What Is the Quantum-Safe Cybersecurity Market Size?

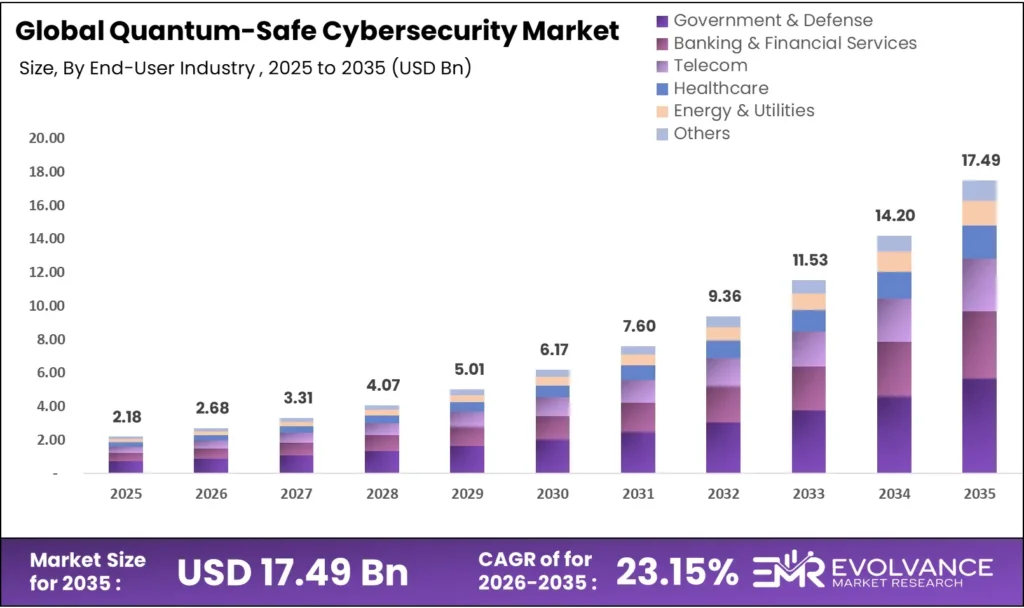

The global quantum-safe cybersecurity market size was valued at approximately USD 2.18 billion in 2025 and is projected to grow from USD 2.68 billion in 2026 to nearly USD 17.49 billion by 2035, registering a CAGR of approximately 23.15% during 2026–2035. The post-quantum cryptography market size accounts for the dominant share, while the broader quantum cybersecurity market forecast reflects accelerating investment across all solution types.

The year 2026 represents a critical inflection point as enterprise migrations from RSA and elliptic curve cryptography (ECC) toward NIST-standardized post-quantum algorithms accelerate across banking, government, and telecommunications. CRYSTALS-Kyber and CRYSTALS-Dilithium finalization by NIST in 2024 catalyzed procurement decisions translating into measurable deployment volumes.

Quantum-safe solutions protect sensitive data against the CRQC threat horizon projected between 2030 and 2035, requiring organizations to initiate migration programs today to avoid harvest-now-decrypt-later vulnerabilities. Market expansion is supported by escalating national cybersecurity investment, surging cloud-native quantum-resistant deployments, expanding QKD pilot networks, and stringent regulatory frameworks globally.

The Quantum-Safe Cybersecurity Market is gaining importance as organizations prepare for the risks posed by quantum computing to traditional encryption methods. The adoption of advanced cryptographic solutions is increasing across industries. This market is strongly connected with the Internet Security and Security Analytics, which provide complementary protection layers. Additionally, sectors such as the Secure Semiconductor Supply Chain are leveraging quantum-safe solutions to enhance hardware security.

