Executive Summary

Quick Insight: The global data center cooling market is set to nearly triple by 2035, driven by surging artificial intelligence infrastructure investments, rapid liquid cooling and immersion cooling adoption, and hyperscale data center expansion across North America and Asia-Pacific. Advanced thermal management has become a board-level capital priority — defining which cloud providers, colocation operators, and enterprise IT organizations can deploy next-generation AI compute infrastructure at full scale and efficiency.

This report delivers comprehensive analysis of market size, cooling technology evolution, component demand dynamics, competitive positioning, energy efficiency mandates, investment flows, and regional growth patterns for 2026–2035. Coverage spans every data center cooling segment — from precision air conditioning and computer room air handlers to advanced direct liquid cooling, two-phase immersion cooling, rear-door heat exchanger systems, and free cooling economization infrastructure.

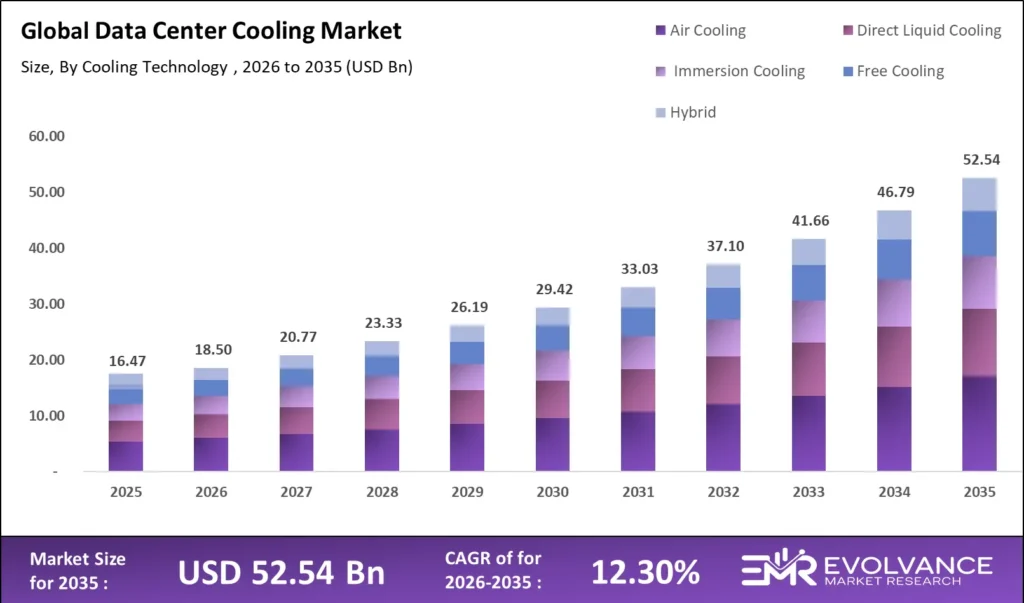

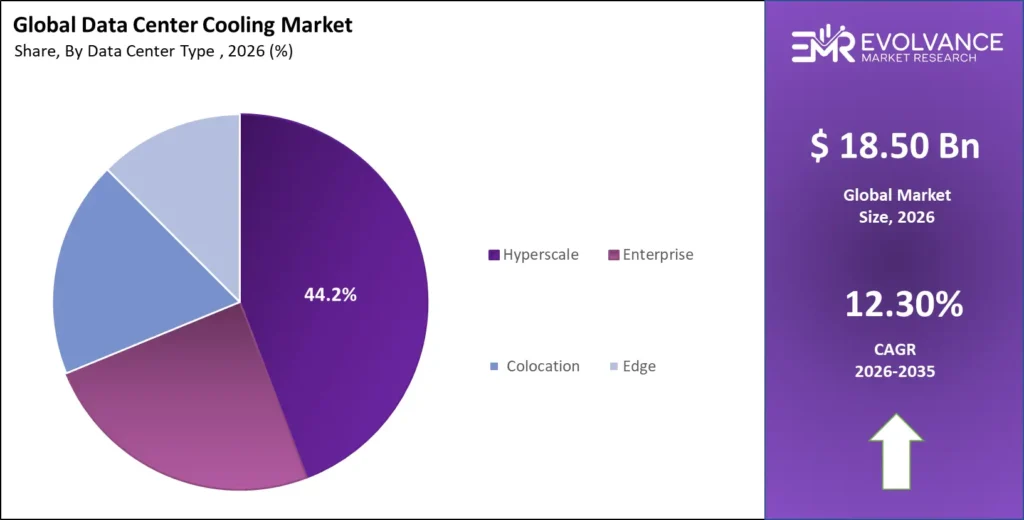

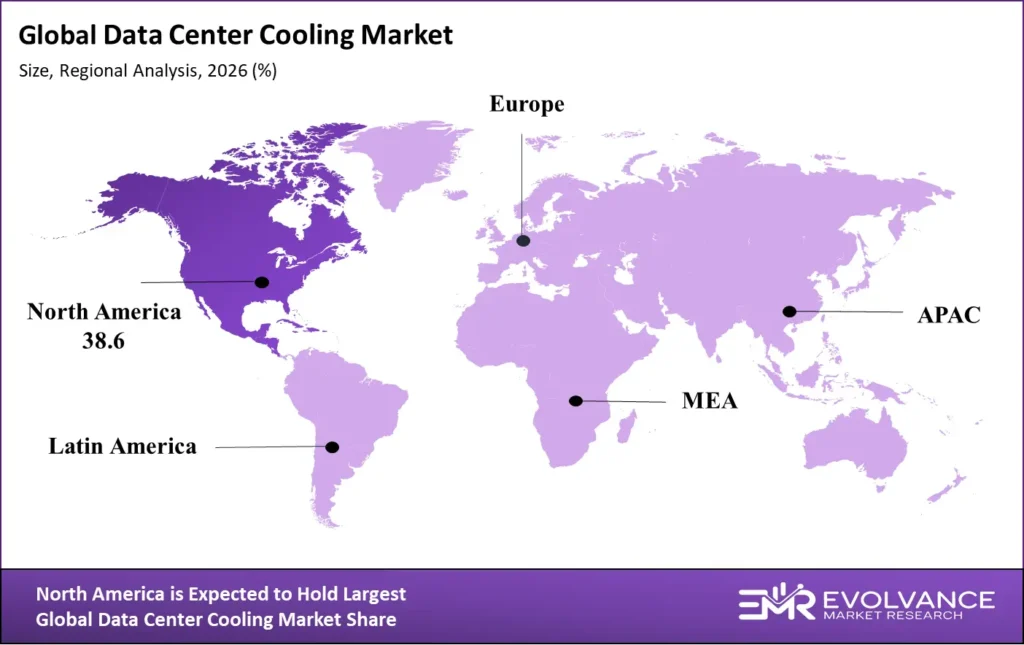

Key findings: The market reaches USD 18.5 billion in 2026, compounds at a 12.3% CAGR, and reaches USD 52.54 billion by 2035. Liquid cooling grows at 24.7% CAGR; immersion cooling at 32.4% CAGR. Hyperscale data centers command 44.2% of end-use cooling revenue. North America leads at 38.6% regional share. Asia-Pacific grows fastest at 15.8% CAGR. AI GPU servers generating 350–1,000 watts per accelerator make advanced data center cooling systems technically mandatory for AI compute deployments.

What Is the Data Center Cooling Market?

The data center cooling market was valued at USD 18.5 billion in 2026 and is projected to reach USD 52.54 billion by 2035 at a CAGR of 12.3%. Escalating compute density requirements from AI infrastructure, generative AI training workloads, and GPU cluster deployments drive structural demand globally. AI-optimized servers — including NVIDIA H100, H200, and Blackwell GPU configurations — generate 350 to 1,000 watts per accelerator, making traditional air-based cooling architectures insufficient for next-generation AI workloads.

The market encompasses all thermal management equipment, systems, and services within data center facilities globally — from computer room air conditioners and precision cooling units to immersion cooling tanks, direct liquid cooling distribution systems, rear-door heat exchangers, and monitoring infrastructure. Services and maintenance represent an additional USD 4.2 billion in annual recurring revenue.

Data Center Cooling Market Highlights: Key Data at a Glance

- Market value: USD 18.5 billion in 2026, forecast to USD 52.54 billion by 2035 at 12.3% CAGR

- Dominant cooling technology: Air Cooling with 54.8% revenue share in 2026

- Fastest-growing technology: Liquid Cooling at 24.7% CAGR; Immersion Cooling at 32.4% CAGR through 2035

- Dominant data center type: Hyperscale with 44.2% end-use revenue share

- Fastest-growing data center type: Edge data centers at 19.3% CAGR

- Dominant end-user vertical: Cloud Service Providers with 36.8% revenue share

- Largest regional market: North America with 38.6% revenue share

- Fastest-growing region: Asia-Pacific at 15.8% CAGR

- Key thermal challenge: AI rack power densities reaching 40–80 kW per rack, exceeding air cooling design limits

- Leading companies: Vertiv, Schneider Electric, Emerson Electric, Stulz, Rittal, Trane Technologies, Motivair, Iceotope

Market Overview: Why Data Center Cooling Market Growth Is Accelerating

The data center cooling market is accelerating due to a fundamental shift in compute architecture that conventional air cooling cannot efficiently address. Average rack power density increased from 8.4 kW per rack in 2020 to 14.2 kW in 2026. In hyperscale AI training clusters, rack densities have reached 40 to 80 kW — with NVIDIA DGX H100 SuperPOD configurations exceeding 100 kW per rack. The IEA projects global data center electricity consumption will exceed 1,000 terawatt-hours annually by 2030, up from 460 TWh in 2022.

Sustainability commitments create a parallel demand driver independent of compute density growth. Microsoft targets carbon negative by 2030, Google targets 24/7 carbon-free energy by 2030, and Amazon Web Services targets net-zero by 2040. Meeting these targets while expanding compute infrastructure requires radical improvements in data center cooling energy efficiency throughout the forecast period.

Cooling Technology Analysis

Air Cooling Holds 54.8% Share While Liquid Cooling Emerges as the Structural Disruptor

Immersion Cooling, Direct Liquid Cooling, and Free Cooling Architecture Gaining Rapid Data Center Adoption

| Cooling Technology | Share % | CAGR 2026–35 | Primary Driver |

|---|---|---|---|

| Air Cooling (CRAC/CRAH/In-Row) | 54.8% | 5.2% | Installed base maintenance, enterprise refresh, edge deployments |

| Direct Liquid Cooling (Cold Plate / Rear-Door) | 19.4% | 24.7% | AI GPU cluster cooling, OCP spec adoption |

| Immersion Cooling (Single-Phase / Two-Phase) | 8.3% | 32.4% | Extreme density AI workloads, HPC clusters |

| Free Cooling & Economization Systems | 11.2% | 9.8% | PUE optimization, EU Energy Efficiency Directive |

| Hybrid Cooling (Air + Liquid) | 6.3% | 18.6% | Enterprise AI workload insertion, brownfield retrofits |

Air cooling holds 54.8% of data center cooling market revenue in 2026, driven by the massive global installed base of enterprise data centers built on precision air conditioning infrastructure between 2000 and 2022. Computer room air conditioners and handlers remain dominant for facilities operating below 15 kW per rack, creating an estimated USD 10.1 billion annual market in replacement and maintenance. Air cooling’s 5.2% CAGR significantly lags the overall market rate of 12.3%, reflecting structural share loss to liquid and immersion alternatives.

Direct liquid cooling is the highest-growth mainstream data center cooling technology at 24.7% CAGR through 2035. Major cloud providers have standardized direct liquid cooling across next-generation AI data center designs. Google’s TPU v5 clusters, Microsoft’s Azure AI infrastructure, and Meta’s AI Research SuperCluster all deploy rear-door heat exchangers or cold plate systems as primary thermal management. The OCP Liquid Cooling Specification Version 2.0, adopted by 68% of hyperscale operators by 2026, is accelerating vendor standardization and reducing integration risk for enterprise operators.

Immersion cooling is the fastest-growing technology at 32.4% CAGR, driven by AI training clusters, high-performance computing, and compelling total cost of ownership economics at extreme density. Single-phase systems submerge servers in dielectric fluid at 25–45°C, enabling rack densities of 200–400 kW per tank. Two-phase systems use fluorocarbon fluids achieving near-zero heat rejection overhead. Immersion-cooled facilities achieve PUE of 1.03–1.06 versus 1.35–1.58 for air-cooled equivalents, representing a 30–45 percent energy cost reduction.

Component Analysis

Chillers and Precision Cooling Units Lead Data Center Cooling Component Revenue

Liquid Cooling Distribution Units Are the Highest-Growth Component at 28.7% Projected Share by 2035

| Component | Share % | Key Growth Driver |

|---|---|---|

| Precision Cooling Units (CRAC/CRAH/In-Row) | 28.4% | Enterprise refresh cycles and edge data center additions |

| Chillers (Air-Cooled and Water-Cooled) | 24.6% | Hyperscale centralized chilled water plant infrastructure |

| Cooling Towers & Dry Coolers | 16.8% | Water-side economization and hyperscale campus cooling loops |

| Liquid Cooling Distribution Units (CDU) | 14.2% | AI GPU cluster liquid cooling and hyperscale buildouts |

| Air Handling Units & Containment Systems | 10.1% | Hot-aisle/cold-aisle containment and airflow optimization |

| Economizers & Free Cooling Infrastructure | 5.9% | Climate-advantaged site PUE optimization programs |

Precision cooling units hold the largest component revenue share at 28.4%, reflecting the global installed base of air-cooled data center infrastructure. The global installed base exceeded 4.2 million units in 2026, with North America and Western Europe representing 61% of installed capacity. Chiller plants hold the second-largest share at 24.6%, as hyperscale data centers deploy centralized chilled water plant infrastructure connecting cooling towers, chillers, distribution units, and server-level heat exchangers through closed-loop systems serving campus-wide AI cooling loads.

Liquid cooling distribution units are the highest-growth component, expanding from 14.2% revenue share in 2026 to a projected 28.7% by 2035. Vendors including Vertiv, Schneider Electric, and Motivair supply units managing 100–1,000 kW thermal loads per rack row. OCP standardization is reducing installation complexity and shortening commissioning timelines across enterprise and colocation deployments.

Data Center Type Analysis

Hyperscale Facilities Command 44.2% of Data Center Cooling Market Revenue

Edge Data Centers Are the Fastest-Growing Segment at 19.3% CAGR Through 2035

| Data Center Type | Share % | CAGR | Primary Cooling Requirement |

|---|---|---|---|

| Hyperscale (Cloud Providers, AI Infrastructure) | 44.2% | 14.8% | Direct liquid cooling, immersion cooling, advanced chiller plant |

| Enterprise (On-Premise IT Facilities) | 24.6% | 6.4% | Precision air cooling refresh, hybrid liquid cooling for AI |

| Colocation (Multi-Tenant Data Centers) | 18.7% | 11.2% | Liquid-ready infrastructure, density upgrades for AI tenants |

| Edge (Telecom, Retail, Healthcare Sites) | 12.5% | 19.3% | Compact precision cooling, passive and hybrid cooling |

Hyperscale data centers hold 44.2% data center cooling market revenue share in 2026, consuming the largest cooling capital per facility of any data center type globally. A single 200 MW campus requires cooling plant investment exceeding USD 280 million. AWS, Microsoft Azure, and Google Cloud collectively added more than 22 gigawatts of new data center capacity between 2024 and 2026, the majority designed for liquid cooling readiness. Microsoft’s Stargate program commits USD 500 billion to AI data center infrastructure through 2029.

Colocation data centers represent the most strategically important transitional segment through 2035. Equinix, Digital Realty, and NTT are retrofitting facilities for AI tenant liquid cooling while designing all new construction for full liquid cooling readiness. Equinix’s xScale AI campus program commits USD 15 billion to hyperscale-capable colocation facilities.

Edge data centers are the fastest-growing type at 19.3% CAGR, driven by 5G network rollouts, retail and healthcare deployments, and autonomous vehicle compute requirements demanding geographically distributed micro-facility cooling solutions.

End-User Vertical Analysis

Cloud Service Providers Drive 36.8% of Data Center Cooling Market Revenue

BFSI, Healthcare, and Government Verticals Accelerate Liquid Cooling Adoption Through 2035

| End-User Vertical | Share % | Key Cooling Driver |

|---|---|---|

| Cloud Service Providers (AWS, Azure, GCP) | 36.8% | AI compute expansion, direct liquid cooling, capital-intensive buildouts |

| Telecom & IT Infrastructure Operators | 18.4% | 5G edge compute cooling, central office refresh, network densification |

| Banking, Financial Services & Insurance | 14.2% | High-density algorithmic trading, GPU analytics clusters |

| Government & Defense Agencies | 11.6% | Classified compute upgrades, data sovereignty, sovereign AI programs |

| Healthcare & Life Sciences | 10.3% | Medical imaging AI, clinical data processing, HIPAA infrastructure |

| Retail, Manufacturing & Others | 8.7% | Edge compute cooling, IoT data processing, operational technology |

Cloud service providers represent 36.8% of global data center cooling market revenue, driven by capital expenditure intensity exceeding every other end-user category. Amazon Web Services invested approximately USD 86 billion in infrastructure capital expenditure in 2025, with thermal management representing 12–18 percent of facility construction costs. Microsoft Azure’s capital expenditure reached USD 56 billion in fiscal year 2025 and Google Cloud exceeded USD 52 billion. The combined hyperscale investment of approximately USD 194 billion in 2025 establishes cloud providers as the dominant cooling demand source through 2035.

BFSI data centers operate some of the highest rack density environments outside hyperscale, with algorithmic trading and GPU analytics workloads requiring direct liquid cooling at JPMorgan Chase, Goldman Sachs, Barclays, and equivalent global financial institutions.

Regional Analysis of the Data Center Cooling Market

North America Leads with 38.6% Revenue Share; Asia-Pacific Is the Fastest-Growing Region at 15.8% CAGR

| Region | Share % | CAGR | Key Driver |

|---|---|---|---|

| North America (U.S., Canada) | 38.6% | 11.8% | Hyperscale AI expansion, liquid cooling adoption, Stargate investment |

| Europe (UK, Germany, Netherlands, Nordics) | 26.4% | 10.2% | EU Energy Efficiency Directive compliance, free cooling advantage |

| Asia-Pacific (China, Japan, Singapore, India) | 24.8% | 15.8% | Cloud expansion, government digital infrastructure, AI investments |

| Middle East & Africa (UAE, Saudi Arabia) | 6.4% | 14.2% | Vision 2030 digital infrastructure, sovereign AI programs |

| Latin America (Brazil, Mexico) | 3.8% | 12.6% | Cloud market development, enterprise digitization, colocation expansion |

North America holds the largest data center cooling market revenue share at 38.6% in 2026. Northern Virginia — the world’s largest data center cluster — consumed more than 3.5 gigawatts of IT load in 2025 across approximately 280 operational facilities, creating consistent procurement demand for precision cooling units, chilled water plant infrastructure, and liquid cooling distribution systems. The USD 500 billion Stargate AI initiative and U.S. federal Executive Order on AI Infrastructure signed January 2025 are accelerating domestic data center construction.

Europe is the second-largest data center cooling market at 26.4% revenue share, driven by GDPR-mandated data localization, EU Green Deal sustainability mandates, and the free cooling advantage across Nordic and Central European climates. The EU Energy Efficiency Directive mandates large data centers above 1 MW to report PUE, water usage effectiveness, and carbon usage effectiveness from 2024.

Asia-Pacific is the fastest-growing regional market at 15.8% CAGR, driven by China’s AI infrastructure expansion, India’s Digital India program projecting 1,600 MW of new capacity between 2026 and 2028, and Saudi Arabia’s USD 37 billion Vision 2030 digital infrastructure commitment.

Key Companies: Vendors Defining the Data Center Cooling Competitive Landscape

Eight global vendors dominate data center cooling infrastructure supply based on cooling technology breadth, software integration, and service network depth. Liquid cooling specialists — Iceotope Technologies, GRC Green Revolution Cooling, and Submer Technologies — are gaining market share against established HVAC incumbents.

| Company | HQ | Key Product Lines | 2026 Market Position |

|---|---|---|---|

| Vertiv Holdings | Columbus, OH, USA | Liebert CRAC/CRAH, liquid cooling CDUs, thermal software | Global market leader; largest data center thermal management revenue |

| Schneider Electric | Rueil-Malmaison, France | APC Precision Cooling, EcoStruxure IT, chilled water systems | #2 globally; strongest software-defined cooling management platform |

| Emerson Electric (Nidec) | St. Louis, MO, USA | Liebert DSE/DM Series precision cooling, CRAC/CRAH | Strong North American and European enterprise data center position |

| Stulz GmbH | Hamburg, Germany | CyberAir CRAC, DX and chilled water precision systems | European precision cooling market leader by installed base |

| Rittal GmbH & Co. KG | Herborn, Germany | Cooling units, liquid cooling infrastructure, IT room solutions | Strong SMB and enterprise IT data center presence globally |

| Trane Technologies | Dublin, Ireland | Chiller plants, free cooling systems, building controls | Hyperscale chiller plant deployments specialist globally |

| Motivair Corporation | Buffalo, NY, USA | Liquid cooling distribution units, immersion cooling systems | Fastest-growing liquid cooling specialist vendor globally |

| Iceotope Technologies | Sheffield, UK | Precision immersion cooling modules, chassis-level liquid cooling | Leading AI data center immersion cooling innovation vendor |

Vertiv maintains the leading global data center cooling market position, with revenue exceeding USD 4.1 billion from thermal management products and services in 2025. The Vertiv CoolChip direct liquid cooling system and full distribution unit portfolio make it the broadest-product-line vendor globally, with operating margin expanding from 12.4% to 16.8% in 2025 as liquid cooling demand consistently outstrips supply capacity. Schneider Electric’s EcoStruxure IT platform monitors more than 80,000 data center facilities globally, enabling automated cooling optimization through machine learning setpoint management.

Key Growth Drivers of the Data Center Cooling Market

AI Infrastructure Investment, Rack Density Escalation, and Sustainability Mandates Drive Structural Long-Term Expansion

The single most powerful demand driver in the data center cooling market is artificial intelligence infrastructure investment. NVIDIA’s Blackwell B200 GPU generates 1,000 watts of thermal output per accelerator, and a full DGX SuperPOD generates approximately 457 kW within a single rack row — making liquid cooling technically mandatory for operational deployment. Goldman Sachs estimates AI-driven data center power demand will grow 160% between 2023 and 2030. Cloud provider capital expenditure exceeding USD 300 billion annually by 2026 provides unprecedented forward demand visibility for data center cooling market vendors.

Regulatory sustainability mandates create a second structural demand pillar. The EU Energy Efficiency Directive Article 12 requires data centers above 1 MW to report PUE, carbon usage effectiveness, and water usage effectiveness from January 2024. California AB 1054 mandates data center energy reporting in 2026, with New York, Virginia, and Texas advancing equivalent requirements.

Market Restraints

High Liquid Cooling Capital Costs and Water Scarcity Constraints Limit Data Center Cooling Market Expansion Velocity

High capital costs present the primary liquid cooling adoption barrier. A direct liquid cooling retrofit of an existing 1 MW data center requires USD 1.8 to USD 3.4 million in capital, with a 4 to 7 year energy-savings payback exceeding many enterprise approval thresholds. Two-phase immersion cooling systems cost USD 250,000 to USD 750,000 per tank, with dielectric fluid replacement costs of USD 40,000 to USD 120,000 per maintenance cycle.

Water scarcity constrains data centers relying on evaporative cooling towers. A 100 MW hyperscale facility consumes 1.5 to 3.5 million gallons of water daily. Drought conditions in Arizona, Nevada, and Texas — three major data center markets — are creating regulatory pressure for water use restrictions through 2030.

Market Opportunities

AI Inference Liquid Cooling Retrofits, Emerging Market Greenfield Development, and Modular Edge Cooling Unlock Premium Revenue Segments

AI inference liquid cooling retrofits represent a significant growth opportunity independent of AI training investment. Inference infrastructure is distributed across thousands of enterprise and colocation facilities lacking liquid cooling capability. McKinsey estimates AI inference will account for 70% of total AI compute demand by 2030, creating a retrofit market exceeding USD 8 billion annually across enterprise and colocation segments.

Emerging market greenfield data center development provides high-growth opportunities for cooling vendors. India, Indonesia, Malaysia, Brazil, and Saudi Arabia are commissioning significant new capacity, and the ASEAN digital infrastructure market requires USD 40 billion in new data center investment through 2030.

AI-Driven Thermal Management and Smart Cooling Intelligence Framework

Machine Learning Optimization Reduces Data Center Cooling Energy Consumption by 15 to 40 Percent

The integration of artificial intelligence and machine learning into data center cooling management is one of the most impactful operational efficiency opportunities in the contemporary market. Google’s DeepMind-developed AI cooling optimization system, expanded significantly through 2025, demonstrated a 40% reduction in cooling energy consumption and 15% overall data center power usage improvement in published peer-reviewed results. The system continuously optimizes chiller plant sequencing, cooling tower fan speeds, and precision cooling unit airflow by processing thousands of temperature sensor data points, workload patterns, and weather forecast inputs.

Vertiv’s Thermal Advisor platform, Schneider Electric’s EcoStruxure IT Expert, and Nlyte Software’s DCIM suite each incorporate machine learning models providing predictive thermal risk alerts, cooling capacity planning, and automated setpoint adjustments. Predictive management prevents hotspot development, reducing unplanned cooling capacity requirements by 22–34 percent while maintaining server inlet temperatures within ASHRAE A1-class thermal design envelopes. Data center operators deploying AI-driven thermal management report average PUE improvements of 0.08–0.22 within 18 months, generating energy cost savings of USD 180,000–640,000 annually per 10 MW of managed IT load.

Digital twin platforms from Cadence Design Systems, 6SigmaDC, and Ansys create physics-accurate CFD models enabling operators to test cooling changes virtually before physical implementation. Microsoft and Equinix mandate digital twin cooling analysis for all new data center designs above 20 MW. AI thermal management is projected to represent a USD 3.8 billion annual software market by 2030.

Power Usage Effectiveness Optimization and Energy Efficiency Benchmarking

PUE Improvement from 1.58 to 1.10 Reduces Annual Energy Costs by USD 2.4 Million per 10 MW Data Center Facility

Power Usage Effectiveness (PUE) is the primary energy efficiency metric for data center operations and the most directly actionable driver of cooling infrastructure investment decisions globally. PUE measures total facility energy divided by IT equipment energy, with a theoretical minimum of 1.0. The global average data center PUE improved from 1.58 in 2022 to 1.46 in 2026 per the Uptime Institute Global Data Center Survey, reflecting hot-aisle and cold-aisle containment adoption, economizer deployment, and cooling setpoint optimization. Hyperscale AI facilities average 1.10–1.18; legacy enterprise data centers average 1.82–2.14.

A 10 MW data center at PUE 1.58 spends approximately USD 9.7 million annually on facility power, with USD 3.5 million representing cooling overhead. Improving PUE to 1.20 reduces annual energy cost to USD 7.4 million — saving USD 2.3 million annually — with a typical capital investment payback period of 2.5 to 4 years for the cooling infrastructure upgrades required.

The Green Grid Association’s 2026 Data Center Efficiency Report benchmarks PUE by facility type and the EU Energy Efficiency Directive mandates a recommended target of PUE 1.30 by 2027 for all European data center operators above 1 MW, creating structured procurement demand throughout the forecast period.

Sustainability, Carbon Neutrality, and Green Cooling Compliance Standards

Net-Zero Data Center Operations Require Advanced Cooling Architecture, Renewable Integration, and Water Use Minimization

Sustainability has become a primary data center cooling procurement criterion rather than a secondary environmental consideration. The Science Based Targets initiative requires participating corporations — including the majority of Fortune 500 companies operating enterprise data centers — to align data center energy efficiency with 1.5 degrees Celsius Paris Agreement targets, creating board-level compliance pressure that translates into capital allocation for advanced cooling infrastructure. A data center at PUE 1.20 rather than 1.58 reduces carbon emissions by approximately 240 metric tons of CO2 per year per megawatt.

Water Usage Effectiveness has emerged as the second critical sustainability metric. Closed-loop liquid cooling eliminates evaporative water consumption entirely. Adiabatic pre-cooling reduces water use by 60–80 percent. Microsoft, Google, and Equinix each pledged to replenish more water than their global data center operations consume by 2030.

The EU Corporate Sustainability Reporting Directive mandates data center energy consumption and PUE disclosure for large enterprises from 2024. ENERGY STAR, LEED, and ISO 50001 certifications are increasingly required in enterprise data center procurement RFPs as of 2025 and 2026.

SWOT Analysis of the Data Center Cooling Market

Strengths, Weaknesses, Opportunities, and Threats Shaping the Global Data Center Cooling Market Through 2035

| SWOT Factor | Details |

|---|---|

| Strengths | Structural AI-driven demand; established global vendor supply chains; proven liquid cooling ROI at scale; deep OEM server integration expanding addressable market |

| Weaknesses | High liquid cooling capital costs limiting enterprise adoption; skilled technician scarcity; dielectric fluid supply chain dependencies; limited immersion cooling interface standardization |

| Opportunities | AI inference retrofit market across existing enterprise facilities; emerging market greenfield construction; edge cooling expansion; AI thermal management software revenue streams |

| Threats | Water scarcity regulations threatening evaporative cooling viability; hyperscale self-design reducing commercial addressable market; supply chain disruptions; alternative compute architectures |

The dominant strength of the data center cooling market is the structural inevitability of demand. Data center cooling expenditure is non-discretionary — every operational data center generates heat that must be managed, and every new AI GPU deployment mandates corresponding cooling infrastructure investment. This creates a market floor that persists through economic cycles. The transition from air to liquid cooling creates an additional growth layer above the maintenance baseline, estimated at 1.8 times the replacement market size by 2030.

The most significant threat to commercial data center cooling market growth is hyperscale self-design. Google’s custom TPU cooling systems, Microsoft’s proprietary immersion tanks, and Meta’s custom rear-door heat exchangers are developed in-house rather than procured commercially, reducing the directly addressable market within these facilities. However, hyperscale innovation creates technology transfer that benefits vendors positioned to productize validated approaches for enterprise and colocation customers through OCP and Green Grid technical working groups.

Investment Landscape and Capital Flow in the Data Center Cooling Market

Venture Capital, Private Equity, and Strategic Investment Accelerate Liquid Cooling Innovation and Market Consolidation Through 2035

The data center cooling market attracted unprecedented levels of venture capital, private equity, and strategic corporate investment between 2023 and 2026. Total disclosed investment in data center cooling technology companies exceeded USD 2.8 billion globally in 2025, nearly doubling the USD 1.5 billion invested in 2023. Immersion cooling companies attracted the largest startup investment share, with Iceotope Technologies, GRC Green Revolution Cooling, and Submer Technologies collectively raising more than USD 380 million in disclosed funding rounds between 2023 and 2026.

Private equity investment in data center cooling infrastructure services is accelerating as investors recognize recurring revenue characteristics of managed cooling contracts. Brookfield Infrastructure Partners, Blackstone, and KKR each made material investments in data center services businesses with significant cooling infrastructure components between 2024 and 2026.

Strategic corporate investment is accelerating through acquisitions and technology partnerships. Emerson Electric’s minority investment in Iceotope Technologies, Schneider Electric’s Motivair commercial rights agreements, and Vertiv’s joint development agreements with NVIDIA and AMD exemplify consolidation reshaping the data center cooling landscape.

Latest Trends in the Data Center Cooling Market

Liquid Cooling Standardization, AI Chip Density Escalation, and Modular Cooling Solutions Reshape Data Center Infrastructure Procurement

Liquid cooling standardization through the Open Compute Project is accelerating enterprise and colocation adoption beyond hyperscale pioneers. The OCP Liquid Cooling Specification Version 2.0, published in 2025, defines rack-level liquid delivery standards, manifold connection interfaces, and leak detection requirements enabling interoperability between server hardware from Dell, HPE, Supermicro, and Lenovo and cooling distribution infrastructure from Vertiv, Schneider Electric, and Motivair. Adoption in new enterprise data center designs expanded from 14% in 2024 to a projected 38% by 2027.

Rear-door heat exchangers are gaining rapid acceptance as a bridge technology enabling liquid cooling without full facility retrofit. Rack-mounted heat exchanger matrices capture 60–80 percent of server exhaust heat, enabling 20–40 kW rack densities without chilled water plant upgrades at 40–55 percent lower capital cost than full direct liquid cooling deployments.

Recent Developments: Hyperscale Investment, Liquid Cooling Expansion, and Regulatory Advancement in 2025–2026

- March 2026: Vertiv announced strategic partnerships with NVIDIA and six hyperscale cloud providers to supply direct liquid cooling for Blackwell GPU data center deployments, covering more than 50,000 liquid cooling distribution units through 2028.

- February 2026: Schneider Electric launched EcoStruxure IT Advisor 4.0 with generative AI-powered thermal risk prediction processing 48-hour forward-looking cooling capacity projections, achieving 94% accuracy across 120 beta data center sites.

- January 2026: Microsoft’s Stargate AI program broke ground on its first dedicated AI training campus in Abilene, Texas, featuring 100% direct liquid cooling for NVIDIA GPU clusters, a PUE target of 1.12, and a USD 2.4 billion cooling investment.

- November 2025: The European Commission published the Data Center Sustainability Assessment Framework defining mandatory PUE, water usage effectiveness, and renewable energy benchmarks for EU data centers above 500 kW, with compliance deadlines of January 2028.

- September 2025: Iceotope Technologies raised USD 80 million in Series C funding led by Emerson Electric and Microsoft Climate Innovation Fund to scale precision immersion cooling manufacturing for AI data center deployments globally.

Competitive Landscape

Market Concentration at the Equipment Layer, Fragmentation at Software and Specialist Levels in 2026

The data center cooling competitive landscape is characterized by concentration among established HVAC vendors at the precision cooling equipment layer, and rapid fragmentation among liquid cooling specialists, software-defined thermal management platforms, and modular cooling vendors targeting emerging liquid and immersion segments. Vertiv, Schneider Electric, and Emerson Electric collectively hold approximately 54% of the traditional precision cooling market by revenue. Liquid cooling procurement decisions increasingly favor specialized vendors with hyperscale-validated deployments, attracting more than USD 2.8 billion in venture and strategic capital investment between 2023 and 2026.

Competitive moats in data center cooling infrastructure deepen on three structural dimensions: technology leadership in liquid and immersion cooling creates first-mover advantages; global service network reach enables single-vendor managed agreements across colocation operators spanning dozens of countries; and software platform integration with DCIM systems creates data-driven switching costs.

Vendors actively participating in OCP and Green Grid technical working groups gain advance knowledge of emerging thermal management standards that enterprise customers will require within 18–36 months of hyperscale adoption, creating a valuable commercialization pipeline for enterprise and colocation cooling solutions.

Key Market Segments

By Cooling Technology

- Air Cooling (CRAC, CRAH, In-Row Precision Cooling Systems)

- Direct Liquid Cooling (Cold Plate Systems, Rear-Door Heat Exchangers)

- Immersion Cooling (Single-Phase Dielectric, Two-Phase Fluorocarbon)

- Free Cooling and Economization (Air-Side, Water-Side Economizers)

- Hybrid Cooling Systems (Integrated Air and Liquid Cooling Architecture)

By Component

- Precision Cooling Units (CRAC, CRAH, In-Row Systems)

- Chillers (Air-Cooled Chillers, Water-Cooled Chillers)

- Cooling Towers and Dry Coolers

- Liquid Cooling Distribution Units and Manifold Systems

- Air Handling Units, Economizers, and Free Cooling Infrastructure

By Data Center Type

- Hyperscale Data Centers (Cloud Providers, AI Training Facilities)

- Enterprise On-Premise Data Centers

- Colocation and Multi-Tenant Data Center Facilities

- Edge Data Centers and Micro-Data Centers

By End-User Vertical

- Cloud Service Providers (AWS, Microsoft Azure, Google Cloud)

- Telecom and IT Infrastructure Operators

- Banking, Financial Services and Insurance (BFSI)

- Government and Defense Agencies

- Healthcare and Life Sciences Organizations

By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

Report Features

| Feature | Description |

|---|---|

| Market Value (2026) | USD 18.5 billion |

| Forecast Revenue (2035) | USD 52.54 billion |

| CAGR (2026–2035) | 12.3% |

| Base Year for Estimation | 2026 |

| Historic Period | 2020–2025 |

| Forecast Period | 2026–2035 |

| Report Coverage | Market Size, Cooling Technology, Component Breakdown, DC Type Segmentation, End-User Verticals, Regional Forecast, AI Thermal Management, PUE Optimization, Green Cooling Compliance, SWOT Analysis, Investment Landscape, Competitive Intelligence |

| Segments Covered | By Cooling Technology, By Component, By Data Center Type, By End-User Vertical, By Region |

| Regional Analysis | North America, Europe, Asia-Pacific, Middle East & Africa, Latin America |

| Dominant Technology (2026) | Air Cooling with 54.8% revenue share |

| Fastest-Growing Technology | Immersion Cooling at 32.4% CAGR through 2035 |

| Dominant Region | North America with 38.6% revenue share |

| Fastest-Growing Region | Asia-Pacific at 15.8% CAGR |

| Competitive Landscape | Vertiv, Schneider Electric, Emerson Electric, Stulz, Rittal, Trane Technologies, Motivair, Iceotope, GRC, Submer Technologies |