What is the Green Hydrogen Production And Storage Market Size?

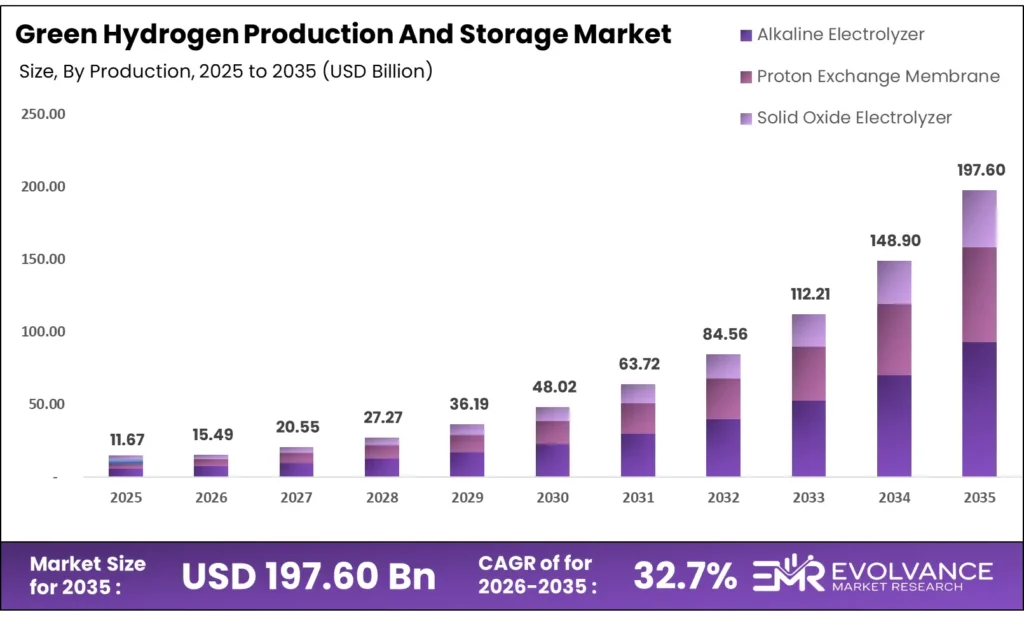

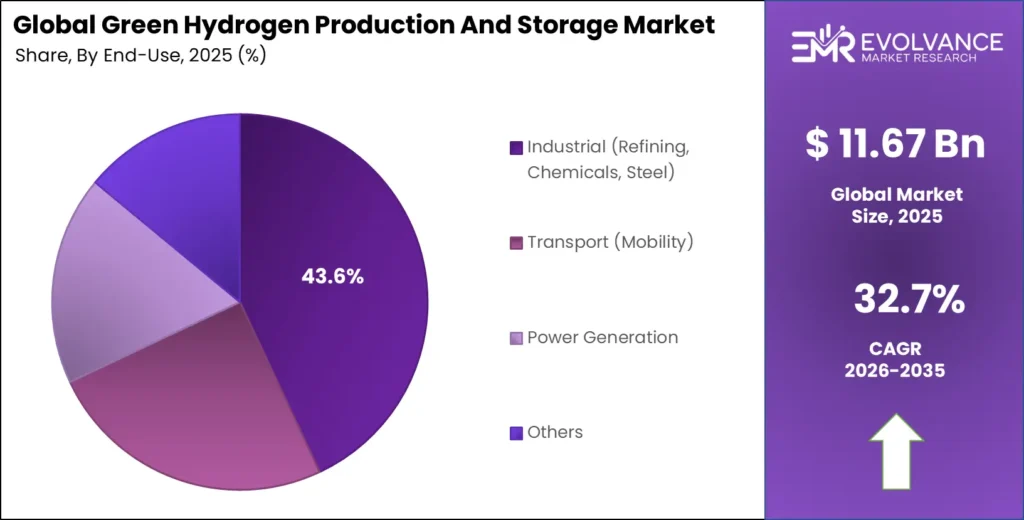

The Global Green Hydrogen Production And Storage Market size will be worth around USD 197.60 Billion by 2035 from USD 11.67 Billion in 2025, growing at a CAGR of 32.7% during the forecast period 2026 to 2035. Steel, Bio-based chemicals, and ammonia producers are shifting capital toward green hydrogen as decarbonization mandates tighten across major industrial economies. Enterprise buyers are committing to long-term offtake agreements, signaling that procurement is moving from pilot budgets to core operating spend. Hydrogen electrolyzer supply chains remain concentrated in China, creating input cost exposure for projects outside Asia.

Market Highlights

- The Global Green Hydrogen Production And Storage Market size reaches USD 197.60 Billion by 2035 from USD 11.67 Billion in 2025, growing at a CAGR of 32.7%.

- Europe leads with a 37.9% share, valued at USD 4.4 Billion in 2025.

- Production segment holds a dominant 68.3% share in 2025.

- Alkaline Electrolyzer leads the By Production segment with 63.7% share.

- Pipeline leads the By Distribution Channel segment with 72.3% share.

- Compressed Gas Storage leads the By Storage segment with 46.1% share.

- Medium-scale Production leads the By Production Scale segment with 48.9% share.

- Industrial (Refining, Chemicals, Steel) leads the By End-Use segment with 43.6% share.

Market Overview

Green hydrogen is produced by splitting water into hydrogen and oxygen using electrolysis powered by renewable energy. Unlike grey or blue hydrogen, it emits no carbon during production. This makes it a core tool for decarbonizing sectors where direct electrification is not possible, including steel, chemicals, shipping, and long-haul transport.

The production side includes electrolyzer technologies such as alkaline, PEM, and solid oxide systems. The storage side spans compressed gas, liquid hydrogen, material-based, and underground options. Each pathway suits different project scales, locations, and end-use applications. The combination of falling electrolyzer costs and rising renewable capacity is making green hydrogen commercially viable in more markets.

The Green Hydrogen Production And Storage Market plays a critical role in the expansion of sustainable aviation fuel technologies. Green hydrogen is widely used in synthetic fuel pathways and next-generation Sustainable Aviation Fuel (SAF) production processes, helping reduce lifecycle emissions in the aviation sector. As renewable energy adoption increases, the integration of hydrogen storage systems with green chemistry solutions and bio-based fuel technologies is expected to accelerate market growth.

Government investment is accelerating across Europe, the U.S., India, and the Middle East. The EU’s Hydrogen Strategy and the U.S. Inflation Reduction Act both provide direct subsidies for clean hydrogen production. India’s National Green Hydrogen Mission targets 5 million tonnes of annual production by 2030, with grid connectivity incentives already shaping project economics.

Global installed water electrolysis capacity reached 2 GW in 2024, with more than 1 GW added by July 2025. This pace of capacity addition signals that the market has moved beyond demonstration into early commercial deployment — a threshold that typically precedes faster cost curve declines. For equipment suppliers, it signals window of opportunity before price competition intensifies.

The IEA, more than 200 low-emissions hydrogen production projects had reached final investment decision by the end of 2024. This milestone shows that capital is committing at scale, not just planning. However, global low-emissions hydrogen still represented less than 1% of total hydrogen production in 2024 — meaning the bulk of addressable market conversion has not yet occurred, and first-movers hold significant long-term positioning advantage.

Type Insights

Production dominates with 68.3% due to upstream capital concentration and electrolyzer scale-up.

In 2025, Production held a dominant market position in the By Type segment of the Green Hydrogen Production And Storage Market, with a 68.3% share. This lead reflects where investment is flowing — electrolyzer plants, renewable power contracts, and site development account for the largest share of project spend. Buyers and governments are prioritizing output capacity before storage networks are fully built, creating a production-first investment cycle.

Storage is gaining ground as offtake agreements mature and transport infrastructure scales. Compressed gas, liquid, and material-based solutions are being selected based on project distance, delivery frequency, and end-use requirements. As production volumes rise, storage becomes the next capital bottleneck — making it the higher-growth sub-segment for infrastructure investors over the 2026–2035 window.

Production Insights

Alkaline Electrolyzer dominates with 63.7% due to lower capital cost and proven large-scale deployment.

In 2025, Alkaline Electrolyzer held a dominant market position in the By Production segment of the Green Hydrogen Production And Storage Market, with a 63.7% share. Alkaline systems carry lower upfront cost than PEM and have decades of industrial operating history, making them the default choice for large projects where cost certainty matters more than response speed.

PEM (Proton Exchange Membrane) Electrolyzer is gaining share in applications requiring faster dynamic response, compact footprint, or higher pressure output. A 2025 analysis published in Propulsion and Power Research found that PEM systems can reach electrical conversion efficiencies of about 65–75% under nominal load. The Ceres–Shell SOEC collaboration achieved roughly 36–37 kWh/kg at MW scale — a benchmark that is pulling PEM adoption in high-efficiency industrial settings where electricity costs dominate the project economics.

SOEC (Solid Oxide Electrolyzer) operates at high temperatures and delivers the highest efficiency of the three electrolyzer types, but requires stable heat input to perform. Its commercial footprint remains smaller than alkaline or PEM. SOEC suits industrial sites with waste heat available — steel plants, refineries, and chemical facilities — where combined heat and hydrogen production can reduce the effective electricity cost per kilogram.

Distribution Channel Insights

Pipeline dominates with 72.3% due to cost efficiency at volume and alignment with industrial cluster demand.

In 2025, Pipeline held a dominant market position in the By Distribution Channel segment of the Green Hydrogen Production And Storage Market, with a 72.3% share. Pipelines offer the lowest per-unit delivery cost once built, making them the preferred channel for high-volume industrial customers. Europe is repurposing natural gas pipeline networks for hydrogen transport, reducing the capital required to build dedicated infrastructure and accelerating deployment timelines.

Cargo (Transport/Shipping) covers liquid hydrogen tankers, compressed tube trailers, and ammonia carriers. This channel is critical for export markets and regions without pipeline access. Japan and South Korea are actively building liquid hydrogen import terminals, and the Deendayal Port Green Hydrogen–Ammonia–Methanol project in India illustrates how port-linked export infrastructure is becoming a discrete market segment with its own investment thesis.

Storage Insights

Compressed Gas Storage dominates with 46.1% due to mature technology and compatibility with existing industrial gas infrastructure.

In 2025, Compressed Gas Storage held a dominant market position in the By Storage segment of the Green Hydrogen Production And Storage Market, with a 46.1% share. Type IV compressed hydrogen systems are the standard for both vehicle fueling and industrial delivery. According to the U.S. Department of Energy, projected cost for 700-bar Type IV compressed hydrogen storage fell about 25% since 2019, from $16.9/kWh to $12.7/kWh — a cost trajectory that sustains adoption even as competing storage methods improve.

Liquid Hydrogen Storage enables higher energy density per unit volume, making it better suited for long-distance shipping and large buffer storage near export hubs. Plug Power’s U.S. liquid hydrogen facility represents one of the first large-scale commercial liquid hydrogen production assets, establishing operational benchmarks for this format at industrial scale. The energy required for liquefaction remains a cost constraint, but falling power prices from dedicated renewable contracts are improving project economics.

Material-based Storage uses metal hydrides or chemical carriers like ammonia and liquid organic hydrogen carriers (LOHCs) to store hydrogen at near-ambient conditions. This removes the need for high-pressure vessels or cryogenic equipment, which reduces safety infrastructure costs. However, the energy required for release adds to the full-cycle cost, limiting current adoption to niche applications where safety or transport convenience outweighs efficiency losses.

Underground Storage in salt caverns and depleted gas fields offers the largest volumetric capacity of any storage format. It is the only option capable of storing seasonal surpluses of renewable hydrogen at the grid scale. The challenge is geographic — suitable geological formations are concentrated in specific regions, and the capital required for site assessment and certification is high. As the market matures and surplus renewable energy volumes grow, underground storage will become a strategic infrastructure asset rather than a niche option.

Production Scale Insights

Medium-scale Production dominates with 48.9% due to balance between cost efficiency and deployment flexibility.

In 2025, Medium-scale Production held a dominant market position in the By Production Scale segment of the Green Hydrogen Production And Storage Market, with a 48.9% share. Mid-scale projects, typically ranging from tens to hundreds of megawatts, allow developers to prove project economics before committing to gigawatt-scale investments. They also align well with the current capacity of off-takers, most of whom are still expanding their hydrogen consumption infrastructure.

Large-scale Production is where the majority of future capital is directed. GAIL’s 10 MW (4.3 TPD) green hydrogen plant in India and VNG’s 30 MW electrolyzer project in Europe — targeting approximately 2,700 tonnes/year — represent the early cohort of large-scale assets. Centralized production achieves levelized cost of hydrogen (LCOH) of 2.66–5.80 €/kg, versus 7–10 €/kg for distributed systems, confirming that scale is the primary lever for cost reduction. Once large-scale plants demonstrate reliable operational performance, capital will shift heavily toward this tier.

Small-scale / On-site Production addresses demand from users who cannot access pipelines or who require hydrogen on short notice. The Adani 5 MW solar-powered plant with battery energy storage in 2025, and the NTPC NETRA campus microgrid hydrogen production pilot in India, both demonstrate viable decentralized models. While unit production costs remain higher, on-site systems eliminate transport costs and provide energy security for remote or critical facilities.

End-Use Insights

Industrial (Refining, Chemicals, Steel) dominates with 43.6% due to captive demand and high decarbonization pressure.

In 2025, Industrial (Refining, Chemicals, Steel) held a dominant market position in the By End-Use segment of the Green Hydrogen Production And Storage Market, with a 43.6% share. These sectors already consume large volumes of grey hydrogen, giving green hydrogen an immediate substitution opportunity rather than a new demand creation challenge. McPhy’s green hydrogen projects with ArcelorMittal and AAK in 2024 illustrate how major industrial buyers are locking in supply through direct partnerships, bypassing spot markets entirely.

Transport (Mobility) covers fuel cell vehicles, buses, trains, and maritime applications. Hydrogen mobility adoption is fastest in markets with public subsidies — Japan, South Korea, Germany, and California. The Ohmium–Toyota Kirloskar partnership is positioning India as an early market for fuel cell mobility, where the combination of large fleet operators and urban air quality mandates creates structured demand for hydrogen fueling infrastructure.

Power Generation uses hydrogen as a backup fuel or grid balancing tool, either in gas turbines or fuel cells. It is currently the smallest commercial end-use segment, but it gains strategic value as variable renewable penetration rises and grid operators need long-duration storage with dispatchable output. FuelCell Energy and Ballard Power Systems are active in this segment, focusing on stationary fuel cell installations for industrial and utility customers.

Market Segments Covered in the Report

By Type

- Production

- Storage

By Production

- Alkaline Electrolyzer

- PEM (Proton Exchange Membrane) Electrolyzer

- SOEC (Solid Oxide Electrolyzer)

By Distribution Channel

- Pipeline

- Cargo (Transport/Shipping)

By Storage

- Compressed Gas Storage

- Liquid Hydrogen Storage

- Material-based Storage

- Underground Storage

By Production Scale

- Large-scale Production

- Medium-scale Production

- Small-scale / On-site Production

By End-Use

- Industrial (Refining, Chemicals, Steel)

- Transport (Mobility)

- Power Generation

- Others

Regional Insights

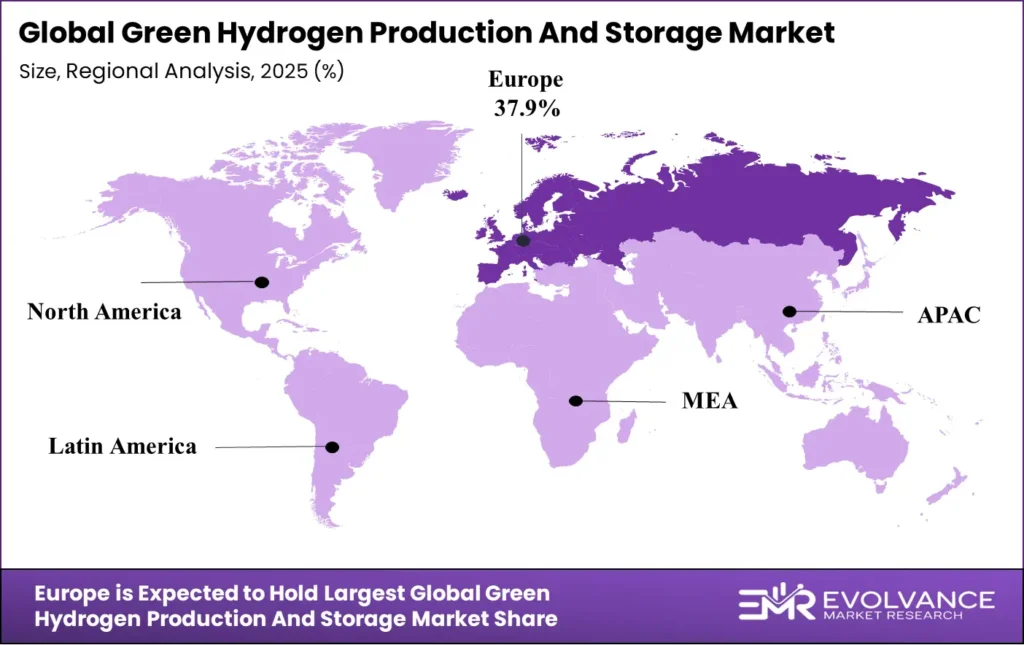

Europe Dominates the Green Hydrogen Production And Storage Market with a Market Share of 37.9%, Valued at USD 4.4 Billion

Europe holds a 37.9% share worth USD 4.4 Billion in 2025, driven by the EU Hydrogen Strategy, mandatory blending targets, and carbon border adjustment mechanisms. Regulatory pressure on industrial emitters is creating captive demand for green hydrogen faster than in any other region. Pipeline repurposing programs in Germany and the Netherlands are reducing infrastructure costs, giving Europe a structural cost advantage in hydrogen delivery that other regions cannot yet replicate.

North America Market Trends

North America is accelerating through the U.S. Inflation Reduction Act’s production tax credit of up to $3/kg for clean hydrogen, which has triggered a wave of project announcements. The U.S. Department of Energy’s $7 Billion Regional Clean Hydrogen Hubs program is building the infrastructure backbone that links producers with industrial offtakers. Canada’s low-cost hydroelectric power gives it a distinct competitive advantage for large-scale electrolysis projects targeting export markets.

Asia Pacific Market Trends

Asia Pacific is the fastest-growing region, led by China, Japan, South Korea, India, and Australia. China’s electrolyzer manufacturing capacity reached about 20 GW/year in 2025, creating significant cost advantages for domestic producers. Japan and South Korea are building import infrastructure to source affordable hydrogen from Australia and the Middle East. India’s National Green Hydrogen Mission is targeting 5 million tonnes/year by 2030, with grid and transmission policy already shaping project bankability.

Latin America Market Trends

Latin America holds early-mover advantage in green hydrogen exports, with Chile and Brazil leading project development. Chile’s high solar irradiation in the Atacama desert enables some of the world’s lowest renewable electricity costs, translating into competitive hydrogen production economics. Brazil’s offshore wind pipeline and biomass integration potential make it a likely supplier to European import terminals by the late 2020s. Regional demand is still nascent, but export positioning is drawing significant foreign investment.

Middle East & Africa Market Trends

The Middle East is repositioning legacy fossil fuel export infrastructure toward green hydrogen and ammonia. Saudi Arabia’s NEOM project and the UAE’s national hydrogen strategy both target large-scale production for export by 2030. Africa’s potential is concentrated in North Africa, where proximity to European markets and abundant solar resources create a viable export corridor. Financing access and policy certainty remain the key constraints slowing project development across both sub-regions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The EU Delegated Regulation on Renewable Fuels of Non-Biological Origin, effective from January 2024, defines the additionality, temporal correlation, and geographical criteria that green hydrogen must meet to qualify under the EU Hydrogen Strategy. This regulation directly shapes project design — producers cannot simply purchase renewable certificates but must demonstrate real-time renewable power links to their electrolyzers.

The U.S. Treasury Department issued final guidance under Section 45V of the Inflation Reduction Act in January 2025, establishing the clean hydrogen production tax credit framework. Projects claiming the full $3/kg credit must meet strict lifecycle emissions thresholds. The three-pillar test — incrementality, deliverability, and temporal matching — closely mirrors EU rules, signaling global regulatory convergence that multinational producers must plan for.

India’s Ministry of New and Renewable Energy released the National Green Hydrogen Mission’s first phase guidelines in 2024, covering incentive structures for electrolyzer manufacturing and green hydrogen production. The Strategic Interventions for Green Hydrogen Transition program allocated INR 17,490 Crore for pilot projects and production-linked incentives. These rules are now active, and project developers must meet domestic content requirements to qualify for the full incentive stack.

Germany’s updated Hydrogen Import Strategy, published in 2024, formalizes bilateral agreements with Norway, Canada, and Namibia for green hydrogen supply. The strategy sets quality and certification standards that imported hydrogen must meet, creating a de facto compliance framework for export-oriented producers targeting the German market. Producers outside these bilateral arrangements face higher certification costs to access Europe’s largest industrial hydrogen market.

Drivers

Large-Scale Electrolyzer Commissioning and Industrial Adoption Unlock Supply-Side Credibility

Industrial buyers have historically delayed green hydrogen commitments because supply reliability was unproven. The commissioning of Plug Power’s U.S. liquid hydrogen facility and GAIL’s 10 MW (4.3 TPD) green hydrogen plant in India changes that calculus. These plants provide operational benchmarks that procurement teams can reference in contract negotiations, removing a key barrier to long-term offtake agreements.

Electrolyzer efficiency gains are compressing the cost curve faster than earlier projections suggested. The Ceres–Shell SOEC achieving roughly 36–37 kWh/kg at MW scale, compared to the typical 50–55 kWh/kg for commercial PEM and alkaline systems, shows that next-generation technologies are approaching thresholds where green hydrogen can compete with grey hydrogen without subsidy in high-electricity-cost markets.

Moreover, strategic partnerships are accelerating commercialization timelines. The Ohmium–Toyota Kirloskar collaboration links electrolyzer supply with mobility demand, creating integrated supply chains that reduce project risk. Shell’s partnership with Ceres on SOEC technology targets industrial deployments where waste heat is available, connecting high-efficiency production with industrial buyers who already have hydrogen consumption infrastructure in place.

Restraints

Policy Uncertainty and Project Cancellations Signal Execution Risk at Scale

Fortescue’s cancellation of its $550 Million hydrogen project due to shifting renewable energy policies illustrates a systemic risk in this market. When government incentive frameworks change mid-project — through election cycles, subsidy redesigns, or permitting delays — developers face stranded development costs that are material at this project scale. Investors are pricing this policy risk into required returns, raising the cost of capital for new projects.

High electrolyzer degradation rates create a second layer of long-term economic uncertainty. Studies show up to a 9-year variance in optimal replacement cycles across different operating conditions, making lifetime cost modeling imprecise. For project finance structures that depend on stable cash flow projections over 20-year periods, this uncertainty directly affects debt serviceability assessments and lender appetite for non-recourse project financing.

Additionally, the current production cost range of 4–6 USD/kg in most markets remains well above the 1–2 USD/kg target needed by 2030 to compete without subsidy, as noted in a 2026 global white paper from IIT Bombay. The gap is not insurmountable, but it means that every project commissioned today depends on either sustained policy support or offtake contracts at above-market prices — both of which carry renewal risk over a decade-long project life.

Growth Factors

Industrial Value Chain Integration Creates Anchored Demand and De-Risks Project Finance

Green hydrogen’s strongest commercial footing comes when it replaces grey hydrogen in existing industrial processes rather than creating new demand. McPhy’s projects with ArcelorMittal for steel and with AAK for specialty chemicals in 2024 exemplify this model. These projects have defined volumes, existing infrastructure, and proven end-use processes — conditions that simplify project finance and reduce completion risk versus greenfield demand.

Port-linked export hubs are building the physical infrastructure that connects low-cost production regions with high-demand import markets. The Deendayal Port Green Hydrogen–Ammonia–Methanol project in India is one example of a model where multiple revenue streams — ammonia for fertilizers, methanol for shipping, and hydrogen for industrial use — are bundled into one export facility. Low-emissions hydrogen projects expanded from a handful to more than 200 committed investments by 2025, showing how this model is replicating globally.

Furthermore, hybrid grid and on-site electrolyzer models are improving cost outcomes by using surplus renewable energy that would otherwise be curtailed. In Gujarat, optimized project configurations can reduce production costs by roughly 33% compared to baseline designs, primarily by reducing electricity charges and optimizing renewable sizing. The Uttar Pradesh Hydrogen Centre, which supports 50 startups and hydrogen mobility projects.

Emerging Trends

Modular High-Density Electrolyzer Designs Reduce Site Costs and Speed Up Deployment

Ohmium has demonstrated a footprint of 29.7 m²/MW in its latest electrolyzer design while exceeding 2030 iridium utilization targets at 18 GW/ton. Smaller physical footprints reduce site preparation and civil engineering costs, making it easier to deploy electrolyzers in industrial settings with limited space. This design direction benefits retrofit projects at existing refineries and chemical plants where space constraints previously made green hydrogen integration impractical.

The emergence of MW-to-100 MW scale electrolysis projects is creating a new commercial tier between demonstration and utility-scale deployment. VNG’s 30 MW plant targeting roughly 2,700 tonnes/year of hydrogen output sits in this tier — large enough for industrial offtake but small enough to finance without sovereign-level backing. This scale enables faster iteration on operational performance data, which will accelerate cost curve improvements across the industry over the 2026–2030 period.

Additionally, decentralized microgrid-based hydrogen production is proving viable in off-grid industrial and institutional settings. The NTPC NETRA campus microgrid hydrogen pilot in India demonstrates that small-scale on-site production can serve captive energy and mobility needs without grid connection. As microgrid technology costs fall and hydrogen fuel cell systems become more reliable, this model will spread to mining operations, remote military bases, and island communities where energy security justifies the higher unit cost of on-site production.

Key Companies Insights

Air Liquide operates one of the world’s most extensive industrial gas networks, giving it a structural distribution advantage that pure-play hydrogen producers cannot quickly replicate. The company has committed billions to low-carbon hydrogen across Europe and North America, with a strategy centered on large anchor customers in refining and chemicals. Its ability to bundle hydrogen supply with existing gas management services makes it a preferred partner for industrial buyers managing complex decarbonization timelines under regulatory pressure.

Air Products and Chemicals has positioned itself as the lead developer for some of the world’s largest green and blue hydrogen projects, including NEOM’s $8.5 Billion green ammonia facility in Saudi Arabia. Its vertically integrated model — owning production, liquefaction, and distribution assets — gives it control over margin at every step in the value chain. This integration reduces its exposure to spot market volatility and makes its project economics more predictable for long-duration project finance structures.

Linde plc brings unmatched scale in industrial gas infrastructure alongside deep electrolyzer engineering expertise. At 50 kWh/kg H₂, a 10 MW electrolyzer can produce about 200 kg of hydrogen per hour — a benchmark Linde uses to size and optimize projects for industrial customers. Its global footprint in petrochemicals, steel, and electronics manufacturing means it can leverage existing customer relationships to convert grey hydrogen consumption to green without requiring buyers to change infrastructure or procurement systems.

ENGIE approaches the market through its renewable energy platform, using excess solar and wind output to power electrolyzers at or near generation assets. This model minimizes electricity transmission costs — the dominant operating cost in green hydrogen production — and allows ENGIE to offer competitive pricing in markets where grid electricity tariffs are high. The company is active across Europe, Australia, and Latin America, targeting both industrial off-takers and government-backed export projects as its primary revenue base.

Key Companies

- Air Liquide

- Air Products and Chemicals

- Linde plc

- ENGIE

- Uniper SE

- Siemens Energy

- Nel ASA

- thyssenkrupp nucera

- ITM Power

- Plug Power

- Cummins Inc.

- Sunfire

- John Cockerill Hydrogen

- LONGi Hydrogen

- ACME Group

- Adani Group

- Fortescue Future Industries

- Electric Hydrogen

- Ballard Power Systems

- FuelCell Energy

Recent Development

- In April 2025, Hy2gen secured €47 million funding led by Hy24, with participation from Technip Energies and BenDa, to accelerate its Power-to-X hydrogen and e-fuels projects.

- In August 2025, HydrogenXT secured a $900 million debt and equity financing term sheet with Kell Kapital Partners to build 10 hydrogen production and dispensing plants across the U.S.

- In January 2025, Evonik and VoltH2 signed a partnership to develop a 50 MW electrolyzer plant in Delfzijl (Netherlands) for industrial hydrogen supply.

- In March 2025, Next Hydrogen and Sungrow Hydrogen formed a strategic partnership to scale electrolyzer production using Sungrow’s 3 GW manufacturing capacity.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.67 Billion |

| Forecast Revenue (2035) | USD 197.60 Billion |

| CAGR (2026-2035) | 32.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Production, Storage), By Production (Alkaline Electrolyzer, PEM Electrolyzer, SOEC), By Distribution Channel (Pipeline, Cargo), By Storage (Compressed Gas Storage, Liquid Hydrogen Storage, Material-based Storage, Underground Storage), By Production Scale (Large-scale Production, Medium-scale Production, Small-scale / On-site Production), By End-Use (Industrial, Transport, Power Generation, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Air Liquide, Air Products and Chemicals, Linde plc, ENGIE, Uniper SE, Siemens Energy, Nel ASA, thyssenkrupp nucera, ITM Power, Plug Power, Cummins Inc., Sunfire, John Cockerill Hydrogen, LONGi Hydrogen, ACME Group, Adani Group, Fortescue Future Industries, Electric Hydrogen, Ballard Power Systems, FuelCell Energy |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |