What is Buy Now Pay Later (BNPL) Market Size?

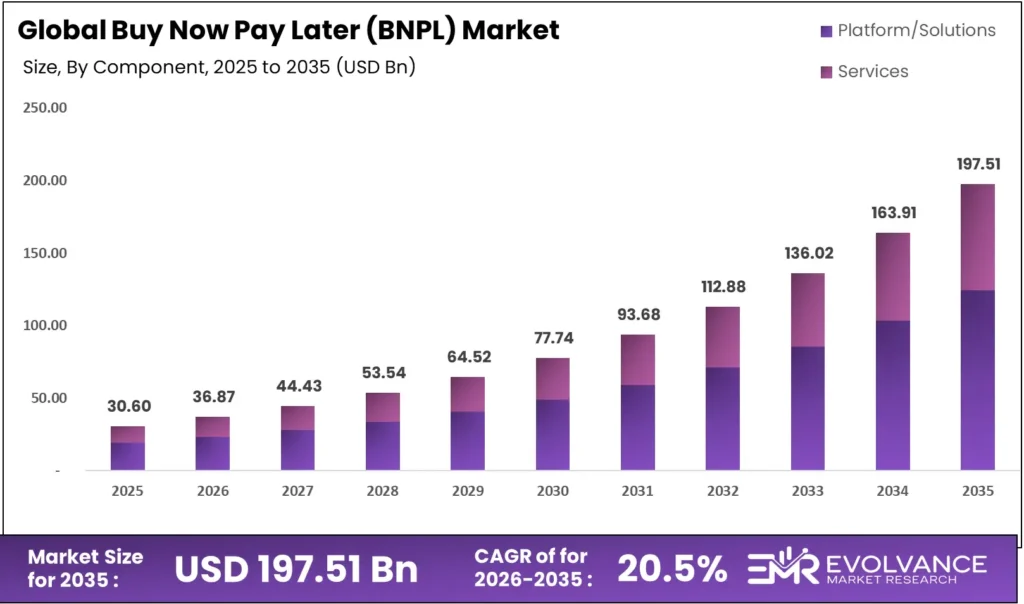

The Global Buy Now Pay Later (BNPL) Market size is calculated at USD 30.60 billion in 2025 and is predicted to increase from USD 36.87 billion in 2026 to approximately USD 197.51 billion by 2035, expanding at a CAGR of 20.5% from 2026 to 2035. Buy Now Pay Later (BNPL) has emerged as one of the fastest-growing digital payment solutions, allowing consumers to split their purchases into interest-free or low-cost installments. The model is becoming a preferred choice for e-commerce shoppers, offline retail buyers, and new-to-credit customers due to its convenience, transparency, and instant approvals.

Buy Now Pay Later (BNPL) platforms provide flexible credit access, helping retailers improve conversion rates and increase average order value. At the same time, financial institutions are integrating BNPL to strengthen customer loyalty, reduce cart abandonment, and expand their digital lending portfolios.

The Buy Now Pay Later (BNPL) Market is gaining significant traction due to the increasing adoption of flexible payment solutions within digital commerce ecosystems. The rise of embedded finance and seamless transaction models is driving widespread consumer acceptance. This trend is closely linked to developments in the Cloud FinOps, where organizations are optimizing financial operations and cost structures. Additionally, the growing digital ecosystem supported by the Internet Security and Security Analytics is ensuring secure and scalable fintech infrastructure.

Market Highlights

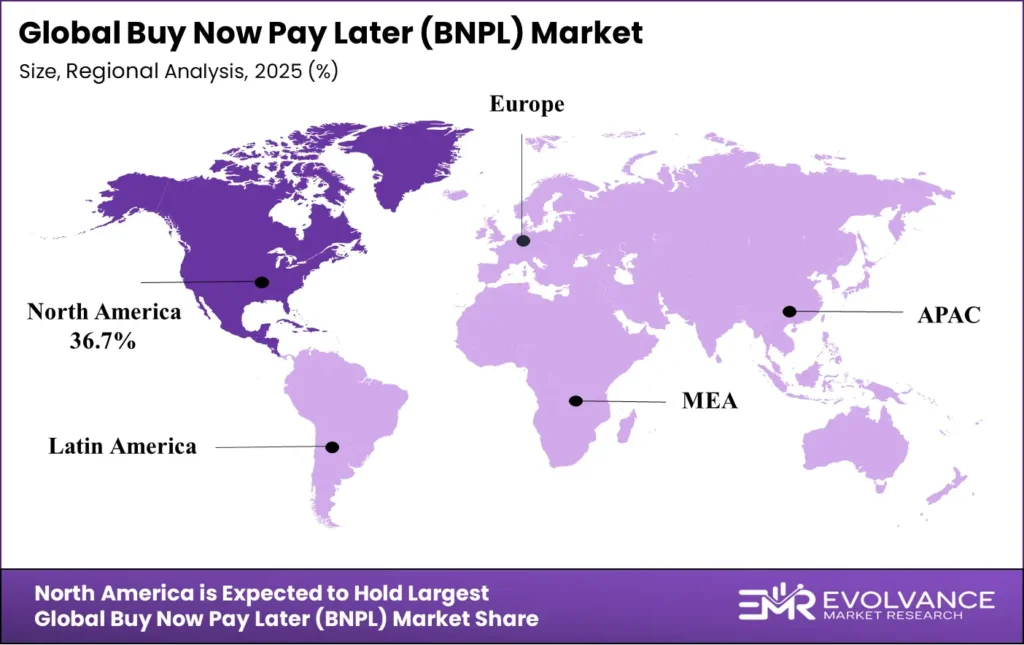

- By region, North America dominated the market, holding largest share of 36.7% in the market during 2025.

- By region, Asia Pacific is expected to expand at the fastest CAGR of 24.5% between 2026 and 2035.

- By Component, the Platform/Solutions segment contributed the biggest market share of 68.5% in 2025.

- By Component, Services is expected to grow at a remarkable CAGR of 22.5% between 2026 and 2035.

- By Purchase Ticket Size, Small Ticket Item (Up to US$ 300) segment held the major market share of 44.8% in 2025.

- By Purchase Ticket Size, Mid Ticket Items (US$ 300 – US$ 1000) is projected to grow at a remarkable CAGR of 23.6% between 2026 and 2035.

- By Business Model, the Business-Driven segment captured the highest market share of 72.2% in 2025.

- By Business Model, the Customer-Driven segment is growing at a remarkable CAGR of 25.3% between 2026 and 2035.

- By Mode, the Online segment captured the highest market share of 60.6% in 2025.

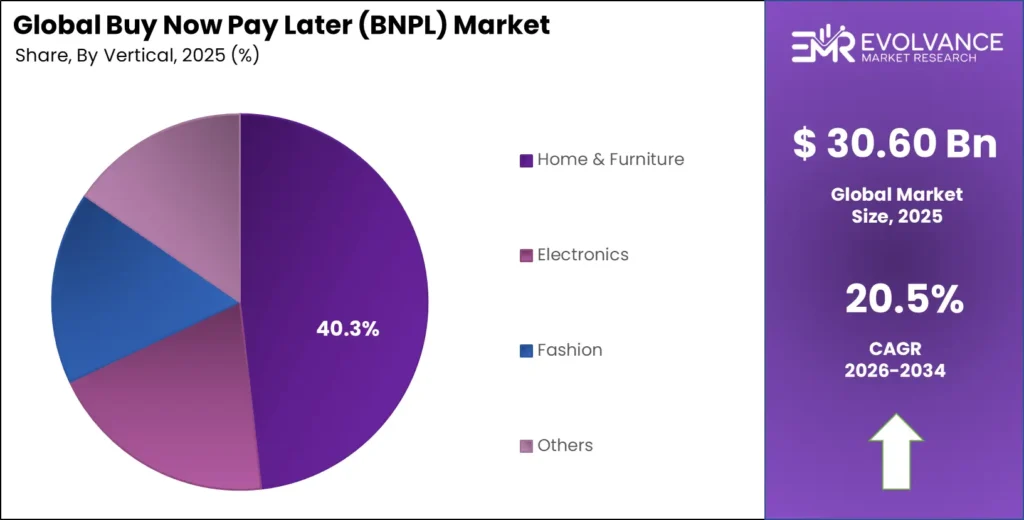

- By Vertical, the Electronics segment held the largest market share of 40.3% in 2025.

- By Vertical, Fashion segment is expanding at a strong CAGR of 23.6% between 2026 and 2035.

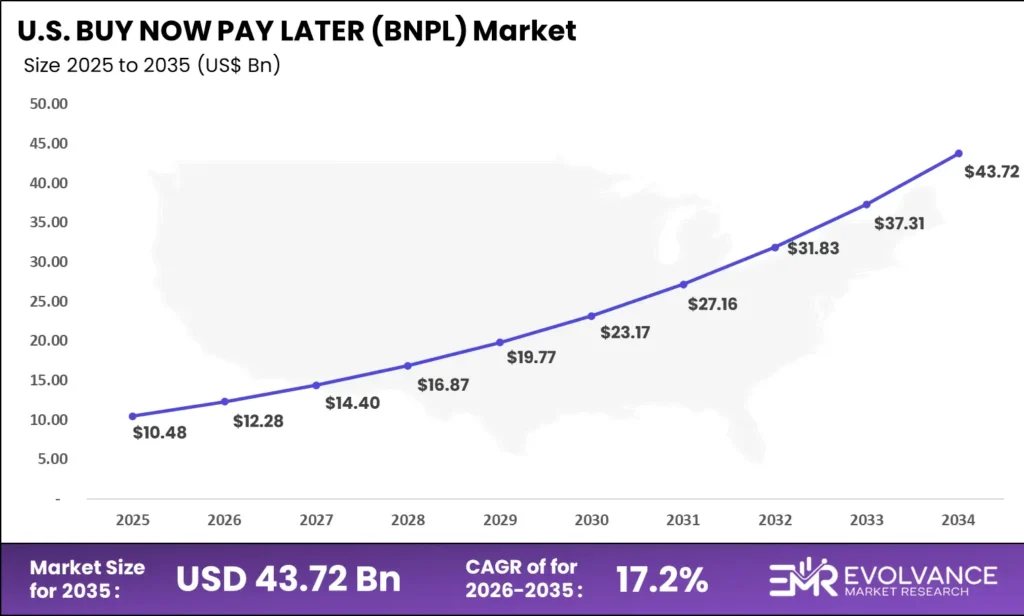

U.S. Buy Now Pay Later (BNPL) Market Size and Growth 2025 to 2035

The U.S. Buy Now Pay Later (BNPL) Market size is exhibited at USD 10.48 billion in 2025 and is projected to be worth around USD 43.72 billion by 2035, growing at a CAGR of 17.2% from 2026 to 2035.

Market Size and Forecast

- Market Size in 2025: USD 30.60 Billion

- Market Size in 2026: USD 36.87 Billion

- Forecasted Market Size by 2034: USD 197.51 Billion

- CAGR (2026-2035): 20.5%

- Largest Market in 2025: North America

- Fastest Growing Market: Asia Pacific

What Is the Buy Now Pay Later (BNPL)?

Buy Now Pay Later (BNPL) is a digital financing solution that lets consumers purchase products and pay in scheduled installments over time. Customers can pay through weekly, bi-weekly, or monthly plans without traditional credit checks or complicated approval procedures. Retailers benefit from higher sales conversions, while consumers enjoy affordability and flexibility.

Buy Now Pay Later (BNPL) is transforming the global payment landscape by offering instant credit, transparent pricing, and seamless checkout experiences integrated across e-commerce, mobile apps, and in-store POS systems. As digitalization accelerates, BNPL is becoming a standardized financial option across retail, travel, healthcare, electronics, and lifestyle sectors.

Buy Now Pay Later (BNPL) Market Outlook

- Industry Growth Overview: The Buy Now Pay Later (BNPL) market is entering a strong growth phase, fueled by rising digital commerce adoption and consumers’ increasing preference for flexible, low-friction payment options. As shoppers shift toward mobile-first transactions, BNPL has become a mainstream alternative to credit cards, offering instant approvals and transparent repayment terms. Retailers are integrating BNPL solutions to boost conversions, reduce cart abandonment, and attract younger, credit-averse customers.

- Sustainability Trends: Sustainability in the BNPL sector is moving beyond customer acquisition and short-term usage — it now focuses on financial wellness, responsible lending, and a transparent repayment ecosystem. Providers are incorporating stronger credit assessment tools, real-time affordability checks, and flexible repayment options to encourage healthy borrowing behaviours. Merchants are also aligning with BNPL partners that promote ethical lending practices and provide clear disclosures to minimize consumer debt risks.

- Major Investors: The BNPL market has become a strategic focus area for venture capital firms, fintech investors, and global payment companies. Capital is flowing into platforms that strengthen underwriting, enhance merchant integrations, and expand cross-border BNPL services. Investors are particularly interested in BNPL solutions built around AI-driven risk scoring, embedded finance APIs, and sector-specific models such as healthcare, travel, and B2B purchases.

- Startup Economy: The startup landscape in the BNPL ecosystem is rapidly expanding, with new ventures offering specialized, customer-centric solutions. Startups are innovating in areas such as instant credit decisioning, merchant dashboards, repayment intelligence, and niche BNPL models tailored to education, lifestyle, and essential services.

Key Market Trends

- Growth of embedded BNPL solutions integrated directly within e-commerce platforms, banking apps, and checkout pages, making repayment plans a seamless part of the shopping experience.

- Wider use of advanced risk-scoring and AI-based credit assessment, enabling providers to offer instant approvals while reducing default rates and improving overall portfolio quality.

- Shift toward omnichannel BNPL adoption, with retailers offering installment plans not only online but also across physical stores, mobile apps, and social commerce channels.

- Expansion of sector-specific BNPL models in categories such as healthcare, travel, education, and automotive services, widening the market beyond traditional retail purchases.

- Rising demand for flexible repayment structures, including “pay in 3,” “pay in 4,” longer-term plans, and subscription-based payment flexibility for higher-ticket items.

- Stronger regulatory oversight and compliance requirements, prompting BNPL providers to adopt more transparent disclosures, affordability checks, and responsible lending frameworks.

- Growth in B2B BNPL services, helping small and medium businesses manage cash flows, finance inventory, and access short-term credit without lengthy approval processes.

- Increasing collaborations between banks, fintechs, and retailers, as financial institutions enter the BNPL landscape through partnerships, acquisitions, or white-label solutions.

- Enhanced focus on customer financial wellness, with tools for budgeting, repayment reminders, spending analytics, and proactive communication to support responsible borrowing.

- Global expansion into emerging markets, where large unbanked and underbanked populations are adopting BNPL as an accessible alternative to credit cards.

Market Scope

| Report Coverage | Details |

|---|---|

| Market Size in 2025 | US$ 30.60 Billion |

| Market Size in 2026 | US$ 36.87 Billion |

| Market Size by 2035 | US$ 197.51 Billion |

| Market Growth Rate from 2026 to 2035 | CAGR of 20.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2025 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Platform/Solutions, Services), By Purchase Ticket Size (Small Ticket Items – Up to US$ 300, Mid Ticket Items – US$ 300–US$ 1000, Higher Prime Segments – Above US$ 1000), By Business Model (Customer Driven, Business Driven), By Mode (Online, Offline), By Vertical (Home & Furniture, Electronics, Fashion, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC Countries, South Africa, North Africa, and Rest of MEA |

Component Insights

Why Platform/Solutions Is Dominating the Buy Now Pay Later (BNPL) Market?

The Platform/Solutions is dominating the Buy Now Pay Later (BNPL) market by holding a share of 68.5%, due to these platforms serve as the core technology layer that enables every BNPL transaction. They connect merchants, consumers, and financial partners through seamless APIs, real-time credit checks, automated approvals, and integrated payment dashboards. These solutions simplify the entire checkout experience, reducing friction and increasing conversion rates for online and offline retailers.

Their leadership comes from their ability to handle large transaction volumes, offer instant decision-making, and support multiple repayment models. BNPL platforms also provide risk scoring, fraud detection, and customer verification tools that merchants cannot manage on their own. This makes them the foundation of the BNPL ecosystem, powering smooth customer journeys and helping brands attract shoppers who prefer flexible payments.

The Services segment is the fastest-growing in the Buy Now Pay Later (BNPL) market and are expected to grow at a 22.5% CAGR due to the rising demand for value-added capabilities around BNPL adoption. These services include customer onboarding, credit risk evaluation, repayment management, compliance support, and technical implementation for merchants. As more businesses adopt BNPL solutions, the need for specialized service providers is increasing rapidly.

Growth is also driven by the expansion of consulting, integration, chargeback management, fraud prevention, and customer support operations. With regulators tightening oversight and retailers scaling their digital payment strategies, service partners help them deploy BNPL efficiently while improving customer trust and repayment performance.

Purchase Ticket Size Insights

Why the Small Ticket Item (Up to US$ 300) Is Dominating the Buy Now Pay Later (BNPL) Market?

The Small Ticket Item (Up to US$ 300) is dominating the Buy Now Pay Later (BNPL) market by holding a share of 44.8%, because it fits the everyday spending habits of mass-market consumers. These low-value purchases — such as apparel, groceries, personal accessories, beauty products, and electronics add-ons — encourage customers to use BNPL as a convenient and risk-free payment alternative. The approval process is quick, the repayment cycle is shorter, and the perceived financial commitment is minimal, which makes this category highly appealing, especially among first-time BNPL users.

Its dominance also comes from the high frequency of online and in-store impulse purchases. For retailers, low-ticket BNPL options help reduce cart abandonment and increase conversion rates without exposing them to high credit risk. BNPL providers prefer this segment because it offers faster repayment turnover, strong repayment discipline, and wider adoption across age groups, especially millennials and Gen Z. The combination of low risk, fast approvals, and frequent purchase cycles solidifies the small-ticket category as the operational backbone of the BNPL market — easy to adopt, scalable, and indispensable for daily transactions.

The Mid Ticket Items (US$ 300 – US$ 1000) are fastest growing in the Buy Now Pay Later (BNPL) market with an expected CAGR of 23.6%, driven by increasing consumer willingness to finance lifestyle, home improvement, travel, and electronics purchases through convenient installment plans. As BNPL providers introduce flexible tenures, transparent charges, and higher spending limits, customers are becoming more confident in using BNPL for planned, value-driven purchases rather than only small daily expenses.

The strong growth also comes from the expansion of online retail, rising preference for budget-friendly financing, and the entry of major BNPL players into categories like smartphones, furniture, appliances, and personal healthcare services. This shift reflects a growing consumer trend: people want high-quality products but prefer splitting payments without interest or credit card dependency. As a result, mid-ticket BNPL usage is expanding rapidly among young professionals and digital-first shoppers, making it the fastest-growing segment in the overall market.

Business Model Insights

Why Business Driven Is Dominating the Buy Now Pay Later (BNPL) Market?

Business Driven is dominating the Buy Now Pay Later (BNPL) market by holding a share of 72.2% primarily due to its pivotal role in driving merchant adoption and ecosystem scalability. This dominance is largely attributed to strong merchant partnerships, integrated financing ecosystems, and the strategic role of BNPL providers as enablers of retail conversion.

Leading BNPL platforms such as Affirm, Klarna, Afterpay, and PayPal Pay Later have established robust collaborations with merchants to embed deferred payment solutions directly within checkout processes. This integration has allowed retailers to boost conversion rates, average order values, and customer retention — making BNPL a vital growth lever in e-commerce and omnichannel retail environments.

The business-driven BNPL model thrives on its B2B synergy, where platforms act as embedded finance partners rather than standalone credit facilitators. Merchants gain from zero-interest promotional financing options that drive impulse purchases and reduce cart abandonment, while BNPL providers benefit from merchant service fees and transaction data insights. With increasing merchant adoption across sectors — specially fashion, electronics, travel, and lifestyle — the model continues to expand its influence.

The structural advantage lies in its scalability and alignment with merchant revenue goals, creating a sustainable feedback loop of growth. Moreover, advances in AI-based credit risk assessment, real-time underwriting, and API integrations are empowering BNPL providers to streamline merchant onboarding and enhance payment flexibility.

Conversely, the Customer-Driven segment, representing 25.3% of the BNPL market, is the fastest-growing model with the highest CAGR during the forecast period. Growth in this segment is primarily fuelled by the rising preference for consumer-centric financial solutions that offer greater transparency, spending control, and accessibility. Consumer-led BNPL platforms — such as Splitit, Zip, and Sezzle — emphasize app-based ecosystems where users can manage purchases across multiple retailers. The increasing awareness of responsible credit usage and the shift toward digital-first payment experiences are accelerating adoption.

In the coming years, customer-driven BNPL models are expected to evolve with enhanced personalization, loyalty-driven incentives, and integrated credit scoring mechanisms. As users seek seamless, mobile-first financial solutions, this segment is poised to redefine the future of flexible consumer finance.

Mode Insights

Why Online Is Dominating the Buy Now Pay Later (BNPL) Market?

Business Driven is dominating the Buy Now Pay Later (BNPL) market by holding a share of 60.6% primarily due to its pivotal role in driving merchant adoption and ecosystem scalability. driven by the rapid digitization of commerce, increased smartphone penetration, and the shift in consumer preference toward seamless digital payment experiences.

E-commerce platforms such as Amazon, Flipkart, Shopify, and Alibaba have integrated BNPL options directly into their checkout systems, enabling instant credit access and frictionless transactions. This ease of use, combined with the growing comfort of consumers with digital payments, has positioned online BNPL as the preferred financing mode.

The dominance of the online mode stems from its structural advantages — scalability, data-driven personalization, and integration with digital ecosystems. BNPL providers leverage AI-based credit scoring and analytics to assess borrower risk instantly, minimizing approval times and expanding access to underserved consumers.

The integration of BNPL options within popular payment gateways, wallets, and fintech apps such as PayPal, Klarna, Afterpay, and Affirm enhances user convenience and merchant conversion rates, strengthening ecosystem loyalty.

Moreover, online BNPL platforms offer dynamic incentives such as zero-interest EMIs, cashback, and instant approvals, which significantly influence consumer purchasing behavior. Retailers benefit from higher average order values (AOVs) and reduced cart abandonment rates, making online BNPL a win-win model for both consumers and merchants. As online retail continues to expand globally — particularly in emerging markets like India, Indonesia, and Brazil — the digital-first model will continue to drive BNPL adoption at scale.

Vertical Insights

Why Electronics Dominating the Buy Now Pay Later (BNPL) Market?

The Electronics is dominating the Buy Now Pay Later (BNPL) market by holding a share of 40.3%, driven by the high-ticket value of electronic products and the growing preference for flexible payment solutions among digital shoppers. Consumers increasingly opt for BNPL options when purchasing gadgets, smartphones, laptops, and home appliances, as these deferred payment plans reduce the immediate financial burden while maintaining access to premium technology.

E-commerce platforms and electronic retailers are aggressively integrating BNPL providers like Afterpay, Klarna, Affirm, and PayPal Credit at checkout to attract cost-conscious yet tech-savvy buyers. This integration is further strengthened by exclusive BNPL promotions, zero-interest installment options, and instant approval processes.

Moreover, the rise in online electronics sales, particularly during festive and promotional seasons, significantly boosts BNPL adoption. The demand surge is further amplified by Gen Z and millennial consumers who prefer digital credit solutions over traditional credit cards due to greater transparency and ease of use.

The dominance of electronics in BNPL is also fuelled by manufacturers and retailers’ strategic partnerships with fintech providers, which enhance customer retention through loyalty programs and seamless financing journeys. As inflationary pressures and cost-of-living challenges persist, BNPL offers a bridge between affordability and aspiration, making it a central payment tool for electronics purchases.

In contrast, the Fashion industry represents the fastest-growing segment, projected to record a CAGR of 23.6% over the forecast period. The segment’s rapid growth is attributed to the rise of impulse-driven shopping, fast fashion trends, and the integration of BNPL options across online apparel and accessories platforms such as ASOS, Zara, H&M, and SHEIN. Younger demographics, who prioritize affordability and variety, increasingly leverage BNPL to buy trending outfits without upfront payments.

As fashion retailers adopt AI-based personalization and social commerce strategies, BNPL services are becoming embedded in the customer journey — encouraging repeat purchases, reducing cart abandonment, and driving higher average order values. With evolving consumer behaviour and retail digitization, BNPL is set to remain a key enabler of growth across both electronics and fashion sectors.

Segments Covered in the Report

By Component

- Platform/Solutions

- Services

By Purchase Ticket Size

- Small Ticket Item (Up to US$ 300)

- Mid Ticket Items (US$ 300 – US$ 1000)

- Higher Prime Segments (Above US$ 1000)

By Business Model

- Customer Driven

- Business Driven

By Mode

- Online

- Offline

By Vertical

- Home & Furniture

- Electronics

- Fashion

- Others

Regional Insights

Why Is North America Leading the Buy Now Pay Later (BNPL) Market?

North America dominates the Global Buy Now Pay Later (BNPL) Market with a 36.7% share, owing to its strong digital payment infrastructure, high consumer spending power, and early adoption of fintech innovations. The region’s leadership is underpinned by the presence of leading BNPL providers such as Affirm, Afterpay, Klarna, and PayPal Credit, which have deeply integrated their services across e-commerce, retail, and omnichannel payment ecosystems.

The maturity of the digital economy in the U.S. and Canada, coupled with high smartphone penetration and tech-driven consumer behavior, has accelerated BNPL usage across both online and in-store channels. Retail giants like Amazon, Walmart, Best Buy, and Target actively promote BNPL options to enhance checkout flexibility and boost conversion rates, particularly among millennials and Gen Z consumers who prefer short-term installment payments over traditional credit cards.

A robust financial services ecosystem and a favorable regulatory environment have enabled fintech firms to innovate rapidly — introducing tailored credit assessments, AI-based risk scoring, and transparent repayment models. Consumers in North America also exhibit strong trust in digital payment methods, further fueling BNPL adoption in categories such as electronics, fashion, travel, and home improvement.

The region’s dominance is reinforced by strategic partnerships between retailers, banks, and fintech companies, as well as significant venture capital investments supporting BNPL expansion. Moreover, rising e-commerce penetration, particularly during festive seasons like Black Friday and Cyber Monday, amplifies transaction volumes processed through BNPL solutions.

North America’s competitive edge also stems from its focus on consumer experience and financial inclusivity, enabling even subprime borrowers to access interest-free payment plans. With continuous innovation in embedded finance, real-time payment systems, and AI-driven credit analytics, North America remains the most technologically advanced and commercially mature BNPL market globally. Its deep-rooted digital infrastructure and evolving consumer credit behavior ensure sustained dominance in the coming years.

Canadian Model in the Buy Now Pay Later (BNPL) Market

The Canadian model in the Buy Now Pay Later (BNPL) market stands out for its balanced blend of innovation, trust, and inclusivity, driven by strong financial regulation, advanced digital infrastructure, and a consumer-first approach. Canada has built a resilient BNPL ecosystem by integrating fintech innovation with responsible lending standards — creating a framework that supports both consumer protection and business growth.

Government support plays a key role in shaping the Canadian BNPL landscape. Through open banking initiatives, financial data transparency, and regulatory oversight from entities like the Financial Consumer Agency of Canada (FCAC), the market fosters innovation without compromising consumer safety. These initiatives have encouraged both domestic startups and global BNPL providers to invest in the Canadian fintech sector, accelerating digital payment adoption.

The Canadian model also benefits from high digital literacy and trust in financial institutions, making it one of the most secure and scalable BNPL environments globally. Consumers across urban centers such as Toronto, Vancouver, and Montreal increasingly prefer BNPL for managing high-value purchases, leveraging the convenience of installment-based payments without interest or credit card dependence.

Why Is the Asia Pacific Leading the Charge in the Buy Now Pay Later (BNPL) Market?

Asia Pacific stands as the fastest-growing region in the Buy Now Pay Later (BNPL) market, projected to record an impressive CAGR of 36.8%, driven by its vast digital population, mobile-first economy, and rapid shift toward cashless transactions. The region’s BNPL boom is fueled by rising e-commerce activity, youthful demographics, and a thriving fintech innovation landscape that is reshaping consumer payment behavior.

Countries like India, China, Indonesia, Japan, and South Korea are at the forefront of this transformation. Together, they represent billions of digitally active consumers who prefer convenient, interest-free payment options over traditional credit models. The proliferation of super apps such as Alipay, WeChat Pay, Paytm, GrabPay, and Gojek — which seamlessly integrate shopping, payments, and finance — has created an ecosystem where BNPL is not just an option but an integral part of the digital lifestyle.

Asia Pacific’s BNPL expansion is also powered by e-commerce giants and retail innovators like Alibaba, Lazada, Shopee, and Flipkart, who embed BNPL features at checkout to drive higher cart values and repeat purchases. Affordable smartphones, low-cost internet access, and digital literacy initiatives have further accelerated adoption, enabling even rural and semi-urban consumers to access flexible payment solutions.

In addition, regulatory support across major markets and partnerships between global players and local fintechs are making BNPL more inclusive, transparent, and scalable. Millennials and Gen Z consumers — known for their comfort with digital finance — are embracing BNPL to manage budgets, access premium products, and build financial independence.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- ASEAN Countries

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of MEA

Market Value Chain Analysis in Buy Now Pay Later (BNPL)

- Fintech BNPL Providers: Fintech BNPL providers such as Klarna, Afterpay, Affirm, Zip, and PayPal Credit form the heart of the BNPL value chain. These platforms design and manage short-term installment payment solutions, allowing consumers to defer payments without interest while merchants receive instant payouts.

- Merchants and Retailers: Merchants and retailers — ranging from e-commerce giants like Amazon, Walmart, and Best Buy to independent Shopify stores — play a crucial role in embedding BNPL at checkout. By offering flexible payment options, they increase conversion rates, reduce cart abandonment, and boost average order values. Retailers benefit from higher sales volumes and customer loyalty as BNPL empowers consumers to make premium purchases with ease. The merchant’s strategic partnerships with BNPL platforms also help optimize marketing campaigns and loyalty programs, enhancing long-term revenue growth.

- Payment Gateway Providers: Entities such as Stripe, Adyen, and Worldpay serve as the technological bridge connecting BNPL providers, merchants, and consumers. Their role is to ensure secure, real-time payment processing through advanced encryption, authentication, and fraud-prevention systems. By enabling seamless integration with merchant platforms, payment gateways uphold transaction reliability and consumer trust — critical for sustaining the BNPL ecosystem’s operational efficiency and scalability.

- Technology Enablers: Technology infrastructure providers like Amazon Web Services (AWS), Google Cloud, Microsoft Azure, and Plaid power the BNPL ecosystem with cloud computing, API connectivity, AI frameworks, and data security solutions. These enablers ensure the scalability, speed, and resilience of BNPL operations while supporting data analytics, personalization, and regulatory compliance. Their platforms also enable real-time insights and automation, making the BNPL experience more intuitive for both users and merchants.

- Financial Institutions and Investors: Banks and investors — including Goldman Sachs, SoftBank Vision Fund, and Sequoia Capital — provide essential capital and liquidity to fuel BNPL expansion. Their funding supports product innovation, international growth, and regulatory adaptation, ensuring the sustainability of this fast-scaling fintech segment. In addition to venture capital, partnerships between BNPL providers and traditional banks enhance credit offerings and operational synergies, fostering ecosystem maturity and competitive advantage.

- Regulators and Policy Bodies: Regulatory agencies such as the U.S. Consumer Financial Protection Bureau (CFPB), the Financial Conduct Authority (FCA, UK), and the Australian Securities and Investments Commission (ASIC) oversee the BNPL industry to ensure transparency, consumer protection, and responsible lending practices. These bodies shape the framework within which BNPL operates, defining rules for credit disclosure, data privacy, and repayment fairness — ultimately maintaining market integrity and public trust.

Top Buy Now Pay Later (BNPL) Market Companies

- Klarna Inc.: It is a global leader in the BNPL ecosystem, renowned for its smooth, user-centric payment experience. With over 150 million active users and partnerships with top retailers, Klarna offers flexible installment plans, transparent repayment options, and AI-driven credit risk management. Its innovative shopping app combines personalized recommendations, loyalty rewards, and post-purchase insights — transforming the consumer journey into a seamless, data-powered experience. Klarna’s integration across online and offline retail makes it a dominant force in digital finance.

- Afterpay (Block Inc.): Afterpay, owned by Block Inc., is revolutionizing consumer spending habits through its “Pay in 4” model, enabling zero-interest installments across global retail networks. The company’s strength lies in its vast merchant partnerships and strong millennial customer base. With embedded payment solutions and strategic collaborations in fashion, beauty, and lifestyle sectors, Afterpay drives both consumer affordability and merchant conversion rates. Its omnichannel integration and focus on responsible spending position it as a growth catalyst in the global BNPL landscape.

- Affirm, Inc.: Affirm stands out for its transparent, no-late-fee financing model that builds consumer trust. Backed by robust AI algorithms and deep retail partnerships — including Amazon, Walmart, and Shopify — Affirm empowers consumers with flexible payment schedules while providing merchants with increased sales and lower cart abandonment. The company’s data-driven risk management system and innovative savings tools strengthen its position as a leading fintech innovator reshaping digital lending.

- PayPal Holdings, Inc.: PayPal Holdings, Inc. leverages PayPal’s massive global user base and trusted payment network to offer BNPL flexibility directly within its checkout system. Its wide merchant integration and seamless digital wallet experience create a unified payment journey for both buyers and sellers. With built-in security, buyer protection, and zero-interest promotional offers, PayPal Credit has become a key enabler of e-commerce growth and consumer loyalty.

Top Key Players in the Market

- Affirm, Inc.

- Klarna Inc.

- Splitit Payments, Ltd.

- Sezzle

- Perpay Inc.

- Zip Co, Ltd

- PayPal Holdings, Inc.

- AfterPay Limited

- Openpay

- LatitudePay Financial Services

- Other Major Players

Recent Developments

- In March 2025, DoorDash Partnered with Klarna to Offer ‘Buy Now, Pay Later’ Options for US Customers. The new payment features allow users to pay for groceries, retail items, and even the DashPass Annual Plan through various flexible methods. The partnership aims to provide users with the convenience of paying in full, making four equal interest-free installments, or postponing payments until a more suitable time.

- In March 2023, Apple Inc. launched its “buy now, pay later” (BNPL) service in the United States, a move that threatens to disrupt the fintech sector. The service, Apple Pay Later, allow users to split purchases into four payments spread over six weeks with no interest or fees. It initially be offered to select users, with plans of a full roll-out in the coming months.