What Is the Hyper-Personalized Technology Market Size?

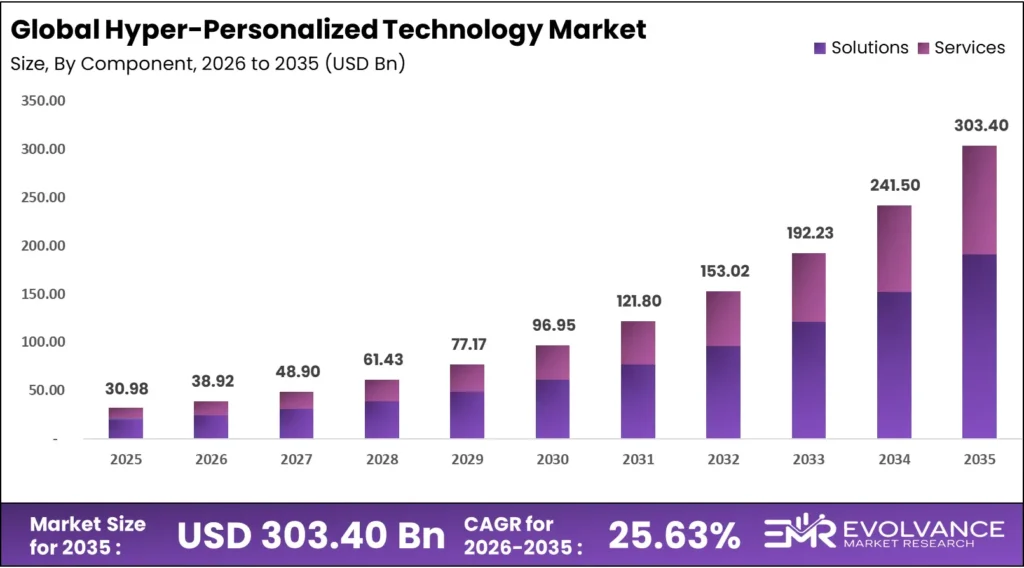

The global hyper-personalized technology market will reach USD 303.40 billion by 2035 from USD 30.98 billion in 2025, growing at a CAGR of 25.63% during 2026 to 2035. This expansion reflects surging enterprise adoption of AI-driven personalization engines, as Accenture and Google Cloud reported deploying over 450 AI agents across industries in 2025. Beyond this, retailers such as Saks Global recorded a 7% revenue increase and 10% higher conversion after launching hyper-personalized homepage experiences, signaling that enterprise investment in personalization now produces measurable bottom-line returns.

Market Highlights

- The global hyper-personalized technology market was valued at USD 30.98 billion in 2025 and will reach USD 303.40 billion by 2035, growing at a CAGR of 25.63% from 2026 to 2035.

- By Component: The Solutions segment dominates with a 62.5% revenue share in 2025.

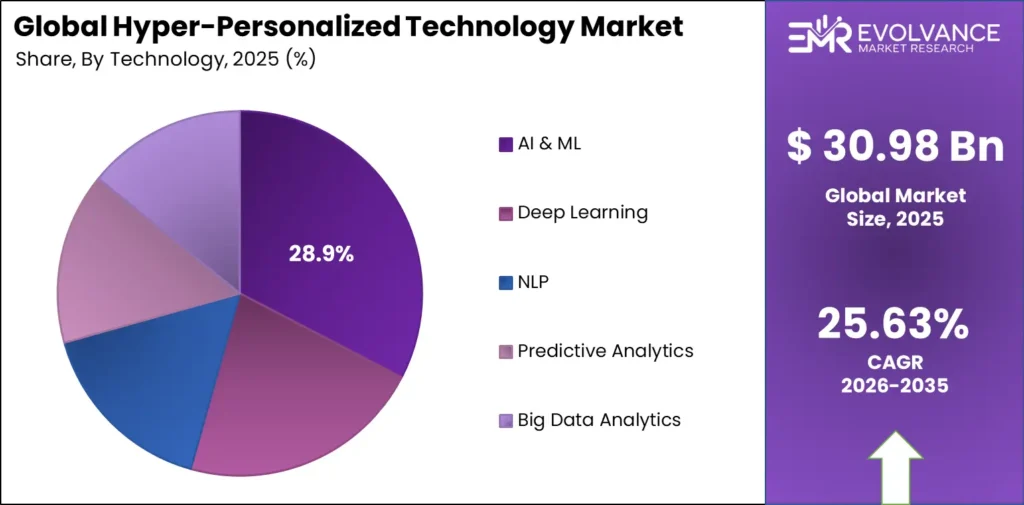

- By Technology: AI & ML leads with a 28.9% revenue share in the technology segment.

- By Application: Product/Content Recommendation holds the highest revenue share among all application segments.

- By End-Use: Retail & E-commerce holds the largest revenue share among all end-use verticals.

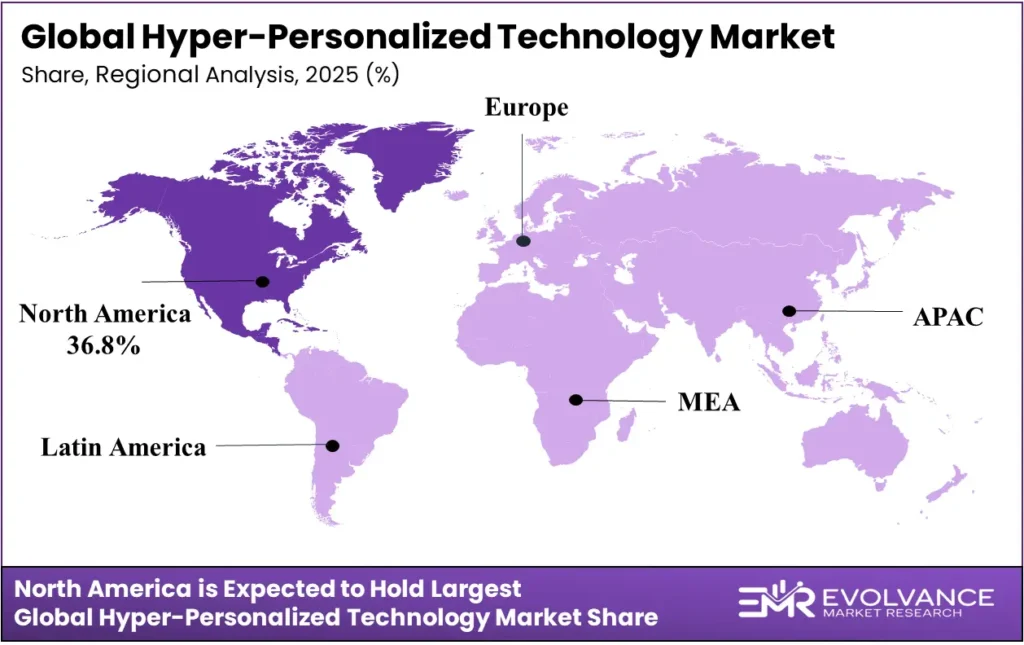

- By Region: North America leads all regions with a 36.8% revenue share, valued at USD 11.45 billion in 2025.

Market Overview

The hyper-personalized technology market covers AI-driven platforms, real-time data engines, and customer intelligence tools that deliver individual-level experiences — spanning retail, financial services, healthcare, and media — replacing broad audience segmentation with continuous, behavior-triggered adaptation for each user.

This analysis draws on primary interviews with enterprise technology buyers, vendor briefings across 6 end-use verticals, and proprietary demand modeling covering 5 regions and 18 market segments. EMR analysts combined quantitative survey data with structured analyst validation to produce a forecast grounded in verified adoption signals.

Enterprises adopt hyper-personalized technology to solve a core revenue problem: generic digital experiences lose customers at scale. Chief Marketing Officers and Chief Technology Officers jointly procure these platforms — CDPs, journey orchestration engines, and generative AI content tools — driven by conversion rate pressure, customer lifetime value targets, and hyper-personalized customer journeys that demand real-time data at every touchpoint.

This adoption velocity is measurable. According to SAP’s Value of AI Report, Indian businesses invested USD 31 million in AI in 2025 — above the global average of USD 26.7 million — while 93% of Indian organizations expected positive returns within three years. IBM’s AI Outlook found 60% of APAC organizations anticipating AI benefits within two to five years. SAP data shows AI supported 23% of business tasks in India in 2025, rising to 41% within two years.

Hyper-Personalized Technology Segmentation Analysis

Component Analysis

Solutions dominates with 62.5% due to AI-native platform deployment demand.

In 2025, Solutions held a dominant position in the hyper-personalized technology market with a 62.5% revenue share. Enterprise buyers prioritize end-to-end personalization platforms — customer data platforms, real-time decisioning engines, and AI orchestration suites — over standalone consulting or managed services. This preference reflects CTO and CMO alignment on owning the personalization stack rather than outsourcing it, concentrating spend in the solutions segment hyper-personalized technology market.

Services support deployment, integration, and ongoing optimization of personalization platforms. As enterprise buyers scale from pilot to full rollout, demand for implementation and managed services grows — particularly among mid-market firms lacking in-house AI engineering capacity. This makes the services segment hyper-personalized technology market a structurally recurring revenue opportunity for platform vendors bundling professional services with SaaS contracts.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Solutions | 62.5% | AI-native CDP and decisioning platform demand |

| Services | N/A | Mid-market rollout and integration support |

Technology Analysis

AI & ML leads with 28.9% due to real-time behavioral modeling at scale.

In 2025, AI & ML held a dominant position in the hyper-personalized technology market with a 28.9% revenue share. This leadership reflects the foundational role of machine learning models. They process behavioral signals — clickstreams, purchase history, session data — and produce individualized outputs faster than any rule-based system. Enterprise personalization programs now treat AI and ML spend as non-discretionary infrastructure.

Deep Learning enables sub-second pattern recognition across unstructured data. Neural networks trained on image, voice, and behavioral inputs allow platforms to personalize visual content, product discovery feeds, and dynamic interfaces without explicit user input — a capability that rule-based engines cannot replicate. This makes deep learning the primary technology investment for retailers and media platforms pursuing ambient personalization.

NLP powers conversational and content personalization at scale. By interpreting intent from search queries, chat inputs, and reviews, NLP engines match users to relevant products, services, and content without requiring structured browsing behavior. In 2025, Contentstack launched EDGE — the first adaptive digital experience platform using NLP-driven real-time content assembly — signaling that NLP is moving from search optimization into full-stack experience personalization.

Predictive Analytics and Big Data Analytics translate historical patterns into forward-looking personalization triggers. Predictive models forecast next-best actions — purchase probability, churn risk, optimal offer timing — while big data pipelines aggregate signals from RFID systems, beacon networks, and omnichannel touchpoints to feed those models. Together, predictive analytics hyper-personalized technology solutions form the demand-sensing layer that gives real-time engines their commercial accuracy.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| AI & ML | 28.9% | Real-time behavioral modeling at enterprise scale |

| Deep Learning | N/A | Unstructured data pattern recognition for content |

| NLP | N/A | Intent-driven content and product personalization |

| Predictive Analytics | N/A | Next-best-action and churn forecasting models |

| Big Data Analytics | N/A | Omnichannel signal aggregation for real-time engines |

Application Analysis

Product/Content Recommendation leads the Application segment due to direct, measurable revenue conversion impact.

In 2025, Product/Content Recommendation held a leading position in the hyper-personalized technology market by application revenue. Recommendation engines are the highest-ROI application of personalization technology — Amazon, Netflix, and Sephora built multi-billion-dollar revenue streams on individually curated product and content feeds. For enterprise buyers, the product content recommendation segment delivers the shortest path from AI investment to measurable conversion uplift.

Marketing & Advertising Personalization activates individual-level targeting across paid and owned channels. Platforms ingest first-party behavioral data to serve dynamically assembled ad creatives, email sequences, and push notifications — replacing broad audience segments with one-to-one message delivery. This application drives the largest share of CMO personalization budget because it directly links data investment to measurable campaign performance metrics.

Customer Journey Personalization orchestrates experience continuity across every touchpoint. Rather than optimizing a single channel, journey personalization platforms map behavioral state across web, mobile, in-store, and service interactions — adapting content, offers, and messaging in real time as context shifts. This capability is the primary reason enterprise buyers move from point personalization tools to full customer journey personalization platforms as their programs mature.

Real-Time Interaction Management and Dynamic Pricing & Offer Personalization address the two highest-velocity personalization use cases. Real-time interaction management triggers context-aware responses within milliseconds of a behavioral signal — enabling abandoned-cart recovery, live chat escalation, and next-best-offer delivery. Dynamic pricing hyper-personalization adjusts price and offer in real time based on individual demand signals, inventory position, and competitive data.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Product/Content Recommendation | Highest share | Direct conversion uplift and measurable ROI |

| Marketing & Advertising Personalization | N/A | First-party data activation across paid channels |

| Customer Journey Personalization | N/A | Cross-channel continuity and platform maturity |

| Real-Time Interaction Management | N/A | Millisecond behavioral trigger response systems |

| Dynamic Pricing & Offer Personalization | N/A | Individual demand signal and inventory optimization |

End-Use Analysis

Retail & E-commerce leads the End-Use segment due to direct revenue linkage between personalization and conversion.

In 2025, Retail & E-commerce held a leading position in the hyper-personalized technology market by end-use revenue. This vertical generates the clearest ROI signal for personalization investment — hyper-personalization in retail drives measurable outcomes in average order value, repeat purchase rate, and cart recovery. RFID systems, beacon networks, and smart shelves extend this personalization layer into physical stores, making retail the broadest deployment environment for the full technology stack.

BFSI deploys hyper-personalized technology to convert data depth into relationship revenue. Banks, insurers, and wealth managers hold some of the richest individual behavioral datasets in any industry — transaction history, life-stage signals, risk profile — and BFSI hyper-personalized technology platforms translate this into personalized product recommendations, dynamic rate offers, and proactive financial guidance. For operators, BFSI represents the highest willingness-to-pay vertical outside retail because personalization directly reduces churn in high-value account relationships.

Healthcare & Life Sciences uses personalization platforms to improve patient engagement, care adherence, and health outcomes. AI-driven journey orchestration delivers individualized care reminders, symptom-triggered content, and personalized wellness programs — replacing generic population health communications with behavior-responsive interventions. This vertical’s adoption accelerates as providers face reimbursement models that reward outcomes over volume, making patient engagement a financial imperative.

IT & Telecom, Media & Entertainment, and Travel & Hospitality each apply hyper-personalization to reduce churn and maximize lifetime value in high-volume subscriber and transaction environments. Telecom operators personalize plan recommendations and retention offers using network usage patterns; media platforms optimize content discovery feeds; and travel brands deploy hyper-personalization to drive ancillary revenue through individually timed upgrade and experience offers.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Retail & E-commerce | Largest share | Direct conversion and cart recovery ROI |

| BFSI | N/A | Transaction data depth and churn reduction |

| Healthcare & Life Sciences | N/A | Outcomes-based care engagement models |

| IT & Telecom | N/A | Usage-pattern plan personalization and retention |

| Media & Entertainment | N/A | Content discovery optimization and churn reduction |

| Travel & Hospitality | N/A | Ancillary revenue from individually timed offers |

Market Segments Covered in the Report

By Component

- Solutions

- Services

By Technology

- AI & ML

- Deep Learning

- NLP

- Predictive Analytics

- Big Data Analytics

By Application

- Product/Content Recommendation

- Marketing & Advertising Personalization

- Customer Journey Personalization

- Real-Time Interaction Management

- Dynamic Pricing & Offer Personalization

By End-Use

- Retail & E-commerce

- BFSI

- Healthcare & Life Sciences

- IT & Telecom

- Media & Entertainment

- Travel & Hospitality

Hyper-Personalized Technology Market Regional Insights

North America Holds 36.8% Share at USD 11.45 Billion

North America leads the hyper-personalized technology market with a 36.8% revenue share and a market value of USD 11.45 billion in 2025, anchored by the U.S. hyper-personalized technology market’s concentration of enterprise AI infrastructure, cloud platform investment, and digital-first retail. Adobe, Salesforce, and Microsoft — all headquartered in the region — supply the dominant personalization stack to Fortune 500 buyers. North America will retain structural leadership as generative AI adoption accelerates enterprise personalization spend through the forecast period.

Asia Pacific Hyper-Personalized Technology Market Trends

Asia Pacific is the fastest-growing regional market for hyper-personalized technology, driven by smartphone penetration, rapid e-commerce expansion, and accelerating enterprise AI adoption across China, India, Japan, and South Korea. Accenture reported Asia Pacific revenues of USD 2.6 billion in Q2 FY2026, up 10% year-over-year — reflecting the region’s rising demand for AI-enabled personalization services. For market entrants, India and Southeast Asia represent the highest-velocity opportunity given urbanization rates and expanding digital commerce infrastructure.

Europe Hyper-Personalized Technology Market Trends

Europe’s hyper-personalized technology market develops under the direct constraint of GDPR, which shapes every vendor product decision around consent architecture, data minimization, and cross-border transfer limits. SAP SE and Adobe have both embedded GDPR-compliant personalization controls into their European platform configurations, turning regulatory compliance into a product differentiator. European deployments favor privacy-by-design CDPs over data-maximalist personalization approaches, creating a distinct regional technology preference that vendors must address to win enterprise deals.

Rest of World Hyper-Personalized Technology Market Trends

Latin America, the Middle East, and Africa represent early-stage but structurally significant hyper-personalization markets. Brazil leads Latin American adoption through expanding digital retail and fintech personalization platforms, while the Kingdom of Saudi Arabia and the UAE drive Middle East investment through Vision 2030-linked digital transformation programs. These regions enter the market at a later adoption stage but benefit from leapfrogging legacy infrastructure — deploying cloud-native personalization stacks without migrating from older systems.

| Region | Share % | USD Value (2025) |

|---|---|---|

| North America | 36.8% | USD 11.45 billion |

| Asia Pacific | N/A | N/A |

| Europe | N/A | N/A |

| Latin America | N/A | N/A |

| Middle East & Africa | N/A | N/A |

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The General Data Protection Regulation — enforced by EU supervisory authorities since 2018 — sets the primary compliance framework for hyper-personalization platforms operating in Europe. Consent requirements, the right to erasure, and restrictions on automated decision-making directly constrain the behavioral data pipelines that personalization engines depend on, requiring vendors to architect privacy controls into their core platforms rather than as add-ons.

In the United States, the California Consumer Privacy Act and its successor the CPRA establish consent and opt-out rights that GDPR CCPA hyper-personalization compliance teams must address for any platform processing Californian consumer data. This has effectively elevated California’s standard toward a de facto national baseline, pushing enterprise personalization vendors to build unified consent management into their CDP and journey orchestration products.

Drivers

AI-Powered Hyper-Personalization Lifts Conversion 10% at Saks Global

Hyper-personalized e-commerce experiences now produce measurable revenue outcomes that justify enterprise-scale investment. In 2025, Saks Global deployed a fully individualized homepage reaching 100% of Saks.com traffic — delivering a 7% revenue increase and 10% conversion uplift. In our view, this outcome marks a structural shift: personalization has moved from a differentiation strategy to a revenue protection requirement for any retailer competing in digital commerce.

Enterprise agentic AI adoption is accelerating personalization at the workflow level, not just the customer-facing layer. The Accenture and Google Cloud deployment of over 450 AI agents across industries in 2025 demonstrates that personalization engines now automate internal workflows — supply chain routing, service escalation, and marketing execution — alongside consumer experiences. This expands the addressable value of customer data platform personalization from front-end engagement tools to full enterprise operating systems.

Brand investment in cross-channel personalization tools — analytics platforms, predictive engines, and journey orchestration suites — expanded consistently through 2025, reflecting CMO and CTO budget alignment on personalization as core digital infrastructure. This sustained spend pattern signals recurring platform revenue rather than one-time project budgets, making hyper-personalization a structurally defensible market even in periods of broader technology spending constraint.

Restraints

GDPR CCPA Hyper-Personalization Compliance Raises Data Usage Costs

Consumer demand for individualized experiences collides directly with rising data privacy obligations under GDPR, CCPA, and emerging national frameworks in 2025. Personalization engines require continuous behavioral data flows. Privacy regulations restrict these inputs through consent gates, data minimization rules, and cross-border transfer limits. This forces platform vendors to invest in compliance architecture that adds cost and complexity without adding personalization capability.

Smaller enterprises face disproportionate barriers to building agentic and machine-learning-driven personalization systems. The capital requirements for AI model training, real-time data infrastructure, and specialist engineering talent create a capability gap between large platform operators and mid-market buyers. This structural disadvantage concentrates advanced hyper-personalization SME capacity in enterprises with existing cloud infrastructure — slowing total market adoption and extending the capability gap.

Algorithmic bias in personalization models presents a compliance and reputational risk that slows enterprise deployment timelines. When recommendation engines trained on historical behavioral data reproduce demographic patterns — surfacing different products, prices, or offers to different user groups — regulators and consumer advocates treat this as discriminatory output. Enterprises must invest in model auditing, bias testing, and explainability frameworks before deploying personalization at scale.

Growth Factors

Hyper-Personalization ROI Drives Real-Time Analytics Platform Adoption

Acceleration in real-time data analytics adoption creates a direct growth pathway for hyper-personalization platforms that deliver contextual user experiences across engagement metrics. As enterprises instrument more touchpoints — web sessions, mobile interactions, in-store sensors — the volume of actionable behavioral signals grows, making real-time analytics infrastructure both more necessary and more commercially viable. Platform vendors with low-latency data pipelines capture disproportionate enterprise budget as buyers upgrade from batch-processing to continuous decisioning.

According to SAP’s Value of AI Report, 85% of Indian businesses rated AI agents as having moderate to high potential to transform operations in 2025, with 50% seeing specific value in complex supply chain and workflow applications. This signals that AI agent adoption is moving beyond early adopters. The shift is now reaching mainstream enterprise procurement across emerging markets.

Platform consolidation through acquisition is accelerating the growth of composable personalization stacks. In January 2025, Contentstack acquired Lytics to power real-time hyper-personalization — combining a composable digital experience platform with a real-time customer data platform — creating an integrated stack that eliminates the integration cost enterprises previously faced when assembling CDP and DXP tools separately.

Emerging Trends

Predictive Analytics Hyper-Personalized Technology Sets Market Standard

Hyper-personalized retail journeys — featuring real-time product recommendations, dynamically assembled content, and behavior-triggered offers — became the operational standard across e-commerce platforms in 2025. Retailers that previously treated personalization as a premium feature now treat it as table-stakes infrastructure, compressing the competitive window for laggards. Personalization platform vendors face growing pressure to deliver out-of-the-box real-time interaction management capabilities rather than custom implementations.

Agentic AI is redefining personalization from a reactive to a proactive capability. Rather than responding to user actions, agentic systems anticipate needs. They schedule follow-ups, adjust offers before a user signals intent, and personalize service interactions autonomously. In October 2025, League Inc. launched League Agent Teams — a multi-agent system delivering 24/7 hyper-personalized healthcare experiences using its Health Story platform — demonstrating that agentic personalization is already commercially deployed in high-stakes verticals.

Generative AI is shifting personalization from rule-based content selection to dynamic content creation. Instead of choosing from pre-built content variants, GenAI-powered platforms assemble individualized copy, imagery, and product descriptions at the moment of interaction. This collapses the content production bottleneck that previously limited personalization scale — enabling brands to deliver unique experiences to millions of users simultaneously without proportional increases in content team headcount.

Key Companies Hyper-Personalized Technology Market Insights

The hyper-personalized technology market competitive landscape concentrates around a core group of enterprise platform leaders — cloud infrastructure providers, marketing technology vendors, and data management specialists — whose personalization revenues reflect sustained double-digit growth across 2025. Adobe Inc. reported Digital Experience segment revenue of USD 5.86 billion in FY2025, up 9% year-over-year, with Digital Experience subscription revenue reaching USD 5.41 billion, up 11% — driven by Adobe Experience Platform, Real-Time CDP, and GenStudio. This confirms Adobe as the solutions segment leader by dedicated personalization platform revenue.

Cloud infrastructure providers power the underlying personalization workload layer. Amazon Web Services reported AWS net sales of USD 128.7 billion in 2025, up 19–20%, with AI infrastructure supporting personalization workloads across retail, media, and BFSI clients. Google LLC reported Google Cloud revenues of USD 58.705 billion in FY2025, up 36%, led by Vertex AI and enterprise personalization solutions.

Our forecast suggests that CRM-integrated and enterprise data platforms will consolidate the largest share of incremental personalization spend through 2035. Salesforce Inc. reported Data Cloud and AI ARR reaching USD 900 million in FY2025, up 120% year-over-year — the strongest growth signal in the competitive landscape. Microsoft reported Intelligent Cloud revenue of USD 106.265 billion in FY2025, up 21%, with Dynamics 365 growing 19% as the enterprise CRM personalization layer.

Oracle Corporation reported cloud revenues of USD 44.0 billion in FY2025, up 12%, with OCI consumption growing 62% in Q4. SAP SE reported cloud revenue of €21.023 billion in FY2025, up 26% at constant currencies, with Cloud ERP Suite revenue reaching €18.1 billion, up 32% — embedding AI-driven personalization into enterprise process workflows across global enterprise deployments.

Key Companies

- Accenture

- SAP SE

- Adobe Inc.

- Amazon Web Services, Inc.

- Google LLC

- Microsoft

- Oracle

- SAS Institute Inc.

- Salesforce, Inc.

- IBM Corporation

Recent Development

- March 2026: League Inc. released its Spring 2026 update featuring advanced agentic AI for hyper-personalized care navigation and gap closure — expanding its multi-agent healthcare personalization platform beyond its October 2025 launch to include proactive care journey management at population scale.

- February 2026: BlastPoint received a strategic investment bringing its total growth round to USD 12.6 million, with funding targeting hyper-personalized customer intelligence solutions for financial services — reinforcing the hyper-personalized technology market outlook for BFSI-specific personalization platform growth through 2026. For full details, see the BlastPoint investment announcement.

- September 2025: Vibe.co raised USD 50 million in Series B funding for hyper-targeted TV ads — bringing individual-level personalization to connected television and signaling that hyper-personalization is expanding beyond digital commerce into broadcast media channels.

- May 2025: Doppel raised USD 35 million in Series B funding for hyper-personalized digital twin technology — enabling brands to create individualized virtual representations of customers for deeper engagement personalization across immersive and interactive channels.

- April 2025: Reelevant raised €6 million in Series A funding for real-time marketing personalization — validating early-stage investor appetite for specialized hyper-personalization tools that operate at the campaign execution layer rather than the full platform stack.

Related Hyper-Personalization Markets

The hyper-personalized technology market connects to a broader network of specialized segments — each addressing a distinct layer of the personalization stack, a specific vertical, or an enabling technology category. Operators and investors tracking this market should monitor these adjacent segments as growth signals and potential consolidation targets through 2035.

Key Related Markets

- B2B Hyper-Personalization Technology — Enterprise workflow personalization is scaling rapidly, with Accenture and Google Cloud deploying over 450 AI agents across B2B industries in 2025 to enable personalized service and operational workflows.

- Generative AI in Hyper-Personalization — Consumer demand for AI-native shopping experiences is measurable: 71% of buyers wanted generative AI integrated into their shopping journeys in 2025, making GenAI the fastest-growing technology input to personalization platforms.

- Customer Data Platform — CDPs form the data infrastructure layer underpinning the solutions segment’s 62.5% revenue dominance, aggregating behavioral signals from every touchpoint to feed real-time personalization engines.

- SME Hyper-Personalization Solutions — AI task automation is reaching mid-market enterprises: SAP data shows AI supporting 23% of business tasks in India in 2025, rising to 41% within two years — signaling expanding SME adoption.

- Privacy-Compliant Personalization Technology — GDPR and global privacy standards directly constrain behavioral data pipelines, creating demand for privacy-by-design personalization platforms that deliver individual targeting within regulatory boundaries.

- Hyper-Personalization in Healthcare — League Inc. launched its Agent Teams platform for 24/7 AI-personalized healthcare experiences in October 2025, demonstrating that clinical and wellness verticals are active deployment environments for agentic personalization systems.

- Hyper-Personalization in BFSI — Financial services personalization attracted USD 12.6 million in strategic investment to BlastPoint in February 2026, confirming BFSI as a high-priority vertical for specialized personalization intelligence platforms.

- Real-Time Interaction Management Technology — Contentstack launched its EDGE adaptive digital experience platform in February 2025 as the first purpose-built system for real-time content personalization, signaling platform-level investment in this application category.

- Omnichannel Personalization Platform — Brand investment in cross-channel personalization tools — analytics platforms, predictive engines, and journey orchestration suites — expanded consistently through 2025, reflecting enterprise commitment to unified experience delivery across all touchpoints.

- Hyper-Personalization ROI and Measurement — Saks Global’s hyper-personalized homepage delivered a 7% revenue increase and 10% conversion uplift in 2025, establishing a measurable ROI benchmark that enterprise buyers reference when building personalization investment cases.

Market Scope

| Market Size Value in 2025 | USD 30.98 Billion |

| Revenue Forecast in 2035 | USD 303.40 Billion |

| Growth Rate | CAGR of 25.63% from 2026 to 2035 |

| Base Year | 2025 |

| Historic Period | 2020 to 2024 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | By Component (Solutions, Services); By Technology (AI & ML, Deep Learning, NLP, Predictive Analytics, Big Data Analytics); By Application (Product/Content Recommendation, Marketing & Advertising Personalization, Customer Journey Personalization, Real-Time Interaction Management, Dynamic Pricing & Offer Personalization); By End-Use (Retail & E-commerce, BFSI, Healthcare & Life Sciences, IT & Telecom, Media & Entertainment, Travel & Hospitality) |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Countries Covered | US, Canada, Germany, France, UK, Spain, Italy, China, Japan, South Korea, India, Australia, Brazil, Mexico, GCC, South Africa |

| Key Companies | Accenture, SAP SE, Adobe Inc., Amazon Web Services Inc., Google LLC, Microsoft, Oracle, SAS Institute Inc., Salesforce Inc., IBM Corporation |