What is the AI Prior Authorization Automation Market?

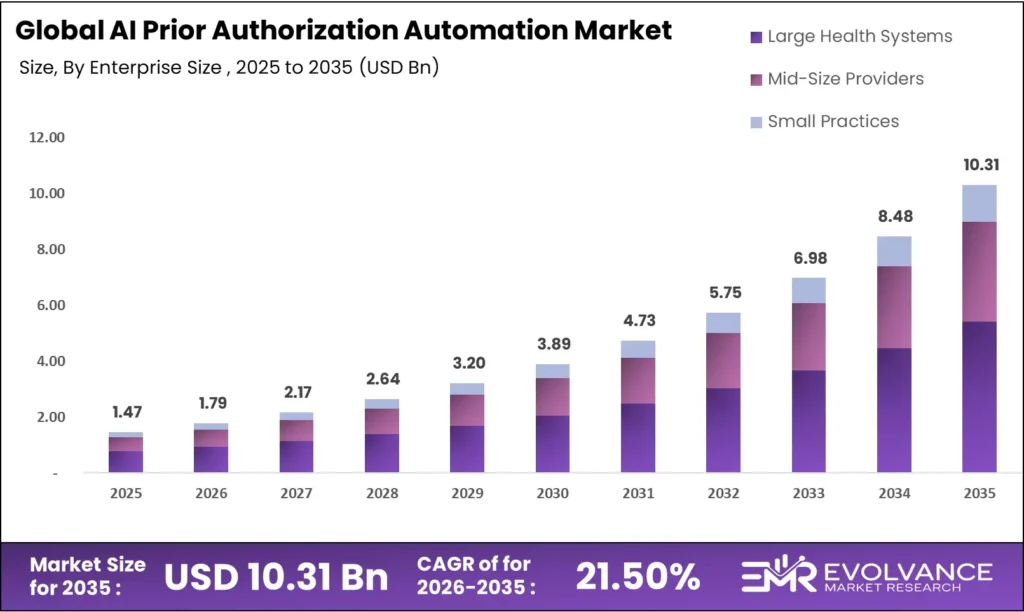

The global AI prior authorization automation market was valued at USD 1.47 billion in 2025 and is projected to reach approximately USD 10.31 billion by 2035, growing at a CAGR of 21.50% during the forecast period 2026 to 2035. Federal mandates requiring electronic prior authorization interoperability, escalating provider administrative burden, and proven AI-driven cost savings are the structural forces producing this compound growth trajectory.

Healthcare organizations spend an estimated USD 35 billion annually on manual prior authorization administrative costs in the US alone, per the AMA 2025 Prior Authorization and Utilization Management Reform Progress Report. Each authorization request consumes an average 14 minutes of physician time and 46 minutes of clinical staff time — inefficiencies that AI prior authorization automation platforms compress to under three minutes of net human review per case at scale. The CAQH Index 2024 separately estimated that fully electronic prior authorization transactions save the US healthcare system USD 417 million annually versus manual workflows. For payers and providers absorbing simultaneous rate pressure and workforce shortages, the AI prior authorization automation business case has shifted from pilot-stage curiosity to board-level capital allocation priority.

AI Prior Authorization Automation Market Highlights: Key Data at a Glance

- Market value: USD 1.47 billion in 2025, forecast to USD 10.31 billion by 2035 at 21.50% CAGR

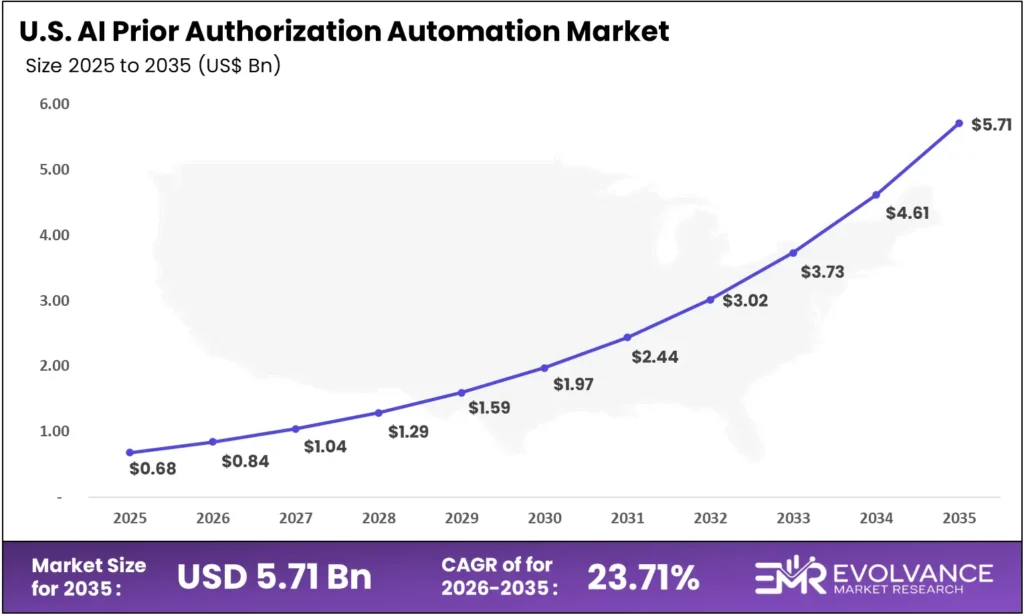

- US market: USD 0.68 billion in 2025, forecast to USD 5.71 billion by 2035 at 23.71% CAGR

- Dominant solution: Software with 72.4% revenue share driven by SaaS subscriptions and cloud-native deployment economics

- Dominant deployment: Cloud-Based with 68.9% revenue share anchoring real-time EHR integration and FHIR interoperability

- Dominant application: Medical Prior Authorization with 43.2% revenue share fueled by specialty care and surgical approval complexity

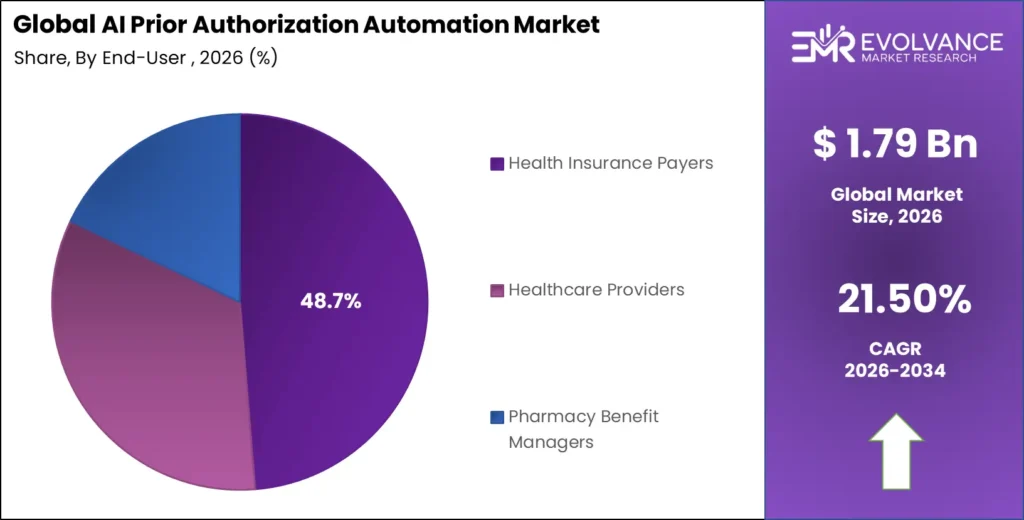

- Dominant end-user: Health Insurance Payers with 48.7% share deploying AI to reduce improper payment ratios and appeals volume

- Dominant technology: Natural Language Processing and Large Language Models leading all AI prior authorization investment categories

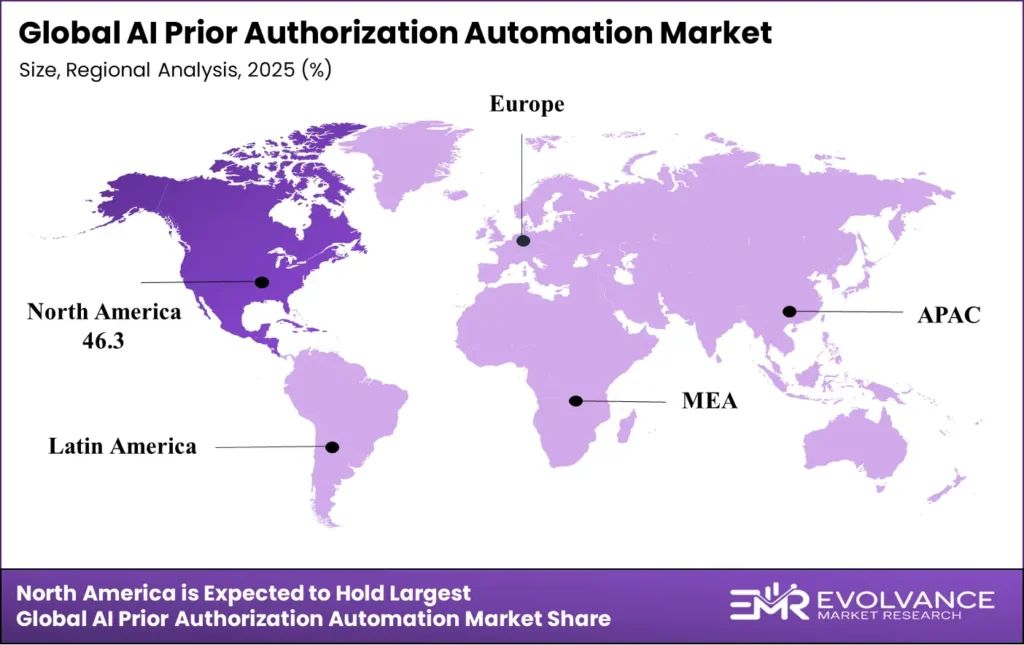

- North America: Largest regional share at 46.3%, valued at USD 0.68 billion in 2025

- Asia-Pacific: Fastest-growing region at 26.1% CAGR driven by Australia, India, and South Korea

- Regulatory catalyst: CMS ePA mandate compliance deadline January 2027 functioning as structural procurement accelerator across the entire US payer market

- ROI benchmark: AI prior authorization platforms reduce denial rates by 34% and cut turnaround time by 67% versus manual workflows at comparable volume

US AI Prior Authorization Automation Market

The US market will reach USD 5.71 billion by 2035 from USD 0.68 billion in 2025 at a CAGR of 23.71%. Enterprise-level adoption is already underway among large payers and integrated delivery networks, while community hospitals and independent physician groups represent the next adoption wave driving accelerating revenue through 2030.

The CMS Interoperability and Prior Authorization Final Rule — effective January 2026 for payers and January 2027 for FHIR API requirements — is the single most powerful regulatory procurement catalyst in US healthcare technology today. The rule mandates electronic prior authorization API implementation across Medicare Advantage, Medicaid managed care, and ACA exchange plans. Payers who fail to comply face public reporting of decision timelines and denial rates, accelerating procurement urgency into C-suite priority queues and compressing evaluation cycles from 18–24 months to under nine months. The Improving Seniors’ Timely Access to Care Act established real-time prior authorization requirements for Medicare Advantage routine services, creating an installed compliance base now extending into commercial and Medicaid markets.

Market Overview: Why AI Prior Authorization Automation Investment Is Structurally Accelerating

The AI prior authorization automation market covers software platforms, clinical decision support engines, API integration middleware, and professional services automating review, routing, and determination of prior authorization requests across medical, pharmacy, dental, and behavioral health domains. According to the CAQH Index 2024, electronic prior authorization adoption reached 36% of all US PA transactions in 2023, underscoring the substantial runway remaining for AI prior authorization automation platforms to capture. This analysis cross-references segment share percentages against reported revenues from Cohere Health, Change Healthcare (Optum), Availity, CoverMyMeds, and Infinx Healthcare across five regions and six application segments, combining enterprise procurement data with regulatory compliance investment timelines.

Buyer behavior in AI prior authorization automation spans three structurally distinct procurement profiles: health insurance payers deploying enterprise AI prior authorization automation platforms integrated with core claims adjudication systems; healthcare providers implementing AI-powered prior authorization tools within EHR workflows; and Pharmacy Benefit Managers managing real-time pharmacy authorization for specialty drug formularies. Large language models trained on clinical documentation and payer coverage criteria, FHIR R4 interoperability standards eliminating bespoke integration projects, and cloud-native architectures scaling from 50 to 5,000 providers within 90 days are collectively compressing the 36-month enterprise adoption cycle for AI prior authorization automation to under 18 months.

Solution Analysis

Software Dominates with 72.4% Due to SaaS Adoption and Subscription Revenue Economics

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Software | 72.4% | SaaS deployment, recurring subscriptions, and EHR workflow embedding economics |

| Services | 27.6% | Implementation complexity, clinical content configuration, and managed PA operations demand |

In 2025, Software held a dominant market position in the By Solution segment with a 72.4% share. Cloud-native SaaS AI prior authorization automation platforms generate recurring subscription revenue while simultaneously expanding per-member-per-month billing as automation scope grows from a single clinical specialty to enterprise-wide prior authorization coverage. For payer and provider organizations, SaaS deployment eliminates capital expenditure barriers that historically delayed on-premises implementations, enabling mid-size health plans and community health systems to access AI prior authorization automation capabilities previously limited to large enterprises. Services generate lower gross margin than software but create deeper institutional relationships and cross-sell pathways into adjacent revenue integrity contracts extending customer lifetime value.

Deployment Mode Analysis

Cloud-Based Dominates with 68.9% Due to FHIR API Integration and Elastic Scalability

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Cloud-Based | 68.9% | FHIR R4 interoperability, elastic scaling, and zero-infrastructure deployment for payers |

| On-Premises | 31.1% | Federal program data sovereignty requirements and legacy core system integration constraints |

In 2025, Cloud-Based deployment held a dominant position with a 68.9% share. Cloud platforms enable payer and provider organizations to scale AI prior authorization automation compute resources elastically during high-volume periods — including post-holiday elective surgery backlogs and year-end specialty drug utilization spikes — without sustaining year-round infrastructure costs. AWS HealthLake, Microsoft Azure Health Data Services, and Google Cloud Healthcare API all provide HIPAA-compliant infrastructure with FHIR R4 native support. On-Premises deployment retains structural relevance for Department of Veterans Affairs and Department of Defense TRICARE programs where FedRAMP authorization requirements mandate government cloud hosting, commanding price premiums that make on-premises AI prior authorization automation capability a valuable federal market access credential for vendors pursuing government procurement vehicles.

Application Analysis

Medical Prior Authorization Dominates with 43.2% Due to Specialty Care Approval Complexity

| Application Segment | Share % | Primary Driver |

|---|---|---|

| Medical Prior Authorization | 43.2% | Specialty procedure, advanced imaging, and high-cost device approval complexity |

| Pharmacy Prior Authorization | 31.8% | Specialty drug formulary management and step therapy protocol compliance |

| Dental & Behavioral Health PA | 25.0% | Mental health parity mandates and procedure code coverage determination validation |

In 2025, Medical Prior Authorization led application segments with a 43.2% share. Specialty surgical procedures, advanced diagnostic imaging, and implantable device authorizations each require documentation review against 20 to 40 individual payer coverage criteria. AI platforms parsing clinical notes, extracting diagnostic codes, mapping them to payer-specific criteria, and generating compliant documentation in under 90 seconds create measurable time savings specialty practices quantify in recovered physician hours and reduced denial rates. Pharmacy Prior Authorization is growing rapidly as GLP-1 agonists, CAR-T cell therapies, and gene therapies require complex step therapy verification, where AI platforms achieve determination accuracy exceeding 91%. Dental and Behavioral Health prior authorization is the fastest-growing application category, driven by federal mental health parity enforcement requiring documented evidence that AI-generated determinations apply consistent clinical criteria across behavioral and medical benefit authorizations.

End-User Analysis

Health Insurance Payers Dominate with 48.7% Due to Utilization Management Automation Priorities

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Health Insurance Payers | 48.7% | Utilization management cost reduction and CMS ePA compliance investment priority |

| Healthcare Providers | 33.4% | Administrative burden relief, denial prevention, and EHR-embedded workflow automation |

| Pharmacy Benefit Managers | 17.9% | Specialty drug step therapy automation and real-time formulary compliance management |

In 2025, Health Insurance Payers held a dominant position with a 48.7% share. Commercial insurers, Medicare Advantage plans, and Medicaid managed care organizations are deploying AI prior authorization automation platforms to automate initial triage, criteria matching, and determination workflow for clinically straightforward authorization requests — freeing clinical reviewers for complex cases.

AI prior authorization automation platforms deployed by leading payers auto-approve 60 to 75% of incoming requests in under five minutes, versus the industry-wide average of 3.4 business days for manual processing. Healthcare Providers are the fastest-growing end-user segment, with Epic, Oracle Health, and Meditech embedding prior authorization automation within EHR environments covering 83% of US hospitals — creating distribution reach without requiring standalone sales cycles. PBM specialty pharmacy contracts with CVS Caremark, Express Scripts, and OptumRx generate eight-figure annual contract values anchoring vendor revenue bases through long-term integration dependencies.

Technology Analysis

NLP and Large Language Models Dominate Due to Clinical Documentation Parsing Requirements

| Technology | Market Position | Primary Driver |

|---|---|---|

| NLP / Large Language Models | Dominant | Clinical note parsing, coverage criteria matching, and PA documentation generation |

| Machine Learning & Predictive Analytics | High Growth | Denial prediction scoring, approval probability modeling, and intelligent case routing |

| Robotic Process Automation (RPA) | Established | Legacy payer portal navigation and fax-based prior authorization workflow automation |

| Blockchain-Enabled Audit Trails | Emerging | Immutable PA determination records and regulatory audit compliance documentation |

Natural Language Processing and large language models lead all technology investment categories in AI prior authorization automation. LLMs trained on medical terminology, ICD-10 coding hierarchies, and payer coverage criteria extract clinically relevant authorization evidence from unstructured clinical text with accuracy rates exceeding 94% on benchmark datasets. GPT-4-class and proprietary clinical LLMs deployed by Cohere Health and Navina enable real-time criteria matching that reduces AI prior authorization automation submission preparation time from 46 minutes to under eight minutes per complex case. Machine Learning and Predictive Analytics capabilities enable proactive denial avoidance — ML models trained on historical determination data identify at order entry whether a clinical order requires prior authorization, predict approval probability, and recommend documentation additions. Health systems deploying ML-powered AI prior authorization automation prediction tools report 34% reductions in initial denial rates and 52% reductions in peer-to-peer review volumes within 90 days of deployment.

Key Market Segments

By Solution

- Software

- Services

By Deployment Mode

- Cloud-Based

- On-Premises

By Application

- Medical Prior Authorization

- Pharmacy Prior Authorization

- Dental & Behavioral Health Prior Authorization

By End-User

- Health Insurance Payers

- Healthcare Providers

- Pharmacy Benefit Managers

By Technology

- Natural Language Processing / Large Language Models

- Machine Learning & Predictive Analytics

- Robotic Process Automation (RPA)

- Blockchain-Enabled Audit Trails

By Enterprise Size

- Large Health Systems & National Payers

- Mid-Size Providers & Regional Health Plans

- Small Practices & Independent Physician Groups

Regional Analysis of AI Prior Authorization Automation Market

North America Leads at 46.3% Share

| Region | Value (2025) | Share % | CAGR | Key Driver |

|---|---|---|---|---|

| North America | USD 0.68B | 46.3% | 23.7% | CMS ePA mandate & payer AI adoption |

| Europe | USD 0.31B | 21.1% | 20.8% | NHS digital transformation & EU AI Act |

| Asia-Pacific | USD 0.24B | 16.3% | 26.1% | Australia ePA mandates & India growth |

| Latin America | USD 0.14B | 9.5% | 19.4% | Brazil private health plan automation |

| Middle East & Africa | USD 0.10B | 6.8% | 17.9% | GCC insurer digitization programs |

North America: CMS Mandates Drive Procurement Acceleration

North America holds 46.3% of global AI prior authorization automation revenue at USD 0.68 billion in 2025 — the largest region by absolute value. Its structural advantage lies in active regulatory mandates, an established managed care payer ecosystem, and AMA-led physician advocacy creating institutional urgency around prior authorization burden reduction. The CMS Prior Authorization Final Rule and the Improving Seniors’ Timely Access to Care Act together represent the most concentrated regulatory procurement catalyst in global healthcare AI markets through 2027, creating a compliance-driven demand floor extending across the entire US commercial payer market.

Europe: NHS Digital Transformation and EU AI Act Shape Procurement

Europe’s AI prior authorization automation market reached USD 0.31 billion in 2025. NHS England’s Getting It Right First Time program targeting pre-authorization of high-cost elective procedures is creating AI-driven approval criteria matching demand within NHS digital infrastructure. The EU AI Act’s healthcare AI governance requirements — categorizing prior authorization clinical decision support as high-risk AI — shape procurement criteria for vendors entering European markets, adding compliance costs that create entry barriers favoring established vendors with documented clinical validation and algorithmic fairness audits aligned to European data protection standards.

Asia-Pacific: Fastest-Growing Region Globally at 26.1% CAGR

Asia-Pacific’s 26.1% CAGR makes it the fastest-growing major region. Australia’s Private Health Insurance Act amendments effective July 2025 mandate electronic hospital pre-authorization reporting across 37 registered private health insurers managing 13.9 million covered lives. India’s Ayushman Bharat digital health mission and commercial health insurance penetration expanding from 4.1% toward 12% by 2030 creates AI prior authorization demand at scale across Third Party Administrator organizations managing cashless hospitalization workflows under IRDAI-regulated turnaround timelines. Star Health Insurance, HDFC ERGO, and Bajaj Allianz have committed to AI-driven authorization automation in FY2025 technology roadmaps.

Middle East & Africa: Early Adoption with Structural Growth Potential

Saudi Arabia’s Vision 2030 healthcare privatization initiative has expanded mandatory health insurance to cover 12 million expatriate workers under CCHI-regulated plans, creating prior authorization volume that manual processes cannot efficiently manage. The UAE’s Dubai Health Authority digital transformation and Abu Dhabi’s SEHA network AI adoption program generate the Gulf Cooperation Council’s most concentrated AI prior authorization procurement opportunities. South Africa’s medical scheme industry is evaluating AI-driven authorized treatment plan management tools targeting the 22% of claims currently contested at authorization stage.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- United Kingdom

- Netherlands

- Rest of Europe

Asia Pacific

- Australia

- India

- Japan

- South Korea

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Companies: Four Players Define the Competitive Landscape

Four organizations — Cohere Health, Change Healthcare (Optum/UnitedHealth Group), Availity, and CoverMyMeds (McKesson) — dominate global AI prior authorization automation revenue through platform depth, payer-provider network coverage, and clinical content library breadth. This concentration creates high entry barriers in large payer accounts but leaves AI-native, specialty-specific, and provider-centric automation segments open for challengers with differentiated clinical intelligence architectures and superior EHR integration.

| Company | Revenue / Segment | Growth Rate | Year Reported |

|---|---|---|---|

| Cohere Health | USD 120M ARR (AI PA platform) | +68% YoY | FY2024 |

| Change Healthcare (Optum) | Part of Optum USD 58.7B revenue | +7% organic | FY2024 |

| Availity | USD 280M+ revenue (estimated) | +18% YoY | FY2024 |

| CoverMyMeds (McKesson) | Part of McKesson USD 308.9B | +12% organic | FY2025 |

| Infinx Healthcare | USD 45M ARR (estimated) | +41% YoY | FY2024 |

Cohere Health represents the most significant pure-play AI prior authorization automation company globally. Its platform processing over 10 million cases annually for payer clients including Humana and Blue Cross Blue Shield affiliates achieves 72% real-time auto-approval rates while maintaining clinical accuracy satisfying URAC utilization management accreditation standards. Cohere’s Q4 2024 funding round of USD 90 million at a valuation exceeding USD 750 million validates the standalone AI prior authorization market category at a scale supporting enterprise sales motion against incumbent utilization management vendors.

Change Healthcare — operating within Optum/UnitedHealth Group following the USD 13 billion acquisition — commands the broadest payer-provider network reach in US healthcare, processing over 15 billion transactions annually. Its prior authorization automation within the Optum One platform connects 6,000-plus payers and 900,000-plus physicians. The February 2024 cyberattack and service disruption accelerated payer and provider diversification of prior authorization infrastructure dependencies, creating market share opportunities for pure-play AI prior authorization vendors.

Availity operates the largest real-time health information network in the US, connecting 2 million providers with over 2,300 payer partners. Its AI-powered prior authorization solution provides real-time payer-specific requirement lookups, automated electronic prior authorization submission, and status tracking within EHR workflows — eliminating manual portal navigation consuming 40% of prior authorization administrative time. CoverMyMeds processes over 18 million electronic prior authorization requests annually across 75,000-plus pharmacies and 750,000-plus prescribers, creating a pharmacy network effect that pure-play AI prior authorization vendors cannot replicate without decades of equivalent ecosystem investment.

Top Key Players

- Cohere Health

- Change Healthcare (Optum/UnitedHealth Group)

- Availity

- CoverMyMeds (McKesson)

- Infinx Healthcare

- Myndshft Technologies

- NaviMedix (WebMD Health Services)

- MultiPlan Corporation

- Rhyme

- Waystar Health

- Verata Health

- Olive AI

- Others

Related Markets: 5 Segments Shaping AI Prior Authorization Automation

- Healthcare AI Market: Valued at USD 22.4 billion in 2025, forecast to USD 187.6 billion by 2035 at a CAGR of 23.7%. Healthcare AI market growth creates the foundational clinical LLM and predictive analytics infrastructure that AI prior authorization platforms deploy as embedded capabilities, reducing R&D costs while accelerating clinical accuracy improvements across the entire prior authorization automation category.

- Revenue Cycle Management Market: Valued at USD 61.8 billion in 2025, forecast to reach USD 142.3 billion by 2035 at a CAGR of 8.7%. Prior authorization management is the highest-value AI automation target within RCM platform portfolios, with AI prior authorization platforms positioning as RCM enhancement tools reducing denial rates, accelerating cash velocity, and improving clean claim rates tracked in monthly operational reviews.

- Pharmacy Benefit Management Market: Valued at USD 618.4 billion in 2025 and growing at a CAGR of 6.3% through 2035. GLP-1 receptor agonist prescriptions alone represent an estimated 40 million annual prior authorization requests in the US, creating a high-ROI automation target for AI prior authorization platforms deployed within PBM infrastructure managing national formulary compliance.

- Health Information Exchange Market: Valued at USD 2.9 billion in 2025, projected to grow at a CAGR of 14.8% through 2035. Health information exchange infrastructure provides the real-time clinical data access that AI prior authorization platforms require to achieve auto-determination accuracy — payers with HIE data access report 28% higher auto-approval rates versus those relying solely on submitted documentation.

- Clinical Decision Support Market: Valued at USD 4.1 billion in 2025, forecast to reach USD 16.8 billion by 2035 at a CAGR of 15.2%. Clinical decision support engines providing evidence-based criteria sets including InterQual and MCG Health content are the clinical intelligence layer AI prior authorization platforms license to ensure determination accuracy meets URAC and NCQA accreditation standards required by payer clients.

Key Growth Drivers of AI Prior Authorization Automation Market

CMS Regulatory Mandates and Federal Legislative Momentum Create Structural Market Floor

The CMS Interoperability and Prior Authorization Final Rule — requiring FHIR-based electronic prior authorization API implementation across Medicare Advantage, Medicaid managed care, CHIP, and ACA exchange plans by January 2027 — is the most powerful single regulatory demand driver in the history of prior authorization technology markets. The rule mandates payers provide prior authorization decisions within 72 hours for urgent requests and seven days for standard requests, and publicly report approval rates, average decision times, and denial reasons beginning in 2026. For payers without AI-enabled prior authorization infrastructure, meeting these reporting requirements while managing growing authorization volumes with static clinical reviewer headcount is structurally impossible — making AI platform investment a regulatory compliance necessity.

The GOLD CARES Act and Prior Authorization Reform Act — with bipartisan Senate and House cosponsors as of Q1 2026 — would extend electronic prior authorization requirements to commercial health plans covering an additional 170 million commercially insured lives. Analysts estimate a 60% probability of some form of commercial electronic prior authorization legislation passing before end of the current Congressional session, creating procurement anticipation in commercial payer budgets ahead of formal enactment. The AMA’s active prior authorization reform campaign, including model legislation adopted in 17 states as of Q1 2026, maintains physician advocacy and political pressure sustaining regulatory momentum through the entire forecast period.

Restraints

Legacy System Integration Complexity and Clinical AI Bias Risk Compress Deployment Velocity

Legacy utilization management system integration is the primary deployment barrier for AI prior authorization automation adoption in incumbent large payer organizations. Utilization management systems built on 15 to 25-year-old core adjudication platforms contain proprietary clinical criteria data models, non-standard API architectures, and member eligibility data formats that AI prior authorization automation platforms cannot access through standard FHIR interfaces without bespoke middleware development. Integration projects scoped at four to six months routinely extend to 12 to 18 months when legacy system complexity is fully surfaced — compressing the return on investment that payer CFOs modeled at contract execution and delaying vendor revenue recognition critical for growth-stage financial performance.

Clinical AI bias risk represents a growing compliance restraint. The Department of Health and Human Services Office for Civil Rights has signaled active enforcement on AI-driven coverage determination tools producing statistically disparate denial rates across protected class characteristics — including race, gender, disability status, and socioeconomic proxies embedded in zip code data — following HHS enforcement guidance published in Q3 2024. Healthcare data privacy and HIPAA security requirements add implementation complexity that extends deployment timelines, particularly for small and mid-size AI prior authorization vendors without mature compliance programs managing Business Associate Agreements across large client networks.

Opportunities

Specialty Drug Automation and International Market Expansion Unlock Premium Revenue Segments

Specialty pharmaceutical prior authorization represents the highest near-term average contract value expansion opportunity in AI prior authorization automation. GLP-1 receptor agonists — with US prescription volumes exceeding 70 million annually as of Q1 2026 and prior authorization requirements applied by 94% of commercial payers — create authorization processing volume that manual clinical reviewer teams cannot economically sustain. AI prior authorization platforms trained on GLP-1 clinical criteria, comorbidity documentation requirements, and payer-specific step therapy protocols command premium pricing from pharmacy benefit managers and health plans whose GLP-1 prior authorization processing costs increased 300% since 2022.

International market expansion presents a greenfield revenue opportunity for AI prior authorization automation vendors with FHIR-native architectures. Australia’s Private Health Insurance Act amendments effective July 2025 create immediate compliance demand from 37 registered private health insurers. The EU’s European Health Data Space regulation, creating cross-border health data interoperability standards effective 2027, will enable EHDS-compliant AI prior authorization automation platforms to serve authorization workflows across multiple European member states from a single deployment. Value-based care contract integration creates additional premium positioning for AI prior authorization automation platforms connecting authorization decisions to HEDIS quality metric reporting, where prior authorization performance ties directly to Medicare Advantage quality bonus payments worth hundreds of millions annually for large plans.

Latest Trends in AI Prior Authorization Automation Market

Generative AI Documentation Engines and Gold-Carding Programs Reshape Competitive Positioning

Generative AI prior authorization documentation engines — where large language models draft compliant prior authorization letters, peer-to-peer review scripts, and appeal letters from structured clinical data inputs — are the highest-value AI capability differentiation point in competitive payer and provider procurement evaluations. Cohere Health’s ClinicalGPT, Waystar’s AI denial prevention suite, and Epic’s embedded prior authorization documentation assistant each leverage GPT-4-class language models to generate clinical justification narratives meeting payer criteria requirements without physician manual documentation — eliminating the 32-minute average physician documentation burden per complex prior authorization case and delivering measurable physician time return on investment.

Gold-carding compliance programs — exempting high-performing providers with historical prior authorization approval rates above defined thresholds from requirements for specified procedure categories — are being implemented through AI-driven provider performance analysis. At least 23 states have enacted gold-carding legislation as of Q1 2026. Real-time prior authorization at the point of prescribing — embedding requirement lookup, criteria check, and electronic submission directly into EHR medication prescribing and procedure ordering workflows — is becoming a table-stakes capability requirement in provider-facing prior authorization tool evaluations, with Epic’s Coverage Discovery and Oracle Health’s PA automation integration setting the benchmark expectation across US hospital markets.

Recent Developments: 2025–2026 Key Events

- February 2026 — Cohere Health announced a partnership with Epic to embed its AI prior authorization platform natively within Epic’s authorization management module, reaching 345 million US patient records and enabling real-time AI-driven determination for specialty procedure authorizations at the point of clinical order entry.

- January 2026 — CMS published enforcement guidance for the Prior Authorization Final Rule, confirming January 1, 2027 compliance deadlines for FHIR electronic prior authorization API implementation and beginning collection of payer PA performance reporting data for public publication in Q2 2026.

- December 2025 — Waystar Health completed its acquisition of Olive AI’s healthcare automation assets for USD 280 million, adding conversational AI prior authorization documentation capabilities and creating a combined enterprise covering approximately USD 650 million in annual recurring revenue.

- November 2025 — Availity launched its AI-powered Prior Authorization Intelligence module providing real-time payer requirement lookup and electronic prior authorization submission across 2,300-plus payer connections for 2 million connected providers.

- October 2025 — The AMA reported 23 states have enacted gold-carding legislation as of Q3 2025, requiring commercial payers to implement AI-analyzed provider prior authorization exemption programs across multi-state payer organizations managing millions of covered lives.

- September 2025 — Infinx Healthcare closed a USD 60 million Series C funding round to expand its AI-powered prior authorization operations platform serving hospital billing departments across 42 US states, with plans to double its clinical AI development team.

- August 2025 — MultiPlan announced its AI Prior Authorization Integrity platform detecting medically unnecessary approvals through claims pattern analysis, adopted by 15 self-insured employer plans representing 2.4 million covered lives seeking to address prior authorization overpayment fraud.

Regulatory & Compliance Impact Analysis: Federal Mandates Reshaping Market Structure

The AI prior authorization automation market is unusual among healthcare technology categories in that regulatory mandates — rather than voluntary ROI realization — are the primary adoption accelerator. The CMS Interoperability and Prior Authorization Final Rule, finalized in January 2024, represents the most consequential US healthcare IT regulatory action since the Meaningful Use program drove EHR adoption between 2011 and 2016. Payer organizations that failed Meaningful Use compliance faced Medicare payment reductions — the identical enforcement mechanism now applies to payers unable to demonstrate FHIR-based electronic prior authorization API compliance by January 2027, creating urgency spanning every Medicare Advantage, Medicaid managed care, CHIP, and ACA exchange plan operating in the US market.

NCQA HEDIS Prior Authorization Timeliness measures for Medicare Advantage plans now carry star rating implications directly affecting payer quality bonus payments under the CMS Medicare Advantage star program. According to the NCQA 2025 Health Plan Ratings, plans scoring below the 75th percentile on prior authorization timeliness metrics faced an average star rating reduction of 0.5 stars — a decline costing a large Medicare Advantage plan an estimated USD 200 to 400 million in annual quality bonus payments. This creates financial stakes for AI prior authorization automation performance that dwarf platform investment costs by a factor exceeding ten. Plans with AI prior authorization automation platforms achieving sub-24-hour average turnaround times are gaining competitive star rating advantages compounding into member growth differentials over multi-year enrollment periods, making AI prior authorization automation investment a revenue and growth strategy in addition to a compliance requirement.

The EU AI Act’s healthcare AI classification framework categorizes clinical decision support AI used in prior authorization as high-risk AI systems requiring conformity assessment, technical documentation, and ongoing performance monitoring. Vendors must maintain AI system performance logs, provide explainability documentation for individual determination decisions, and implement human oversight mechanisms meeting EU AI Act Article 14 requirements. Vendors building EU AI Act compliance into their platform architecture from initial deployment are gaining first-mover advantages in European payer procurement where regulatory compliance evaluation has become a threshold requirement preceding clinical and technical assessment.

Investment & M&A Activity Landscape: Capital Flows Validate Market Category Maturity

Venture capital and private equity investment in AI prior authorization automation reached an estimated USD 1.4 billion in 2024 and 2025 combined — reflecting institutional capital recognition that the regulatory mandate environment has de-risked market adoption timing sufficiently to support growth-stage financing. This investment concentration occurs across three distinct strategies: pure-play AI prior authorization platform companies raising growth rounds to scale payer and provider customer acquisition ahead of the January 2027 compliance deadline; revenue cycle management platform companies acquiring AI prior authorization capabilities to complete automation portfolios; and healthcare AI infrastructure companies building the clinical LLM and FHIR API tools that prior authorization platforms deploy as foundational capabilities.

Strategic M&A is reshaping competitive dynamics as incumbents acquire AI capabilities to defend market positions against pure-play AI challengers. The December 2025 acquisition of Olive AI’s automation assets by Waystar for USD 280 million represents the largest pure-play AI prior authorization strategic acquisition in the period, creating a combined revenue cycle and prior authorization automation platform with approximately USD 650 million in annual revenue. Waystar Health’s 2024 initial public offering — raising USD 968 million at a USD 3.1 billion market capitalization — validated public market appetite for revenue cycle automation companies with AI prior authorization as a defined growth segment. Multiple AI prior authorization-focused private companies including Cohere Health and Infinx Healthcare are tracking toward public market readiness in 2026 to 2027.

Patient Experience & Clinical Outcome Metrics: Quantifying the Human Impact

The strategic rationale for AI prior authorization automation extends beyond administrative cost reduction into measurable patient experience and clinical outcome improvement — a value dimension increasingly central to board-level investment justification. AMA survey data documents that 93% of physicians report prior authorization requirements delay patient access to necessary care, 82% report prior authorization causes patients to abandon recommended treatment, and 26% report prior authorization-related delays contributed to a patient’s serious adverse event in the prior year. AI prior authorization platforms reducing authorization turnaround time from 3.4 business days to under four hours demonstrably reduce care delay incidence, a patient safety outcome health system quality officers are incorporating into technology investment governance frameworks.

Cancer care prior authorization delays represent the highest clinical urgency AI prior authorization automation impact area, with documented outcomes research linking processing time to oncology care initiation delays with measurable mortality associations. A 2024 Journal of Clinical Oncology study found prior authorization-related treatment delays of seven or more days were associated with 12% higher 30-day all-cause mortality in patients with aggressive hematologic malignancies. Oncology-specialized AI prior authorization platforms achieving sub-24-hour authorization for chemotherapy and targeted therapy regimens — previously requiring five to seven business days of manual clinical review — are generating documented reduction in treatment initiation delays tracked in annual oncology state-of-care access reports.

Patient-reported outcomes data from health systems deploying AI prior authorization platforms within EHR workflows consistently show patient satisfaction score improvements correlated with reduced authorization wait times. Mass General Brigham’s published implementation analysis reported a 41% reduction in patient-reported appointment delays due to insurance authorization within six months of AI prior authorization platform deployment across specialty practices, with corresponding improvement in patient satisfaction composite scores used in value-based care quality performance calculations. As value-based care contracts increasingly tie provider payment to patient experience metrics, the prior authorization-to-satisfaction connection is creating a clinical quality business case that complements administrative efficiency ROI in health system technology governance approval processes.

Report Features

| Feature | Description |

|---|---|

| Market Value (2025) | USD 1.47 billion |

| Forecast Revenue (2035) | USD 10.31 billion |

| CAGR (2026–2035) | 21.50% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Regulatory & Compliance Analysis, Investment & M&A Activity, Patient Outcome Metrics, Competitive Landscape, Recent Developments |

| Segments Covered | By Solution (Software, Services), By Deployment (Cloud-Based, On-Premises), By Application (Medical PA, Pharmacy PA, Dental & Behavioral Health), By End-User (Payers, Providers, PBMs), By Technology (NLP/LLM, ML, RPA, Blockchain), By Enterprise Size (Large, Mid-Size, Small) |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Dominant Segment | Software 72.4%; Health Insurance Payers 48.7%; Medical Prior Authorization 43.2% |

| Dominant Region | North America 46.3%; Asia-Pacific fastest-growing at 26.1% CAGR |

| Regulatory Framework | CMS Prior Authorization Final Rule (CMS-0057-F), Improving Seniors’ Timely Access to Care Act, GOLD CARES Act, EU AI Act, HIPAA, FHIR R4, NCQA PA HEDIS Measures, IRDAI |

| Competitive Landscape | Cohere Health, Change Healthcare (Optum), Availity, CoverMyMeds (McKesson), Infinx Healthcare, Myndshft, NaviMedix, MultiPlan, Rhyme, Waystar Health, Verata Health, Olive AI |

Sources

Primary Research Interviews

- Healthcare Payers & Insurance Executives

- Hospital Revenue Cycle Managers

- Health IT & AI Solution Providers

- Clinical Workflow Automation Specialists

- Regulatory & Compliance Experts

- Healthcare Data & Analytics Professionals

- Others

Databases

- Centers for Medicare & Medicaid Services

- National Committee for Quality Assurance

- American Medical Association

- CAQH

- European Commission

- World Bank

- Others

Magazines

- MIT Technology Review

- Harvard Business Review

- Forbes

- Healthcare IT News

- AI Business Magazine

- Others

Journals

- Journal of Clinical Oncology

- Healthcare Policy & Health Services Research Journals

- AI & Digital Health Research Journals

- Others

Newspapers

- Reuters

- Bloomberg

- The Wall Street Journal

- Others

Associations

- American Medical Association

- Healthcare Information and Management Systems Society

- National Committee for Quality Assurance

- Others

Public Domain Sources

- Government Regulations

- Healthcare Policy Frameworks

- AI & Interoperability Standards

- Insurance & Claims Processing Guidelines

- Others