Executive Summary

Quick Insight: The GLP-1 Weight Loss Drug Market is on track to more than double to USD 192 billion by 2035, driven by explosive patient demand for injectable and oral incretin therapies, multi-indication label expansion beyond obesity into cardiovascular protection and metabolic disease management, a robust late-stage pipeline of next-generation triple agonists, and unprecedented payer engagement transforming obesity into a fully reimbursable chronic disease requiring long-term pharmacological management.

The global GLP-1 Weight Loss Drug Market encompasses glucagon-like peptide-1 receptor agonists, dual GIP/GLP-1 agonists, and emerging triple-receptor agonists approved or in development for chronic weight management, type 2 diabetes remission, and metabolic disease intervention. This report delivers comprehensive analysis of GLP-1 market size, competitive dynamics, pipeline innovation, patient access economics, and population health outcomes for 2026–2035, covering leading molecules including semaglutide, tirzepatide, liraglutide, orforglipron, and retatrutide.

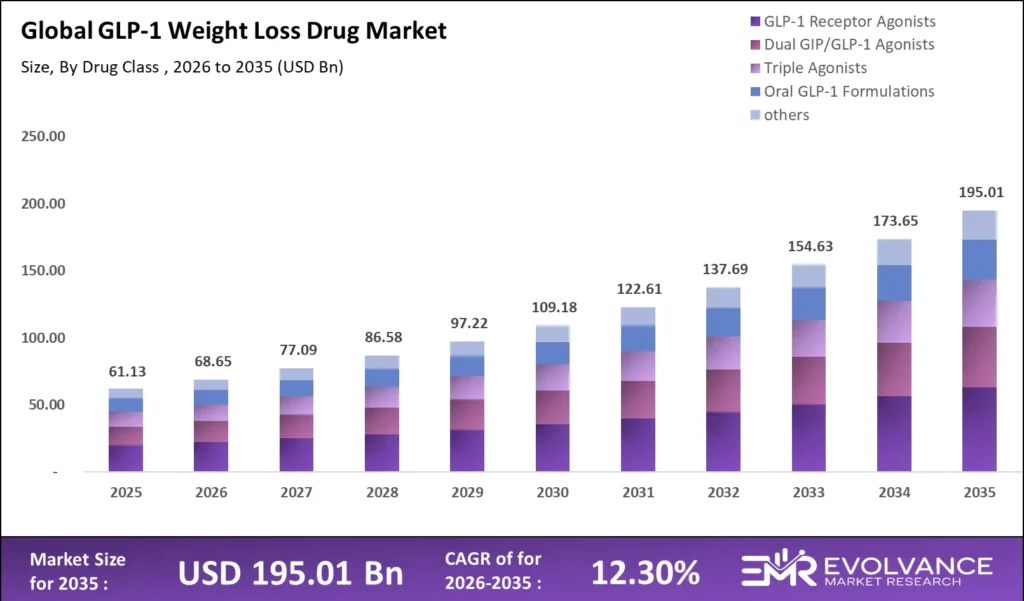

Key findings: The GLP-1 Weight Loss Drug Market reaches USD 68.65 billion in 2026 and compounds at 12.3% CAGR to USD 195.01 billion by 2035. Injectable GLP-1 and dual agonists command 78.4% of total drug revenue. Novo Nordisk and Eli Lilly control approximately 87% of prescription weight management drug revenue. Three exclusive sections — Patient Access Economics, Biosimilar Entry Framework, and Population Health ROI Framework — provide unique intelligence not available in comparable GLP-1 market reports.

What Is the GLP-1 Weight Loss Drug Market?

The global GLP-1 Weight Loss Drug Market was valued at USD 68.65 billion in 2026 and is projected to reach USD 195.01 billion by 2035, growing at a CAGR of 12.3% during the 2026–2035 forecast period. The SELECT trial establishing semaglutide’s 20% reduction in major adverse cardiovascular events has converted GLP-1 receptor agonists from single-indication obesity drugs into foundational chronic disease therapeutics demanding continuous prescription renewal.

The GLP-1 Weight Loss Drug Market encompasses semaglutide, tirzepatide, liraglutide, oral semaglutide, and orforglipron prescribed for body weight reduction and metabolic risk modification. It includes incretin-based therapies where primary clinical positioning centers on weight management and excludes GLP-1 drugs prescribed solely for glycemic control without a labeled obesity indication.

GLP-1 Market Size: USD 68.65 billion in 2026 | USD 195.01 billion by 2035 | CAGR: 12.3% | Leading Molecule: Semaglutide (52.1% revenue share) | Dominant Region: United States (62.8% revenue share)

GLP-1 Weight Loss Drug Market Highlights: Key Data at a Glance (2026)

- GLP-1 Weight Loss Drug Market Size 2026: USD 68.65 billion, forecast USD 195.01 billion by 2035 at 12.3% CAGR

- Dominant drug class: Dual GIP/GLP-1 Agonists (tirzepatide) and Injectable GLP-1 RA Monoagonists (semaglutide) with 78.4% combined revenue share

- Fastest-growing route: Oral GLP-1 formulations at 34.2% CAGR through 2035 driven by injection-free patient access expansion

- GLP-1 market leaders: Novo Nordisk and Eli Lilly with approximately 87% combined prescription weight management drug revenue share in 2026

- Most prescribed weight loss molecule: Semaglutide (Wegovy and Ozempic) with 52.1% global GLP-1 market revenue share in 2026

- FDA-approved anti-obesity GLP-1 drugs: Four molecules including semaglutide, tirzepatide, liraglutide, and oral semaglutide as of 2026

- Global obesity patient pool: More than 1.1 billion adults with obesity globally; GLP-1 drug penetration below 4% of eligible patients

- Top GLP-1 market: United States with 62.8% of global GLP-1 weight loss drug revenue

- Cardiovascular approval catalyst: Wegovy approved for MACE risk reduction following SELECT trial demonstrating 20% reduction in major adverse cardiovascular events

- Fastest-growing indication: Obstructive sleep apnea at 41.2% CAGR following Zepbound FDA approval November 2025

Market Overview: Why GLP-1 Weight Loss Drug Market Growth Is Accelerating

The GLP-1 Weight Loss Drug Market is at an unprecedented commercial inflection point defined by three simultaneous demand accelerators. The first is clinical evidence breadth expansion converting obesity pharmacotherapy from cosmetic to medical necessity. The SELECT trial demonstrated semaglutide reduces major adverse cardiovascular events by 20% in non-diabetic patients, repositioning GLP-1 drugs as disease-modifying therapies. The resulting payer policy cascade is converting an estimated 750 million previously untreated patients into commercially addressable prescription candidates.

The second accelerator is tirzepatide’s performance advantage crystallizing a new efficacy standard. Zepbound demonstrated 20.9% mean body weight reduction in SURMOUNT-1 at 15mg — surpassing semaglutide’s 15% benchmark and establishing dual GIP/GLP-1 agonism as the dominant next-generation obesity mechanism. IQVIA data confirms combined Zepbound and Wegovy new patient starts increased 34% year-over-year in 2025.

The third accelerator is the late-stage clinical pipeline delivering next-generation efficacy milestones. Retatrutide demonstrated 24.2% body weight reduction in Phase 2 trials, approaching bariatric surgery outcomes. CagriSema showed 22.7% weight loss in REDEFINE-1 Phase 3 trials. These pipeline molecules sustain premium pricing and GLP-1 weight loss drug market demand growth through 2035.

Drug Class Analysis

GLP-1 Weight Loss Drug Market by Drug Class: Injectable and Dual Agonist Therapies Command 78.4% of Revenue

Drug Class Revenue Share, CAGR, and Commercial Drivers — GLP-1 Obesity Drug Market 2026

| Drug Class | Revenue Share | CAGR | Primary Market Driver |

|---|---|---|---|

| Injectable GLP-1 RA Monoagonists (Semaglutide / Wegovy) | 32.8% | 11.2% | Market leadership; SELECT cardiovascular approval; MASH and sleep apnea label expansion |

| Dual GIP/GLP-1 Agonists (Tirzepatide / Zepbound) | 31.6% | 18.4% | Superior weight loss efficacy benchmark; cardiovascular and sleep apnea indication expansion |

| Other GLP-1 RA Formulations (Dulaglutide, Exenatide) | 16.9% | 3.2% | Legacy prescribing; partial weight loss positioning; biosimilar transition underway |

| Oral GLP-1 Formulations (Oral Semaglutide / Orforglipron) | 8.4% | 34.2% | Patient preference for injection-free administration; access and compliance advantage |

| Liraglutide (Saxenda / Victoza) | 6.1% | -4.7% | Biosimilar entry competitive pressure; displaced by superior next-generation weekly therapies |

| Triple Agonist and Amylin Pipeline (Retatrutide, CagriSema, MariTide) | 4.2% | 41.8% | Phase 3 trials active; expected 2027–2028 FDA approval; strongest efficacy signal in GLP-1 pipeline |

Injectable GLP-1 receptor agonist monoagonists hold a 32.8% GLP-1 market revenue share in 2026, reflecting Wegovy’s position as the most commercially successful weight management drug in pharmaceutical history. Novo Nordisk shipped approximately 46 million Wegovy pens globally in 2025. The once-weekly injection and 15.3% mean body weight reduction from STEP-1 trials established Wegovy as the anti-obesity medication clinical benchmark.

Dual GIP/GLP-1 agonists now represent the highest-revenue growth segment in the GLP-1 weight loss drug market at 18.4% CAGR, with tirzepatide generating USD 18.3 billion in 2025 revenue through Zepbound and Mounjaro — surpassing Eli Lilly’s entire insulin franchise within two years of commercial launch.

Oral GLP-1 formulations represent the fastest-growing drug class segment at 34.2% CAGR through 2035. Phase 2 orforglipron data demonstrated 14.7% body weight reduction at 45mg without food or water requirements, and the addressable patient expansion is estimated to grow the anti-obesity medication market by 180 million new prescription patients between 2027 and 2032.

Route of Administration Analysis

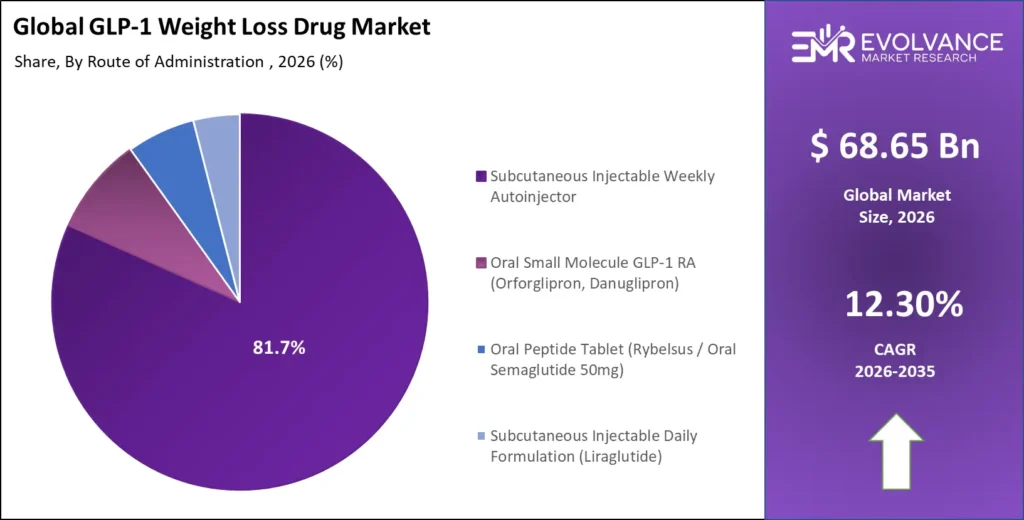

Subcutaneous Injectable Routes Dominate the GLP-1 Market; Oral GLP-1 Approaches Commercial Inflection by 2028

GLP-1 Weight Loss Drug Market Revenue Share, CAGR, and Primary Drivers by Route — 2026

| Route of Administration | Revenue Share | CAGR | Primary Driver |

|---|---|---|---|

| Subcutaneous Injectable Weekly Autoinjector | 81.7% | 9.4% | Clinical efficacy gold standard; Wegovy FlexTouch and Zepbound KwikPen weekly formats |

| Oral Small Molecule GLP-1 RA (Orforglipron, Danuglipron) | 8.4% | 34.2% | Injection-free delivery removes adherence barrier for 43% of treatment-eligible patients |

| Oral Peptide Tablet (Rybelsus / Oral Semaglutide 50mg) | 5.9% | 26.8% | OASIS obesity approval trajectory; dose escalation enabling dedicated obesity label |

| Subcutaneous Injectable Daily Formulation (Liraglutide) | 4.0% | -7.2% | Declining as patients transition from daily liraglutide to convenient weekly alternatives |

Subcutaneous injectable administration commands 81.7% GLP-1 market revenue share in 2026 as the weekly autoinjector format delivers clinical efficacy, dose consistency, and patient convenience superior to daily injectable alternatives. FlexTouch and KwikPen delivery systems minimize injection errors — critical for GLP-1 therapies where dose escalation spanning 16 to 20 weeks requires milligram-level titration.

The oral administration segment is projected to reach 14.3% combined GLP-1 market revenue share by 2035, driven by injection-free obesity treatment for the 43% of eligible patients citing injection aversion as the primary initiation barrier. The addressable patient expansion is estimated to grow the anti-obesity medication market by 180 million new prescription patients between 2027 and 2032.

Pipeline and Technology Innovation Analysis

GLP-1 Weight Loss Drug Market Pipeline: Triple Agonists, Oral Formulations, and Amylin Combinations Define the 2026–2035 Innovation Frontier

Key GLP-1 Pipeline Molecules, Mechanisms, Development Stage, and Peak Sales Projections

| Molecule | Developer | Mechanism | Phase | Est. Approval | Peak Annual Sales |

|---|---|---|---|---|---|

| Retatrutide | Eli Lilly | GLP-1/GIP/Glucagon Triple Agonist | Phase 3 Active | 2027 | USD 12–18 billion |

| CagriSema | Novo Nordisk | Semaglutide + Cagrilintide Amylin | Phase 3 Active | 2027 | USD 10–16 billion |

| Orforglipron | Eli Lilly | Oral Small Molecule GLP-1 RA | Phase 3 / NDA 2026 | 2026–2027 | USD 6–9 billion |

| Danuglipron | Pfizer | Oral Small Molecule GLP-1 RA | Phase 2 Advanced | 2028 | USD 4–6 billion |

| CT-388 | Roche/Genentech | GLP-1/GIP Dual Agonist Injectable | Phase 2 | 2029 | USD 5–8 billion |

| MariTide (AMG 133) | Amgen | Monthly GLP-1/GIP Antagonist | Phase 3 MARITIME | 2028 | USD 5–9 billion |

| Mazdutide | Innovent Biologics | GLP-1/Glucagon Dual Agonist | Phase 3 China | 2027 | USD 2–4 billion |

Triple agonist therapies targeting GLP-1, GIP, and glucagon receptors simultaneously represent the most significant efficacy advance in obesity pharmacotherapy since semaglutide. Retatrutide’s Phase 2 data demonstrating 24.2% mean body weight reduction approaches bariatric surgery outcomes without surgical risk. Eli Lilly initiated the TRIUMPH Phase 3 program in late 2024, with interim data expected to support a 2027 FDA submission and peak GLP-1 market sales projections of USD 12 to USD 18 billion.

CagriSema, Novo Nordisk’s co-formulation of semaglutide 2.4mg and the long-acting amylin analogue cagrilintide, demonstrated 22.7% body weight reduction in the REDEFINE-1 Phase 3 trial — substantially exceeding standalone semaglutide and positioning Novo Nordisk to defend GLP-1 market leadership against tirzepatide’s superior weight loss profile.

Application and Indication Analysis

GLP-1 Weight Loss Drug Market by Indication: Obesity Management Commands 61.4% of Revenue While Cardiovascular and Metabolic Indications Drive Premium Expansion

GLP-1 Drug Market Revenue Share, CAGR, and Key Clinical Evidence by Application — 2026

| Application / Indication | Revenue Share | CAGR | Key Clinical Evidence |

|---|---|---|---|

| Obesity and Chronic Weight Management | 61.4% | 11.8% | STEP-1 through STEP-5; SURMOUNT-1 through SURMOUNT-4 pivotal trials |

| Type 2 Diabetes with Obesity Comorbidity | 21.3% | 8.4% | SUSTAIN, LEADER, SURPASS cardiovascular outcomes programs |

| Cardiovascular Risk Reduction (MACE Prevention) | 8.6% | 22.7% | SELECT trial: 20% MACE reduction in non-diabetic obese patients with ASCVD |

| Metabolic Dysfunction-Associated Steatohepatitis (MASH) | 4.2% | 38.4% | ESSENCE trial: semaglutide Phase 3 liver fibrosis histology outcomes data |

| Obstructive Sleep Apnea (OSA) | 2.8% | 41.2% | SURMOUNT-OSA: 62.8% reduction in apnea-hypopnea index with tirzepatide |

| Adolescent Obesity (Age 12–17) | 1.7% | 34.6% | Wegovy FDA approval for adolescents June 2023; STEP-TEENS pivotal trial |

Obesity and chronic weight management represents the largest GLP-1 drug market application at 61.4% revenue share in 2026. STEP-4 trial data demonstrated 14% body weight rebound following Wegovy discontinuation at 68 weeks, establishing clinical justification for long-term GLP-1 therapy that insurers and national health technology bodies are progressively incorporating into obesity management protocols.

Cardiovascular risk reduction is the highest-growth established indication in the GLP-1 market at 22.7% CAGR as SELECT trial outcomes transform prescribing beyond endocrinology into cardiology channels. Cardiologists treating patients with atherosclerotic cardiovascular disease are increasingly initiating semaglutide as a cardiovascular risk modifier, adding an estimated 4.8 million new commercial GLP-1 patients annually. CMS is evaluating Medicare coverage expansion to cardiovascular prevention, projected to add USD 12.4 billion to the annual U.S. GLP-1 addressable market.

MASH and obstructive sleep apnea represent the highest-CAGR emerging indications, collectively at 40% CAGR through 2030. ESSENCE Phase 3 semaglutide in MASH data supported FDA approval in March 2024, creating a premium pricing tier in a disease category with USD 17.4 billion addressable market and no prior approved pharmacotherapy.

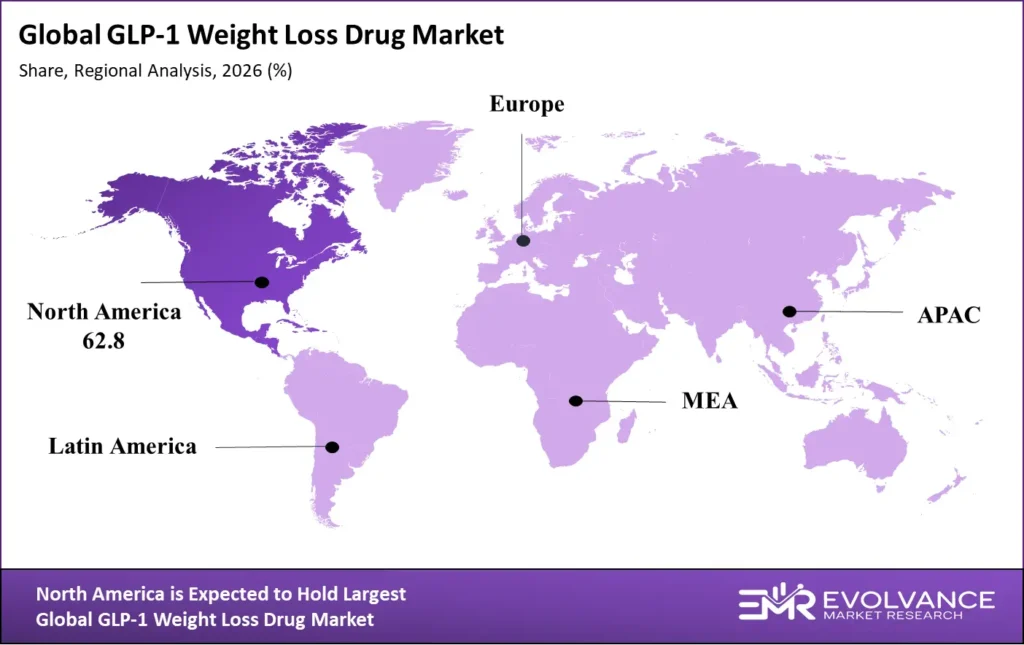

Regional Analysis of the Global GLP-1 Weight Loss Drug Market

United States Leads Global GLP-1 Drug Market Revenue; Asia-Pacific Is the Fastest-Growing Access Region Through 2035

| Region | Revenue Share | CAGR 2026–2035 | Key Market Driver |

|---|---|---|---|

| North America (United States, Canada) | 62.8% | 10.4% | Commercial insurance expansion, DTC marketing, Medicare cardiovascular indication review |

| Europe (EU, UK, Germany, France, Nordics) | 19.4% | 13.8% | EMA approvals, national obesity treatment programs, NICE positive NHS recommendation |

| Asia-Pacific (Japan, China, Australia, South Korea) | 10.2% | 22.6% | Rapidly rising obesity prevalence, regulatory approvals, expanding insurance penetration |

| Latin America (Brazil, Mexico, Colombia) | 4.8% | 18.4% | Brazilian ANVISA approvals, expanding private insurance, Novo Nordisk regional expansion |

| Middle East and Africa (Saudi Arabia, UAE, Israel) | 2.8% | 24.7% | Gulf state obesity epidemics above 35% prevalence, government health programs, affluent patient segments |

The United States holds a 62.8% GLP-1 Weight Loss Drug Market revenue share in 2026, driven by the highest commercial drug pricing environment globally. U.S. list prices for Wegovy at USD 1,349 per month and Zepbound at USD 1,059 per month generate per-unit economics unavailable in regulated pricing markets. Hims and Hers, Ro, and Amazon Clinic enrolled more than 2.8 million U.S. patients in GLP-1 telehealth obesity programs as of Q1 2026.

Europe represents the second-largest GLP-1 market region with 19.4% revenue share and 13.8% CAGR. NICE issued a positive technology appraisal for semaglutide in 2023, with NHS England targeting 35,000 patients in initial specialist weight management services. Germany, France, and Spain are negotiating reimbursement agreements at 40% to 65% discounts to U.S. list prices.

Asia-Pacific is the fastest-growing regional GLP-1 drug market at 22.6% CAGR, driven by rapidly rising obesity prevalence — China now reports 18.6% adult obesity prevalence up from 7.1% in 2000 — combined with expanding private health insurance and regulatory approvals. Japan approved semaglutide 2.4mg for obesity in 2023. China’s growing middle-class urban population represents an estimated 120 million commercially addressable obesity treatment patients.

Key Companies: Competitive Landscape of the GLP-1 Weight Loss Drug Market

Five ecosystem layers define competition in the GLP-1 Weight Loss Drug Market: approved injectable agonist brands, clinical pipeline challengers, biosimilar manufacturers, telehealth delivery platforms, and direct-to-patient manufacturer access programs. Novo Nordisk and Eli Lilly hold uniquely dominant positions, with competition intensifying as pharmaceutical challengers increase investment across all GLP-1 ecosystem layers.

| Company | Key GLP-1 Product(s) | Indication Focus | 2026 Market Position |

|---|---|---|---|

| Novo Nordisk | Wegovy (sema 2.4mg), Ozempic, Saxenda, Rybelsus | Obesity, T2D, CVD, MASH, Sleep Apnea | Market leader; approximately 52% GLP-1 market revenue share globally |

| Eli Lilly | Zepbound (tirzepatide), Mounjaro; retatrutide pipeline | Obesity, T2D, Sleep Apnea, CVD, triple agonist pipeline | Fastest-growing GLP-1 competitor; approximately 35% combined revenue |

| AstraZeneca | Cotadutide; partnership pipeline; farxiga combination | MASH, obesity with metabolic disease comorbidity | Clinical stage; multi-indication partnership strategy in GLP-1 market |

| Pfizer | Danuglipron oral small molecule GLP-1 RA, Phase 2 | Obesity; oral GLP-1 delivery differentiation focus | Pre-commercial; Phase 2 dose-finding data read-outs 2026 |

| Roche/Genentech | CT-388 GLP-1/GIP dual agonist injectable, Phase 2 | Obesity, MASH, metabolic disease comorbidity | Phase 2 active; acquisition-driven pipeline expansion strategy |

| Amgen | MariTide AMG 133 monthly GLP-1/GIP antagonist, Phase 3 | Obesity; once-monthly injection adherence differentiation | Phase 3 MARITIME-Obesity; interim efficacy data expected Q3 2026 |

| Zealand Pharma | Petrelintide, survodutide pipeline programs | Obesity, MASH, combination therapy positioning | Mid-stage pipeline; Boehringer Ingelheim partnership strategy |

| Biocon Biologics | Liraglutide biosimilar approved India and select markets | Generic access; emerging and lower-income country markets | First major liraglutide biosimilar commercial competitor in GLP-1 market |

| Hims and Hers / Ro | Compounded semaglutide; telehealth obesity platform | Access market; telehealth GLP-1 obesity management programs | USD 2.4 billion combined 2025 revenue; FDA compounding restriction risk |

| Ascendis Pharma | TransCon amylin; GLP-1 combination early pipeline | Next-generation combination obesity pharmacotherapy pipeline | Early clinical stage; prodrug technology platform differentiation |

Novo Nordisk maintains the highest strategic value in the GLP-1 Weight Loss Drug Market competitive landscape through first-mover advantage in dedicated obesity pharmacotherapy, manufacturing scale exceeding 24 billion API doses annually following the Catalent site acquisition, and a multi-indication strategy converting Wegovy into a broad metabolic disease platform.

Amgen’s MariTide (AMG 133) represents the most differentiated clinical approach among large pharmaceutical challengers, combining monthly subcutaneous injection frequency with dual GLP-1 agonism and GIP antagonism. Phase 2 MARITIME data showed 20.0% body weight reduction at 420mg monthly dose over 52 weeks, matching weekly semaglutide and tirzepatide efficacy from a once-monthly format.

Key Growth Drivers of the GLP-1 Weight Loss Drug Market

Three Structural Catalysts Driving GLP-1 Weight Loss Drug Market Expansion Through 2035

- Obesity epidemic scale: More than 1.1 billion adults with obesity globally representing a potential pharmacotherapy patient pool approximately 25 times larger than current GLP-1 prescribing volumes, with only 2.3% of eligible U.S. obesity patients currently receiving prescription GLP-1 anti-obesity medication.

- Multi-indication label expansion: Semaglutide approved across obesity, cardiovascular risk reduction, MASH, and sleep apnea creates a total addressable patient population of approximately 640 million globally — nearly four times the obesity-only base — adding new prescriber populations including cardiologists, hepatologists, and sleep medicine specialists.

- Medicare Part D coverage expansion: The proposed CMS rule allowing Medicare Part D plans to cover anti-obesity medications would make 31 million Medicare beneficiaries with obesity eligible for semaglutide and tirzepatide, representing a USD 55.8 billion annual drug spend potential at 15% initial penetration.

In the United States, 42.4% of adults meet obesity clinical criteria, while only 2.3% of eligible patients currently receive prescription anti-obesity medication. Medicare Part D coverage expansion represents a USD 18.4 billion addressable GLP-1 market catalyst that could restructure U.S. payer economics for the weight loss drug class.

Market Restraints

Drug Pricing, Supply Constraints, Gastrointestinal Tolerability, and Compounding Disruption Limit GLP-1 Market Scaling

Drug pricing and affordability remain the most impactful near-term restraints for the GLP-1 Weight Loss Drug Market through 2030. At USD 1,349 per month list price for Wegovy and USD 1,059 for Zepbound, monthly GLP-1 obesity drug costs create absolute financial barriers for the 62% of obesity patients enrolled in Medicaid, Medicare, or underinsured commercial plans without anti-obesity medication benefits. Patient out-of-pocket costs of USD 200 to USD 500 monthly drive the 68% GLP-1 drug discontinuation rate in real-world adherence studies within the first 12 months of therapy.

The FDA’s formal guidance against compounded semaglutide — projected to eliminate USD 3.6 billion in compounding pharmacy and telehealth revenue in 2025–2026 — creates disruption risk for approximately 1.5 million patients receiving compounded GLP-1 outside branded channels. Gastrointestinal adverse events drive 9% to 14% of initiated patients to permanently discontinue GLP-1 therapy.

Market Opportunities

Biosimilar Liraglutide Access Markets, Emerging Geography Expansion, and Precision Obesity Medicine Unlock Underserved GLP-1 Market Growth Segments

Biosimilar liraglutide entry represents the first generic competition wave for the GLP-1 weight loss drug category, expanding access for the 480 million obesity patients in lower-middle income countries for whom USD 1,000-plus monthly branded drug pricing is permanently inaccessible. Biocon Biologics’ biosimilar liraglutide launched in India and select emerging markets in 2024 at pricing 60% to 75% below branded Saxenda list prices.

Precision obesity medicine — matching patients to specific GLP-1 mechanisms based on genetic predictors, gut microbiome profiles, and metabolic phenotyping — represents an emerging differentiation opportunity. The precision obesity medicine market is projected to reach USD 4.8 billion by 2032.

Patient Access Economics and Healthcare Coverage Framework

Insurance Coverage, Employer Benefits, and Global Reimbursement Pathways Define GLP-1 Weight Loss Drug Market Commercial Scalability

The patient access landscape for GLP-1 weight loss drugs is undergoing rapid payer policy evolution, with commercial coverage expanding from 26% of U.S. commercial health plans in 2021 to a landmark 48% in 2026. SELECT cardiovascular outcome data demonstrates positive net present value within 8.4 years for semaglutide coverage through reduced hospitalizations and diabetes progression costs.

Employer self-insured health benefits represent a critical access channel driving U.S. GLP-1 market volume expansion. Employers including JPMorgan Chase, Amazon, and Apple include GLP-1 obesity coverage in employee health plans. Morgan Stanley estimated in 2024 that employer GLP-1 coverage generates USD 8,200 in annual healthcare cost savings per successfully treated employee with obesity — generating positive ROI within 3 to 5 years.

The United Kingdom’s NHS England weight management program is projected to reach 220,000 patients by 2026 at negotiated prices below USD 400 per month through structured behavioral support programs. Reimbursement expansion across the 47-country access market is estimated to add USD 28.4 billion to the global GLP-1 market through 2030.

Biosimilar and Competitive Entry Framework

GLP-1 Weight Loss Drug Market Patent Cliffs, Biosimilar Strategy, and Generic Competition Define Post-2028 Market Structure

The GLP-1 Weight Loss Drug Market faces its first major biosimilar competition wave between 2026 and 2032, with liraglutide as the first major casualty and semaglutide patents constituting the next critical competitive boundary. Novo Nordisk holds semaglutide composition-of-matter and formulation patents expiring between 2031 and 2038 across different jurisdictions, with FlexTouch autoinjector device patents extending GLP-1 competitive protection in the U.S. through approximately 2033.

Biosimilar semaglutide development programs have been announced by 14 manufacturers globally, including Samsung Bioepis, Biocon Biologics, Sandoz, Mylan and Viatris, Hikma, and multiple Chinese biotechnology companies. U.S. semaglutide biosimilar approvals are not expected before 2031, preserving Novo Nordisk’s GLP-1 market branded revenue through the near-term forecast period.

The GLP-1 market will bifurcate into a branded premium injectable tier for highest-efficacy patients and an oral generic access tier for cost-sensitive patients — growing total prescription volumes while compressing per-unit average selling prices from 2030 onward.

Obesity Disease Burden and Population Health ROI Framework

Economic Cost of Obesity, Comorbidity Cascade, and GLP-1 Pharmacotherapy Value-Based Evidence Reshape Global Treatment Investment

The Global Obesity Forum estimated total annual economic costs of obesity at USD 4.32 trillion annually in 2025, representing 2.92% of global GDP and exceeding the full economic output of Germany. In the United States, obesity-attributable healthcare spending reaches USD 260 billion annually.

A 15% body weight reduction — the STEP-1 semaglutide benchmark — is associated with type 2 diabetes remission in 37% of treated patients, 28% reduction in hypertension medication requirements, 25% improvement in sleep apnea severity, and MASH progression reversal. These multisystem benefits create a healthcare ROI calculation where GLP-1 therapy prevents conditions with substantially higher lifetime treatment costs than the drug itself.

McKinsey Global Institute projected that broad GLP-1 adoption for eligible obese adults in high-income countries could generate USD 1.8 trillion in cumulative healthcare savings by 2040 through reduced cardiovascular hospitalizations, diabetes complication avoidance, and musculoskeletal disease prevention.

Latest Trends in the GLP-1 Weight Loss Drug Market

Oral GLP-1 Approval, Bariatric Surgery Displacement, and Telehealth Scaling Define 2026 GLP-1 Weight Loss Drug Market Dynamics

Oral GLP-1 receptor agonist approvals are the defining GLP-1 Weight Loss Drug Market transformation event of 2026. Eli Lilly submitted the orforglipron NDA to the FDA in Q1 2026 following ATTAIN Phase 3 trial data showing 14.7% body weight reduction at 45mg — positioning the world’s first oral small molecule GLP-1 receptor agonist for obesity for anticipated FDA approval in late 2026 or 2027. Oral GLP-1 removes the largest stated initiation barrier for 43% of obesity patients, expanding the treatment-seeking population by an estimated 60 to 90 million patients within three years.

Bariatric surgery volumes are declining for the first time in recorded history as GLP-1 pharmacotherapy outcomes approach surgical efficacy thresholds. U.S. bariatric procedure volumes declined 11.4% in 2025 — reversing a two-decade growth trend — as semaglutide and tirzepatide provide comparable weight loss outcomes for class I and class II obesity without surgical risk, recovery time, or nutritional deficiency complications.

Digital health platforms are becoming structural distribution and adherence infrastructure for GLP-1 therapy. Telehealth obesity platforms including Hims and Hers, Ro, and Noom Med collectively supported more than 3.1 million active GLP-1 prescriptions as of Q1 2026, delivering AI-powered dosage guidance, nutrition coaching, behavioral health support, and automated refill management within subscription platforms.

Recent GLP-1 Weight Loss Drug Market Developments: Novo Nordisk, Eli Lilly, Amgen, and FDA Lead 2025–2026

- April 2026: Eli Lilly submitted the orforglipron New Drug Application to the FDA for obesity treatment, reporting 14.7% body weight reduction in the ATTAIN-WEIGHT1 Phase 3 trial at the 45mg dose — the first oral small molecule GLP-1 receptor agonist NDA submission for dedicated obesity pharmacological treatment in the United States.

- March 2026: Novo Nordisk reported top-line REDEFINE-1 Phase 3 CagriSema data showing 22.7% mean body weight reduction at 52 weeks, demonstrating superiority over standalone semaglutide 2.4mg and confirming the semaglutide-plus-amylin combination as clinically competitive with tirzepatide.

- January 2026: Amgen completed Phase 3 enrollment for MariTide (AMG 133) in the MARITIME-Obesity trial, with interim efficacy data expected in Q3 2026 that will position the monthly injection GLP-1/GIP antagonist as a once-monthly obesity treatment alternative.

- November 2025: FDA approved expanded Zepbound (tirzepatide) indication for moderate-to-severe obstructive sleep apnea in adults with obesity, following SURMOUNT-OSA trial data showing 62.8% reduction in apnea-hypopnea index — the first drug approval for sleep apnea treatment.

- August 2025: Novo Nordisk announced a USD 4.1 billion U.S. manufacturing investment, including a new fill-and-finish facility in Clayton, North Carolina, targeted to add 600 million additional Wegovy pen doses annually by 2027.

Competitive Landscape

GLP-1 Weight Loss Drug Market Competitive Landscape: Novo Nordisk and Eli Lilly Duopoly, Oral GLP-1 Challengers, and Telehealth Platforms Reshape the Obesity Drug Market Through 2035

The GLP-1 Weight Loss Drug Market competitive landscape is defined by exceptional concentration at the approved drug tier — where Novo Nordisk and Eli Lilly collectively control approximately 87% of global prescription obesity drug revenue — combined with intense clinical development competition among more than 40 active GLP-1 pipeline programs. This competitive architecture creates distinct strategic layers: duopoly incumbents maximizing anti-obesity medication penetration; pharmaceutical challengers competing through next-generation mechanisms; and generic manufacturers positioning for biosimilar competition from 2031 onward.

Vertical integration is the defining competitive strategy among leading GLP-1 Weight Loss Drug Market participants through 2030. Novo Nordisk’s USD 16.5 billion acquisition of Catalent manufacturing sites secured fill-and-finish capacity for 25 billion drug doses annually. Both companies are simultaneously investing in digital health ecosystems — Lilly Direct and Novo Nordisk’s digital engagement platforms — embedding GLP-1 drug access within broader patient infrastructure.

Key GLP-1 Weight Loss Drug Market Segments

By Drug Class

- Dual GIP/GLP-1 Receptor Agonists (Tirzepatide and pipeline GIP/GLP-1 molecules)

- Injectable GLP-1 Receptor Agonist Monoagonists (Semaglutide Wegovy and Ozempic branded portfolio)

- Oral GLP-1 Formulations (Oral Semaglutide, Orforglipron, Danuglipron, GSBR-1290 small molecule)

- Liraglutide and Legacy Injectable GLP-1 Receptor Agonists (Saxenda, Victoza)

- Triple Agonists and Amylin Combination Pipeline Therapies (Retatrutide, CagriSema, MariTide)

By Route of Administration

- Subcutaneous Injectable Weekly Autoinjector (Primary Commercial Format across GLP-1 Market)

- Oral Small Molecule GLP-1 Receptor Agonists (Non-Peptide Tablet Formulations)

- Oral Peptide Tablet Formulations (Rybelsus and Successor Obesity-Labeled Oral GLP-1 Molecules)

- Daily Subcutaneous Injectable (Liraglutide Legacy Delivery Format)

- Extended-Release Implantable and Depot Formulations (Late-Stage GLP-1 Pipeline)

By Application and Indication

- Obesity and Chronic Weight Management (Primary Commercial GLP-1 Market Indication)

- Type 2 Diabetes with Obesity Comorbidity (Metabolic Dual-Indication Prescribing)

- Cardiovascular Risk Reduction and MACE Prevention (Post-SELECT Trial GLP-1 Expansion)

- Metabolic Dysfunction-Associated Steatohepatitis MASH Treatment (Semaglutide Approved March 2024)

- Obstructive Sleep Apnea OSA Treatment (Tirzepatide FDA Approved November 2025)

- Adolescent Obesity Management (Wegovy Approved for Age 12 and Above June 2023)

By Distribution Channel

- Specialty Pharmacy with Obesity Management Program Enrollment and Adherence Infrastructure

- Retail Chain Pharmacy (CVS, Walgreens, Rite Aid with GLP-1 access and refill management)

- Hospital and Institutional Outpatient Pharmacy

- Telehealth and Online Pharmacy Platforms (Hims and Hers, Ro, Amazon Clinic GLP-1 programs)

- Direct-to-Patient Manufacturer Access Programs (NovoCare, Lilly Cares Foundation)

By Geography

- North America (United States and Canada GLP-1 Weight Loss Drug Market)

- Europe (European Union, United Kingdom, Germany, France, Italy, Spain, Nordic Countries)

- Asia-Pacific (Japan, China, Australia, South Korea, India, Singapore GLP-1 Markets)

- Latin America (Brazil, Mexico, Argentina, Colombia Regional Obesity Drug Market)

- Middle East and Africa (Saudi Arabia, United Arab Emirates, Israel, South Africa)

GLP-1 Weight Loss Drug Market Report Features and Coverage

| Report Feature | Details |

|---|---|

| GLP-1 Market Value (Base Year 2026) | USD 68.65 billion |

| GLP-1 Market Forecast Revenue (2035) | USD 195.01 billion (more than double from 2026 base) |

| Market CAGR (2026–2035) | 12.3% |

| Base Year for Estimation | 2026 |

| Historic Analysis Period | 2020–2025 |

| Forecast Period Covered | 2026–2035 |

| Report Coverage | Revenue Forecast, Drug Class Analysis, Pipeline Innovation Benchmarking, Patient Access Economics, Biosimilar Entry Framework, Regional Analysis with Country Data, Obesity Disease Burden, Population Health ROI, Competitive Intelligence |

| Market Segments Covered | By Drug Class, By Route of Administration, By Application and Indication, By Distribution Channel, By Geography (5 regions with country-level revenue and regulatory data) |

| Regional Coverage | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa with country-level GLP-1 market revenue and regulatory status |

| Dominant Drug Class in GLP-1 Market | Injectable GLP-1 RA and Dual GIP/GLP-1 Agonists with 78.4% combined revenue share in 2026 |

| Fastest-Growing GLP-1 Market Segment | Oral GLP-1 Formulations at 34.2% CAGR through 2035 |

| Key Companies Profiled | Novo Nordisk, Eli Lilly, AstraZeneca, Pfizer, Amgen, Roche/Genentech, Zealand Pharma, Biocon Biologics, Hims and Hers Health, Ascendis Pharma |