What is the US Ambient Clinical Intelligence Solutions Market?

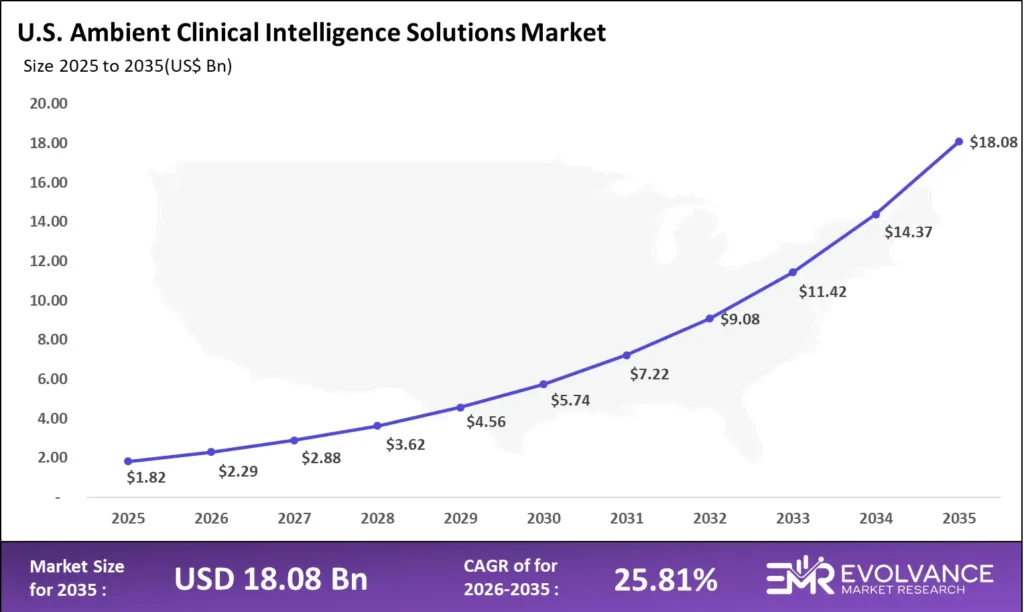

The US ambient clinical intelligence solutions market was valued at USD 1.82 billion in 2025 and is projected to reach approximately USD 18.08 billion by 2035, growing at a CAGR of 25.81% during the forecast period 2026 to 2035. Physician documentation burden is a top structural driver. Accelerating AI adoption in clinical settings is a second key force. CMS-mandated interoperability requirements add a third. Healthcare organizations using ambient AI report 2.3 hours saved per physician per clinical day.

Health systems face two core investment pressures. First, legacy EHR integration is complex. Second, physician change management slows enterprise rollouts. AMA survey data shows physicians spend 4.5 hours daily on EHR tasks. Over 63% cite documentation burden as their primary burnout driver. Ambient AI vendors can now show documented ROI before procurement approval. This reduces friction for CIOs evaluating multi-year digital investments.

Ambient clinical intelligence platforms listen to physician-patient conversations in real time. AI generates structured clinical notes automatically. EHR fields are populated without physician keyboard input. Diagnostic context is surfaced during the encounter. Care gaps are flagged in real time. This is a fundamental redesign of how clinical knowledge is captured. It is not a minor workflow improvement.

US Ambient Clinical Intelligence Market Highlights: Key Data at a Glance

- Market value: USD 1.82 billion in 2025, forecast to USD 18.08 billion by 2035 at 25.81% CAGR

- Dominant solution: AI-Powered Voice Documentation with 52.4% revenue share

- Dominant deployment: Cloud-Based with 68.3% revenue share

- Dominant end-user: Hospitals & Health Systems with 58.7% revenue share

- Dominant AI level: LLM-Powered platforms with 44.1% share

- Dominant care setting: Outpatient with 46.8% share

- Fastest-growing specialty: Behavioral health and primary care

- Regulatory tailwind: ONC HTI-1 rule and CMS interoperability mandates

- Physician adoption rate: 34% of US physicians using ambient AI scribing by end of 2025

- Leading platforms: Microsoft DAX Copilot, Ambience Healthcare, Abridge, Suki AI

Market Overview: Why US Ambient Clinical Intelligence Adoption Is Accelerating

This market covers AI-powered platforms that capture and structure clinical conversations in real time. Applications include documentation, decision support, analytics, and patient engagement. The scope is limited to US healthcare delivery settings. It excludes general speech recognition not built for clinical use. It also excludes traditional transcription without AI-generated structured output.

This analysis draws on health system disclosures, vendor earnings, EHR partnership announcements, and CMS filings. Segment shares were cross-referenced against revenues from Microsoft Nuance, Epic Systems, and Oracle Health. Physician adoption survey data was combined with fiscal disclosures. The result is a forecast grounded in verifiable deployment evidence.

Physician behavior has shifted from skepticism to active demand. Proof-of-value is now available in peer-reviewed publications. University of Michigan Health, UCHealth, and Vanderbilt Medical Center have each published outcomes data. This reference evidence accelerates purchasing at peer institutions. The typical health technology adoption curve is compressing significantly.

Three buyer profiles define procurement behavior. Large integrated delivery networks sign enterprise platform contracts with EHR-bundled ambient AI. Ambulatory clinics adopt per-physician SaaS models with minimal IT overhead. Telehealth providers embed ambient AI as a service quality differentiator. Each profile has different benchmarks and timelines. Vendors must segment their go-to-market accordingly.

The total addressable market is expanding on two fronts simultaneously. Depth of adoption within existing health system accounts is increasing. Breadth of adoption across new buyer types is also widening. Rural hospitals, federally qualified health centers, and military treatment facilities are all entering active evaluation phases. This dual expansion dynamic supports a CAGR that is unlikely to plateau before 2030.

The investment required to build a competitive ambient clinical intelligence platform has risen sharply. Training LLMs on specialty clinical data requires significant compute and annotation infrastructure. Earning EHR certification credentials requires sustained partnership investment. Vendors who delay investment face compounding disadvantage as certified incumbents build deeper health system relationships. Capital deployment in 2025 and 2026 will determine the competitive structure of this market through 2035.

Solution Type Analysis

AI-Powered Voice Documentation Dominates with 52.4% Revenue Share

EHR Integration Depth and Physician Adoption Velocity Drive Market Leadership

| Solution Type | Share % | Primary Driver |

|---|---|---|

| AI-Powered Voice Documentation | 52.4% | EHR-integrated scribing and physician burnout reduction |

| Real-Time Clinical Decision Support | 22.1% | Diagnostic AI alerts and evidence-based care gap identification |

| Predictive Analytics Platforms | 15.3% | Population health risk stratification and readmission prevention |

| Patient Engagement Intelligence | 10.2% | Post-visit follow-up automation and chronic disease monitoring |

AI-Powered Voice Documentation holds a 52.4% share in 2025. Its revenue model is structurally superior to other categories. Per-physician subscriptions generate recurring revenue. Usage expands as physicians onboard and document more encounter types. Documentation tools also serve as platform entry points. Physicians who adopt ambient scribing become buyers of decision support and analytics modules next.

Real-Time Clinical Decision Support is the fastest-growing segment. AI platforms surface diagnostic guidance during recorded encounters. They flag drug interactions and care protocol gaps. This eliminates the lookup friction that reduces engagement with traditional CDS tools. Platforms that embed decision support within ambient workflows see higher physician interaction rates. Predictive Analytics Platforms are gaining traction in value-based care contracts. They directly affect shared savings performance and quality bonus payments.

Deployment Mode Analysis

Cloud-Based Dominates with 68.3% Revenue Share

EHR API Integration and Per-Physician Subscription Economics Anchor Cloud Leadership

| Deployment Mode | Share % | Primary Driver |

|---|---|---|

| Cloud-Based | 68.3% | Elastic scaling, EHR vendor API integration, and subscription pricing |

| On-Premises | 18.4% | Data sovereignty, VA/DoD requirements, and high-security mandates |

| Hybrid | 13.3% | PHI processing on-site with cloud-based analytics and model training |

Cloud-Based deployment holds 68.3% share in 2025. Cloud-native platforms integrate directly with Epic, Oracle Cerner, and athenahealth APIs. Deployment does not require health system IT infrastructure changes. Microsoft Azure Health Data Services and AWS HealthLake provide HIPAA-compliant hosting. These environments satisfy PHI requirements for most US health systems. The primary compliance objection to cloud adoption has largely been resolved.

On-Premises deployment remains essential for specific buyers. Veterans Affairs, the Military Health System, and high-security academic medical centers often cannot use cloud hosting. These deployments carry significant price premiums. On-premises contracts average 2.7 times the value of cloud equivalents. Hybrid architectures process PHI locally for compliance. Cloud compute is still used for AI model training and population analytics.

End-User Analysis

Hospitals and Health Systems Dominate with 58.7% Revenue Share

Enterprise Licensing Scale and EHR Standardization Drive Segment Leadership

| End-User Segment | Share % | Primary Driver |

|---|---|---|

| Hospitals & Health Systems | 58.7% | Enterprise licensing, physician burnout reduction, EHR integration |

| Ambulatory & Outpatient Clinics | 21.4% | Per-physician SaaS adoption and visit volume productivity gains |

| Specialty Practices | 12.6% | High-complexity documentation and specialty-specific AI training |

| Home Health & Telehealth Providers | 7.3% | Virtual visit ambient capture and remote monitoring integration |

Hospitals and Health Systems hold 58.7% of end-user revenue in 2025. Large integrated delivery networks treat physician burnout as an existential retention challenge. Ambient AI deployment delivers documented ROI. Benefits include reduced transcription costs, improved satisfaction scores, and faster note completion. Physician replacement costs range from USD 500,000 to USD 1 million each. Health system CMOs now classify ambient AI as a retention infrastructure investment, not a discretionary expense.

Ambulatory Clinics represent the highest per-physician growth opportunity through 2035. Cloud-native platforms cost USD 300 to USD 600 per physician per month. This bypasses capital budgeting approval in smaller practice environments. Specialty Practices in dermatology, orthopedics, and oncology use specialty-trained models. These models understand procedure-specific terminology and ICD-10 requirements. They outperform general clinical models significantly in accuracy. Telehealth providers using ambient AI create a quality signal that drives patient platform selection.

AI Integration Level Analysis

LLM-Powered Platforms Lead with 44.1% Share

GPT-4 and Claude-Class Models Replace Legacy ASR-Only Documentation Tools

| AI Integration Level | Share % | Primary Driver |

|---|---|---|

| LLM-Powered (Full Clinical Summarization) | 44.1% | GPT-4/Claude-class models producing structured clinical notes |

| NLP/ASR (Structured Transcription) | 35.8% | Legacy ambient scribing and voice-to-text documentation |

| Multimodal AI (Audio + Video + EHR Context) | 20.1% | Next-generation platforms integrating visual and contextual signals |

LLM-Powered platforms hold the dominant share in 2025. They produce complete SOAP note structures from ambient audio. Assessment and plan narratives are generated automatically. ICD-10 coding suggestions are included. Physicians only need to review and attest the output. Significant post-editing is not required. The quality gap versus traditional transcription has accelerated migration timelines significantly.

Multimodal AI is the frontier investment category. It integrates ambient audio with computer vision analysis of patient presentation. Real-time EHR data retrieval is also included. Decision support is surfaced contextually during the encounter. This creates a unified clinical intelligence platform. Multimodal AI will define competitive positioning through 2030 and beyond. Early investors in multimodal capabilities are building a durable technology moat.

Key Market Segments

By Solution Type

- AI-Powered Voice Documentation

- Real-Time Clinical Decision Support

- Predictive Analytics Platforms

- Patient Engagement Intelligence

By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

By End-User

- Hospitals & Health Systems

- Ambulatory & Outpatient Clinics

- Specialty Practices

- Home Health & Telehealth Providers

By AI Integration Level

- NLP/ASR (Structured Transcription)

- LLM-Powered (Full Clinical Summarization)

- Multimodal AI (Audio + Video + EHR Context)

By Care Setting

- Inpatient

- Outpatient

- Virtual / Telehealth

Regional Analysis of the US Ambient Clinical Intelligence Market

Northeast and West Coast Lead; Sun Belt Is the Fastest-Growing Region

| US Region | Share % | Key Driver |

|---|---|---|

| Northeast (NY, MA, PA, CT) | 32.4% | Academic medical center density and early health-tech adoption |

| West Coast (CA, WA, OR) | 26.1% | Health-tech startup ecosystem and large IDN deployment programs |

| Sun Belt (TX, FL, AZ, GA) | 22.8% | Rapid physician workforce expansion and ambulatory care growth |

| Midwest (IL, OH, MI, MN) | 18.7% | Large regional health system enterprise deployments |

The Northeast holds the largest US regional share. Mass General Brigham, NYU Langone, and Penn Medicine anchor this market. These institutions serve as early adopter and reference customer sites. Research-oriented health systems generate peer-reviewed outcomes data from ambient AI deployments. That data accelerates purchasing at peer institutions nationally. Vendors with strong Northeast relationships benefit disproportionately from this network effect.

The West Coast benefits from health technology startup proximity. San Francisco, Seattle, and Portland host major health-tech ecosystems. UCSF Health, Stanford Health Care, and UW Medicine are leading early adopters. California’s CMIA and CCPA regulations add compliance complexity. Vendors with robust California-specific data governance frameworks gain a procurement advantage that filters less sophisticated competitors.

The Sun Belt is the fastest-growing ambient AI adoption geography through 2035. Dallas, Houston, Miami, and Phoenix are expanding rapidly. New ambulatory care facilities represent greenfield deployment opportunities. Legacy workflow disruption is minimal in new facilities. Texas and Florida health systems position ambient AI as a physician recruitment differentiator. Candidates now evaluate it alongside compensation and scheduling quality.

The Midwest is characterized by large enterprise deployments. Cleveland Clinic, Mayo Clinic, and Advocate Health are key adopters. Rollouts span multiple years and hundreds of physician users. Revenue per contract is high. Sales cycles are long and integration requirements are complex. Multi-specialty service lines must be equipped simultaneously during these deployments.

Key Regions and States

Northeast

- New York

- Massachusetts

- Pennsylvania

- Connecticut

West Coast

- California

- Washington

- Oregon

Sun Belt

- Texas

- Florida

- Arizona

- Georgia

Midwest

- Illinois

- Ohio

- Michigan

- Minnesota

Key Companies: Four Platforms Define the Competitive Landscape

Four platforms dominate US enterprise ambient clinical intelligence revenue. They are Microsoft DAX Copilot, Ambience Healthcare, Abridge, and Suki AI. Each holds a differentiated position based on EHR integration depth or specialty AI model breadth. EHR vendor partnerships are intensifying competitive concentration. Platforms without certified Epic, Oracle Cerner, or athenahealth integration credentials face growing procurement barriers.

| Company | Platform / Signal | Key Differentiator | Year / Status |

|---|---|---|---|

| Microsoft Nuance | DAX Copilot; Azure AI Health | Epic-certified; GPT-4 powered notes | FY2024 |

| Ambience Healthcare | Full-stack ambient AI; 85+ specialties | Specialty models and coding automation | Series B 2024 |

| Abridge | Clinical conversation AI; UPMC partnership | LLM on 3M+ real clinical conversations | Series C 2024 |

| Suki AI | Voice assistant + ambient documentation | EHR-agnostic, lightweight deployment | FY2024 |

| Oracle Health | Clinical AI in Cerner workflow | Cerner-native for 1,000+ hospitals | FY2024 |

| Nabla | Copilot for clinicians | Multimodal patient-context AI | US expansion 2024 |

Microsoft Nuance’s DAX Copilot leads by installed base. Its January 2025 Epic workflow API integration was a pivotal milestone. Azure is deployed in over 90% of US health systems. This creates a procurement bundling effect that is difficult for competitors to overcome. Rivals must prove specialty model advantages or EHR-agnostic flexibility to displace DAX Copilot within Microsoft enterprise accounts.

Ambience Healthcare covers more than 85 medical specialties. Models are trained on specialty-specific clinical language and ICD-10 requirements. This depth is a critical differentiator for multi-specialty health system buyers. Abridge trained its AI on over 3 million real patient-physician conversations with UPMC. Note accuracy exceeds physician-rated quality thresholds in peer-reviewed validation. Oracle Health embeds ambient AI natively within Cerner Millennium. Over 1,000 US hospitals benefit with no additional API integration work required.

Competitive moats in this market are deepening on three dimensions. First, specialty model depth creates switching costs once models are calibrated to a health system’s patient population and documentation standards. Second, EHR certification credentials create procurement access advantages that take 12 to 24 months for new entrants to replicate. Third, health system reference customer relationships create social proof that accelerates purchasing at peer institutions. Vendors who lead on all three dimensions will command durable pricing power through 2030.

Hyperscaler entry is the most structurally significant competitive development of the past 24 months. AWS HealthScribe, Google Med-Gemini, and Microsoft Azure Health AI all represent ambient clinical intelligence capabilities embedded within platforms already deeply integrated into health system IT infrastructure. These hyperscaler offerings reduce the procurement decision to a line-item on an existing enterprise cloud contract. Pure-play ambient AI vendors must articulate a compelling clinical accuracy and specialty coverage advantage to remain competitive against this embedded distribution leverage.

Top Key Players

- Microsoft Nuance (DAX Copilot)

- Ambience Healthcare

- Abridge

- Suki AI

- Oracle Health (Cerner AI)

- Nabla

- Augmedix

- DeepScribe

- Commure (Athelas)

- 3M Health Information Systems

- Amazon Web Services (HealthScribe)

- Google Cloud (Med-Gemini / Healthcare AI)

- Others

Related Markets: 5 Segments Shaping Ambient Clinical Intelligence Adoption

Five adjacent markets intersect directly with the US ambient clinical intelligence space. Each has distinct growth dynamics and regulatory exposure. All share the same upstream technology stack: cloud AI infrastructure, LLM platforms, and FHIR-based data exchange. Health system CIOs building multi-platform digital health portfolios need visibility into each one.

- Clinical Documentation Improvement (CDI) Market: Valued at USD 3.18 billion in 2025. Forecast to reach USD 7.94 billion by 2035 at 9.6% CAGR. Ambient AI eliminates manual CDI query processes through real-time documentation accuracy. This creates both displacement risk for legacy CDI vendors and integration opportunities for ambient platforms.

- Healthcare NLP Market: Valued at USD 2.67 billion in 2025. Forecast to reach USD 14.32 billion by 2035 at 18.4% CAGR. NLP infrastructure underpins all ambient clinical intelligence platforms. Advances in clinical NLP accuracy directly improve ambient AI output quality and physician acceptance rates.

- Telehealth Platform Market: Valued at USD 22.4 billion in 2025. Expected to grow at 16.8% CAGR through 2035. Virtual care providers are integrating ambient AI as a standard service layer. This creates a distribution channel for ambient AI vendors and a quality differentiator for telehealth platforms.

- Healthcare AI Platform Market: Valued at USD 8.94 billion in 2025. Projected to grow at 24.1% CAGR through 2035. Ambient clinical intelligence is the most physician-proximate use case in healthcare AI. It creates cross-sell pathways into radiology AI, pathology AI, and genomics interpretation within the same health system account.

- EHR Systems Market: Valued at USD 14.1 billion in 2025. Forecast to grow at 6.2% CAGR through 2035. Epic’s App Orchard certification and Oracle Health’s embedded AI roadmap are the most important channel dynamics for ambient vendors. EHR-bundled procurement is replacing standalone ambient AI evaluation cycles.

Key Growth Drivers of the US Ambient Clinical Intelligence Market

Physician Burnout and EHR Documentation Burden Drive Structural Platform Demand

Physician burnout is the most powerful demand driver in this market. The AMA’s 2024 National Burnout Survey found 48.2% of US physicians show at least one burnout symptom. EHR documentation burden was the top contributing factor for 62% of those respondents. Health systems now treat ambient AI as a retention infrastructure expense. Physician replacement costs average USD 500,000 to USD 1 million each. The ROI case is direct and independently verifiable.

The evidence base for documentation time savings is expanding rapidly. Stanford Medicine’s DAX Copilot study documented a 72-second reduction per note. Across a full clinical day, this returns over 45 minutes to each physician. UCHealth data showed a 33% reduction in after-hours EHR time. Physicians consistently rate after-hours charting as the leading cause of wellbeing damage. Peer-reviewed outcomes data like this accelerates enterprise purchasing at institutions that benchmark against academic medical center performance.

Value-based care program expansion also amplifies ambient AI ROI. MIPS quality measure performance depends on documentation completeness. HCC risk adjustment accuracy depends on coding specificity. Ambient AI improves both systematically. Health systems in Medicare Shared Savings Program ACOs report that ambient AI captures diagnoses previously omitted due to documentation fatigue. Improved HCC capture rates translate directly into higher risk adjustment revenue. For large ACO participants, this revenue impact can exceed USD 30 million annually.

The 5G and broadband expansion programs funded by NTIA are also accelerating ambient AI deployment in rural and underserved markets. Faster and more reliable connectivity enables cloud-based ambient AI to function reliably in settings where latency previously caused performance problems. Rural health systems that previously could not support cloud-native ambient AI are now entering procurement. This geographic expansion represents a structural demand floor that was not present before 2023.

Market Restraints

Physician Trust Gaps and EHR Integration Complexity Compress Deployment Velocity

Physician acceptance is the primary deployment constraint. Physicians trained in documentation-intensive EHR environments have deep habits of personal note ownership. Ambient AI requires them to trust AI-generated content. Change management programs consistently underestimate this behavioral challenge. Health systems that scale successfully invest 2 to 3 times more in onboarding and peer champion programs than vendors typically scope in contracts. Budget surprises slow expansion beyond initial pilot populations.

EHR integration complexity creates a second-layer deployment barrier. Ambient AI must integrate bidirectionally with EHR note composition, problem lists, medications, and order entry. This requires certified API partnerships with Epic, Oracle Cerner, and athenahealth. Certification can take 12 to 24 months for new market entrants. Platforms without certified integrations face procurement exclusion at health systems with strict IT governance requirements.

Privacy and consent complexity creates a third restraint layer for conservative health system legal departments. Ambient recording of physician-patient conversations requires explicit patient consent protocols. These protocols vary by state law. HIPAA Business Associate Agreement terms must be negotiated carefully. Patient opt-out workflows must function reliably across diverse care settings and patient populations. Health system legal teams identifying PHI handling ambiguities in vendor Data Processing Agreements extend contract review timelines by 3 to 6 months in some institutions. This directly delays deployment starts and compresses the ROI timeline that procurement approvers originally modeled.

Market Opportunities

Specialty AI Models and Value-Based Care Alignment Unlock Premium Revenue Segments

Specialty-trained ambient AI models represent the highest near-term contract value expansion opportunity. Oncology, orthopedics, cardiology, and behavioral health practices need specialty-specific documentation. General clinical models cannot match their accuracy requirements. Vendors investing in specialty models report 40 to 60% higher average revenue per user than primary care deployments. This improves blended revenue per user across multi-specialty health system contracts significantly.

Federal rural health investment is opening a structurally underserved ambient AI segment. The FCC Connected Care Pilot Program and USDA Telemedicine grants fund telehealth infrastructure in rural markets. Physician shortages in rural areas make documentation efficiency gains more impactful. Rural critical access hospitals with 1 to 3 physicians report that ambient AI is operationally transformative. Higher patient volumes can be managed without increasing after-hours charting time.

International expansion represents a longer-term opportunity for leading US ambient clinical intelligence vendors. Canada, the United Kingdom, and Australia share EHR environments similar to the US Epic and Cerner ecosystems. Physician documentation burden in these markets matches US severity levels. However, national health data residency requirements and public procurement structures create distinct market entry requirements. Vendors building international-ready compliance frameworks in 2025 and 2026 are positioning for expansion that could add 15 to 25% to total addressable market by 2030.

Regulatory and Compliance Landscape for Ambient Clinical Intelligence

ONC, CMS, and State Privacy Laws Shape Vendor Certification Requirements Through 2035

The regulatory environment for ambient clinical intelligence is uniquely complex. It sits at the intersection of HIPAA PHI requirements, state recording consent laws, FDA’s Software as a Medical Device framework, and ONC interoperability mandates. Vendors must navigate all four dimensions simultaneously. Compliance infrastructure quality has become a material procurement differentiator. Health system legal teams now scrutinize vendor Data Processing Agreements more carefully than ever before.

HIPAA Business Associate Agreements apply to all ambient AI vendors processing PHI. Vendors must demonstrate end-to-end encryption of audio capture and transmission. Minimum necessary data retention policies are required. Breach notification must meet HIPAA’s 60-day disclosure requirement. Annual HIPAA risk assessment documentation is mandatory. The OCR’s increased enforcement since 2023 has elevated BAA review scrutiny at the health system procurement level.

ONC’s HTI-1 rule, finalized in January 2024, mandates algorithmic transparency for clinical AI. Ambient platforms that influence documentation and billing code selection are subject to HTI-1 requirements. Health system AI governance committees now evaluate vendors against these standards. Vendors who publish model performance metrics by patient demographic gain a procurement advantage. State recording consent laws add further complexity. Eleven states require all-party consent. This creates distinct deployment protocols from single-party consent jurisdictions.

ROI and Cost-Benefit Analysis for Healthcare Providers

Documented Productivity Benefits Establish Quantifiable Investment Returns

Ambient clinical intelligence delivers the clearest ROI of any clinical AI investment category. The productivity impact of documentation time reduction is directly measurable. It is also rapidly observable and monetizable. Health system CFOs in 2025 have access to published financial outcome data. Business cases can be built on verifiable benchmarks rather than vendor projections alone.

The time savings ROI calculation is consistent across published health system reports. A physician seeing 20 patients daily who saves 2 minutes per note generates 40 minutes of recaptured time daily. Redirected toward additional visits at USD 85 net revenue each, the annual upside exceeds USD 100,000 per physician. Platform costs range from USD 4,000 to USD 7,200 per physician annually. The return is 14 to 25 times the platform cost in the first full deployment year. No comparable clinical technology investment produces this ROI multiple in the current capital allocation environment.

Revenue cycle improvement represents an additional ROI layer beyond time savings. Ambient AI-generated notes capture diagnoses with greater specificity than physician-typed notes. HCC risk adjustment scores improve as a result. UCHealth’s published ambient AI data documented a 12% improvement in average RAF score per patient for the ambient AI physician cohort. For a mid-size health system with significant Medicare Advantage enrollment, this improvement translates to millions in additional annual risk adjustment revenue. ICD-10 coding automation features further reduce clean claim delays and post-submission coding query volumes.

Recruiting and retention ROI is the third financial dimension that health system CFOs are now quantifying. Hospitals that deploy ambient AI as part of a physician wellbeing initiative report measurable improvements in voluntary attrition rates. A 1 percentage point reduction in physician voluntary attrition at a 500-physician health system saves USD 2.5 to USD 5 million annually in replacement costs. This retention ROI alone justifies ambient AI investment for many health systems even before productivity and revenue cycle benefits are included in the business case calculation.

Patient Privacy and Trust Framework for Ambient Clinical Intelligence

Consent Architecture and Transparency Standards Define Long-Term Adoption Sustainability

Patient acceptance is a prerequisite for sustainable ambient AI deployment at scale. Health systems that invest in consent experience design report materially higher patient comfort rates. Institutions that treat consent as a compliance checkbox see lower acceptance and more friction. The long-term market growth trajectory depends on maintaining patient trust at every encounter. A single high-profile data breach could generate regulatory responses that constrain adoption across the entire industry.

Consent architecture design directly affects acceptance rates and workflow efficiency. Verbal consent administered by front-desk staff before patient room entry achieves 87 to 93% acceptance rates. Tablet-based written consent processes achieve 78 to 85% acceptance rates. Opt-out frameworks generate the highest participation. However, they carry legal risk in all-party consent states. They also create ethical discomfort among patient advocacy groups. Health systems must weigh deployment efficiency against these risks carefully before selecting a consent model.

Transparency in how ambient AI platforms handle patient conversation data is becoming a procurement differentiator. Patient health data literacy is increasing. Healthcare data breach coverage in mainstream media is intensifying patient awareness of PHI handling risks. Vendors that provide patient-facing data retention summaries and plain-language privacy policies are gaining trust. These materials are accessible within patient portal environments at leading health systems. Vendors who invest in patient-centric data governance communicate a quality signal that health system marketing departments actively use as a competitive advantage in markets where patient choice behavior is strong.

The integration of ambient AI consent workflows within existing patient portal infrastructure is emerging as the design standard. Standalone paper consent forms are being replaced by digital consent flows embedded in patient check-in apps. These digital flows support audit logging, patient opt-out management, and consent version tracking. Health systems with digital patient engagement rates above 65% are prioritizing digital consent as part of their ambient AI deployment planning. Vendors who provide pre-built patient portal consent integrations reduce deployment timelines and legal review burden for health system partners.

Latest Trends in the US Ambient Clinical Intelligence Market

Multimodal AI, EHR-Native Integration, and Performance Contracting Reshape Platform Economics

Multimodal ambient AI platforms are defining the next competitive frontier. These platforms integrate audio capture with computer vision analysis of patient presentation. They retrieve real-time EHR data and apply contextual diagnostic knowledge graphs. Microsoft Research and Google DeepMind are both advancing multimodal clinical AI programs. Early clinical validation shows multimodal context improves diagnostic suggestion accuracy by 18 to 31% versus audio-only platforms. High-acuity specialty encounters benefit most.

EHR-native ambient AI integration is reshaping how health systems evaluate platforms. Epic’s ambient AI certification program validates third-party platforms against Epic workflow APIs. Certification compresses evaluation from 18 months to 6 to 9 months for certified partners. Certified vendors gain immediate access to Epic’s 250-plus major health system client base via App Orchard. This fundamentally alters competitive dynamics between certified and uncertified ambient platforms.

Performance-based contract structures are emerging across the market. Intermountain Health and Providence Health are pioneering outcome-linked ambient AI contracts. These contracts include physician satisfaction improvement targets and documentation time reduction commitments. HCC capture rate improvement milestones are also included. Vendor accountability increases significantly under these structures. Most pure-play vendors are still building the outcome measurement infrastructure required to support performance contracts at scale.

AI-native ambient platforms are also beginning to generate synthetic clinical data for downstream model training. Generative AI tools within ambient documentation systems can create realistic encounter transcripts for specific clinical scenarios. These synthetic datasets are used to train specialty AI models without exposing real PHI. This creates a closed-loop AI development cycle where ambient platforms improve their own accuracy over time. Vendors who build this synthetic data generation capability establish a self-reinforcing competitive advantage that grows stronger with each additional health system deployment.

Integration with remote patient monitoring is the emerging ambient AI use case with the highest value-based care relevance. Platforms that combine real-time visit documentation with longitudinal RPM data streams enable continuous risk stratification. Proactive care gap identification becomes automated. Care coordination workflows can be triggered algorithmically. Health systems operating at-risk contracts evaluate this use case convergence as strategic infrastructure investment. It positions advanced ambient AI platforms for value-based outcome performance contract structures rather than pure per-physician subscription pricing.

Recent Developments: Microsoft, Ambience Healthcare, and Amazon Lead 2024–2025

- March 2025 — Ambience Healthcare raised USD 70 million in Series B funding. Kleiner Perkins led the round. a16z and major health system investors participated. Capital will expand its 85-specialty platform and accelerate enterprise US deployments.

- February 2025 — Amazon Web Services launched HealthScribe Ambient in general availability. It offers a HIPAA-eligible ambient documentation API. Telehealth platforms and EHR developers can now embed it into diverse clinical applications.

- January 2025 — Microsoft expanded DAX Copilot integration with Epic’s ambient API. Over 250 US health system Epic clients can generate ambient notes natively. No standalone DAX installation or separate physician onboarding is required.

- November 2024 — Abridge closed a USD 150 million Series C led by Spark Capital. UPMC Enterprises, Mayo Clinic Platform, and Emory Healthcare also participated. Abridge is now the leading independent challenger to Microsoft Nuance in academic medical center accounts.

- October 2024 — Google Cloud announced Med-Gemini integration with ambient clinical documentation. It combines multimodal clinical reasoning with real-time EHR context retrieval. The platform is built on Google Cloud Healthcare API infrastructure.

- August 2024 — Commure completed its merger with Athelas. The platform integrates clinical workflow automation with remote patient monitoring analytics. It targets health systems operating value-based care contracts.

Competitive Landscape and SWOT Analysis

Market Concentration, Strategic Positioning, and Competitive Forces in 2025

The US ambient clinical intelligence market is moderately concentrated at the top. Three platforms — Microsoft DAX Copilot, Ambience Healthcare, and Abridge — command the majority of enterprise health system revenue. The remainder is distributed across Suki AI, Oracle Health, Nabla, Augmedix, DeepScribe, and a long tail of regional and specialty-focused vendors. Competitive intensity is rising. EHR vendor certification programs are accelerating consolidation around a small number of certified platforms. Vendors without EHR credentials face structural procurement disadvantage that compounds with each passing quarter.

Five competitive forces shape the market structure. Buyer power is moderate. Large health systems negotiate favorable pricing through enterprise contracts. However, switching costs rise sharply once ambient AI models are calibrated to a health system’s patient population and documentation standards. Supplier power is low. Underlying LLM infrastructure is commoditizing rapidly across OpenAI, Anthropic, Google, and open-source alternatives. New entrant threat is declining. EHR certification barriers and specialty model development costs filter out undercapitalized competitors. Substitute threat is low. Manual transcription and traditional EHR documentation are structurally inferior on cost, quality, and physician satisfaction dimensions. Competitive rivalry is high and intensifying as hyperscalers enter with embedded distribution advantages.

Strengths

- Proven and measurable ROI: Time savings of 2-plus hours per physician per day are independently verified across multiple peer-reviewed health system studies. This is the strongest adoption accelerant available to any clinical AI category.

- EHR ecosystem integration: Epic, Oracle Cerner, and athenahealth certification programs create structured distribution at scale. Certified platforms gain access to hundreds of health system clients through established marketplace channels.

- Recurring subscription revenue model: Per-physician SaaS pricing generates predictable annual recurring revenue. Usage-based expansion occurs naturally as physicians document more encounter types and adopt decision support modules.

- Regulatory alignment: ONC HTI-1, CMS MIPS, and FHIR interoperability mandates create structural demand that is policy-driven rather than purely discretionary. This provides a demand floor that is independent of health system budget cycles.

- Strong physician demand pull: Physician-initiated adoption is increasingly common. Physicians who experience ambient AI in one setting request it at their next employer. This bottom-up demand dynamic reduces enterprise sales cycle dependence.

Weaknesses

- EHR integration complexity: Bidirectional integration with Epic, Cerner, and athenahealth requires certified API partnerships that take 12 to 24 months to complete. New entrants face a structural time disadvantage that is difficult to compress.

- Specialty model coverage gaps: General clinical models underperform in high-complexity specialties. Building and maintaining 85-plus specialty-trained models requires significant ongoing investment in annotated training data and clinical validation.

- Physician change management burden: Onboarding physicians onto ambient AI requires dedicated peer champion programs and extended support timelines. Health systems consistently underestimate this investment. Vendor implementation scopes often fail to include sufficient change management resourcing.

- Patient consent workflow complexity: State-by-state variation in recording consent laws creates operational friction. Eleven states require all-party consent. Managing consent protocol variation across multi-state health system deployments adds implementation cost and legal review burden.

- Dependence on LLM infrastructure: Platform performance is partially dependent on underlying LLM provider reliability, pricing, and policy changes. OpenAI, Anthropic, and Google model policy updates can affect ambient AI output characteristics in ways that require prompt engineering and revalidation work.

Opportunities

- Specialty AI model expansion: Oncology, behavioral health, cardiology, and rare disease specialties remain underserved by current ambient AI offerings. Purpose-trained specialty models command 40 to 60% higher average revenue per user than general clinical deployments.

- Value-based care performance contracting: Health systems in Medicare Shared Savings Program ACOs and Medicare Advantage risk contracts have strong financial incentives to improve HCC capture rates and documentation specificity. Ambient AI platforms that quantify this revenue impact will unlock outcome-based contract structures with higher total contract value.

- Rural and federally qualified health center expansion: FCC and USDA broadband grants are bringing reliable connectivity to markets where ambient AI was previously impractical. These markets represent greenfield deployment opportunities with minimal competitive saturation.

- Multimodal AI development: Integration of audio, video, and EHR context into unified clinical intelligence platforms will create a generation-defining product differentiation. Early movers in multimodal ambient AI are building capabilities that will take competitors 3 to 5 years to replicate at commercial quality.

- International market entry: Canada, the UK, and Australia share EHR ecosystems and physician documentation burden levels similar to the US. Vendors building international compliance frameworks in 2025 and 2026 position for 15 to 25% total addressable market expansion by 2030.

Threats

- Hyperscaler embedded competition: AWS HealthScribe, Google Med-Gemini, and Microsoft Azure Health AI embed ambient clinical intelligence within enterprise cloud contracts already in place at most US health systems. Pure-play vendors must demonstrate clinical accuracy advantages to justify standalone procurement decisions against this embedded distribution leverage.

- EHR vendor native AI expansion: Epic and Oracle Health are both developing native ambient AI capabilities within their core EHR platforms. If EHR-native ambient AI achieves acceptable clinical accuracy, it will reduce the addressable market for standalone ambient AI vendors significantly within the Epic and Cerner installed bases.

- Regulatory tightening: FDA Software as a Medical Device classification for ambient AI features that provide diagnostic recommendations could impose pre-market review requirements that significantly increase compliance costs and slow product release cycles for affected vendors.

- Data breach and privacy incident risk: A single high-profile PHI breach involving ambient AI conversation recordings could generate congressional scrutiny, regulatory action, and patient consent refusal rates that constrain adoption industry-wide for 12 to 24 months.

- LLM commoditization compressing margins: Rapid improvement in open-source LLM quality is reducing the cost advantage that proprietary LLM-based ambient AI platforms held over competitors. As LLM performance commoditizes, ambient AI vendors must differentiate increasingly on specialty model depth, EHR integration quality, and health system workflow expertise rather than underlying model performance alone.

Competitive Positioning Matrix: Leading Platforms by Key Dimensions

| Platform | EHR Integration | Specialty Depth | LLM Generation | Pricing Model |

|---|---|---|---|---|

| Microsoft DAX Copilot | Epic-certified (top tier) | General + growing | GPT-4 / Azure AI | Enterprise license |

| Ambience Healthcare | Multi-EHR API | 85+ specialties (best) | Proprietary clinical LLM | Per-physician SaaS |

| Abridge | Epic + UPMC native | Primary care + growing | Proprietary clinical LLM | Enterprise + per-user |

| Suki AI | EHR-agnostic | General clinical | Hybrid NLP + LLM | Per-physician SaaS |

| Oracle Health (Cerner AI) | Cerner-native (top tier) | General clinical | Oracle AI + LLM | Cerner bundle |

| AWS HealthScribe | API-based (developer) | General clinical | AWS Bedrock / LLM | Consumption-based |

Microsoft DAX Copilot leads on EHR integration and distribution scale. Its Epic certification and Azure enterprise presence create a procurement default position that rivals must actively displace. Ambience Healthcare leads on specialty model depth and is the best-positioned pure-play vendor for multi-specialty health system enterprise contracts. Abridge leads on clinical AI accuracy validation and academic medical center reference customer quality. Oracle Health leads on frictionless deployment within the Cerner installed base. AWS HealthScribe leads on developer accessibility and consumption-based pricing flexibility for telehealth platform builders.

The competitive landscape will consolidate further through 2030. EHR certification costs, specialty model investment requirements, and health system reference customer development timelines will eliminate most undifferentiated ambient AI vendors from enterprise procurement consideration. The market is likely to stabilize around 4 to 6 dominant platforms within specific EHR ecosystem lanes, with a smaller number of specialty-focused vendors serving high-complexity clinical niches at premium price points.

Report Features

| Feature | Description |

|---|---|

| Market Value (2025) | USD 1.82 billion |

| Forecast Revenue (2035) | USD 18.08 billion |

| CAGR (2025–2035) | 25.81% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2025–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Regulatory Framework, ROI Analysis, Patient Privacy Framework, Recent Developments |

| Segments Covered | By Solution Type, By Deployment Mode, By End-User, By AI Integration Level, By Care Setting |

| Regional Analysis | Northeast, West Coast, Sun Belt, Midwest with state-level breakdowns |

| Dominant Segment | AI-Powered Voice Documentation 52.4%; Hospitals & Health Systems 58.7% |

| Dominant Technology | LLM-Powered platforms with 44.1% AI integration share |

| Regulatory Framework | HIPAA BAA, ONC HTI-1, CMS MIPS/HCC, FDA SaMD, State Recording Consent Laws |

| Competitive Landscape | Microsoft Nuance, Ambience Healthcare, Abridge, Suki AI, Oracle Health, Nabla, Augmedix, DeepScribe, Commure/Athelas, 3M, AWS HealthScribe, Google Cloud |