Executive Summary

Quick Insight: The global AI-Powered Quality Inspection market is set to expand nearly 5× by 2035, driven by accelerating deployment of computer vision systems across automotive, electronics, semiconductor, pharmaceutical, and food processing industries worldwide. Manufacturers are replacing manual visual inspection with AI-driven automated systems that deliver sub-second defect detection at accuracy rates exceeding 99.7%, dramatically reducing costly downstream recalls and improving production yield economics across every major production vertical.

The global AI-Powered Quality Inspection market encompasses computer vision hardware, machine vision cameras, deep learning inference software, X-ray and CT inspection systems, robotic integration platforms, and cloud-connected quality analytics services enabling real-time defect detection, dimensional measurement, and surface anomaly classification across manufacturing lines. This report delivers a comprehensive analysis of market size, technology stack dynamics, deployment economics, end-use industry adoption benchmarks, and competitive intelligence for the 2026–2035 forecast period.

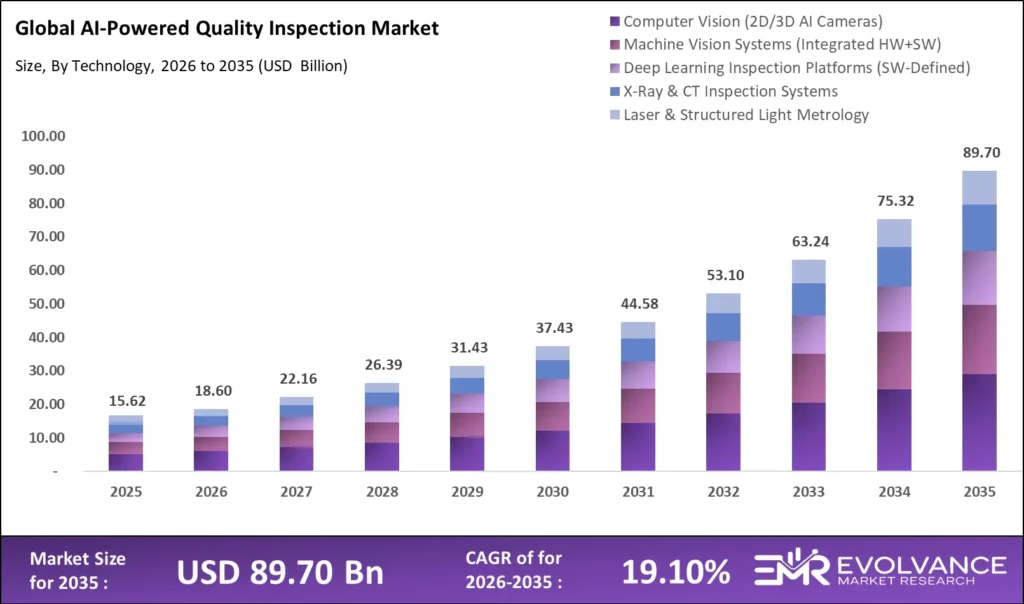

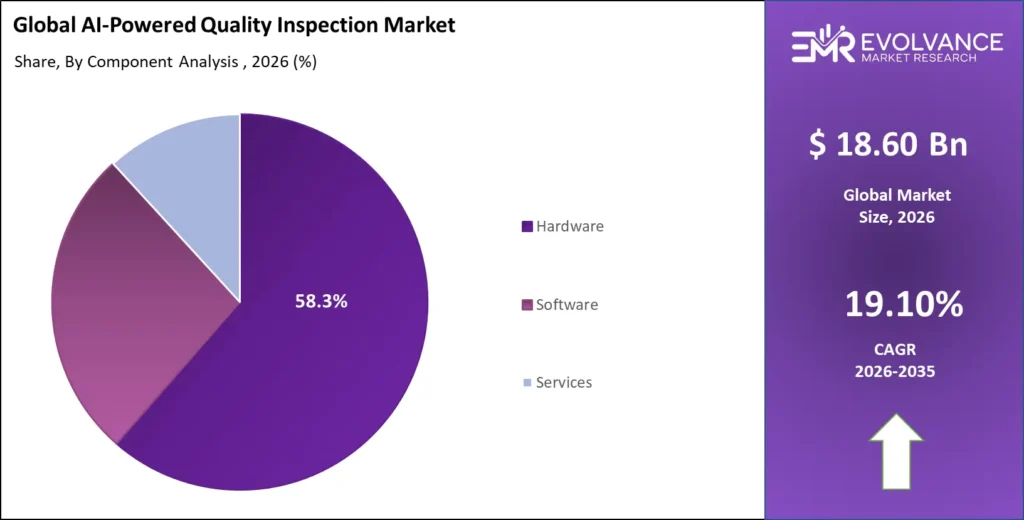

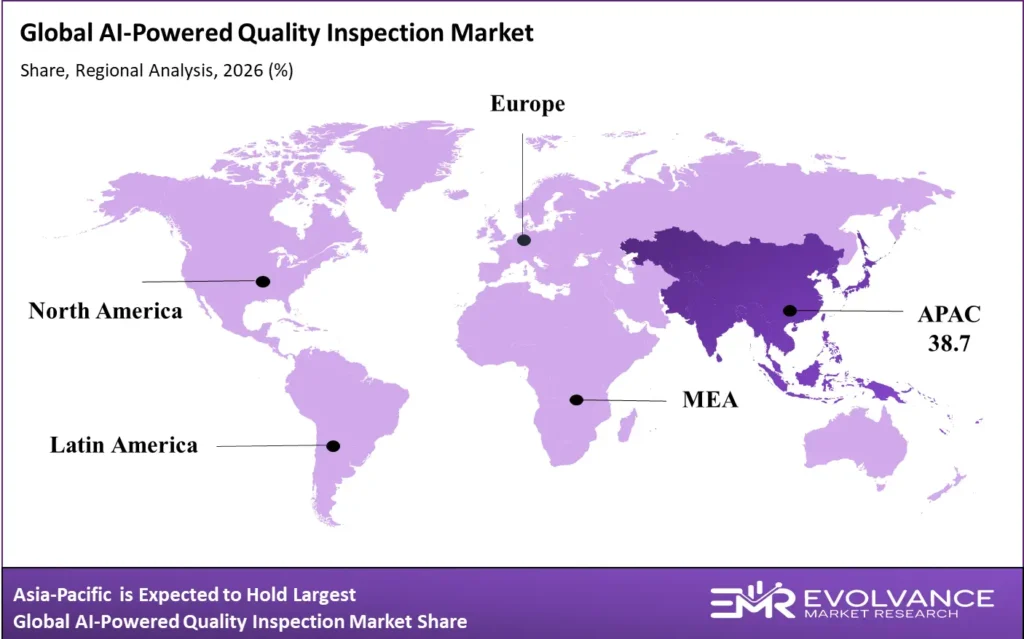

Key findings: The market reaches USD 18.60 billion in 2026 and compounds at 19.10% CAGR to USD 89.7 billion by 2035. Computer vision systems command 43.2% of total market revenue. Edge AI deployment is the fastest-growing mode at 34.8% CAGR. The automotive sector holds 24.6% end-use revenue share, while semiconductor inspection grows at 28.3% CAGR. Cognex Corporation and Keyence Corporation together account for approximately 29% of global hardware revenue. Three distinctive analytical frameworks — Smart Manufacturing Industry 4.0 Integration, AI Quality Inspection ROI Economics, and Edge AI Real-Time Defect Detection Architecture — provide actionable intelligence unavailable in comparable market research reports.

What Is the AI-Powered Quality Inspection Market?

The global AI-Powered Quality Inspection market was valued at USD 18.60 billion in 2026 and is projected to reach approximately USD 89.70 billion by 2035, growing at a CAGR of 19.10% during the forecast period. The integration of deep learning neural networks with high-speed industrial cameras, edge AI processors, and robotic inspection systems is the primary structural demand driver. Manufacturers across every major production vertical are discovering that AI inspection systems reduce quality escapes by 47% to 83% compared with statistical sampling approaches, justifying accelerated capital expenditure now embedded in multi-year smart factory investment programs.

The market encompasses deep learning-based visual inspection platforms, 2D and 3D machine vision cameras and lighting systems, AI inference accelerators for edge deployment, automated optical inspection (AOI) systems for printed circuit board manufacturing, X-ray and CT inspection for food and pharmaceutical quality assurance, laser profilometry for dimensional metrology, and cloud-connected quality management software platforms. It excludes standalone coordinate measuring machines (CMMs) where AI integration is not a primary system feature.

AI-Powered Quality Inspection Market Highlights: Key Data at a Glance

- Market value: USD 18.60 billion in 2026, forecast to USD 89.70 billion by 2035 at 19.10% CAGR

- Dominant technology: Computer Vision systems with 43.2% revenue share in 2026

- Dominant deployment mode: On-Premise industrial deployment with 52.4% revenue share in 2026

- Fastest-growing deployment: Edge AI inference at 34.8% CAGR through 2035

- Dominant end-use industry: Automotive manufacturing with 24.6% end-use revenue share

- Fastest-growing end-use: Semiconductor inspection at 28.3% CAGR through 2035

- Leading hardware vendor: Cognex Corporation with approximately 18% global machine vision camera market share

- AI defect detection accuracy: Best-in-class systems achieving 99.7%+ detection rates at under 5ms inference latency per frame

- Top inspection market geography: North America with 34.2% of global AI quality inspection revenue in 2026

- Inspection throughput advantage: AI systems process 400–1,200 units per minute versus 60–120 units per minute for skilled manual inspection

Market Overview: Why AI Quality Inspection Growth Is Accelerating

The AI-Powered Quality Inspection market is at a structural inflection point shaped by three simultaneous demand accelerators. The first is zero-defect manufacturing mandates from automotive OEMs, semiconductor foundries, and aerospace integrators. BMW, Toyota, and TSMC have declared zero-defect supplier quality objectives as core supply chain requirements for 2025 onward, making legacy sampling-based inspection processes contractually untenable and forcing tier-one and tier-two suppliers to transition to 100% inline AI inspection. Each supplier transition represents USD 2.4 million to USD 18 million capital deployment per production line.

The second accelerator is the labor economics transformation in manufacturing quality. The U.S. manufacturing sector reports 622,000 unfilled positions as of Q1 2026, with quality inspection roles among the hardest to staff. AI quality inspection systems eliminate dependency on expert human inspectors for repetitive visual tasks, eliminating inspector fatigue and inter-rater reliability problems that drive 12% to 31% false-rejection rates in manual quality control environments.

The third accelerator is the convergence of affordable AI hardware with proven inspection software platforms. NVIDIA’s Jetson Orin modules deliver 275 TOPS of AI inference at USD 499 unit cost. NVIDIA’s TAO toolkit, Cognex VisionPro Deep Learning, and Keyence’s AI vision platform have reduced inspection system development time from 18 months to 6 to 10 weeks, accelerating deployment cycles and expanding market penetration across mid-market manufacturers globally.

Technology Analysis

Computer Vision Commands 43.2% of AI Quality Inspection Revenue

Computer Vision, Machine Vision, Deep Learning & X-Ray/CT Inspection — Technology Revenue Breakdown 2026

| Technology Segment | Share % | CAGR | Primary Application |

|---|---|---|---|

| Computer Vision (2D/3D AI Cameras) | 43.2% | 18.6% | Surface defect detection, dimensional verification, OCR, label inspection, cosmetic quality |

| Machine Vision Systems (Integrated HW+SW) | 28.7% | 17.4% | Automotive body-in-white, PCB AOI, precision assembly verification, weld inspection |

| Deep Learning Inspection Platforms (SW-Defined) | 16.4% | 24.8% | Texture anomaly, multi-class defect classification, adaptive thresholding, few-shot learning |

| X-Ray & CT Inspection Systems | 7.9% | 21.3% | Internal void detection, pharma tablet inspection, food foreign body, EV battery cell |

| Laser & Structured Light Metrology | 3.8% | 16.2% | 3D dimensional measurement, weld seam profiling, surface roughness, gap-and-flush |

Computer Vision systems hold a 43.2% technology revenue share in 2026, driven by deployment of 2D line-scan and 3D area-scan cameras with NVIDIA GPU-accelerated inference. Cognex In-Sight 3800 and Keyence CV-X series are volume-shipping products, with global AI quality camera shipments reaching 4.2 million units in 2025, up from 1.8 million in 2022. The transition from rule-based blob analysis to CNN defect classifiers within existing hardware is driving a software-led upgrade cycle, improving detection sensitivity while extending hardware asset utilization life.

Deep Learning Inspection Platforms are the fastest-growing technology segment at 24.8% CAGR, as pretrained foundation models — Cognex ViDi, Landing AI LandingLens, MVTec Halcon — reduce training dataset requirements from thousands of labeled images to fewer than 50 examples per defect class. Software-defined inspection enables per-SKU model customization at scale, with subscription revenue streams estimated at USD 3.4 billion annually by 2028 at vendor gross margins above 72%.

X-Ray and CT Inspection systems are growing at 21.3% CAGR, driven by pharmaceutical serialization requirements, food safety foreign body detection mandates, and EV battery cell quality requirements. A single lithium-ion cell with an internal short-circuit defect can cause thermal runaway events generating liability exceeding USD 200 million per recall, driving 100% cell-level CT inspection mandates from BMW, Volkswagen Group, and Panasonic Energy, generating USD 1.8 billion in dedicated inspection equipment spend in 2026.

Component Analysis

Hardware Dominates with 58.3% Revenue Share; Software Is the Fastest-Growing Component

| Component | Share % | CAGR | Primary Driver |

|---|---|---|---|

| Hardware (Cameras, Sensors, AI Accelerators, Lighting, Optics) | 58.3% | 16.8% | Production line deployment, EV battery gigafactory CapEx, new semiconductor fab construction |

| Software (AI Inspection Platforms, Analytics, MES Integration) | 24.7% | 27.3% | Deep learning subscription revenue, defect analytics dashboards, cloud quality management platforms |

| Services (Integration, Training, Maintenance, Consulting) | 17.0% | 18.4% | System commissioning, custom model development, annual service contracts, model retraining |

Hardware holds a 58.3% component revenue share in 2026, reflecting the capital-intensive nature of industrial inspection system deployment. High-resolution line-scan cameras for flat panel display inspection cost USD 45,000 to USD 280,000 per unit, while a complete semiconductor wafer inspection cell reaches USD 2 million to USD 8 million per system. The expansion of EV battery manufacturing — with global gigafactory capacity projected to reach 6,200 GWh annually by 2030 — is generating particularly concentrated hardware inspection demand.

Software is the fastest-growing component segment, expanding at 27.3% CAGR through 2035. AI inspection software is transitioning from perpetual license to annual subscription pricing models, with vendors including Cognex, Landing AI, and Instrumental Inc. reporting 40% to 65% of new software revenue on subscription terms as of 2026. Manufacturers embedding AI inspection analytics into production control workflows generate data assets with five-to-seven year strategic value, sustaining software renewal rates above 92% annually for leading platform vendors.

Deployment Mode Analysis

On-Premise Leads with 52.4% Share; Edge AI Is the Fastest-Growing Deployment Mode at 34.8% CAGR

| Deployment Mode | Share % | CAGR | Primary Driver |

|---|---|---|---|

| On-Premise (Factory Floor Systems) | 52.4% | 16.8% | Real-time process control, data security, regulated industry compliance, sub-millisecond latency requirements |

| Edge AI (Embedded Inference at Machine) | 24.8% | 34.8% | NVIDIA Jetson Orin, Intel OpenVINO; autonomous robot vision; production bandwidth reduction |

| Cloud-Connected (Hybrid Inference+Analytics) | 15.3% | 22.4% | Multi-site quality analytics, centralized model governance, remote monitoring, MES integration |

| Fully Cloud (Off-Premise AI Inspection) | 7.5% | 19.1% | Batch offline inspection, archive analytics, SME AI inspection-as-a-service subscription adoption |

On-Premise deployment holds a 52.4% share in 2026 as the physics of high-speed production lines demand sub-millisecond inspection decision latency that cloud-routed inference cannot deliver. A bottling line operating at 1,200 containers per minute requires inspection decisions within 8 milliseconds to enable in-line ejection of defective units. Semiconductor fabs require continuous data throughput at 4 Gb/s to 40 Gb/s and processing cycles under 2 milliseconds per die, making on-premise GPU or FPGA-based AI inference mandatory.

Edge AI is the fastest-growing deployment mode at 34.8% CAGR through 2035. The commercialization of high-performance AI accelerator modules — NVIDIA Jetson AGX Orin at 275 TOPS, Hailo-8 at 26 TOPS, and Google Coral TPU at 4 TOPS — has made embedded AI inference viable at unit costs of USD 150 to USD 2,500 per inspection node. The total addressable market for edge AI inspection modules is projected to grow from USD 1.8 billion in 2026 to USD 18.4 billion by 2035 as the installed base of smart inspection nodes reaches 42 million units globally.

End-Use Industry Analysis

Automotive and Electronics Command Combined 45.3% of AI Quality Inspection Demand

Sector-by-Sector AI Inspection Spend Benchmarks, CAGR, and Primary Use Cases — 2026

| End-Use Industry | Share % | CAGR | Top Inspection Use Case |

|---|---|---|---|

| Automotive Manufacturing | 24.6% | 18.4% | Body-in-white, weld verification, EV battery cell inspection, paint surface, assembly compliance |

| Electronics & PCB Manufacturing | 20.7% | 19.8% | SMT solder joint AOI, BGA void inspection, display panel defect detection, component presence |

| Semiconductor & Wafer Fabrication | 13.4% | 28.3% | Wafer die inspection, reticle defect review, advanced node CD metrology, packaging alignment |

| Food & Beverage Processing | 11.8% | 17.6% | Foreign body detection, fill-level verification, label accuracy, packaging seal integrity |

| Pharmaceutical & Medical Devices | 10.6% | 21.4% | Tablet cosmetic defects, vial particulate inspection, sterile fill-finish, device assembly |

| Aerospace & Defense | 8.2% | 16.8% | Composite laminate void detection, turbine blade surface, NDT weld, structural bond inspection |

| Consumer Goods & Packaging | 6.4% | 15.3% | Print quality verification, dimensional compliance, surface cosmetic inspection, date code |

| Metals & Glass Manufacturing | 4.3% | 17.1% | Surface crack detection, thickness profiling, inclusion identification, edge quality |

Automotive holds the largest end-use revenue share at 24.6% in 2026. The EV transition generates a step-change in inspection capital expenditure: an ICE vehicle requires approximately 180 AI inspection checkpoints, while a BEV requires 340 to 420 incorporating battery cell, module, pack, high-voltage harness, and power electronics stages. BMW Group’s iFactory targets 100% AI inspection coverage across all lines by 2027 — a EUR 340 million investment.

Semiconductor inspection is the fastest-growing end-use at 28.3% CAGR as advanced node fabrication below 5nm requires defect detection capability at feature sizes where human inspection is physically impossible. KLA Corporation’s AI-enhanced Puma 9900 and Applied Materials are integrating AI process control with inspection feedback loops that compress yield learning cycles from 18 months to under 6 months at leading foundries. TSMC’s N3 and N2 process nodes require defect inspection sensitivity below 8nm.

Pharmaceutical and medical device inspection is expanding at 21.4% CAGR, driven by EU Annex 1 GMP mandating 100% container closure integrity testing for all parenteral products. A single contamination defect escaping inspection averages USD 380 million in recall remediation cost — a compelling ROI driver independent of capital budget cycles.

Regional Analysis of the Global AI-Powered Quality Inspection Market

Asia-Pacific Holds Largest Share; North America Leads Advanced Inspection Investment per Facility

| Region | Share % | CAGR | Key Driver |

|---|---|---|---|

| North America (U.S., Canada, Mexico) | 34.2% | 18.6% | Automotive reshoring, semiconductor fab investment, FDA compliance, EV battery gigafactories, CHIPS Act |

| Asia-Pacific (China, Japan, South Korea, Taiwan, India) | 38.7% | 22.4% | Semiconductor fab expansion, China EV production, electronics manufacturing scale, India PLI scheme |

| Europe (Germany, France, Italy, Netherlands, UK) | 19.4% | 16.8% | Automotive OEM zero-defect mandates, EU MDR medical device compliance, Industry 4.0 programs |

| Middle East & Africa (UAE, Saudi Arabia, Turkey) | 4.2% | 24.8% | Industrial diversification, pharma manufacturing expansion, food safety infrastructure modernization |

| Latin America (Brazil, Mexico, Argentina) | 3.5% | 19.3% | Nearshoring automotive production, food export quality compliance, electronics assembly growth |

Asia-Pacific holds a 38.7% global revenue share in 2026 — the largest regional share — growing at 22.4% CAGR. Taiwan’s semiconductor concentration generates the world’s highest per-facility AI inspection spend, with TSMC, UMC, and ASE Group collectively investing an estimated USD 4.8 billion annually in inspection and metrology. China’s domestic market, valued at USD 6.2 billion in 2026, is driven by smartphone electronics, automotive production at BYD, SAIC, and Geely, and food safety modernization.

North America is experiencing an AI inspection investment surge driven by manufacturing reshoring. The CHIPS and Science Act allocation of USD 52.7 billion for semiconductor manufacturing has triggered fab construction commitments from TSMC (USD 65 billion, Arizona), Samsung (USD 44 billion, Texas), and Intel (USD 100 billion, Ohio and Arizona). Automotive EV gigafactory construction is generating concentrated AI inspection capital demand projected at USD 2.1 billion through 2028 from battery and powertrain inspection systems alone.

Europe remains a technology leader in AI inspection system standards and automotive quality. Germany’s automotive OEM ecosystem represents the densest concentration of production-deployed AI inspection systems globally, with an estimated 12,400 AI inspection stations operating across German automotive facilities as of Q1 2026. The EU Medical Device Regulation (MDR) compliance deadline is driving accelerated AI inspection investment across European medical device manufacturers.

Key Companies: Vendors Defining the AI Quality Inspection Competitive Landscape

| Company | Segment | Key Differentiator | 2026 Market Position |

|---|---|---|---|

| Cognex Corporation | Machine Vision Systems | In-Sight 3800 + ViDi Deep Learning; 2,400+ direct sales globally; largest installed base | ~18% global camera market share; USD 1.04B revenue (2025) |

| Keyence Corporation | Vision Sensors & Systems | CV-X AI vision; XG-X series; direct sales dominance in Asia-Pacific manufacturing | Asia-Pacific leader; USD 7.4B total corporate revenue (2025) |

| KLA Corporation | Semiconductor Inspection | Puma 9900 AI wafer review; e-D7 eBeam; process control integration dominance | Dominant semiconductor inspection; USD 10.5B revenue FY2025 |

| Basler AG | Industrial Cameras | ace 2 Pro; Hailo-8L AI integration; European OEM camera standard for automotive | Strong EU automotive OEM; EUR 0.21B revenue (2025) |

| Teledyne DALSA | High-Speed Line Scan | Piranha4 series; semiconductor and print inspection specialization; TDI sensors | Semiconductor & print inspection leader |

| Landing AI | Deep Learning SW Platform | LandingLens low-shot learning; rapid deployment; USD 1.4B valuation post-Series C March 2026 | Fastest-growing AI-native inspection software vendor |

| Antares Vision Group | Pharma & Food Inspection | Track-and-trace; container closure integrity; serialization AI platform for Annex 1 | EU pharma Annex 1 compliance leader; EUR 0.22B revenue (2025) |

| SICK AG | Industrial Sensor & Vision | Inspector series; AI anomaly detection; safety-integrated inspection platforms | Strong EU and global industrial market; EUR 2.3B revenue (2025) |

| Hexagon AB | Metrology & 3D Inspection | AICON 3D; photogrammetry AI; smart factory metrology integration platform | Aerospace and automotive 3D metrology leader |

| NVIDIA (Metropolis) | AI Inference Platform | Metropolis Manufacturing Edition; Jetson Orin; Isaac robotics; TAO training toolkit | Cross-vendor AI backbone for quality inspection systems |

Cognex Corporation maintains the highest brand recognition in the global machine vision market through its In-Sight smart camera platform with ViDi deep learning pre-integrated and a 2,400+ direct sales force trained as application specialists. ViDi-enabled deployments achieve 40% to 70% faster implementation versus rule-based systems and command a 28% software premium. Cognex reported USD 1.04 billion in 2025 revenue, with semiconductor inspection recovery and EV battery inspection driving renewed growth.

KLA Corporation dominates semiconductor inspection as the undisputed revenue leader when semiconductor-specific systems are included. KLA’s Puma 9900 and e-D7 eBeam systems deploy AI-enhanced defect classifiers trained on billions of labeled die images across process nodes from 28nm to sub-2nm. KLA reported USD 10.5 billion in revenue for fiscal year 2025, with AI-powered inspection and metrology software representing an increasing share of service contract and upgrade revenue.

Key Growth Drivers of the AI Quality Inspection Market

Zero-Defect Mandates, EV Battery Production, Deep Learning Accessibility, and Regulatory Compliance Drive Structural Demand

EV battery manufacturing quality requirements are the single largest discrete demand catalyst for AI quality inspection through 2030. Global lithium-ion battery cell production capacity is projected to reach 6,200 GWh annually by 2030, up from approximately 1,400 GWh in 2025. Each gigawatt-hour of annual capacity requires USD 8 million to USD 14 million in AI inspection capital equipment. Total AI inspection spend attributable to EV battery manufacturing is projected to reach USD 12.4 billion annually by 2030.

Semiconductor advanced node transition is a compounding structural demand driver. As logic nodes progress from 3nm to 2nm and below, inspection steps required per wafer increase from approximately 180 at 28nm to 520 at 2nm. TSMC’s N2 node qualification requires an additional USD 3.2 billion in inspection and metrology tool procurement versus N3 tooling.

Labor shortage economics are converting AI inspection from capital investment to operational necessity. In North America, average hourly costs for skilled quality inspectors have risen from USD 18.40 in 2019 to USD 26.80 in 2026, with turnover averaging 34% annually. An automated AI inspection system amortized over 7 years costs USD 4.20 to USD 9.80 per operating hour — a 65% to 73% reduction versus skilled inspector labor costs including benefits, training, and supervisory overhead.

Market Restraints

Integration Complexity, Defect Dataset Scarcity, and CapEx Barriers Constrain Adoption Velocity

Integration complexity with legacy manufacturing execution systems is the primary near-term restraint. Most manufacturing facilities operate MES platforms implemented before 2018 without AI inspection data interfaces. Integrating AI inspection output requires custom middleware development averaging 4 to 8 months and USD 180,000 to USD 640,000 per facility, creating project risk that defers AI inspection investments.

Defect training dataset scarcity is a structural constraint for novel applications and new product introductions. Deep learning models require representative labeled examples of every defect class. For new product introductions, accumulating sufficient defect images before launch is often impossible — aerospace composite or specialty medical implant manufacturers may encounter critical defect types fewer than 10 times per year. While few-shot learning and synthetic data augmentation are reducing this constraint, dataset scarcity remains a meaningful barrier in low-volume, high-mix manufacturing environments.

Market Opportunities

Generative AI Synthetic Training Data, Inspection-as-a-Service, and Agricultural Quality AI Unlock Premium Growth Segments

Generative AI for synthetic defect training data is the most commercially significant emerging opportunity through 2028. Diffusion models and GAN-based synthesis generate photorealistic synthetic defect images — scratches, inclusions, delaminations, voids — enabling training datasets of 10,000 examples from as few as 5 to 20 real defect samples. NVIDIA Omniverse Replicator, Synthesis AI, and DataRobot are integrating with leading inspection platforms. Manufacturers deploying synthetic data report 35% to 55% reduction in new product inspection qualification time.

AI Inspection-as-a-Service is an underpenetrated opportunity targeting the USD 80 million-to-USD 2 billion revenue manufacturing segment. Cloud-managed AI inspection services reduce the adoption barrier from USD 350,000 to USD 2.4 million CapEx to USD 8,000 to USD 28,000 monthly OpEx, with vendors building subscription inspection businesses targeted at projected 38.4% CAGR through 2030.

Smart Manufacturing & Industry 4.0 Integration Framework

How AI Quality Inspection Integrates with Digital Twins, IIoT Platforms, and Closed-Loop Process Control

AI-powered quality inspection is evolving from a standalone defect detection tool into a foundational data layer within Industry 4.0 smart manufacturing architectures. Real-time inspection streams — defect type, location, severity, frequency, and upstream process correlations — create a new category of manufacturing intelligence driving closed-loop process optimization beyond the original quality assurance function.

Digital twin integration is the highest-value near-term deployment pattern. Siemens Xcelerator, PTC ThingWorx, and Dassault Systèmes 3DEXPERIENCE platforms are integrating AI inspection defect feeds with virtual production models, enabling real-time correlation of surface defect patterns with robot path deviations, tooling wear curves, and material batch variation signatures. A Tier-1 automotive supplier integrating AI inspection data with its Siemens digital twin achieved a 23% reduction in scrap rate within 90 days by identifying a correlation between weld spatter defect frequency and contact tip wear that manual quality review had failed to detect across three years of accumulated production data.

Closed-loop process control integration represents the frontier capability unlocking maximum economic value. Rather than inspecting outputs after production, closed-loop systems use real-time AI defect classification to automatically adjust upstream process parameters — laser power, robot speed, temperature, pressure, coating weight — before defects exceed specification limits. Robert Bosch has deployed closed-loop AI inspection control on its PowerCap ultracapacitor production line, reducing scrap rates by 41% and achieving process capability indices (Cpk) exceeding 1.67 across all critical characteristics. The integration requires OPC-UA protocol connectivity between the AI inspection platform and the process control PLC, natively supported by Cognex, Keyence, and SICK inspection systems as of 2025.

AI Quality Inspection ROI Economics Framework

Total Cost of Ownership, Payback Analysis, and Value Realization Benchmarks for 2026–2035

Total Cost of Ownership for a production-scale AI inspection system — comprising 4 to 8 AI cameras, edge computing infrastructure, inspection software licensing, integration services, and annual maintenance — ranges from USD 380,000 to USD 2.4 million for a single inspection station. Annual operating costs including software subscriptions, maintenance contracts, model retraining services, and power consumption typically represent 12% to 22% of initial capital expenditure. A complete 5-year TCO for a mid-complexity AI inspection deployment averages USD 620,000 to USD 3.8 million, compared with USD 480,000 to USD 2.1 million for equivalent manual inspection headcount — approaching cost parity before scrap reduction and warranty value capture are incorporated.

ROI payback timelines vary significantly by defect severity, production volume, and product value. High-volume automotive stamping lines achieve payback periods of 6 to 14 months when downstream warranty cost avoidance is included. Pharmaceutical fill-finish inspection systems typically deliver payback within 10 to 18 months. Food processing AI inspection for foreign body detection — where a single contamination recall can cost USD 60 million to USD 420 million — delivers immediate risk-adjusted ROI exceeding 800% in year one. Semiconductor wafer inspection systems deliver ROI measured in avoided yield loss: a 0.5 percentage point improvement in wafer yield at a 12-inch fab running 100,000 wafer starts per month generates USD 18 million to USD 42 million in annual incremental revenue.

Edge AI and Real-Time Defect Detection Architecture

NVIDIA Jetson, Intel OpenVINO, and Hailo-8 Define the Edge Inference Landscape for Smart Inspection 2026–2035

NVIDIA’s Jetson platform has become the reference architecture for high-performance edge AI inspection. The Jetson AGX Orin delivers 275 TOPS in a 30W TDP footprint, enabling simultaneous inference across 4 to 8 high-resolution camera streams at sub-5ms latency per frame. Cognex, Keyence, and SICK have introduced AI vision systems using Jetson Orin as the inference backbone with IP67 industrial enclosures, LED lighting, and deep learning model management. The TAO Transfer Learning Toolkit enables cloud-trained models to be compressed and deployed to edge nodes without accuracy degradation.

Intel’s OpenVINO toolkit enables edge AI inspection on heterogeneous CPU, GPU, FPGA, and VPU hardware, providing manufacturers with hardware flexibility that NVIDIA’s CUDA ecosystem does not offer. OpenVINO-optimized inspection models run on Intel 12th-generation Core processors with integrated Xe graphics at 40 to 90 TOPS — sufficient for 2-camera inspection cells operating below 400 units per minute.

Hailo-8 and Hailo-8L AI accelerators are emerging as cost-optimized edge inference solutions for volume deployment. At USD 149 for the Hailo-8L M.2 module delivering 13 TOPS, Hailo embeds AI inference in every camera at a cost previously achievable only through GPU server amortization. Hailo’s partnership with Basler, Allied Vision, and IDS Imaging is producing cameras with integrated Hailo accelerators — creating AI-native smart cameras that process inspection inference autonomously without external compute infrastructure.

Latest Trends in the AI Quality Inspection Market

Foundation Vision Models, Robotic Inspection Cells, Multimodal AI, and Generative Data Augmentation Reshape the Market in 2026

Foundation vision models adapted for industrial inspection are the defining technology trend of 2026. Meta’s Segment Anything Model (SAM) and Google’s Vision Transformer (ViT) architectures, fine-tuned on industrial defect datasets, are enabling zero-shot and few-shot inspection capabilities where models generalize to new defect types from fewer than 10 labeled examples. Landing AI’s LandingLens and Cognex’s ViDi Deep Learning are incorporating SAM-derived segmentation capabilities that automatically identify defect boundaries without manual polygon annotation — reducing labeling effort by 60% to 80% and accelerating new product inspection qualification from weeks to days. Foundation model-powered inspection is projected to represent 34% of all new inspection system deployments by 2028.

Collaborative robot integration with AI vision inspection is creating a category of flexible inspection cells. Universal Robots, FANUC, and KUKA are offering pre-integrated AI inspection cobot packages that reprogram for new parts in under 2 hours versus 3 to 6 weeks for dedicated fixed automation. The flexible AI inspection cobot market is estimated at USD 1.4 billion in 2026, growing to USD 12.8 billion by 2035.

Multimodal AI inspection combining visual, acoustic, and thermal sensing is the premium inspection paradigm for complex assemblies. A multimodal AI system deployed for lithium-ion battery cell inspection can detect electrolyte wetting defects through acoustic emission, tab weld voids through X-ray, electrode coating thickness variation through laser, and casing cosmetic defects through RGB vision in a single 12-second inspection cycle replacing five separate manual test stations.

Recent Developments: Key Industry Milestones 2025–2026

- April 2026: Cognex Corporation launched the In-Sight L38 Series featuring NVIDIA Jetson Orin NX embedded inference, achieving 12ms full-frame defect detection at 50 megapixel resolution — a 3× throughput improvement over the prior generation In-Sight 3800 at equivalent power consumption, targeting semiconductor and flat panel display inspection.

- March 2026: Landing AI raised USD 140 million in Series C funding led by Insight Partners and B Capital, reaching a USD 1.4 billion valuation, validating AI-native industrial inspection software as an independent commercial category distinct from traditional machine vision hardware-software bundles.

- February 2026: KLA Corporation announced the Puma 9900+ broadband plasma inspection system incorporating transformer-based AI defect classifiers achieving 22% improved sensitivity versus predecessor rule-based systems for EUV lithography defect detection at sub-10nm advanced logic nodes.

- January 2026: NVIDIA launched Metropolis for Smart Manufacturing — a pre-integrated AI inspection platform combining Jetson AGX Orin hardware, pretrained inspection foundation models, OPC-UA MES integration, and cloud quality analytics — available through Cognex, Keyence, and 14 additional ISV partners globally.

- November 2025: Antares Vision Group reported 34% revenue growth for Q3 2025, driven by pharmaceutical Annex 1 GMP compliance deadline deployments across 28 European fill-finish manufacturing facilities completing AI-enabled 100% container closure integrity testing installation programs.

- September 2025: Basler AG and Hailo Technologies announced a joint development agreement to produce AI-embedded smart cameras integrating Hailo-8L M.2 inference accelerators in Basler’s ace 2 Pro industrial camera line, targeting USD 149-per-node AI inspection deployments for small and medium enterprise manufacturers across Europe and North America.

Competitive Landscape

Hardware Consolidation at the Camera Layer, AI Software Fragmentation, and Vertical Integration Define Competitive Dynamics

The AI Quality Inspection competitive landscape features moderate hardware concentration — Cognex, Keyence, Teledyne DALSA, and Basler commanding approximately 58% of industrial camera revenue — combined with rapid AI software fragmentation as AI-native startups, traditional vision vendors, and hyperscaler platforms compete for the model development stack.

Vertical integration is the dominant competitive strategy among market leaders. Cognex’s ViDi deep learning platform generates recurring subscription revenue from the installed hardware base. KLA’s AI process control spans inspection tools, metrology, and yield management. NVIDIA’s Metropolis embeds Jetson hardware, TAO training, and cloud analytics in a single ecosystem creating switching costs of USD 180,000 to USD 1.2 million per station — sustaining customer retention above 91% annually for leading platform vendors.

AI-native challengers are disrupting traditional machine vision vendors at the software layer. Landing AI’s LandingLens has achieved deployments across 350+ manufacturers in 28 countries since 2021. Instrumental Inc. targets electronics manufacturing with an AI analytics platform that learns normal assembly appearance from production images without defect labeling — removing the dataset barrier for electronics OEMs deploying AI inspection across hundreds of product SKUs.

Key Market Segments

By Technology

- Computer Vision (2D & 3D AI Camera Systems)

- Machine Vision (Integrated Hardware & Software Platforms)

- Deep Learning Inspection Software (AI-Native Platforms)

- X-Ray & CT Inspection Systems

- Laser & Structured Light Metrology

By Component

- Hardware (Cameras, Sensors, AI Accelerators, Lighting, Optics)

- Software (AI Inspection Platforms, Quality Analytics, MES Integration)

- Services (System Integration, Custom Model Development, Maintenance, Retraining)

By Deployment Mode

- On-Premise (Factory Floor AI Inspection Systems)

- Edge AI (Embedded Smart Camera and Robot Vision Nodes)

- Cloud-Connected (Hybrid On-Premise and Cloud Analytics)

- Fully Cloud (AI Inspection-as-a-Service Subscription)

By End-Use Industry

- Automotive Manufacturing

- Electronics & PCB Manufacturing

- Semiconductor & Wafer Fabrication

- Food & Beverage Processing

- Pharmaceutical & Medical Devices

- Aerospace & Defense

- Consumer Goods & Packaging

- Metals & Glass Manufacturing

By Geography

- North America (U.S., Canada, Mexico)

- Asia-Pacific (China, Japan, South Korea, Taiwan, India, Australia)

- Europe (Germany, France, Italy, Netherlands, UK, Spain)

- Middle East & Africa (UAE, Saudi Arabia, Turkey, South Africa)

- Latin America (Brazil, Mexico, Argentina)

Report Features

| Feature | Description |

|---|---|

| Market Value (2026) | USD 18.60 billion |

| Forecast Revenue (2035) | USD 89.70 billion |

| CAGR (2026–2035) | 19.10% |

| Base Year for Estimation | 2026 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Technology Analysis, Component Breakdown, Deployment Mode Economics, Smart Manufacturing Integration Framework, AI Inspection ROI Economics, Edge AI Architecture Analysis, Competitive Intelligence, Regional Analysis with Country Data |

| Segments Covered | By Technology (5), By Component (3), By Deployment Mode (4), By End-Use Industry (8), By Geography (5 regions with country-level data) |

| Regional Analysis | North America, Asia-Pacific, Europe, Middle East & Africa, Latin America |

| Dominant Technology | Computer Vision Systems with 43.2% revenue share in 2026 |

| Fastest-Growing Segment | Edge AI Inference Deployment at 34.8% CAGR through 2035 |

| Dominant End-Use | Automotive Manufacturing with 24.6% end-use revenue share |

| Key Companies Profiled | Cognex, Keyence, KLA Corporation, Basler, Teledyne DALSA, Landing AI, Antares Vision, SICK AG, Hexagon, NVIDIA Metropolis |

| Unique Report Sections | Smart Manufacturing & Industry 4.0 Integration, AI Inspection ROI Economics Framework, Edge AI Architecture & Vendor Comparison, Synthetic Data Generation Opportunity Analysis |