Market Highlights

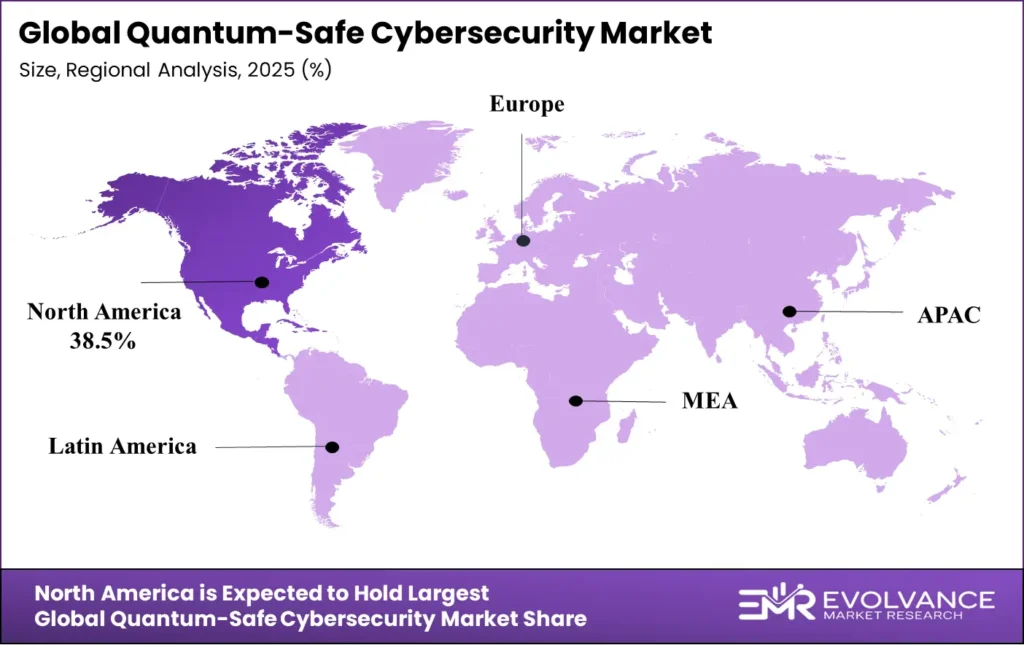

- North America dominated the market, holding the largest share of 38.5% in 2025.

- Asia Pacific is expected to expand at the fastest CAGR of 29.3% during 2026–2035.

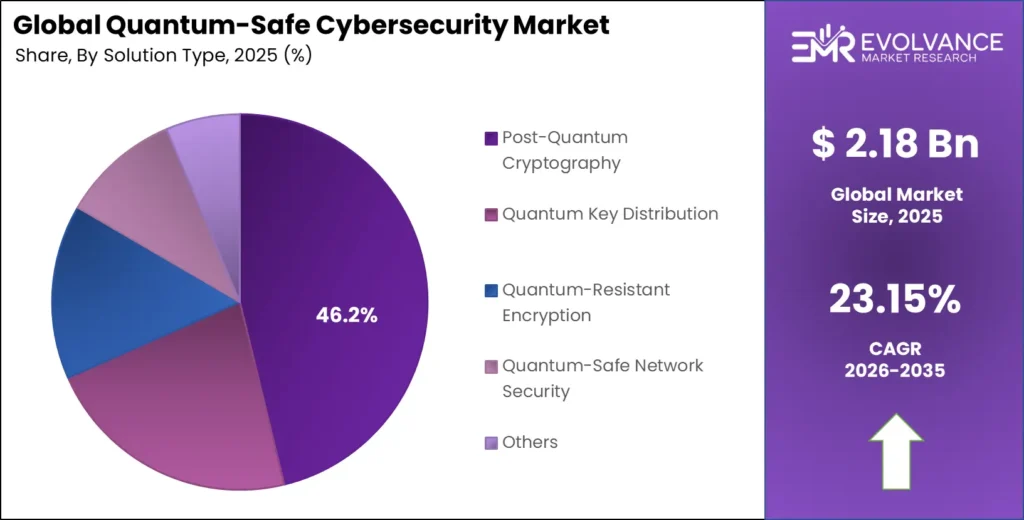

- By solution type, the post-quantum cryptography (PQC) segment accounted for the biggest market share of 46.2% in 2025.

- By solution type, the quantum key distribution (QKD) segment is expected to grow at the fastest CAGR of 32.4% during 2026–2035.

- By deployment, the cloud-based segment contributed the highest market share of 51.3% in 2025.

- By deployment, the hybrid deployment segment is expected to expand at the fastest CAGR of 28.7% during 2026–2035.

- By end-user industry, the banking & financial services segment captured the highest market share of 28.4% in 2025.

- By end-user industry, the healthcare segment is expected to expand at the fastest CAGR of 31.8% during 2026–2035.

U.S. Quantum-Safe Cybersecurity Market Size and Growth 2026 to 2035

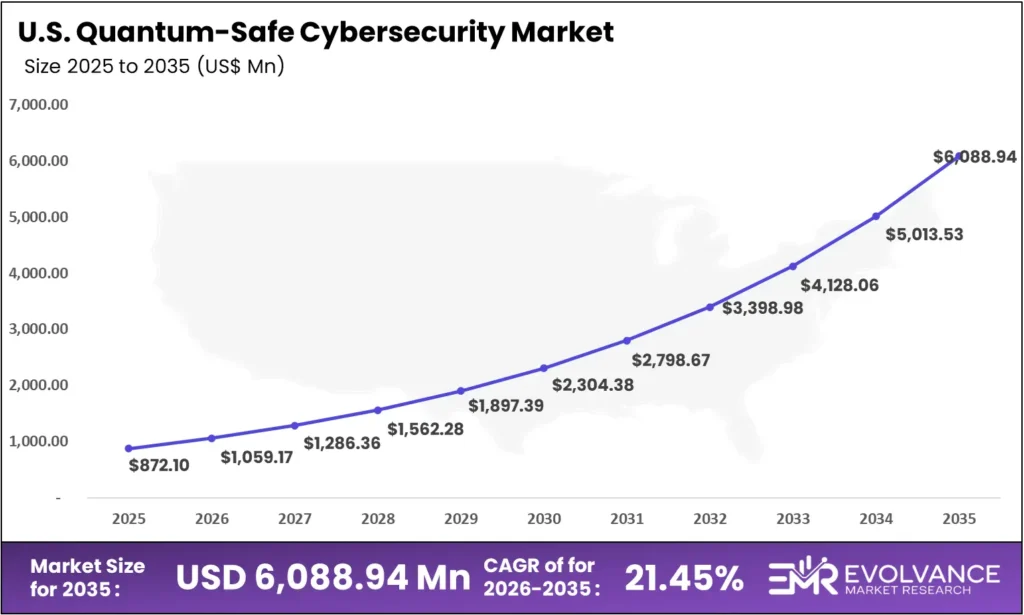

The U.S. quantum-safe cybersecurity market is estimated at USD 872.10 million in 2025, growing at a CAGR of 21.45% from 2026 to 2035. The NSA CNSA 2.0 mandate, NIST PQC algorithm finalization, and executive branch cryptographic modernization directives are driving federal agencies, financial institutions, and defense contractors to invest in quantum-resistant encryption. Cloud security integration, telecom upgrades, and healthcare data protection further support long-term U.S. market growth.

What Is Quantum-Safe Cybersecurity?

Quantum-safe cybersecurity encompasses cryptographic algorithms and security architectures designed to resist attacks from both classical computers and cryptographically relevant quantum computers (CRQCs). The quantum cybersecurity solutions landscape spans post-quantum cryptography (PQC), quantum key distribution (QKD), and quantum-resistant network security frameworks, collectively driving the quantum cybersecurity solutions market forecast to USD 18.76 billion by 2035.

Post-quantum algorithms are founded on mathematical problems resistant to known quantum attacks, including lattice-based cryptography (CRYSTALS-Kyber, CRYSTALS-Dilithium, FALCON), hash-based signatures (SPHINCS+), and code-based cryptography (Classic McEliece). QKD leverages quantum mechanical principles to enable information-theoretically secure key exchange over optical channels. Applications span enterprise encryption, cloud communications, financial transaction authentication, government data protection, telecommunications security, and healthcare records integrity globally.

The growth of the Quantum-Safe Cybersecurity Market is being driven by the increasing need for robust Internet Security frameworks capable of withstanding next-generation threats, including those posed by quantum computing. Organizations are rapidly adopting advanced Security Analytics solutions to detect vulnerabilities, monitor network behavior, and ensure proactive threat mitigation. Additionally, the use of High Content Screening (HCS) is gaining importance in identifying and managing large volumes of sensitive digital data, helping enterprises maintain compliance and strengthen their overall security posture in an evolving threat landscape.

Quantum-Safe Cybersecurity Market Outlook

- NIST PQC Standardization Driving Enterprise Adoption: The finalization of NIST post-quantum cryptography standards in 2024 — CRYSTALS-Kyber for key encapsulation and CRYSTALS-Dilithium for digital signatures — provided the definitive algorithm framework enterprises needed to initiate migration programs. The quantum-resistant encryption industry is responding with rapid deployment of PQC libraries, hardware security modules, and cryptographic agility platforms to systematically replace vulnerable RSA and ECC implementations across IT and OT infrastructure.

- Harvest-Now-Decrypt-Later Attacks Accelerating Migration: Nation-state adversaries are intercepting and archiving encrypted communications with strategic intent to decrypt them once quantum computers reach cryptographic relevance. This threat creates immediate urgency for organizations handling long-lived sensitive data — particularly in defense, financial services, and healthcare — to deploy quantum-safe encryption before the CRQC threat horizon materializes.

- Government Mandates Creating Structured Demand: The U.S. NSA CNSA 2.0 mandate requires national security systems to adopt quantum-resistant algorithms by 2030–2033. ENISA, Germany’s BSI, and the UK NCSC have issued parallel recommendations, creating multinational compliance demand driving enterprise procurement programs and vendor roadmap acceleration globally.

- Cloud Security Integration Expanding Accessibility: Major cloud providers including AWS, Microsoft Azure, and Google Cloud are integrating post-quantum cryptographic capabilities into TLS connections, key management services, and identity frameworks. Cloud-native PQC deployment enables mid-market enterprises to achieve quantum-safe security through configuration updates rather than on-premises hardware replacement, dramatically lowering migration barriers.

Key Market Trends

- Cryptographic Agility Architecture Adoption: Enterprises are deploying cryptographic agility frameworks enabling simultaneous support for classical and post-quantum algorithms during transition periods. This hybrid approach allows organizations to upgrade cryptographic primitives dynamically without full architectural rebuilds, reducing migration risk while maintaining security continuity across heterogeneous IT environments.

- QKD Metropolitan Network Expansion: Telecom operators and governments are deploying commercial QKD networks connecting data centers, financial exchanges, and government facilities with quantum-secure optical links. China’s national QKD backbone, European quantum communication infrastructure initiatives, and commercial QKD deployments in South Korea, Japan, and Singapore signal accelerating transition from laboratory demonstrations to production-grade networks.

- PQC-Enabled Hardware Security Modules: HSM providers including Thales, Entrust, and Utimaco are releasing post-quantum algorithm-enabled hardware security modules supporting NIST-standardized PQC implementations within tamper-resistant physical boundaries. Hardware-accelerated PQC processing addresses performance overhead concerns associated with lattice-based cryptographic operations across enterprise deployments.

- Quantum-Safe VPN and TLS Deployment: Network security vendors are integrating hybrid key exchange combining classical ECDH with CRYSTALS-Kyber into VPN gateways and TLS 1.3 implementations. Hybrid approaches provide quantum resistance while maintaining backwards compatibility with existing infrastructure, enabling phased migration without disrupting established network communication patterns.

- Financial Sector Leading Enterprise PQC Investment: Banks, payment networks, and central banks are prioritizing PQC investment to protect long-duration financial contracts, interbank settlement systems, and customer authentication. SWIFT and the Bank for International Settlements are coordinating quantum-safe transition roadmaps to ensure systemic financial infrastructure security.

- Integrated Quantum-Safe Security Platforms: Enterprise vendors are expanding beyond point PQC solutions to offer integrated platforms combining algorithm management, cryptographic inventory discovery, migration planning, and compliance monitoring. Vendor consolidation is accelerating as organizations prefer end-to-end partners capable of managing enterprise-wide migrations across diverse legacy infrastructure.

Market Scope

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | USD 2.18 Billion |

| Market Size in 2026 | USD 2.68 Billion |

| Forecasted Market Size by 2035 | USD 17.49 Billion |

| Market Growth Rate (2026–2035) | CAGR of 23.15% |

| Base Year | 2025 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | Solution Type, Deployment, End-User Industry, Region |

| Regional Coverage | North America, Europe, Asia-Pacific, Latin America, MEA |

Post-Quantum Cryptography & Quantum Key Distribution Market Trends by Solution Type

The post-quantum cryptography (PQC) segment dominated with the largest share of 46.2% in 2025, driven by rapid enterprise adoption of NIST-standardized lattice-based and hash-based algorithms following the 2024 standardization. PQC software libraries, cryptographic agility platforms, and PQC-enabled TLS implementations represent the most accessible migration entry point, requiring software-level updates rather than hardware replacement. The broad applicability of PQC across web communications, document signing, email encryption, and key management positions it as the foundational quantum-safe technology layer across all industries.

The quantum key distribution (QKD) segment is expected to grow at the fastest CAGR of 32.4% during 2026–2035, driven by compelling quantum key distribution market trends including metropolitan QKD network rollouts, satellite-based secure link deployment, and government communication channel upgrades. QKD leverages quantum mechanical photon properties to generate information-theoretically secure keys immune to computational attack. Quantum-resistant encryption appliances, quantum-safe network security solutions, and cloud-integrated offerings sustain strong demand across remaining solution segments.

Quantum-Safe Cybersecurity Market Growth by Deployment Mode

The cloud-based deployment segment contributed the highest share of 51.3% in 2025, driven by cloud-native security architecture migration and PQC integration by major providers into core service portfolios. Cloud-based quantum-safe offerings enable organizations to deploy PQC-protected key management and authentication without on-premises hardware investment. On-premises retains significant share in defense, intelligence, and financial infrastructure requiring dedicated security hardware. The hybrid segment is expected to expand at the fastest CAGR of 28.7% during 2026–2035, reflecting enterprise preference for combining cloud PQC services with on-premises HSM-anchored key storage.

Quantum-Resistant Encryption Industry Demand by End-User Sector

The banking & financial services segment captured 28.4% in 2025, driven by critical data sensitivity, long-duration records, and systemic infrastructure interdependencies requiring quantum-safe protection ahead of the CRQC threat horizon. Major banks, payment networks, and securities exchanges are investing in enterprise-scale PQC migration, HSM upgrades, and quantum-safe inter-institutional protocols. The healthcare segment is expected to expand at the fastest CAGR of 31.8% during 2026–2035, driven by patient data privacy regulations, long medical record retention requirements, and digital health transformation creating urgent demand for quantum-resistant health data encryption.

Government & Defense Insights

Government and defense accounts for 23.8% of total market revenue in 2025, driven by national security agencies implementing binding quantum-safe mandates. The NSA CNSA 2.0 framework, EU quantum security directives, and equivalent programs in the UK, Germany, France, South Korea, Japan, and Australia create structured procurement requirements translating into measurable deployment volumes. Defense contractors are investing in quantum-safe hardware security and satellite communication encryption to protect national security communications.

Segments Covered in the Report

By Solution Type

- Post-Quantum Cryptography (PQC) Software and Libraries

- Quantum Key Distribution (QKD) Systems

- Quantum-Resistant Encryption Appliances

- Quantum-Safe Network Security Solutions

- Quantum Random Number Generators

- Others

By Deployment

- On-Premises

- Cloud-Based

- Hybrid

By End-User Industry

- Banking & Financial Services

- Government & Defense

- Telecommunications

- Healthcare & Life Sciences

- Energy & Utilities

- Others

Regional Insights

North America — Leading the Quantum-Safe Cybersecurity Market

North America dominated with the largest share of 38.5% in 2025, underpinned by federal cybersecurity mandates, concentrated defense investment, leading technology vendor ecosystems, and mature enterprise security procurement. The NSA CNSA 2.0 directive, NIST PQC standardization leadership, and executive branch memoranda mandating quantum-safe migration across civilian federal agencies created the world’s most advanced regulatory demand framework. U.S. vendors including IBM, Microsoft, Google, Palo Alto Networks, and specialized quantum security firms including PQShield and Quantinuum drive global product development leadership. Canada’s National Quantum Strategy and active academic research commercialization further strengthen regional innovation and commercial deployment momentum.

Asia Pacific — Fastest Growing Post-Quantum Cryptography Market

Asia Pacific is expected to register the fastest regional CAGR of 29.3% during 2026–2035, driven by China’s national quantum communication infrastructure investment, South Korea’s PQC standardization initiatives, Japan’s quantum innovation strategy, and expanding enterprise cloud adoption. China has deployed the world’s largest operational QKD network connecting major cities with quantum-secure fiber and satellite links. South Korea’s government-industry quantum security roadmap, India’s National Quantum Mission, and Singapore’s commercial PQC enterprise adoption collectively sustain the region’s fastest-growing market position. Rapid digital transformation across financial services, telecom, and healthcare amplifies post-quantum encryption demand throughout the region.

Europe — Significant Market Position

Europe holds a significant market position driven by the European Quantum Flagship program, stringent GDPR data protection requirements, and quantum-safe transition guidance from BSI Germany, ANSSI France, and the UK NCSC. The EuroQCI initiative is deploying a pan-European quantum-secure network connecting government institutions and critical infrastructure operators with fiber and satellite QKD. EU Cyber Resilience Act requirements and NIS2 Directive provisions are progressively mandating cryptographic agility across operators of essential services, creating compliance-driven procurement demand across member states.

Latin America — Emerging Opportunities

Latin America’s quantum-safe cybersecurity market is developing steadily, driven by digital transformation across banking, government, and telecommunications sectors. Brazil and Mexico represent the largest markets, with central banks beginning to evaluate post-quantum cryptography frameworks. Cloud infrastructure expansion, fintech adoption, and regulatory modernization programs are compelling organizations to incorporate quantum-safe security planning within enterprise technology transformation roadmaps.

Middle East & Africa — Growing Demand

The Middle East and Africa region presents expanding opportunities driven by national digital transformation ambitions, government cybersecurity investment, and growing enterprise cloud adoption across GCC nations. Saudi Vision 2030, UAE National Cybersecurity Strategy, and Qatar’s quantum research investments create structured government demand. The region’s critical energy infrastructure, sovereign wealth fund operations, and cross-border payment systems create acute demand for long-lived data protection solutions, with managed security providers beginning to offer quantum-safe advisory and deployment services across regional enterprise markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- ASEAN Countries

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of MEA

Quantum-Safe Cybersecurity vs. Traditional Encryption

Quantum-safe cybersecurity delivers superior long-term security assurance by replacing computational assumptions vulnerable to Shor’s algorithm with mathematical problems resistant to both classical and quantum computers. Traditional encryption based on RSA and ECC remains widely deployed with established performance and operational tooling, representing practical advantages during the transition period.

| Feature | Quantum-Safe Security | Traditional Encryption |

|---|---|---|

| Threat Resistance | Resistant to quantum computing attacks | Vulnerable to Shor’s algorithm |

| Algorithm Basis | Lattice, hash-based, code-based cryptography | RSA, ECC, Diffie-Hellman |

| NIST Standardization | CRYSTALS-Kyber, Dilithium (2024) | Legacy standards pre-2000 |

| Key Sizes | Larger keys for lattice-based schemes | Compact RSA/ECC structures |

| Performance | Moderate compute overhead | Optimized over decades |

| Regulatory Alignment | NSA CNSA 2.0, NIST PQC standards | FIPS 140-2 / legacy compliance |

| Deployment Status | Active enterprise rollout | Widely deployed, sunset planned |

Market Value Chain Analysis

- Research Institutions and Algorithm Developers: Academic institutions, national laboratories, and standardization bodies including NIST, ETSI, and ISO develop and standardize post-quantum cryptographic algorithms and QKD protocols forming the technical foundation of the quantum-safe cybersecurity market. Research at MIT, ETH Zurich, University of Waterloo, and CWI Amsterdam creates innovations commercialized by enterprise security vendors.

- Quantum Hardware and Photonics Component Suppliers: Manufacturers of single-photon detectors, quantum random number generators, photonic integrated circuits, and fiber optical components provide specialized hardware enabling quantum key distribution systems. Suppliers including ID Quantique and Toshiba Research supply components to QKD integrators and telecom vendors deploying commercial quantum-secure network infrastructure.

- Cryptographic Library and Platform Developers: Software providers and open-source communities developing PQC algorithm libraries, cryptographic agility middleware, quantum-safe TLS implementations, and HSM firmware upgrades form the core software supply layer. The Open Quantum Safe project, PQShield, IBM Research, and major cloud vendors deliver PQC components integrated into enterprise security stacks.

- Enterprise Security Solution Providers: Cybersecurity vendors including Thales, Entrust, IBM Security, Palo Alto Networks, and Cisco integrate PQC algorithms and QKD capabilities into enterprise-grade security solutions including network encryption appliances, identity management platforms, key management systems, and PKI infrastructure for enterprise quantum-safe deployments.

- System Integrators and Managed Security Providers: Professional services firms and managed security providers deliver cryptographic inventory assessment, quantum risk analysis, PQC migration roadmap development, and implementation services enabling enterprises to execute quantum-safe transitions within defined compliance timelines.

Top Quantum-Safe Cybersecurity Market Companies

IBM

IBM is a global quantum-safe cybersecurity leader combining quantum computing research with enterprise-grade PQC deployment. IBM has integrated CRYSTALS-Kyber and CRYSTALS-Dilithium across IBM z16 mainframes, IBM Cloud services, and its Security portfolio. The IBM Quantum Safe technology framework provides enterprises with cryptographic discovery, assessment, and migration planning, positioning IBM as the premier quantum-safe security partner for financial institutions, government agencies, and critical infrastructure operators globally.

ID Quantique

ID Quantique is the world’s leading commercial QKD and quantum random number generator provider, delivering fiber-based QKD systems and quantum-safe network encryption to government, financial services, and telecom customers across more than 60 countries. Its Centauris quantum-safe network encryption platform combines QKD with post-quantum algorithms for maximum long-term security assurance on enterprise and carrier-grade network infrastructure.

Thales Group

Thales Group provides comprehensive quantum-safe solutions through its Cyber Solutions division, including Luna Network Hardware Security Modules with PQC algorithm support, CipherTrust Key Management platform, and enterprise data protection solutions incorporating NIST PQC standards. Thales serves government, defense, banking, telecom, and cloud services sectors globally, leveraging deep cryptographic expertise and established enterprise relationships to drive quantum-safe adoption.

Palo Alto Networks

Palo Alto Networks is integrating post-quantum capabilities across its Prisma Cloud platform, Next-Generation Firewalls, and SASE architecture. Its quantum-safe networking approach prioritizes hybrid key exchange combining classical and PQC algorithms in TLS connections, enabling enterprises to achieve quantum resistance during the transition period while maintaining compatibility with existing network infrastructure.

Other key players include Microsoft (Azure Quantum Safe, CRYSTALS across Microsoft 365), Google (Chrome PQC integration, NIST PQC cloud services), Cisco (quantum-safe VPN), Entrust (PKI with PQC), Quantinuum, evolutionQ, PQShield, Toshiba (QKD for metro networks), ISARA Corporation, CryptoNext Security, Post-Quantum, and QuintessenceLabs, competing across hardware, software, and managed service delivery models.

Recent Developments

- February 2026 — IBM integrated CRYSTALS-Kyber and CRYSTALS-Dilithium across IBM Cloud Key Protect and Hyper Protect Crypto Services, enabling enterprise cloud customers to benefit from NIST-standardized quantum-safe key encapsulation and digital signatures across all cloud-hosted cryptographic operations.

- January 2026 — The European Union awarded €1.1 billion in EuroQCI contracts for pan-European QKD infrastructure connecting 27 EU member state government networks with quantum-secure fiber and satellite links by 2030.

- December 2025 — Thales released Luna Network HSM 7.4 firmware incorporating full NIST PQC algorithm support including CRYSTALS-Kyber, Dilithium, FALCON, and SPHINCS+, enabling quantum-safe migration within existing deployed hardware without capital expenditure for replacement.

- October 2025 — Google completed deployment of CRYSTALS-Kyber hybrid key exchange in Chrome browser TLS connections, marking the largest commercial PQC deployment by volume and accelerating de-facto internet quantum-safe TLS protocol adoption globally.

Future Outlook 2030–2035

Between 2030 and 2035, the quantum-safe cybersecurity market is expected to transition from early enterprise adoption toward broad-market standardization as PQC algorithms become embedded defaults across operating systems, network equipment firmware, and cloud security primitives. Post-quantum cryptography market growth will accelerate as quantum computing advances toward cryptographic relevance within the 2030–2035 window, intensifying urgency for quantum-safe investment across all verticals. QKD networks will expand from metropolitan fiber toward satellite-based global quantum-secure communications. The convergence of quantum-safe cryptography with zero-trust architecture and AI-driven threat detection will define next-generation enterprise security frameworks supporting the projected expansion to USD 17.49 billion by 2035.