What is the Esters Market Size?

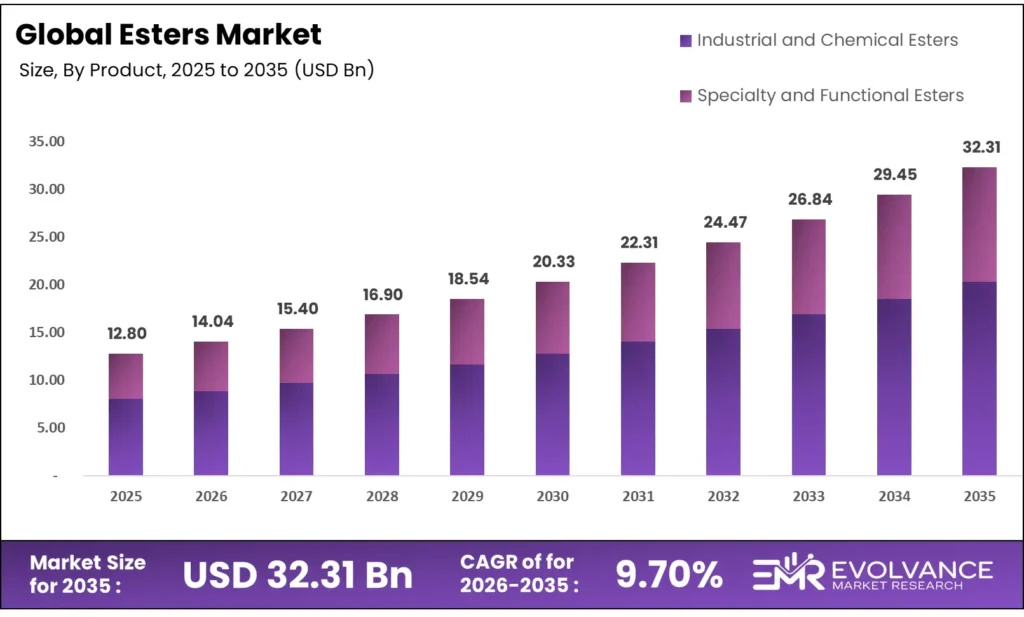

The Global Esters Market size will be worth around USD 32.31 Billion by 2035 from USD 12.80 Billion in 2025, growing at a CAGR of 9.70% during the forecast period 2026 to 2035. Demand for bio-based esters is climbing fast as sustainability mandates reshape transformer fluid and fuel additive procurement. Enterprise buyers are accelerating their switch from mineral oil alternatives to certified biodegradable ester fluids. Feedstock price swings of 20-30% remain the key supply-side risk constraining new capacity decisions.

Market Highlights

- The Global Esters Market valued at USD 12.80 Billion in 2025, reaching USD 32.31 Billion by 2035 at a CAGR of 9.70%.

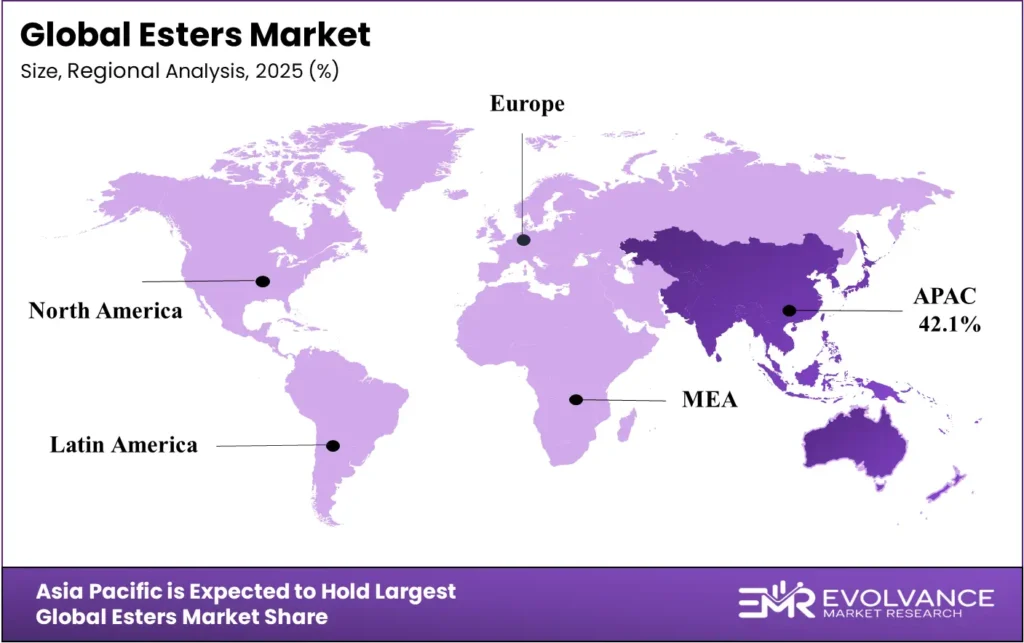

- Asia Pacific leads all regions with a 42.1% market share, valued at USD 5.4 Billion.

- Synthetic esters dominate the By Source segment with a 69.2% share.

- Industrial and Chemical Esters lead the By Product segment with a 64.3% share.

- Lubricants hold the largest By Application share at 31.8%.

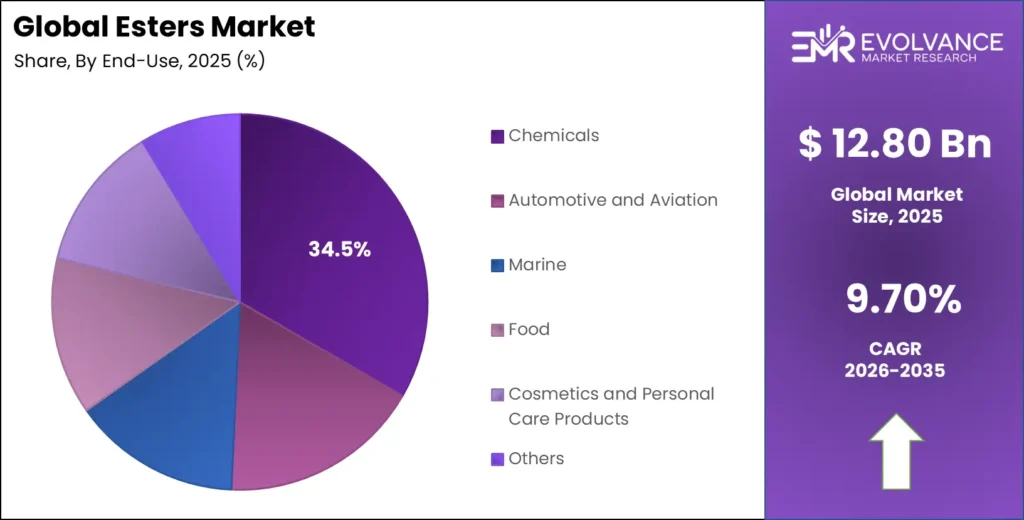

- Chemicals end-use leads the By End-Use segment with a 34.5% share.

Market Overview

The esters market covers a wide set of organic compounds formed by reacting acids with alcohols. These compounds serve as core inputs across lubricants, solvents, plasticizers, flavoring agents, and fuel additives. Their chemical versatility makes them hard to replace in both performance-critical and consumer-facing applications.

The market splits into two structural tiers. Industrial and chemical esters — including methyl, fatty acid, acrylic, and phosphate esters — serve bulk processing industries. Specialty and functional esters, such as nitrate and sucrose esters, serve high-margin sectors like pharmaceuticals, food, and advanced cosmetics. This two-tier structure creates very different competitive dynamics and margin profiles for producers.

- According to the World Bioenergy Association, Indonesia’s fatty acid methyl ester biodiesel output reached approximately 14 billion liters in 2023, powered by the national B35 palm oil blending mandate. This single country now accounts for the largest share of global FAME production, showing how blending policy can concentrate industrial-scale ester demand in one market.

Data published by the World Bioenergy Association shows global FAME biodiesel production approached approximately 50 billion liters in 2024 across renewable fuel markets worldwide. This scale signals that fatty acid esters are no longer a specialty product — they are core industrial inputs in global energy infrastructure, with production volumes rivaling major petrochemical streams.

Regulatory pressure is reshaping where ester demand grows fastest. Governments across Europe, Southeast Asia, and North America have introduced biofuel blending mandates and sustainable fluid standards. These policies convert regulatory compliance into direct procurement volume for ester producers. India’s free trade push and anti-dumping actions further signal that trade policy is now a primary demand lever in this market.

Esters Market Segmentation Insights

Source Insights

Synthetic esters dominate with 69.2% due to process control and application versatility.

In 2025, Synthetic Esters held a dominant market position in the By Source segment of the Esters Market, with a 69.2% share. Their lead reflects a structural cost and performance advantage — synthetic routes allow precise molecular tailoring for high-performance lubricants, polymer coatings, and specialty films. Manufacturers rely on synthetic esters because natural feedstock variability adds quality risk to finished goods.

Natural Esters serve a distinct and fast-growing demand pocket driven by sustainability mandates. Transformer fluid standards in Europe and North America now recognize natural vegetable-based ester fluids as compliant alternatives to mineral oil. Cargill’s FR3 natural ester fluid — positioned for utility-scale transformer applications — is a direct example of how regulatory compliance is converting natural ester demand from niche to mainstream procurement.

Product Insights

Industrial and Chemical Esters dominate with 64.3% due to broad industrial deployment.

In 2025, Industrial and Chemical Esters held a dominant market position in the By Product segment of the Esters Market, with a 64.3% share. This group spans methyl esters, fatty acid esters, vinyl esters, acrylic esters, phosphate esters, dibasic esters, and polyol esters. Their dominance reflects how deeply embedded these compounds are in manufacturing supply chains — from automotive coatings to construction adhesives to packaging films.

Methyl Esters represent the single largest volume sub-category within industrial esters, driven almost entirely by biodiesel programs. Brazil’s national biofuel mandate pushed soybean-based methyl ester output to approximately 8 billion liters in 2023, per the World Bioenergy Association. Countries with active blending mandates convert methyl esters from chemical inputs into regulated infrastructure commodities — a fundamentally different buyer dynamic than specialty chemistry.

Acrylic Esters are a strategically concentrated segment dominated by a small group of large-scale producers. Research from ReportPrime shows BASF generated USD 0.95 billion in acrylic ester revenue in 2024 against 420 kilotons per year of production capacity, while Dow maintained USD 0.54 billion in revenue at 280 kilotons annually. This concentration means pricing in acrylic esters is effectively set by a handful of operators — buyers have limited switching leverage.

Specialty and Functional Esters generate disproportionate margin relative to their volume share. This group includes nitrate esters and sucrose esters. Producers who shift mix toward specialty esters improve returns even without volume growth — a key strategic lever as bulk ester markets face pricing pressure from Chinese capacity additions.

Nitrate Esters serve defense, mining, and construction explosives markets. Their demand is driven by infrastructure project pipelines and defense procurement budgets rather than commercial consumer cycles. This makes nitrate ester revenue relatively predictable, though volume is constrained by strict handling and transport regulations globally.

Sucrose Esters are emerging as the clean-label emulsifier of choice in food and personal care formulations. As major food companies expand their natural ingredient portfolios, sucrose esters — derived from sugar and fatty acids — meet both function and label requirements simultaneously. Brand owners paying premium pricing for natural certification are accelerating adoption faster than volume forecasts suggested two years ago.

Application Insights

Lubricants dominate with 31.8% due to performance requirements and regulatory substitution.

In 2025, Lubricants held a dominant market position in the By Application segment of the Esters Market, with a 31.8% share. Ester-based lubricants outperform mineral oil alternatives in biodegradability, thermal stability, and lubricity at extreme temperatures. Both regulatory mandates and OEM specifications are pushing automotive and industrial buyers toward ester lubricants — a structural shift that makes this the most durable growth application in the market.

Insecticides use ester-based active ingredients and carrier solvents as core formulation components. Agricultural intensification in South and Southeast Asia is the primary volume driver. Crop protection chemical demand in India and Indonesia is expanding faster than in mature markets, concentrating new insecticide ester demand in Asia Pacific.

Solvents represent a large and structurally shifting application. Tightening VOC regulations in the EU and China are accelerating the substitution of aromatic solvents with dibasic and other ester-based alternatives. The regulatory tailwind here is durable — producers who move early into low-VOC ester solvents will capture formulation share that is very hard to displace once embedded in customer specifications.

Flame Retardants using phosphate esters benefit from halogen-free regulatory trends in electronics and construction materials. As global building codes and electronics standards tighten, phosphate ester flame retardants are moving from preferred option to mandatory specification in a growing set of applications.

Flavoring Agents represent a high-value, low-volume ester application in food and beverage. Natural ester flavors carry significant price premiums over synthetic equivalents. The clean-label movement is driving food manufacturers to pay those premiums at scale — shifting flavoring agent ester demand from cost-sensitive to quality-driven procurement.

Fuel and Oil Additives using esters improve combustion efficiency, reduce engine wear, and meet increasingly tight emissions standards. As engine technology moves toward tighter tolerances and longer service intervals, high-performance ester additives become standard specifications rather than optional upgrades.

End-Use Insights

Chemicals end-use dominates with 34.5% due to broad upstream supply chain integration.

In 2025, Chemicals held a dominant market position in the By End-Use segment of the Esters Market, with a 34.5% share. Chemical manufacturers consume esters as both intermediates and finished inputs across solvents, coatings resins, and polymer precursors. Their scale and purchasing discipline make them the price-setting buyers in the esters value chain.

Automotive and Aviation end-use represents the highest-performance demand tier for esters. Polyol esters in aviation lubricants and synthetic esters in automotive gear oils face no viable low-cost substitutes. As fleet operators extend maintenance intervals and engine manufacturers tighten thermal specifications, premium ester lubricants shift from optional to mandatory — locking in demand independent of fuel price cycles. Enzymatic synthesis and precision catalysis technologies are enabling the development of tailored ester grades specifically optimized for next-generation aviation turbine lubricants.

Marine end-use is driven by environmental discharge regulations on the high seas. IMO regulations restricting use of petroleum-based lubricants in underwater machinery are converting marine operators to biodegradable ester alternatives. Compliance is mandatory, not elective — making marine a structurally growing ester end-use regardless of shipping cycle volatility.

Food end-use spans emulsifiers, flavoring carriers, and food-grade lubricants. Sucrose esters and fatty acid esters serve as the primary food-approved compounds in this segment. Regulatory approval barriers create a natural moat — only esters with GRAS or E-number status can serve food applications, limiting which producers can participate in this high-margin segment.

Textiles use esters as fiber spin finishes, softeners, and lubricants in synthetic fiber manufacturing. Polyester fiber production volumes — concentrated in China and India — directly determine textile ester demand. India’s textile expansion programs are adding capacity and pulling ester demand along with it.

Cosmetics and Personal Care represents the fastest-growing end-use for specialty esters. Emollient esters in skin care and hair care formulations are commanding significant premiums as brands shift toward high-performance, naturally derived alternatives. Manufacturers pivoting to specialty-led growth strategies are specifically targeting ester-based actives as their margin expansion lever.

Market Segments Covered in the Report

By Source

- Synthetic

- Natural

By Product

- Industrial and Chemical Esters

- Methyl Esters

- Fatty Acid Esters

- Vinyl Esters

- Acrylic Esters

- Phosphate Esters

- Dibasic Esters

- Polyol Esters

- Specialty and Functional Esters

- Nitrate Esters

- Sucrose Esters

By Application

- Lubricants

- Insecticides

- Explosives

- Solvents

- Surfactants

- Plasticizers

- Flame Retardants

- Flavoring Agents

- Fuel and Oil Additives

By End-Use

- Chemicals

- Automotive and Aviation

- Marine

- Food

- Textiles

- Cosmetics and Personal Care Products

- Others

Esters Market Regional Insights

Asia Pacific Dominates the Esters Market with a Market Share of 42.1%, Valued at USD 5.4 Billion

Asia Pacific holds a 42.1% share worth USD 5.4 Billion, anchored by Indonesia’s palm oil-based FAME mandates, China’s industrial chemical base, and India’s accelerating construction and textile sectors. The region’s dominance is structural — three of the world’s five largest ester-consuming industries are headquartered or expanding here. India is now outpacing China’s growth rate in construction-sector ester demand, signaling a geographic shift in the region’s growth center of gravity.

North America Esters Market Trends

North America is a mature but strategically important market, anchored by the US Renewable Fuel Standard which drove approximately 6 billion liters of fatty acid methyl ester biodiesel production in 2023. Beyond biodiesel, the US leads in specialty ester adoption for aviation lubricants and pharmaceutical intermediates. The market is transitioning from volume growth to value growth — a dynamic that rewards specialty ester producers over commodity methyl ester manufacturers.

Europe Esters Market Trends

Europe produced approximately 13 billion liters of FAME biodiesel in 2023, primarily from rapeseed oil and used cooking oil across Germany, Spain, and France. The EU’s RED III directive is tightening feedstock sustainability requirements, which will progressively shift biodiesel ester demand toward certified waste-based feedstocks. This regulatory shift creates a two-tier market: compliant producers gain pricing power, non-compliant producers face volume displacement.

Latin America Esters Market Trends

Latin America’s ester market is built on Brazil’s dominant soybean-based biodiesel program, which drove approximately 8 billion liters of FAME output in 2023 under national blending mandates. Brazil’s blend mandate trajectory — moving toward B15 and beyond — guarantees sustained volume growth in fatty acid methyl esters. Mexico adds demand through chemical manufacturing and automotive supply chain activity. The region’s ester market is primarily a function of biofuel policy, not end-use diversification.

Middle East & Africa Esters Market Trends

Middle East & Africa represents an emerging demand center rather than a production hub for esters. GCC countries are expanding chemical manufacturing as part of petrochemical diversification strategies — creating local demand for ester intermediates in plastics and coatings. Sub-Saharan Africa’s agricultural processing expansion is generating early-stage fatty acid ester demand. The region’s growth is off a small base but directionally consistent with industrial development trends.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The EU’s Renewable Energy Directive III (RED III), finalized in 2023 and in force from 2024, mandates that member states source at least 42% of energy from renewables by 2030. For the ester market, RED III restricts FAME biodiesel credits for first-generation crop-based feedstocks, pushing producers toward waste and advanced feedstocks. This directly reshapes procurement in the European ester biodiesel supply chain.

India’s Plastic Waste Management Rules, updated in 2024, require brand owners to meet recycled content thresholds in flexible packaging. This regulation is converting rPET ester film demand from voluntary to mandated. Producers of specialty ester films serving Indian FMCG and food packaging customers must now align their product lines with recycled-content specifications or risk losing shelf space.

The US Renewable Fuel Standard (RFS), administered by the EPA, set the 2024 renewable volume obligation at a level that sustains roughly 6 billion liters of annual domestic FAME biodiesel production. The RFS is the single largest policy mechanism supporting fatty acid ester demand in North America. Any revision to volumetric obligations directly affects ester producer revenue forecasts and capacity investment decisions.

India’s Directorate General of Trade Remedies (DGTR) launched an anti-dumping investigation in 2025 into Chinese BOPET film imports. If duties are imposed, domestic Indian ester film producers gain pricing power that has been compressed by predatory import pricing. The investigation outcome — expected in 2026 — represents a binary regulatory event with direct margin implications for Indian specialty ester film manufacturers.

Esters Market Dynamics

Drivers

Bio-Based Ester Mandates and Sustainable Fluid Standards Accelerate Enterprise Procurement Shifts

Governments across Southeast Asia, Europe, and North America are embedding bio-based ester requirements into energy, transport, and infrastructure regulation. Indonesia’s B35 mandate alone converted palm oil-derived FAME into a nationally mandated input at industrial scale. When procurement is regulatory rather than discretionary, demand becomes volume-guaranteed — the most durable demand signal available to ester producers.

India’s free trade agreements with the EU and the UK are opening new export corridors for BOPET films and specialty ester products. As tariff barriers fall, Indian producers with quality-certified output can compete in European markets previously inaccessible due to cost disadvantages. This trade architecture shift is more durable than any single product cycle — it repositions India as a permanent supply-side player in global specialty esters.

The EU produced approximately 13 billion liters of FAME biodiesel in 2023, according to the World Bioenergy Association, primarily from rapeseed and used cooking oil. Europe’s continued investment in waste-based feedstock conversion signals that demand for compliant fatty acid esters will grow as RED III enforcement tightens. Producers with certified waste-oil supply chains are structurally better positioned than those relying on crop-based inputs.

Restraints

Feedstock Price Volatility and Import Competition Compress Margins and Deter New Capacity Investment

Fatty acid and alcohol feedstock prices fluctuate by 20-30% annually due to agricultural output variability, energy price linkages, and currency movements. This level of input cost uncertainty makes long-term capacity investment decisions financially difficult. Producers who cannot hedge feedstock exposure effectively face margin compression even in periods of strong end-market demand.

US trade tariffs and predatory Chinese BOPET film exports are compressing margins and disrupting high-margin specialty film sales for non-Chinese producers. China’s ester film capacity additions — built behind domestic demand and supported by state financing — create pricing floors that Western and Indian producers cannot profitably match at full scale. This asymmetric cost competition is the most immediate structural restraint in the specialty ester film segment.

Nippon Shokubai generated USD 0.62 billion in acrylic ester revenue in 2024 operating approximately 300 kilotons of annual capacity. Even at scale, specialty ester producers face margin pressure when commodity acrylic esters from Asian capacity additions enter their primary markets. The data confirms that production scale alone does not guarantee margin protection — feedstock access and product differentiation determine profitability.

Growth Factors

Trade Policy Realignment and Advanced Synthesis Technology Unlock New Revenue Streams for Specialty Ester Producers

India’s expected tariff reduction on specialty ester films from 50% to 18% under the India-US trade deal (expected March 2026) creates a direct margin recovery pathway for exporters. At the current tariff, US buyers absorb a cost penalty that makes Indian specialty films uncompetitive. At 18%, the value proposition changes fundamentally — enabling Indian producers to capture share in one of the world’s highest-value packaging markets.

The US biofuel sector — which produced approximately 6 billion liters of FAME biodiesel in 2023, per the World Bioenergy Association — is expanding capacity under Renewable Fuel Standard incentives. Brazil reached approximately 8 billion liters of FAME output in 2023 using soybean feedstock under national mandates. Together, these two programs represent over 14 billion liters of guaranteed annual FAME demand — a procurement floor that de-risks methyl ester investment in the Americas.

Enzymatic synthesis and precision catalysis technologies are enabling producers to engineer ester molecules with tailored performance characteristics for pharmaceutical and advanced lubricant applications. These technologies reduce the scale requirements for specialty ester development, allowing mid-size producers to compete in high-margin niches previously accessible only to large integrated chemical companies. The technology shift is a structural enabler of specialty-segment growth.

Emerging Trends

Ester-Based Lubricant Substitution and India’s Market Emergence Reshape the Global Demand Map

Mineral oil-based lubricants are being replaced by ester-based biodegradable alternatives in automotive and aviation sectors at a measurably faster pace than three years ago. OEM specifications in Europe and North America now increasingly mandate biodegradable lubricants for outdoor and marine equipment. The US biofuel production reached approximately 1,917 petajoules in 2024, making the US the largest national biofuel producer globally at 38.8% of total output — a scale that validates how deep ester integration into energy infrastructure has become.

India’s ester market is now growing faster than China’s in construction and coatings sectors — a reversal of the long-standing China-led growth assumption. China’s real estate sector contraction, driven by the Evergrande crisis, has reduced ester demand in paints, coatings, and adhesives applications. India fills that growth gap with its own infrastructure and housing programs, making it the more reliable growth market in Asia Pacific for construction-sector ester demand.

The clean-label movement is converting natural vegetable-based ester adoption in food and beverage from trend to standard procurement practice. Major food companies are embedding natural ingredient requirements into supplier specifications, which locks in ester sourcing at the contract level rather than the spot market. Producers who secure natural ester supply agreements with food majors gain multi-year revenue visibility that commodity ester producers cannot replicate.

Key Companies Insights

Exxon Mobil Corporation approaches the esters market through its lubricant base oil and synthetic fluid platforms. Its scale in petrochemical feedstock integration gives it a structural cost advantage in polyol and phosphate ester production for aviation and industrial lubricant applications. However, Exxon’s primary competitive strength lies in distribution reach and OEM qualification status rather than specialty chemistry — a positioning that may limit its ability to capture the high-margin specialty ester segments where growth is most concentrated.

BASF SE operates one of the most vertically integrated acrylic ester businesses in the global market. With 420 kilotons per year of acrylic ester production capacity generating USD 0.95 billion in revenue in 2024, BASF is the dominant scale player in this sub-segment, per ReportPrime. Its integrated feedstock access — from propylene to acrylic acid to esters — insulates it from spot market pricing volatility that pressures smaller competitors. BASF’s challenge is maintaining this cost lead as Asian capacity additions reduce the premium for European production location.

The Dow Chemical Company focuses its ester strategy on coatings, sealants, and adhesive applications where acrylic ester performance specifications are most demanding. Dow maintained USD 0.54 billion in acrylic ester revenue in 2024 at 280 kilotons per year of installed capacity, per ReportPrime. Dow’s strength is its formulation depth — it sells not just the ester but the application knowledge that justifies premium pricing. This consultative commercial model creates switching costs that price-only competitors cannot easily erode.

Arkema has been building its specialty ester position through both organic chemistry investment and targeted acquisitions. Its focus on high-performance acrylics, bio-based monomers, and adhesive platforms positions it for above-market growth in the specialty and functional ester segments. Evonik Industries reported €15.157 billion in total sales for FY2024, per GuideChem, demonstrating that the large European chemical players adjacent to Arkema are generating substantial revenues from diversified specialty chemical portfolios — increasing competitive pressure on specialty ester margin pools.

Key Companies

- Exxon Mobil Corporation

- BASF SE

- The Dow Chemical Company

- Arkema

- Solvay

- Evonik Industries AG

- Esters and Solvents LLP

- Croda International Plc.

- Estelle Chemicals Pvt. Ltd.

- Mitsubishi Chemical Group Corporation

Recent Development

- In 2025 – Cargill launched FR3 natural ester transformer fluid, targeting utility-scale electrical grid applications requiring sustainable dielectric fluid alternatives. The product positions Cargill directly in the regulatory-driven shift from mineral oil transformer fluids to certified biodegradable ester alternatives across North America and Europe.

- March 2026 – India-US trade deal tariff reduction on specialty ester films from 50% to 18% is expected to take effect, creating a direct margin recovery opportunity for Indian BOPET ester film exporters. This tariff shift materially changes the competitiveness of Indian specialty ester films in the US packaging market.

- In 2025 – India’s DGTR launched a formal anti-dumping investigation into Chinese BOPET film imports. The investigation targets predatory pricing practices that have compressed margins for domestic Indian ester film producers. A positive ruling would restore pricing power and potentially trigger capacity reinvestment decisions among Indian manufacturers.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 12.80 Billion |

| Forecast Revenue (2035) | USD 32.31 Billion |

| CAGR (2026-2035) | 9.70% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source (Synthetic, Natural), By Product (Industrial and Chemical Esters, Specialty and Functional Esters), By Application (Lubricants, Insecticides, Explosives, Solvents, Surfactants, Plasticizers, Flame Retardants, Flavoring Agents, Fuel and Oil Additives), By End-Use (Chemicals, Automotive and Aviation, Marine, Food, Textiles, Cosmetics and Personal Care Products, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Exxon Mobil Corporation, BASF SE, The Dow Chemical Company, Arkema, Solvay, Evonik Industries AG, Esters and Solvents LLP, Croda International Plc., Estelle Chemicals Pvt. Ltd., Mitsubishi Chemical Group Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |