held 59.05% of the shampoo market by application. Individual consumers buying for personal and family use generate the category’s volume base — frequent low-value transactions that aggregate into a structural majority no commercial channel can displace at current penetration rates.

The commercial channel — covering salons, hotels, and spas — represents the highest-margin application segment for manufacturers because institutional buyers purchase in bulk at contracted rates, reducing distribution cost per unit. The professional salon shampoo market within this channel gives premium brands like Kérastase and Schwarzkopf Professional a credentialing platform that supports full-price retail sell-through.

Distribution Channel Analysis

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Hypermarkets / Supermarkets | 62.15% | High footfall and cross-category basket buying |

| Online Stores | — | Subscription models and D2C brand scaling |

| Drug Stores / Pharmacy | — | Medicated and dermatology-positioned shampoo demand |

| Specialty Beauty Stores | — | Premium and prestige brand discovery |

| Convenience Stores | — | Sachet and travel-size impulse purchase |

| Social Commerce | — | TikTok Shop-driven impulse and influencer conversion |

| Mass Merchandiser | — | Value-pack and private-label volume |

| Mono-Brand Stores | — | Brand immersion and hero SKU focus |

| Departmental Stores | — | Prestige gifting and premium discovery |

Hypermarkets and supermarkets lead with 62.15% share — anchored by high footfall, cross-category basket buying, and mass-brand shelf dominance.

In 2025, hypermarkets and supermarkets controlled 62.15% of global shampoo distribution revenue. Physical retail’s majority position reflects shampoo’s impulse and habitual repurchase nature — consumers buying shampoo alongside groceries during weekly shop cycles, where shelf placement and price promotion convert reliably at scale.

The e-commerce shampoo market represents the fastest-growing distribution channel, driven by subscription refill models, D2C brand launches, and TikTok Shop-powered social commerce converting influencer discovery into direct purchase. Online channels remove shelf-space barriers for independent premium brands. This structural shift is gradually compressing the hypermarket share advantage that Procter & Gamble and Unilever have held for decades.

End-User / Demographics Analysis

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Women | 66.89% | Higher wash frequency and multi-product routine |

| Men | — | Grooming category expansion and premium adoption |

| Kids / Toddlers / Infants | — | Tear-free and gentle formulation preference |

Women account for 66.89% of global shampoo revenue — reflecting higher wash frequency, longer hair care routines, and greater product variety across the women’s segment.

In 2025, women held a 66.89% revenue share in the shampoo market’s By End-User segment. Women wash hair more frequently than men on average, purchase across a wider range of product types — from everyday to bond-repair and scalp-treatment — and drive the premium tier through willingness to pay for ingredient-specific claims backed by clinical positioning.

Men’s shampoo market growth is the most strategically important demographic shift in the category. Male consumers are trading up from generic 2-in-1 formats into dedicated scalp-care and hair-fall shampoos, with brands like American Crew, Beardo, and Man Matters accelerating premiumization in men’s hair care a segment that large FMCG players have historically underinvested in. The baby shampoo market sustains steady volume through tear-free and sulfate-free formulation standards that parents treat as non-negotiable purchase criteria.

Hair Type Analysis

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Straight Hair | 35.99% | Population-dominant hair type in Asia Pacific |

| Dry & Damaged Hair | — | Heat styling and chemical treatment prevalence |

| Oily Hair | — | Scalp microbiome concern driving specialist formulas |

| Curly / Wavy Hair | — | Natural hair movement and co-wash routine growth |

| Color-Treated Hair | — | Salon color service frequency and protection demand |

| Textured Hair | — | Black hair care market expansion and representation |

| Normal Hair | — | Everyday maintenance at mass-market price points |

Straight hair leads with 35.99% revenue share — a direct reflection of its dominance as the most prevalent hair type across Asia Pacific, the world’s largest shampoo market.

In 2025, straight hair held a 35.99% revenue share within the By Hair Type segment of the shampoo market. Asia Pacific’s population size — anchoring 39.8% of global shampoo revenue — means that straight hair’s regional prevalence translates directly into a structural majority at the global level, a dynamic that will persist through the 2035 forecast horizon.

Dry and damaged hair and color-treated hair sub-segments are growing faster than any other hair type category. Heat tool adoption, salon chemical services, and the bond-repair product trend — led by Olaplex and expanding into mass-market via L’Oréal — are creating a clinically-motivated buyer cohort willing to pay premium prices for measurable damage protection. Black hair care industry statistics confirm that textured hair remains the most underserved segment relative to its population size.

Price Point Analysis

Medium price point leads the shampoo market by purchase frequency and volume.

| Sub-segment | Primary Driver | Key Brands / Examples |

|---|---|---|

| Medium | Broadest consumer accessibility and brand reach | Pantene, Dove, Garnier, Herbal Essences |

| Low / Mass | Price sensitivity in emerging markets and sachet formats | Sunsilk, Meera, Nyle Naturals |

| High / Premium / Luxury | Ingredient transparency and clinical positioning | Olaplex, Kérastase, Oribe |

| Ultra-Premium | Prestige rituals and salon-exclusive distribution | Sienna Naturals, Ouai, Living Proof |

Technology / Method Analysis

AI-Driven Personalization leads shampoo technology adoption as brands move from one-size-fits-all formulas to data-informed scalp diagnostics.

| Sub-segment | Primary Driver | Key Application |

|---|---|---|

| AI-Driven Personalization | Consumer demand for custom scalp and hair solutions | Prose, Function of Beauty, brand diagnostics tools |

| Microbiome-Based Formulation | Scalp health science and dermatology adjacency | Prebiotic and postbiotic shampoo launches |

| Scalp Analysis Tools | AI diagnostic devices at salon and retail touchpoints | In-salon scalp camera systems |

| IoT-Connected Devices | Smart shower and personalized dispensing integration | Connected home beauty device ecosystem |

Market Segments Covered in the Report

By Product Type

- Non-Medicated / Regular

- Medicated / Special Purpose

- Anti-Dandruff

- Hair-fall

- Volumizing

- Everyday

- 2-in-1

- Anti-Frizz

- Bond Repair

By Form

- Liquid

- Solid / Bar

- Powder

- Gel

- Cubes

By Application

- Household

- Commercial (Salons, Hotels, Spas)

- Professional Use

By Distribution Channel

- Hypermarkets / Supermarkets

- Online Stores

- Convenience Stores

- Drug Stores / Pharmacy

- Specialty Beauty Stores

- Departmental Stores

- Mono-Brand Stores

- Mass Merchandiser

- Social Commerce

By End-User / Demographics

- Women

- Men

- Kids / Toddlers / Infants

By Hair Type

- Straight Hair

- Dry & Damaged Hair

- Oily Hair

- Normal Hair

- Curly / Wavy Hair

- Color-Treated Hair

- Textured Hair

By Price Point

- Medium

- Low / Mass

- High / Premium / Luxury

- Ultra-Premium

By Technology / Method

- AI-Driven Personalization

- Microbiome-Based Formulation

- Scalp Analysis Tools

- IoT-Connected Devices

United States Shampoo Market

The United States shampoo market was valued at USD 13.96 billion in 2025 and will reach USD 17.90 billion by 2035, growing at a CAGR of 2.80%. The US market’s below-category-average CAGR reflects a mature penetration base — virtually every American household already purchases shampoo regularly — shifting competition from volume growth to premiumization, ingredient differentiation, and scalp-health positioning.

The US is the single largest national market in the global shampoo category and the leading market for Unilever across all beauty and personal care segments in 2025. Procter & Gamble, L’Oréal, and Henkel each run North American headquarters and innovation labs here — meaning the US market sets product and pricing benchmarks that influence global portfolio decisions for the entire category.

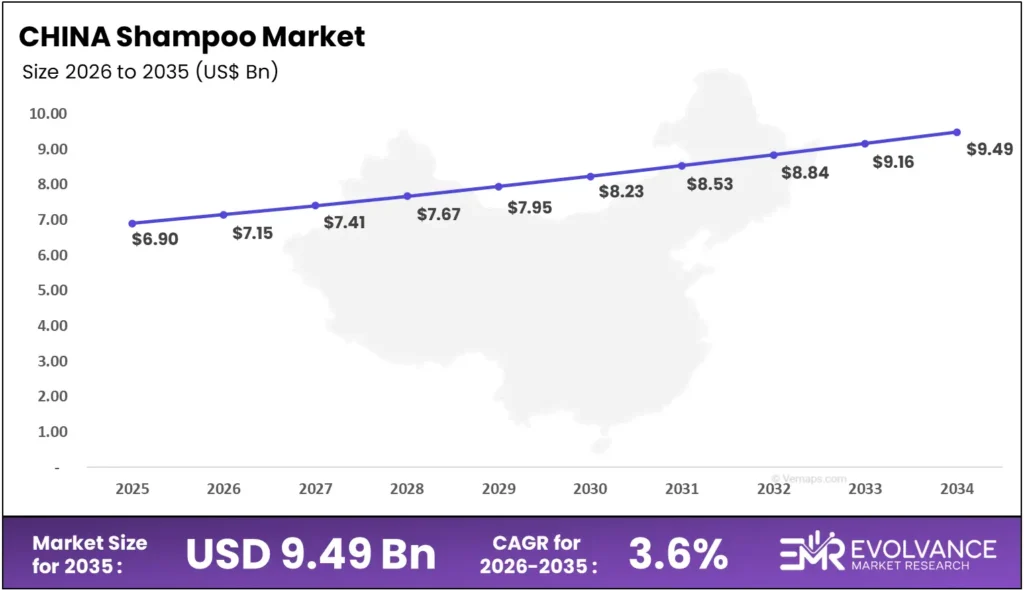

China Shampoo Market

The China shampoo market was valued at USD 6.90 billion in 2025 and will reach USD 9.49 billion by 2035, growing at a CAGR of 3.6%. China’s above-average category growth rate — against a USD 6.90 billion base — signals that premiumization and import cosmetic demand are driving value expansion faster than volume alone can explain.

According to China Customs data, cosmetics imports reached 110,942.9 tons January to April 2025 — with an approximate value of USD 5.60 billion for that period alone. Japan ranked as the largest supplier of hair care tools and accessories to China in 2024, with exports valued at USD 1.53 million — confirming that premium Asian hair care trade flows through China at scale. Both domestic and international brands will compete within this import-driven landscape through 2035.

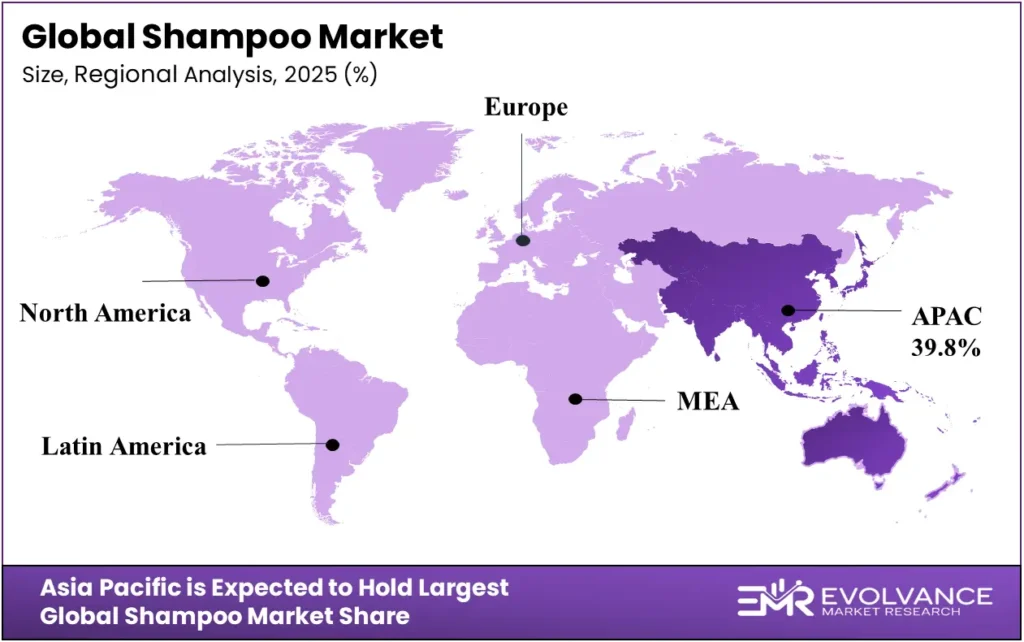

Shampoo Market Regional Insights

Asia Pacific Holds 39.8% Share at USD 15.21 Billion

| Region | Market Value (2025) | Share % | Year |

|---|---|---|---|

| Asia Pacific | USD 15.21 Billion | 39.8% | 2025 |

| North America | USD 13.96 Billion (US only) | — | 2025 |

| Europe | — | — | 2025 |

| South America | — | — | 2025 |

| Middle East & Africa | — | — | 2025 |

Asia Pacific anchors global shampoo demand at USD 15.21 billion and 39.8% revenue share in 2025 — a position built on population scale, rising urban incomes, and straight hair’s structural dominance as the most prevalent hair type across China, Japan, South Korea, and India simultaneously.

Asia Pacific leads because no other region combines population size, urbanization momentum, and a fast-premiumizing middle class in the same market footprint. Japan ranked as the largest hair care supplier to China in 2024, with USD 1.53 million in tool and accessory exports — confirming that intra-regional trade flows reinforce brand credentialing across the bloc’s premium tier. Operators entering any Asia Pacific market gain cross-regional distribution optionality that no other geography offers at scale.

North America Shampoo Market Trends

North America’s shampoo market centers on the United States, valued at USD 13.96 billion in 2025 — the world’s largest single-country shampoo market and the primary arena where Procter & Gamble, Unilever, and L’Oréal compete for mass-channel shelf dominance and premium D2C market share simultaneously. A 2.80% CAGR signals a mature market where value creation comes from mix shift, not volume growth.

Europe Shampoo Market Trends

Europe represents a dual-speed shampoo market — mass-channel volumes led by Henkel‘s Schwarzkopf and Unilever‘s Dove, alongside a fast-growing prestige segment anchored by professional salon brands. According to Kao Corporation’s FY2024 financial results, Kao Europe sales reached 93.5 billion yen in 2024 — a 17.7% reported increase — confirming that premium Asian hair care brands are scaling meaningfully in European retail and professional channels.

South America Shampoo Market Trends

Brazil anchors South American shampoo demand as a top-5 global market for Unilever‘s Personal Care and Beauty & Wellbeing segments in 2025 — a position driven by high hair care engagement, a large curly and wavy hair population, and strong brand loyalty to mass-market staples at competitive price points. Brands targeting South America must price for volume while building toward premiumization as urban incomes rise.

Middle East and Africa Shampoo Market Trends

The Middle East and Africa shampoo market is driven by a young, urbanizing population, rising personal care spending, and fast-growing demand for halal shampoo market products that meet Islamic certification standards across the GCC, Saudi Arabia, and South Africa. Brands that secure halal certification gain a structural market access advantage in the GCC that uncertified competitors cannot replicate through price competition alone.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The FDA‘s OTC drug monograph framework governs medicated shampoos sold in the United States — covering anti-dandruff active ingredients including zinc pyrithione, selenium sulfide, and ketoconazole at defined concentration limits. The Modernization of Cosmetics Regulation Act (MoCRA), enacted in 2022 and phased through 2025, expanded FDA authority over cosmetic safety reporting and adverse event disclosure for all non-OTC shampoo products.

The EU Cosmetics Regulation (EC) No 1223/2009 requires full INCI ingredient labeling and pre-market safety assessment for all shampoo products sold across European Union member states. Reformulation pressure is rising as the European Chemicals Agency continues restricting specific preservatives and synthetic fragrances — forcing manufacturers to replace incumbent ingredients with compliant alternatives at increased R&D and reformulation cost.

Halal certification requirements across GCC markets and Indonesia add a third regulatory layer for global shampoo manufacturers seeking market access in Muslim-majority countries. Brands must reformulate to remove alcohol-based surfactants and non-halal-sourced ingredients — a compliance step that requires separate production runs and third-party audits.

Drivers

Premiumization Pushes Hair Care Sales Mid-Single Digits

Premiumization across mass and prestige shampoo channels accelerated in 2025 as large FMCG manufacturers reported mid-single-digit hair care organic sales growth. Consumer willingness to pay more for scalp-health claims, bond-repair technology, and dermatology-adjacent ingredients has lifted average selling prices. Unit volumes across the category’s leading brands have held steady — confirming that premium positioning is not trading volume for value. Our forecast suggests this pricing power will sustain 6.51% CAGR through 2035 as premium mix continues shifting upward.

According to Procter & Gamble’s FY2025 innovation blog, Pantene Abundant & Strong reduces hair loss by up to 85% — a clinically proven claim that positions a mass-market brand at a dermatology price tier. This kind of ingredient-science anchor converts a routine repurchase into a considered health investment, expanding revenue per transaction across the brand’s entire shampoo portfolio.

Unilever‘s Power Brands — representing 78% of total group turnover — posted 4.3% underlying sales growth and 2.2% volume increase in 2025, confirming that hair care industry growth is running ahead of general FMCG volume trends. Volume growth alongside value growth signals that the category is adding new buyers, not just extracting more revenue from existing ones — a structural driver that supports the forecast period through 2035.

Restraints

Regulatory Pressure Raises Ingredient Compliance Costs

Regulatory pressure on cosmetic ingredients is intensifying as governments in the United States, European Union, and GCC markets implement stricter safety, chemical, and environmental compliance requirements for personal care products including shampoos. Reformulation timelines of 18 to 36 months compress margins for manufacturers already absorbing raw material cost increases, forcing smaller brands to delay innovation cycles or exit markets.

Input cost volatility in key raw materials — including palm-oil derivatives, sulfate-based surfactants, and synthetic fragrance compounds — challenged profit margins for shampoo manufacturers throughout 2024 and 2025. Palm-oil supply disruptions from Southeast Asian production regions drive surfactant cost spikes that FMCG manufacturers cannot fully pass through to price-sensitive mass-market consumers without risking volume loss at retail.

Counterfeit shampoo products circulating through informal trade channels in Asia Pacific, South America, and Middle East and Africa undercut brand-owner pricing and erode consumer trust in authentic formulations. Brands selling through uncontrolled distribution networks — particularly in markets without strong trademark enforcement — face margin dilution and reputational risk simultaneously, making channel control a critical priority for the forecast period.

Growth Factors

Premium Segments Expand as D2C Brands Scale Globally

Premium and prestige hair care segments are expanding globally as multinational FMCG companies scale high-margin beauty and wellness brands within their shampoo portfolios. Henkel‘s adjusted operating profit reached EUR 3,089 million in fiscal 2024 — a 20.9% increase over the prior year — proving that premiumization within the hair care business converts directly into margin improvement at the group level.

According to L’Oréal Finance’s announcement, L’Oréal agreed to acquire Color Wow in June 2025 — one of the fastest-growing professional haircare brands globally. This acquisition signals that large FMCG players view independent premium hair care brands as the most efficient vehicle for capturing prestige-segment growth without building new brand equity from scratch.

Digital commerce and direct-to-consumer beauty platforms are expanding market access for shampoo brands that lack the distribution scale to compete on physical retail shelves. Independent brands like Olaplex, Prose, and Function of Beauty have built nine-figure revenue bases entirely through D2C and e-commerce channels — proving that the shampoo market opportunities created by digital distribution are large enough to sustain standalone businesses outside the FMCG model.

Emerging Trends

Bond-Repair and Scalp-Focused Products Gain Share

Premium hair care formulations featuring lamellar technology, bond-repair science, and scalp-microbiome positioning are gaining global market share as brands move the category’s value proposition from cleansing to treatment. L’Oréal‘s Consumer Products Division posted 3.5% like-for-like growth in 2025, with a marked second-half acceleration attributed to successful haircare innovations — confirming that treatment-positioned shampoos are outpacing standard cleansing formats in value capture.

The wellness-beauty convergence is reshaping shampoo positioning as consumer goods companies integrate hair care into broader health and wellbeing ecosystems alongside supplements, scalp serums, and diagnostic tools. Brands like Nutrafol and Viviscal that built reputations in hair supplement categories are now adjacent competitors to shampoo brands — compressing the white space between topical hair care and ingestible wellness at the premium consumer’s consideration set.

Price strategy adjustments across FMCG personal care categories intensified in 2025 as manufacturers navigated tax changes, input cost inflation, and currency headwinds simultaneously. The competitive consequence is a polarizing market structure — mass-tier brands compressing margins to hold volume while premium brands raise prices supported by ingredient claims — a bifurcation that makes the middle price point the most contested and least defensible position in the shampoo market trends landscape.

Shampoo Market Key Companies Insights

In our view, Procter & Gamble holds the most defensible competitive position in the global shampoo market, combining mass-channel dominance through Head & Shoulders and Pantene with an active innovation pipeline extending into scalp-health and bond-repair positioning. According to P&G’s FY2025 earnings, net sales reached USD 84.3 billion with Hair Care organic sales growing low single digits, and the February 2026 Head & Shoulders upgrade launch confirms continued category investment at scale.

Unilever holds the second-largest shampoo portfolio globally through Dove, Sunsilk, and TRESemmé — brands that span mass to mid-premium positioning across every major geography. According to Unilever’s FY2025 results, group turnover reached EUR 50.5 billion in 2025. Beauty & Wellbeing delivered 4.3% underlying sales growth — confirming that Unilever shampoo brands are gaining value share even as 5.9% adverse currency headwinds compressed reported revenue.

L’Oréal S.A. leads the premium and professional shampoo segments through Kérastase, L’Oréal Paris, and the newly acquired Color Wow brand. According to L’Oréal’s half-year results, Professional Products Division exceeded EUR 5 billion for the first time — posting 7.5% like-for-like growth that confirms the L’Oréal shampoo market position in professional channels is widening the gap with all competitors.

Henkel AG & Co. KGaA competes through Schwarzkopf — a brand with strong professional and retail presence across Europe and emerging market distribution. According to Henkel’s FY2024 results, annual sales reached EUR 21,586 million with Consumer Brands organic growth of 3.0% driven primarily by the Hair business area — a result that positions Henkel as the most margin-improved major player in the competitive landscape.

Key Companies

- Procter & Gamble

- Unilever PLC

- L’Oréal S.A.

- Henkel AG & Co. KGaA

- Kao Corporation

- Shiseido Company, Limited

- Johnson & Johnson

- Coty Inc.

- Beiersdorf AG

- Amway Corporation

- Olaplex Holdings, Inc.

- Godrej Consumer Products Limited

Recent Development

- February 2026 — KKR prepared Wella Company for a potential US IPO following its full ownership acquisition, according to Reuters reporting. This signals that the professional haircare segment — including salon shampoos — is attracting public-market capital at valuations that validate premium channel investment.

- December 2025 — Coty Inc. sold its remaining 25.8% stake in Wella Company to KKR for USD 750 million upfront cash, according to Bloomberg reporting. The disposal signals Coty’s strategic exit from the professional haircare segment and concentrates Wella’s salon shampoo positioning under single private-equity ownership ahead of a potential IPO.

- November 2025 — Procter & Gamble introduced Gemz, a first-of-its-kind water-activated haircare solution after 14 years of R&D, redefining formulation science beyond the liquid bottle format. According to P&G’s innovation blog, Gemz redefines haircare for modern consumers — a launch that positions waterless formats as a credible mass-market category, not a niche sustainability play.

- November 2025 — Procter & Gamble‘s Aussie brand launched the Ultra Wonder Collection — premium multi-tasking curl care products with amino acids and strengthening lipids, priced under USD 10. The mass-market price point for a clinically positioned curl care system confirms that P&G is targeting the textured hair segment’s volume tier, not just the premium consumer.

- March 2025 — Henkel announced a share buyback program of up to EUR 1 billion following strong fiscal 2024 financial performance. The buyback signals management confidence that hair care-driven margin improvement is sustainable — and that excess capital returns are preferred over near-term M&A activity.

Related Shampoo Markets

The shampoo market sits within a broader hair care and personal care ecosystem where adjacent sub-markets share formulation science, distribution infrastructure, and consumer demand drivers. The global Hair Care Product Market reached USD 118.93 billion in 2025 and will hit USD 261.56 billion by 2035, growing at 8.2% CAGR. This parent market frames the scale within which shampoo competes for consumer wallet share.

India Shampoo Market: India is one of the fastest-growing shampoo markets in Asia Pacific, with Dabur, Marico, Patanjali Ayurved, Himalaya Wellness Company, and Godrej Consumer Products competing in a herbal and Ayurvedic segment that has no direct equivalent in any other major geography.

Indonesia Shampoo Market: Indonesia ranked among the top-5 global markets for Unilever‘s Personal Care business in 2025 — confirming that Southeast Asia’s most populous market is a structural priority for every major FMCG shampoo brand operating in Asia Pacific.

Anti-dandruff remains the largest medicated shampoo sub-segment globally, anchored by Head & Shoulders — the world’s best-selling anti-dandruff brand — and supported by a growing pipeline of dermatologist-recommended alternatives from CeraVe and clinical skin care brands.

Shampoo Bar Market. Solid shampoo bars are gaining shelf space as sustainability-conscious consumers seek plastic-free alternatives, with concentrated formulas reducing packaging waste by up to 80% compared with equivalent liquid volumes.

The men’s shampoo segment is the fastest-growing demographic sub-market in the category, driven by grooming category expansion and scalp-health awareness among male consumers aged 18 to 45.

Baby shampoo demand is sustained by strict tear-free and sulfate-free formulation standards, with Johnson & Johnson maintaining category leadership through decades of pediatric safety positioning.

The professional salon shampoo market generates the highest per-unit revenue in the category, with back-bar brands like Kérastase, Schwarzkopf Professional, and Wella commanding 3x to 5x the average retail price per liter.

The Black hair care market addresses textured and coily hair types with specialized cleansing, moisture-retention, and protective styling formulations — a segment where independent brands like Sienna Naturals and Ceremonia are outpacing legacy FMCG innovation cycles.

The halal shampoo market is growing fastest in Indonesia, Malaysia, and GCC markets, where certification-compliant formulations are a prerequisite for retail listing in major supermarket chains and pharmacy networks.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 38.23 Billion |

| Forecast Revenue (2035) | USD 71.83 Billion |

| CAGR (2026–2035) | 6.51% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Non-Medicated / Regular, Medicated / Special Purpose, Anti-Dandruff, Hair-fall, Volumizing, Everyday, 2-in-1, Anti-Frizz, Bond Repair), By Form (Liquid, Solid / Bar, Powder, Gel, Cubes), By Application (Household, Commercial, Professional Use), By Distribution Channel (Hypermarkets / Supermarkets, Online Stores, Convenience Stores, Drug Stores / Pharmacy, Specialty Beauty Stores, Departmental Stores, Mono-Brand Stores, Mass Merchandiser, Social Commerce), By End-User / Demographics (Women, Men, Kids / Toddlers / Infants), By Hair Type (Straight Hair, Dry & Damaged Hair, Oily Hair, Normal Hair, Curly / Wavy Hair, Color-Treated Hair, Textured Hair), By Price Point (Medium, Low / Mass, High / Premium / Luxury, Ultra-Premium), By Technology / Method (AI-Driven Personalization, Microbiome-Based Formulation, Scalp Analysis Tools, IoT-Connected Devices) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Procter & Gamble, Unilever PLC, L’Oréal S.A., Henkel AG & Co. KGaA, Kao Corporation, Shiseido Company Limited, Johnson & Johnson, Coty Inc., Beiersdorf AG, Amway Corporation, Olaplex Holdings Inc., Godrej Consumer Products Limited |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |