Executive Summary

Quick Insight: The global Humanoid Robots in Manufacturing market is on track to expand more than 19× by 2035, driven by rapid advances in AI-powered locomotion and dexterous manipulation, accelerating Industry 5.0 adoption mandates, unprecedented venture and strategic investment from automotive and electronics manufacturers, and the demonstrated operational superiority of humanoid platforms across assembly, material handling, and precision inspection applications in real-world production environments.

The global Humanoid Robots in Manufacturing market encompasses fully autonomous and collaborative bipedal robotic systems deployed across factory floor operations including precision assembly, sub-component handling, quality inspection, welding, packaging, and intralogistics. This report delivers comprehensive analysis of market size, robot type segmentation, technology stack dynamics, end-use industry deployment economics, and competitive positioning for the 2026–2035 forecast period — covering AI vision architectures, actuator technology, deployment cost curves, and the competitive strategies of platform developers reshaping industrial automation globally.

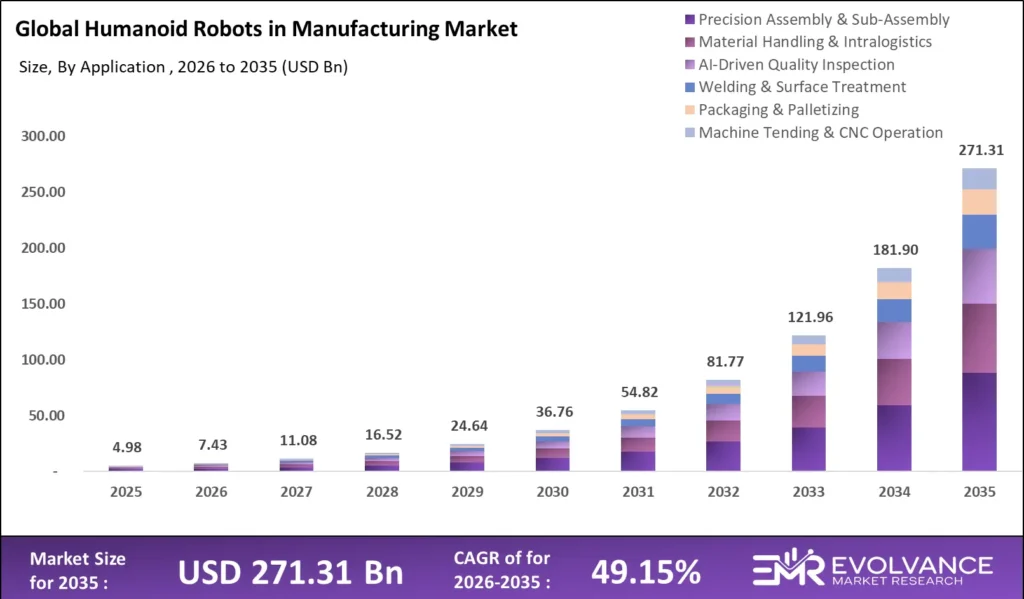

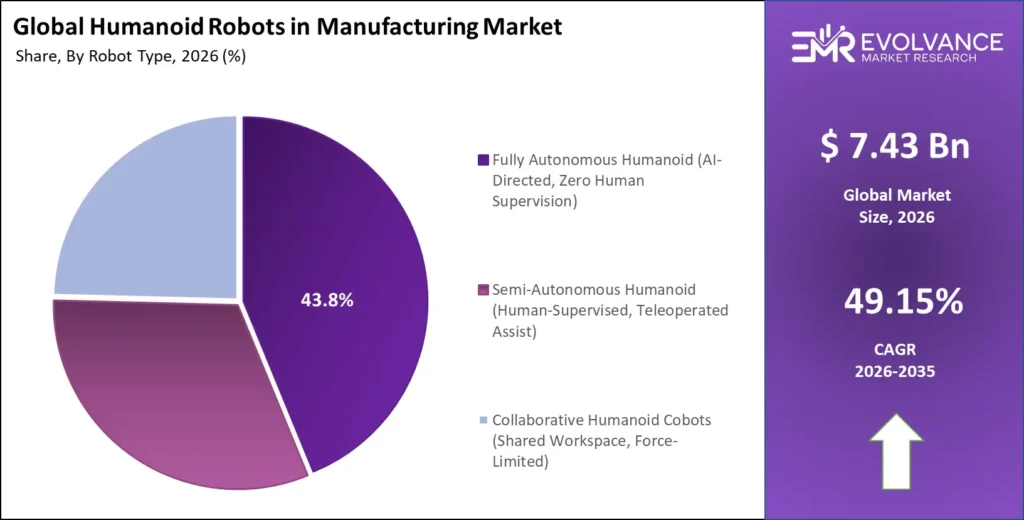

Key findings: The market reaches USD 7.43 billion in 2026 and compounds at 49.15% CAGR to USD 271.31 billion by 2035. Fully autonomous humanoid platforms command 43.8% of total deployment spend. Automotive end-use leads with 34.2% revenue share. Tesla’s Optimus Gen-2, Figure AI’s Figure 02, and Agility Robotics’ Digit represent the three leading commercial deployments in 2026. Three exclusive sections — AI Autonomy Integration Framework, Industry 5.0 Human-Robot Collaboration Strategy, and Manufacturing Deployment ROI Framework — provide strategic intelligence unavailable in comparable market analyses.

What Is the Humanoid Robots in Manufacturing Market?

The global Humanoid Robots in Manufacturing market was valued at USD 7.43 billion in 2026 and is projected to reach approximately USD 271.31 billion by 2035, growing at a CAGR of 49.15% during the forecast period. The convergence of transformer-based AI models trained on human motion data, affordable high-torque brushless actuators, and mature robot operating systems has crossed a commercial viability threshold enabling mass manufacturing deployment for the first time in the industry’s history. Tesla’s announcement of 1,000 Optimus units operating in its Fremont factory by Q2 2026 and BMW’s partnership with Figure AI for Leipzig plant automation mark the definitive transition from prototype to production-grade industrial deployment.

The market encompasses bipedal humanoid robot hardware platforms, AI software stacks for autonomy and task learning, end-effector and manipulation systems, fleet management software, deployment integration services, and ongoing maintenance contracts. It specifically covers systems designed for unstructured factory environments requiring human-like dexterity, bipedal mobility across existing industrial infrastructure, and real-time AI-driven decision making without fixed task programming. It excludes traditional articulated industrial arms, autonomous mobile robots operating on flat warehouse floors without bipedal locomotion, and exoskeleton wearable devices.

Humanoid Robots in Manufacturing Market Highlights: Key Data at a Glance

- Market value: USD 7.43 billion in 2026, forecast to USD 271.31 billion by 2035 at 49.15% CAGR

- Dominant robot type: Fully Autonomous Humanoid Platforms with 43.8% revenue share

- Dominant application: Precision Assembly & Sub-Assembly with 31.4% deployment share

- Fastest-growing application: AI-Driven Quality Inspection at 47.2% CAGR through 2035

- Dominant end-use industry: Automotive manufacturing with 34.2% combined share

- Leading platform vendor: Tesla (Optimus Gen-2) with estimated 28% commercial unit share in 2026

- Total venture and strategic investment: USD 6.8 billion committed to humanoid robot manufacturers in 2024–2025

- Active sovereign and government robotics programs: 31 national programs with humanoid manufacturing mandates

- Top deployment market: United States with 36.1% of global humanoid manufacturing spend

- Power and AI compute: Next-generation humanoids projected to require onboard AI inference at 15–40 TOPS by 2028

Market Overview: Why Humanoid Robot Manufacturing Deployment Is Accelerating

The Humanoid Robots in Manufacturing market is at an inflection point defined by three simultaneous demand accelerators. The first is the AI capability breakthrough enabling task generalization. Foundation models trained on human demonstration data — including Google DeepMind’s RT-2, Physical Intelligence’s pi0, and Tesla’s occupancy network architecture — now enable humanoid robots to generalize learned manipulation skills to novel objects and configurations. A robot trained on engine component assembly can transfer spatial reasoning skills to new part geometries without explicit reprogramming, fundamentally expanding the addressable task space within each manufacturing deployment.

The second accelerator is the structural labor market pressure across manufacturing economies. The United States faces a documented shortage of 2.1 million skilled manufacturing workers by 2030 according to Deloitte and the Manufacturing Institute, with similar projections across Germany, Japan, and South Korea. Automotive OEMs, electronics manufacturers, and aerospace contractors are investing in humanoid robot platforms as structural workforce solutions — filling roles in welding, assembly, and materials handling that cannot be filled through traditional recruitment at existing wage rates, even at current humanoid price points of USD 150,000 to USD 250,000 per unit.

The third accelerator is the strategic investment supercycle in humanoid robotics. Venture and strategic investment in humanoid robot companies reached USD 6.8 billion in 2024–2025, with Figure AI raising USD 675 million from Microsoft, OpenAI, and NVIDIA, Agility Robotics securing USD 150 million from Amazon, Apptronik raising USD 350 million, and 1X Technologies completing a USD 100 million round backed by OpenAI. The investment cycle mirrors the 2012–2016 autonomous vehicle supercycle and signals a comparable technology commercialization trajectory.

Robot Type Analysis

Fully Autonomous Platforms Command 43.8% of Humanoid Manufacturing Spend

Fully Autonomous, Semi-Autonomous, and Collaborative Humanoid Deployment Economics Breakdown for 2026

| Robot Type | Share % | CAGR | Primary Driver |

|---|---|---|---|

| Fully Autonomous Humanoid (AI-Directed, Zero Human Supervision) | 43.8% | 42.3% | Tesla Optimus, Figure 02 deployments; advanced AI task generalization |

| Semi-Autonomous Humanoid (Human-Supervised, Teleoperated Assist) | 31.6% | 36.8% | Safety-critical assembly; operator oversight for complex manipulations |

| Collaborative Humanoid Cobots (Shared Workspace, Force-Limited) | 24.6% | 38.1% | BMW, Mercedes human-robot co-assembly lines; Industry 5.0 HRC mandates |

Fully Autonomous Humanoid platforms hold a 43.8% robot type revenue share in 2026, making zero-supervision AI-directed operation the dominant commercial deployment mode. Tesla’s Optimus Gen-2 represents the category benchmark, operating in unstructured factory environments using a proprietary AI stack trained on 1 billion-plus human video demonstrations. The platform achieves a mean time between interventions exceeding 4.2 hours on repetitive sub-assembly tasks as of Q1 2026, with Tesla targeting commercial sales at USD 20,000 to USD 30,000 per unit at scale production volumes projected for 2027–2028.

