What is the Biodegradable Polymers Market Size?

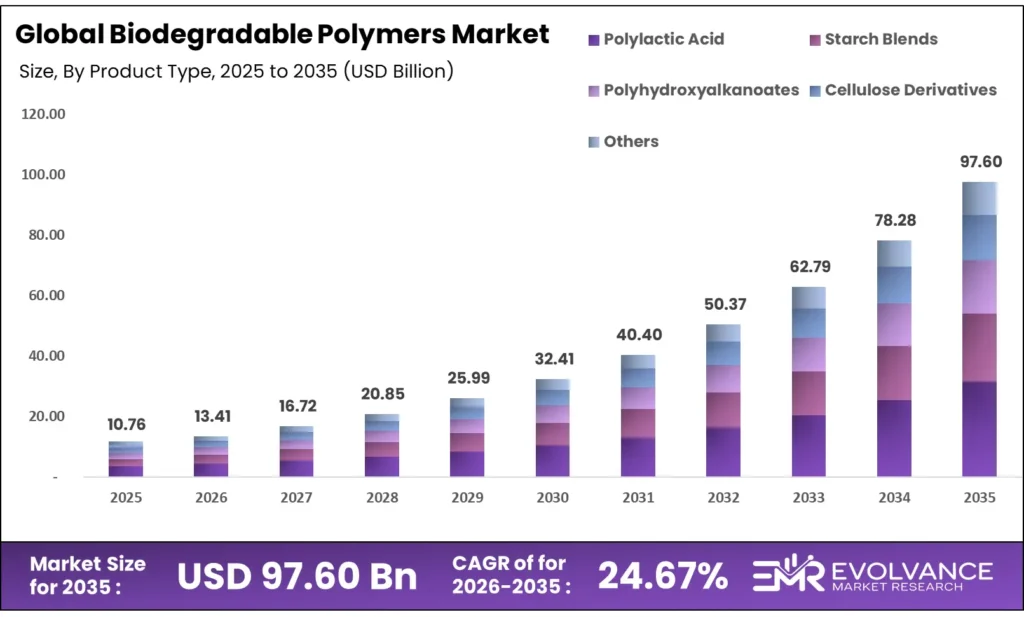

The Global Biodegradable Polymers Market size will be worth around USD 97.60 Billion by 2035 from USD 10.76 Billion in 2025, growing at a CAGR of 24.67% during the forecast period 2026 to 2035. Packaging mandates under the EU Packaging and Packaging Waste Regulation are forcing brand owners to replace conventional plastics in food-contact applications. Buyers are shifting spend toward certified compostable grades rather than generic bio-based claims, raising the bar for polymer suppliers. New vertically integrated PLA plants in Thailand have added 150,000 tonnes per year of supply capacity, but industrial composting gaps still limit end-of-life scalability in many markets.

Market Highlights

- The Global Biodegradable Polymers Market valued at USD 10.76 Billion in 2025, projected to reach USD 97.60 Billion by 2035 at a CAGR of 24.67%

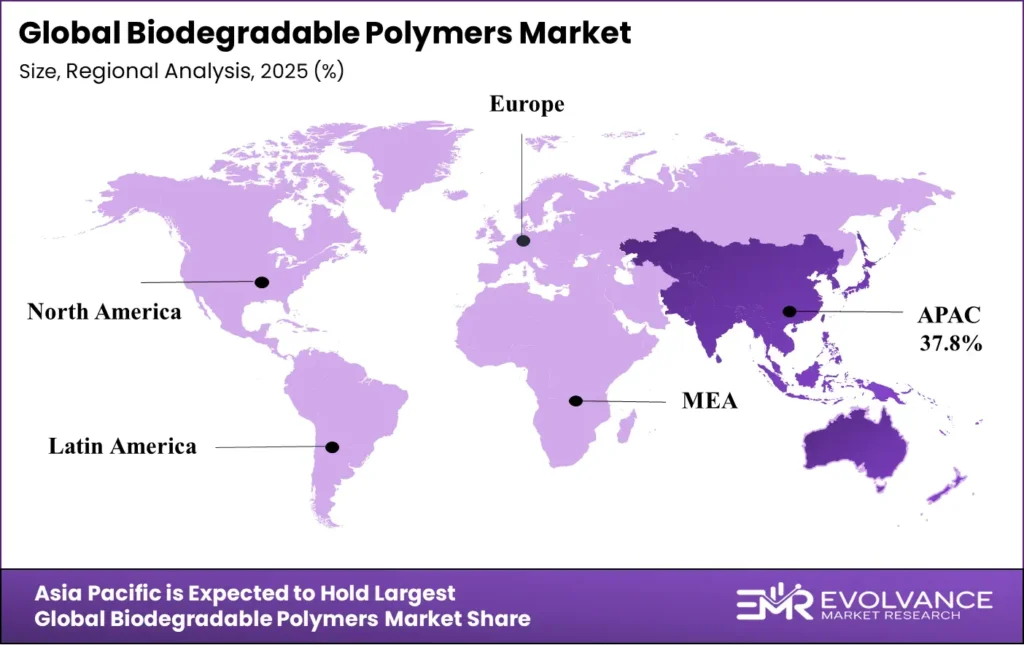

- Asia-Pacific leads with 37.8% market share, valued at USD 4.06 Billion in 2025

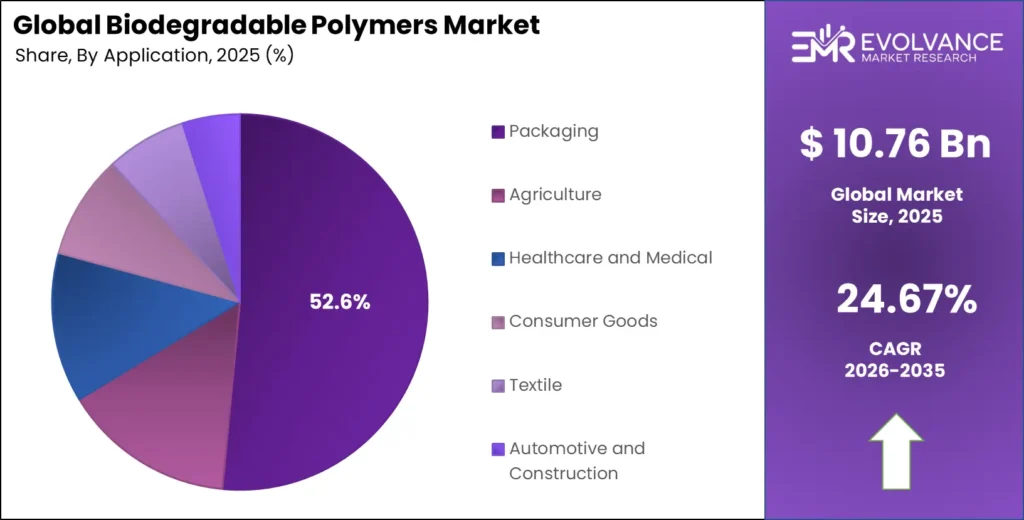

- Packaging is the dominant application segment with 52.6% share.

- Polylactic Acid (PLA) leads by product type with 37.2% share

Market Overview

Biodegradable polymers are materials that break down through biological processes into water, carbon dioxide, and biomass under specific conditions. These include PLA, starch blends, PHA, PBAT, PBS, PCL, and cellulose-based grades, each suited to different end-use needs. Packaging, agriculture, and healthcare drive the bulk of demand globally.

The shift from general “bio-based” claims toward certified compostable materials is reshaping procurement. Brands now require ASTM D6400 or EN 13432 certification before committing to long-term supply contracts. This certification-first approach is filtering out low-quality suppliers and creating structural advantage for producers with verified grades. Loop Industries and Ester Industries announced a joint venture investment of approximately US$165 million to build an Infinite Loop facility in India producing recycled specialty polymers from polyester waste.

Government policy is a core growth engine in this market. The EU Packaging and Packaging Waste Regulation mandates stricter recyclability and waste-reduction targets through 2030, directly pushing industrial buyers toward certified compostable food-contact packaging. Thailand’s Bio-Circular-Green policy and a record 12.6 billion baht financing package for biopolymer production are making Asia-Pacific a primary investment destination for new capacity.

Biodegradable PLA polymers were expanding at annual growth rates of 10% to 15% through 2025, supported by rising food packaging, textile, and 3D-printing demand. This rate signals that buyer adoption is outpacing historical projections, creating a narrow window for producers who can ship certified grades at scale to lock in long-term supply agreements.

The commissioning of its 75,000 tonne per year Thailand facility pushed global PLA production capacity to approximately 240,000 tonnes annually — a near 50% increase in global supply. This capacity jump matters because it reduces the supply risk premium that has historically inflated PLA contract prices, making biodegradable grades more cost-competitive against conventional plastics in volume packaging.

Product Type Insights

Polylactic Acid (PLA) dominates with 37.2% due to scalable production and broad packaging compatibility.

In 2025, Polylactic Acid (PLA) held a dominant market position in the By Product Type segment of the Biodegradable Polymers Market, with a 37.2% share. PLA’s lead reflects its position as the only biodegradable polymer with vertically integrated production at commercial scale. NatureWorks and TotalEnergies Corbion together built 150,000 tonnes per year of PLA capacity in Thailand, covering lactic acid, lactide, and polymer production within single facilities — a cost structure competitors in fragmented product types cannot match.

Starch Blends serve price-sensitive packaging and agricultural film applications where material cost outweighs performance requirements. These grades compete on raw material cost using locally sourced starch feedstocks, making them the default choice in emerging markets where certified compostability is less enforced. However, tightening EU sustainability rules are eroding cost-only procurement rationale and driving buyers toward certified grades.

Polyhydroxyalkanoates (PHA) attract interest in applications demanding marine biodegradability, where PLA and starch blends do not perform. Brands targeting plastic-free ocean claims have begun specifying PHA in rigid packaging and coatings. Production costs remain above PLA, limiting broad adoption, but premium foodservice and cosmetic packaging segments are absorbing that cost differential today.

PBAT (Polybutylene Adipate Terephthalate) functions primarily as a flex-film modifier blended with PLA or starch to improve tear resistance and processability. Its role as an enabling additive rather than a standalone resin makes it structurally dependent on PLA demand growth — as certified flexible film adoption accelerates in frozen food and bakery packaging, PBAT volumes follow.

PBS (Polybutylene Succinate) targets compostable foam and rigid packaging applications where PLA’s brittleness limits performance. PBS grades are gaining traction in agricultural mulch films requiring controlled degradation timelines, a segment not well served by PLA-only formulations.

PCL (Polycaprolactone) is used in specialty medical and slow-release agricultural coating applications where controlled degradation rates over months or years are required. Commercial volumes remain small relative to PLA, but the medical device pipeline provides a stable, high-margin demand base.

Application Insights

Packaging dominates with 52.6% due to regulatory mandates and brand-level sustainability commitments.

In 2025, Packaging held a dominant market position in the By Application segment of the Biodegradable Polymers Market, with a 52.6% share. Packaging’s share reflects the direct impact of mandatory legislation rather than voluntary adoption. The EU Packaging and Packaging Waste Regulation is forcing food-contact packaging buyers to qualify compostable polymer alternatives before 2030 deadlines, producing a wave of supplier qualification activity that benefits certified PLA and PBAT-blend suppliers most.

Agriculture applications include compostable mulch films, slow-release coatings, and seedling containers designed to eliminate film recovery costs after harvest. This segment benefits from growing farmer and distributor awareness that conventional plastic film recovery rates in field conditions are below 50% in most markets, making biodegradable alternatives an operational solution rather than just an environmental one.

Healthcare and Medical applications use biodegradable polymers in sutures, drug delivery systems, implantable scaffolds, and sterile packaging. This segment grows independently of packaging regulation, driven by clinical outcomes data supporting biodegradable medical devices. Procurement cycles are long, but once a material is qualified, switching costs are high — creating durable revenue streams for certified medical-grade suppliers.

Market Segments Covered in the Report

By Product Type

- Polylactic Acid (PLA)

- Starch Blends

- Polyhydroxyalkanoates (PHA)

- PBAT (Polybutylene Adipate Terephthalate)

- PBS (Polybutylene Succinate)

- PCL (Polycaprolactone)

- Cellulose Derivatives

- Others

By Application

- Packaging

- Agriculture

- Healthcare and Medical

- Consumer Goods

- Textile

- Automotive and Construction

Regional Insights

Asia-Pacific Dominates the Biodegradable Polymers Market with a Market Share of 37.8%, Valued at USD 4.06 Billion

Asia-Pacific holds 37.8% share, worth USD 4.06 Billion in 2025, anchored by Thailand’s emergence as a global PLA manufacturing hub. NatureWorks and TotalEnergies Corbion together established 150,000 tonnes per year of integrated PLA capacity in Thailand, backed by Board of Investment approval and the BCG bioeconomy policy. This combination of government support and private investment positions Asia-Pacific as the dominant supply-and-demand center for biodegradable polymers through 2035.

North America Biodegradable Polymers Market Trends

North America benefits from mature foodservice and retail channels that are actively replacing petroleum-based single-use formats. NatureWorks’ Thailand facility was designed specifically to serve North American packaging and fiber demand at 75,000 tons per year. The commercial launch of compostable coffee pods compatible with North American production lines in April 2024 signals that certified biodegradable formats are moving from pilot to mainstream procurement in the region.

Europe Biodegradable Polymers Market Trends

Europe is the global policy driver for biodegradable polymer adoption. The EU Packaging and Packaging Waste Regulation mandates food-contact compostability and stricter recyclability targets through 2030, converting regulatory pressure into hard procurement deadlines. Investing over 100 million euros to build that capacity and serving certified compostable packaging demand under EN 13432 standards.

Latin America Biodegradable Polymers Market Trends

Latin America is an early-stage market where Brazil and Mexico show the highest near-term adoption potential. Brazil’s sugarcane ethanol infrastructure provides a natural feedstock base for bio-based polymer production, while Mexico’s proximity to North American supply chains reduces logistics barriers for certified biodegradable imports. Extended producer responsibility legislation in both countries is beginning to create compliance-driven demand for compostable packaging alternatives.

Middle East & Africa Biodegradable Polymers Market Trends

The Middle East and Africa remain a small but fast-shifting segment. GCC countries are actively drafting single-use plastic bans modeled on EU frameworks, creating advance procurement activity among regional foodservice operators. South Africa is piloting compostable packaging mandates for organized retail. Lack of industrial composting infrastructure remains the primary barrier preventing certified biodegradable packaging from scaling across both sub-regions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The EU Packaging and Packaging Waste Regulation (PPWR), advancing through the European Parliament since 2023 with binding targets effective through 2030, mandates strict recyclability and waste-reduction standards for all food-contact packaging sold in the EU. This regulation directly requires brand owners to qualify certified compostable formats, raising the compliance bar for polymer producers supplying European markets.

The European Commission’s Green Claims Directive, proposed in March 2023 and under active legislative review through 2025, restricts vague “biodegradable” and “compostable” product claims unless backed by verified third-party certification. This directive increases compliance costs for polymer producers but creates structural advantage for those already certified under EN 13432 or ASTM D6400 standards.

Industrial compostability standards — ASTM D6400 in North America and EN 13432 in Europe — require biodegradable polymers to degrade under sustained temperatures of 60 to 65 degrees Celsius at certified composting facilities. These technical thresholds are increasingly referenced in procurement contracts, making certification a minimum commercial requirement rather than a marketing differentiator in regulated markets.

Drivers

EU Packaging Mandates Force Industrial-Scale Compostable Polymer Adoption Before 2030 Deadlines

The EU Packaging and Packaging Waste Regulation is not a voluntary framework — it sets binding recyclability and waste-reduction targets that force food-contact packaging buyers to qualify certified compostable alternatives. Brand owners cannot miss these deadlines without regulatory exposure. This makes biodegradable polymer qualification a procurement priority rather than a sustainability preference across European supply chains.

The commercial impact is direct and measurable. NatureWorks and IMA launched industrial-scale compostable coffee pod solutions compatible with North American production lines in April 2024. This move shows that biodegradable packaging formats are converting at the production-line level — brand owners are not testing alternatives, they are replacing legacy formats at commercial scale, which pulls polymer volumes through the supply chain.

Moreover, the expansion of certified PFAS-free compostable food packaging requirements across North American and European foodservice sectors is opening a premium demand channel. Suppliers who hold both PFAS-free and compostability certifications simultaneously face less competition and command stronger contract terms. This dual-certification requirement is an entry barrier that benefits established producers with existing regulatory compliance programs.

Restraints

Missing Industrial Composting Infrastructure Breaks the End-of-Life Case for Biodegradable Polymers

The core commercial weakness of biodegradable polymers is not the material — it is the disposal system. PLA requires sustained temperatures of 60 to 65 degrees Celsius for hydrolysis before bacterial breakdown can occur. Most municipal waste systems cannot consistently provide these conditions. Without certified industrial composting access, certified compostable packaging ends up in landfill or incineration, removing the end-of-life benefit that justifies the price premium.

This infrastructure gap limits procurement willingness among cost-sensitive buyers who weigh the full lifecycle cost of biodegradable packaging. A procurement manager cannot justify a price premium for compostable grades if fewer than half of collection points in their distribution area can process the material correctly. Until composting networks expand, the addressable market remains confined to regions with mature organics recycling systems.

Additionally, tightening EU scrutiny over misleading “biodegradable” and “compostable” product claims under the Green Claims Directive increases legal and certification costs for all polymer producers. Smaller producers without dedicated regulatory compliance teams face disproportionate cost burdens, which may reduce competitive supply diversity and concentrate market share among larger certified producers. This compliance pressure is a barrier to entry that slows the pace of new producer qualification.

Growth Factors

Thailand’s PLA Manufacturing Hub and Government Bioeconomy Support Create Asia-Pacific Supply Anchors

The vertical integration model adopted by both producers in Thailand creates a cost and supply-chain resilience advantage that standalone polymer compounders cannot replicate. TotalEnergies Corbion expanded lactide monomer production capacity to 100,000 tonnes per year alongside its 75,000 tonne PLA facility at the same site. NatureWorks designed its Nakhon Sawan complex to combine lactic acid, lactide, and polymer production within a single footprint, reducing raw material cost volatility and import dependency.

Furthermore, industrial 3D-printing applications are creating a new high-margin demand channel for PLA biopolymers. TotalEnergies Corbion optimized Luminy PLA grades for extrusion, thermoforming, injection molding, fiber spinning, and 3D-printing processes — converting a single resin portfolio into a multi-sector revenue stream. As additive manufacturing ecosystems push bio-based feedstocks, PLA producers gain volume leverage across sectors beyond their core packaging base.

Emerging Trends

Measurable Compostability Certification Replaces “Biodegradable” Claims as the New Commercial Standard

The biodegradable polymers market is moving past marketing language and into technical compliance. Buyers now specify ASTM D6400 or EN 13432 certification rather than accepting generic biodegradable claims in supplier tenders. Novamont confirmed that all MATER-BI biodegradable polymer grades are certified under UNI EN 13432, and MATER-BI achieved renewable content levels of up to 100%, reflecting how leading producers are converting certification into commercial differentiation.

The shift toward end-of-life circularity is equally reshaping producer strategy. Major biopolymer manufacturers are prioritizing vertically integrated production models that combine feedstock, lactic acid, lactide, and polymer manufacturing in single facilities to reduce supply-chain risk. This model removes external input price volatility from the cost structure and gives integrated producers pricing flexibility that toll manufacturers cannot match.

TotalEnergies Corbion confirmed its Thailand plant uses locally sourced non-GMO sugarcane feedstock for high-heat PLA and PDLA grades. Rising adoption of sugarcane-derived and plant-based feedstocks is not only improving the carbon lifecycle profile of biodegradable polymers — it is enabling net-negative or carbon-neutral lifecycle claims that are becoming a procurement specification in European retail and foodservice tendering, creating a sustainability compliance threshold that differentiates certified bio-based producers from fossil-based competitors.

Key Companies Insights

BASF holds a broad biodegradable polymer portfolio anchored by its Ecoflex PBAT and Ecovio PLA-blend grades, which serve flexible film, mulch, and compostable packaging applications globally. BASF’s strength lies in formulation expertise — its ability to blend PBAT with PLA or starch at commercial scale gives converters a single-source supply of certified compostable flexible films. This positions BASF ahead of mono-material producers in flexible packaging markets where processability is a buyer requirement alongside compostability certification.

NatureWorks LLC is the world’s largest PLA biopolymer producer, with its fully integrated Ingeo manufacturing complex in Nakhon Sawan, Thailand designed to produce 75,000 tons per year of lactic acid, lactide, and PLA polymer from a single site. This vertical integration gives NatureWorks a structural cost and supply reliability advantage over producers dependent on purchased lactic acid. The Thailand facility positions NatureWorks to serve Asia-Pacific, European, and North American markets simultaneously from a single low-cost, government-supported production base.

Novamont S.p.A. built its MATER-BI franchise on certified compostability under European standards. Novamont’s ORIGO-BI renewable biopolyester capacity at Patrica stands at 100,000 tonnes per year, feeding MATER-BI compostable grades for organics recycling markets. Its deep institutional relationships with European composting networks and retail chains give Novamont a channel advantage that new entrants would need years to replicate.

Corbion operates its PLA business through its TotalEnergies Corbion joint venture, which runs the 75,000 tonne per year Luminy PLA facility in Rayong, Thailand — commissioned as the second-largest PLA plant in the world at startup. The joint venture expanded lactide capacity to 100,000 tonnes per year at the same complex, securing raw material supply independence. Corbion’s focus on high-heat PLA and PDLA grades from non-GMO sugarcane feedstock targets the premium food packaging and automotive trim segments, where standard PLA performance falls short and material qualification creates durable supplier stickiness.

Key Companies

- BASF

- Changsu

- Evonik Industries AG

- Corbion

- Biome Technologies

- Borealis Group

- Kaneka

- FKUR

- Danimer Scientific

- Polysciences

- Polysciences Inc

- TotalEnergies

- NatureWorks LLC

- NaturTec

- Novamont S.p.A.

- Jiangmen Xinshuo New Materials Co., Ltd

- Mitsubishi Chemical Group Corporation

Recent Development

- In October 2024, Birla Cellulose and Circ signed a long-term partnership under which Birla Cellulose may purchase up to 5,000 tons annually of Circ recycled pulp from its first commercial facility over five years.

- In March 2024, Dow and Procter & Gamble launched a joint development program for a proprietary recycling technology aimed at converting hard-to-recycle plastic waste into near-virgin recycled polyethylene with lower greenhouse gas emissions. Dow and Procter & Gamble entered into a global joint development agreement focused on dissolution-based plastic recycling technologies for polyethylene waste streams.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 10.76 Billion |

| Forecast Revenue (2035) | USD 97.60 Billion |

| CAGR (2026-2035) | 24.67% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Polylactic Acid (PLA), Starch Blends, Polyhydroxyalkanoates (PHA), PBAT, PBS, PCL, Cellulose Derivatives, Others), By Application (Packaging, Agriculture, Healthcare and Medical, Consumer Goods, Textile, Automotive and Construction) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | BASF, Changsu, Evonik Industries AG, Corbion, Biome Technologies, Borealis Group, Kaneka, FKUR, Danimer Scientific, Polysciences, Polysciences Inc, TotalEnergies, NatureWorks LLC, NaturTec, Novamont S.p.A., Jiangmen Xinshuo New Materials Co. Ltd, Mitsubishi Chemical Group Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |