Executive Summary

Quick Insight: The global data center switch market is set to grow 3.1× by 2035, driven by hyperscaler AI fabric expansion, 400GbE and 800GbE port speed adoption, spine-leaf architecture proliferation, and open networking software decoupling.

The data center switch market is one of the most strategically significant segments of global networking infrastructure. This report delivers comprehensive analysis of market size, port speed adoption, architecture economics, end-user demand, vendor positioning, open networking disruption, AI workload requirements, and sustainability benchmarks for 2026–2035. It covers enterprise, colocation, hyperscaler, and telecom operators deploying switching infrastructure across spine-leaf, three-tier, and fat-tree architectures globally.

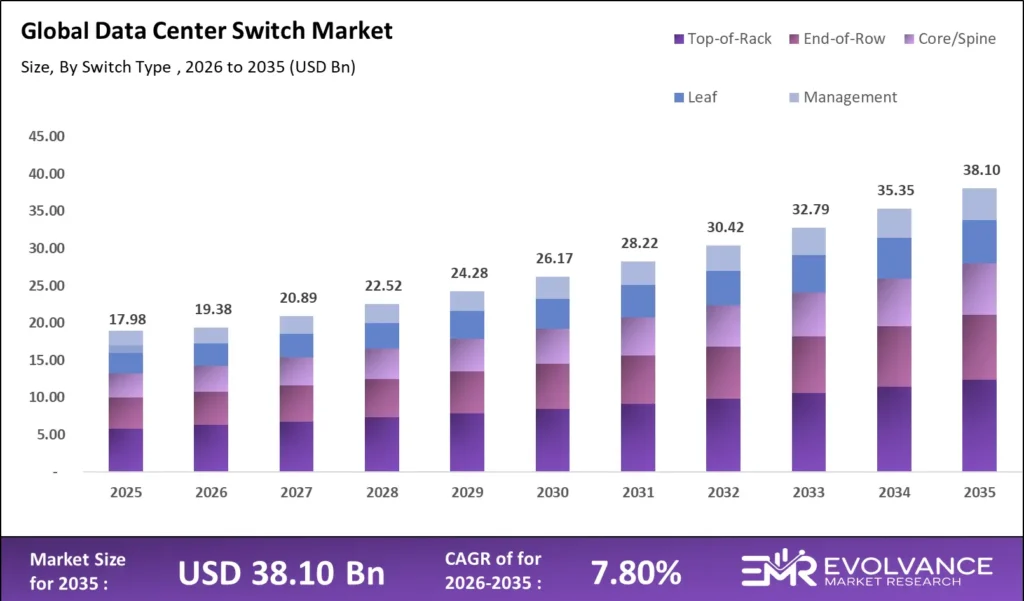

Key findings: The market reaches USD 19.38 billion in 2026, compounding at 7.80% CAGR to USD 38.10 billion by 2035. Cloud service providers account for 48.2% of total switch spending. 400GbE reaches 34.7% of new enterprise deployments. Spine-leaf represents 61.3% of net-new fabric deployments globally. AI and ML cluster infrastructure grows at 39.4% annually. Open networking reaches 22.8% of hyperscaler procurement by port count. Three new sections — AI Fabric Economics, Open Networking Framework, and Sustainability Standards — deliver differentiated intelligence.

What Is the Data Center Switch Market?

The data center switch market was valued at USD 19.38 billion in 2026 and is projected to reach USD 38.10 billion by 2035, growing at a CAGR of 7.80%. Ethernet switching forms the foundational packet-forwarding layer of every hyperscale campus, enterprise data center, colocation facility, and telecom core network. The market spans top-of-rack, leaf, spine, and purpose-built AI cluster switches. Rapid 400GbE and 800GbE migration, AI infrastructure build-out by AWS, Microsoft, Google, and Meta, and the structural shift to spine-leaf architectures are simultaneously expanding addressable market size and accelerating installed-base refresh.

The global data center network spans more than 10,000 hyperscale and large-scale enterprise facilities, with 340 hyperscale data centers operated by the five largest cloud providers. Ethernet switching accounts for 18% to 23% of total data center network hardware capital expenditure, rising proportionally in AI-optimized deployments where fabric bandwidth directly constrains GPU utilization. Port speed migration from 25GbE to 100GbE, 400GbE, and 800GbE is the primary hardware refresh driver, enabled by Broadcom Tomahawk and Marvell Teralynx ASIC generations delivering higher bandwidth per watt.The Data Center Switch Market is increasingly interconnected with the Data Center Cooling Market as AI-driven high-speed switches generate higher rack power density and heat output. Growing adoption of 400G/800G architectures is accelerating demand for liquid cooling and energy-efficient thermal management solutions globally.

Data Center Switch Market Highlights: Key Data at a Glance

- Market value: USD 19.38 billion in 2026, forecast to USD 38.10 billion by 2035 at 7.80% CAGR

- Dominant switch type: Leaf switches with 38.6% revenue share in spine-leaf fabric deployments

- Dominant port speed: 100GbE with 41.2% share of total switch port revenue, accelerating to 400GbE

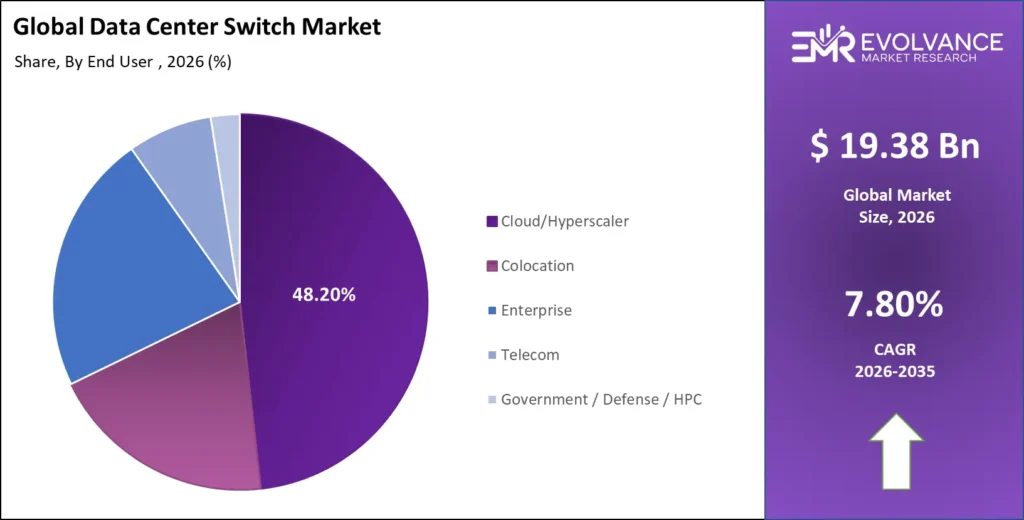

- Dominant end user: Cloud Service Providers and Hyperscalers with 48.2% of total switch spending

- Fastest-growing application: AI and ML Cluster Fabric Infrastructure at 39.4% annual growth rate

- Total data center switches shipped: Approximately 22 million units globally in 2026, up 14.2% year-over-year

- Leading silicon vendors: Broadcom (Tomahawk 5), Marvell (Teralynx 10), Intel (Tofino 3)

- Open networking adoption: 22.8% of hyperscaler switch procurement by port count in 2026

- Fastest-growing geography: Asia-Pacific at 18.7% CAGR, led by China, India, and Southeast Asia data center builds

- AI cluster switch fabric spend: USD 2.1 billion in 2026, projected to reach USD 11.4 billion by 2030

Market Overview: Why Data Center Switch Market Growth Is Accelerating

The data center switch market covers all revenue from Ethernet switching hardware, network operating system software, and switching ASICs deployed within data center network infrastructure. The market excludes WAN routing, telecom carrier access systems, and campus LAN switching outside data center perimeters. Understanding data center switch market growth requires examining four structural demand drivers: hyperscaler AI infrastructure investment, port speed migration, edge computing expansion, and sovereign cloud build-out.

The global hyperscaler construction cycle is accelerating: Microsoft committed USD 80 billion in data center investment in 2025, Amazon Web Services announced USD 100 billion for 2026, and Google committed USD 75 billion for 2025 expansion. Port speed migration from 10GbE to 100GbE and 400GbE drives full switch refresh cycles since mixed-speed fabrics bottleneck AI workloads. Edge computing and 5G expansion create net-new switching demand in distributed facilities independent of the core hyperscaler build cycle.

Switch Type Analysis

Leaf Switches Dominate with 38.6% Revenue Share

Spine-Leaf Fabric Architecture Displaces Three-Tier Hierarchy Across Hyperscale and Enterprise Data Centers

| Switch Type | Revenue Share % | Primary Deployment Driver |

|---|---|---|

| Leaf / ToR (Top-of-Rack) Switches | 38.6% | Spine-leaf fabric scale-out, server port density, 100GbE/400GbE server connectivity |

| Spine / Core Switches | 27.4% | High-radix 400GbE/800GbE fabric interconnect, ultra-low latency AI cluster backplane |

| Aggregation / Distribution Switches | 16.2% | Three-tier legacy enterprise refresh, hybrid multi-tier migration deployments |

| AI Cluster / Non-Blocking Fabric Switches | 11.3% | GPU cluster interconnect, RoCEv2/RDMA traffic, ultra-low latency AI training fabric |

| Out-of-Band Management Switches | 6.5% | 1GbE/10GbE dedicated management plane isolation, zero-trust network segmentation |

Leaf switches hold a 38.6% revenue share in 2026, driven by global adoption of spine-leaf fabric architectures as the dominant data center network design pattern. In a spine-leaf fabric, each leaf switch connects every server rack to every spine switch through a non-blocking Clos topology, eliminating oversubscription inherent in three-tier designs. The scale-out nature of spine-leaf means each new server row requires additional leaf switches, creating a proportional relationship between data center capacity growth and leaf switch unit shipments that sustains strong demand through 2035.

Spine switches represent 27.4% of market revenue and are the highest-ASP switch category, with high-radix 400GbE and 800GbE platforms from Cisco, Arista, and Juniper priced between USD 120,000 and USD 680,000 per chassis. AI cluster switches — a newly discrete category in 2026 — represent 11.3% of revenue but grow at 41.2% annually. Non-blocking AI cluster switches supporting RoCEv2 and RDMA-capable Ethernet for GPU-to-GPU communication are differentiated by sub-500-nanosecond latency requirements, adaptive routing, and specialized traffic management for AI collective communications.

Port Speed Analysis

100GbE Leads Revenue Share; 400GbE Is the Fastest-Growing Speed Tier

Port Speed Migration Curve Drives Switch Hardware Refresh and Silicon Revenue Growth Through 2035

| Port Speed | Revenue Share % | Average Selling Price (per port) | Growth Rate YoY |

|---|---|---|---|

| 10GbE | 8.4% | USD 18–USD 45 | -12.3% (declining) |

| 25GbE | 22.1% | USD 28–USD 72 | 4.2% |

| 100GbE | 41.2% | USD 85–USD 240 | 16.8% |

| 400GbE | 21.6% | USD 380–USD 920 | 47.3% |

| 800GbE / 1.6TbE | 6.7% | USD 740–USD 2,100 | 81.4% (emerging) |

100GbE maintains the largest port speed revenue share at 41.2% in 2026, reflecting its position as the mainstream server connectivity standard for enterprise data centers and mid-tier cloud deployments. Broadcom’s Tomahawk 4 ASIC enabled commodity 64-port 100GbE switches that have become the standard leaf platform for enterprise and colocation operators managing general-purpose workloads.

400GbE is the fastest-growing established port speed at 47.3% annual growth, driven by hyperscaler AI procurement and migration of HPC workloads from InfiniBand to Ethernet. Arista and Cisco’s Nexus 9000 with Broadcom Tomahawk 5 silicon delivered 128-port 400GbE switches at volume in 2025–2026, enabling hyperscalers to build fabrics for multi-thousand-GPU AI training clusters. The 800GbE tier posts 81.4% annual growth, with volume hyperscaler deployment expected by 2028 and enterprise adoption by 2030–2031.

End-User Segment Analysis

Cloud Service Providers and Hyperscalers Command 48.2% of Total Switch Spending

Enterprise Refresh Cycles and Colocation Build-Out Define Mid-Market Switching Demand Through 2035

| End-User Segment | Revenue Share % | Avg. Switch Refresh Cycle | Primary Port Speed |

|---|---|---|---|

| Cloud Service Providers / Hyperscalers | 48.2% | 3–4 years | 400GbE / 800GbE |

| Colocation Data Center Operators | 19.6% | 5–7 years | 100GbE / 400GbE |

| Enterprise Data Centers | 22.4% | 6–8 years | 25GbE / 100GbE |

| Telecom / ISP / Carrier | 7.3% | 7–10 years | 100GbE / 400GbE |

| Government / Defense / HPC | 2.5% | 5–8 years | 100GbE / InfiniBand |

Cloud service providers and hyperscalers are the dominant end-user segment at 48.2% of total switch revenue. The five largest hyperscalers — AWS, Microsoft Azure, Google Cloud, Meta, and Alibaba Cloud — collectively operate more than 250 hyperscale campuses and represent a combined switching procurement budget of USD 5.9 billion in 2026. Hyperscaler procurement is characterized by high-volume standards-based purchasing, multi-year vendor agreements, and increasing open networking adoption combining disaggregated white-box hardware with SONiC, reducing dependency on proprietary NOS from Cisco, Arista, and Juniper.

Enterprise data centers represent 22.4% of market revenue, characterized by longer refresh cycles of six to eight years, lower port speed adoption versus hyperscalers, and stronger reliance on integrated hardware-software solutions from established vendors. Enterprise switching decisions prioritize operational simplicity, vendor support, and existing infrastructure compatibility over raw port density and lowest unit cost — characteristics favoring Cisco, Arista, and Juniper with broad portfolio depth.

Network Architecture Analysis

Spine-Leaf Fabric Represents 61.3% of Net-New Data Center Deployments

Fat-Tree Topology Scales for Ultra-Large AI Clusters While Three-Tier Legacy Migration Sustains Enterprise Refresh Demand

| Architecture | Deployment Share % | Primary Use Case | Dominant Vendor |

|---|---|---|---|

| Spine-Leaf (Clos Network) | 61.3% | Hyperscale cloud, enterprise refresh, colocation scale-out | Arista, Cisco, Juniper |

| Three-Tier (Core-Aggregation-Access) | 24.1% | Legacy enterprise, campus data center integration | Cisco, HPE Aruba, Dell |

| Fat-Tree / Dragonfly (AI Clusters) | 10.2% | AI/ML GPU cluster fabrics, HPC interconnect | NVIDIA, Arista, Cisco |

| Two-Tier Collapsed Core | 4.4% | Small enterprise, branch office, edge deployments | Cisco Meraki, Juniper EX |

Spine-leaf architecture accounts for 61.3% of net-new data center fabric deployments in 2026. Its advantages over three-tier designs are significant: uniform any-to-any latency between servers, linear scale-out by adding spine-leaf pairs, elimination of Spanning Tree Protocol dependencies, equal-cost multi-path routing, and higher bandwidth efficiency per dollar. These advantages compound at scale, making spine-leaf disproportionately favorable for hyperscale operators while also delivering meaningful operational and economic benefits for mid-market enterprise operators managing facilities above 500 server racks.

Regional Analysis of the Data Center Switch Market

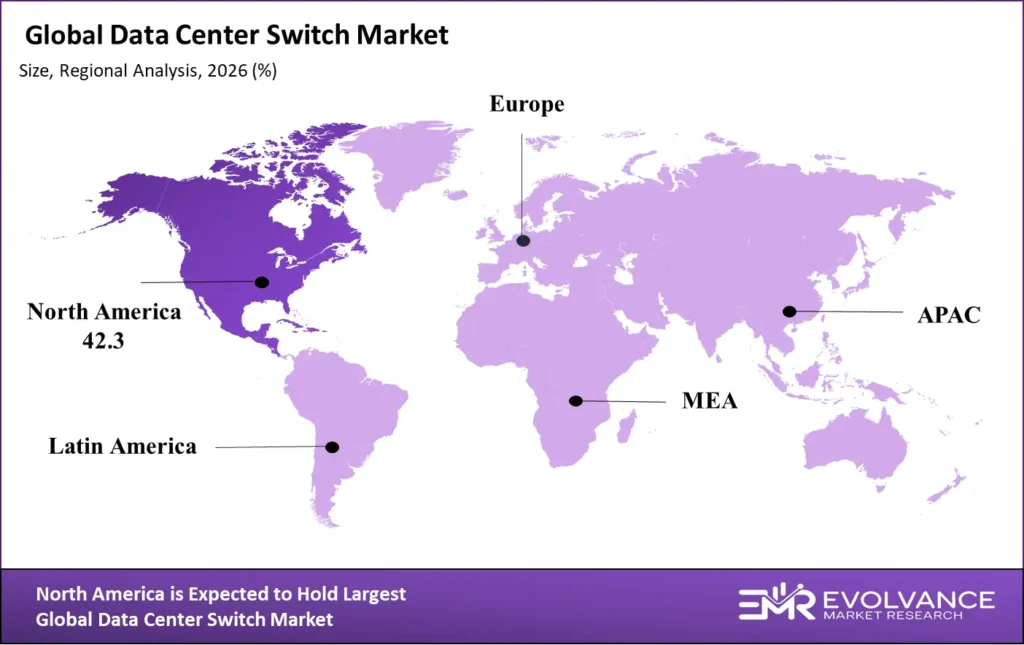

North America Leads Global Switch Revenue; Asia-Pacific Is the Fastest-Growing Region

| Region | Revenue Share % | 2026–2035 CAGR | Key Driver |

|---|---|---|---|

| North America (U.S. / Canada) | 42.3% | 12.8% | Hyperscaler AI capex, Northern Virginia and Phoenix mega-campuses, AWS/Azure/Google expansion |

| Asia-Pacific (China, India, SEA, Japan, ANZ) | 28.7% | 18.7% | China cloud sovereignty build, India data center boom, SEA hyperscaler campus expansion |

| Europe (Germany, UK, Ireland, Netherlands) | 18.4% | 11.4% | GDPR-driven sovereign cloud, Amsterdam and Frankfurt carrier-neutral hub growth |

| Latin America (Brazil, Mexico, Chile) | 6.2% | 16.3% | Brazil hyperscaler entry, Mexico near-shoring data center demand |

| Middle East & Africa (UAE, Saudi Arabia, South Africa) | 4.4% | 21.6% | Saudi Vision 2030 data center investment, UAE smart city infrastructure, Microsoft and Google ME expansion |

North America holds the largest regional share at 42.3% of global revenue, anchored by the United States as the world’s largest hyperscale data center market. Northern Virginia represents an estimated 32% of U.S. data center power capacity and is the primary deployment geography for AWS, Azure, and Google Cloud eastern facilities. Phoenix has emerged as the second-largest U.S. hyperscale campus market. Tier-2 markets — Columbus, Atlanta, and Salt Lake City — are accelerating as hyperscalers diversify geographic risk, deploying 400GbE fabrics as the baseline AI campus specification.

Asia-Pacific is the fastest-growing region at 18.7% CAGR through 2035. India’s data center capacity is projected to triple between 2026 and 2030, supported by data localization mandates, rapid cloud adoption, and hyperscaler commitments including Microsoft’s USD 3 billion and Google’s USD 2 billion India investments. Middle East and Africa leads at 21.6% CAGR, propelled by Saudi Arabia’s Vision 2030 programs and the UAE’s position as the leading MENA data center hub.

Key Companies: Vendors Defining the Data Center Switch Competitive Landscape

The data center switch market is defined by six primary hardware vendors, two dominant silicon providers, and an emerging layer of open networking and white-box ODM participants. Cisco, Arista, Juniper, Huawei, HPE Aruba, and Dell collectively account for approximately 74% of market revenue. Broadcom and Marvell control an estimated 86% of merchant silicon in data center switches, giving their ASIC roadmaps outsized influence over industry-wide port speed migration and power efficiency trajectories.

| Company | Market Position | Key Differentiator | 2026 Revenue Est. |

|---|---|---|---|

| Cisco Systems | Market Leader (28.4% share) | Nexus 9000 series, ACI SDN fabric, Silicon One custom ASIC integration | USD 3.52B (DC Switching) |

| Arista Networks | Fast Challenger (22.1% share) | EOS open network OS, CloudVision management, 7800R AI cluster switches | USD 2.74B (DC Switching) |

| Juniper Networks / HPE | Established Challenger (11.6%) | QFX spine-leaf portfolio, Apstra intent-based networking, Junos OS | USD 1.44B (DC Switching) |

| Huawei Technologies | APAC Leader (9.8% global) | CloudEngine series, dominant China market, 1.6TbE roadmap leadership | USD 1.21B (DC Switching) |

| Dell Technologies / OEM | White-Box Channel (7.3%) | PowerSwitch portfolio, SONiC integration, open networking ODM channel | USD 0.91B (DC Switching) |

| Broadcom Inc. | Silicon Dominant (ASIC) | Tomahawk 5 (51.2Tbps), Trident 4, Jericho 3 — 86% merchant silicon share | ASIC revenue est. USD 4.1B |

Cisco Systems maintains the largest revenue share at 28.4%, supported by its Nexus 9000 series, ACI SDN platform, and proprietary Silicon One ASIC designed to reduce Broadcom dependency on high-end spine platforms. Arista Networks holds 22.1% share and is the fastest-growing major vendor, expanding from its hyperscaler stronghold into enterprise through CloudVision. Arista’s 7800R series AI cluster switches — optimized for GPU cluster RoCEv2 traffic — position it as a primary AI infrastructure cycle beneficiary through 2030.

Key Growth Drivers of the Data Center Switch Market

AI Infrastructure Investment, Port Speed Migration, and Hyperscaler Capacity Expansion Drive Data Center Switch Market Structural Demand

The generative AI infrastructure investment cycle is the most powerful demand driver in the data center switch market’s history. AI training clusters generate concentrated, high-value switch procurement at every fabric layer. A 10,000-GPU cluster requires approximately 3,200 leaf switch ports at 400GbE and 320 spine ports at 800GbE — USD 12 million to USD 38 million in hardware per cluster. Microsoft’s plan to deploy more than 1.8 million GPUs by 2026 implies a multi-billion-dollar annual switching demand increment attributable to AI workloads alone.

Port speed migration is a structurally predictable demand driver. Each generation triggers a full hardware refresh because mixed-speed fabrics bottleneck AI workload performance. Silicon cost curves for each new speed tier decline approximately 35% to 45% per year following volume ramp, driving mainstream adoption three to five years after introduction and enterprise deployment five to seven years after hyperscaler adoption.

Data Center Switch Market Restraints

Supply Chain Concentration, Open Networking Commoditization, and Power Constraints Moderate Data Center Switch Market Growth

Silicon supply chain concentration is the primary structural vulnerability in the market’s growth trajectory. Broadcom’s estimated 86% merchant silicon share creates systemic risk from supply disruptions, export control complications, or pricing leverage in vendor negotiations. U.S. export controls expanded in 2023–2024 to include certain networking ASICs above performance thresholds, creating regulatory complexity for vendors selling into Chinese hyperscaler markets — a segment representing 12% to 18% of total global switch demand by value.

Open networking and white-box adoption introduces commoditization pressure on proprietary switch vendors. As hyperscalers combine commodity white-box hardware with SONiC, the price premium commanded by integrated solutions from Cisco and Arista is compressed. Power density constraints also present a moderation factor — 800GbE switches consume substantially more power than 100GbE platforms, and legacy facilities with power densities below 10kW per rack require infrastructure upgrades before deploying next-generation high-bandwidth switching at full port density.

Data Center Switch Market Opportunities

Edge Computing, Sovereign Cloud, and AI Inference Infrastructure Unlock Premium Data Center Switch Market Growth Segments

Edge computing infrastructure expansion is a structurally new demand source independent of the hyperscale AI cluster cycle. The 5G edge market is projected to require more than 1.2 million edge switching deployments globally between 2026 and 2030 — a cumulative hardware opportunity of USD 3.8 billion. Sovereign cloud development represents a high-value market opportunity in Europe, the Middle East, India, and Southeast Asia, where governments are investing in cloud infrastructure legally isolated from U.S. hyperscaler operations. AI inference infrastructure distributed from centralized training clusters adds a third high-growth opportunity across a geographically dispersed installation base.

AI and Machine Learning Cluster Switch Fabric Infrastructure

GPU Cluster Interconnect Economics and Switch Fabric Architecture Requirements for Large-Scale AI Workloads

AI Infrastructure Switch Spending Projected to Reach USD 11.4 Billion by 2030, Representing the Fastest-Growing Sub-Segment in Data Center Networking

AI and ML cluster switch fabric infrastructure is the most rapidly expanding sub-segment of the data center switch market, growing at 39.4% annually and projected to reach USD 11.4 billion by 2030. Large-scale AI training workloads — characterized by all-reduce and all-to-all collective communication between thousands of GPUs — impose unique switch fabric requirements. Standard Ethernet switches are suboptimal for AI collective communications, which require ultra-low deterministic latency, adaptive load balancing across equal-cost paths, RoCEv2 protocol support, and lossless switching under sustained all-to-all traffic.

A large-scale AI cluster switch fabric follows a fat-tree or modified Clos topology providing full bisection bandwidth between all GPU servers. Achieving full bisection bandwidth for a 10,000-GPU cluster at 400GbE per GPU requires approximately 3,200 leaf switches plus 400 spine switches — a hardware investment of USD 280 million to USD 620 million. NVIDIA’s InfiniBand Quantum-2 and Arista’s 7800R are the primary platforms in AI training clusters in 2026, with Cisco’s Nexus 9000 competitive for inference workloads requiring enterprise network integration.

The economic case for optimized AI cluster switch fabric is quantifiable. GPU utilization efficiency is directly proportional to switch fabric bandwidth and latency. A 400GbE fabric at 98% bisection bandwidth efficiency enables GPU utilization of 82% to 91% for LLM training, versus 68% to 74% on a 100GbE fabric. At USD 30,000 to USD 40,000 per GPU, a 10-percentage-point utilization gain translates to USD 9 million to USD 14 million in annual savings for a 1,000-GPU cluster.

Open Networking and White-Box Switch Adoption Framework

Disaggregated Switch Hardware and Open-Source NOS Drive Hyperscaler Cost Reduction and Vendor Independence

Open Networking Adoption Reaches 22.8% of Hyperscaler Switch Procurement by Port Count in 2026, Projected to Reach 41% by 2031

Open networking — the disaggregation of switch hardware from network operating system software — is the most significant long-term competitive disruption in the data center switch market. The traditional value proposition combined proprietary hardware, ASICs, and NOS from a single vendor. Open networking separates these layers: commodity white-box hardware from ODMs using Broadcom or Marvell silicon is combined with SONiC, OpenConfig-compatible software, or commercial open NOS products. This disaggregation enables hyperscalers to achieve unit costs 35% to 55% below equivalent proprietary solutions while gaining NOS customization flexibility.

Microsoft’s SONiC — open-sourced in 2016 — runs across an estimated 14 million switch ports at Azure globally as of 2026. Google operates its Jupiter network fabric management system; Meta deploys FBOSS across its global infrastructure. The ecosystem has attracted substantial investment: Delta Electronics, Edgecore Networks, Celestica, and Wistron NeWeb Corporation are the leading white-box ODMs, shipping an estimated 2.8 million white-box units annually in 2026.

Proprietary switch vendors are responding with hybrid strategies embracing SONiC compatibility and open APIs while defending value through advanced software and management platforms open networking cannot yet replicate. Arista’s EOS supports SONiC management interfaces and open-source telemetry, enabling it to serve both open-networking hyperscalers and integrated-solution-preferring enterprises from a unified platform.

Sustainability and Power Efficiency Standards in Data Center Switching

Power Usage Effectiveness, Energy Star Certification, and EU Energy Efficiency Directive Shape 2026–2035 Switch Procurement

Power Efficiency Per Terabit of Switch Bandwidth Is the New Primary Procurement KPI for Hyperscale and Regulated Enterprise Data Center Operators

Sustainability and power efficiency are now primary procurement criteria, driven by hyperscaler carbon neutrality commitments, EU Energy Efficiency Directive compliance, and AI-driven power density challenges. The data center sector consumes 1.5% to 2.0% of global electricity production, projected to reach 3.5% to 5.0% by 2030. Switch infrastructure accounts for 8% to 14% of total facility power consumption. Microsoft (carbon negative by 2030), Google (24/7 carbon-free by 2030), and AWS (net-zero by 2040) formally evaluate switch power efficiency as a primary procurement criterion alongside performance and cost.

The primary efficiency metric is watts per terabit of switching bandwidth. Broadcom’s Tomahawk 5 achieves approximately 0.68 watts per terabit — a 42% improvement over Tomahawk 4’s 1.18 watts per terabit — driven by 5-nanometer process technology and power management innovations. Marvell’s Teralynx 10 delivers 0.71 watts per terabit. Deploying Tomahawk 5-based spine switches across a 10,000-server facility saves approximately 1.4 megawatts of continuous power. The EU’s Energy Efficiency Directive, effective 2027 for facilities above 500 kilowatts, mandates PUE reporting and minimum efficiency standards accelerating switch refresh cycles.

Liquid cooling integration with high-density switch chassis is accelerating in 2026. Direct liquid cooling allows high-density chassis to operate at full port capacity while reducing cooling energy consumption by 30% to 45%. Liquid-cooled switch chassis adoption is projected to reach 18% of new hyperscale deployments by 2028 and 34% by 2031.

Latest Trends in the Data Center Switch Market

800GbE Commercialization, Co-Packaged Optics, and SONiC Ecosystem Expansion Reshape 2026 Market Dynamics

The commercialization of 800GbE switching is the most significant technology transition of 2026 in data center networking. Broadcom’s Tomahawk 5 and Marvell’s Teralynx 10 ASICs deliver 51.2 terabits per second per chip — sufficient for a 64-port 800GbE switch at full line rate. Arista Networks announced its 7800R4 series 800GbE AI cluster switches at OCP Global Summit 2025, with hyperscaler deployments beginning Q1 2026. The 800GbE transition is proceeding faster than the prior 100GbE-to-400GbE shift due to AI cluster demand pull eliminating typical adoption hesitation.

Co-packaged optics — integrating optical transceivers directly into switch ASIC packages rather than pluggable modules — is advancing to early commercial deployment in 2026. Co-packaged optics reduce optical interconnect power by 50% to 70% versus pluggable transceiver solutions and eliminate the bandwidth bottleneck constraining pluggable performance at 800GbE and beyond. Microsoft and Intel Foundry Services announced a collaboration in November 2025 targeting volume production readiness in 2027.

Recent Developments: Cisco, Arista, and Broadcom Lead 2025–2026

- April 2026 — Arista Networks reported Q1 2026 revenue of USD 2.1 billion, with data center switching accounting for 91% of total revenue and AI-driven backlog growing to USD 8.4 billion. CEO Jayshree Ullal confirmed that 400GbE spine switches now represent more than 60% of new order volume, with 800GbE systems entering commercial availability.

- February 2026 — Broadcom announced Tomahawk 6 silicon roadmap targeting 102.4 terabits per second switching capacity per chip in 2028, enabling 128-port 800GbE and 64-port 1.6TbE switch configurations. The announcement triggered competitive ASIC roadmap acceleration from Marvell and Intel Foundry.

- January 2026 — Cisco Systems launched Nexus 9808 with Silicon One G202 ASIC, delivering 736 ports of 400GbE in a single chassis. The platform targets AI cluster spine infrastructure and represents Cisco’s most direct competitive response to Arista’s 7800R AI switching family.

- November 2025 — Microsoft and Edgecore Networks expanded their white-box SONiC deployment agreement, with Microsoft committing to procure 1.2 million white-box switch ports annually through 2028 across Azure global regions. The agreement is the largest single open networking procurement commitment in industry history by port count.

- September 2025 — Marvell Technology introduced Teralynx 10, a 5-nanometer ASIC delivering 12.8 terabits per chip with industry-leading 0.71 watts per terabit efficiency. Initial production customers include three unnamed Tier-1 hyperscalers deploying the platform in 2026 AI cluster expansion programs.

Competitive Landscape

Market Concentration at the Vendor Layer and Silicon Layer Defines Competitive Dynamics Through 2035

The data center switch market is characterized by moderate concentration at the integrated vendor layer and high concentration at the silicon layer. Cisco, Arista, and Juniper collectively hold approximately 62.1% of global switch revenue, while Broadcom and Marvell control an estimated 86% of merchant silicon deployed in data center switches globally. This dual concentration creates structural dynamics where silicon vendor ASIC roadmaps largely determine the pace of innovation, while integrated vendors compete primarily on software capabilities, management platform differentiation, and total cost of ownership.

Competitive intensity is increasing simultaneously across multiple levels. Open networking pressures hardware margins for proprietary integrated switch vendors. AI cluster fabric requirements create a high-growth sub-segment where Arista and NVIDIA Networking’s early leadership attracts responses from Cisco and new InfiniBand-to-Ethernet entrants. Vendors defending proprietary value through software differentiation and AI-optimized hardware will maintain premium positioning through 2035; those relying solely on hardware margin face sustained compression from open networking commoditization.

Key Market Segments

By Switch Type

- Leaf / Top-of-Rack Switches

- Spine / Core Switches

- Aggregation / Distribution Switches

- AI Cluster / Non-Blocking Fabric Switches

- Out-of-Band Management Switches

By Port Speed

- 10GbE

- 25GbE

- 100GbE

- 400GbE

- 800GbE / 1.6TbE

By Architecture

- Spine-Leaf (Clos Network)

- Three-Tier (Core-Aggregation-Access)

- Fat-Tree / Dragonfly (AI/HPC Clusters)

- Two-Tier Collapsed Core

By End User

- Cloud Service Providers / Hyperscalers

- Colocation Data Center Operators

- Enterprise Data Centers

- Telecom / ISP / Carrier Networks

- Government / Defense / HPC

By Application

- AI and Machine Learning Cluster Fabric

- Cloud Computing and Virtualization

- Big Data Analytics and Distributed Computing

- High-Performance Computing (HPC)

- Content Delivery Network (CDN) Infrastructure

By Geography

- North America (United States, Canada)

- Europe (Germany, United Kingdom, Ireland, Netherlands, Nordics)

- Asia-Pacific (China, India, Japan, Singapore, Southeast Asia, Australia)

- Latin America (Brazil, Mexico, Chile, Colombia)

- Middle East and Africa (UAE, Saudi Arabia, South Africa)

Report Features

| Feature | Description |

|---|---|

| Market Value (2026) | USD 19.38 billion |

| Forecast Revenue (2035) | USD 38.10 billion |

| CAGR (2026–2035) | 7.8% |

| Base Year for Estimation | 2026 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Port Speed Migration Analysis, Switch Architecture Economics, AI Cluster Fabric Deep Dive, Open Networking Adoption Framework, Sustainability Standards, End-User Segment Analysis, Regional Intelligence, Competitive Landscape, Silicon Vendor ASIC Roadmap Analysis |

| Segments Covered | By Switch Type, By Port Speed, By Architecture, By End User (5 segments), By Application, By Geography |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa with country-level data |

| Dominant Switch Type | Leaf / ToR Switches with 38.6% revenue share |

| Dominant Port Speed | 100GbE with 41.2% revenue share, 400GbE fastest-growing |

| Dominant End User | Cloud Service Providers / Hyperscalers with 48.2% of market spending |

| Competitive Landscape | Cisco, Arista, Juniper/HPE, Huawei, Dell, Broadcom, Marvell, Edgecore, Delta Electronics, Celestica, Wistron NWC |

| New Analytical Sections | AI Cluster Switch Fabric Economics, Open Networking Adoption Framework, Sustainability and Power Efficiency Standards |