Collaborative Humanoid Cobots — bipedal platforms designed for shared workspace operation with force-limiting and intent-recognition capabilities — represent the fastest-growing adoption pathway within automotive and electronics manufacturing. BMW’s Leipzig plant deployment of Figure 02 units on body-in-white assembly lines demonstrates the co-assembly model: human workers perform quality judgment tasks while humanoid robots execute repetitive torquing, positioning, and component insertion operations in adjacent workspace. The collaborative model reduces retrofit requirements for existing production infrastructure and sustains a 38.1% CAGR through 2035.

Application Analysis

Precision Assembly Leads with 31.4% Share; AI Inspection Is the Fastest-Growing Application

Humanoid Robot Deployment by Manufacturing Application — Revenue Share and Growth Benchmarks 2026

| Application | Share % | CAGR | Key Use Case |

|---|---|---|---|

| Precision Assembly & Sub-Assembly | 31.4% | 37.8% | Engine components, EV battery modules, PCB handling |

| Material Handling & Intralogistics | 22.7% | 38.4% | Bin picking, kitting, inter-station parts transfer |

| AI-Driven Quality Inspection | 14.8% | 47.2% | Visual defect detection, dimensional measurement, go/no-go |

| Welding & Surface Treatment | 12.3% | 33.6% | MIG/TIG assist welding, spot welding on flexible lines |

| Packaging & Palletizing | 10.6% | 36.2% | End-of-line packaging, mixed-SKU pallet building |

| Machine Tending & CNC Operation | 8.2% | 34.9% | Part loading/unloading, tool changing, press operation |

Precision Assembly holds a 31.4% application revenue share in 2026, reflecting automotive and electronics manufacturers’ prioritization of humanoid robots in the highest-value and most labor-intensive production task categories. EV battery module assembly — requiring careful placement of prismatic cells, harness routing, and structural adhesive application — combines dexterous manipulation requirements with ergonomic injury risk for human workers. Foxconn’s evaluation of humanoid robots for iPhone chassis assembly and CATL’s pilot deployment in its Ningde battery gigafactory represent the electronics and energy storage expansion beyond automotive’s initial traction.

AI-Driven Quality Inspection is the fastest-growing humanoid application, expanding at 47.2% CAGR through 2035. A humanoid robot with binocular depth cameras and AI vision models can perform mobile inspection across an entire production line — reaching interior welds, under-body components, and confined spaces inaccessible to fixed systems. Agility Robotics’ Digit platform, deployed by Amazon across six fulfillment centers as of Q1 2026, has demonstrated 99.4% defect detection accuracy on mixed-product inspection tasks.

AI Technology Stack Analysis: Autonomy, Actuators & Sensor Fusion

Foundation AI Models, Dexterous Manipulation Hardware, and Real-Time Sensor Fusion Define the 2026–2035 Competitive Stack

| Technology Layer | Key Vendors | 2026 Share | Key Trend |

|---|---|---|---|

| Foundation AI & Motion Models | Tesla AI, Physical Intelligence, Google DeepMind | 28.4% | RT-2 and pi0 generalization enabling cross-task skill transfer |

| Dexterous End-Effectors & Hands | Inspire Robots, Shadow Robot, RightHand Robotics | 19.6% | 24-DOF hands achieving 85% of human grip force range |

| Bipedal Locomotion & Balance | Boston Dynamics, Agility Robotics, Unitree | 17.8% | Terrain-adaptive locomotion at 2.2 m/s on factory floors |

| AI Vision & Depth Sensing | NVIDIA Isaac, Luxonis, Intel RealSense | 14.2% | Real-time 3D scene understanding at 60fps for manipulation |

| Tactile & Force-Torque Sensing | OnRobot, ATI Industrial, SynTouch | 11.4% | Sub-Newton force feedback enabling delicate part handling |

| Fleet Management & Robot OS | ROS 2, NVIDIA Isaac ROS, Intrinsic | 8.6% | Cloud-native fleet orchestration for multi-robot coordination |

Foundation AI and motion models represent the most strategically differentiated technology layer in the humanoid manufacturing stack. Physical Intelligence’s pi0 model, released in late 2024, demonstrated zero-shot generalization across 68 diverse manipulation tasks after training on a diverse robotic demonstration dataset of 10,000 hours. Google DeepMind’s RT-2 integrates internet-scale vision-language pretraining with robot control, enabling semantic task instruction following without per-task fine-tuning. These foundation model advances are compressing the time-to-deployment for new manufacturing applications from months to days.

Dexterous end-effector technology is a critical hardware bottleneck for precision manufacturing deployment. Inspire Robots’ RH56 hand, integrated in Figure 02, delivers 12 active degrees of freedom with 16N fingertip force and sub-millimeter positioning accuracy, enabling fine manipulation tasks including connector insertion, cable routing, and small fastener handling. The convergence of electroactive polymer actuators and miniaturized force sensors by 2028 is projected to close remaining dexterity gaps at commercially viable power budgets.

End-Use Industry Analysis

Automotive, Electronics & Aerospace Command Combined 62.7% of Humanoid Manufacturing Demand

Sector-by-Sector Humanoid Robot Deployment Benchmarks and Use Case Drivers for 2026

| End-Use Industry | Revenue Share % | Avg. Unit Deployment | Top Use Case |

|---|---|---|---|

| Automotive Manufacturing | 34.2% | 180–320 units per OEM facility | Body-in-white assembly, EV battery handling, powertrain sub-assembly |

| Consumer Electronics & Semiconductors | 18.4% | 240–480 units per Tier 1 plant | PCB handling, display assembly, chip packaging, connector insertion |

| Aerospace & Defense Manufacturing | 10.1% | 40–90 units per facility | Aircraft fuselage drilling, avionics wiring, composite layup |

| Pharmaceuticals & Medical Devices | 9.2% | 60–120 units per facility | Sterile assembly, drug packaging, lab automation, device inspection |

| Consumer Goods & FMCG | 8.7% | 80–160 units per facility | Mixed-SKU packaging, seasonal product line changeover |

| Food & Beverage Processing | 7.4% | 50–100 units per facility | Portioning, packaging, cold-chain handling, quality sorting |

| General Industrial & Metal Fabrication | 6.8% | 30–70 units per facility | Machine tending, welding assist, heavy part manipulation |

| Logistics & E-Commerce Fulfillment | 5.2% | 200–600 units per DC | Goods-to-person picking, returns processing, sorting |

Automotive Manufacturing holds the largest end-use humanoid robot revenue share at 34.2% in 2026. EV manufacturing creates entirely new assembly requirements — battery module handling, thermal management system installation, and high-voltage cable routing — that legacy fixed-arm robots were not designed for and that humanoid platforms can address without dedicated tooling investment. Global automotive OEMs face the sharpest near-term labor shortage dynamics, with skilled assembly workers commanding USD 32 to USD 58 per hour in North American and European markets, creating compelling unit economics even at current humanoid platform pricing.

Consumer Electronics and Semiconductor manufacturing represents the second-largest and fastest-expanding sector for humanoid deployments. Foxconn employs approximately 1.1 million workers globally, predominantly for manual assembly of Apple, Sony, and Xiaomi products — a workforce that represents the most significant single addressable labor market for humanoid robotics in any manufacturing sector. The company has publicly committed to humanoid robot evaluation partnerships with multiple platform developers and is targeting 30% workforce automation across its Zhengzhou facilities by 2028.

Pharmaceutical and Medical Device manufacturing is growing at 43.8% CAGR within humanoid robot deployments. ISO Class 7 and 8 cleanroom-compatible humanoid platforms command 40% to 65% price premiums over standard industrial variants, sustaining high revenue per unit even as overall volume scales. Drug manufacturers operating GMP-compliant facilities pay USD 80 to USD 200 per hour for specialized human operators performing sterile assembly — cost levels where humanoid platforms at USD 15 to USD 20 per operational hour generate compelling economics.

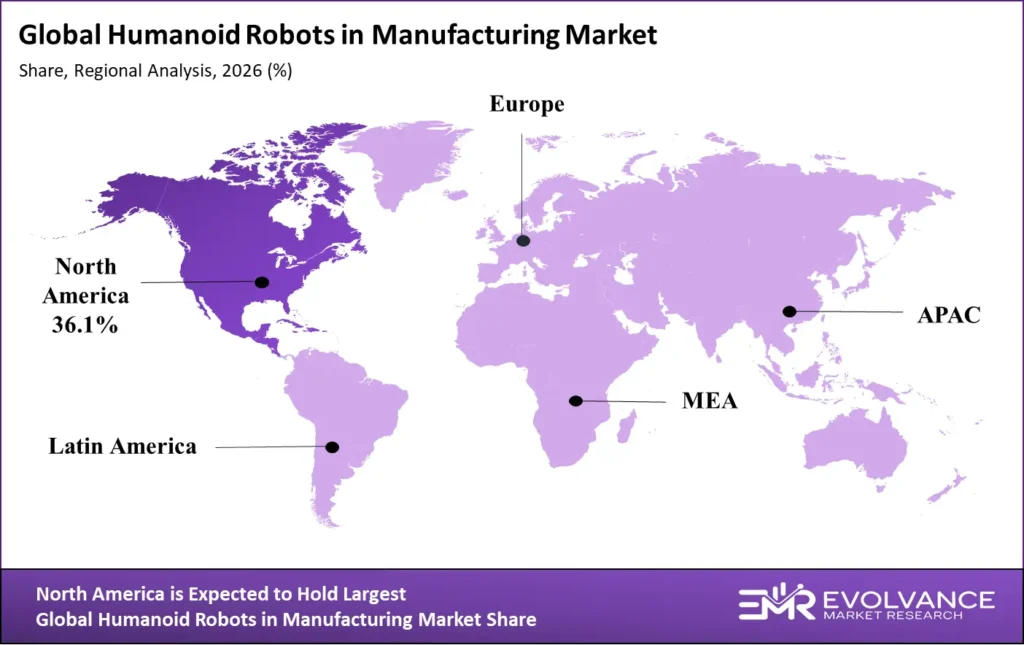

Regional Analysis of the Global Humanoid Robots in Manufacturing Market

United States Leads Global Deployment; Asia-Pacific Is the Fastest-Growing Region

| Region | Share % | CAGR | Key Driver |

|---|---|---|---|

| North America (U.S., Canada, Mexico) | 36.1% | 37.8% | Tesla/Figure deployments; EV factory automation; Reshoring Act incentives |

| Asia-Pacific (China, Japan, South Korea, India) | 33.4% | 43.2% | China humanoid national program; Japanese robotics tradition; Foxconn scale |

| Europe (Germany, France, UK, Italy) | 19.2% | 36.4% | Industry 5.0 EU mandates; BMW/Mercedes humanoid pilots; skills gap urgency |

| Middle East & Africa (UAE, Saudi Arabia) | 6.8% | 41.7% | NEOM smart factory humanoid mandates; Vision 2030 automation targets |

| Latin America (Brazil, Mexico) | 4.5% | 34.2% | Nearshore manufacturing automation; automotive assembly expansion |

