What is the Sustainable Aviation Fuel (SAF) Market Size?

The Global Sustainable Aviation Fuel (SAF) Market size will be worth around USD 4,026.74 Billion by 2035 from USD 23.47 Billion in 2025, growing at a CAGR of 67.2% during the forecast period 2026 to 2035. Mandatory blending targets in the EU, UK, and ICAO net-zero mandates are pushing airlines to lock in long-term SAF supply contracts. Buyers are shifting from spot purchases to multi-year offtake agreements, signaling a move from trial adoption to strategic fuel planning. Supply-side risks remain acute, as only 30% of announced SAF production capacity was completed by end of 2025.

Market Highlights

- The Global Sustainable Aviation Fuel (SAF) Market is set to grow from USD 23.47 Billion in 2025 to USD 4,026.74 Billion by 2035, at a CAGR of 67.2%.

- North America leads the market with a 43.2% share, valued at USD 10.1 Billion in 2025.

- By Fuel Type, Biofuel dominates with a 67.3% share.

- By Platform Type, Commercial Aviation leads with 54.2%.

- By Capacity, the Above 100 MW segment holds 37.3%.

- By Feedstock, Used Cooking Oil leads at 47.2%.

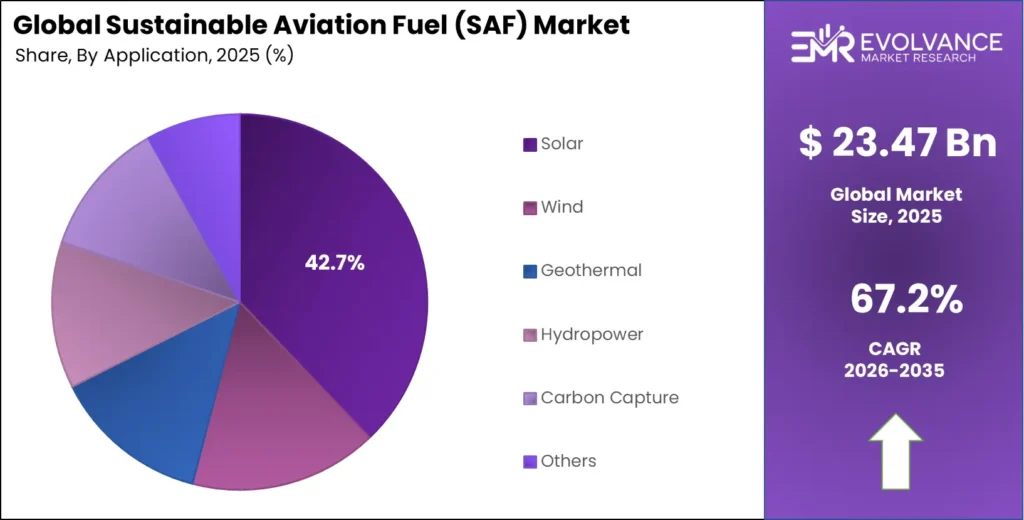

- By Application, Solar leads at 42.7%.

Market Overview

Sustainable Aviation Fuel (SAF) refers to drop-in jet fuel produced from non-petroleum sources, including used cooking oil, agricultural residues, municipal waste, and synthetic feedstocks. SAF is chemically equivalent to conventional jet fuel, requiring no changes to aircraft engines or airport fuel systems. It can be blended at ratios up to 50% with conventional Jet A-1 under current ASTM D7566 certification standards.

The SAF market sits at the intersection of aviation decarbonization and industrial energy transition. Airlines face binding emissions targets under the ICAO Carbon Offsetting and Reduction Scheme (CORSIA) and regional mandates that make SAF procurement non-optional. This converts what was once a voluntary green purchase into a compliance-driven procurement decision, which changes the entire demand structure for suppliers and investors.

The Sustainable Aviation Fuel (SAF) Market is gaining momentum as airlines and governments focus on reducing aviation carbon emissions. Advanced fuel production technologies increasingly rely on renewable feedstocks, green hydrogen integration, and bio-based chemical processes to improve SAF efficiency and scalability. Growing investments in green chemistry solutions and bio-based esters are further supporting the development of low-carbon aviation fuel infrastructure.

According to the European Union Aviation Safety Agency (EASA), SAF delivered at EU airports in 2024 achieved approximately 91% lower lifecycle emissions than fossil jet fuel, saving 714,000 tonnes of CO₂e. This data confirms that SAF’s environmental benefit is real and measurable — not theoretical — which is critical for airlines reporting under ESG frameworks and facing investor scrutiny.

SAF accounted for about 0.6% of total global jet fuel consumption in 2025, with production reaching approximately 1.9 million tonnes. This low share against a high production ramp signals that demand is growing faster than supply can scale at competitive prices, creating a structural opening for producers who can deliver cost-efficiently at scale. Cathay Pacific’s SAF use grew by 430% year-over-year in 2025, reaching 36,242 tonnes — a signal that airline uptake is accelerating faster than supply-side capacity.

Fuel Type Insights

Biofuel dominates with 67.3% due to mature feedstock supply chains and proven certification.

In 2025, Biofuel held a dominant market position in the By Fuel Type segment of the Sustainable Aviation Fuel (SAF) Market, with a 67.3% share. Biofuels — particularly HEFA-derived SAF — lead because they use existing lipid feedstocks, require no major process changes, and are already certified under ASTM D7566.

HEFA (Hydroprocessed Esters and Fatty Acids) is the dominant production pathway within the biofuel category. HEFA yields an average of 62% SAF from feedstock inputs and converts lipids with less energy than competing processes. The UK Government confirmed that HEFA-based SAF can supply 100% of SAF demand under its 2025–2026 mandate, confirming HEFA’s commercial readiness at scale.

Fischer-Tropsch (FT) SAF offers the lowest lifecycle emissions among certified pathways. FT-SAF achieves just 1.7 kg CO₂e per gallon, compared to HEFA’s maximum of 8.1 kg CO₂e per gallon. FT SAF is better suited for airlines with deep sustainability targets, but high capital costs for FT gasification plants have slowed commercial deployment versus HEFA’s lower setup burden.

Alcohol-to-Jet (ATJ) SAF expands the feedstock base to agricultural residues and purpose-grown energy crops. ATJ offers flexibility in sourcing but faces scrutiny over crop-based pathways — the ICCT confirmed that corn grain ATJ may achieve near-zero GHG reduction versus fossil jet fuel. This finding limits ATJ’s appeal in markets where lifecycle emissions verification is mandatory, pushing developers toward waste-based ATJ feedstocks.

Power-to-Liquid (PtL) Fuel — also called eSAF — uses renewable electricity, green hydrogen, and captured CO₂ to produce synthetic SAF. Genvia, and Hinicio, a Fischer-Tropsch eSAF plant using SOEC co-electrolysis achieves 49% overall energy efficiency and cuts electricity consumption by 31% versus conventional alkaline electrolysis. PtL is still pre-commercial at scale, but SOEC advances are lowering the cost curve faster than expected.

Platform Type Insights

Commercial Aviation dominates with 54.2% due to regulatory mandates and fleet-scale fuel volumes.

In 2025, Commercial Aviation held a dominant market position in the By Platform Type segment of the Sustainable Aviation Fuel (SAF) Market, with a 54.2% share. Commercial carriers operate the largest fuel volumes and face the most direct regulatory pressure — EU, UK, and ICAO mandates apply directly to scheduled commercial flights.

It used approximately 139,000 metric tonnes of SAF in 2025, representing roughly 1.5% of its total fuel. This confirms that large carriers are building SAF into core operations, not just using it for pilot programs.

Military Aviation represents a growing SAF demand stream as defense forces align with national net-zero commitments. The UK Ministry of Defence estimated SAF at $1.62 per litre in 2025 versus $0.56 per litre for conventional Jet A-1 — a gap that limits full-fleet adoption but drives targeted blending in training and domestic operations where political pressure to decarbonize is highest.

General Aviation covers private, charter, and business jet operations. This segment shows early but fast-moving SAF adoption, driven by high-net-worth travelers and corporate clients who pay fuel premiums for verified sustainability credentials. The smaller volume per aircraft makes general aviation an easier proving ground for new SAF suppliers entering the market.

Unmanned Aerial Vehicles (UAV) form an emerging platform for SAF. Cargo drone fleets operated by logistics companies are beginning to specify SAF for last-mile delivery, particularly in Europe where regulatory pressure on commercial cargo is intensifying. UAV SAF volumes are small today but forecast to scale as autonomous freight corridors expand.

Capacity Insights

Above 100 MW dominates with 37.3% due to economies of scale in large-scale SAF production.

In 2025, the Above 100 MW capacity segment held a dominant market position in the By Capacity segment of the Sustainable Aviation Fuel (SAF) Market, with a 37.3% share. Large-scale SAF plants can spread fixed capital costs over greater output volumes, reducing per-litre production costs. Only high-capacity plants can realistically serve airline offtake agreements covering tens of thousands of tonnes per year, making this size tier the primary target for institutional capital.

The Up to 20 MW capacity tier serves regional airports, military bases, and general aviation facilities where local SAF production reduces logistics costs. These smaller plants often rely on locally available waste feedstocks — such as municipal solid waste — and benefit from proximity to end users rather than competing purely on cost.

The 20–50 MW segment offers a middle ground suited to mid-tier airports and industrial SAF hubs. Plants in this range can serve regional SAF demand cost-efficiently, and several European and Asian producers are targeting this scale as an entry point before expanding capacity as offtake agreements firm up.

The 50–100 MW tier bridges the gap between regional and utility-scale production. Plants at this capacity level can supply multiple airlines from a single facility and are increasingly integrated with renewable energy co-location strategies, particularly where solar or wind power anchors eSAF synthesis.

Feedstock Type Insights

Used Cooking Oil dominates with 47.2% due to proven supply chains and strong emissions credentials.

In 2025, Used Cooking Oil (UCO) held a dominant market position in the By Feedstock Type segment of the Sustainable Aviation Fuel (SAF) Market, with a 47.2% share. UCO is the most commercially established SAF feedstock because it is a genuine waste stream — it has no competing food use — and its use delivers high lifecycle GHG savings. The ICCT confirmed that waste-derived SAFs including UCO reduce lifecycle GHG emissions by up to 80% versus fossil jet fuel, a level that satisfies the strictest sustainability criteria in regulated markets.

Animal Fats (tallow, distillers corn oil) function similarly to UCO in HEFA processing and carry comparable sustainability credentials. Supply is limited by rendering industry output volumes, which means animal fats serve as a complementary feedstock alongside UCO rather than a standalone supply pillar. Prices track closely with UCO and are similarly subject to competition from biodiesel producers.

Agricultural Residues include corn stover, wheat straw, and forestry residues used in gasification or ATJ pathways. These feedstocks offer large-scale potential given the volume of residues generated globally, but processing complexity and seasonal supply variability add cost and logistics risk compared to liquid waste feedstocks like UCO.

Application Insights

Solar dominates with 42.7% due to falling renewable energy costs and co-location with eSAF production.

In 2025, Solar held a dominant market position in the By Application segment of the Sustainable Aviation Fuel (SAF) Market, with a 42.7% share. Solar power’s declining cost curve makes it the preferred renewable energy source for eSAF and PtL production facilities. Electricity accounts for 32–48% of total eSAF production costs in SOEC-integrated plant designs, Genvia, and Hinicio — meaning solar cost reductions directly lower SAF production costs.

Wind power is the second major renewable energy source for SAF production. Offshore and onshore wind provides high-capacity-factor electricity that suits continuous industrial SAF synthesis processes. Northern Europe’s wind resources are driving several eSAF projects in Scandinavia and the UK where wind assets and SAF demand infrastructure co-exist.

Geothermal energy provides stable baseload electricity for SAF production in geologically active regions. Iceland and parts of the US Pacific Northwest use geothermal power to support low-carbon fuel production. While the total resource base is smaller than solar or wind, geothermal’s consistent output makes it well-suited for eSAF processes that require steady-state electricity.

Hydropower supports SAF production in regions with large hydro endowments, particularly in Canada, Brazil, and parts of Southeast Asia. Hydropower’s reliability and low carbon intensity align well with PtL SAF certification requirements, and several proposed green hydrogen and SAF projects in Canada and Norway plan to use hydroelectric power as their primary energy source.

Carbon Capture applications in SAF involve capturing CO₂ from industrial or direct-air sources to use as a feedstock in PtL synthesis. SAF made from captured CO₂ and green hydrogen can achieve near-zero or net-negative lifecycle emissions, making it the most climate-effective variant in the market. Scale-up is currently limited by the cost of direct air capture, but falling CAPEX is narrowing this barrier.

Market Segments Covered in the Report

By Fuel Type

- Biofuel

- HEFA (Hydroprocessed Esters & Fatty Acids)

- Fischer-Tropsch (FT)

- Alcohol-to-Jet (ATJ)

- Hydrogen Fuel

- Power-to-Liquid Fuel

By Platform Type

- Commercial Aviation

- Military Aviation

- General Aviation

- Unmanned Aerial Vehicle (UAV)

By Capacity

- Up to 20 MW

- 20–50 MW

- 50–100 MW

- Above 100 MW

By Feedstock Type

- Used Cooking Oil

- Animal Fats

- Agricultural Residues

- Municipal Waste

- Algae / Synthetic Feedstock

By Application

- Solar

- Wind

- Geothermal

- Hydropower

- Carbon Capture

- Others

Regional Insights

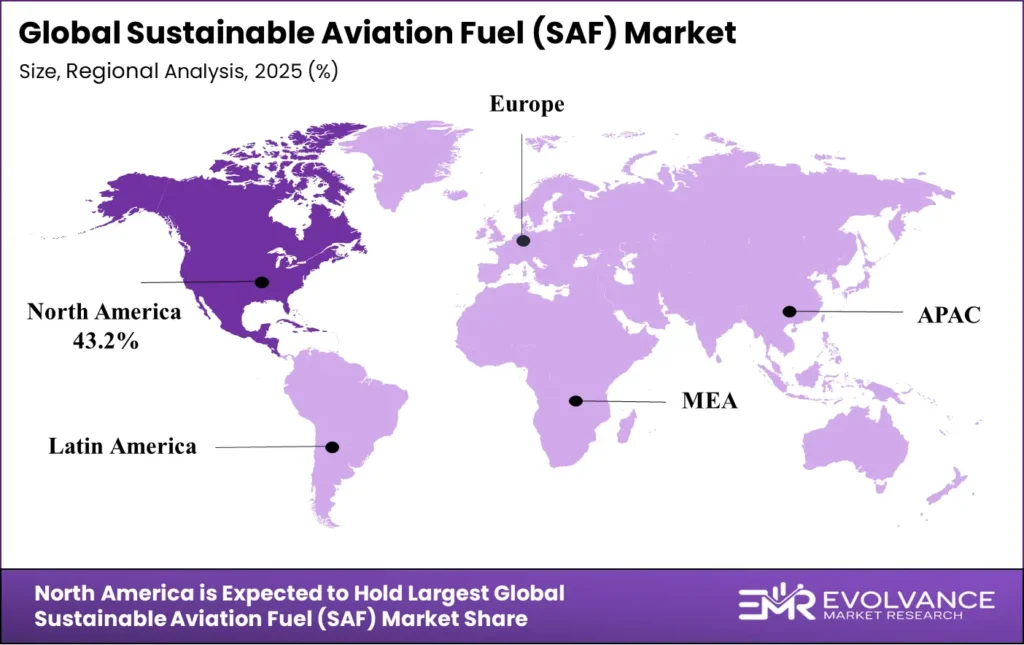

North America Dominates the Sustainable Aviation Fuel (SAF) Market with a Market Share of 43.2%, Valued at USD 10.1 Billion

North America holds a 43.2% share worth USD 10.1 Billion, anchored by US federal policy — the Inflation Reduction Act blenders’ tax credits reduce SAF production costs for domestic plants and create a financial incentive structure that Europe and Asia are only beginning to replicate. US and European producers together with China accounted for more than 85% of all new SAF capacity additions in 2025, confirming that North America is not just the largest demand market but also the primary supply-side growth engine.

Europe Sustainable Aviation Fuel (SAF) Market Trends

Europe is the most policy-dense SAF market in the world. The EU’s ReFuelEU Aviation regulation mandates a minimum 2% SAF usage starting in 2025, applying to over 95% of flights departing EU airports. The UK runs a parallel mandate requiring the same 2% blend rate, equivalent to approximately 230,000 tonnes of SAF demand. These mandates transform SAF from voluntary procurement into a legal compliance requirement, which guarantees baseline demand regardless of price volatility.

Asia Pacific Sustainable Aviation Fuel (SAF) Market Trends

Asia Pacific is emerging as the next major SAF growth region, driven by rapid aviation traffic growth and rising sustainability mandates. Singapore’s Changi Airport became a key SAF distribution point in 2024 after Neste integrated SAF supply into the airport’s fuel system — a move that demonstrates the region’s infrastructure readiness to scale. India is emerging as a potential SAF production hub via a collaboration between Airbus and CSIR-IIP targeting indigenous feedstock pathways.

Latin America Sustainable Aviation Fuel (SAF) Market Trends

Latin America has significant SAF feedstock potential, particularly from sugarcane ethanol used in ATJ pathways and agricultural residues from Brazil’s large farming sector. Brazil’s existing biofuel infrastructure and ethanol expertise position it as a future SAF exporter, particularly for the ATJ pathway. However, domestic SAF mandates are not yet in force, so near-term demand remains tied to international airline offtake agreements rather than local compliance requirements.

Middle East & Africa Sustainable Aviation Fuel (SAF) Market Trends

The Middle East hosts some of the world’s largest aviation hubs — Dubai, Doha, and Abu Dhabi — which are starting to integrate SAF into their fuel systems to align with international airline sustainability requirements. Gulf carriers face growing pressure from European routes subject to ReFuelEU rules. Africa is at an earlier stage, with SAF procurement limited to select international airlines, but feedstock potential from agricultural waste streams is significant.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The EU’s ReFuelEU Aviation regulation — in force from January 2025 — mandates a minimum 2% SAF blend at all EU airports, covering over 95% of departing flights. The regulation sets a clear escalating schedule, reaching 70% SAF by 2050 including a 35% Power-to-Liquid sub-quota. Fuel suppliers, not airlines, bear the blending obligation — shifting compliance risk upstream in the supply chain and incentivizing production investment.

The UK launched its own SAF Mandate from January 2025, requiring 2% SAF blending equivalent to approximately 230,000 tonnes. The mandate uses a certificate-based compliance system, with buy-out prices set at £0.137/MJ for standard SAF and £0.145/MJ for Power-to-Liquid SAF. Compliance certificates represent 34 MJ of energy per unit, creating a transparent market for SAF attribute trading alongside physical supply.

The US Inflation Reduction Act (IRA), signed in 2022 and operational through 2024–2032, provides a blenders’ tax credit of up to $1.75 per gallon for SAF achieving at least a 50% lifecycle emissions reduction. This subsidy directly narrows the cost gap with conventional jet fuel and has triggered significant new SAF investment in US refining capacity. The IRA’s SAF provisions have made the US the most financially attractive large market for new SAF production facilities.

Drivers

Binding Decarbonization Targets Convert SAF from Voluntary to Mandatory Procurement

The ICAO mandate to cut emissions 15% from 2019 levels starting in 2024, combined with a net-zero aviation target for 2050, makes SAF spending non-optional for airlines on international routes. This is not a preference signal — it is a compliance obligation with financial penalties. Airlines that delay SAF procurement now face higher spot prices and limited supply as forward contracts absorb available volumes.

Airlines are responding by scaling up SAF use far beyond early-stage trials. As reported by IATA, SAF use added approximately USD 3.6 Billion to airline fuel costs in 2025 due to price premiums — a figure that shows the scale of current SAF spending and signals that airlines are willing to absorb significant cost to meet compliance targets. This level of spend de-risks long-term supplier investment by confirming deep demand at today’s elevated prices.

Ryanair signed an offtake deal with Enilive for up to 100,000 tonnes of SAF between 2025 and 2030 — one of the largest volume commitments in the sector to date. Long-term deals like this lock in revenue for producers, reduce financing risk, and allow capital markets to fund new capacity builds with greater confidence. The shift toward multi-year contracts signals that SAF is entering a supply-demand cycle more like conventional fuel procurement than a green premium experiment.

Restraints

SAF Price Premium of Up to 5x Conventional Fuel Limits Full-Fleet Adoption

SAF remains 2 to 5 times more expensive than conventional jet fuel. In regulated EU markets, the effective cost at mandated airports reaches up to five times the fossil fuel price when compliance fees are included. The UK Ministry of Defence estimated SAF at $1.62 per litre in 2025 versus $0.56 per litre for Jet A-1 — a gap of $1.06 per litre. At current fleet sizes, moving beyond mandated blend rates would add billions in annual fuel costs that airlines cannot fully pass on to price-sensitive passengers.

Production capacity is falling well short of announced targets. Only 30% of announced SAF production capacity had been completed by end of 2025. Roughly 29% of announced capacity was paused, cancelled, or went silent. This shortfall constrains supply and keeps prices elevated, which in turn delays voluntary adoption beyond mandated minimums.

The SAF “realization gap” — the difference between announced and installed production capacity — grew from 7.0 million tonnes in 2024 to 11.6 million tonnes in 2025, even as more facilities came online. This widening gap means supply is not keeping pace with policy-driven demand. For airlines facing mandatory blending targets, it creates procurement risk; for investors, it signals that the market is supply-constrained, not demand-constrained — a situation that favors established producers over new entrants.

Growth Factors

Infrastructure Integration and Corporate Cargo Deals Unlock New SAF Revenue Streams

Airport-level SAF delivery systems are removing a key barrier to adoption. Neste’s integration of SAF supply at Singapore Changi Airport in 2024 demonstrated that SAF can be embedded into a major hub’s fueling operations at scale. Once airport infrastructure supports SAF, every airline using that hub gains access without needing individual logistics arrangements — an effect that multiplies adoption rates across carriers simultaneously.

Corporate cargo clients are mandating SAF blending in their air freight operations. Repsol, Iberia, and Inditex signed an agreement requiring 5% SAF usage in air cargo logistics — a deal that creates a traceable, contracted demand stream from retail supply chains to fuel producers. The US, Europe, and China together accounted for more than 85% of all new SAF capacity additions in 2025, confirming these three geographies as the production growth engine for the decade ahead.

India is emerging as a future SAF production hub through a collaboration between Airbus and India’s CSIR-IIP research body, targeting indigenous feedstock pathways. India’s large agricultural residue base, growing aviation sector, and government interest in energy security make it a structurally strong candidate for SAF production at scale. Early investment in India’s SAF capability could position it as a key supplier for Asia Pacific aviation by the early 2030s.

Emerging Trends

Book-and-Claim Systems and Circular Feedstocks Reshape SAF Market Structure

SAF “book-and-claim” and environmental attribute trading systems are enabling SAF adoption by companies that cannot physically receive blended fuel. A multi-company pilot at Narita Airport in 2024 demonstrated how airlines and cargo shippers can purchase SAF environmental certificates without needing the physical fuel to travel through their specific supply chain. This model dramatically widens the addressable market for SAF producers, as any company with aviation-related emissions can become a customer.

Airlines are increasing SAF blending ratios beyond the minimum required. Iberia cargo operations adopted 5% SAF blends in 2024, and Finnair’s SAF use reached 1.6% of total fuel in 2025 — well above what most mandates currently require. Aerosol Science and Technology, using 100% SAF reduces non-volatile particulate matter (nvPM) emissions by up to 81% compared to Jet A-1 fuel, making SAF a local air quality solution as well as a climate tool. This dual benefit is accelerating SAF demand at airports under air quality regulations.

Waste-based and circular feedstocks are replacing virgin and crop-based inputs as the default for new SAF production. Used cooking oil, animal fats, and agricultural residues now dominate the feedstock mix in commercial production. The shift away from crop-based inputs reduces the reputational and regulatory risk of SAF deployment — addressing concerns about food system impacts that slowed early adoption. Producers using certified waste feedstocks can access premium pricing tiers and satisfy the strictest sustainability requirements in mandated markets.

Key Companies Insights

Neste holds the strongest commercial position in the global SAF market, operating the world’s largest renewable fuel refinery in Porvoo, Finland, and supplying SAF to over 90 airports globally. Neste’s 2024 integration of SAF into Singapore Changi Airport’s fueling system shows its ability to serve major international hubs at scale. Its established HEFA production capacity and long-term airline offtake agreements give Neste a supply security advantage that new entrants cannot quickly replicate.

TotalEnergies is scaling SAF production from its European refining network while simultaneously investing in next-generation feedstocks. TotalEnergies benefits from its integrated energy position — it can co-produce SAF alongside conventional fuels using existing refinery assets, which lowers per-unit capital cost. Its broad customer base across European airlines and its active role in EU regulatory discussions position it as a key beneficiary of ReFuelEU Aviation’s mandatory blending requirements.

Gevo focuses on the Alcohol-to-Jet pathway, using low-carbon corn and agricultural inputs to produce SAF with high GHG reduction scores under CORSIA and the US IRA. Gevo’s Net-Zero 1 plant in South Dakota represents its first commercial-scale ATJ SAF facility. The company’s strategy targets corporate aviation customers and airlines seeking verified lifecycle emissions data — a segment that is less price-sensitive and more focused on verifiable sustainability credentials.

LanzaTech deploys gas fermentation technology that converts industrial waste gases — including steel mill emissions and municipal solid waste syngas — into ethanol, which is then processed into ATJ SAF. This approach turns heavy industrial emitters into SAF feedstock providers, creating revenue from waste streams that previously had no value. LanzaTech’s technology is operational at commercial scale in China and the US, giving it first-mover advantage in the waste-gas-to-fuel segment as carbon pricing makes industrial waste valorization more financially compelling.

Key Companies

- Aemetis Inc.

- AVFUEL CORPORATION

- Neste

- Preem AB

- Sasol Limited

- SkyNRG B.V.

- Fulcrum BioEnergy

- Gevo

- TotalEnergies

- LanzaTech

- World Energy, LLC

Recent Development

- In February 2026, LanzaJet raised $47 million (first close of a targeted $135 million equity round at $650 million pre-money valuation), co-led by IAG and Shell with participation from Groupe ADP, LanzaTech, and Mitsui, plus a UK grant, to support commercial deployment of its Alcohol-to-Jet (ATJ) technology.

- In April 2026, Sora Fuel closed a $14.6 million funding round co-led by Spero Ventures and Inspired Capital, with participation from Engine Ventures and Wireframe Ventures, to build and operate a pilot production facility for its air-to-SAF technology.

- In September 2025, OXCCU raised £20.75 million in an oversubscribed Series B funding round with investors including IAG (via IAGi Ventures), Safran Corporate Ventures, Orlen VC, and others to accelerate scale-up and commercialization of its one-step waste carbon to SAF technology.

- In December 2025, Aether Fuels secured $15 million in additional convertible note funding (including from Aster Ventures and EDBI) to accelerate Project Beacon and commercialization of its Aether Aurora SAF in Singapore.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 23.47 Billion |

| Forecast Revenue (2035) | USD 4,026.74 Billion |

| CAGR (2026-2035) | 67.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Fuel Type (Biofuel – HEFA, Fischer-Tropsch, ATJ; Hydrogen Fuel; Power-to-Liquid Fuel), By Platform Type (Commercial Aviation, Military Aviation, General Aviation, UAV), By Capacity (Up to 20 MW, 20–50 MW, 50–100 MW, Above 100 MW), By Feedstock Type (Used Cooking Oil, Animal Fats, Agricultural Residues, Municipal Waste, Algae / Synthetic Feedstock), By Application (Solar, Wind, Geothermal, Hydropower, Carbon Capture, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Aemetis Inc., AVFUEL CORPORATION, Neste, Preem AB, Sasol Limited, SkyNRG B.V., Fulcrum BioEnergy, Gevo, TotalEnergies, LanzaTech, World Energy, LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |