Report Overview

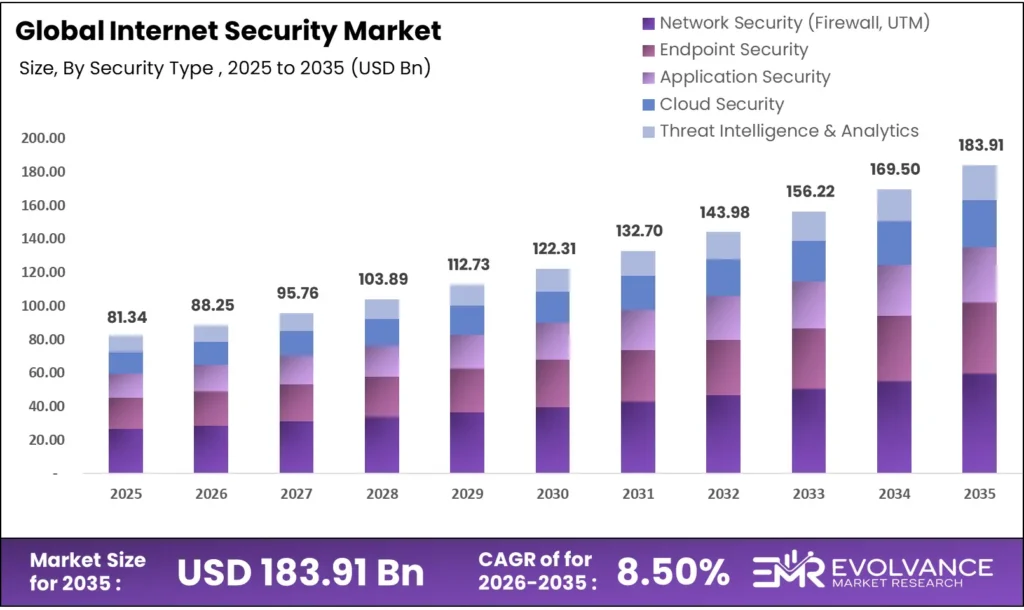

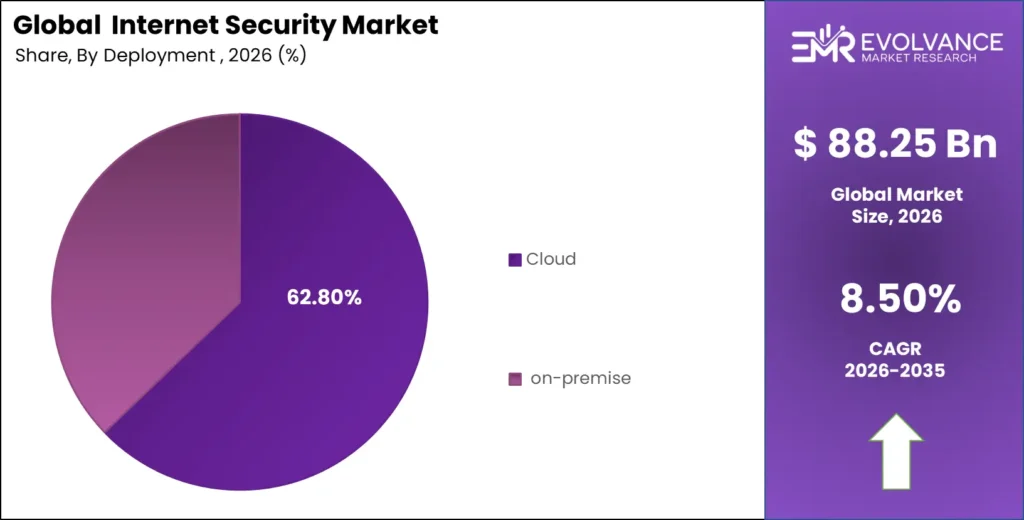

The global Internet Security Market was valued at USD 81.34 billion in 2025 and is projected to reach USD 183.91 billion by 2035, growing at a CAGR of 8.50%. North America leads with a 38.42% revenue share, while Asia Pacific is the fastest-growing region. The cloud deployment segment dominates with 62.8% market share, and large enterprises hold 65.74% of total revenue.

Network security is the largest security type segment (31.5% share), with BFSI the leading end-user vertical at 27.64%. Key growth drivers include escalating cyber threats and ransomware attacks, rapid adoption of zero-trust security frameworks, increasing cloud migration and remote workforce expansion, AI and machine learning integration for threat detection, and stringent regulatory compliance mandates across industries worldwide.

The Internet Security Market is expanding rapidly due to the growing need for protecting digital infrastructure from cyber threats. Organizations are investing in advanced security solutions to safeguard data and networks. This trend is closely linked with the Security Analytics, which enhances threat detection capabilities, and the Cloud FinOps, which supports secure cloud environments. Additionally, the rise of digital platforms in the Buy Now Pay Later (BNPL) is further driving demand for robust internet security solutions.

What Is the Internet Security Market Size?

The global Internet Security Market was valued at approximately USD 81.34 billion in 2025 and is projected to grow from USD 88.25 billion in 2026 to nearly USD 183.91 billion by 2035, registering a compound annual growth rate (CAGR) of around 8.50% during 2026–2035. The year 2026 represents a critical acceleration phase as organizations strengthen their cybersecurity postures in response to increasingly sophisticated threat landscapes, AI-driven cyberattacks, and expanding digital ecosystems.

Internet security encompasses technologies, services, and practices designed to protect digital networks, devices, applications, and data from unauthorized access, cyberattacks, and information theft. Market expansion is supported by rising cybercrime costs projected to exceed USD 15.6 trillion annually by 2035, accelerating cloud adoption, proliferating IoT devices, expanding remote work environments, and evolving regulatory frameworks including GDPR, CCPA, NIS2 Directive, and sector-specific cybersecurity mandates across BFSI, healthcare, government, and critical infrastructure sectors.

Market Highlights

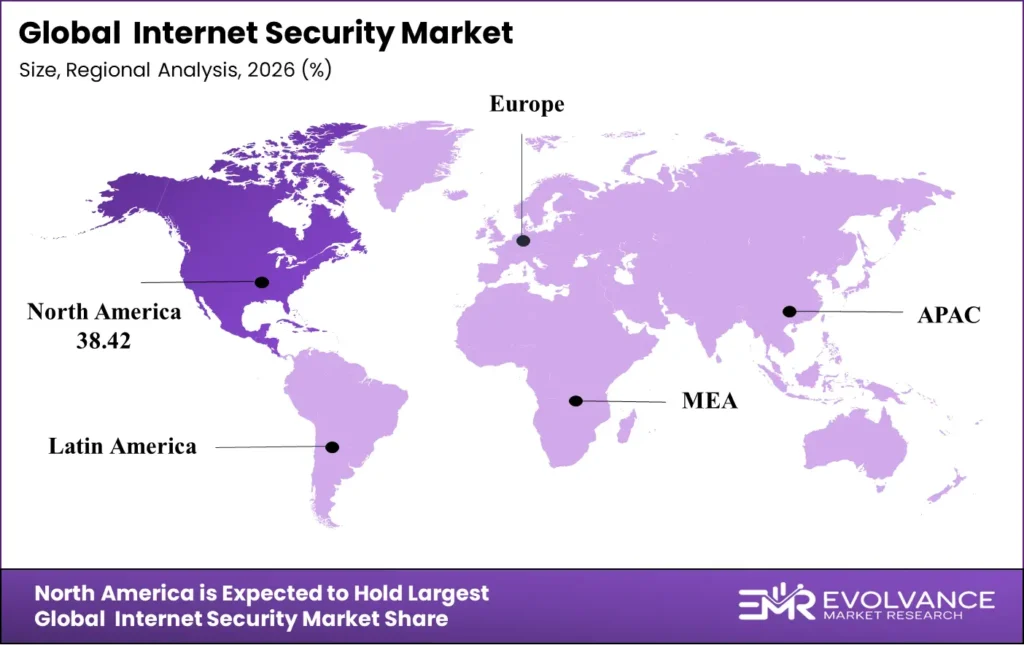

- North America dominated the market, holding the largest share of 38.42% in 2025.

- Asia Pacific is expected to expand at the fastest CAGR of 11.6% during 2026–2035.

- By component, the solutions segment dominated the Internet Security Market with the largest share of 64.35% in 2025.

- By component, the services segment is expected to expand at the fastest CAGR of 10.4% during 2026–2035.

- By deployment, the cloud segment accounted for the biggest market share of 62.8% in 2025.

- By deployment, the on-premise segment is expected to grow at a CAGR of 6.8% during 2026–2035.

- By security type, the network security segment contributed the highest market share of 31.5% in 2025.

- By security type, the cloud security segment is expected to expand at the fastest CAGR of 12.3% during 2026–2035.

- By organization size, the large enterprises segment held the major market share of 65.74% in 2025.

- By organization size, the SMEs segment is expected to expand at the fastest CAGR of 10.9% during 2026–2035.

- By end-user, the BFSI segment captured the highest market share of 27.64% in 2025.

- By end-user, the healthcare segment is expected to expand at the fastest CAGR of 11.2% during 2026–2035.

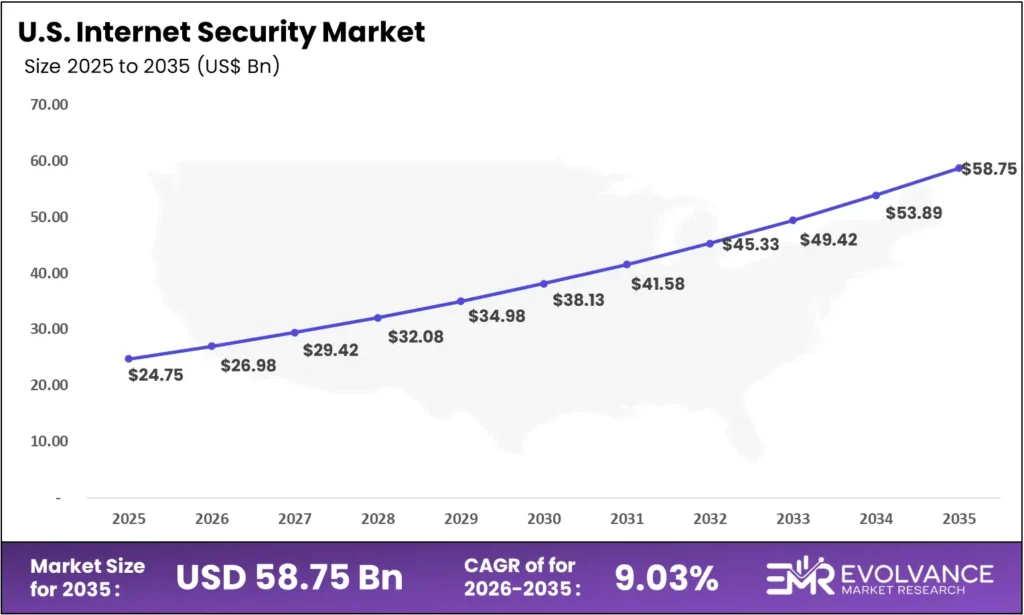

U.S. Internet Security Market Size and Growth 2026 to 2035

The U.S. Internet Security Market size is estimated at USD 24.75 billion in 2025 and is projected to reach approximately USD 26.98 billion in 2026, reflecting robust enterprise and government investment in cybersecurity infrastructure. The market is expected to grow at a strong CAGR of 9.03% from 2026 to 2035, driven by escalating ransomware attacks, critical infrastructure protection mandates, and expanding zero-trust architecture deployments.

The United States federal government’s cybersecurity spending continues to rise sharply, with Executive Orders on cybersecurity strengthening compliance requirements across defense, healthcare, financial services, and energy sectors. Organizations are investing heavily in AI-powered threat detection, extended detection and response (XDR), secure access service edge (SASE), and cloud-native security platforms to protect distributed workforces, multi-cloud environments, and expanding digital supply chains.

What Is Internet Security?

Internet Security refers to the comprehensive set of technologies, policies, processes, and practices designed to protect digital networks, computing systems, applications, and data from cyber threats, unauthorized access, data breaches, and malicious attacks transmitted through internet-connected environments. Unlike traditional perimeter-based security, modern internet security adopts layered defense strategies including network security, endpoint protection, application security, cloud security, identity and access management, encryption, and threat intelligence. By leveraging advanced technologies such as artificial intelligence, machine learning, behavioral analytics, and zero-trust architectures, internet security solutions provide real-time threat detection, automated incident response, continuous monitoring, and predictive risk assessment, enabling organizations to safeguard critical assets, ensure regulatory compliance, maintain business continuity, and protect customer trust across increasingly complex and distributed digital ecosystems.

Internet Security Market Outlook

Escalating Cyber Threats and Ransomware Attacks

The global cyber threat landscape continues to escalate at an unprecedented pace, with ransomware attacks increasing by over 150% since 2022. Organizations across all sectors face sophisticated, multi-vector attacks including advanced persistent threats (APTs), supply chain compromises, phishing campaigns, and state-sponsored cyber warfare. The average cost of a data breach reached USD 4.88 million in 2025, compelling enterprises to significantly increase cybersecurity investments. Growing attack surfaces driven by cloud migration, IoT proliferation, and remote work expansion further amplify the urgency for comprehensive internet security solutions.

Zero-Trust Security Framework Adoption

The rapid adoption of zero-trust security architectures is fundamentally transforming enterprise cybersecurity strategies. Zero-trust eliminates implicit trust within network perimeters, requiring continuous verification of every user, device, and application attempting to access organizational resources. Over 70% of enterprises are expected to implement zero-trust frameworks by 2027, driving demand for identity and access management (IAM), micro-segmentation, multi-factor authentication (MFA), and continuous monitoring solutions. Government mandates including the U.S. federal zero-trust strategy and the EU NIS2 Directive are accelerating adoption across public and private sectors.

AI and Machine Learning in Cybersecurity

Artificial intelligence and machine learning are revolutionizing internet security by enabling predictive threat intelligence, automated anomaly detection, real-time behavioral analysis, and autonomous incident response. AI-powered security platforms can analyze billions of security events daily, identifying patterns and threats that human analysts cannot detect at scale. However, adversaries are also leveraging AI to create more sophisticated attacks including deepfake-based social engineering, AI-generated malware, and automated vulnerability exploitation, creating an ongoing cybersecurity arms race.

Cloud Security and SASE Convergence

The shift toward cloud-first business models and distributed workforces is driving rapid adoption of cloud-native security platforms and Secure Access Service Edge (SASE) architectures. SASE converges network security functions including SD-WAN, secure web gateways, cloud access security brokers (CASB), and zero-trust network access (ZTNA) into a unified cloud-delivered service. Approximately 65% of enterprises are expected to adopt SASE frameworks by 2028, significantly expanding the addressable market for integrated cloud security solutions.

Key Market Trends

- AI-Powered Threat Detection: Growing deployment of machine learning algorithms and generative AI for real-time threat identification, automated response orchestration, and predictive vulnerability assessment across enterprise security operations centers.

- Zero-Trust Architecture Expansion: Widespread adoption of zero-trust frameworks requiring continuous verification, micro-segmentation, and least-privilege access policies across hybrid and multi-cloud environments.

- Extended Detection and Response (XDR): Rising demand for unified XDR platforms that consolidate endpoint, network, cloud, and email security telemetry into a single threat detection and investigation platform.

- Cybersecurity Mesh Architecture: Emergence of distributed security architectures that extend security controls to distributed assets, enabling composable security policies across diverse digital environments.

- Quantum-Safe Cryptography: Growing investment in post-quantum encryption standards and crypto-agile solutions as organizations prepare for the potential threat of quantum computing to existing encryption methods.

- Managed Security Services (MSS): Expanding demand for managed detection and response (MDR) and security-as-a-service models among SMEs lacking in-house cybersecurity expertise and resources.

Market Scope

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | USD 81.34 Billion |

| Market Size in 2026 | USD 88.25 Billion |

| Forecasted Market Size by 2035 | USD 183.91 Billion |

| Market Growth Rate (2026–2035) | CAGR of 8.50% |

| Base Year | 2025 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Segments Covered | Component, Deployment, Security Type, Organization Size, End-User, Region |

| Regional Coverage | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

Segment Insights

Component Insights

The solutions segment dominated the Internet Security Market with the largest share of 64.35% in 2025, driven by growing enterprise demand for advanced firewalls, intrusion detection/prevention systems, antivirus and anti-malware software, encryption solutions, and identity management platforms. Organizations are investing in integrated security suites that combine multiple protection layers including endpoint detection and response (EDR), network detection and response (NDR), and security information and event management (SIEM) platforms. The services segment is expected to expand at the fastest CAGR of 10.4% during 2026–2035, driven by rising demand for managed security services, consulting, implementation, and training as organizations seek expert guidance to navigate increasingly complex cybersecurity challenges.

Deployment Insights

The cloud deployment segment accounted for the biggest market share of 62.8% in 2025, driven by its scalability, rapid deployment capabilities, automatic updates, and cost-effectiveness for protecting distributed workforces and multi-cloud environments. Cloud-based security solutions eliminate the need for extensive on-premises hardware and enable organizations to scale protection dynamically with business growth. The on-premise segment is expected to maintain steady growth at a CAGR of 6.8% during 2026–2035, supported by stringent data sovereignty requirements, regulatory compliance mandates, and the need for complete control over security infrastructure in highly regulated industries such as defense, banking, and government agencies.

Security Type Insights

The network security segment contributed the highest market share of 31.5% in 2025, reflecting the critical importance of protecting enterprise networks from unauthorized access, DDoS attacks, and lateral threat movement. Network security solutions including next-generation firewalls (NGFW), intrusion detection systems (IDS), virtual private networks (VPN), and network access control (NAC) remain foundational elements of enterprise cybersecurity architectures. The cloud security segment is expected to expand at the fastest CAGR of 12.3% during 2026–2035, driven by accelerating cloud migration, multi-cloud complexity, containerization security challenges, and the growing need for cloud workload protection platforms (CWPP) and cloud security posture management (CSPM) solutions.

Organization Size Insights

The large enterprises segment held the major market share of 65.74% in 2025, driven by higher cybersecurity budgets, complex IT ecosystems, and strong regulatory compliance requirements. Large organizations increasingly deploy advanced threat intelligence, zero-trust frameworks, AI-driven security analytics, and multi-layered protection systems to safeguard critical assets and sensitive customer data. Meanwhile, the SMEs segment is expected to expand at the fastest CAGR of 10.9% during 2026–2035, supported by rising cyberattack incidents, rapid cloud adoption, and growing awareness of cost-effective SaaS-based security solutions.

End-User Insights

The BFSI segment captured the highest market share of 27.64% in 2025, as financial institutions face the highest frequency and sophistication of cyberattacks targeting customer data, transaction systems, and digital banking platforms. Regulatory compliance requirements including PCI DSS, SOX, and Basel III mandates drive continuous investment in advanced security infrastructure. The healthcare segment is expected to expand at the fastest CAGR of 11.2% during 2026–2035, driven by the rapid digitalization of health records, telemedicine expansion, IoMT device proliferation, and HIPAA compliance requirements compelling healthcare organizations to strengthen their cybersecurity postures significantly.

Segments Covered in the Report

By Component

- Solutions

- Services

By Deployment

- Cloud

- On-Premise

By Security Type

- Network Security (Firewall, UTM)

- Endpoint Security

- Application Security

- Cloud Security

- Threat Intelligence & Analytics

By Organization Size

- SMEs

- Large Enterprises

By End User

- BFSI

- Healthcare

- IT & Telecommunications

- Government & Defense

- Retail & E-Commerce

- Others

Regional Insights

North America — Leading the Market

North America dominated the internet security market with the largest share of 38.42% in 2025. The region’s leadership is supported by advanced digital infrastructure, high enterprise cybersecurity spending exceeding USD 80 billion annually, the presence of leading security vendors, and strong government investment in critical infrastructure protection. The U.S. federal cybersecurity strategy, CISA directives, and increasing state-level data privacy regulations further drive market expansion. Canada’s Critical Cyber Systems Protection Act and growing financial sector cybersecurity investments additionally strengthen North America’s dominant position.

Asia Pacific — Fastest Growing Region

Asia Pacific is expected to expand at the fastest CAGR of 11.6% during 2026–2035, driven by rapid digital transformation, increasing cyber threats targeting emerging economies, and growing government cybersecurity mandates. China’s Cybersecurity Law and Data Security Law, India’s Digital Personal Data Protection Act, Japan’s cybersecurity strategy, and Australia’s Critical Infrastructure Protection Act are compelling organizations to strengthen security investments. The rapid expansion of digital banking, e-commerce, and cloud computing across the region is further accelerating demand for comprehensive internet security solutions.

Europe — Significant Market Position

Europe holds a significant position in the internet security market, driven by the stringent GDPR framework, the NIS2 Directive strengthening critical infrastructure cybersecurity requirements, and the EU Cybersecurity Act establishing a comprehensive certification framework. The European Cyber Resilience Act mandating security requirements for connected products is further expanding the addressable market. Organizations across Germany, the United Kingdom, France, and the Nordics are increasingly investing in zero-trust architectures, AI-powered threat detection, and managed security services.

Latin America — Emerging Opportunities

Latin America’s internet security market is growing steadily, driven by increasing cybercrime rates, digital banking expansion, and evolving data protection regulations including Brazil’s LGPD and Mexico’s Federal Law on Protection of Personal Data. Brazil and Mexico represent the largest markets in the region, with organizations investing in cloud security platforms, managed detection and response services, and endpoint protection solutions. The rapid growth of fintech ecosystems and e-commerce platforms across the region is compelling enterprises to significantly strengthen their cybersecurity capabilities.

Middle East & Africa — Growing Demand

The Middle East and Africa region presents expanding opportunities for internet security, driven by government-led digital transformation initiatives, smart city developments, and rising cyber threats targeting critical infrastructure. The UAE’s National Cybersecurity Strategy, Saudi Arabia’s National Cybersecurity Authority mandates aligned with Vision 2030, and South Africa’s Cybercrimes Act are driving security investments. Key sectors including BFSI, telecommunications, energy, and government agencies are prioritizing advanced threat protection, cloud security, and managed security services to protect rapidly digitalizing operations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- ASEAN Countries

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East Africa

- GCC Countries

- South Africa

- Rest of MEA

Market Value Chain Analysis

- Technology Providers and Infrastructure Vendors: Cloud providers, semiconductor companies, hardware manufacturers, and AI technology developers supplying compute resources, networking equipment, threat intelligence feeds, and machine learning engines that form the foundational technology layer of internet security platforms.

- Internet Security Solution Developers: Cybersecurity companies designing and developing firewalls, endpoint protection platforms, SIEM systems, IAM solutions, encryption technologies, and AI-powered threat detection engines, transforming raw security telemetry into actionable threat intelligence and automated defense capabilities.

- System Integrators and Managed Security Service Providers: Implementation partners, managed security service providers (MSSPs), and managed detection and response (MDR) vendors deploying, customizing, and managing security solutions, ensuring seamless integration with existing enterprise IT infrastructure, compliance frameworks, and industry-specific security requirements.

- End-Use Industries and Enterprises: Organizations across BFSI, healthcare, government, IT, retail, manufacturing, and energy sectors utilizing internet security solutions to protect critical assets, ensure regulatory compliance, maintain business continuity, prevent data breaches, and safeguard customer trust across increasingly complex digital ecosystems.

Top Internet Security Market Companies

Palo Alto Networks

Palo Alto Networks leads the internet security market with its comprehensive Strata, Prisma, and Cortex platforms. The company’s AI-driven security operations platform, Cortex XSIAM, integrates endpoint, network, and cloud security telemetry for autonomous threat detection, investigation, and response. Prisma Cloud delivers industry-leading cloud-native application protection across multi-cloud and hybrid environments.

CrowdStrike

CrowdStrike delivers cloud-native endpoint security through its Falcon platform, leveraging AI and behavioral analytics for real-time threat detection and response. The platform provides unified visibility across endpoints, cloud workloads, identities, and data, enabling organizations to consolidate security tools and reduce mean time to detect and respond to cyber threats.

Fortinet

Fortinet provides a broad, integrated security fabric combining next-generation firewalls, SD-WAN, SASE, and endpoint protection into a unified platform. FortiGuard Labs delivers AI-powered threat intelligence, while the FortiOS operating system enables consistent security policies across on-premises, cloud, and hybrid environments.

Cisco Systems

Cisco offers comprehensive security solutions spanning network security, cloud security, endpoint protection, and zero-trust access through its SecureX platform. Cisco’s acquisition of Splunk strengthens its security analytics, observability, and SIEM capabilities, positioning the company as a leader in integrated security operations.

Other Key Players

Other key players include Check Point Software Technologies, Zscaler, Microsoft, IBM Security, Broadcom (Symantec), Trend Micro, SentinelOne, Okta, Cloudflare, and McAfee, each focusing on specialized cybersecurity capabilities including zero-trust access, cloud security, identity management, and managed detection and response.

Top Company Competitive Comparison (2025)

| Company | Core Strength | Strategic Focus 2025–2026 |

|---|---|---|

| Palo Alto Networks | AI-driven XSIAM Platform | Autonomous SOC & Cloud Security |

| CrowdStrike | Falcon Endpoint Platform | AI-powered Threat Hunting |

| Fortinet | Security Fabric Architecture | Integrated SASE & NGFW |

| Cisco Systems | SecureX + Splunk Integration | Security Analytics & Observability |

| Zscaler | Zero Trust Exchange | Cloud-native Zero Trust Expansion |

Recent Developments

- March 2025 — Palo Alto Networks launched Cortex XSIAM 3.0 with enhanced generative AI capabilities, enabling autonomous security operations and reducing mean time to respond (MTTR) by 85% compared to traditional SIEM platforms.

- June 2025 — CrowdStrike expanded its Falcon platform with Charlotte AI, an AI-powered security analyst that automates threat hunting, incident investigation, and remediation across multi-cloud and hybrid environments.

- September 2025 — Fortinet introduced FortiSASE with integrated digital experience monitoring (DEM), providing unified secure access and performance visibility for distributed workforces across global enterprises.

- January 2026 — Zscaler announced the expansion of its Zero Trust Exchange platform with AI-driven data protection capabilities, enabling real-time classification and protection of sensitive data across SaaS, cloud, and private applications.

- February 2026 — Multiple leading cybersecurity vendors began integrating post-quantum cryptographic algorithms into their encryption solutions, preparing enterprise customers for the emerging quantum computing threat landscape.

Future Outlook 2030–2035

Between 2030 and 2035, the internet security market is expected to evolve into AI-augmented autonomous security platforms capable of predicting, preventing, and remediating cyber threats with minimal human intervention. The convergence of artificial intelligence, quantum-safe cryptography, extended detection and response (XDR), and cybersecurity mesh architectures will redefine enterprise security operations. As organizations continue to expand their digital footprints through IoT, edge computing, 5G networks, and multi-cloud ecosystems, internet security will become a foundational component of digital business infrastructure, supporting the projected market expansion to USD 183.91 billion by 2035. The integration of security into DevOps (DevSecOps), API-first security models, and automated compliance frameworks will drive platform consolidation and create new growth opportunities across all enterprise segments.