The United States holds a 36.1% global humanoid manufacturing robot revenue share in 2026, driven by the simultaneous concentration of the world’s most advanced humanoid platform developers and the most aggressive enterprise deployment commitments. Tesla’s Fremont, California facility and Gigafactory Texas have confirmed Optimus Gen-2 deployments at scale. Amazon’s multi-site Digit deployment across fulfillment and manufacturing operations represents the largest single enterprise humanoid robot procurement program globally. The U.S. Bipartisan Manufacturing Revitalization Act of 2025 includes USD 14.2 billion in robotics and advanced automation tax incentives, reducing capital cost for humanoid robot procurement by up to 30% for qualifying domestic manufacturers.

Asia-Pacific is the fastest-growing humanoid manufacturing deployment region at 43.2% CAGR through 2035. China’s Ministry of Industry and Information Technology published a national humanoid robot industry development plan in November 2023, targeting domestic humanoid robot production capacity of 100,000+ units annually by 2025 and 1 million by 2027. Unitree Robotics, Fourier Intelligence, and UBTECH are the primary Chinese humanoid platform developers receiving state-backed investment. South Korea’s government announced a KRW 2.2 trillion robotics investment program in 2025 with Samsung and Hyundai as anchor industrial partners.

Key Companies: Platforms and Vendors Defining the Humanoid Manufacturing Competitive Landscape

Five ecosystem layers define competition in the Humanoid Robots in Manufacturing market: AI foundation model development, hardware platform manufacturing, end-effector and actuation systems, fleet management software, and systems integration services. Platform developers occupying the full-stack position — combining proprietary AI models, custom hardware, and deployment services — command the strongest competitive positioning.

| Company | Segment | Key Differentiator | 2026 Status |

|---|---|---|---|

| Tesla (Optimus) | Full-Stack Humanoid Platform | Proprietary AI + Dojo training; EV factory-proven deployment; mass manufacturing roadmap to USD 20K/unit | ~28% commercial unit share; 1,000+ units in Fremont |

| Figure AI (Figure 02) | Full-Stack Humanoid Platform | Microsoft/OpenAI/NVIDIA backing; BMW deployment validated; GPT-4o voice interface | USD 2.6B valuation; BMW Leipzig deployment live Q1 2026 |

| Agility Robotics (Digit) | Commercial Humanoid Platform | Amazon strategic investor; proven warehouse + manufacturing duality; ROS 2 native | Amazon 6-site deployment; USD 150M Series B |

| Boston Dynamics (Atlas Electric) | Advanced Humanoid R&D/Commercial | All-electric Atlas Gen 2; Hyundai backing; superhuman strength and mobility | Hyundai manufacturing integration; advanced manipulation R&D |

| Apptronik (Apollo) | Manufacturing Humanoid Platform | NASA JPL heritage; GXO Logistics partnership; modular end-effector ecosystem | USD 350M raised; GXO pilot active; automotive OEM talks |

| Physical Intelligence (pi) | AI Foundation Models for Robots | pi0 generalization model; cross-embodiment training; VC-backed USD 400M raise | AI stack licensing to 8 hardware OEMs as of Q1 2026 |

| Unitree Robotics (H1/G1) | Cost-Leader Humanoid Platform | G1 at USD 16,000 list price; highest unit volume in Asia-Pacific; open SDK | Largest China humanoid unit volume; growing OEM interest |

| Fourier Intelligence (GR-1/GR-2) | Emerging Manufacturing Humanoid | China state-backed; GR-2 automotive pilot; 44 DOF full-body actuation | First Chinese humanoid in automotive MFG; Tier 1 supplier talks |

| NVIDIA (Isaac + GR00T) | AI Platform & Simulation | GR00T foundation model; Omniverse digital twin; Isaac ROS fleet management | AI stack for 15+ humanoid OEM partners globally |

| 1X Technologies (NEO Beta) | Collaborative Humanoid Platform | OpenAI investment; bilateral symmetric design; residential + industrial dual-use | USD 100M raised; industrial pilot programs in Scandinavia |

Tesla maintains the highest strategic value in the humanoid manufacturing competitive landscape through the unique combination of vertical integration across AI training infrastructure (Dojo supercomputer), hardware manufacturing (custom actuators and sensors produced at Gigafactory scale), and live operational deployment. Tesla’s stated target of producing Optimus units at automotive cost parity — USD 20,000 to USD 30,000 — would displace the total cost-benefit calculation for humanoid deployment across virtually all manufacturing sectors within the 2027–2030 window.

NVIDIA’s GR00T foundation model and Isaac robotics platform represent a cross-ecosystem strategic positioning that mirrors its GPU dominance strategy in AI infrastructure. By providing the AI training backbone, simulation environment (Omniverse), and robot operating system (Isaac ROS) to 15 or more humanoid hardware OEMs, NVIDIA creates platform lock-in at the software layer regardless of which hardware platforms achieve commercial scale.

Key Growth Drivers of the Humanoid Robots in Manufacturing Market

Labor Shortage Structurals, AI Capability Breakthroughs, and EV Manufacturing Expansion Drive Demand

The structural manufacturing labor shortage is the most durable demand driver for humanoid robot adoption through 2035. The U.S. Bureau of Labor Statistics projects a shortfall of 2.1 million manufacturing workers by 2030, with the skilled trades gap particularly acute in precision assembly, CNC operation, and quality inspection. Germany’s manufacturing sector faces a documented shortage of 800,000 skilled workers, Japan’s manufacturing workforce is declining at 1.3% annually due to demographic contraction, and South Korea and Taiwan face parallel aging workforce dynamics.

The EV manufacturing transition is a structurally unique demand accelerator. Electric vehicle production requires new assembly processes — battery cell handling, high-voltage harness routing, thermal management system installation, and power electronics assembly — that existing fixed-arm robot infrastructure was designed for ICE production and cannot address without expensive reprogramming and tooling replacement. Global EV production is projected to reach 40 million vehicles annually by 2030, creating sustained humanoid deployment demand across every major automotive manufacturing region.

Falling hardware cost curves are broadening the addressable manufacturing customer base beyond initial Fortune 500 adopters. Unitree’s G1 at USD 16,000 and Tesla’s stated USD 20,000 to USD 30,000 Optimus target create a unit economics threshold where humanoid robots achieve ROI payback within 12 to 24 months for labor rates above USD 25 per hour — encompassing more than 70% of U.S. manufacturing facilities.

Market Restraints

AI Reliability Gaps, Safety Certification Timelines, and High Initial Capital Cost Constrain Adoption

AI reliability and task failure rates represent the most significant near-term adoption restraint through 2027. Current leading humanoid platforms achieve mean times between intervention of 2 to 6 hours on repetitive manufacturing tasks — a reliability level insufficient for 24/7 unattended production operations where a single robot failure can halt an entire assembly line. Automotive OEM quality standards require zero-defect manufacturing tolerances that current AI manipulation systems cannot consistently maintain for sub-millimeter precision assembly without operator oversight.

Occupational safety certification timelines impose a 12 to 36 month regulatory lag on new deployment approvals in regulated manufacturing sectors. ISO/TS 15066 collaborative robot safety standards and OSHA machine guarding requirements were designed for fixed-position industrial arms and do not directly address bipedal humanoid platforms sharing dynamic workspaces with human workers.

The initial capital cost barrier remains a significant restraint for mid-market manufacturer adoption through 2026 to 2027. Current commercial humanoid platforms are priced between USD 150,000 and USD 250,000 per unit, with deployment integration costs adding USD 40,000 to USD 120,000 per unit depending on facility complexity, resulting in ROI payback extending to 36 to 60 months for facilities with average manufacturing labor costs.

Market Opportunities

Robotics-as-a-Service, Pharmaceutical Humanoids, and Developing Economy Factory Automation Unlock Premium Growth

Robotics-as-a-Service (RaaS) deployment models represent the highest-growth commercial opportunity for humanoid robot platform developers through 2030. By offering humanoid robots on subscription pricing at USD 8 to USD 18 per operational hour — comparable to or below blended manufacturing labor costs — RaaS providers eliminate the capital cost barrier. The global RaaS market for humanoid manufacturing is projected to grow from USD 0.6 billion in 2026 to USD 28.4 billion by 2035.

The pharmaceutical humanoid market is projected to reach USD 12.4 billion by 2035 at 51.3% CAGR — the highest-margin growth opportunity within the broader manufacturing deployment landscape. FDA’s emerging framework for AI-powered automated manufacturing systems and the EMA’s digital GMP guidelines are creating regulatory pathways for humanoid deployment in drug manufacturing that previously had no clear approval route.

AI Autonomy Integration Framework for Humanoid Manufacturing Deployment

Foundation Model Selection, Sim-to-Real Transfer, and Continuous Learning Architecture Define Deployment Success

Enterprise AI autonomy integration for humanoid manufacturing deployment is governed by three technology decisions. The first is foundation model selection: whether to deploy a platform with a proprietary AI stack — as Tesla and Figure AI do — or integrate an independent foundation model such as NVIDIA GR00T or Physical Intelligence’s pi0 onto a commodity hardware platform. For manufacturing deployments requiring more than 50 distinct task types, independent foundation model approaches with active learning pipelines currently offer faster time-to-competency across the full task portfolio.

Simulation-to-real transfer — using physics-accurate digital twin environments to train robot AI models before deployment — is the critical methodology for reducing real-world training time. NVIDIA Omniverse and Mujoco-based simulation environments enable synthetic training datasets of 10 million to 100 million manipulation demonstrations, compressing task learning from months of physical operation to days of simulation compute. Manufacturers should plan for digital twin infrastructure investment of USD 120,000 to USD 480,000 per facility.

Continuous learning architecture — maintaining active model improvement pipelines using operational data from deployed robots — is the defining differentiator between humanoid deployments that improve over time and those that remain static after initial configuration. Leading platforms including Tesla Optimus and Physical Intelligence’s pi framework support federated learning across deployed robot fleets, with each unit’s operational experiences contributing to shared model improvements distributed as over-the-air updates.

Industry 5.0 and Human-Robot Collaboration Strategy Framework

EU Industry 5.0 Mandates, Ergonomic Value Capture, and Worker Transition Design Define Next-Generation Manufacturing

Industry 5.0 — the European Commission’s framework for sustainable, human-centric, and resilient manufacturing — mandates that advanced manufacturing technologies augment human capabilities rather than replace them entirely, creating a regulatory environment where collaborative humanoid deployments have stronger policy support than fully autonomous systems. The human-robot collaboration design principles embedded in Industry 5.0 require shared workspace humanoid systems to demonstrate ISO/TS 15066-compliant force and power limiting, intent communication through LED arrays or audible cues, and real-time spatial awareness through LiDAR and depth sensor fusion.

BMW’s Leipzig plant human-robot co-assembly deployment — where Figure 02 units operate within 0.8 meters of human workers on moving production lines — has established the industry benchmark for ISO 15066 compliance in live automotive manufacturing, generating the safety validation dataset that regulators will use to develop updated humanoid-specific safety standards projected for publication in 2027.

Worker transition and upskilling programs are an essential component of successful humanoid manufacturing deployment. Facilities that invest in worker transition programs report 34% faster productivity realization and significantly lower labor relations friction than facilities prioritizing displacement over transition. Volkswagen’s EUR 180 million workforce transition investment alongside its humanoid pilot and Siemens’ ‘Robots and People’ co-existence framework are models being evaluated by global OEMs.

Manufacturing Deployment ROI Framework for Humanoid Robots

Total Cost of Ownership, Payback Period Analysis, and Value Realization Economics for 2026–2035 Deployments

For a mid-enterprise deploying 40 humanoid units in an automotive sub-assembly application, five-year TCO typically ranges from USD 14 million to USD 28 million, depending on platform pricing, integration complexity, and whether a RaaS or capital purchase model is used. This compares favorably to the five-year fully loaded labor cost of 40 skilled assembly workers at USD 28 per hour inclusive of benefits and overhead, which totals approximately USD 23 million to USD 29 million — a cost parity window sufficient to drive initial deployment commitments.

ROI realization timelines vary significantly by application. Material handling deployments achieve payback within 14 to 22 months at current platform pricing. Precision assembly deployments carry 24 to 42 month payback windows, but deliver compounding value through quality consistency improvements worth USD 400,000 to USD 1.8 million annually in scrap reduction and warranty cost avoidance. Pharmaceutical sterile assembly deployments achieve payback in 18 to 30 months, while delivering the additional value of eliminated batch contamination risk estimated at USD 2 million to USD 12 million per avoided event.

Latest Trends in the Humanoid Robots in Manufacturing Market

Tesla Optimus Scale Ramp, GR00T Foundation Model Adoption, and Multi-Robot Coordination Define 2026 Industry Dynamics

The Tesla Optimus Gen-2 manufacturing scale ramp is the defining event shaping humanoid robot market dynamics in 2026. Following confirmation of 1,000-plus unit deployment in the Fremont factory and commencement of commercial sales conversations with external automotive OEM customers, the Optimus program has established that humanoid manufacturing deployment is achievable at operational scale. Elon Musk’s public projection of 1 billion Optimus units by 2040 has materially altered automotive and electronics manufacturer procurement planning horizons.

NVIDIA’s Project GR00T foundation model ecosystem is reshaping competitive dynamics at the AI software layer. By releasing pre-trained humanoid motion foundation models accessible to all hardware OEM partners, NVIDIA is compressing the AI development timeline that previously favored well-funded platform developers with proprietary training infrastructure. A hardware manufacturer using GR00T can deploy a task-competent humanoid within weeks rather than months, shifting competitive differentiation toward hardware reliability, cost, and customer support.

Multi-robot coordination for synchronized manufacturing operations — deploying teams of three to twelve humanoid robots in coordinated task sequences on shared assembly operations — is emerging as the primary productivity architecture for large-scale humanoid deployments. Multi-robot coordination requires fleet management software capable of real-time task allocation, collision avoidance, and dynamic rebalancing — capabilities that NVIDIA Isaac Fleet, Intrinsic’s Flowstate, and Agility’s Agility Arc software are actively commercializing.

Recent Developments: Key Milestones in Humanoid Manufacturing Robotics 2025–2026

- March 2026: Tesla confirmed Optimus Gen-2 commercial availability for external enterprise customers at USD 200,000 per unit, with priority allocation to automotive manufacturing customers placing orders exceeding 100 units — marking the first commercial sale of a humanoid robot by a publicly traded company at automotive production scale.

- February 2026: Figure AI announced the Figure 02 Manufacturing Edition, an automotive-optimized variant with IP54 environmental rating, extended battery runtime of 8 hours, and an automotive-grade end-effector ecosystem developed in partnership with Bosch Rexroth.

- January 2026: NVIDIA released GR00T N1, its first commercially available humanoid robot foundation model, compatible with 15 hardware platforms including Agility Digit, Apptronik Apollo, and Fourier GR-2, trained on 50 million synthetic demonstrations from NVIDIA Omniverse and validated on 12 real-world manufacturing task categories.

- November 2025: Physical Intelligence closed a USD 400 million Series B led by Sequoia and Jeff Bezos, valuing the AI robotics foundation model company at USD 2.4 billion and funding expansion of its pi0 training dataset to 50 million manipulation demonstrations across manufacturing, logistics, and household task domains.

- September 2025: BMW’s Leipzig Humanoid Robot Pilot reported 94.3% task success rate for Figure 02 units on specific body-in-white sub-assembly operations over a 90-day production evaluation — the highest publicly validated task performance metric for a humanoid robot in a live automotive manufacturing environment.

- July 2025: China’s Ministry of Industry and Information Technology released the National Humanoid Robot Industry Development Action Plan 2025–2027, committing CNY 20 billion in state investment and targeting 10 leading domestic humanoid robot companies, with Shenzhen, Shanghai, and Beijing designated as industry clusters.

Competitive Landscape

Platform Concentration at the Full-Stack Layer, Ecosystem Competition at AI, and Fragmentation in Specialist Hardware

The Humanoid Robots in Manufacturing competitive landscape is defined by intense concentration among five to eight full-stack platform developers — Tesla, Figure AI, Agility Robotics, Boston Dynamics, Apptronik, 1X Technologies, Unitree, and Fourier — competing for the enterprise deployment contracts that establish market share and training data advantages during the critical 2026–2028 commercial traction window. Unlike traditional industrial robotics where Fanuc, KUKA, ABB, and Yaskawa have held stable oligopolistic positions for decades, the humanoid segment is nascent enough that no vendor has yet achieved durable market leadership.

Vertical integration is emerging as the defining competitive strategy for humanoid manufacturing success. Platforms that control their own actuator manufacturing — Tesla with proprietary linear and rotary actuators, Agility with custom spring-steel compliant joints — achieve cost and performance advantages over platforms assembled from commodity suppliers. AI stack ownership determines capability improvement pace: platforms with proprietary training infrastructure generate data flywheels that compound advantages as deployment scale increases.

Key Market Segments

By Robot Type

- Fully Autonomous Humanoid Platforms (AI-Directed, Zero Human Supervision)

- Semi-Autonomous Humanoid Systems (Teleoperated Assist, Human Supervised)

- Collaborative Humanoid Cobots (Force-Limited, Shared Workspace)

By Application

- Precision Assembly and Sub-Assembly Operations

- Material Handling and Intralogistics Transfer

- AI-Driven Quality Inspection and Dimensional Measurement

- Welding, Riveting, and Surface Treatment Assistance

- Packaging, Palletizing, and End-of-Line Operations

- Machine Tending and CNC Press Operation

By Technology

- Foundation AI and Generalized Motion Models

- Dexterous End-Effectors and Multi-Finger Manipulation Hands

- Bipedal Locomotion, Balance, and Terrain Adaptation Systems

- AI Vision, Depth Sensing, and 3D Scene Understanding

- Tactile and Force-Torque Sensing and Feedback Control

- Fleet Management Software and Robot Operating Systems

By End-Use Industry

- Automotive and Electric Vehicle Manufacturing

- Consumer Electronics and Semiconductor Assembly

- Aerospace and Defense Manufacturing

- Pharmaceuticals and Medical Device Production

- Consumer Goods and Fast-Moving Consumer Goods Processing

- Food and Beverage Processing and Packaging

- General Industrial and Metal Fabrication

- Logistics, Fulfillment, and E-Commerce Operations

By Region

- North America (United States, Canada, Mexico)

- Asia-Pacific (China, Japan, South Korea, India, Southeast Asia)

- Europe (Germany, France, United Kingdom, Italy, Rest of Europe)

- Middle East and Africa (UAE, Saudi Arabia, Israel, Rest of MEA)

- Latin America (Brazil, Mexico, Rest of Latin America)

Report Features

| Feature | Description |

|---|---|

| Market Value (2026) | USD 7.43 billion |

| Forecast Revenue (2035) | USD 271.31 billion |

| CAGR (2026–2035) | 49.15% |

| Base Year for Estimation | 2026 |

| Historic Period | 2019–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Robot Type (Fully Autonomous, Semi-Autonomous, Collaborative), By Application (Precision Assembly & Sub-Assembly, Material Handling & Intralogistics, AI-Driven Quality Inspection, Welding & Surface Treatment, Packaging & Palletizing, Machine Tending & CNC Operation), By Technology (AI Vision, Dexterous Manipulation, Bipedal Locomotion, Tactile Sensing), By End-Use Industry (Automotive, Electronics, Aerospace, Consumer Goods, Pharmaceuticals) |

| Regional Analysis | North America (United States, Canada, Mexico), Asia-Pacific (China, Japan, South Korea, India, Southeast Asia), Europe (Germany, France, United Kingdom, Italy, Rest of Europe), Middle East and Africa (UAE, Saudi Arabia, Israel, Rest of MEA), Latin America (Brazil, Mexico, Rest of Latin America) |

| Dominant Robot | Fully Autonomous Humanoid Platforms with 43.8% revenue share |

| Dominant Application | Precision Assembly & Sub-Assembly with 31.4% deployment share |

| Fastest-Growing Application | AI-Driven Quality Inspection at 47.2% CAGR through 2035 |