What is the High Content Screening (HCS) Market Size?

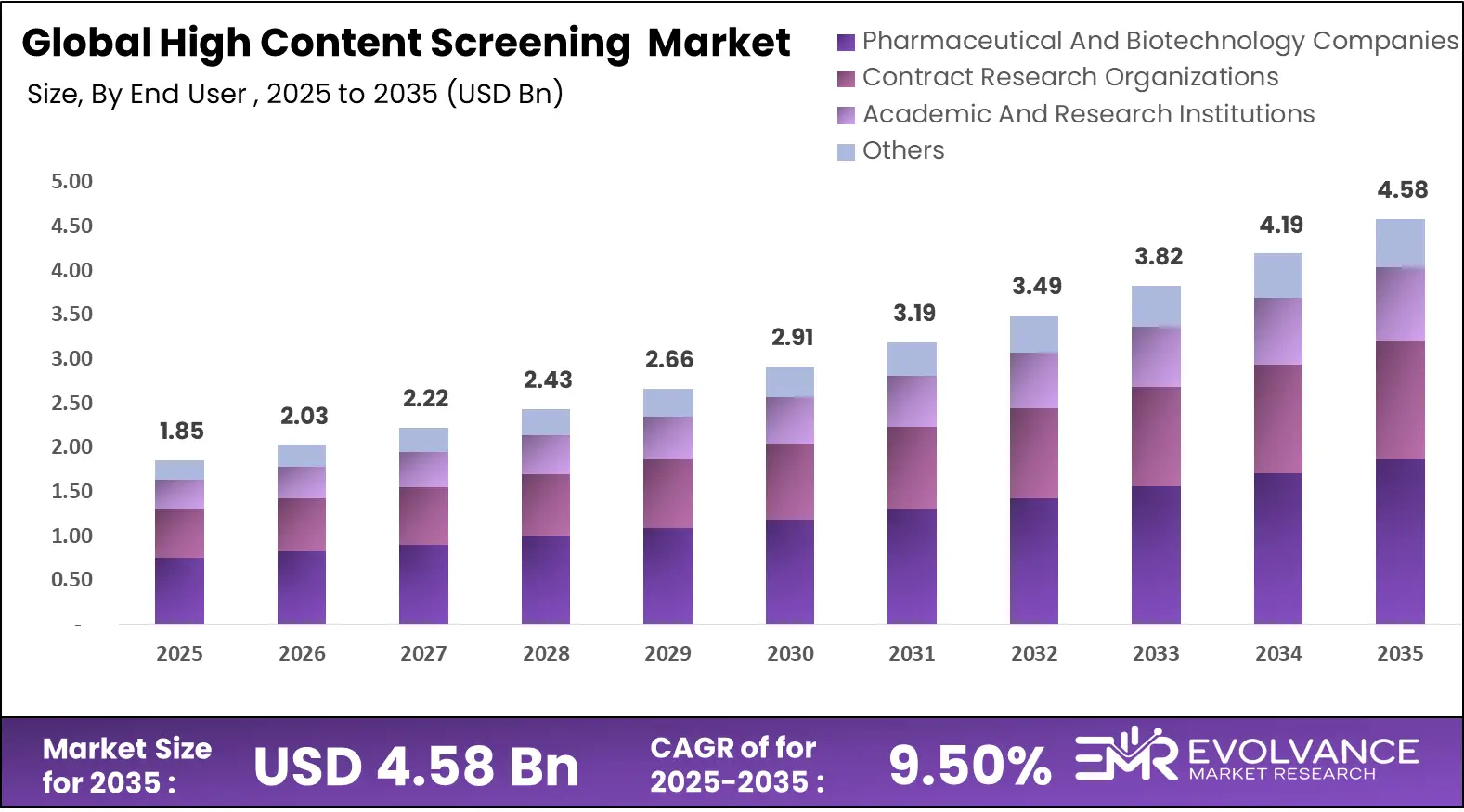

The Global High Content Screening (HCS) Market size is estimated at USD 1.85 billion in 2025 and is expected to grow from USD 2.03 billion in 2026 to nearly USD 4.58 billion by 2035, registering a CAGR of about 9.50% during 2026–2035. High Content Screening represents an advanced cell-based analysis approach that combines automated microscopy, image processing, and data analytics to support drug discovery, toxicology testing, and disease research across pharmaceutical, biotechnology, and academic laboratories globally, driven by high-throughput screening adoption trends worldwide.

Market Highlights

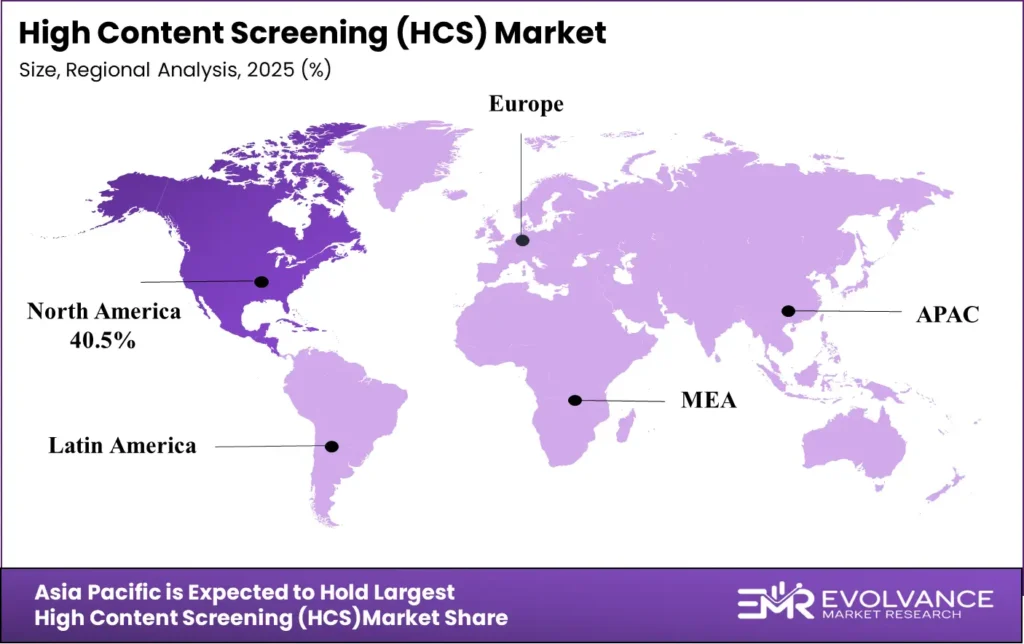

- North America dominated the market, holding the largest share of 40.5% in the market during 2025.

- Asia Pacific is expected to expand at the fastest CAGR of 9.50% between 2026 and 2035.

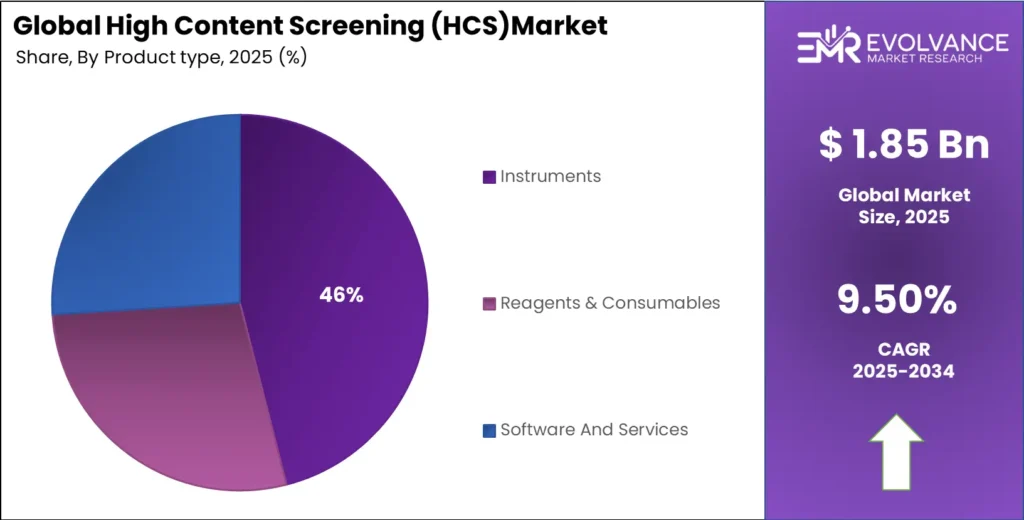

- The instruments segment contributed the biggest market share of 46% in 2025.

- The software & services segment is expected to grow at a remarkable CAGR of 6.9% between 2025 and 2035.

- The drug discovery & development segment held the major market share of 48% in 2025.

- The toxicology testing segment is projected to grow at a remarkable CAGR of 6.6% between 2025 and 2035.

- The pharmaceutical & biotechnology companies segment held the largest market share of 44% in 2025.

- Contract research organizations (CROs) are expanding at a strong rate of 8% CAGR between 2025 and 2035.

Market Size and Forecast

- Market Size in 2025: USD 1.85 Billion

- Market Size in 2026: USD 2.03 Billion

- Forecasted Market Size by 2035: USD 4.58 Billion

- CAGR (2026-2035): 9.50%

- Largest Market in 2025: North America

- Fastest Growing Market: Asia Pacific

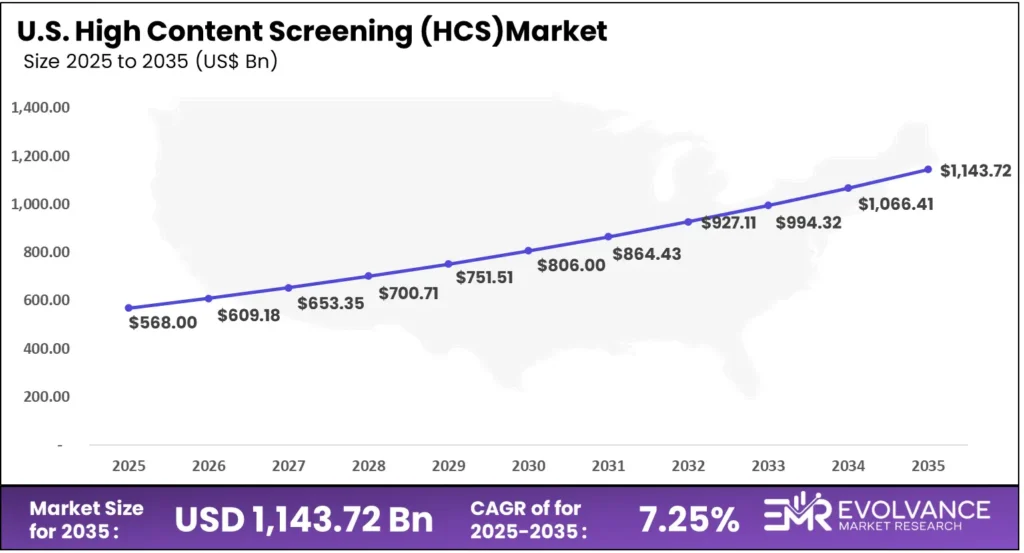

U.S. High Content Screening (HCS) Market Size and Growth 2025 to 2035

The U.S. High Content Screening (HCS) market size is projected at approximately USD 568 billion in 2025 and is expected to grow from around USD 609.18 billion in 2026 to about USD 1,143.72 billion by 2035, expanding at a CAGR of roughly 7.25% over the forecast period. Growth in the U.S. is driven by strong investment in life sciences research, rising demand for phenotypic and high-throughput screening in drug discovery, expanding biotechnology activities, and increasing adoption of advanced imaging and data analytics platforms across pharmaceutical and academic institutions.

What Is the High Content Screening (HCS) market?

The High Content Screening (HCS) market is a global industry focused on advanced cell-based imaging and analytical technologies for studying complex biological processes. HCS combines automated microscopy, fluorescent labeling, robotics, and sophisticated image analysis software to produce quantitative, multiparametric cellular data. Unlike conventional screening methods that assess a single biological endpoint, HCS captures detailed information on cell morphology, protein expression, signaling pathways, and phenotypic changes within one experiment.

The market comprises instruments, reagents, consumables, software platforms, and related services supporting drug discovery, toxicology testing, stem cell research, oncology, and precision medicine. Key end users include pharmaceutical and biotechnology companies, academic institutions, and contract research organizations. Market growth is driven by rising demand for predictive, high-throughput screening solutions, which improve research efficiency, reduce development risks, and enable deeper biological insights across diverse therapeutic areas.

Product Type Insight

Why Instruments Segment Dominate the High Content Screening (HCS) Market?

The Instruments segment dominated the High Content Screening (HCS) market with a share of approximately 46% in 2025, primarily due to its central role in enabling automated, high-resolution cellular imaging across advanced biological workflows. HCS instruments form the foundational infrastructure for screening operations, supporting key applications in drug discovery, toxicity evaluation, and phenotypic analysis.

Pharmaceutical and biotechnology companies continue to prioritize capital investments in advanced imaging platforms, including confocal, spinning-disk, and widefield microscopy systems, to enhance throughput, reproducibility, and experimental precision. These technologies allow simultaneous multiparametric analysis of cellular structures and biological pathways, making them indispensable for modern research pipelines.

Meanwhile, the software and services segment is expected to grow at the fastest rate, with an anticipated CAGR of approximately 6.9% over the forecast period. Growth is fueled by increasing image complexity and expanding data volumes generated by next-generation screening platforms. Advanced analytics, AI-driven image processing, and cloud-based data management tools are becoming essential for optimizing research efficiency and long-term data value.

Application Insights

Why Is the Application Segment Dominating the High Content Screening (HCS) Market?

The application segment dominates the High Content Screening (HCS) market due to its direct impact on decision-making across drug discovery, development, and translational research workflows. The drug discovery & development segment held the largest revenue share of approximately 48% in 2025, highlighting reliance on multiparametric screening to support modern R&D strategies.

Pharmaceutical and biotechnology companies use HCS for target identification, lead optimization, and mechanism-of-action studies, where single-endpoint assays fail to capture complex cellular behavior. HCS platforms enable simultaneous analysis of cell morphology, signaling pathways, and phenotypic responses, making application-driven screening central to early-stage research.

Toxicology testing strengthens segment dominance by allowing early detection of off-target effects and cytotoxicity. The toxicology testing segment is expected to expand with a CAGR of 6.6%, driven by predictive, cell-based safety models and regulatory requirements.

Growing adoption in phenotypic, oncology, and stem cell research further fuels demand. Overall, the application segment reflects a shift toward outcome-focused screening that transforms complex biological data into actionable insights, solidifying its central role in the HCS market.

End User Insights

Which End User Segment Led the High Content Screening (HCS) Market?

The pharmaceutical and biotechnology companies segment led the High Content Screening (HCS) market, reflecting its key role in driving demand for advanced cell-based analysis. In 2025, this end-user group dominated the market with a share of approximately 44%, supported by sustained R&D investment and the need for predictive screening in drug discovery pipelines.

These organizations rely on HCS to improve early-stage research efficiency, where accurate biological insight reduces downstream development risk. HCS enables multiparametric analysis of cellular responses, assessing morphology, viability, signaling pathways, and phenotypic changes simultaneously, which is crucial for complex therapeutic areas like oncology and immunology.

Strong financial capacity allows investment in high-cost imaging systems, specialized reagents, and advanced analytics platforms. Large-scale programs require automated, standardized screening systems for high sample volumes with reproducibility.

The contract research organizations (CROs) segment is expected to witness the fastest growth with a CAGR of 8%, driven by outsourcing and cost-efficiency strategies. Pharmaceutical and biotechnology firms maintain dominance due to scale, funding strength, and integration of HCS into commercial drug development.

Segments Covered in the Report

By Product Type

- Instruments

- Reagents & Consumables

- Software & Services

By Application

- Drug Discovery & Development

- Primary & Secondary Screening

- Target Identification & Validation

- Toxicology Testing

- Phenotypic/Stem Cell/Cancer Research & Others

By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Other Users

Regional Insights

Why Does North America Dominate the High Content Screening (HCS) Market?

North America leads the High Content Screening (HCS) market due to its advanced life sciences ecosystem, research infrastructure, and early adoption of high-end screening technologies. In 2025, the region held approximately 40.5% share of the global market, reflecting leadership in pharmaceutical innovation and biotechnology research.

The presence of numerous pharmaceutical, biotech companies, and academic institutions drives HCS adoption in drug discovery, cancer, neuroscience, and stem cell research. Supportive government funding, regulatory focus on predictive toxicology, and investments in AI-enabled image analytics and cloud-based data platforms further enhance scalability, accuracy, and collaboration. North America’s dominance stems from innovation, funding, and widespread integration of advanced screening methodologies.

Why Is the Asia Pacific Leading the Charge in the High Content Screening (HCS) Market?

Asia Pacific is rapidly becoming one of the fastest-growing regions in the High Content Screening (HCS) market due to expanding life sciences research, increasing R&D investments, and rising adoption of advanced screening technologies. In 2025, the region held a significant portion of the global market and is projected to grow at a CAGR of around 9% from 2026 to 2035, outpacing several established markets.

Growth is driven by the expansion of pharmaceutical, biotechnology, and contract research sectors across China, India, Japan, and South Korea. Governments are prioritizing biomedical research and infrastructure development, enabling institutions and biotech firms to invest in automated HCS platforms. Increasing academic and translational research, alongside AI-driven image analysis and cloud-based data management integration, is further strengthening regional market momentum.

Latin America – High Content Screening (HCS) Market

Latin America is witnessing gradual growth in the High Content Screening market, driven by expanding pharmaceutical research, improving laboratory infrastructure, and rising participation in clinical studies. Brazil and Mexico are leading adoption, supported by academic collaborations and increasing investment in biotechnology and translational research initiatives.

Europe – High Content Screening (HCS) Market

Europe represents a mature and innovation-driven HCS market, supported by strong academic networks, advanced research infrastructure, and regulatory emphasis on predictive toxicology models. Countries such as Germany, the UK, and France contribute significantly through sustained R&D funding and growing adoption of AI-enabled screening technologies.

Middle East & Africa (MEA) – High Content Screening (HCS) Market

The MEA High Content Screening market is developing steadily, supported by healthcare modernization, research partnerships, and emerging biotechnology initiatives. Gulf countries are investing in laboratory automation and biomedical research, while academic institutions across the region are gradually expanding capabilities in cell-based screening applications.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- ASEAN Countries

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of MEA

Top High Content Screening (HCS) Companies

Thermo Fisher Scientific: Thermo Fisher Scientific leads the HCS market with integrated imaging instruments, reagents, and analytics software. In 2025, it is estimated to hold approximately 18–20% of global HCS installations, supported by scalable platforms and strong service networks.

Revvity (formerly PerkinElmer Life Sciences): Revvity focuses on phenotypic screening, automated imaging, and multiparametric analysis. Its solutions are widely used in drug discovery and academic research, with an estimated 14–16% market share in 2025 due to continuous innovation and client relationships.

Danaher Corporation (Molecular Devices): Danaher, via Molecular Devices, offers flexible imaging platforms and high-content analysis software. Its systems ensure reproducibility and workflow integration. In 2025, it represents approximately 11–13% of the HCS market, supported by CRO and pharma adoption.

Becton, Dickinson and Company (BD): BD integrates automated imaging, standardized consumables, and data solutions for HCS. Widely used in regulated research, the company is estimated to hold around 8–10% of the global market in 2025.

Top Key Players in the Market

- Thermo Fisher Scientific Inc.

- Danaher Corporation

- Becton, Dickinson and Company (BD)

- PerkinElmer Inc.

- Agilent Technologies, Inc.

- Carl Zeiss AG

- Merck KGaA

- GE Healthcare

- Bio-Rad Laboratories, Inc.

- Tecan Trading AG

- Yokogawa Electric Corporation

- Nikon Corporation

- Sartorius AG

- Corning Incorporated

- Revvity, Inc.

- Other Major Players

High Content Screening (HCS) Market Outlook

- Industry Growth Overview: The High Content Screening (HCS) economy is growing steadily, driven by demand for phenotypic screening, expanding drug discovery programs, automated imaging platforms, and AI-enabled analytics enhancing research efficiency.

- Sustainability Trends: Sustainability in HCS focuses on reducing reagent waste, improving energy-efficient imaging systems, reusable microplates, and software optimization to minimize repeat experiments while maintaining scientific productivity and operational cost efficiency.

- Major Investors: Major investors include life science venture capital firms, pharmaceutical corporate R&D units, imaging technology funds, and public research programs supporting platforms integrating AI analytics and scalable data management solutions.

- Startup Economy: The HCS startup ecosystem includes innovators in AI-based image analysis, cloud-native data platforms, and advanced assays, collaborating with CROs and academic labs to accelerate commercialization and technology adoption.

Key Market Trends

- AI-Enhanced Analysis: AI and machine learning improve image interpretation accuracy and automate pattern detection, accelerating biological insights from high-content datasets.

- Cloud Data Integration: Cloud platforms enable scalable storage and remote collaboration, facilitating real-time analysis across global research teams.

- Multiparametric Assays: Growing use of multiplexed assays enhances throughput and reveals complex cellular responses in a single experiment.

- Phenotypic Screening Focus: Increased demand for phenotypic screening supports discovery of novel therapeutic mechanisms beyond target-based approaches.

- Miniaturization: Smaller, high-density formats reduce reagent use and enable cost-effective, high-throughput workflows.

- Collaborative Ecosystems: Partnerships between academia, startups, and industry broaden application development and technology adoption.

- Automated Workflows: Robotics and automation reduce manual intervention, increasing reproducibility and lowering operational errors.

- Regulatory Alignment: Greater emphasis on standardized imaging and data practices drives compliance and cross-laboratory data comparability.

- Advanced 3D Cell Models: Increasing adoption of 3D cell cultures and organoids improves physiological relevance and enhances predictive accuracy in screening workflows.

Market Value Chain Analysis in High Content Screening (HCS)

- Technology & Component Development: The HCS value chain begins with developing imaging instruments, optical components, reagents, and labeling technologies. Innovations focus on improved resolution, automation, assay compatibility, and multiplexing, providing the foundational tools for accurate, high-content cellular analysis in research.

- Platform Integration & Software Enablement: Integrated HCS platforms combine instruments with image acquisition software, workflow automation, and analytics tools. AI-driven image analysis, scalable data processing, and cloud connectivity transform raw images into structured, interpretable datasets, enabling downstream research applications and actionable biological insights.

- Distribution, Deployment & Services: Manufacturers and distributors supply HCS systems to pharmaceutical firms, CROs, and academic labs. Installation, training, maintenance, and regulatory support ensure high adoption, system performance, and operational efficiency across diverse laboratory environments and research workflows.

- End-User Application & Insight Generation: End users leverage HCS for drug discovery, toxicology, and phenotypic research, generating actionable insights, reducing experimental risks, improving decision-making, and accelerating research timelines, highlighting the strategic role of HCS in modern life sciences R&D.

Recent Developments

- March 2025 – AI-Augmented Screening Software Launch: In March 2025, a leading HCS software developer introduced an AI-augmented analytics platform that significantly reduces image processing time and enhances morphological feature detection. This development enables researchers to interpret high-dimensional cellular data with higher confidence and faster turnaround, especially in phenotypic and oncology screening workflows.

- July 2025 – High-Throughput 3D Cell Model Integration: July 2025 saw major instrument manufacturers expand HCS platforms to fully support 3D cell models and organoid assays. These enhancements allow automated imaging and analysis of more physiologically relevant biological models, improving predictive accuracy in drug safety and efficacy studies.

- November 2025 – Cloud-Native Data Collaboration Tools: In November 2025, several HCS vendors rolled out cloud-native data collaboration tools designed for secure, real-time sharing of screening results between geographically dispersed research teams. These tools help accelerate multi-center drug discovery programs and improve cross-institution data standardization.

- February 2026 – Modular Automation System Release: In February 2026, an HCS instrumentation provider launched a modular automation system that integrates robotics, liquid handling, and imaging in a single workflow. This upgrade streamlines high-volume screening experiments, reduces manual steps, and increases reproducibility in large-scale screening campaigns.

Market Scope

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | US$ 1.85 Billion |

| Market Size in 2026 | US$ 2.03 Billion |

| Market Size by 2035 | US$ 4.58 Billion |

| Market Growth Rate from 2025 to 2035 | 9.50% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2025 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Instruments, Reagents & Consumables, Software And Services), By Application (Drug Discovery And Development, Primary And Secondary Screening, Target Identification And Validation, Toxicology Testing, Phenotypic, Stem Cell And Cancer Research, And Others), By End User (Pharmaceutical And Biotechnology Companies, Contract Research Organizations, Academic And Research Institutions, And Other End Users) |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |