What is the Agentic AI in Supply Chain and Logistics Market Size?

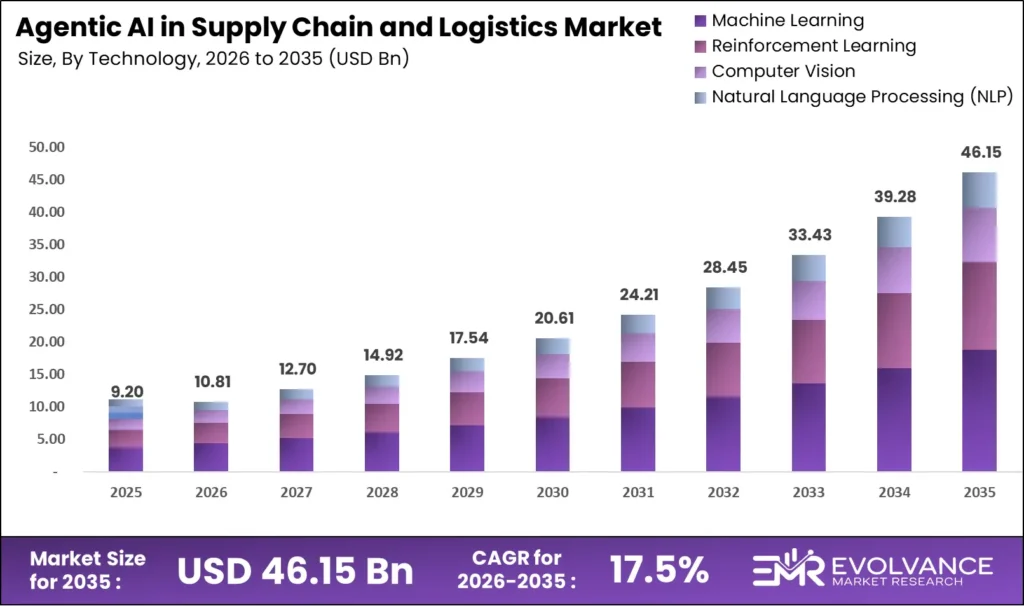

The global agentic AI in the supply chain and logistics market will reach USD 46.15 billion by 2035 from USD 9.2 billion in 2025, growing at a CAGR of 17.5% during 2026 to 2035. Walmart reports AI and automation have nearly doubled distribution center capacity, now covering 95% of U.S. households for same-day delivery in 2025. This scale of deployment signals that agentic AI is moving from pilot projects into core logistics infrastructure across major operators globally.

Market Highlights

- The global agentic AI in supply chain and logistics market is valued at USD 9.2 billion in 2025, projected to reach USD 46.15 billion by 2035 at a CAGR of 17.5%.

- By Deployment Mode: Cloud-based leads with 63.73% revenue share in 2025.

- By Technology: Machine Learning holds 39.42% revenue share in 2025.

- By Organization Size: Large Enterprises account for 68.65% revenue share in 2025.

- By Component: Software Platforms command 57.8% revenue share in 2025.

- By Autonomy Level: Full Autonomy (Fully Automated Execution) is the dominant segment in 2025.

- By Application: Demand Forecasting and Planning leads with 35.86% revenue share in 2025.

- By Pricing Model: Subscription-based is the dominant pricing model in 2025.

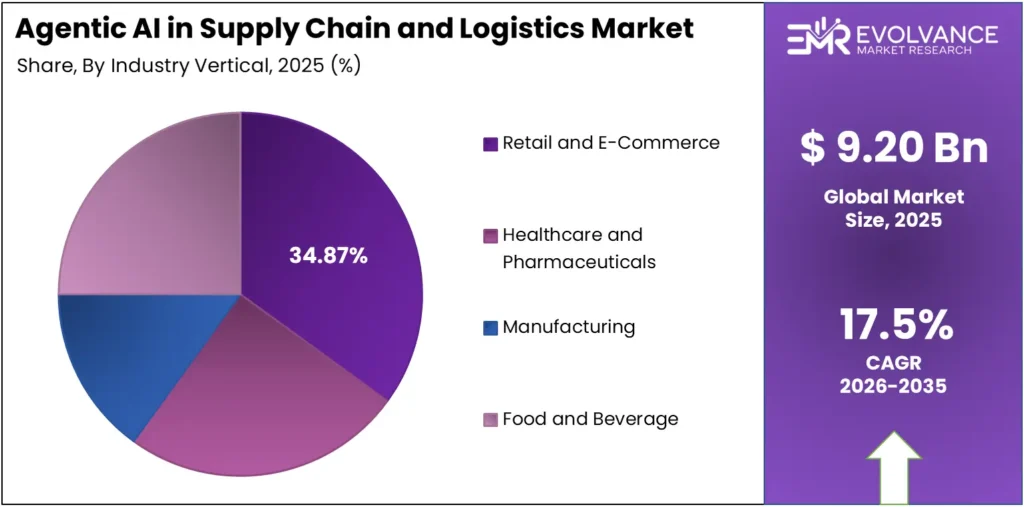

- By Industry Vertical: Retail and E-Commerce holds 34.87% revenue share in 2025.

- By Agent Architecture: Multi-Agent Systems lead with 56.87% revenue share in 2025.

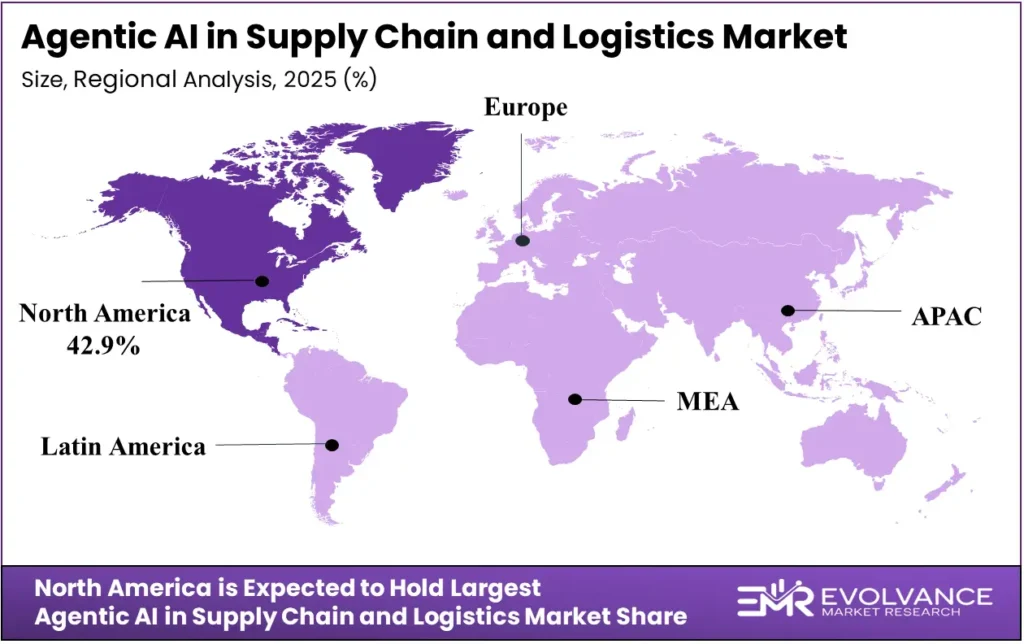

- By Region: North America is the largest market with 42.9% revenue share in 2025.

- Asia-Pacific is the fastest-growing region at a 16.1% CAGR through 2035.

Market Overview

The agentic AI in supply chain and logistics market covers autonomous software systems that sense real-time data, reason across multiple variables, and execute multi-step supply chain decisions without human intervention. It spans demand forecasting, warehouse optimization, transportation routing, procurement automation, and last-mile delivery orchestration across retail, manufacturing, healthcare, and food and beverage industries.

EMR analysts gathered primary data across 5 regions and 9 segment dimensions, combining enterprise interviews, vendor briefings, and public financial disclosures with analyst validation. Buyers consistently cited labor cost reduction and supply chain resilience as the two dominant investment triggers accelerating agentic AI adoption ahead of schedule.

Agentic AI solves a structural problem that rule-based automation cannot: the ability to handle exceptions, reroute dynamically, and optimize across competing objectives simultaneously. Procurement teams, logistics directors, and chief supply chain officers drive purchase decisions, typically evaluating platforms on integration depth with existing ERP and TMS environments, total cost of ownership, and measurable KPI outcomes within the first operating year.

Three forces are compressing adoption timelines in 2025. Randstad’s 2025 report confirms 76% of logistics firms face acute talent shortages, while 60% of logistics roles are undergoing AI and robotics transformation. Simultaneously, U.S. tariffs reaching 145% on Chinese imports in April 2025 created immediate demand for autonomous rerouting tools. Gartner projects that 40% of enterprise applications will embed task-specific AI agents by end of 2026, up from just 5% in 2025, confirming the pace of platform-level adoption across supply chain software stacks.

Deployment Mode Analysis

Cloud-based deployment dominates with 63.73% due to hyperscaler AI agent packaging and consumption pricing.

In 2025, cloud-based deployment held a dominant position in the agentic AI in supply chain and logistics market with a 63.73% share. Hyperscalers bundle multi-agent orchestration directly into consumption-based services, reducing the capital barrier for enterprises running complex forecasting and routing workloads. Oracle and Microsoft announced a joint integration blueprint in October 2025 to pipe live factory sensor feeds directly into AI-driven supply chain workflows, reinforcing cloud as the default architecture for real-time agentic decision-making.

Hybrid deployment is accelerating as data-residency laws and plant-level latency requirements push enterprises to split inference workloads between edge nodes and central cloud environments. Enterprises processing sensitive supplier contracts or operating in GDPR-regulated jurisdictions route master data on-premise while retraining agent policies overnight using aggregated cloud telemetry. This bifurcated topology is now standard among tier-one automotive and pharmaceutical supply chains where regulatory compliance and sub-second response times must coexist.

On-premise deployment retains relevance in defense logistics, regulated pharmaceutical distribution, and public-sector procurement environments where data sovereignty requirements prohibit external cloud routing. However, container-based portability and confidential compute advances are gradually eroding pure on-premise deployments even in these sensitive verticals. Most operators pursuing on-premise today are managing legacy transitions rather than making net-new architectural decisions against cloud.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Cloud-based | 63.73% | Hyperscaler AI agent bundling and consumption pricing |

| Hybrid | – | Data residency laws and edge latency requirements |

| On-Premise | – | Defense and pharma data sovereignty mandates |

Technology Analysis

Machine Learning dominates with 39.42% due to proven forecasting accuracy across high-volume SKU environments.

In 2025, machine learning held a dominant position in the agentic AI in supply chain and logistics market with a 39.42% share. ML models underpin demand forecasting, inventory rebalancing, and carrier-mix optimization across retail and manufacturing verticals, where pattern recognition on historical transaction data delivers measurable stock-out reductions and excess inventory cuts. Walmart posted a 50% leap in U.S. store-fulfilled delivery sales in 2025, driven directly by AI forecasting and dynamic delivery window allocation across its distribution network.

Reinforcement Learning is gaining ground fastest as enterprises deploy multi-agent systems that negotiate capacity, price, and routing paths simultaneously across complex logistics networks. RL architectures allow agents to update policies continuously as freight rates, tariff structures, and port dwell times shift, delivering optimization outcomes that static ML models cannot match in volatile trade environments. The 145% U.S. tariff on Chinese imports imposed in April 2025 accelerated enterprise interest in RL-based rerouting agents that can respond to trade shocks within hours rather than planning cycles.

Computer Vision anchors warehouse automation use cases including automated damage detection, pallet identification, and goods-in verification at receiving docks. Natural Language Processing extends agentic capability into supplier communication, customs document processing, and freight rate negotiation, with platforms like HappyRobot automating freight broker workflows including rate negotiation, appointment booking, and document processing as of September 2025. Together these technologies expand the addressable scope of agentic AI beyond planning into physical execution layers.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Machine Learning | 39.42% | Demand forecasting accuracy across high-volume SKUs |

| Reinforcement Learning | – | Dynamic routing and tariff rerouting in volatile markets |

| Computer Vision | – | Warehouse automation and damage detection at scale |

| Natural Language Processing | – | Freight negotiation and customs document automation |

Organization Size Analysis

Large Enterprises dominate with 68.65% due to integration depth requirements and multi-region deployment budgets.

In 2025, large enterprises held a dominant position in the agentic AI in supply chain and logistics market with a 68.65% share. Tier-one operators possess the ERP and TMS infrastructure, data volumes, and cross-functional change management capacity needed to deploy multi-agent orchestration at scale across thousands of SKUs and dozens of supplier tiers. SAP‘s Joule agentic platform reached 40 specialized AI agents and 2,400 Joule Skills by Q1 2026, including a Production Planning and Operations Agent targeting enterprise supply chain order release without human planner intervention.

Small and Medium Enterprises represent the market’s fastest-expanding adoption cohort as cloud-native agent toolkits lower the entry barrier and outcome-based pricing models shift financial risk to vendors. SMEs in third-party logistics, food distribution, and industrial components are deploying lightweight agentic tools for freight rate comparison, carrier selection, and basic demand sensing without requiring dedicated AI engineering teams. Augment Technologies raised USD 85 million in September 2025 specifically to expand AI teammate tools targeting SME logistics operators, signaling strong venture conviction in this segment’s growth trajectory.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Large Enterprises | 68.65% | Multi-region deployment scale and ERP integration depth |

| Small and Medium Enterprises | – | Cloud-native toolkits and outcome-based pricing models |

Component Analysis

Software Platforms dominate with 57.8% due to unified decision environments coupling planning and execution layers.

In 2025, software platforms held a dominant position in the agentic AI in supply chain and logistics market with a 57.8% share. Vendors bundle multi-agent orchestration, digital twin modeling, and low-code customization into platforms that span planning and execution without requiring separate point solutions. Manhattan Associates unveiled its Agent Foundry within Manhattan Active solutions in May 2025, enabling autonomous digital agents for supply chain commerce execution with general availability starting Fall 2025.

Services covering integration, consulting, and change management are growing at the fastest rate within the component mix as enterprises face complex data governance and process re-engineering requirements when operationalizing agentic systems at scale. Integrators retrofit legacy WMS event buses to expose high-velocity data streams, while advisory teams codify governance models that delegate bounded decision rights to software agents. Enterprises consistently report that services spend equals or exceeds platform license costs over the first three years of an agentic AI implementation.

AI-enabled Hardware Systems including edge compute gateways, smart sensors, and robotics controllers remain a smaller revenue base but are essential for yard automation, port operations, and micro-fulfillment nodes where inference must happen close to material flow. NVIDIA‘s GPU infrastructure underpins the foundation model layer that major platform vendors rely on for agent training and real-time inference, positioning hardware as a critical enabler even as its direct revenue share remains modest relative to software and services.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Software Platforms | 57.8% | Unified planning and execution decision environments |

| Services | – | Integration complexity and change management lift |

| AI-enabled Hardware Systems | – | Edge inference for yard and micro-fulfillment automation |

Autonomy Level Analysis

Full Autonomy leads the Autonomy Level segment due to measurable ROI in high-volume repetitive logistics decisions.

In 2025, Full Autonomy held a leading position in the agentic AI in supply chain and logistics market. Fully automated execution delivers the clearest ROI in logistics decisions that are high-frequency, data-rich, and consequence-bounded — carrier selection, slot booking, inventory replenishment triggers, and route optimization across known networks. C.H. Robinson launched its Agentic Supply Chain category in October 2025, enabling instant AI deployment for real-time logistics decisions across industries without human approval loops at the transaction level.

Human-in-the-Loop systems remain standard for decisions carrying significant financial, regulatory, or reputational risk, including supplier contract renegotiation, cross-border customs filings, and exception handling in cold chain pharmaceutical logistics. These architectures ensure human judgment anchors high-stakes outcomes while agents handle the data aggregation, option generation, and recommendation steps that previously consumed planner time. Most enterprise deployments in 2025 operate in HITL mode for strategic sourcing while running full autonomy for transactional execution.

Human-on-the-Loop configurations represent an intermediate maturity state where agents execute autonomously but surface alerts to human supervisors who can intervene within defined time windows. This model suits food and beverage cold chain operations and pharmaceutical distribution where regulatory frameworks require documented human oversight without mandating per-transaction approval. As trust in agent decision quality builds through audit trails and KPI validation, operators are gradually shifting HoTL deployments toward full autonomy for well-understood decision classes.

Application Analysis

Demand Forecasting and Planning dominates with 35.86% due to direct revenue impact from stock-out and overstock reduction.

In 2025, demand forecasting and planning held a dominant position in the agentic AI in supply chain and logistics market with a 35.86% share. Agentic forecasting systems ingest clickstream, IoT, and POS signals simultaneously to rebalance inventory and trigger replenishment at a cadence that weekly planning cycles cannot match. General Mills confirmed multi-million-dollar savings after deploying agentic forecasting and inventory optimization, with agentic systems reducing both stock-out frequency and excess inventory carrying costs across its North American distribution network.

Transportation, routing, and fleet management are advancing at one of the fastest application-level growth rates as reinforcement learning agents weigh congestion, port dwell times, tariff exposure, and driver-hours regulations simultaneously to produce dispatch grids that refresh continuously. FedEx Freight is targeting a 12% operating margin for 2026 with USD 8.7 billion annual revenue, leveraging agentic AI built on Salesforce, Microsoft, and Oracle native platforms alongside custom agents to refactor its legacy application stack post-spinoff.

Procurement and Sourcing Automation is scaling as multi-objective agents negotiate supplier agreements across price, ESG score, and geopolitical exposure simultaneously. Warehouse and Fulfillment Optimization benefits directly from robotics integration, with more than 60% of Walmart U.S. stores served by automated distribution centers and over 50% of eCommerce packages flowing through automated DCs by early 2026. Last-Mile Delivery Orchestration is emerging as the highest-growth application as urban autonomous delivery networks scale from pilot to commercial deployment.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Demand Forecasting and Planning | 35.86% | Direct revenue impact from inventory accuracy gains |

| Transportation Routing and Fleet Management | – | RL agents optimizing multi-variable dispatch grids |

| Procurement and Sourcing Automation | – | Multi-objective supplier negotiation at scale |

| Last-Mile Delivery Orchestration | – | Urban autonomous delivery network commercialization |

| Warehouse and Fulfillment Optimization | – | Robotics integration and automated DC expansion |

Pricing Model Analysis

Subscription-based pricing leads the Pricing Model segment due to predictable cost structures preferred by enterprise procurement.

In 2025, subscription-based pricing held a leading position in the agentic AI in supply chain and logistics market. Enterprise procurement teams favor annual subscription structures that allow multi-year budget planning and align vendor incentives with platform utilization rather than one-time license revenue. Kinaxis demonstrated the commercial strength of this model through consistent SaaS revenue growth on new enterprise planning wins, with subscription contracts anchoring long-term customer relationships across retail and CPG verticals.

Outcome-based pricing with KPI-guarantee contracts is gaining traction among buyers who lack internal benchmarks for agentic AI ROI and want vendors to share performance risk. These contracts tie platform fees to measurable improvements in on-time delivery rates, inventory turns, or freight cost per unit, creating alignment between vendor and operator that subscription models alone cannot provide. Several leading integrators now offer hybrid structures combining a base subscription with outcome-linked performance bonuses tied to quarterly supply chain KPI reviews.

Usage-based and consumption-based pricing appeals to SMEs and enterprises running variable workload profiles, such as seasonal retailers and event-driven manufacturers who need agent capacity to scale elastically during peak periods without committing to annual seat-based contracts. As hyperscalers commoditize the underlying inference infrastructure, consumption pricing is expected to migrate down from cloud platforms into application-layer agentic tools, compressing per-decision costs and broadening the accessible buyer base across mid-market logistics operators.

Industry Vertical Analysis

Retail and E-Commerce dominates with 34.87% due to established omnichannel data infrastructure and high SKU velocity.

In 2025, retail and e-commerce held a dominant position in the agentic AI in supply chain and logistics market with a 34.87% share. Online order volumes and SKU complexity create a natural deployment environment for agentic systems that must rebalance inventory, trigger micro-fulfillment, and orchestrate drop-ship networks at millisecond cadence. Amazon invested more than USD 340 billion in U.S. infrastructure, AI, and logistics in 2025, with operating income reaching USD 80.0 billion, up from USD 68.6 billion in 2024, partly driven by AI-enabled same-day delivery and agentic commerce tools.

Manufacturing is adopting agentic AI to synchronize production planning with supplier availability, machine capacity, and logistics slots simultaneously. Advanced and intelligent manufacturing operations are accelerating this shift by embedding agentic AI directly into production execution systems to reduce unplanned downtime and improve throughput across global facilities. Siemens posted record net income of EUR 10.4 billion for fiscal year 2025 with orders climbing 5% to EUR 78.9 billion, driven by AI and software integration across its industrial operations and supply chain platforms. Academic research published in Taylor and Francis in February 2026 confirms Siemens is running live agentic digital twin systems to autonomously model supplier failures and tariff shocks across more than 10,000 SKUs.

| Sub-segment | Share % | Primary Driver |

|---|---|---|

| Retail and E-Commerce | 34.87% | Omnichannel data depth and high SKU velocity |

| Manufacturing | – | Production-logistics synchronization and digital twins |

| Healthcare and Pharmaceuticals | – | Cold chain complexity and regulatory traceability |

| Food and Beverage | Perishability windows and dynamic repricing needs | |

| Automotive | – | Just-in-time assembly and tier-two disruption management |

Agent Architecture Analysis

Multi-Agent Systems dominate with 56.87% due to superior performance on complex multi-variable logistics orchestration.

In 2025, multi-agent systems held a dominant position in the agentic AI in supply chain and logistics market with a 56.87% share. Fleets of collaborative agents negotiate capacity, price, and routing paths simultaneously across supplier networks, carrier ecosystems, and fulfillment centers, delivering optimization outcomes that single-agent architectures cannot achieve on problems with competing objectives. Walmart and Siemens are already running unified multi-agent supply chain architectures in production, as confirmed by Deloitte Insights research published in March 2026.

Single-Agent Systems serve focused, bounded use cases where problem scope is narrow and decision authority is clearly defined. Customs classification agents, freight rate comparison tools, and individual warehouse slotting optimizers operate effectively as single-agent deployments that deliver measurable value without the orchestration complexity of multi-agent frameworks. Deloitte’s March 2026 agentic supply chain report notes that most enterprise deployments begin with single-agent proofs of concept before expanding to multi-agent orchestration as integration confidence and governance frameworks mature.

Market Segments Covered in the Report

By Deployment Mode

- Cloud-based

- Hybrid

- On-Premise

By Technology

- Machine Learning

- Reinforcement Learning

- Computer Vision

- Natural Language Processing (NLP)

By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By Component

- Software Platforms

- Services (Integration and Consulting)

- AI-enabled Hardware Systems

By Autonomy Level

- Full Autonomy (Fully Automated Execution)

- Human-in-the-Loop (HITL)

- Human-on-the-Loop (HoTL)

By Application

- Demand Forecasting and Planning

- Transportation Routing and Fleet Management

- Procurement and Sourcing Automation

- Last-Mile Delivery Orchestration

- Warehouse and Fulfillment Optimization

By Pricing Model

- Subscription-based

- Outcome-based (KPI-guarantee contracts)

- Usage-based / Consumption-based

By Industry Vertical

- Retail and E-Commerce

- Healthcare and Pharmaceuticals

- Manufacturing

- Food and Beverage

- Automotive

By Agent Architecture

- Multi-Agent Systems

- Single-Agent Systems

Agentic AI in Supply Chain and Logistics Market Regional Insights

North America Holds 42.9% Share, Anchored by Enterprise Scale and Venture-Backed Innovation

North America generated 42.9% of global agentic AI in supply chain and logistics revenue in 2025, supported by the world’s largest domestic consumption base, deep cloud infrastructure penetration, and the highest concentration of enterprise logistics operators deploying autonomous decision systems at scale. UPS delivered 5.2 billion packages in 2025 on USD 88.7 billion in revenue, anchoring the region’s logistics scale, while AI logistics startups raised a combined USD 129 million in a single week in September 2025 — Augment Technologies securing USD 85 million and HappyRobot USD 44 million — signaling sustained venture conviction in North American agentic logistics innovation. Operators evaluating market entry should prioritize integration partnerships with Oracle, SAP, and Microsoft, whose enterprise platforms now serve as the primary deployment layer for agentic supply chain applications across the region.

Asia-Pacific Agentic AI in Supply Chain and Logistics Market Trends

Asia-Pacific is the fastest-growing region at a 16.1% CAGR through 2035, driven by China’s manufacturing scale, India’s expanding third-party logistics base, and the urgent need to orchestrate outbound flows disrupted by U.S. tariffs reaching 145% on Chinese imports in April 2025. Amazon committed USD 35 billion to India for AI and logistics operations expansion, with Amazon Seller Services operating revenue rising 19% to ₹30,139 crore in FY25, making India the region’s single largest agentic logistics investment announcement of 2025. Suppliers entering Asia-Pacific should build cloud-native deployment architectures that accommodate India’s Production-Linked Incentive schemes and China’s integrated supplier network requirements simultaneously, as buyers in both markets prioritize cost-effective platforms over premium feature sets.

Europe Agentic AI in Supply Chain and Logistics Market Trends

Europe maintains resilient growth underpinned by sustainability mandates, shipbuilding modernization programs, and the EU AI Act’s accountability requirements that are reshaping how enterprises architect agentic decision systems across multi-jurisdictional supply chains. DHL Group recorded EUR 82.9 billion in FY2025 revenue with EBIT reaching EUR 6.1 billion, up 3.7%, with DHL Supply Chain delivering 8.7% EBIT growth as European agentic logistics adoption accelerated across its regional footprint. Regulatory compliance infrastructure — particularly GDPR-compliant data pipeline redesign and CBAM quarterly reporting automation — is emerging as a competitive differentiator for platform vendors that can deliver certifiable audit trails alongside operational optimization outcomes.

Latin America Agentic AI in Supply Chain and Logistics Market Trends

Latin America is building an agentic logistics foundation on the back of automotive manufacturing expansion and a rising installed base for cloud-based supply chain tools across Brazil, Mexico, and Argentina. ESAB‘s strategic acquisitions in Brazil and South America during 2024 expanded automation and service capabilities across the Americas, illustrating how global industrials are treating the region as a growth frontier for integrated supply chain technology rather than a secondary market. First-time automation buyers in Latin America favor outcome-based pricing models that reduce adoption risk, making the region a natural testing ground for KPI-guarantee contract structures that platform vendors are now packaging for emerging market rollouts.

Middle East and Africa Agentic AI in Supply Chain and Logistics Market Trends

The Middle East and Africa present a dual-speed adoption profile, with Gulf Cooperation Council states deploying agentic AI across port operations and pharmaceutical cold chains while sub-Saharan markets remain in early-stage evaluation driven by infrastructure variability and talent constraints. DHL Group‘s EUR 2 billion commitment through 2030 to expand GDP-certified multi-temperature pharma hubs spans the Americas, Asia-Pacific, and EMEA, with Middle East hub expansion forming a core component of the cold chain infrastructure build. Saudi Arabia’s Vision 2030 industrial diversification program is channeling direct investment into logistics technology adoption, positioning the Kingdom as the region’s primary demand anchor for enterprise-grade agentic supply chain platforms through 2035.

| Region | Share % | Key Growth Driver |

|---|---|---|

| North America | 42.9% | Enterprise scale and venture-backed AI logistics innovation |

| Asia-Pacific | Fastest growing at 16.1% CAGR | Tariff disruption driving autonomous rerouting adoption |

| Europe | – | EU AI Act compliance and sustainability mandates |

| Latin America | – | Automotive expansion and outcome-based adoption models |

| Middle East and Africa | – | Gulf pharma cold chain and Vision 2030 investments |

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Top Use Cases

- 1. Autonomous Demand Forecasting & Adaptive Planning: Agentic AI moves beyond static historical forecasts by continuously ingesting real-time signals such as POS data, weather, social media trends, and macroeconomic indicators to adjust predictions on the fly. It doesn’t just update numbers — it autonomously triggers downstream actions like modifying procurement plans, rebalancing inventory, and alerting stakeholders to anomalies.

- 2. Dynamic Route Planning & Real-Time Logistics Orchestration: Logistics agents integrate live traffic, weather, vehicle load, and delivery deadlines to compute optimal routes, then dynamically reroute fleets mid-transit when disruptions occur (e.g., port shutdowns, breakdowns) without human intervention. For example, Uber Freight uses AI-driven matching to reduce empty miles by 10–15%, while Flexport’s agents reportedly cut transportation costs by 30% and transit times by 25%.

- 3. Smart Inventory Rebalancing & Optimization: Inventory agents evaluate demand patterns, order velocity, and transit costs across the network to autonomously move stock between warehouses before human planners detect imbalances. They can automatically adjust stock levels in real time, reducing carrying costs and waste while preventing stockouts.

- 4. Exception Handling & Supply Chain Risk Mitigation: Rather than waiting for humans to spot problems, agentic AI continuously monitors for exceptions — late shipments, stuck POs, missing materials — and acts immediately by reassigning carriers, updating ETAs, and notifying warehouses. At a strategic level, these agents monitor global events to predict disruptions and automatically execute contingency plans, which is critical since 75% of companies now consider supply chain resilience a top priority.

- 5. Intelligent Procurement & Last-Mile Delivery Automation: Procurement agents autonomously evaluate suppliers, negotiate terms, and place orders based on forecasted demand and supplier risk metrics. On the delivery side, last-mile assistants allocate drops to drivers, optimize sequences, and navigate traffic conditions, while returns agents manage authorizations, pickups, and restock/refurbish/dispose decisions.

Regulatory Landscape

The EU AI Act, which came into force in 2024 with phased compliance deadlines through 2026, classifies high-autonomy supply chain decision systems under its risk-tiered framework, requiring enterprises to document agent decision logic, maintain audit trails, and ensure human oversight mechanisms for consequential logistics decisions. This is reshaping platform architecture across European operations as vendors embed explainability layers and decision logging into agentic systems that previously operated as black-box optimizers.

U.S. Customs and Border Protection is advancing ACE 2.0 modernization through 2025 to enable AI anomaly detection and global data exchange for customs compliance, directly expanding the technical foundation that agentic trade compliance platforms rely on for automated sanctions screening across 85 embargo lists. Agentic platforms like Digicust are already automating CBAM quarterly filings and multi-jurisdictional export control workflows on top of this evolving infrastructure, turning regulatory modernization into a commercial deployment opportunity.

GDPR enforcement and cross-border data sovereignty laws are constraining multi-jurisdictional agentic deployments that require training data and operational telemetry to flow freely across national boundaries. Enterprises operating across the EU, U.S., and Asia-Pacific are redesigning data pipelines to comply with residency requirements, creating demand for hybrid deployment architectures that confine sensitive master data on-premise while routing non-sensitive operational data to cloud-based agent training environments.

Trends

Gartner: 40% of Enterprise Apps Will Embed AI Agents by End of 2026

Enterprise-wide agentic AI orchestration frameworks are replacing point-solution automation across the supply chain as Gartner projects 40% of enterprise applications will integrate task-specific AI agents by end of 2026 — up from less than 5% in 2025 — representing an eightfold increase that signals platform-level architectural transformation rather than incremental feature addition. Walmart, Siemens, and SAP are already deploying unified multi-agent supply chain architectures that span planning, execution, and compliance functions within single orchestration environments, establishing the operational blueprint that mid-market operators will follow through 2028. Gartner further projects agentic AI will account for 30% of enterprise software sales by 2035, up from just 2% in 2025, confirming that the current adoption wave is a structural market shift rather than a technology cycle.

Digital twin integration with agentic AI is becoming the flagship supply chain resilience strategy as academic research published in the International Journal of Production Research in February 2026 confirms that Walmart and Siemens are running live agentic digital twin systems to autonomously model supplier failures, port closures, and tariff shocks across more than 10,000 SKUs without human intervention. The growing adoption of digital twin in manufacturing is enabling real-time visibility into supplier networks, production lines, and logistics flows that static planning tools cannot replicate. These systems compress scenario analysis from multi-day planning exercises into continuous background processes, enabling operators to identify and respond to supply chain disruptions before they materialize into service failures or inventory gaps. The convergence of digital twin fidelity and agentic decision speed is creating a new competitive capability class that separates operators with real-time resilience infrastructure from those still running weekly S&OP cycles.

Sustainability-driven AI route optimization is rising to boardroom priority as the green logistics market reaches USD 1.2 trillion in 2025 and carbon accounting becomes embedded in carrier selection algorithms under EU CBAM and voluntary corporate net-zero commitments. LLM-powered multi-agent customs and trade compliance automation is gaining rapid traction as U.S. CBP advances ACE 2.0 modernization to enable AI anomaly detection and global data exchange, while agentic platforms automate sanctions screening across 85 embargo lists and multi-jurisdictional export control workflows simultaneously. Together these sustainability and compliance automation trends are expanding the value proposition of agentic supply chain platforms beyond cost reduction into risk management and regulatory assurance, broadening the executive buyer base beyond supply chain functions into legal, compliance, and ESG leadership teams.

Trends

Gartner: 40% of Enterprise Apps Will Embed AI Agents by End of 2026

Enterprise-wide agentic AI orchestration frameworks are replacing point-solution automation across the supply chain as Gartner projects 40% of enterprise applications will integrate task-specific AI agents by end of 2026 — up from less than 5% in 2025 — representing an eightfold increase that signals platform-level architectural transformation rather than incremental feature addition. Walmart, Siemens, and SAP are already deploying unified multi-agent supply chain architectures that span planning, execution, and compliance functions within single orchestration environments, establishing the operational blueprint that mid-market operators will follow through 2028. Gartner further projects agentic AI will account for 30% of enterprise software sales by 2035, up from just 2% in 2025, confirming that the current adoption wave is a structural market shift rather than a technology cycle.

Digital twin integration with agentic AI is becoming the flagship supply chain resilience strategy as academic research published in the International Journal of Production Research in February 2026 confirms that Walmart and Siemens are running live agentic digital twin systems to autonomously model supplier failures, port closures, and tariff shocks across more than 10,000 SKUs without human intervention. These systems compress scenario analysis from multi-day planning exercises into continuous background processes, enabling operators to identify and respond to supply chain disruptions before they materialize into service failures or inventory gaps. The convergence of digital twin fidelity and agentic decision speed is creating a new competitive capability class that separates operators with real-time resilience infrastructure from those still running weekly S&OP cycles.

Sustainability-driven AI route optimization is rising to boardroom priority as the green logistics market reaches USD 1.2 trillion in 2025 and carbon accounting becomes embedded in carrier selection algorithms under EU CBAM and voluntary corporate net-zero commitments. LLM-powered multi-agent customs and trade compliance automation is gaining rapid traction as U.S. CBP advances ACE 2.0 modernization to enable AI anomaly detection and global data exchange, while agentic platforms automate sanctions screening across 85 embargo lists and multi-jurisdictional export control workflows simultaneously. Together these sustainability and compliance automation trends are expanding the value proposition of agentic supply chain platforms beyond cost reduction into risk management and regulatory assurance, broadening the executive buyer base beyond supply chain functions into legal, compliance, and ESG leadership teams.

Key Drivers

Labor Shortage Forces 76% of Logistics Firms to Prioritize AI Automation in 2025

Randstad’s 2025 report confirms 76% of logistics organizations face acute talent shortages beyond the holiday season, with 60% of logistics roles undergoing AI and robotics transformation. Chronic workforce gaps in warehouse operations, freight brokerage, and last-mile dispatch are removing the human capacity buffer that traditionally absorbed demand spikes and exception handling. In our view, this labor constraint is the single most durable structural driver in this market, because it creates irreversible automation pressure that persists regardless of macroeconomic cycles.

Geopolitical tariff volatility is compressing enterprise decision timelines on agentic AI investment as U.S. tariffs reaching 145% on Chinese imports and 84% Chinese retaliatory tariffs in April 2025 made manual rerouting processes commercially untenable. McKinsey’s 2025 Supply Chain Risk Pulse identifies tariffs as the defining threat triggering digital transformation urgency, with 30% of global supply chain activities directly affected by the new U.S. tariff structure. Enterprises that deployed agentic scenario-simulation tools before April 2025 demonstrated measurably faster supplier rerouting than those relying on weekly planning cycles.

Real-time IoT sensor proliferation is creating the foundational data layer that enables agentic AI to execute autonomous multi-step decisions across freight, inventory, and cold chain networks simultaneously. Oracle and Microsoft announced a joint integration blueprint in October 2025 bridging Oracle Fusion Cloud SCM with Microsoft Azure IoT Operations, piping live factory sensor feeds directly into agentic supply chain workflows at production scale. This infrastructure convergence means the data readiness barrier that previously blocked agentic deployment is dissolving faster than vendor adoption timelines originally projected.

Restraints

Gartner Projects 40% of Agentic AI Projects Canceled by 2027 on Integration Costs

Legacy ERP and TMS infrastructure incompatibility creates a high-cost integration barrier that Gartner projects will cause over 40% of agentic AI supply chain projects to be canceled by 2027 due to escalating costs, technical debt, and inadequate risk controls. Many tier-one manufacturers operate multi-decade ERP stacks lacking modern APIs, making event-stream connectivity to agentic engines both technically complex and commercially expensive. Integration programs lasting 18 to 24 months and requiring dedicated middleware development erode near-term ROI expectations and extend the payback horizon beyond what many enterprise investment committees will approve.

Cross-border data sovereignty laws and the EU AI Act’s strict accountability requirements are constraining agentic AI deployment in multi-jurisdictional supply chains where training data and operational telemetry must remain within national boundaries. Enterprises must redesign data pipelines to comply simultaneously with GDPR, CBAM reporting mandates, and U.S. CBP ACE 2.0 modernization requirements, adding compliance engineering costs that divert budget from agentic capability development. This regulatory fragmentation is particularly acute for global third-party logistics providers operating across more than 10 jurisdictions, where a single unified agent architecture cannot satisfy all applicable data residency requirements without significant customization.

Workforce readiness gaps slow adoption even among enterprises that have resolved integration and compliance barriers, as CNC-equivalent operator training requirements for agentic platform management are outpacing available talent supply. Only 28% of logistics workers report access to AI training and upskilling programs despite 60% of their roles undergoing transformation, creating a change management bottleneck that delays go-live timelines and limits the operational scope of initial deployments. Smaller logistics operators facing both budget constraints and talent shortages are deferring agentic investments until platform vendors deliver more accessible onboarding experiences that reduce dependence on specialized AI engineering resources.

Growth Factors

Pharma Cold Chain Commits EUR 2 Billion Through 2030 as High-Value Agentic Arena

DHL Group committed EUR 2 billion through 2030 to expand AI-monitored, GDP-certified multi-temperature pharma hubs across the Americas, Asia-Pacific, and EMEA, establishing pharmaceutical cold chain as the highest-value near-term deployment arena for agentic logistics AI. Temperature excursion prevention, lot traceability, and regulatory audit automation align precisely with agentic AI’s core capability set, creating a vertically differentiated market where performance requirements justify premium platform pricing. DHL AI pilots already demonstrate up to 12% reduction in temperature-controlled shipment waste alongside measurable empty-mile and fuel use decreases, providing the ROI evidence that pharmaceutical logistics buyers require before committing to multi-year platform contracts.

Autonomous last-mile delivery is scaling from pilot to commercial deployment across urban markets, with the global autonomous last-mile delivery market valued at USD 21.5 billion in 2024 and projected to reach USD 228.74 billion by 2035 as Amazon, FedEx, and Starship Technologies accelerate ground robot and drone rollouts. Amazon India committed Rs 2,800 crore in April 2026 to expand logistics, quick commerce, and AI-driven operations, reflecting the scale of investment flowing into last-mile agentic infrastructure across high-density urban markets. This deployment wave creates demand for orchestration platforms that coordinate mixed fleets of human drivers, ground robots, and drones within unified agentic decision environments.

AI-native supply chain orchestration platforms are unlocking a new enterprise software category as SAP launches supply chain orchestration with Joule agentic AI targeting tariff impact assessment, multi-agent supplier rerouting, and compressing week-long disruption resolution cycles down to hours or minutes, with general availability planned for Q2 2026. SAP’s Joule platform reached 40 specialized AI agents and 2,400 Joule Skills by Q1 2026, with the Production Planning and Operations Agent autonomously validating material availability, capacity, and releasing production orders without human planner intervention. This category creation dynamic benefits established platform vendors with deep ERP integration while simultaneously opening opportunities for point-solution specialists that can demonstrate measurable KPI outcomes faster than large suite vendors.

Agentic AI in Supply Chain and Logistics Market Key Companies Insights

Blue Yonder leads enterprise planning revenue with its Autonomous Planning suite, commanding strong adoption among retail and CPG majors seeking end-to-end supply chain orchestration. The platform’s multi-agent architecture spans demand sensing, inventory optimization, and transportation execution within a unified environment that reduces the integration burden enterprises face when assembling point solutions. Blue Yonder’s installed base among tier-one retailers gives it structural advantage as buyers consolidate planning and execution onto fewer platforms through 2027.

We believe Oracle Corporation is positioning most aggressively for the next phase of agentic supply chain adoption, having launched new AI agents embedded in Oracle Fusion Cloud Applications in February 2026 — including a Planning Measure Expression Agent, Autonomous Sourcing Agent, and Service Parts Advisor Agent — followed by Fusion Agentic Applications for finance and supply chain in April 2026. Oracle’s October 2025 integration blueprint with Microsoft bridges Oracle Fusion Cloud SCM with Azure IoT Operations, creating a live sensor-to-agent pipeline that competitors have not yet replicated at equivalent enterprise scale. This sequenced product releases strategy positions Oracle to capture budget from enterprises consolidating ERP and agentic supply chain tooling onto a single vendor relationship.

Manhattan Associates extended its WMS dominance by unveiling Agent Foundry within Manhattan Active solutions in May 2025, enabling autonomous digital agents for supply chain commerce execution with general availability from Fall 2025. The company’s deep warehouse management heritage gives its agentic tools a credibility advantage in fulfillment-intensive verticals including e-commerce, grocery, and pharmaceutical distribution where warehouse execution accuracy directly determines customer experience outcomes. Manhattan’s strategy of embedding agentic capability into existing WMS deployments rather than requiring net-new platform purchases reduces buyer switching risk and accelerates adoption within its established customer base.

Pactum AI and C.H. Robinson represent the specialized agentic AI category that is challenging suite vendors on specific high-value use cases. Pactum AI focuses on autonomous supplier contract negotiation, having raised USD 20 million with Maersk participation to scale procurement copilots that negotiate contract clauses without human involvement. C.H. Robinson launched the Agentic Supply Chain category in October 2025, enabling instant AI deployment for real-time freight decisions, while HappyRobot raised USD 44 million in September 2025 to automate freight broker workflows including rate negotiation and appointment booking across TMS, ERP, and CRM integrations.

Key Companies

- CrewAI

- Oracle Corporation

- FourKites, Inc.

- Accenture

- Kinaxis Inc.

- Amazon Web Services, Inc.

- WiseTech Global (e2open)

- Manhattan Associates, Inc.

- GEP

- Capgemini

- C.H. Robinson Worldwide, Inc.

- NVIDIA Corporation

- Genpact

- IBM Corporation

- DHL Group

- Pactum AI

- Microsoft Corporation

- A.P. Moller – Maersk

- Infosys

- SAP SE

- project44, Inc.

- o9 Solutions, Inc.

- Coupa Software Incorporated

- Blue Yonder, Inc.

Recent Development

- April 2026: Oracle introduced Fusion Agentic Applications — a new class of enterprise applications for finance and supply chain operations powered by agentic AI, expanding its autonomous workflow suite beyond individual agents into integrated application architecture.

- February 2026: Oracle announced new AI agents embedded in Oracle Fusion Cloud Applications including a Planning Measure Expression Agent, Autonomous Sourcing Agent, and Service Parts Advisor Agent to automate planning, procurement, manufacturing, and logistics workflows.

- February 2026: Flexport launched a fleet of agentic AI tools led by Audit Your Customs Broker, an autonomous compliance agent that reviews past filings, identifies mistakes, and helps businesses recover tariff refunds.

- November 2025: DHL Group announced an enterprise partnership with HappyRobot to deploy AI agents for appointment scheduling, driver follow-up calls, and high-priority warehouse coordination across multiple regions.

- October 2025: C.H. Robinson launched the Agentic Supply Chain category, an intelligent ecosystem built on its Lean AI foundation that continuously senses, decides, and acts across freight lifecycles without human intervention per transaction.

- September 2025: HappyRobot raised a USD 44 million Series B round led by Base10 Partners, with participation from Andreessen Horowitz and Y Combinator, valuing the company at approximately USD 500 million and bringing total funding to USD 62 million.

- May 2025: Manhattan Associates unveiled Agentic AI assistants and Agent Foundry within Manhattan Active solutions at Momentum 2025, with general availability starting Fall 2025, enabling autonomous digital agents for supply chain commerce execution.

- December 2025: Oracle partnered with J.P. Morgan Payments to launch a supply chain finance solution integrated directly into Oracle Cloud ERP, supporting agentic finance workflows across enterprise supply chains.

Market Scope

| Report Features | Description |

|---|---|

| Market Size Value in 2025 | USD 9.2 Billion |

| Revenue Forecast in 2035 | USD 46.15 Billion |

| Growth Rate | CAGR of 17.5% from 2026 to 2035 |

| Base Year | 2025 |

| Historic Period | 2020 – 2024 |

| Forecast Period | 2026 – 2035 |

| Segments Covered | By Deployment Mode, By Technology, By Organization Size, By Component, By Autonomy Level, By Application, By Pricing Model, By Industry Vertical, By Agent Architecture |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, India, Japan, Australia, South Korea, Germany, France, United Kingdom, Spain, Italy, Brazil, Mexico, GCC, South Africa |

| Key Companies | CrewAI, Oracle Corporation, FourKites, Accenture, Kinaxis, Amazon Web Services, WiseTech Global, Manhattan Associates, GEP, Capgemini, C.H. Robinson, NVIDIA, Genpact, IBM, DHL Group, Pactum AI, Microsoft, A.P. Moller – Maersk, Infosys, SAP SE, project44, o9 Solutions, Coupa Software, Blue Yonder |