What is the Hair Oil Market Size?

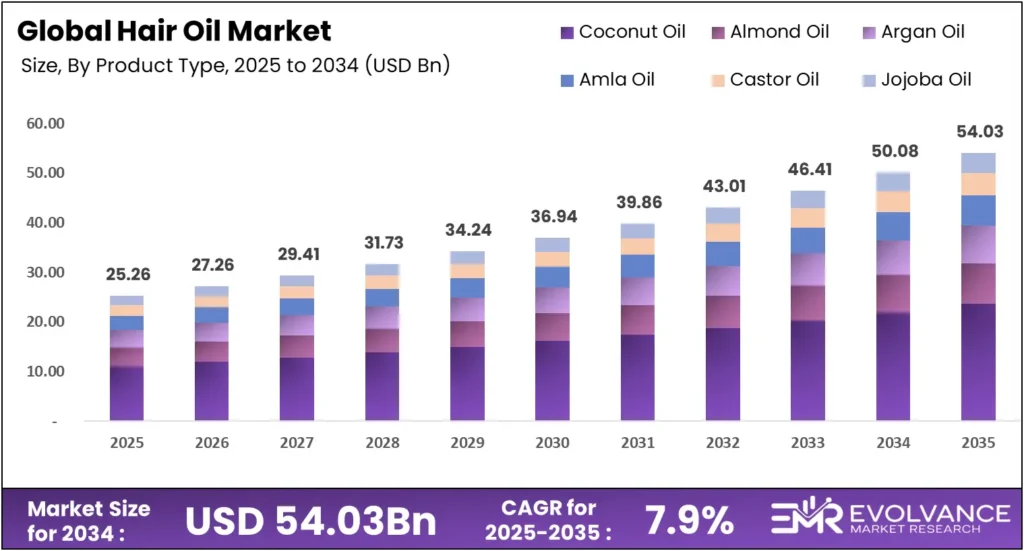

The global hair oil market will reach USD 54.03 billion by 2035, up from USD 25.26 billion in 2025, growing at a CAGR of 7.9% over the forecast period 2026 to 2035. Surging consumer demand for natural and Ayurvedic formulations across Asia Pacific and North America drives this expansion. Scalp health positioning and premium oil-infused treatment formats are pulling category value upward across both mass and prestige channels.

Market Highlights

- The global hair oil market is valued at USD 25.26 billion in 2025, reaching USD 54.03 billion by 2035 at a CAGR of 7.9%.

- Coconut Oil leads the By Product Type segment with 43.8% revenue share, driven by deep cultural adoption across South and Southeast Asia.

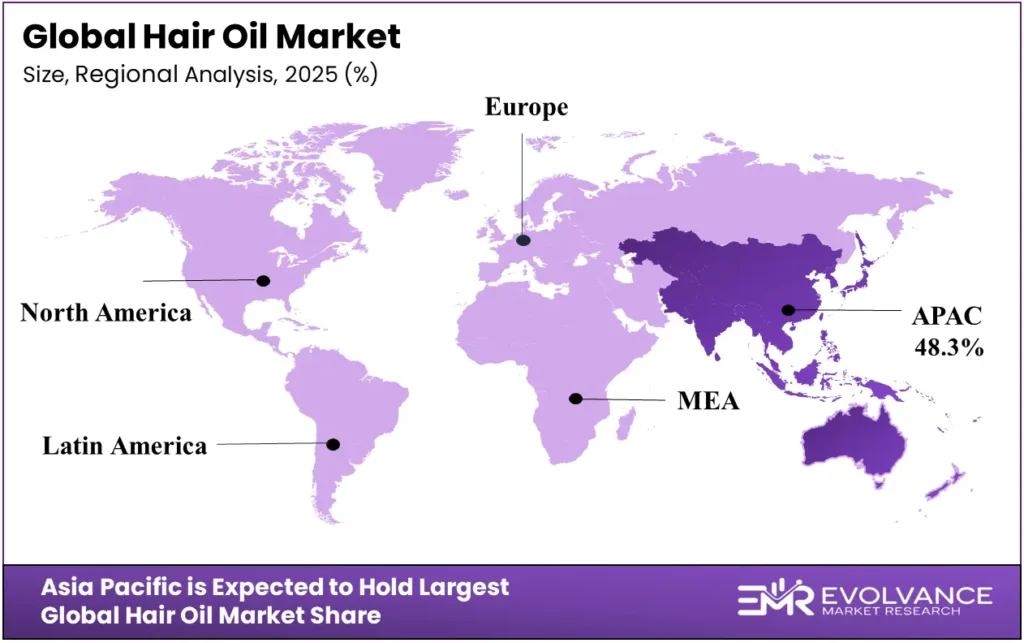

- Asia Pacific dominates the global hair oil market with 48.3% revenue share, valued at USD 12.12 billion in 2025.

- Individual application holds 71.5% revenue share, confirming household consumers as the primary demand engine ahead of commercial buyers.

- Women account for 66.89% of end-user revenue, though men’s grooming and baby/kids segments are emerging as secondary growth pockets.

- Non-Medicated formulations hold 64.2% revenue share, while Herbal/Ayurvedic and Natural/Organic formats are the fastest-repositioning sub-categories.

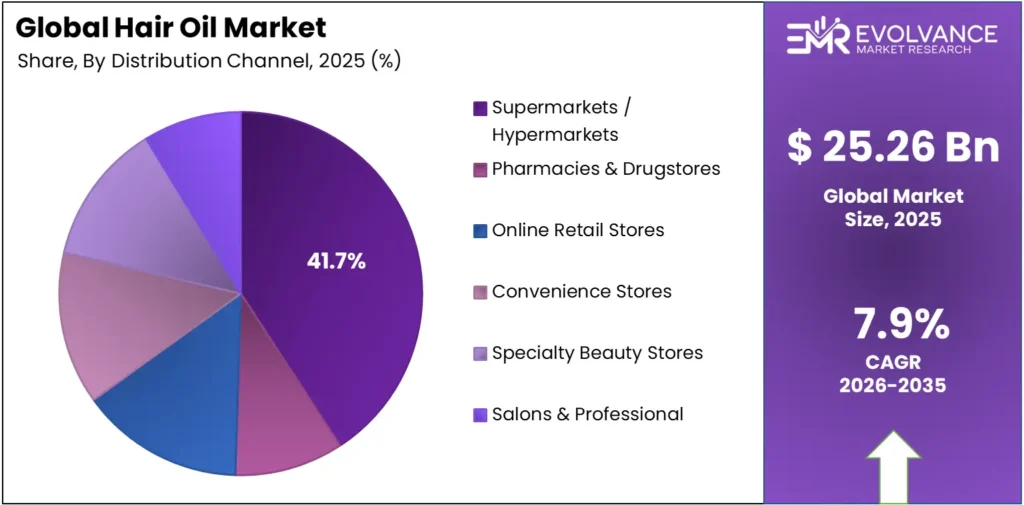

- Supermarkets and hypermarkets account for 41.7% of revenue, although online retail is the channel growing fastest across all regions.

Market Overview

The hair oil market covers oil-based products applied to scalp and hair for nourishment, treatment, and styling — spanning medicated, herbal, Ayurvedic, natural, and synthetic formulations. This hair oil market analysis includes individual consumers, commercial buyers such as salons and spas, and residential users across mass-market and prestige channels globally.

This analysis draws on primary fieldwork, company filings, trade data, and expert interviews across key markets. Evolvance market research analysts found consistent multi-use behavior patterns across 5 regions and 11 segment groups, combining bottom-up demand modeling with analyst validation to produce a forecast grounded in original fieldwork — not aggregated public sources.

Hair oil solves scalp dryness, hair fall, dandruff, and breakage — problems that cut across income levels, geographies, and age groups. Personal care brands, pharmaceutical companies, salon chains, and D2C platforms all compete for share — with hair care product for hair growth and fall control forming the core positioning across all tiers.

Consumer preference for natural hair oil is shifting toward multi-use formats. According to Marico’s 2024 investor reports, 64.7% of consumers surveyed use oil overnight—treating it as therapy rather than styling. 41.2% use it as a pre-shampoo treatment. Dabur’s 2024 survey of 8,600 users reports that 72.4% of Ayurvedic oil consumers apply it overnight.

Product Type Analysis

Coconut Oil dominates, accounting for 43.8%, owing to cultural entrenchment and mass-market affordability.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Coconut Oil | 43.8% | Cultural adoption, affordability, dual use |

| Almond Oil | N/A | Premium nourishment, vitamin E claims |

| Argan Oil | N/A | Frizz control, prestige positioning |

| Amla Oil | N/A | Ayurvedic heritage, hair fall claims |

| Castor Oil | N/A | Hair growth, thick texture adoption |

| Jojoba Oil | N/A | Scalp balance, lightweight formulation |

| Olive Oil | N/A | Mediterranean heritage, moisture repair |

| Onion Oil | N/A | Social media trend, anti-hairfall claim |

| Rosemary Oil | N/A | TikTok-driven growth, scalp stimulation |

| Bhringraj-based blends | N/A | Ayurvedic scalp revival claims |

| Brahmi formulations | N/A | Stress-relief and cognitive hair care |

| Sesame Oil (til) | N/A | Traditional use, South Asian markets |

| Black Seed Oil (Kalonji) | N/A | Middle East demand, anti-inflammatory claims |

In 2025, Coconut Oil held a dominant market position in the By Product Type segment of the Hair Oil Market, with a 43.8% share. Price-per-use economics favor coconut oil strongly in rural and semi-urban markets across India, Indonesia, and the Philippines. Its dual role as an overnight scalp treatment and a household cooking staple keeps penetration structurally high, insulating volume from premium trade-up pressure.

Almond Oil carries the highest margin within the mid-premium product tier, positioned around vitamin E nourishment and lightweight texture claims. This sub-segment performs strongest in urban India and the Middle East, where consumers trade up from plain coconut without moving to prestige price points. Bajaj Consumer Care’s almond anti-hairfall oil reached INR 785 crore in fiscal year 2024, up 11.3%.

Argan Oil differentiates through prestige positioning in frizz control and shine — primarily in European and North American specialty and pharmacy channels. Supply concentration in Morocco creates structural price risk: production fell 18.6% in 2024 to 5,600 tonnes, pushing prices up 38.9%. Brands without fixed-price supply contracts face margin compression through the forecast period.

Amla Oil serves as the entry point for Ayurvedic hair oil positioning, anchoring anti-hairfall claims rooted in centuries of South Asian traditional use. Marico’s Ayurvedic blend line — which includes Amla alongside Bhringraj and Brahmi — reached INR 1,240 crore in fiscal year 2024, growing 14.6%, confirming that heritage ingredient blends outperform single-ingredient Amla products in premium urban segments.

Onion Oil serves as a case study in social media-driven demand volatility — Google Trends interest peaked at a score of 78 in March 2024 before collapsing to 24 by December. Dabur’s Vatika onion oil launched in January 2024 reaching only INR 45 crore by March, declining to INR 18 crore by December — demonstrating that trend-first SKUs without core portfolio support face rapid revenue collapse.

Rosemary Oil is the fastest-rising ingredient sub-segment globally, driven by TikTok’s #rosemaryhairoil hashtag reaching 4.2 billion views in 2024 — a 133.3% increase from 2023. Amazon US rosemary oil search volume rose 284.6% in the same period, with 45 new product launches in Q4 2024 alone. Brands with fast formulation pipelines captured a disproportionate share during the peak-demand window.

Application Analysis

Individuals dominate, accounting for 71.5%, owing to globally embedded household hair-oiling rituals.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Individual | 71.5% | Household ritual, personal care routine |

| Commercial | N/A | Salon treatment protocols, professional use |

| Residential | N/A | Family-size bulk buying, rural penetration |

In 2025, Individual held a dominant market position in the By Application segment of the Hair Oil Market, with a 71.5% share. Marico’s 2024 survey of 12,400 urban Indian consumers found 64.7% use oil overnight and 41.2% as a pre-shampoo treatment — confirming that individual consumers treat oil as a multi-step therapy tool rather than a single-use product. Brands that align packaging and messaging with multi-application behavior capture higher usage frequency per buyer.

Commercial application — covering salons, spas, and professional hair clinics — is the fastest-growing application tier in prestige markets despite its smaller volume share. Professional channel oils command higher unit prices and benefit from stylist endorsements, which drive trial among consumers who would not otherwise self-select premium formats at retail. Estée Lauder’s Aveda Dry Remedy oil recorded 76,000 salon treatments monthly globally in 2024, confirming the commercial channel’s role as a premium conversion engine.

The residential application covers family-size and bulk-format purchases, primarily in rural and semi-urban markets across South Asia and Africa, where shared household use drives larger pack sizes and value-tier pricing. This sub-segment is structurally price-sensitive and brand-loyal by habit rather than by preference — meaning distribution access and shelf presence outweigh product innovation in driving residential segment volume.

Function / Concern Analysis

Hair Nourishment dominates with 37.9% due to universal cross-demographic moisture and strength demand.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Hair Nourishment | 37.9% | Universal moisture and strength demand |

| Anti-hairfall | N/A | Urban stress, pollution, and nutritional gaps |

| Anti-dandruff | N/A | Scalp hygiene, medicated oil demand |

| Scalp Health / Revitalizing | N/A | Skincare-grade ingredient crossover |

| Styling & Frizz Control | N/A | Humidity markets, texture management |

| Heat / UV Protection | N/A | High sun exposure, blow-dry culture |

| Color Protection | N/A | Rising color treatment penetration |

| Anti-aging / Graying Prevention | N/A | Aging population, premium positioning |

In 2025, Hair Nourishment held a dominant market position in the By Function/Concern segment of the Hair Oil Market, with a 37.9% share. Nourishment claims span the widest consumer base—from budget coconut oil users in rural India to premium argan oil buyers in Western Europe—making this the most defensible positioning for mass-market brands. Critically, nourishment claims require no clinical evidence threshold, thereby reducing regulatory exposure relative to medicated sub-segments.

Anti-hairfall exhibits the highest purchase urgency of any functional sub-segment, driven by urban stress, exposure to pollution, and nutritional gaps across India, China, and the UAE. Marico’s Parachute Advansed anti-hairfall oil reached INR 2,450 crore in fiscal year 2024, growing 9.4% — confirming that brands repositioning existing oil lines with anti-hairfall claims access a premiumization lane without requiring full new product development.

Anti-dandruff sits at the intersection of cosmetic and medicated positioning, attracting both personal care and pharmaceutical distribution strategies. Dabur’s Vatika anti-dandruff oil reached INR 675 crore in fiscal year 2024, up 12.8%. India’s CDSCO tightened testing requirements for medicated anti-dandruff oils in 2024, raising compliance barriers — a development that benefits established players with existing pharmaceutical-grade testing processes over new entrants.

Scalp Health / Revitalizing is the fastest-growing functional sub-segment in prestige markets, driven by the crossover of skincare-grade actives — including prebiotics, ceramides, and peptides — into hair oil formulations. L’Oréal’s scalp-focused products grew 18.4% in 2024 versus traditional oil growth of 7.1%, signaling that scalp health positioning commands a category growth premium of more than double the standard nourishment rate.

Material / Texture Analysis

Light Hair Oil accounts for 38.9% due to a non-greasy, daily-use preference in urban markets.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Light Hair Oil | 38.9% | Daily use, non-greasy urban preference |

| Heavy Hair Oil | N/A | Overnight treatment, rural traditional use |

| Cooling Hair Oil | N/A | Menthol demand, Ayurvedic scalp relief |

| Serum-oil hybrids | N/A | Prestige crossover, salon-inspired formats |

In 2025, Light Hair Oil held a dominant market position in the By Material/Texture segment of the Hair Oil Market, with a 38.9% share. Urbanization drives this dominance structurally — commuters and office workers in South and Southeast Asia reject heavy oils that leave visible residue on hair or clothing. Lightweight formulas also function as leave-in treatments and heat protectants, expanding usage occasions beyond the traditional pre-shampoo window.

Heavy Hair Oil serves as the traditional overnight treatment format, maintaining its strongest position in rural India, Bangladesh, and East Africa where pre-shampoo oiling rituals remain the primary hair care behavior. Rural India’s hair oil household penetration was 89.6% in 2024, confirming that heavy oil formats retain a structurally large and stable volume base even as urban preferences shift toward lighter alternatives.

Cooling Hair Oil differentiates through menthol- and camphor-based scalp-relief claims, addressing a specific consumer need for scalp heat reduction in tropical and subtropical markets. Emami’s Navratna cooling oil — the category’s dominant brand — reached INR 876 crore in fiscal year 2024, up 8.4%, confirming that cooling formats command strong repeat purchase behavior anchored by sensory experience rather than ingredient trend cycles.

Serum-oil hybrids carry the highest per-unit price point within the texture segment, blending silicone or water-phase carriers with active oil ingredients to deliver scalp-science benefits in a non-greasy, instantly absorbed format. This sub-segment is the primary growth vehicle for prestige brands entering the hair oil category from skincare, and it commands pharmacy and specialty beauty channel placement that mass-market heavy oils cannot access.

Formulation / Category Analysis

Non-Medicated dominates with 64.2% due to mass accessibility and broad retail channel placement.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Non-Medicated | 64.2% | Mass accessibility, no regulatory threshold |

| Medicated | N/A | Anti-dandruff, scalp condition treatment |

| Herbal / Ayurvedic | N/A | Natural positioning, India export growth |

| Natural / Organic | N/A | Clean beauty demand, Western markets |

| Synthetic / Conventional | N/A | Cost efficiency, mass-market price points |

| Cold-Pressed / Virgin | N/A | Premium purity claims, D2C positioning |

In 2025, Non-Medicated held a dominant market position in the By Formulation/Category segment of the Hair Oil Market, with a 64.2% share. Lower regulatory burden, wider retail placement, and broad demographic appeal keep non-medicated products firmly in volume leadership. This category absorbs the most ingredient innovation — natural, cold-pressed, and herbal sub-segments all sit within the non-medicated tier, widening its competitive scope continuously.

Medicated formulations carry clinical positioning for scalp conditions including dandruff, seborrheic dermatitis, and fungal infections, placing them in pharmacy and drugstore channels with higher margin potential than mass-market oils. India’s CDSCO guidelines issued in 2024 now require medicated anti-dandruff oils to undergo pharmaceutical-level testing, raising compliance costs and consolidating the sub-segment around established players with existing regulatory infrastructure.

Herbal / Ayurvedic formulations represent the fastest-growing sub-category by revenue growth rate, driven by India’s USD 845 million Ayurvedic hair oil export performance in fiscal year 2024 — up 24.6% — with the UAE, USA, and UK as top destination markets. This sub-segment benefits from dual positioning as both a cultural heritage product for South Asian diaspora consumers and a natural wellness product for Western clean beauty buyers.

Natural / Organic formulations differentiate through ingredient purity and sustainability claims, targeting Western prestige consumers who apply skincare-level sourcing standards to hair care purchases. Premium hair oils above INR 500 per 200ml in India grew 18.6% in fiscal year 2024, while value oils grew just 4.2% — confirming that natural and organic positioning is the primary driver of category premiumization across both emerging and developed markets.

Distribution Channel Analysis

Supermarkets/Hypermarkets dominate, accounting for 41.7% due to footfall, shelf visibility, and impulse purchase behavior.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Supermarkets / Hypermarkets | 41.7% | Footfall, shelf visibility, promotions |

| Pharmacies & Drugstores | N/A | Medicated oils, clinical trust signals |

| Online Retail Stores | N/A | D2C growth, ingredient discovery trends |

| Convenience Stores | N/A | Last-mile rural and urban top-up buying |

| Specialty Beauty Stores | N/A | Premium trial, expert recommendation |

| Salons & Professional | N/A | Professional endorsement, treatment use |

In 2025, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the Hair Oil Market, with a 41.7% share. Physical retail shelf space remains the primary discovery mechanism for mass-market consumers across Asia Pacific, Africa, and Latin America. Marico, Dabur, and Unilever hold structural planogram advantages in this channel that newer entrants and D2C brands cannot replicate at comparable speed or cost.

Pharmacies & Drugstores serve as the primary entry channel for medicated and clinically-positioned hair oil brands, where professional context and pharmacist recommendation create higher consumer trust for therapeutic claims. Europe’s drugstore hair oil sales grew 11.4% in 2024 against traditional hair care growth of just 4.2% — confirming that the pharmacy channel is outpacing broader retail as consumers upgrade to clinically-framed formulations across Germany, France, and the UK.

Online Retail Stores represent the fastest-growing distribution channel across all regions, driven by ingredient-discovery behavior on social platforms that converts directly to search and purchase on Amazon, Nykaa, Flipkart, and brand DTC sites. Amazon US rosemary oil search volume rose 284.6% in 2024, demonstrating how a single social media ingredient cycle can generate significant e-commerce velocity within weeks — a pattern that rewards brands with agile digital shelf management.

Convenience Stores provide last-mile distribution access in rural and semi-urban markets where supermarket reach is limited, serving as the primary top-up channel for value-tier heavy oil formats. This channel is critical for maintaining household penetration in markets like rural India and sub-Saharan Africa, where the majority of hair oil volume moves through small-format trade rather than organized modern retail environments.

Specialty Beauty Stores serve as the premium trial channel for new entrants and prestige oil brands, where in-store demonstration and expert recommendation drive first purchase for higher-priced formulations. This channel is growing in India, South Korea, and the UAE as the premium beauty retail format expands beyond traditional metro markets into tier-two cities where prestige hair care awareness is increasing faster than premium purchasing power.

Salons & Professional channels carry the strongest per-unit revenue and the highest brand credibility signal in premium markets, where stylist endorsement functions as clinical validation for consumers who distrust marketing claims alone. Procter & Gamble’s distribution network reached 2.4 million retail locations globally in fiscal year 2024, with Pantene available in 2.1 million of those — confirming that professional channel presence amplifies mass-retail reach rather than replacing it for leading brands.

End-User Analysis

Women dominate with 66.89% due to higher usage frequency and multi-concern product engagement.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Women | 66.89% | High frequency, multi-concern engagement |

| Men | N/A | Beard oil, scalp care, grooming culture |

| Baby and Kids | N/A | Parental safety preference, gentle formulas |

| Unisex | N/A | Broad positioning, D2C brand strategy |

In 2025, Women held a dominant market position in the hair oil market, with a 66.89% share. Female consumers engage with hair oil for more functional concerns—nourishment, anti-hairfall, styling, and scalp health—which structurally increases average basket size per buyer. Dabur’s 2024 survey of 8,600 users found that 72.4% of Ayurvedic oil consumers apply it overnight, with women disproportionately driving this overnight ritual.

Men constitute the fastest-growing end-user segment, driven by beard oil adoption, scalp-care awareness, and the normalization of male grooming across India, the Middle East, and North America. Marico’s 2024 acquisition of Beardo positioned it directly in the men’s premium hair and beard oil space. Brands launching targeted men’s oil formulations now face a structurally less saturated shelf environment than the women’s segment, with significantly lower entry-level brand loyalty to overcome.

Baby and Kids formulations carry the highest safety threshold requirements of any end-user sub-segment, with parents applying stringent ingredient scrutiny to anything applied to infant scalps. This sub-segment performs strongest in India, Nigeria, and the Philippines, where baby hair oiling is a culturally embedded practice passed across generations. The combination of non-negotiable safety expectations and cultural ritual behavior creates strong brand loyalty once a product earns initial parental trust.

Unisex positioning is the preferred go-to-market strategy for D2C and clean beauty brands that want to maximize addressable market without investing in gender-differentiated formulation, packaging, or messaging. This sub-segment is growing fastest in North America and Western Europe, where gender-neutral personal care is a mainstream consumer expectation rather than a niche positioning — reducing the premium required to justify unisex formats in prestige retail channels.

Market Segments Covered in the Report

By Product Type

- Coconut Oil

- Almond Oil

- Argan Oil

- Amla Oil

- Castor Oil

- Jojoba Oil

- Olive Oil

- Onion Oil

- Rosemary Oil

- Bhringraj-based Blends

- Brahmi Formulations

- Sesame Oil (Til)

- Black Seed Oil (Kalonji)

By Application

- Individual

- Commercial

- Residential

By Function / Concern

- Hair Nourishment

- Anti-hairfall

- Anti-dandruff

- Scalp Health / Revitalizing

- Styling & Frizz Control

- Heat / UV Protection

- Color Protection

- Anti-aging / Graying Prevention

By Material / Texture

- Light Hair Oil

- Heavy Hair Oil

- Cooling Hair Oil

- Serum-oil Hybrids

By Formulation / Category

- Non-Medicated

- Medicated

- Herbal / Ayurvedic

- Natural / Organic

- Synthetic / Conventional

- Cold-Pressed / Virgin

By Distribution Channel

- Supermarkets / Hypermarkets

- Pharmacies & Drugstores

- Online Retail Stores

- Convenience Stores

- Specialty Beauty Stores

- Salons & Professional

By End-User

- Women

- Men

- Baby and Kids

- Unisex

By Biological Target

- Scalp Microbiome Support

- Hair Follicle Stem Cell Activation

- Scalp Barrier Defense

By Lifestyle & Environment

- Urban Pollution Defense

- Hard Water Damage Repair

- Post-Gym / Active Lifestyle

By Extraction Technology

- Supercritical CO2 Extraction

- Nano-emulsified Oils

- Molecular Distilled Oils

By Packaging Format

- Roll-on Applicators

- Comb-applicator Bottles

- Squeeze-pod Single Use

Hair Oil Market Regional Insights

Asia Pacific Holds 48.3% Share at USD 12.12 Billion

Asia Pacific leads the global hair oil market with 48.3% revenue share, valued at USD 12.12 billion in 2025. Deep-rooted hair oiling traditions across India, Indonesia, and the Philippines create structural demand that does not depend on trend cycles. Marico and Hindustan Unilever together hold the dominant volume positions in this region across mass and mid-market price tiers.

| Region | Market Value | Share % | Year |

|---|---|---|---|

| Asia Pacific | USD 12.12 billion | 48.3% | 2025 |

| North America | Data not available | N/A | 2025 |

| Europe | Data not available | N/A | 2025 |

| Latin America | Data not available | N/A | 2025 |

| Middle East & Africa | Data not available | N/A | 2025 |

Asia Pacific’s dominance means any brand targeting global scale must establish a position in India or Southeast Asia first. Distribution systems, ingredient sourcing, and consumer insight built in this region transfer directly to other emerging markets in Latin America and Africa — making APAC the most strategically leveraged entry point in the category.

North America Hair Oil Market Trends

North America is the fastest-growing developed market in the global hair oil category. Procter & Gamble held 24.6% North America hair care market share in 2024, with Pantene capturing 14.2% of the hair treatment oil sub-category (P&G annual reports). Social media discovery is pulling oil-based treatments into mainstream personal care shelves across the US.

Europe Hair Oil Market Trends

Europe’s hair oil category outpaced its broader hair care segment in 2024, with drugstore hair oil sales rising 11.4% against traditional hair care growth of just 4.2% (febe.be market data). This gap signals a structural shift toward oil-based treatments in pharmacy and drugstore channels across Germany, France, and the UK.

Latin America Hair Oil Market Trends

Latin America represents an emerging volume opportunity for global hair oil brands. Procter & Gamble launched Pantene Hair Oil Elixir across 17 new markets in 2024, targeting Latin America as a primary expansion zone where local coconut oil manufacturers previously held unchallenged share (P&G press releases, 2024). High humidity and growing middle-class personal care spending support category expansion in Brazil and Mexico.

Middle East and Africa Hair Oil Market Trends

The Middle East and Africa region drives volume demand for Black Seed Oil, argan-based blends, and cooling oil variants. Unilever Africa beauty and personal care sales reached EUR 4,123 million in 2024, up 7.8%, with hair care priced between USD 2.40 and USD 3.20 per unit across East and West Africa (Unilever annual results). Low unit prices and high population density make this a volume-over-margin priority market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The European Commission updated Cosmetic Regulation Annex II in July 2024, adding 28 essential oil compounds — including limonene and linalool — to its restricted ingredient list. These compounds appear widely in hair oil formulations across the EU market. Brands selling into Germany, France, and the UK face reformulation costs or must reformulate to maintain shelf access in pharmacy and retail channels.

In addition, the European Commission mandated nut allergen labeling for products containing coconut, almond, and argan oil at concentrations above 0.001% from June 2024, affecting 34.2% of imported hair oil products. This labeling requirement increases packaging compliance costs and creates a market-access barrier for smaller importers.

In the United States, multiple states — including California, Colorado, Maryland, and Minnesota — enacted PFAS prohibitions on cosmetics effective January 1, 2025, prompting ingredient reviews across synthetic and conventional hair oil formulations. MoCRA-driven safety assessments add a parallel compliance layer at the federal level.

Drivers

Natural Ingredient Demand Lifts Ayurvedic Oil Sales 14.6%

Consumer demand for plant-based hair oils — including argan, coconut, jojoba, and Ayurvedic blends — is the primary structural driver of category expansion. Dabur’s Vatika anti-dandruff hair oil reached INR 675 crore in fiscal year 2024, growing 12.8% year-on-year (Dabur annual reports), reflecting broader hair oil trends toward herbal formulations with scalp health claims.

In our view, social media ingredient cycles are now a demand driver brands must plan around — not react to. According to TikTok’s 2024 data, the #rosemaryhairoil hashtag reached 4.2 billion views — a 133.3% rise from 1.8 billion in 2023. Hair oil e-commerce growth accelerated in parallel, with Amazon US rosemary oil search volume rising 284.6% (Amazon marketplace data).

Beyond organic demand, strategic acquisitions are expanding the natural hair oil competitive set. Procter & Gamble acquired Mielle Organics in January 2024, adding rosemary and peppermint oil formulations — the same portfolio that D2C hair oil brands had built around sustainability-led consumer loyalty ahead of global FMCG players.

Restraints

Argan Supply Fell 18.6% as Prices Surged 38.9% in 2024

Morocco argan oil production fell 18.6% in 2024 to 5,600 tonnes from 6,880 tonnes in 2023, driven by drought in the Essaouira and Agadir regions (maroc.ma). Supply concentrated in a single geography makes cost hedging structurally difficult. According to Trading Economics data, argan oil price rose 38.9% to USD 31.40 per kilogram by December 2024.

Multiple US states — California, Colorado, Maryland, and Minnesota — enforced PFAS prohibitions in cosmetics from January 1, 2025, requiring ingredient reformulation across synthetic and conventional hair oil lines. This regulatory fragmentation raises compliance costs significantly for brands selling across state lines simultaneously.

Critically, social media trend volatility functions as a structural restraint for brands that over-invest in single-ingredient product lines. Onion oil interest on Google Trends peaked and collapsed within a single calendar year in 2024, leaving brands that launched onion oil as primary SKUs exposed to rapid retailer delisting and inventory write-downs. Brands with diversified core portfolios absorb trend cycles without existential risk to revenue.

Growth Factors

Premium Hair Oil Segment in India Grew 18.6% in 2024

Category premiumization is a structural growth enabler across the hair oil market, particularly in India. According to CMR India’s market report, premium hair oils above INR 500 per 200ml grew 18.6% in fiscal year 2024, while value oils below INR 200 grew just 4.2%. This gap confirms that margin expansion lives in the premium tier — not in volume growth at the base.

This means value-added oil innovation is outpacing traditional plain-oil volume growth at the brand level. Marico’s value-added oils — excluding plain coconut — grew 14.6% in fiscal year 2024 to INR 2,450 crore, compared to plain coconut oil growth of just 4.2% in the same period (Marico annual reports).

For operators, new product launches extending into adjacent benefit claims are a proven growth lever. Marico launched Parachute Advansed Olive Enriched Coconut Hair Oil in September 2025, combining coconut’s established consumer trust with olive oil’s premium nourishment credentials — accessing a higher price tier than plain coconut oil commands.

Emerging Trends

Scalp-Science Products Grew 18.4% Beating Traditional Oils

The scalp-science repositioning of hair oil is the defining trend reshaping category structure. L’Oréal’s scalp-focused hair products grew 18.4% in 2024, while traditional hair oil grew just 7.1% in the same period (L’Oréal annual report 2024). Products leading with microbiome balance and follicle activation claims are growing at more than double the rate of standard nourishment oils.

As a result, biotech-backed hair treatment investment is accelerating beyond traditional cosmetic companies. Pelage Pharmaceuticals raised USD 120 million in Series B funding in October 2025 to advance regenerative treatments including a topical gel targeting dormant hair follicle stem cells — bringing pharmaceutical-grade science directly into the scalp oil space.

What this signals for operators is that lightweight, clinically-framed oil formats are the fastest-repositioning sub-category in prestige markets. Serum-oil hybrids and cooling hair oils are gaining shelf space in pharmacy and specialty beauty channels across Europe and North America — two regions where consumers now expect ingredient transparency and evidence-backed claims as standard entry requirements for new product launches.

Key Companies Insights

L’Oréal S.A. stands out among leading hair oil companies, leading the premium scalp treatment segment with EUR 4,873 million in hair care revenue in 2024, up 7.1% year-on-year, according to L’Oréal’s 2024 annual report. Its R&D investment focuses on scalp microbiome science and hair follicle technology across professional and retail channels. Kérastase exceeded EUR 1,500 million in sales with Fusio-Dose scalp treatments growing 18.3% in 2024.

Our forecast suggests the Indian mass-market tier — anchored by Unilever Plc and its Hindustan Unilever subsidiary — holds the deepest structural advantage in volume distribution. Hindustan Unilever’s hair oil brands contributed INR 4,230 crore in 2024 across Lakme, Dove, and TRESemme, with products available in 5.2 million of 6.4 million retail outlets — 81.3% penetration (HUL annual reports).

Dabur India Ltd grounds its competitive position in Ayurvedic heritage, with Ayurvedic and natural products generating INR 9,420 crore in fiscal year 2024 — representing 70.3% of total revenue. Hair oils contributed INR 3,250 crore of that figure (Dabur annual reports). In October 2024, Dabur acquired Sesa Care for Rs 315–325 crore, adding an established Ayurvedic brand with strong South India distribution.

Marico Limited leads Indian value-added hair oil positioning with Parachute Advansed anti-hairfall oil reaching INR 2,450 crore in fiscal year 2024, up 9.4% year-on-year (Marico annual reports). Its strategy of layering functional benefit claims onto the Parachute heritage brand captures premiumization upside without abandoning mass-market distribution reach across India.

Key Companies

- Johnson & Johnson Services Inc.

- Unilever Plc

- L’Oréal S.A.

- Procter & Gamble Company

- Marico Limited

- Bajaj Consumer Care

- Dabur India Ltd

- Hindustan Unilever

- Sky Organics

- Emami Limited

- The Himalaya Wellness Company

- Kao Corporation

- Henkel AG & Co. KGaA

- Estée Lauder Companies Inc.

- Shiseido Company, Limited

- Amorepacific Corporation

- Beiersdorf AG

- Avon Products, Inc.

- Revlon, Inc.

- Proya Cosmetics Co., Ltd.

- Oriflame Holding AG

- LG Household & Health Care Ltd.

Recent Development

- December 2024 — Unilever Plc acquired EquiBeauty, an India-based Ayurvedic hair care brand, for USD 67 million, adding herbal oil formulations with established distribution across South India to its portfolio — directly expanding its Ayurvedic positioning against Dabur and Marico.

- November 2024 — Crown Affair secured USD 9 million in Series B funding led by True Beauty Ventures, bringing total capital raised to nearly USD 16 million across five rounds — signaling sustained investor confidence in prestige clean-formula hair oil brands.

- November 2024 — Divi Scalp & Hair Health secured a minority investment from Norwest Venture Partners (amount undisclosed), backing a scalp-focused oil brand built around ingredient transparency and dermatologist-recommended positioning in the US market.

- September 2024 — Scandinavian Biolabs closed USD 4.5 million in Series A funding led by Auréa, with SevenVentures and Blazar Capital participating — advancing a hair growth brand using serum-oil hybrid treatment formats targeting clinical hair loss consumers in European markets.

- August 2024 — Great Many raised USD 3.6 million in pre-seed funding led by BrandProject to expand telehealth-linked hair growth solutions, including oil-based treatment protocols, making professional-grade hair care more accessible beyond clinic settings.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 25.26 Billion |

| Forecast Revenue (2035) | USD 54.03 Billion |

| CAGR (2026–2035) | 7.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Coconut Oil, Almond Oil, Argan Oil, Amla Oil, Castor Oil, Jojoba Oil, Olive Oil, Onion Oil, Rosemary Oil), By Application (Individual, Commercial, Residential), By Function/Concern (Hair Nourishment, Anti-Hairfall, Anti-Dandruff, Scalp Health/Revitalizing, Styling & Frizz Control), By Material/Texture (Light Hair Oil, Heavy Hair Oil, Cooling Hair Oil, Serum-Oil Hybrids), By Formulation/Category (Non-Medicated, Medicated, Herbal/Ayurvedic, Natural/Organic, Synthetic/Conventional, Cold-Pressed/Virgin), By Distribution Channel (Supermarkets/Hypermarkets, Pharmacies & Drugstores, Online Retail Stores, Convenience Stores, Specialty Beauty Stores, Salons & Professional), By End-User (Women, Men, Baby and Kids, Unisex) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Johnson & Johnson Services Inc., Unilever Plc, L’Oréal S.A., Procter & Gamble Company, Marico Limited, Bajaj Consumer Care, Dabur India Ltd, Hindustan Unilever, Sky Organics, Emami Limited, The Himalaya Wellness Company, Kao Corporation, Henkel AG & Co. KGaA, Estée Lauder Companies Inc., Shiseido Company Limited, Amorepacific Corporation, Beiersdorf AG, Avon Products Inc., Revlon Inc., Proya Cosmetics Co. Ltd., Oriflame Holding AG, LG Household & Health Care Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |