Executive Summary

Quick Insight: The global Predictive Maintenance market is positioned to expand more than 6× by 2035, driven by accelerating Industrial Internet of Things adoption, AI-powered failure prediction algorithms, smart manufacturing mandates across heavy industry, and the measurable cost reduction outcomes that real-time condition monitoring delivers across asset-intensive sectors worldwide.

The global Predictive Maintenance market encompasses AI and ML software platforms, IIoT sensor hardware, edge analytics devices, cloud condition monitoring services, and managed maintenance intelligence solutions enabling enterprises to predict and prevent equipment failures. This report provides comprehensive analysis of market size, technology stack dynamics, deployment economics, and competitive intelligence for 2026–2035, covering AI model architectures, IIoT sensor networks, digital twin integration, and smart manufacturing trends reshaping industrial asset management globally.

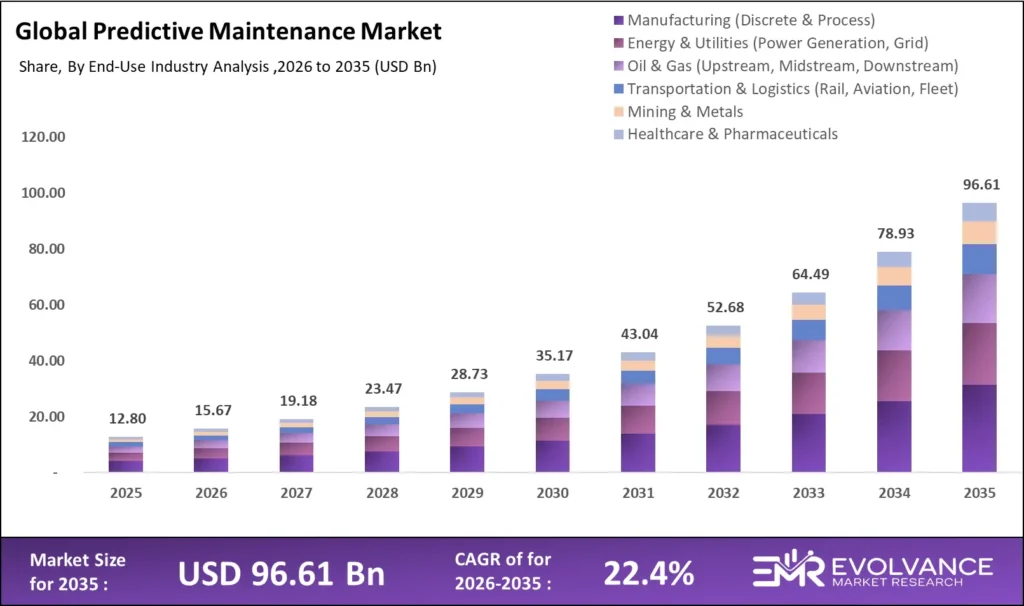

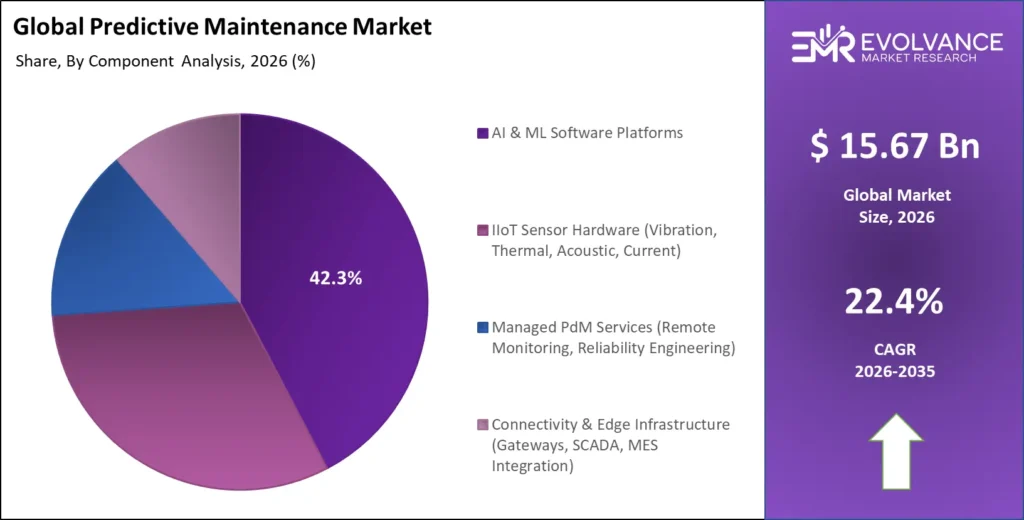

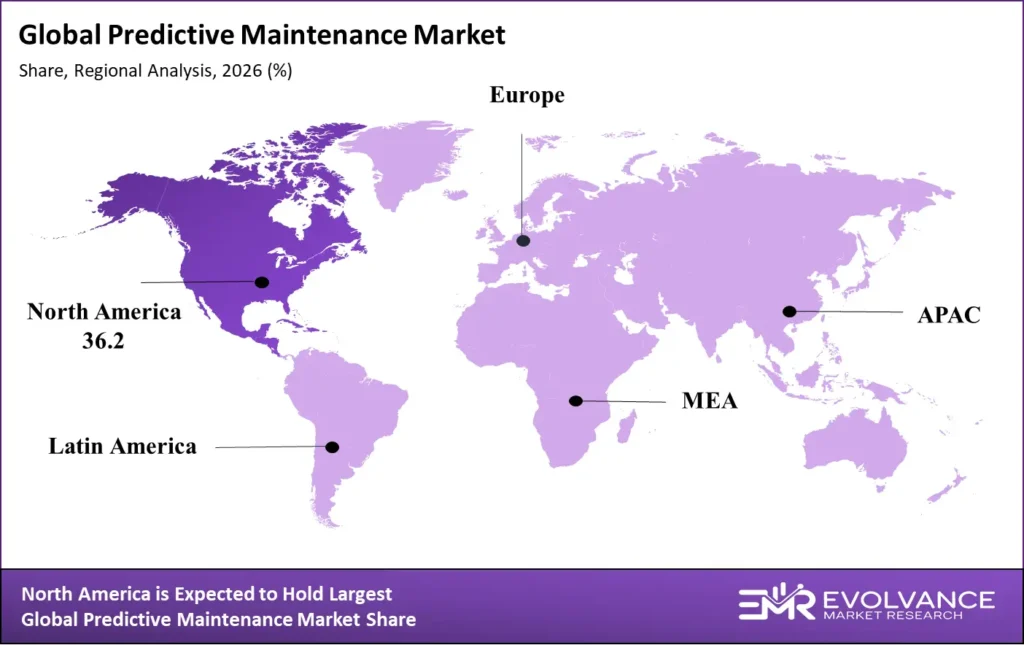

Key findings: The market reaches USD 15.67 billion in 2026 and compounds at 22.4% CAGR to USD 96.61 billion by 2035. AI and ML software platforms command 42.3% of total solution spend. Cloud deployment leads with 41.8% revenue share. Manufacturing holds the largest end-use sector share at 28.4%. Unplanned industrial downtime costs global manufacturing an estimated USD 864 billion annually — the primary economic justification accelerating enterprise PdM adoption through 2035.

What Is the Predictive Maintenance Market?

The global Predictive Maintenance market was valued at USD 15.67 billion in 2026 and is projected to reach approximately USD 96.61 billion by 2035, growing at a CAGR of 22.40% during the forecast period. The convergence of affordable IIoT sensor hardware, cloud-native AI analytics platforms, and demonstrable return on investment — with leading industrial enterprises reporting 25% to 40% reductions in unplanned downtime — is converting predictive maintenance from a pilot-stage initiative into core operational technology budget spend globally.

The market encompasses vibration, temperature, acoustic, and current signature sensor hardware; edge analytics gateways and IIoT connectivity platforms; AI and ML software for anomaly detection, remaining useful life prediction, and failure mode classification; digital twin simulation environments integrating physical asset models with real-time sensor streams; and managed PdM services including remote condition monitoring, reliability engineering consulting, and maintenance scheduling optimization.

Predictive Maintenance Market Highlights: Key Data at a Glance

- Market value: USD 15.67 billion in 2026, forecast to USD 96.61 billion by 2035 at 22.4% CAGR

- Dominant component: AI & ML Software Platforms with 42.3% revenue share

- Dominant deployment mode: Cloud with 41.8% infrastructure revenue share

- Fastest-growing deployment: Edge AI Analytics at 34.7% CAGR through 2035

- Dominant end-use industry: Manufacturing with 28.4% sector share

- Economic driver: USD 864 billion in annual global unplanned downtime costs

- IIoT device installed base: 18.3 billion connected industrial sensors projected by 2030

- Top infrastructure market: North America with 36.2% of global PdM spend

- AI accuracy benchmark: Leading PdM platforms achieve 94% to 97% failure prediction accuracy at 72-hour advance warning

- Fastest-growing region: Asia-Pacific at 28.6% CAGR driven by smart manufacturing programs

Market Overview: Why Predictive Maintenance Growth Is Accelerating

The Predictive Maintenance market is at an inflection point defined by three simultaneous demand accelerators reshaping industrial asset management across every major sector. The first is the AI maturation cycle: machine learning models trained on vibration, thermal, acoustic, and electrical signature datasets have crossed the commercial reliability threshold required for industrial deployment. Platforms from Siemens, IBM Maximo, and Azure Digital Twins now deliver failure predictions with 94% to 97% accuracy at 72-hour advance warning windows — sufficient for planned maintenance execution without production interruption.

The second accelerator is the structural economics of IIoT sensor hardware commoditization. Wireless vibration sensor nodes that cost USD 800 to USD 1,200 per unit in 2019 are available at USD 180 to USD 320 in 2026 from manufacturers including Emerson, Honeywell, and a growing array of Asian sensor suppliers. This 65% to 75% hardware cost reduction expands the economic justification for comprehensive sensor coverage from high-criticality rotating equipment to secondary assets including pumps, fans, conveyors, and compressors that collectively represent 60% to 75% of industrial maintenance cost.

The third accelerator is the enterprise sustainability and operational efficiency imperative. Condition-based maintenance reduces asset energy consumption by 5% to 15% by eliminating the mechanical degradation that causes inefficient operation before catastrophic failure. These dual economic and sustainability benefits — cost reduction plus ESG compliance — are placing PdM on capital expenditure approval pathways previously reserved for safety-critical investments, accelerating enterprise adoption velocity through 2035.

Component Analysis

AI & ML Software Platforms Command 42.3% of Predictive Maintenance Spend

Condition Monitoring Software, IIoT Sensor Hardware, Edge Analytics, and Managed Services Drive Revenue by Component

| Component | Share % | Primary Driver |

|---|---|---|

| AI & ML Software Platforms | 42.3% | Failure prediction models, anomaly detection, RUL estimation, digital twin integration |

| IIoT Sensor Hardware (Vibration, Thermal, Acoustic, Current) | 31.6% | Asset coverage expansion, wireless sensor node commoditization, greenfield IIoT deployments |

| Managed PdM Services (Remote Monitoring, Reliability Engineering) | 14.8% | SME adoption, outsourced reliability programs, managed condition monitoring SLAs |

| Connectivity & Edge Infrastructure (Gateways, SCADA, MES Integration) | 11.3% | Industrial protocol bridging, OT/IT convergence, edge-to-cloud data pipeline deployment |

AI and ML Software Platforms hold a 42.3% component revenue share in 2026, making intelligent analytics the central economic driver of the Predictive Maintenance market. The leading AI PdM software platforms use ensemble machine learning models — combining gradient boosting, long short-term memory neural networks, and physics-informed models — trained on multivariate sensor time-series data. Microsoft Azure Predictive Maintenance, IBM Maximo Application Suite, SAP Asset Intelligence Network, and purpose-built platforms from Aspentech, Uptake, and Seeq are competing for enterprise industrial analytics spending growing at 28.3% annually through 2030.

IIoT Sensor Hardware represents 31.6% of market revenue in 2026. The global installed base of industrial IIoT condition monitoring sensors is projected to grow from 4.2 billion units in 2026 to 18.3 billion by 2030, generating recurring software subscription and services revenue that will exceed hardware revenue by 2028.

Managed PdM Services — encompassing remote condition monitoring centers, reliability engineering consulting, and full maintenance program outsourcing — represent the fastest-growing professional services category within the market, expanding at 31.4% annually. SKF’s Remote Diagnostic Centre, Siemens Xcelerator Remote Monitoring, and Emerson’s Plantweb Optics service platform operate 24/7 monitoring centers staffed by rotating equipment specialists.

Deployment Mode Analysis

Cloud Leads with 41.8% Share; Edge AI Analytics Is the Fastest-Growing Deployment Mode

Cloud PdM Platforms, On-Premise SCADA Integration, Hybrid Architecture, and Edge Inference — Deployment Economics Breakdown

| Deployment Mode | Share % | CAGR | Primary Driver |

|---|---|---|---|

| Cloud (SaaS PdM Platform) | 41.8% | 20.6% | AWS IoT, Azure Digital Twins, Google Cloud IoT — enterprise PdM platform subscriptions |

| On-Premise (SCADA/MES Integration) | 29.4% | 18.2% | Air-gapped facility requirements, OT security policy, legacy DCS integration |

| Hybrid (Edge + Cloud) | 20.1% | 27.4% | Bandwidth optimization, latency-sensitive fault detection, OT/IT convergence |

| Edge AI (Real-Time Inference) | 8.7% | 34.7% | Sub-100ms fault detection, offline capability, 5G-connected smart factory |

Cloud deployment holds a 41.8% share of Predictive Maintenance revenue in 2026. Microsoft Azure IoT Hub and Azure Digital Twins, AWS IoT SiteWise, Google Cloud IoT Core, and purpose-built industrial cloud platforms from OSIsoft (PI Cloud), Aspentech, and Bentley Systems collectively represent the dominant cloud PdM platform ecosystem. Cloud PdM’s primary advantage is continuous model improvement: platforms aggregating sensor data from thousands of assets across multiple customers develop statistical training datasets that single-site on-premise deployments cannot replicate.

Edge AI is the fastest-growing deployment mode, expanding at 34.7% CAGR through 2035. Real-time fault detection demands inference latency below 100 milliseconds, achievable only through on-device or local edge AI. NVIDIA’s Jetson AGX Orin, Intel’s OpenVINO edge inference toolkit, and Siemens’ Industrial Edge platform are enabling AI-powered anomaly detection at the sensor gateway level. The global installed base of edge AI inference nodes for industrial predictive maintenance is projected to reach 340 million units by 2030, generating USD 8.9 billion in annual edge hardware and software revenue.

AI Technology Stack Analysis: IIoT Sensors, Machine Learning Platforms & Digital Twins

AI Failure Prediction, IIoT Sensor Networks, Digital Twin Architecture, and Edge Analytics Define the 2026–2035 PdM Stack

| Technology Layer | Key Vendors | 2026 Share % | Key Trend |

|---|---|---|---|

| AI/ML Analytics (LSTM, Gradient Boost, Physics-Informed Models) | IBM, Microsoft, Aspentech, Uptake | 28.4% | Foundation models for industrial time-series accelerating cross-asset transfer learning |

| IIoT Sensor Networks (Vibration, Thermal, Acoustic) | Emerson, Honeywell, SKF, Augury | 24.6% | Wireless sensor cost reduction enabling comprehensive secondary asset coverage |

| Digital Twin Platforms (Real-Time Asset Simulation) | Siemens, Ansys, Bentley, PTC | 16.2% | Physics-AI hybrid twins delivering remaining useful life predictions at 95%+ accuracy |

| Edge Computing & Industrial Gateways | NVIDIA, Intel, Siemens, Cisco | 12.8% | On-device inference eliminating cloud latency for safety-critical detection |

| Cloud IIoT Platforms (Data Pipeline, Storage, Orchestration) | AWS, Azure, Google, IBM | 11.3% | Industrial data lakehouse architectures consolidating multi-site OT data at scale |

| SCADA/CMMS Integration Middleware | OSIsoft, Inductive Automation, GE Vernova | 6.7% | OT/IT convergence bridging legacy historian data into modern AI analytics pipelines |

AI and ML analytics represent the highest-value technology layer in the predictive maintenance stack, with LSTM networks and physics-informed machine learning models emerging as the dominant architectures for industrial time-series anomaly detection. LSTM networks capture temporal dependencies in vibration and acoustic sensor streams that traditional statistical process control methods cannot model — enabling detection of incipient bearing defects, rotor imbalance, and misalignment at fault severity levels invisible to human operators or threshold-based alert systems.

Digital Twin platforms are transitioning from geometric visualization tools to physics-AI hybrid simulation environments that integrate real-time sensor telemetry with finite element models, computational fluid dynamics, and thermodynamic simulation. Siemens’ Simcenter Amesim, Ansys Twin Builder, and PTC’s ThingWorx enable engineers to simulate asset degradation trajectories under varying operating conditions — generating synthetic failure mode training data for rare failure modes that may occur only once per decade in normal operations.

End-Use Industry Analysis

Manufacturing, Energy & Utilities, and Oil & Gas Command Combined 60.2% of Global PdM Demand

Sector-by-Sector AI Predictive Maintenance Spend Benchmarks and Use Case Drivers for 2026

| End-Use Industry | Revenue Share % | CAGR | Top Use Case |

|---|---|---|---|

| Manufacturing (Discrete & Process) | 28.4% | 21.8% | CNC machine tool health, injection molding presses, conveyor systems, motor drives |

| Energy & Utilities (Power Generation, Grid) | 18.2% | 24.3% | Wind turbine gearboxes, steam turbine bearings, transformer condition monitoring |

| Oil & Gas (Upstream, Midstream, Downstream) | 13.6% | 19.4% | Compressor trains, pump condition monitoring, pipeline integrity, offshore equipment |

| Transportation & Logistics (Rail, Aviation, Fleet) | 11.4% | 28.7% | Rail wheel and track monitoring, aircraft engine health management, fleet diagnostics |

| Mining & Metals | 9.2% | 22.6% | Crusher and conveyor reliability, haul truck drivetrain, slurry pump monitoring |

| Healthcare & Pharmaceuticals | 7.8% | 31.2% | HVAC validation, cleanroom equipment, GMP-compliant production asset monitoring |

| Chemical & Petrochemical | 6.4% | 18.8% | Reactor agitator monitoring, centrifugal compressors, heat exchanger fouling detection |

| Other (Water, Food & Beverage, Defense) | 5.0% | 20.3% | Water pump networks, bottling line reliability, military equipment readiness |

Manufacturing holds the largest end-use industry revenue share at 28.4% in 2026. Automotive manufacturers including Toyota, BMW, and Volkswagen have deployed enterprise-wide PdM programs covering 80,000 to 200,000 monitored assets per manufacturing group, achieving reported reductions of 35% to 47% in unplanned downtime and 18% to 28% in total maintenance cost.

Energy and Utilities is the second-largest sector at 18.2%, growing at 24.3% CAGR. A single offshore wind turbine gearbox replacement costs USD 300,000 to USD 800,000, requires specialized marine crane vessels, and causes 5 to 14 days of energy production loss — making even a single prevented catastrophic failure sufficient to justify an entire wind farm PdM program investment.

Healthcare and Pharmaceuticals is the fastest-growing end-use segment at 31.2% CAGR, driven by FDA Process Analytical Technology guidance and GMP compliance requirements that make equipment reliability a regulatory imperative. AI-powered predictive maintenance platforms that automatically generate maintenance records, predict calibration drift, and forecast sterile filling line component replacements are enabling compliance automation with validated electronic batch record integration.

Regional Analysis of the Global Predictive Maintenance Market

North America Leads Global PdM Investment; Asia-Pacific Is the Fastest-Growing Region

| Region | Share % | CAGR | Key Driver |

|---|---|---|---|

| North America (U.S., Canada) | 36.2% | 20.8% | Smart manufacturing mandates, IIoT platform investments, Industrial AI venture funding |

| Asia-Pacific (China, Japan, South Korea, India, Australia) | 33.8% | 28.6% | China Made in China 2025 digital factory programs, Japan Society 5.0, India smart manufacturing |

| Europe (Germany, UK, France, Netherlands, Italy) | 18.4% | 21.2% | EU Digital Industry Strategy, Germany Industrie 4.0, renewable energy PdM expansion |

| Middle East & Africa (Saudi Arabia, UAE, South Africa) | 7.2% | 26.4% | Saudi Vision 2030 industrial digitalization, petrochemical asset optimization |

| Latin America (Brazil, Mexico, Chile) | 4.4% | 19.6% | Mining sector digitalization, automotive manufacturing expansion, energy sector modernization |

North America holds a 36.2% global PdM revenue share in 2026, driven by the highest concentration of industrial AI software vendors, IIoT platform providers, and enterprise manufacturing corporations with active smart factory transformation programs. The U.S. Department of Energy’s Manufacturing USA institutes have deployed USD 2.4 billion in manufacturing digitalization co-investment since 2014. General Motors, Caterpillar, ExxonMobil, and Duke Energy represent the archetypes of large North American industrial enterprises with enterprise-wide PdM programs covering hundreds of facilities.

Asia-Pacific is the fastest-growing region at 28.6% CAGR through 2035. China’s Made in China 2025, Japan’s Society 5.0, South Korea’s Smart Factory program targeting 30,000 smart factories by 2030, and India’s National Manufacturing Policy drive IIoT and AI investment independent of commercial enterprise economics. Chinese IIoT platform vendors including Sany Heavy Industry’s ROOTCLOUD, Haier COSMOPLAT, and Baidu’s Edge Intelligence deploy domestic PdM solutions at price points expanding adoption into SME segments.

Key Companies: Platforms and Vendors Defining the Predictive Maintenance Competitive Landscape

Five ecosystem layers define PdM competition: IIoT sensor hardware, AI analytics software, industrial cloud infrastructure, OEM integrated services, and managed reliability outsourcing. Siemens holds the most integrated position across the first three layers, with hyperscalers, independent IIoT vendors, and AI-native startups intensifying competition across all segments.

| Company | Segment | Key Differentiator | 2026 Status |

|---|---|---|---|

| IBM (Maximo Application Suite) | AI PdM Software | Enterprise CMMS + AI integration; Watson-powered anomaly detection; 6,000+ enterprise deployments | Asset management market leader |

| Siemens (Xcelerator, Mindsphere) | Integrated IIoT + PdM | Xcelerator industrial IoT platform; factory automation data integration; digital twin capabilities | Largest industrial PdM ecosystem |

| Microsoft (Azure IoT, Digital Twins) | Cloud PdM Platform | Azure IoT Hub; Azure Digital Twins SDK; Time Series Insights; OpenAI model integration | Cloud PdM platform leader |

| Emerson Electric (AMS, Plantweb) | Sensor Hardware + Services | Wireless sensor networks; Plantweb Optics analytics; Remote Diagnostics Centre services | Process industry leader |

| Honeywell (Forge, Connected Plant) | Industrial Analytics | Honeywell Forge Asset Performance; refining and petrochemical expertise; OPC-UA integration | Energy sector PdM leader |

| SKF (Enlight, Remote Diagnostics) | Bearing OEM + Services | Bearing physics models; Remote Diagnostic Centre; rotating equipment domain expertise | Mechanical PdM specialist |

| GE Vernova (APM, Predix) | Asset Performance Mgmt | APM platform for power and industrial assets; digital twin for gas and wind turbines | Power generation PdM leader |

| Aspentech (Aspen Mtell) | AI Failure Prediction | Pattern recognition AI; proactive failure detection 90+ days advance warning; process industry focus | AI accuracy benchmark setter |

| Augury | AI-Native PdM Startup | Machine health platform; vibration and ultrasound AI; USD 1.1B valuation Series E funding | Fastest-growing independent PdM vendor |

| PTC (ThingWorx, Vuforia) | IIoT Platform | ThingWorx industrial connectivity; Vuforia AR maintenance guidance; Kepware OPC integration | Industrial IoT platform challenger |

Siemens maintains the highest breadth of strategic value in the PdM competitive landscape through its unique position as both automation hardware OEM, industrial software platform provider, and energy infrastructure operator. Its acquisition of Bentley Systems positions Siemens at the intersection of predictive maintenance and infrastructure digital twin intelligence, a convergence that will drive USD 4.2 billion in incremental platform revenue by 2030.

Augury’s machine health platform — combining proprietary vibration and ultrasound sensor hardware with AI diagnostic software — has achieved USD 1.1 billion valuation with enterprise deployments at Colgate-Palmolive, General Mills, and Heineken. Its AI models are trained on more than 80,000 monitored machines globally, creating a failure mode database that establishes network effect competitive advantages compounding as deployment scale increases through 2030.

Key Growth Drivers of the Predictive Maintenance Market

IIoT Sensor Commoditization, AI Accuracy Milestones, and Smart Manufacturing Mandates Drive Structural Demand

The global unplanned downtime cost of USD 864 billion annually is the primary demand driver for predictive maintenance across all industrial sectors through 2035. Aberdeen Research reports that average hourly unplanned downtime costs range from USD 12,000 for small manufacturing facilities to USD 2.4 million for continuous process industries including petroleum refining, petrochemical production, and semiconductor fabrication. Industrial enterprises that deploy AI-powered condition monitoring consistently report payback periods of 8 to 18 months and five-year NPV returns of 3× to 7× initial investment.

IIoT sensor hardware commoditization is the structural technology enabler accelerating PdM deployment velocity. MEMS accelerometer manufacturing scale, Bluetooth 5.0 Low Energy adoption, and low-power microcontroller advances have reduced wireless vibration sensor node costs from USD 1,200 in 2019 to USD 220 in 2026. Comprehensive coverage of a 400-asset manufacturing facility costs USD 88,000 in sensor hardware — recouped within three to six months of first prevented outage — crossing the SME adoption threshold and expanding the addressable market by 12 million additional facilities globally.

Government smart manufacturing policy creates structural public co-investment accelerating enterprise PdM adoption. Germany’s Industrie 4.0, Japan’s Connected Industries, China’s Made in China 2025, and the U.S. Manufacturing USA network collectively represent more than USD 18 billion in manufacturing digitalization investment.

Market Restraints

OT Cybersecurity Concerns, Legacy System Integration Complexity, and Workforce Skill Gaps Constrain Adoption

OT network security vulnerabilities represent the most impactful near-term market restraint through 2028. Connecting IIoT sensors to cloud analytics platforms requires bridging operational technology networks — historically air-gapped from internet connectivity — to IT infrastructure. The IEC 62443 industrial cybersecurity standard and NIST Cybersecurity Framework for operational technology provide compliance frameworks, but implementation requires 12 to 24 months of security architecture validation before enterprise-scale IIoT deployment can proceed.

Legacy SCADA, distributed control system, and plant historian infrastructure creates integration complexity that elevates deployment cost beyond initial capital estimates. Facilities with 20- to 30-year-old automation infrastructure running Modbus, Profibus, and vendor-specific DCS protocols require custom middleware for integration with modern OPC-UA and MQTT IIoT platforms. Integration projects for large petrochemical or power generation facilities regularly require 6 to 18 months of engineering engagement, adding USD 500,000 to USD 3 million in professional services cost to enterprise deployments.

Market Opportunities

SME Industrial Adoption, Renewable Energy PdM, and Generative AI Maintenance Assistants Unlock Premium Growth Segments

SME manufacturer PdM adoption is the largest underpenetrated opportunity segment through 2030. Companies with USD 5 million to USD 250 million in annual revenue represent 87% of global manufacturing establishments but less than 14% of current predictive maintenance software spend. PdM-as-a-service models — combining wireless sensor hardware rental, cloud analytics subscriptions, and remote monitoring services for fixed monthly fees of USD 2,000 to USD 8,000 per facility — are eliminating the capital expenditure barrier.

Renewable energy expansion creates a decade-long greenfield PdM opportunity. The IEA forecasts 5,400 gigawatts of new wind and solar capacity through 2030, with offshore wind delivering USD 15,000 to USD 45,000 in annual PdM service revenue per turbine. Total monitored power sector assets will grow from 2.4 million in 2026 to 11.8 million by 2035.

Generative AI integration with predictive maintenance is the most transformative near-term technology opportunity. Large language models integrated with asset historian data, maintenance records, and OEM technical documentation enable maintenance engineers to query complex failure histories in natural language. IBM Maximo Application Suite, ServiceNow Field Service Management, and SAP Asset Intelligence Network are actively integrating LLM capabilities that will fundamentally transform maintenance workflow automation through 2028.

AI & IIoT Integration Framework for Predictive Maintenance

Sensor Network Architecture, Data Pipeline Design, and AI Model Deployment Strategy for Industrial Asset Intelligence

Enterprise predictive maintenance deployments integrate four cohesive technology layers. The sensor layer — wireless vibration, temperature, acoustic emission, and current signature sensors — provides raw physical measurement streams from monitored assets. Sensor selection follows failure mode sensitivity: bearing defect detection requires frequency response to 10 kilohertz; rotor unbalance detection needs 1 to 10 kilohertz.

The edge computing layer aggregates sensor streams, applies Fast Fourier Transform and envelope analysis feature extraction, and executes pre-trained inference models without cloud latency. The cloud analytics layer ingests feature vectors, executes deep learning models for remaining useful life estimation and failure mode classification, and routes AI recommendations into CMMS work order management. Microsoft Azure IoT Hub processes more than 10 billion device messages daily; the full pipeline from sensor anomaly to maintenance recommendation completes within 2 to 8 minutes for non-safety-critical applications.

Model governance represents the capability gap most underestimated in enterprise PdM program design. AI models experience accuracy degradation — concept drift — as equipment ages or operating conditions shift. Enterprises establishing governance frameworks with defined accuracy thresholds, automated performance dashboards, and structured retraining pipelines sustain 90%+ prediction accuracy over multi-year deployments; those treating model deployment as a one-time project observe degradation within 12 to 24 months.

Smart Manufacturing ROI Framework for Predictive Maintenance

Total Cost of Ownership, Maintenance KPI Benchmarks, and AI Value Realization Economics for 2026–2035

For a mid-size manufacturing facility with 150 monitored rotating assets, three-year TCO ranges from USD 380,000 to USD 720,000 for cloud-based PdM-as-a-service, versus USD 520,000 to USD 1.1 million for a fully integrated on-premise deployment with dedicated engineering resources. Cloud SaaS economics favor facilities with limited OT engineering staff and variable asset utilization; on-premise economics favor high-criticality continuous process operations where cloud connectivity latency or availability risk is operationally unacceptable.

PdM ROI realization timelines vary significantly by industry and asset criticality profile. Manufacturing operations focused on high-speed packaging lines, injection molding presses, and CNC machining centers typically achieve measurable ROI within 6 to 12 months. Process industries carry higher per-failure consequences and larger maintenance budgets, generating ROI payback within 12 to 24 months. Offshore oil and gas — where a single prevented compressor failure generates USD 1 million to USD 8 million in avoided production loss and repair cost — delivers among the highest demonstrated PdM ROI.

Rigorous PdM ROI frameworks track five KPIs: MTBF improvement, unplanned downtime reduction, planned-to-unplanned maintenance ratio shift, spare parts inventory reduction, and labor productivity improvement. Mature PdM programs operating three or more years consistently show MTBF improvements of 35% to 60%, unplanned downtime reductions of 25% to 50%, and maintenance cost savings of 10% to 25% versus reactive baselines.

Digital Twin and Predictive Analytics Architecture

Real-Time Asset Simulation, Physics-AI Hybrid Models, and Remaining Useful Life Prediction for Industrial Equipment

Digital twin integration represents the most technically advanced tier of predictive maintenance intelligence, combining physics-based simulation models with real-time sensor data streams to generate asset-specific predictions that generic machine learning models cannot produce. A digital twin of a centrifugal compressor train integrates the thermodynamic performance model, rotor dynamics simulation, bearing load calculations, and seal leakage characteristics of the specific machine configuration. Siemens Simcenter Amesim, Ansys Twin Builder, and PTC Windchill Quality Solutions represent the leading commercial platforms.

Remaining Useful Life prediction is the highest-value capability enabled by digital twin architectures. Unlike binary fault detection, RUL prediction estimates the continuous time remaining before failure probability reaches an unacceptable level, enabling maintenance teams to schedule interventions during planned production windows days or weeks in advance. Aspentech Mtell has demonstrated RUL prediction accuracy within ±15% of actual failure time for refinery rotating equipment, enabling clients to operate assets beyond conservative time-based maintenance intervals. Condition-based extension of maintenance intervals reduces overall spare parts consumption by 18% to 32% and maintenance labor by 12% to 22% versus calendar-based replacement strategies.

Generative AI integrated with digital twin platforms is creating AI maintenance copilots that synthesize physics predictions, sensor anomaly alerts, maintenance history, and OEM technical bulletins into natural-language recommendations. Market adoption is projected to reach USD 4.8 billion in annual copilot-assisted maintenance platform revenue by 2030.

Latest Trends in the Predictive Maintenance Market

Generative AI Maintenance Assistants, Foundation Models for Industrial Time-Series, and Autonomous Maintenance Systems Reshape the PdM Landscape in 2026

Foundation models for industrial time-series data represent the defining AI architecture transition in predictive maintenance for 2026. Transformer-architecture models pre-trained on hundreds of millions of industrial sensor data sequences — vibration, temperature, current, pressure, and flow from rotating equipment across multiple industries — are enabling zero-shot anomaly detection on new asset types without historical failure data. IBM Research’s Industrial Foundation Model, Siemens’ SieberTwin AI, and startup Aqarios are demonstrating that foundation model transfer learning reduces the labeled failure data requirement from thousands of hours to tens of hours per new asset type.

Autonomous maintenance systems — integrating predictive AI with robotic inspection and self-optimizing operating setpoints — represent the leading edge of PdM evolution. ABB’s autonomous mine, Honeywell’s autonomous process plant pilot, and Siemens’ Autonomous Control program demonstrate facilities where AI anomaly detection triggers inspection drones and robotic maintenance arms. These programs project to USD 12.4 billion in autonomous maintenance revenue by 2035.

Recent Developments: IBM, Siemens, Augury, and Microsoft Lead 2025–2026

- April 2026: Microsoft announced Azure Predictive Maintenance 2.0 with native OpenAI GPT-4o integration, enabling natural-language maintenance queries against asset historian data and automatic work order generation from AI-detected anomalies across Azure IoT SiteWise deployments.

- February 2026: Augury closed a USD 180 million Series E round at USD 1.1 billion valuation, accelerating its machine health platform expansion into European and Asia-Pacific manufacturing markets with a declared target of 500,000 monitored machines by 2028.

- January 2026: Siemens launched Xcelerator PdM Plus, an integrated digital twin and AI analytics upgrade for Xcelerator industrial IoT platform customers, including pre-built digital twin templates for 340 rotating equipment asset categories covering motors, pumps, fans, compressors, and turbines.

- November 2025: IBM Maximo Application Suite 9.0 released with integrated generative AI maintenance assistant, achieving 94.7% alert accuracy in customer validation testing across 28 manufacturing and energy utility deployments covering 380,000 monitored assets.

- September 2025: GE Vernova announced Asset Performance Management cloud expansion covering 50,000 wind turbines globally, representing the single largest predictive maintenance deployment in renewable energy industry history by monitored asset count.

Competitive Landscape

Platform Concentration Among Industrial OEMs, Hyperscaler Cloud Expansion, and AI-Native Startup Disruption Define the PdM Market

The Predictive Maintenance competitive landscape is characterized by three competing dynamics. Industrial automation OEMs including Siemens, Emerson, Honeywell, and ABB leverage installed equipment relationships and proprietary sensor data access to command premium pricing for integrated hardware-software-services PdM bundles. Enterprise IT platform vendors including IBM, SAP, and Microsoft leverage existing enterprise software relationships to embed PdM capabilities within broader asset management and ERP platforms. AI-native PdM startups including Augury, SparkCognition, Uptake, and Aspentech’s Mtell compete on AI model accuracy, deployment speed, and SME accessibility.

Vertical integration is the defining competitive strategy among leading PdM participants through 2030. Siemens’ Xcelerator creates a unified IIoT and analytics stack from PLC to cloud. IBM’s Watson-Maximo integration embeds AI within the world’s most widely deployed industrial CMMS, reaching 6,000 enterprise customers. Emerson’s 2022 acquisition of AspenTech created the first combined process optimization and PdM platform — delivering 23% higher retention rates than single-capability competitors.

Key Market Segments

By Component

- AI & ML Software Platforms (Failure Prediction, Anomaly Detection, RUL Estimation)

- IIoT Sensor Hardware (Vibration, Thermal, Acoustic, Current, Ultrasonic)

- Managed PdM Services (Remote Condition Monitoring, Reliability Engineering)

- Edge Analytics & Industrial Gateway Infrastructure

By Deployment Mode

- Cloud (SaaS PdM Platforms, Industrial IoT Cloud Services)

- On-Premise (SCADA/DCS Integration, Air-Gapped Industrial Deployments)

- Hybrid (Edge + Cloud, OT/IT Converged Architecture)

- Edge AI (Real-Time Inference, 5G-Connected Smart Factory)

By Technology

- Artificial Intelligence and Machine Learning Analytics

- IIoT Sensor Networks and Wireless Condition Monitoring

- Digital Twin and Physics-Informed Simulation Platforms

- SCADA / CMMS / MES Integration Middleware

- Edge Computing and Industrial Gateway Platforms

By End-Use Industry

- Manufacturing (Discrete & Process Industry)

- Energy & Utilities (Power Generation, Wind, Solar, Grid)

- Oil & Gas (Upstream, Midstream, Downstream, Offshore)

- Transportation & Logistics (Rail, Aviation, Fleet Management)

- Mining & Metals

- Healthcare & Pharmaceuticals

- Chemical & Petrochemical

By Geography

- North America (United States, Canada)

- Asia-Pacific (China, Japan, South Korea, India, Australia)

- Europe (Germany, United Kingdom, France, Netherlands, Italy)

- Middle East & Africa (Saudi Arabia, UAE, South Africa)

- Latin America (Brazil, Mexico, Chile, Argentina)

Report Features

| Feature | Description |

|---|---|

| Market Value (2026) | USD 15.67 billion |

| Forecast Revenue (2035) | USD 96.61 billion |

| CAGR (2026–2035) | 22.4% |

| Base Year for Estimation | 2026 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Component Analysis, Deployment Economics, AI Technology Stack, IIoT Integration Framework, Smart Manufacturing ROI Framework, Digital Twin Architecture, Competitive Intelligence, Regional Analysis |

| Segments Covered | By Component, By Deployment Mode, By Technology, By End-Use Industry (8 sectors), By Geography (5 regions) |

| Regional Analysis | North America, Asia-Pacific, Europe, Middle East & Africa, Latin America with country-level data |

| Dominant Component | AI & ML Software Platforms with 42.3% revenue share |

| Dominant Deployment Mode | Cloud with 41.8% revenue share |

| Fastest-Growing Segment | Edge AI Analytics at 34.7% CAGR |

| Competitive Landscape | IBM, Siemens, Microsoft, Emerson, Honeywell, SKF, GE Vernova, Aspentech, Augury, PTC |