What is the Bio-Based Chemicals Market Size?

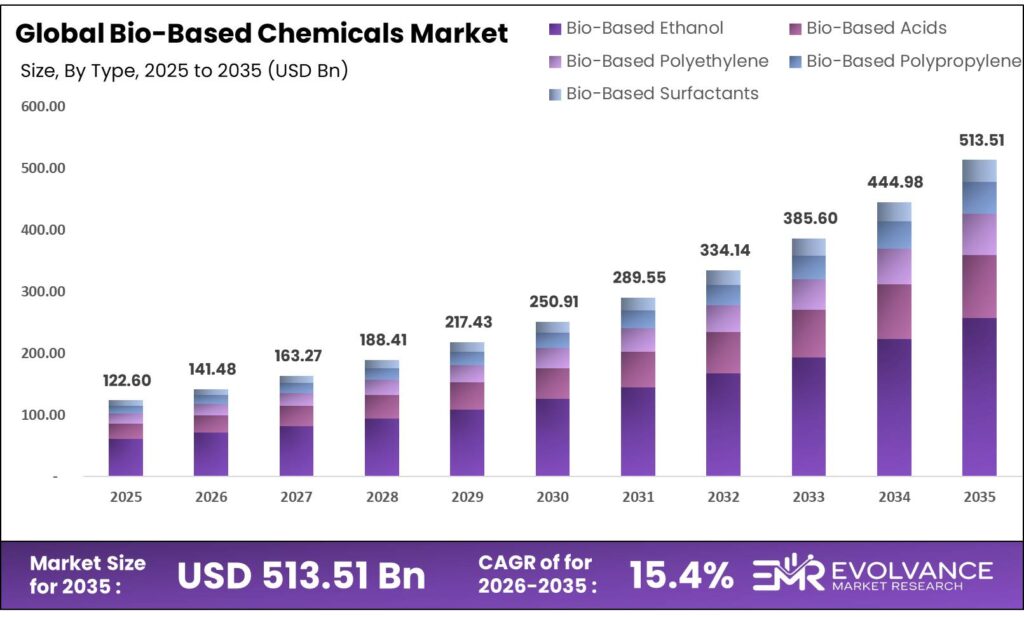

Global Bio-Based Chemicals Market size is expected to be worth around USD 513.51 Billion by 2035 from USD 122.60 Billion in 2025, growing at a CAGR of 15.4% during the forecast period 2026 to 2035. Rising demand for green raw materials in packaging and automotive sectors drives this rapid growth. Government mandates for renewable chemicals and net-zero targets across industries fuel market expansion globally.

Market Highlights

- The Global Bio-Based Chemicals Market valued at USD 122.60 Billion in 2025, projected to reach USD 513.51 Billion by 2035, at a CAGR of 15.4% during the forecast period 2026-2035.

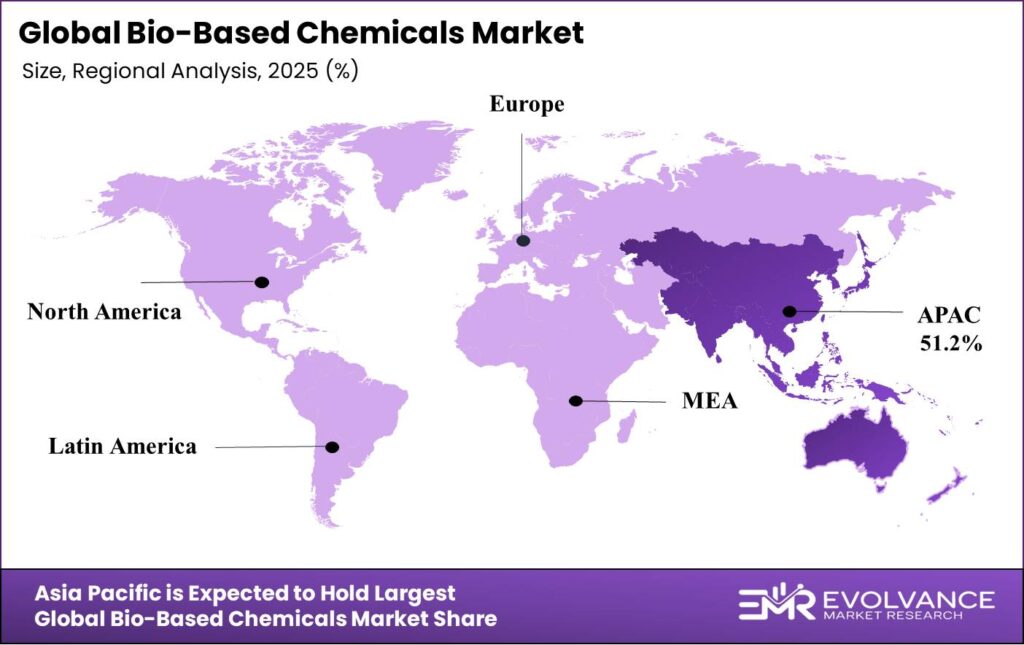

- Asia Pacific dominates with 51.2% market share, valued at USD 62.8 Billion.

- Bio-Based Ethanol segment dominates by type with 39.4% market share in 2025.

- Liquid form segment leads with 43.6% share driven by solvent and surfactant applications.

- Plant-Based source segment holds 47.1% share due to abundant agricultural feedstock availability.

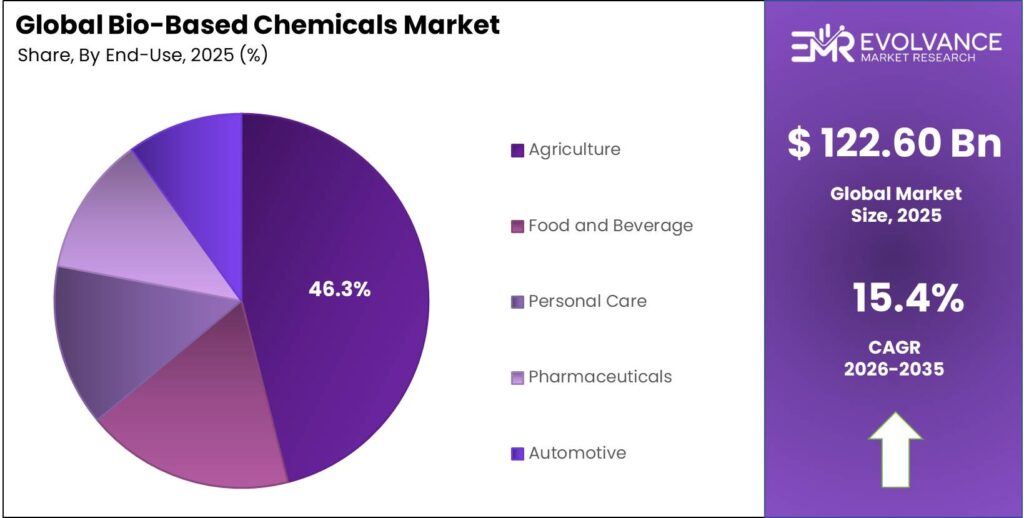

- Agriculture end-use sector commands 46.3% market share in 2025.

Market Overview

Bio-based chemicals refer to products made from renewable biomass sources rather than fossil fuels. These chemicals include ethanol, acids, polymers, surfactants, and solvents derived from plant, animal, microbial, or waste materials. They serve as green options for traditional petrochemical products across multiple sectors.

The shift toward renewable materials gains speed as industries face pressure to cut carbon footprints. Companies now pursue net-zero goals that require low-carbon raw materials. Crude oil price swings push chemical makers to explore stable, renewable feedstock options for long-term supply security.

According to the IEA Bioenergy report, global bio-based chemical and polymer production currently stands at around 90 million tonnes. This compares to about 330 million tonnes of petrochemical production worldwide. The data shows significant room for bio-based market share growth in coming years.

As per the European Bioplastics Association, the global bioplastics market will reach 2.74 million tons by 2024. This growth reflects rising adoption of bio-based polymers in packaging films, bottles, and automotive components. China targets bio-based products to account for 30% of total chemical output by 2030.

Data from the IEA Bioenergy report indicates the fermentation products market exceeded 110 million tonnes with a value of 207 billion USD. Alcohols made up 94% of volume and 87% of value in this segment. The Brazilian government reports bioethanol accounted for roughly 27% of the country’s fuel supply in 2020.

Government policies worldwide favor bio-based production through tax breaks, grants, and mandates. The European Union, United States, and Asian nations invest billions in bio-refinery plants and research programs. These moves create strong support for market players entering the renewable chemicals space.

Consumer brands demand sustainable ingredients for personal care, food packaging, and automotive parts. This pull from end users drives chemical suppliers to expand bio-based product lines. Brand owners use renewable content as a key selling point in marketing campaigns.

Technology advances in enzyme design and microbial fermentation lower production costs steadily. Second-generation feedstocks from non-food crops and agricultural waste reduce competition with food supplies. These breakthroughs make bio-based chemicals more competitive against conventional petrochemical products in price and performance.

By Type Insights

Bio-Based Ethanol dominates with 39.4% due to widespread use in fuel blending and industrial applications.

In 2025, Bio-Based Ethanol held a dominant market position in the By Type segment of Bio-Based Chemicals Market, with a 39.4% share. Ethanol serves as a key fuel additive and solvent in pharma, cosmetics, and food processing. Government mandates for renewable fuel content in gasoline drive consistent demand across North America, Europe, and Brazil.

Bio-Based Acids find broad use in food preservation, cleaning products, and polymer production. Citric acid, lactic acid, and succinic acid production grows as companies seek biodegradable alternatives. These acids offer lower toxicity and better environmental profiles compared to petroleum-derived options in multiple industrial processes.

Bio-Based Polyethylene gains traction in packaging films, bottles, and containers as brands commit to renewable content. Major consumer goods companies now specify minimum bio-based plastic content in their supply chains. This segment benefits from existing processing equipment compatibility and similar performance to fossil-based polyethylene.

Bio-Based Polypropylene serves automotive interiors, textiles, and durable goods with growing commercial adoption. Recent pilot projects prove technical feasibility for large-scale production from biomass. Price competitiveness improves as production volumes scale up through new bio-refinery investments globally.

Bio-Based Surfactants replace petroleum-derived cleaning agents in detergents, personal care products, and industrial cleaners. Plant oil-based surfactants show superior biodegradability and skin compatibility. Regulatory pressure to remove harmful chemicals from household products accelerates market penetration in Europe and North America.

By Form Insights

Liquid dominates with 43.6% due to ease of handling in chemical processing and blending operations.

In 2025, Liquid held a dominant market position in the By Form segment of Bio-Based Chemicals Market, with a 43.6% share. Liquid bio-based chemicals work well as solvents, fuel additives, and intermediate products in manufacturing. Ethanol, glycerol, and liquid acids flow easily through existing pipelines and storage tanks without major equipment changes.

Solid bio-based chemicals include polymers, resins, and crystalline acids used in plastics and coatings. Pelletized bio-based polyethylene and polypropylene ship efficiently and feed directly into injection molding machines. Solid forms offer longer shelf life and reduced transportation costs per unit of active ingredient.

Gas bio-based chemicals consist mainly of biogas and syngas from biomass gasification processes. These gases serve as fuel for power generation or feedstock for methanol and ammonia synthesis. Gas products require specialized storage and handling systems but deliver high energy density for industrial applications.

By Source Insights

Plant-Based dominates with 47.1% due to abundant crop residues and dedicated energy crops worldwide.

In 2025, Plant-Based held a dominant market position in the By Source segment of Bio-Based Chemicals Market, with a 47.1% share. Corn, sugarcane, wheat, and vegetable oils provide proven feedstocks for ethanol, acids, and polymer production. Agricultural infrastructure already exists for growing, harvesting, and transporting these materials to bio-refineries at commercial scale.

Animal-Based sources include fats, oils, and proteins from meat processing byproducts and dairy operations. Tallow and animal fats convert efficiently into biodiesel, surfactants, and lubricants. This segment helps divert waste streams from landfills while creating value-added chemical products for industrial customers.

Microbial-Based production uses bacteria, yeast, and algae to synthesize specialty chemicals through fermentation. Engineered microbes produce high-value compounds like amino acids, vitamins, and industrial enzymes. Precision fermentation offers year-round production without seasonal constraints or land use competition.

Waste-Based feedstocks utilize municipal solid waste, food scraps, and agricultural residues as raw materials. Converting waste to chemicals reduces disposal costs while creating renewable products. Technology improvements in waste sorting and pre-treatment make this source increasingly cost-competitive with virgin biomass.

By Application Insights

Solvents dominates with 41.2% due to extensive use in coatings, adhesives, and pharmaceutical manufacturing.

In 2025, Solvents held a dominant market position in the By Application segment of Bio-Based Chemicals Market, with a 41.2% share. Bio-ethanol and bio-based esters replace toxic petroleum solvents in paints, inks, and cleaning products. Regulatory restrictions on volatile organic compounds push formulators toward greener solvent alternatives across industrial and consumer applications.

Surfactants serve as cleaning and emulsifying agents in detergents, personal care items, and industrial processes. Plant oil-based surfactants match or exceed performance of synthetic versions while offering better biodegradability. Consumer preference for natural ingredients drives reformulation of household and beauty products worldwide.

Adhesives made from bio-based resins and polymers bond wood, paper, and packaging materials effectively. Starch-based and protein-based adhesives work well in paper mills and furniture production. These products reduce formaldehyde emissions and improve indoor air quality in residential and commercial buildings.

Plastics represent the fastest-growing application as brands seek renewable polymer content in packaging and products. Bio-based polyethylene, polylactic acid, and polyhydroxyalkanoates replace conventional plastics in bottles, films, and containers. Compostable options gain favor in food service and single-use applications.

Coatings incorporate bio-based resins, oils, and additives for paints, varnishes, and protective finishes. Linseed oil, soy-based resins, and bio-based pigments deliver durable performance with lower environmental impact. Construction and automotive sectors adopt these coatings to meet green building standards and emissions targets.

By End Use Insights

Agriculture dominates with 46.3% due to high demand for bio-pesticides, fertilizers, and soil treatments.

In 2025, Agriculture held a dominant market position in the By End Use segment of Bio-Based Chemicals Market, with a 46.3% share. Bio-based pesticides, herbicides, and plant growth regulators offer safer alternatives to synthetic agrochemicals. Organic farming expansion and integrated pest management practices drive adoption of natural crop protection products globally.

Food and Beverage industries use bio-based acids, enzymes, and preservatives in processing and packaging applications. Natural preservatives extend shelf life without synthetic additives that consumers avoid. Bio-based packaging films and bottles align with sustainability goals of major food brands and retailers.

Personal Care products incorporate bio-based surfactants, emollients, and active ingredients in cosmetics and toiletries. Plant-derived ingredients appeal to consumers seeking clean beauty and natural formulations. Premium pricing for natural personal care items supports higher costs of bio-based raw materials.

Pharmaceuticals rely on bio-based solvents, excipients, and active pharmaceutical ingredients in drug production. Fermentation-derived antibiotics, vitamins, and amino acids represent established bio-based chemical applications. Strict quality standards and regulatory approval processes ensure product consistency and safety.

Automotive manufacturers specify bio-based plastics, foams, and composites for interior parts and under-hood components. Natural fiber composites reduce vehicle weight while meeting performance requirements. European auto makers lead adoption driven by circular economy regulations and corporate sustainability commitments.

Market Segments Covered in the Report

By Type

- Bio-Based Ethanol

- Bio-Based Acids

- Bio-Based Polyethylene

- Bio-Based Polypropylene

- Bio-Based Surfactants

By Form

- Liquid

- Solid

- Gas

By Source

- Plant-Based

- Animal-Based

- Microbial-Based

- Waste-Based

By Application

- Solvents

- Surfactants

- Adhesives

- Plastics

- Coatings

By End Use

- Agriculture

- Food and Beverage

- Personal Care

- Pharmaceuticals

- Automotive

Bio-Based Chemicals Market Regional Insights

Asia Pacific Dominates the Bio-Based Chemicals Market with a Market Share of 51.2%, Valued at USD 62.8 Billion

Asia Pacific leads the global bio-based chemicals market with a 51.2% share valued at USD 62.8 Billion. China invests over USD 20 billion in bio-based chemical plants targeting 30% of chemical output by 2030. Abundant agricultural feedstock, low production costs, and strong government support position the region for continued dominance.

North America Market Trends

North America shows robust growth driven by federal renewable fuel standards and state-level green chemistry programs. The United States leads in advanced enzyme technology and industrial biotechnology research. Major chemical companies partner with agricultural producers to secure consistent biomass supply chains across corn and soy-growing regions.

Europe Market Trends

Europe pursues aggressive circular economy policies that favor bio-based materials over fossil alternatives. The European Union funds bio-refinery projects and sets renewable content mandates for plastics and chemicals. Germany, France, and the Netherlands host leading bio-based chemical production facilities serving regional manufacturing clusters.

Latin America Market Trends

Latin America benefits from large-scale sugarcane and soy production that supports bio-ethanol and bio-diesel industries. Brazil maintains 27% bioethanol fuel blending rates and exports renewable chemicals globally. Investment in second-generation technologies using bagasse and crop residues expands production capacity without increasing farmland use.

Middle East & Africa Market Trends

Middle East & Africa explores bio-based chemicals as economic diversification strategy beyond petroleum exports. South Africa develops bio-refinery projects using local agricultural waste and dedicated energy crops. GCC nations invest in research partnerships to leverage biotechnology expertise for sustainable chemical production.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The European Union updated its Renewable Energy Directive in 2024 with stricter sustainability criteria for biomass sourcing. Member states must ensure bio-based chemicals come from certified sustainable forestry and agriculture. These rules prevent deforestation and protect biodiversity while promoting circular economy practices across chemical supply chains.

China announced plans in 2024 to achieve 30% bio-based chemical output by 2030 through the National Bio-Based Industry Development Plan. This policy directs over 20 billion USD in government funding toward bio-refinery construction and technology development. Tax incentives and preferential loans support companies transitioning from petrochemical to renewable feedstock operations.

The United States maintains renewable fuel standards requiring minimum volumes of bio-based ethanol and biodiesel in transportation fuel. EPA renewable identification numbers track compliance and create market incentives for bio-based chemical production. State-level green chemistry initiatives in California and New York offer additional grants and tax credits for bio-based manufacturing facilities.

Emerging Trends

Digital Transformation Reshapes Market Landscape

Artificial intelligence optimizes fermentation parameters, enzyme selection, and process control in real time. Machine learning models predict yields and quality based on feedstock characteristics and operating conditions. These digital tools help bio-refineries maximize output while minimizing energy consumption and waste generation.

The market size for production of fermentation products was above 110 million tonnes and with a value of USD 207 billion. Alcohols made up the largest share (94% of volume and 87% of value) of which the largest share was ethanol used as transportation fuel. Production of fine chemicals was around 11 million tonnes. The projected market growth for fermentation products until 2020 is 4.6% annually and 6.5% if excluding alcohols.

Pilot plants test new bio-based chemical routes at smaller scale before full commercial deployment. Modular bio-refinery designs allow flexible production of multiple products from the same feedstock. This adaptability helps producers respond quickly to market demand shifts and feedstock availability changes.

Drivers

Accelerating Government Mandates and Incentive Programs Supporting Renewable and Low-Carbon Chemical Production

Renewable fuel standards in North America and Europe create guaranteed demand for bio-ethanol and biodiesel. These mandates require fuel suppliers to blend specific volumes of renewable content into gasoline and diesel. Compliance tracking systems and trading mechanisms ensure market stability for bio-based chemical producers.

Governments worldwide implement policies that mandate or incentivize bio-based chemical adoption across industries. Tax credits, grants, and low-interest loans reduce financial barriers for companies building bio-refineries. China targets 30% bio-based chemical output by 2030 with over 20 billion USD in planned investments.

Carbon pricing policies and emissions trading schemes make fossil-based chemicals more expensive relative to bio-based alternatives. Companies facing carbon taxes seek low-carbon raw materials to reduce their emissions footprint. This regulatory pressure accelerates switching from petroleum to renewable feedstocks across chemical value chains.

Restraints

High Production Costs Associated with Biomass Processing and Conversion Technologies

Bio-based chemical production requires expensive pre-treatment, fermentation, and separation equipment compared to petroleum refining. Capital costs for bio-refineries run higher per unit of output than conventional chemical plants. Smaller production scales prevent bio-based facilities from achieving the same economies of scale as large petrochemical complexes.

Enzyme costs, energy inputs, and yield losses during conversion drive up operating expenses significantly. Many bio-based processes achieve lower conversion efficiency than petrochemical routes. The Brazilian government has implemented policies to promote bioethanol, which accounted for approximately 27% of the country’s fuel supply in 2020.

Research and development spending to improve process efficiency and reduce costs remains substantial. Companies must invest heavily in technology development before achieving commercial viability. The long payback periods and technical risks deter some investors from funding bio-based chemical projects at scale.

Growth Factors

Technological Advancements Accelerate Market Expansion

Enzyme engineering breakthroughs improve conversion rates and reduce processing time for biomass breakdown. Advanced fermentation techniques using genetically modified microbes produce higher yields of target chemicals. These innovations lower production costs and make bio-based chemicals more competitive against petroleum-derived products in price and performance.

Synthesis gas (syngas) is a gas mixture of carbon monoxide (CO), hydrogen (H2), methane (CH4) and carbon dioxide (CO2) and nitrogen (N2). It is produced by subjecting biomass to extreme heat, typically in the range 800-1500˚C, in the presence of oxygen or air in a process known as gasification.

Integration of carbon capture systems within bio-refineries creates carbon-negative production processes. Biomass growth absorbs atmospheric CO2 while processing emissions get captured and stored or reused. This positions bio-based chemicals as climate solutions that actively remove carbon rather than just reducing emissions.

Key Companies Insights

BASF SE operates multiple bio-based chemical production lines including bio-based succinic acid and bio-polyamides. The company invests heavily in partnerships with biotechnology firms to develop new enzyme technologies. BASF targets renewable content across its portfolio to meet customer demand for sustainable ingredients in coatings, plastics, and personal care products.

Braskem SA leads bio-based polyethylene production with commercial-scale plants using Brazilian sugarcane ethanol as feedstock. The company supplies bio-PE to major consumer goods brands for packaging applications worldwide. Braskem continues expanding capacity to meet growing demand for renewable plastic resins in bottles, films, and containers.

Cargill Incorporated produces bio-based acids, sweeteners, and specialty ingredients through fermentation and chemical processing. The company leverages its agricultural supply network to source consistent biomass feedstock at competitive prices. Cargill partners with chemical companies to commercialize new bio-based products for food, pharma, and industrial markets.

DuPont develops advanced bio-based polymers and specialty chemicals using proprietary fermentation and catalysis technologies. The company focuses on high-performance materials for automotive, electronics, and industrial applications. DuPont’s research pipeline includes new bio-based intermediates that enable drop-in replacement of petroleum-derived chemicals.

Key Companies

- BASF SE

- Braskem SA

- Cargill Incorporated

- AGAE Technologies

- Toray Industries Inc.

- Total Energies

- Vertec BioSolvents

- DuPont

- Evonik Industries

- Koninklijke DSM N.V

- Dow Chemicals

- GFBiochemicals Ltd.

- IP Group PLC

- LyondellBasell

- Archer Daniels Midland Company

- Mitsubishi Chemical Corporation

Recent Development

- January 2025 – BASF SE launched a new bio-based polyamide production line in Germany with capacity of 50,000 tonnes annually. The facility uses renewable feedstock and cuts carbon emissions by 60% compared to conventional production methods.

- March 2025 – Braskem SA announced expansion of its bio-based polyethylene plant in Brazil adding 100,000 tonnes annual capacity. The investment of 250 million USD responds to growing demand from packaging customers in North America and Europe.

- May 2025 – Cargill Incorporated partnered with a European biotech firm to commercialize bio-based acrylic acid from corn starch. The joint venture plans pilot production of 10,000 tonnes by 2026 for coatings and adhesives applications.

- July 2025 – Total Energies opened a bio-refinery in France producing 40,000 tonnes of bio-based surfactants from vegetable oils. The facility supplies renewable ingredients to detergent and personal care manufacturers across Europe.

- September 2025 – DuPont introduced a new bio-based polymer for automotive interiors achieving 70% renewable content. The material meets automotive industry specifications while reducing carbon footprint by 45% versus petroleum-based alternatives.

- November 2025 – Evonik Industries invested 150 million EUR in a bio-based specialty chemicals plant in Singapore with 25,000 tonnes capacity. Production focuses on amino acids and performance additives for animal nutrition and personal care markets.

- January 2025 – Archer Daniels Midland Company acquired a bio-based chemicals startup for 500 million USD to expand its specialty ingredients portfolio. The deal adds fermentation technology for producing bio-based solvents and plasticizers at commercial scale.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 122.60 Billion |

| Forecast Revenue (2035) | USD 513.51 Billion |

| CAGR (2026-2035) | 15.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Bio-Based Ethanol, Bio-Based Acids, Bio-Based Polyethylene, Bio-Based Polypropylene, Bio-Based Surfactants), By Form (Liquid, Solid, Gas), By Source (Plant-Based, Animal-Based, Microbial-Based, Waste-Based), By Application (Solvents, Surfactants, Adhesives, Plastics, Coatings), By End Use (Agriculture, Food and Beverage, Personal Care, Pharmaceuticals, Automotive) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BASF SE, Braskem SA, Cargill Incorporated, AGAE Technologies, Toray Industries Inc., Total Energies, Vertec BioSolvents, DuPont, Evonik Industries, Koninklijke DSM N.V, Dow Chemicals, GFBiochemicals Ltd., IP Group PLC, LyondellBasell, Archer Daniels Midland Company, Mitsubishi Chemical Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |