What is the Advanced Electrode Binder Chemicals Market Size?

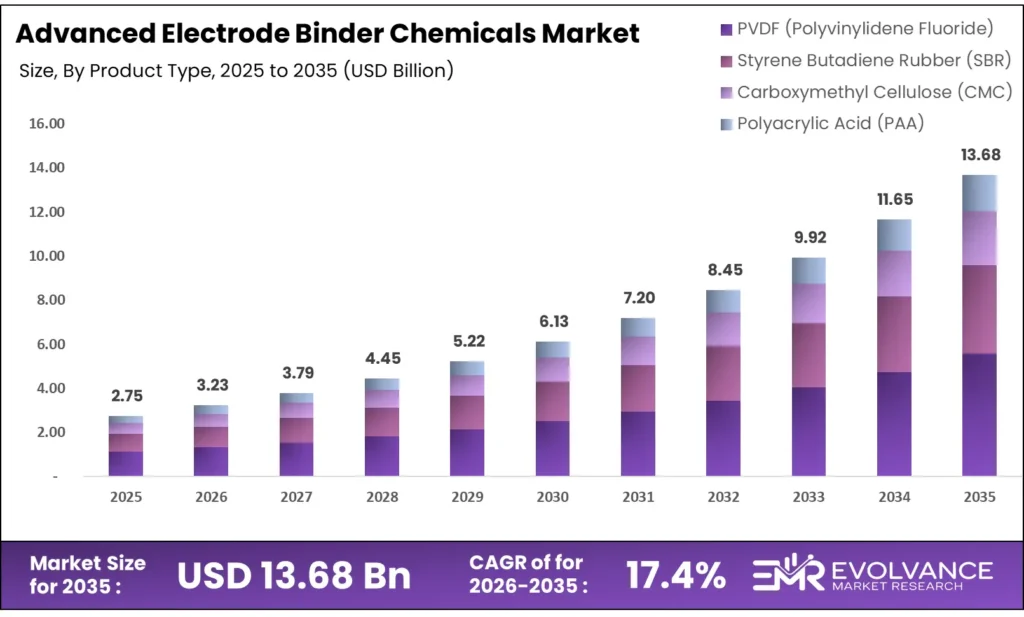

The Global Advanced Electrode Binder Chemicals Market size will be worth around USD 13.68 Billion by 2035 from USD 2.75 Billion in 2025, growing at a CAGR of 17.4% during the forecast period 2026 to 2035. Battery makers scaling lithium-ion production lines are pulling demand for high-performance binder chemistries faster than supply chains anticipated. EV manufacturers are prioritizing binders that extend cycle life and raise energy density, shifting procurement away from standard PVDF toward advanced polymer systems. On the supply side, regulatory pressure on fluorinated materials in Europe is forcing chemistry reformulation, adding cost and timeline risk for established binder producers.

Market Highlights

- The Global Advanced Electrode Binder Chemicals Market valued at USD 2.75 Billion in 2025, reaching USD 13.68 Billion by 2035 at a CAGR of 17.4%.

- Asia Pacific leads with a 46.2% market share, valued at USD 1.3 Billion.

- PVDF dominates the product type segment with a 43.6% share.

- Lithium-ion batteries represent the top battery type segment at 53.2%.

- Powder form commands 67.3% of the form segment.

- Water-based binders lead binder type with 63.2% share.

- Anode binders dominate electrode type with 72.1% share.

- Wet coating process holds 59.6% of the technology segment.

- Graphite-based anodes top the application segment at 61.7%.

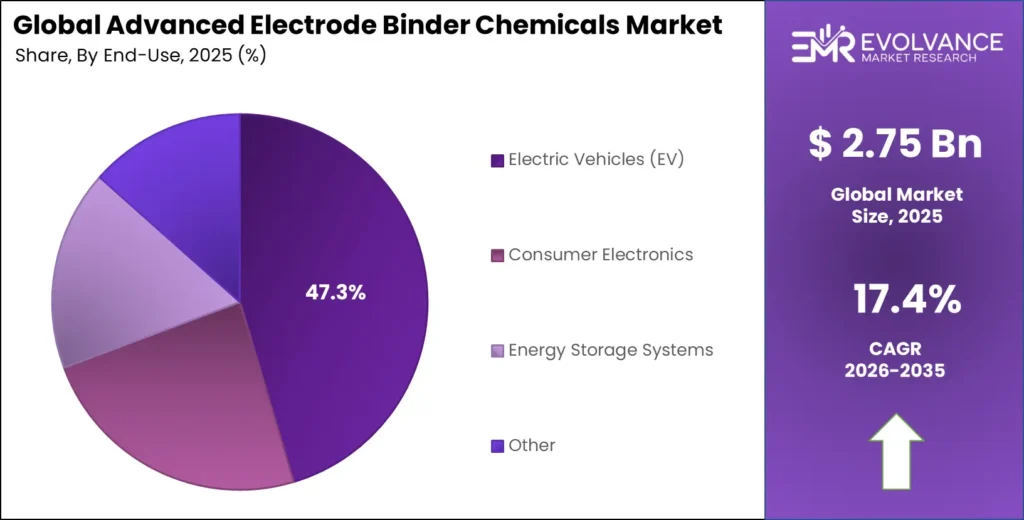

- Electric Vehicles drive the end-use segment with 47.3% share.

Market Overview

Advanced electrode binder chemicals are specialty polymers that hold active electrode particles together in lithium-ion and next-generation battery cells. They bind electrode materials to current collectors while allowing ion movement and maintaining structural integrity through charge-discharge cycles. Without effective binders, electrodes degrade rapidly, shortening battery life and reducing energy output.

The market spans several chemistry classes — PVDF, SBR, CMC, and PAA — each serving specific electrode types, battery chemistries, and performance targets. Cathode-side applications rely heavily on PVDF dissolved in NMP solvent, while anode formulations increasingly use water-based SBR-CMC systems. This split creates two distinct supply and cost structures within the same market.

Manufacturers face a structural shift as Europe moves to restrict fluorinated compounds, including PVDF, under emerging chemical regulations. This pressure is accelerating R&D into fluorine-free alternatives, opening a new competitive front where specialty chemical firms can gain share by commercializing next-generation chemistries ahead of larger incumbents.

According to the International Energy Agency, global battery production capacity reached 2.6 TWh in 2024, with Asia accounting for over 80% of output. This concentration signals that binder chemical demand is structurally tied to Asian manufacturing expansion — and any capacity shift to Europe or North America will directly create new regional binder procurement channels.

Global trade in rechargeable batteries exceeded USD 120 Billion in 2024. Trade at this scale requires upstream chemical supply chains, including binders, to operate at volumes and quality levels that most emerging suppliers cannot yet match — sustaining pricing power for established producers while creating a performance barrier new entrants must clear to compete.

Product Type Insights

PVDF (Polyvinylidene Fluoride) dominates with 43.6% due to electrochemical stability and cathode compatibility.

In 2025, PVDF (Polyvinylidene Fluoride) held a dominant market position in the By Product Type segment of the Advanced Electrode Binder Chemicals Market, with a 43.6% share. Its dominance reflects decades of adoption in NMC and NCA cathode formulations where chemical resistance and high voltage stability are non-negotiable. However, Kureha Corporation’s Advanced Materials segment recorded a revenue decline of 22.0% year-on-year in 2024 due to softer PVDF binder demand in EV markets — a signal that buyers are beginning to test alternatives even as PVDF retains overall share leadership.

Styrene Butadiene Rubber (SBR) is the primary binder for graphite anodes in water-based electrode slurries. Its cost advantage over PVDF and compatibility with CMC as a co-binder makes it the default choice for high-volume anode manufacturing. SBR’s water-based processing eliminates NMP solvent costs and associated recovery systems, giving battery makers a direct manufacturing cost benefit.

Carboxymethyl Cellulose (CMC) functions as a thickener and co-binder paired with SBR in anode electrode formulations. CMC improves slurry viscosity control and enhances adhesion to copper current collectors. Its bio-derived origin positions it well as battery producers respond to sustainability mandates and seek to reduce synthetic polymer content in electrode coatings.

Polyacrylic Acid (PAA) is gaining traction in silicon-anode applications where conventional binders fail under the high volumetric expansion of silicon particles during cycling. PAA’s carboxyl groups form chemical bonds with silicon oxide surfaces, preventing electrode delamination at high charge rates — a critical advantage as battery designers push toward silicon-blended anodes for higher energy density.

Battery Type Insights

Lithium-ion Batteries dominate with 53.2% due to global manufacturing scale and established supply chains.

In 2025, Lithium-ion Batteries held a dominant market position in the By Battery Type segment of the Advanced Electrode Binder Chemicals Market, with a 53.2% share. China’s battery output exceeded 940 GWh in 2024, according to the China National Bureau of Statistics, driving massive domestic demand for PVDF and CMC/SBR binder chemicals. This production scale creates a self-reinforcing dynamic — high volumes lower binder unit costs, making lithium-ion cells even more competitive against emerging chemistries.

Lithium Iron Phosphate (LFP) batteries are reshaping binder demand patterns as EV makers in China and increasingly in Europe shift toward the chemistry for its safety and cost profile. LFP cathodes operate at lower voltages and tolerate water-based binder processing better than high-nickel alternatives, pulling demand toward aqueous binder systems and reducing PVDF’s cathode-side dominance within this sub-segment.

Nickel Manganese Cobalt (NMC) batteries demand high-performance PVDF binders that can withstand elevated operating voltages without oxidation or adhesion loss. As battery makers pursue higher nickel content to improve energy density, binder chemistry must evolve in parallel — high-nickel NMC cathodes impose stricter requirements on binder chemical resistance and electrode structural integrity.

Form Insights

Powder Form dominates with 67.3% due to storage stability and formulation flexibility.

In 2025, Powder Form held a dominant market position in the By Form segment of the Advanced Electrode Binder Chemicals Market, with a 67.3% share. Powder binders offer longer shelf life, easier transport, and broader compatibility with both solvent-based and aqueous slurry systems. Battery manufacturers with global supply chains prefer powder formats because they can dissolve or disperse them on-site at the point of electrode manufacturing, reducing logistics complexity.

Slurry Form binders reduce on-site preparation steps for large battery factories that operate continuous coating lines. Pre-dispersed slurries eliminate binder dissolution time and reduce batch-to-batch variability in electrode slurry rheology. However, shorter shelf life and higher transport costs limit slurry adoption to manufacturers with stable, high-volume production schedules and reliable local supply arrangements.

Type Insights

Water-based Binders dominate with 63.2% due to environmental compliance and cost advantages over NMP solvent systems.

In 2025, Water-based Binders held a dominant market position in the By Type segment of the Advanced Electrode Binder Chemicals Market, with a 63.2% share. The shift away from NMP solvents is being driven by the rising costs of NMP recovery systems, stricter worker exposure limits, and sustainability mandates from automotive OEM customers. Fluorine-free and siloxane-based binder systems are showing over 1.4× higher lifespan stability compared to PVDF systems, accelerating water-based adoption in both anode and increasingly cathode applications.

Solvent-based Binders remain essential for high-nickel NMC cathode electrodes where water sensitivity limits aqueous processing. PVDF dissolved in NMP solvent delivers superior adhesion and electrochemical stability at high voltages. However, NMP’s toxicity classification and recovery infrastructure requirements are adding cost pressure that is slowly pushing formulation teams toward aqueous alternatives wherever cathode chemistry allows.

Electrode Type Insights

Anode Binders dominate with 72.1% due to widespread water-based SBR-CMC adoption in graphite anodes.

In 2025, Anode Binders held a dominant market position in the By Electrode Type segment of the Advanced Electrode Binder Chemicals Market, with a 72.1% share. Graphite anode manufacturing at scale uses SBR-CMC water-based systems that are cost-effective and environmentally compatible. The high volume of lithium-ion cell production globally ensures strong, sustained demand for anode binder chemistries. South Korea’s lithium-ion battery exports reached USD 9.8 Billion in 2024, per KOSIS, reflecting the industrial scale of cathode and anode manufacturing that anchors binder demand.

Cathode Binders represent a smaller but higher-value segment where PVDF dominates and unit pricing reflects the technical performance requirements of high-voltage cathode electrodes. As NMC cathodes push toward higher nickel content, binder chemistry requirements become more demanding, creating pricing power for producers who can deliver proven, high-performance cathode binder formulations at manufacturing scale.

Technology Insights

Wet Coating Process dominates with 59.6% due to established manufacturing infrastructure and slurry compatibility.

In 2025, Wet Coating Process held a dominant market position in the By Technology segment of the Advanced Electrode Binder Chemicals Market, with a 59.6% share. The wet process is deeply embedded in existing gigafactory designs, with capital-intensive smart coating lines built around liquid slurry systems. Switching costs are high — not just in equipment but in process qualification time — which locks in wet process binder demand even as dry electrode alternatives gain attention.

Dry Electrode Coating is an emerging technology that eliminates solvents entirely by processing binder and electrode materials as dry powders that are calendered into free-standing films. This approach reduces manufacturing energy use and eliminates NMP recovery systems. Tesla’s early adoption of dry electrode technology in specific cell formats has validated the concept at industrial scale, raising industry interest and drawing R&D investment from both binder producers and cell manufacturers.

Application Insights

Graphite-based Anodes dominate with 61.7% due to established lithium-ion production volumes.

In 2025, Graphite-based Anodes held a dominant market position in the By Application segment of the Advanced Electrode Binder Chemicals Market, with a 61.7% share. Graphite remains the default active material in commercial lithium-ion cells, and SBR-CMC binder systems are purpose-optimized for graphite’s physical properties and expansion behavior during cycling. The massive installed base of graphite anode production lines globally ensures sustained binder demand well through the forecast period.

Silicon-based Anodes require fundamentally different binder chemistries because silicon expands up to 300% by volume during lithiation, causing conventional binders to delaminate and fail. PAA and other carboxyl-functionalized binders form covalent bonds with silicon oxide surfaces, maintaining electrode integrity across thousands of cycles. As cell makers blend silicon into graphite anodes to raise energy density, demand for specialized silicon-compatible binder chemistries will grow faster than the overall electrode binder market.

Solid-state Batteries represent an early-stage application where binder chemistry is undergoing fundamental rethinking. Solid electrolytes introduce new interface compatibility requirements, and the absence of liquid electrolyte changes the mechanical and chemical role of the binder entirely. Binder producers investing in solid-state R&D now are positioning to capture first-mover advantage in a segment expected to scale commercially in the second half of the forecast period.

End-Use Industry Insights

Electric Vehicles (EV) dominate with 47.3% due to scale of battery procurement and performance requirements.

In 2025, Electric Vehicles (EV) held a dominant market position in the By End-Use Industry segment of the Advanced Electrode Binder Chemicals Market, with a 47.3% share. The U.S. alone imported USD 13.1 Billion in lithium-ion batteries in 2024, according to the USITC, reflecting the scale of EV battery demand flowing through North American supply chains. EV buyers set the most demanding performance specifications — cycle life, energy density, and thermal stability which directly raises the technical bar for binder chemistries across the entire supply chain.

Consumer Electronics represents a mature but stable demand channel where compact, high-cycle-life cells require binders optimized for thin electrode coatings and consistent quality across billions of small cells. The consumer electronics segment provides binder producers with volume predictability and long-term customer relationships, even as EV contracts attract more R&D attention and higher unit margins.

Energy Storage Systems are an expanding end-use segment driven by grid-scale battery deployments linked to renewable power capacity additions. Grid energy storage cells prioritize cycle count and calendar life over energy density, which shifts binder selection criteria toward chemistries that minimize degradation over thousands of shallow discharge cycles. The European Battery Alliance’s €6.1 Billion in public funding for battery material supply chains supports this segment’s growth trajectory across European markets.

Market Segments Covered in the Report

By Product Type

- PVDF (Polyvinylidene Fluoride)

- Styrene Butadiene Rubber (SBR)

- Carboxymethyl Cellulose (CMC)

- Polyacrylic Acid (PAA)

By Battery Type

- Lithium-ion Batteries

- Lithium Iron Phosphate (LFP)

- Nickel Manganese Cobalt (NMC)

By Form

- Powder Form

- Slurry Form

By Type

- Water-based Binders

- Solvent-based Binders

By Electrode Type

- Anode Binders

- Cathode Binders

By Technology

- Wet Coating Process

- Dry Electrode Coating

By Application

- Graphite-based Anodes

- Silicon-based Anodes

- Solid-state Batteries

- Other

By End-Use Industry

- Electric Vehicles (EV)

- Consumer Electronics

- Energy Storage Systems

- Other

Regional Insights

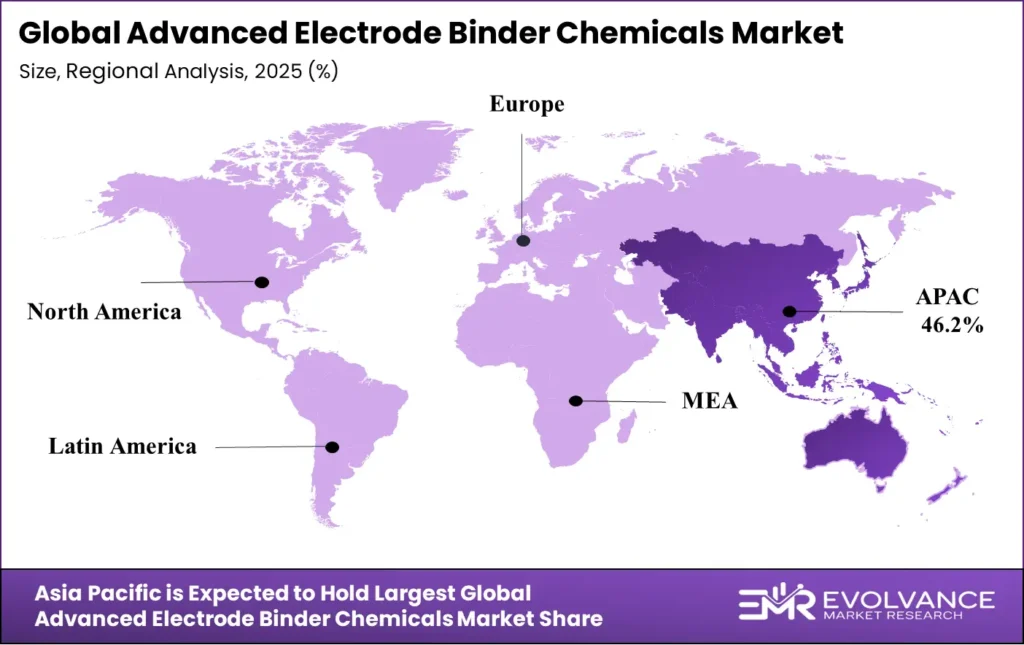

Asia Pacific Dominates the Advanced Electrode Binder Chemicals Market with a Market Share of 46.2%, Valued at USD 1.3 Billion

Asia Pacific commands 46.2% of the global market, valued at USD 1.3 Billion in 2025. China’s battery production exceeding 940 GWh and Japan’s battery industry output of ¥2.4 trillion in 2024 explain this dominance structurally — binder chemical producers co-locate with cell manufacturers to reduce lead times and logistics costs. This geographic concentration means any disruption in Asian production directly impacts global binder supply.

North America Market Trends

North America is transitioning from a binder import market to a domestic production hub. The U.S. Department of Energy’s USD 7 Billion in Battery Materials Processing Grants in 2024 is building local electrode material supply chains, including binders. U.S. lithium-ion battery imports of USD 13.1 Billion in 2024 signal the downstream scale already present — domestic binder capacity is being built to serve it.

Europe Market Trends

Europe’s market is shaped by two forces pulling in opposite directions: regulatory pressure restricting fluorinated materials like PVDF, and massive public investment in battery gigafactories. The European Investment Bank financed €1.8 Billion in gigafactory projects in 2024. EU lithium-ion accumulator imports of €23.5 Billion in 2024 show the region’s dependence on Asian supply — a gap European binder producers are positioned to help close.

Latin America Market Trends

Latin America remains an early-stage market for advanced electrode binder chemicals, with demand primarily linked to nascent EV assembly and consumer electronics manufacturing in Brazil and Mexico. The region’s primary role in the battery value chain is currently upstream — supplying lithium and other minerals — rather than in electrode chemical processing. Domestic binder demand will build as local battery manufacturing capacity develops through the forecast period.

Middle East & Africa Market Trends

The Middle East and Africa region is at the earliest stage of electrode binder market development. GCC nations are investing in battery and clean energy manufacturing as part of economic diversification strategies, which will create incremental binder demand over the forecast period. South Africa’s mineral wealth, including manganese and other battery materials, positions it as a potential upstream supplier to battery value chains rather than a near-term binder consumer.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Regulatory Landscape

The European Commission’s REACH regulation is tightening restrictions on per- and polyfluoroalkyl substances (PFAS), a category that includes PVDF binder materials widely used in cathode electrodes. The proposed universal PFAS restriction under REACH, active from 2023 to 2025 in the assessment phase, is pushing battery material producers to accelerate fluorine-free binder development. Manufacturers operating in European markets face compliance timelines that will require reformulation before commercialization deadlines.

The U.S. Environmental Protection Agency (EPA) issued updated solvent emission standards under the National Emission Standards for Hazardous Air Pollutants (NESHAP) framework in 2024, targeting NMP solvent use in battery electrode manufacturing. These rules require stricter NMP capture and recovery systems or shift to aqueous processes. Battery producers building U.S. gigafactories are designing around water-based binder systems to avoid NMP compliance costs from the outset.

India’s Ministry of Heavy Industries allocated ₹18,100 crore under the PLI scheme for Advanced Chemistry Cells in 2024, setting performance benchmarks for cells manufactured under the program. These benchmarks specify electrode quality standards that influence binder performance requirements. Binder suppliers targeting Indian PLI-funded customers must demonstrate compliance with the technical and domestic content criteria embedded in the scheme’s incentive structure.

Germany’s Federal Ministry for Economic Affairs published battery supply chain due diligence guidelines in 2025 aligned with the EU Battery Regulation, requiring chemical traceability for electrode materials including binders. German battery production of €12.3 Billion in 2024 represents a market where compliance documentation is becoming a procurement prerequisite — suppliers without full chain-of-custody records will be excluded from contracts at major German cell and EV manufacturers.

Drivers

EV Battery Scaling Forces Adoption of High-Performance Binder Chemistries

EV battery makers are buying binder chemicals in volumes that reflect cell production ambitions, not current EV sales. China’s battery output of over 940 GWh in 2024 required proportional binder chemical procurement at a scale that smaller, regional suppliers cannot serve. This demand concentration rewards binder producers who can guarantee consistent quality across multi-gigawatt supply agreements.

Performance limitations of standard PVDF binders — including poor ionic conductivity and mechanical stress under repeated cycling — are pushing cell engineers toward multifunctional polymer alternatives. When a binder improves electrode efficiency by reducing charge-transfer resistance, it becomes a performance input, not just an adhesive. This shift raises the technical bar and the value buyers assign to premium binder formulations.

Moreover, EV manufacturers are setting longer warranty and cycle life targets that cascade into stricter binder performance specifications. A binder that fails after 800 cycles is unacceptable in a vehicle targeting 1,500-cycle battery life. This requirement gap is driving active procurement decisions away from commodity binder sources toward specialty producers with validated long-cycle performance data.

Restraints

Water Reactivity in Cathodes Limits Large-Scale Aqueous Binder Rollout

Aqueous binder adoption in cathode electrodes faces technical barriers that have proven difficult to solve at commercial scale. Water reacts with lithium salts in high-nickel NMC cathode powders, causing lithium leaching and surface chemistry changes that degrade cell performance. Aluminum current collector corrosion in aqueous slurries adds a secondary failure mode that manufacturers must engineer around.

These technical barriers mean that cathode electrode producers cannot simply substitute water-based binders for PVDF without significant reformulation and qualification work. The qualification process for a new cathode binder in an automotive cell can take 18 to 24 months, during which the cell maker continues purchasing incumbent binders. This timeline creates a structural lag between chemistry readiness and commercial adoption.

Additionally, emerging binder-free electrode technologies pose a longer-term structural risk. Research programs targeting electrode designs that eliminate binders entirely — through direct material sintering or conductive additive networks — represent a substitution threat that, while not commercially mature, creates uncertainty for binder market long-term demand projections. Investors and buyers alike must weigh this risk against near-term market commitments.

Growth Factors

Fluorine-Free Binder Commercialization Opens New Revenue Streams for Specialty Producers

Fluorine-free and siloxane-based binder systems delivering over 1.4× higher lifespan stability than PVDF represent a high-value commercial opportunity for the producers who reach market first. European regulatory pressure on PFAS materials is creating a compliance deadline that converts R&D investment into a strategic asset. The first producers to offer validated, scalable fluorine-free cathode binders will control a market segment currently dominated by PVDF.

Water-based and solvent-free binder technologies also lower total manufacturing cost for battery producers by eliminating NMP solvent procurement, recovery systems, and associated environmental compliance costs. India’s USD 2.2 Billion PLI scheme for Advanced Chemistry Cells supports domestic battery manufacturing that is being designed around environmentally compliant aqueous processes from the start — creating a built-in customer base for water-based binder suppliers targeting the Indian market.

Furthermore, R&D in conductive and multifunctional binders — chemistries that simultaneously bind, conduct lithium ions, and reduce charge-transfer resistance — opens the possibility of removing conductive additives from electrode formulations. This functional consolidation increases the value contribution of the binder, justifying higher unit pricing and deeper integration into cell design decisions. Specialty producers who can demonstrate this dual functionality gain a pricing advantage over commodity binder suppliers.

Emerging Trends

Dry Electrode Processing Reshapes Binder Technical Requirements and Supply Models

Dry electrode coating eliminates liquid slurry processing entirely, requiring binders to function as fibrillated networks rather than dissolved adhesives. This fundamental change in processing mode means existing PVDF and SBR binder products are incompatible with dry electrode lines without modification. Binder producers must develop new product forms — dry-processable PTFE fibers or specialty polymer powders — that fit dry electrode manufacturing specifications.

The trend toward bio-based and aqueous binders is also reshaping supplier selection criteria among battery makers responding to OEM sustainability mandates. Automotive customers are embedding carbon footprint requirements into battery procurement contracts, and binder chemistry is a measurable input. Bio-derived CMC and other renewable-origin binders are gaining specification advantage in tenders where lifecycle emissions reporting is required alongside technical performance data.

Additionally, binder engineering for electrode microstructure optimization — including modeling how binders migrate and distribute at pore scale during drying — is emerging as a technical differentiator. Producers who can provide binders engineered for specific microstructure targets, rather than generic formulations, are moving from commodity suppliers to technical development partners for battery manufacturers. This repositioning supports higher margins and longer customer relationships.

Key Companies Insights

Kureha Corporation is the world’s leading PVDF binder producer, with Specialty Chemicals segment revenue of ¥33.95 Billion (USD 230 Million) in 2024 including PVDF binder materials. However, the company’s Advanced Materials segment posted a 22.0% revenue decline year-on-year in 2024 due to weaker EV market demand for PVDF binders — a signal that even the category leader must diversify into next-generation binder chemistries to maintain long-term revenue stability.

Arkema S.A. occupies a strong position in fluoropolymer-based binder chemicals, competing directly with Kureha in PVDF supply for battery cathode applications. Arkema’s vertically integrated fluorochemical capabilities — from HF production through to specialty polymer compounding — give it a cost and supply security advantage that pure-play binder producers cannot replicate. Its PVDF product lines for battery applications are marketed under the Kynar brand, which holds strong recognition among cathode electrode manufacturers globally.

Solvay S.A. brings broad specialty polymer expertise to the electrode binder market, with products addressing both cathode and anode binder needs. Solvay’s active participation in European battery alliance programs positions it to benefit from the region’s push for domestic battery material supply chains. The company’s R&D investment in next-generation binder systems — including fluorine-reduced and high-performance alternatives — aligns with European regulatory direction and OEM procurement trends favoring local, compliant suppliers.

Daikin Industries Ltd. is a fluorochemical specialist whose binder product portfolio serves cathode electrode applications in lithium-ion cells. Daikin’s deep fluoropolymer manufacturing know-how and integrated production across Japan and global facilities give it reliable supply capacity at automotive cell manufacturing scale. The company’s ongoing investment in PVDF production capacity expansion reflects its long-term commitment to the battery materials market even as regulatory pressure on fluorinated materials builds in Europe.

Key Companies

- Kureha Corporation

- Arkema S.A.

- Solvay S.A.

- Daikin Industries Ltd.

- ZEON Corporation

- BASF SE

- Dow Inc.

- DuPont de Nemours Inc.

- Evonik Industries AG

- Wacker Chemie AG

- Henkel AG & Co. KGaA

- Nippon A&L Inc.

- BOBS-TECH

- Chengdu Indigo Power Sources

- Shanghai 3F New Materials Co., Ltd.

- Zhejiang Juhua Co., Ltd.

- Dongyue Group Limited

- Suzhou Crystal Clear Chemical Co., Ltd.

- Sinochem Lantian Co., Ltd.

Recent Development

- In March 2024, Zeon Corporation (via Zeon Ventures Inc.) invested in Coreshell Technologies, Inc. (a U.S. startup developing nano-layer coating materials for lithium-ion battery electrodes). The investment amount was undisclosed. Zeon will partner on commercialization, combining its electrode binder technology with Coreshell’s coatings to enhance capacity, heat resistance, safety, and cost efficiency without major manufacturing changes.

- In May 2025, Arkema introduced/ highlighted its Kynar PVDF electrode binder solutions for dry coating processes as part of its portfolio for next-generation semi-solid (gel electrolyte) batteries. This supports more efficient and sustainable dry electrode manufacturing (eliminating solvents to reduce energy use and carbon footprint). Arkema is investing in a lab-scale dry coating facility in France with dedicated R&D resources.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.75 Billion |

| Forecast Revenue (2035) | USD 13.68 Billion |

| CAGR (2026-2035) | 17.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (PVDF, SBR, CMC, PAA), By Battery Type (Lithium-ion Batteries, LFP, NMC), By Form (Powder Form, Slurry Form), By Type (Water-based Binders, Solvent-based Binders), By Electrode Type (Anode Binders, Cathode Binders), By Technology (Wet Coating Process, Dry Electrode Coating), By Application (Graphite-based Anodes, Silicon-based Anodes, Solid-state Batteries, Other), By End-Use Industry (Electric Vehicles, Consumer Electronics, Energy Storage Systems, Other) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Kureha Corporation, Arkema S.A., Solvay S.A., Daikin Industries Ltd., ZEON Corporation, BASF SE, Dow Inc., DuPont de Nemours Inc., Evonik Industries AG, Wacker Chemie AG, Henkel AG & Co. KGaA, Nippon A&L Inc., BOBS-TECH, Chengdu Indigo Power Sources, Shanghai 3F New Materials Co., Ltd., Zhejiang Juhua Co., Ltd., Dongyue Group Limited, Suzhou Crystal Clear Chemical Co., Ltd., Sinochem Lantian Co., Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |