What is the Satellite-to-Mobile (NTN) Communication Market?

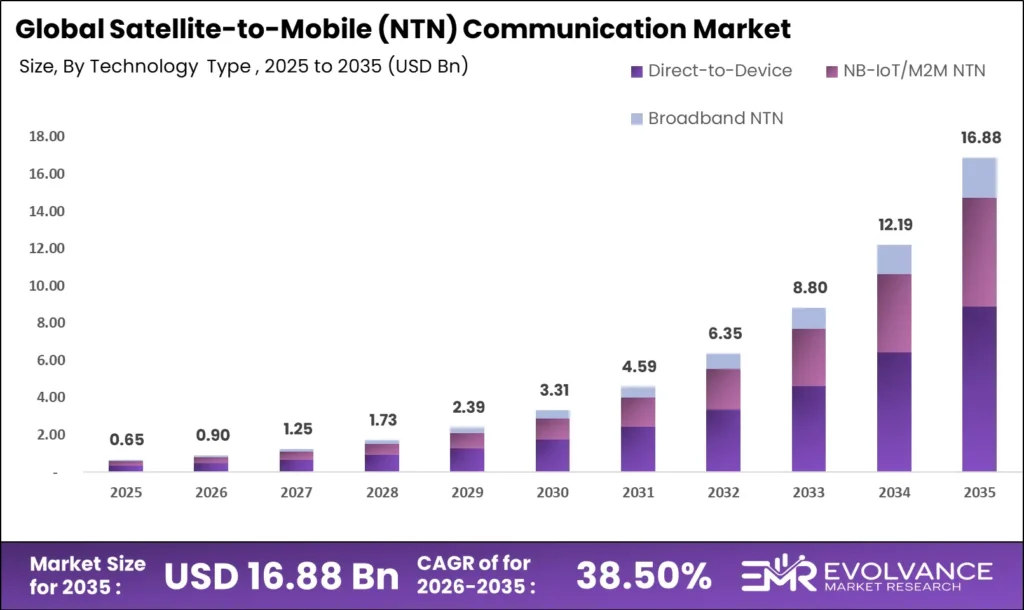

The global satellite-to-mobile (NTN) communication market was valued at USD 0.65 billion in 2025 and is projected to reach approximately USD 16.88 billion by 2035, growing at a CAGR of 38.50% during the forecast period 2026 to 2035. Accelerating direct-to-device satellite deployments, 3GPP NTN standardization under Release 17 and 18, and mounting commercial demand for ubiquitous connectivity beyond terrestrial network reach are the structural forces driving this expansion.

The convergence of low-cost launch economics and miniaturized satellite hardware has created a viable commercial pathway. SpaceX Starlink Direct to Cell, AST SpaceMobile’s BlueBird constellation, and Lynk Global’s licensed operator partnerships have all reached commercial milestones within a 24-month window — compressing a decade-long technology transition into a near-term procurement reality for mobile network operators. Consumer handset manufacturers embed satellite chips targeting emergency notification for the 3.6 billion people globally outside reliable terrestrial coverage, while industrial IoT operators require ultra-low-power NTN with multi-year battery autonomy. Each demand driver generates distinct revenue per connection, contract structure, and technology requirement — creating multiple parallel growth engines rather than a single demand thesis.

Satellite-to-Mobile (NTN) Market Highlights: Key Data at a Glance

- Market value: USD 0.65 billion in 2025, forecast to USD 16.88 billion by 2035 at 38.50% CAGR

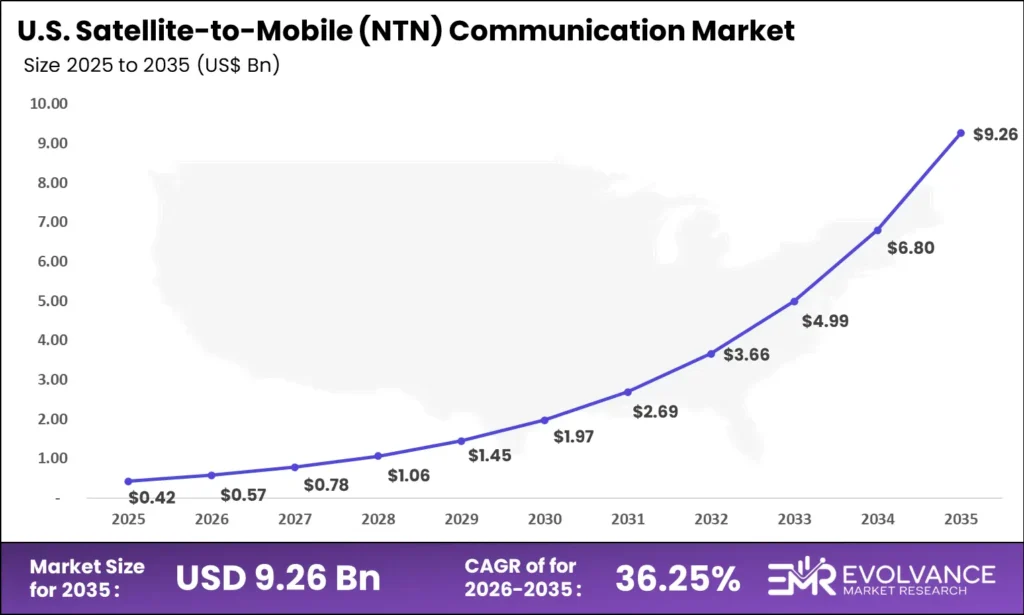

- US market: USD 0.42 billion in 2025, forecast to USD 9.26 billion by 2035 at 36.25% CAGR

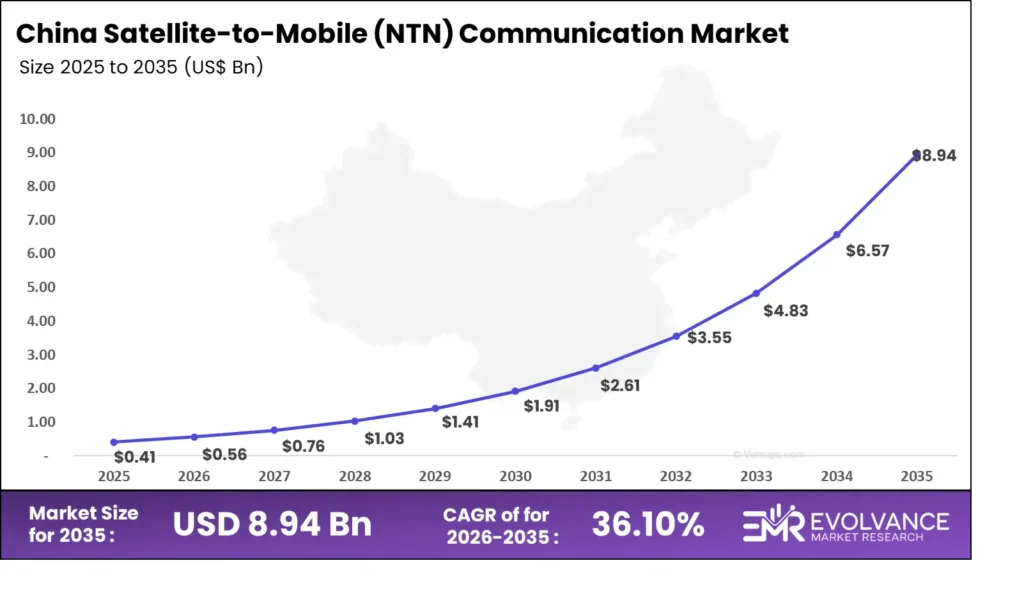

- China market: USD 0.41 billion in 2025, forecast to USD 8.94 billion by 2035 at 36.1% CAGR

- Dominant technology: Direct-to-Device (D2D) Satellite at 42.3% revenue share

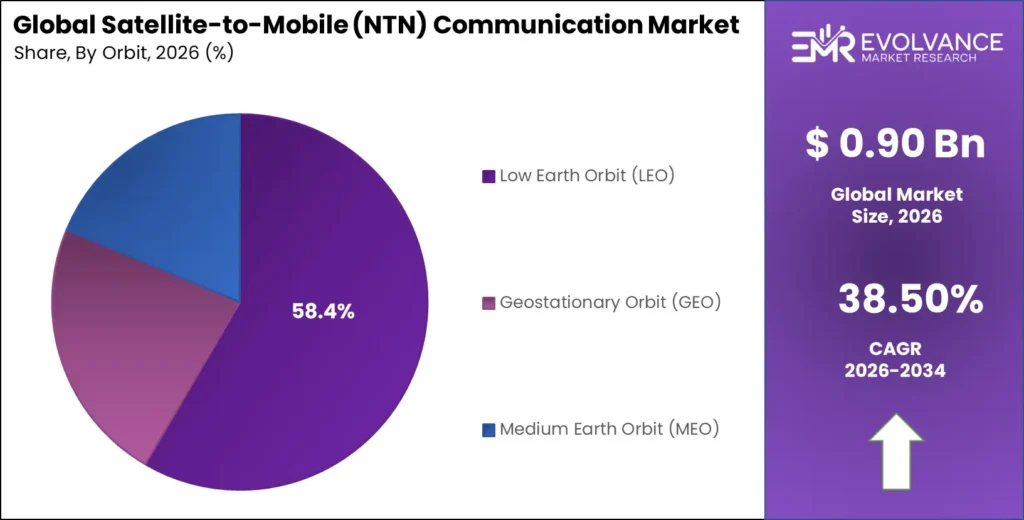

- Dominant orbit: Low Earth Orbit (LEO) at 58.4% revenue share

- Dominant application: Emergency & Safety Communications at 29.4% revenue share

- Dominant end-use: Consumer / Mobile Users at 38.7% revenue share

- Dominant component: Space Segment at 44.2% revenue share

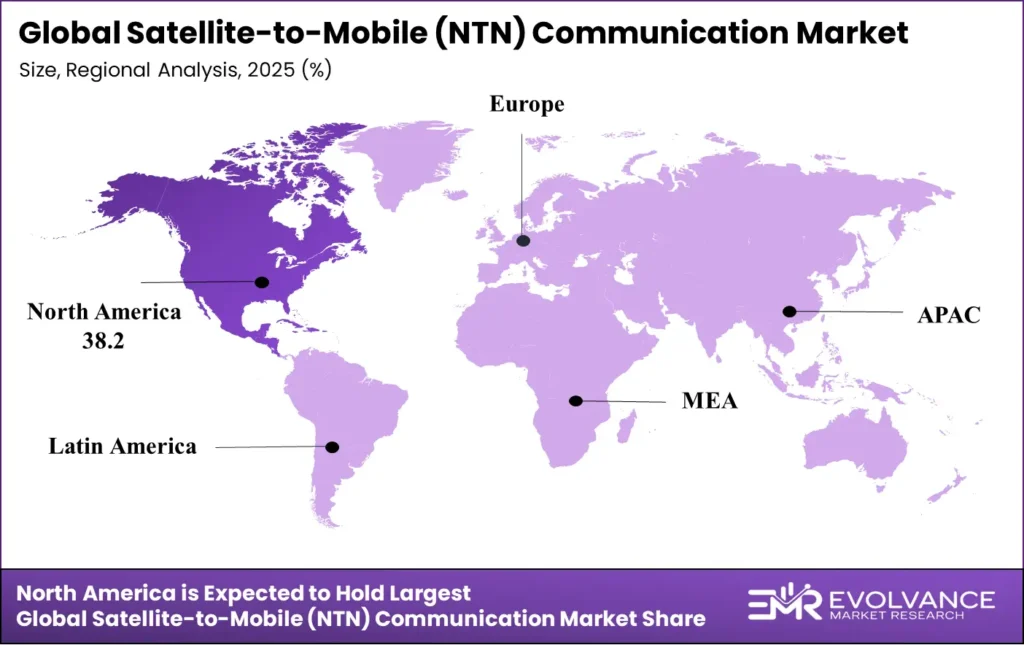

- North America: Largest regional share at 38.2%, valued at USD 0.83 billion in 2025

- Asia-Pacific: Fastest-growing region globally at 31.8% CAGR

US Satellite-to-Mobile (NTN) Market

The US NTN market will reach USD 0.42 billion by 2035 from USD 9.26 billion in 2025 at a CAGR of 36.25%. The US leads global NTN adoption through domestic constellation operators — SpaceX, AST SpaceMobile, Globalstar, and Iridium — and the FCC’s 2023 Supplemental Coverage from Space (SCS) licensing framework that compressed multi-year regulatory barriers into a replicable market entry pathway.

The T-Mobile and SpaceX Starlink Direct partnership — commercially launched in 2024 and expanded to voice in February 2026 — validates both consumer adoption and the MNO revenue model across T-Mobile’s 115 million subscribers. AT&T’s parallel engagement with AST SpaceMobile and Verizon’s exploratory Kuiper partnerships create competitive urgency. FCC proceedings on co-primary MSS spectrum allocation remain the most material regulatory variable determining commercial velocity for full broadband D2D services beyond the current text and emergency SOS tier.

China Satellite-to-Mobile (NTN) Market

The China NTN market will reach USD 0.41 billion by 2035 from USD 8.94 billion in 2025 at a CAGR of 36.1%. Growth is anchored by the state-directed Guowang (SatNet) mega-constellation targeting 13,000+ LEO satellites, and Geespace deploying direct-to-device automotive and consumer connectivity. MIIT’s NTN integration roadmap within 5G-A standards creates structured domestic procurement for Huawei and ZTE NTN radio solutions.

China Telecom, China Mobile, and China Unicom are piloting NTN architectures routing satellite connectivity through terrestrial 5G core functions under 3GPP Release 17 hybrid specifications. Domestic handset manufacturers Huawei, Xiaomi, and OPPO have launched smartphone models with Beidou satellite messaging, building a consumer device ecosystem independent of international constellation operators. Foreign operators entering China face vendor preference architecture alongside spectrum licensing requirements that structurally favor domestic satellite operators in co-primary allocation decisions.

China Telecom, China Mobile, and China Unicom are piloting NTN architectures routing satellite connectivity through terrestrial 5G core functions under 3GPP Release 17 hybrid specifications. Domestic handset manufacturers Huawei, Xiaomi, and OPPO have launched smartphone models with Beidou satellite messaging, building a consumer device ecosystem independent of international constellation operators. Foreign operators entering China face vendor preference architecture alongside spectrum licensing requirements that structurally favor domestic satellite operators in co-primary allocation decisions.

Market Overview: Why NTN Investment Is Structurally Accelerating

The satellite-to-mobile NTN communication market encompasses satellites, ground infrastructure, user terminal hardware, and software platforms enabling mobile devices — smartphones, IoT sensors, and maritime terminals — to connect directly to satellite networks without dedicated dish antennas. It excludes traditional fixed-satellite broadband requiring installation hardware and military-only classified satellite systems. Market scope covers both standardized 3GPP NTN architectures and proprietary direct-to-device implementations commercialized ahead of formal standards.

This analysis integrates satellite operator filings with the FCC, Ofcom, and ITU; publicly disclosed constellation CAPEX from SpaceX, AST SpaceMobile, and Amazon; device shipment data from IDC and Counterpoint Research; and regulatory proceedings across 14 national spectrum authorities. Segment share percentages were cross-referenced against reported revenues from Iridium, Globalstar, and Inmarsat alongside funding rounds for Skylo, Lynk Global, and Telesat to construct a forecast grounded in verified commercial performance.

Technology Analysis

Direct-to-Device (D2D) Satellite Dominates with 42.3% Due to Smartphone Integration Momentum

| Technology | Share % | Primary Driver |

|---|---|---|

| Direct-to-Device (D2D) Satellite | 42.3% | Smartphone-native satellite capability and emergency SOS adoption |

| Narrowband IoT / M2M NTN | 31.8% | Agricultural sensors, logistics tracking, remote industrial monitoring |

| Broadband NTN | 25.9% | Maritime, aviation, and enterprise high-throughput connectivity |

In 2025, Direct-to-Device satellite technology held a dominant market position with a 42.3% share. Apple’s Emergency SOS via satellite — deployed across iPhone 14 series globally since November 2022 — established the consumer proof-of-concept, while SpaceX Starlink Direct to Cell, operating with T-Mobile, SoftBank, Rogers, and Optus, expanded the addressable D2D revenue base toward two-way text, voice, and data on unmodified SIM-capable handsets. Qualcomm’s Snapdragon Satellite platform and MediaTek’s NTN-integrated chipset portfolio are converting D2D from a hardware upgrade into a standard baseband capability — the inflection enabling mass-market adoption by 2027.

Narrowband IoT and M2M NTN serves the largest device volume market. Agricultural precision farming — soil sensors, livestock tracking, weather monitoring — represents over 500 million globally addressable devices of which fewer than 15% have reliable connectivity. Skylo, Kineis, and OQ Technology are enabling existing cellular IoT chipsets to connect via satellite under 3GPP Release 17 without hardware redesign. Broadband NTN addresses the highest average revenue per user — maritime operators, airlines, and remote enterprise managers require sustained throughput that LEO and MEO constellations deliver competitively, with 28,000 commercial aircraft representing recurring monthly revenue across the aviation inflight connectivity segment.

Orbit Analysis

Low Earth Orbit (LEO) Dominates with 58.4% Due to Latency Advantage and Constellation Scale

| Orbit Type | Share % | Primary Driver |

|---|---|---|

| Low Earth Orbit (LEO) | 58.4% | Sub-100ms latency and high satellite count enabling global coverage density |

| Geostationary Orbit (GEO) | 22.9% | Continuous regional coverage and legacy maritime/aviation installed base |

| Medium Earth Orbit (MEO) | 18.7% | GPS-adjacent spectrum assets and balanced latency/coverage trade-off |

In 2025, Low Earth Orbit held a dominant market position with a 58.4% share. SpaceX’s Starlink constellation — exceeding 6,700 operational satellites by Q1 2026 — and AST SpaceMobile’s BlueBird commercial constellation together represent the largest LEO capacity deployment in history. The fundamental LEO advantage for mobile applications is propagation latency: at 550 km altitude, round-trip delay is approximately 40–60 ms versus 600+ ms for GEO — the threshold below which voice calls, video, and real-time data function acceptably on standard mobile protocols.

Geostationary orbit retains commercial relevance through continuous regional coverage from a single satellite position, eliminating LEO’s handover complexity. Maritime VSAT operators including Inmarsat, SES, and Eutelsat maintain multi-year equipment contracts with shipping operators certified to GEO terminal specifications — terminal replacement costs sustain GEO revenue into the late 2020s even as LEO throughput economics improve. SES O3b mPOWER in MEO occupies a commercially differentiated position serving island nations and maritime platforms requiring throughput levels entry-level LEO services do not yet consistently deliver at enterprise SLA standards.

Application Analysis

Emergency & Safety Communications Dominates with 29.4% Due to Government Mandate and Life-Safety Demand

| Application Segment | Share % | Primary Driver |

|---|---|---|

| Emergency & Safety Communications | 29.4% | Government mandates and life-safety demand for ubiquitous coverage |

| Maritime & Aviation Connectivity | 22.1% | Regulatory inflight connectivity requirements and maritime digitalization |

| IoT & Agricultural Monitoring | 18.6% | Precision agriculture and remote industrial asset tracking |

| Consumer Mobile Broadband | 16.8% | Rural broadband gap filling and handset-native satellite fallback |

| Government & Defense | 13.1% | Mission-critical communications and infrastructure resilience |

In 2025, Emergency and Safety Communications led application segments with a 29.4% share. Government-mandated emergency alerting requirements — including the US Wireless Emergency Alert system, the EU-Alert framework, and Japan’s earthquake early warning — are being extended to satellite connectivity to address coverage gaps during terrestrial network failures. The 2023 Maui wildfires, 2024 Chile earthquake, and 2025 Pakistan flooding each demonstrated the public safety cost of terrestrial-only emergency communication, creating legislative pressure for satellite emergency connectivity mandates that provide NTN operators with a regulatory revenue floor distinct from commercial subscription revenue.

Maritime and Aviation connectivity represents the highest average revenue per terminal despite lower device counts. Maritime VSAT subscriptions generate USD 1,000–3,500 per month per vessel, with Inmarsat’s Fleet XPress maintaining over 15,000 vessel contracts as of 2025. IoT and Agriculture carries the largest total addressable connection count — 1.4 billion hectares of global agricultural land where Trimble, John Deere, and CNH Industrial are integrating NTN into precision agriculture platforms generating recurring IoT subscription revenue.

End-Use Analysis

Consumer / Mobile Users Dominate with 38.7% Due to Smartphone Satellite Capability Integration

| End-Use Segment | Share % | Primary Driver |

|---|---|---|

| Consumer / Mobile Users | 38.7% | Smartphone-native satellite SOS and outdoor activity safety |

| Enterprise & Industrial | 34.2% | Maritime, aviation, logistics, and agriculture connectivity SLAs |

| Government & Defense | 27.1% | Resilient mission-critical communications and emergency infrastructure |

In 2025, Consumer and Mobile Users held a dominant position with a 38.7% share. Apple’s Emergency SOS via satellite in 2022 was the inflection — the first mass-market satellite feature in a standard smartphone form factor. Google Pixel Satellite SOS and Samsung Galaxy satellite messaging integration have since broadened the addressable base beyond iOS. As per IDC Q4 2025 data, over 280 million smartphones shipped annually include satellite communication capability, forecast to exceed 600 million by 2028 as NTN baseband integration migrates from flagship to mid-range tiers.

Enterprise and Industrial end-use generates higher revenue per connection than consumer despite lower volumes. Maritime shipping, offshore energy, remote mining, and aviation sign multi-year agreements with throughput and availability SLAs commanding significant pricing premiums. Government and Defense commands the highest absolute contract values — US DoD programs, NATO resilient communication mandates, and sovereign procurement across Australia, Canada, and the EU generate multi-year revenue visibility at margins substantially above commercial operator deployments.

Component Analysis

Space Segment Dominates with 44.2% Due to Constellation CAPEX Concentration

| Component | Share % | Primary Driver |

|---|---|---|

| Space Segment | 44.2% | Constellation manufacturing, launch, and on-orbit operations costs |

| User Terminal / Device | 32.8% | NTN chipset integration in smartphones, IoT modules, and enterprise terminals |

| Ground Segment | 23.0% | Gateway infrastructure, network operations centers, and spectrum management |

In 2025, the Space Segment held a dominant position with a 44.2% share, reflecting concentrated constellation construction CAPEX. SpaceX’s Starbase facility produces up to 6 satellites per day with launch economics reducing cost per satellite below USD 500,000 at scale. AST SpaceMobile’s BlueBird — the largest commercial communications satellites by aperture ever deployed at LEO — eliminate ground hardware upgrade requirements for direct standard-handset service, shifting cost structure toward space assets. LEO satellite replacement every 5–7 years represents recurring CAPEX investors must model within service revenue projections.

User Terminal and Device integration is the highest-leverage component for adoption velocity. The transition from proprietary satellite handsets retailing at USD 800–1,500 to standard smartphone capability eliminates the device acquisition barrier previously confining satellite connectivity to enterprise and government buyers. Qualcomm’s Snapdragon Satellite embeds satellite messaging within standard 5G chipsets at BOM cost below USD 5 per device — the threshold allowing consumer manufacturers to absorb cost within standard margins — while MediaTek’s NTN chipset extends satellite capability below the USD 300 retail price point critical for emerging market adoption.

Key Market Segments

By Technology

- Direct-to-Device (D2D) Satellite

- Narrowband IoT / M2M NTN

- Broadband NTN

By Orbit

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

By Application

- Emergency & Safety Communications

- Maritime & Aviation Connectivity

- IoT & Agricultural Monitoring

- Consumer Mobile Broadband

- Government & Defense

By End-Use

- Consumer / Mobile Users

- Enterprise & Industrial

- Government & Defense

By Component

- Space Segment

- User Terminal / Device

- Ground Segment

Regional Analysis of Satellite-to-Mobile (NTN) Communication Market

North America Leads at 38.2% Share

| Region | Market Value (2025) | Share % | CAGR |

|---|---|---|---|

| North America (US) | USD 0.83 billion | 38.2% | 28.9% |

| Asia-Pacific | USD 0.60 billion | 27.4% | 31.8% (fastest) |

| Europe | USD 0.41 billion | 18.9% | 26.7% |

| Latin America | USD 0.19 billion | 8.7% | 27.3% |

| Middle East & Africa | USD 0.15 billion | 6.8% | 24.1% |

North America holds 38.2% of global NTN revenue at USD 0.83 billion in 2025. The FCC’s progressive SCS licensing, domestic presence of SpaceX, AST SpaceMobile, Globalstar, Iridium, and Amazon Kuiper, and smartphone penetration exceeding 85% collectively create structural advantage for US NTN operators. Europe’s NTN market reached USD 0.41 billion in 2025, driven by the EU’s IRIS² sovereign constellation program and national operator NTN partnerships — Deutsche Telekom with SpaceX and Orange’s Skylo IoT NTN integration demonstrate that European Tier-1 operators treat NTN as a standard network layer.

Asia-Pacific Satellite-to-Mobile (NTN) Communication Market: Fastest-Growing Region Globally

Asia-Pacific’s 31.8% CAGR makes it the fastest-growing major region. India’s TRAI satellite spectrum proceedings, Japan’s NTT DOCOMO NTN partnership, and Southeast Asia’s archipelago geography — Indonesia, Philippines, Vietnam — create structural NTN demand that terrestrial 5G economics cannot resolve. The Middle East and Africa region features Sub-Saharan Africa’s 1.1 billion population — fewer than 35% with reliable mobile broadband — representing the global NTN addressable market with the greatest per-connection impact. MTN Group’s pan-African Starlink enterprise partnership and Saudi Arabia’s Vision 2030 mandate are generating structured procurement for NTN maritime and emergency platforms.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- United Kingdom

- Netherlands

- Sweden

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Investment Landscape & Funding Activity

Over USD 4.5 Billion in Disclosed NTN Financing Validates Commercial Market Maturity

| Company | Round / Instrument | Amount (USD) | Year | Investor Profile |

|---|---|---|---|---|

| AST SpaceMobile | Equity — Public Markets | USD 400M+ raised | 2024–2025 | AT&T, Verizon, Google, Rakuten strategic + public |

| Telesat Lightspeed | Government Debt + Equity | USD 2.4B CAD government | 2025 | Canada government + export financing |

| Skylo Technologies | Series C+ Equity | USD 300M+ cumulative | 2023–2025 | SoftBank, Deutsche Telekom, Lockheed Martin |

| Lynk Global | Series B Equity | USD 110M | 2024 | Strategic telecom investors, SpaceCom |

| Amazon Kuiper | Internal CAPEX | USD 10B+ committed | 2020–2025 | Amazon balance sheet |

| OQ Technology | Series A/B Equity | USD 50M cumulative | 2023–2025 | European space VCs, ESA BIC alumni |

Investment activity across the satellite-to-mobile NTN ecosystem exceeded USD 4.5 billion in disclosed equity and debt financing during 2024–2025, signaling institutional confidence in the market’s commercial trajectory. Strategic investors — mobile network operators including AT&T, Verizon, SoftBank, Deutsche Telekom, and Rakuten — are providing both capital and commercial validation by becoming equity stakeholders in the NTN operators they intend to partner with, eliminating the customer acquisition uncertainty that typically characterizes early-stage technology markets. Government financing programs — Canada’s Telesat Lightspeed commitment, EU’s IRIS² allocation, and Australia’s Defence Space Strategy — are simultaneously de-risking constellation CAPEX for operators targeting sovereign market segments.

Third, the venture capital entry point for NTN IoT operators — Skylo, Lynk Global, OQ Technology, and Kineis — is systematically lower than broadband LEO investments, reflecting narrower but more predictable revenue models anchored in industrial IoT subscriptions. For investors, the risk spectrum runs from early-stage IoT NTN operators with validated MNO partnerships but pre-scale revenue, to mature companies like Iridium and Globalstar generating recurring service revenue with visible CAPEX cycles. The most significant unresolved valuation question remains the revenue ceiling for direct-to-device consumer broadband at the scale SpaceX and AST SpaceMobile are targeting.

Key Companies: Competitive Landscape

Three companies — SpaceX (Starlink), AST SpaceMobile, and Iridium Communications — define the competitive architecture of the satellite-to-mobile NTN market through constellation scale, operator partnership depth, and direct-to-device technology differentiation. This concentration in D2D coexists with meaningful competition in IoT NTN (Skylo, Kineis), broadband NTN (SES O3b, Inmarsat), and chipset integration (Qualcomm, MediaTek).

| Company | Revenue / Segment | Growth | Year |

|---|---|---|---|

| SpaceX (Starlink) | Est. USD 8.0B (Starlink segment) | +80% YoY (est.) | FY2024 (est.) |

| AST SpaceMobile | USD 36.6M (commercial launch phase) | N/A — early-stage | FY2024 |

| Iridium Communications | USD 796.2M (total service revenue) | +4% YoY | FY2024 |

| Inmarsat (Viasat) | Part of Viasat USD 2.03B | Stable / integrating | FY2024 |

| Globalstar | USD 256.4M (total revenue) | +6% YoY | FY2024 |

| SES S.A. | EUR 1.88B (total revenue) | -3% reported | FY2024 |

Competitive Landscape Matrix: NTN Operator Capability Comparison

| Capability | SpaceX Starlink | AST SpaceMobile | Iridium | Amazon Kuiper | Skylo | SES O3b |

|---|---|---|---|---|---|---|

| Standard Handset D2D | ✔ Commercial | ✔ Commercial | ✔ Via Qualcomm | ✘ In development | ✔ IoT only | ✘ |

| Voice Services | ✔ Launched Feb 2026 | ✔ Beta | ✔ Certus | ✘ | ✘ | ✔ Enterprise |

| Broadband (>1 Mbps) | ✔ Business tier | ✔ LTE-speed | ✘ | ✔ Enterprise | ✘ | ✔ mPOWER |

| IoT / NB-IoT NTN | ✔ Indirect | ✘ | ✔ Short burst | ✔ Planned | ✔ Core product | ✘ |

| Global Coverage | ✔ Near-global | Partial (24 countries) | ✔ Full polar | Partial | ✔ Via MNO partners | Regional |

| MNO Partnerships | T-Mobile, SoftBank, Rogers | AT&T, Verizon, Rakuten | Apple, Qualcomm OEMs | TBD | DT, SoftBank, BSNL | Enterprise only |

| 3GPP NTN Compliant | Release 17/18 | Release 17/18 | Proprietary + R17 | Release 17/18 | Release 17 | Release 17/18 |

| Commercial Status | Full commercial | Commercial (limited) | Full commercial | Beta enterprise | Full commercial | Full commercial |

SpaceX Starlink leads all competitive dimensions in coverage breadth and commercial scale, with enterprise maritime and aviation tiers generating average monthly revenues of USD 250–500 per terminal. AST SpaceMobile is the only operator designed from inception for full LTE-speed standard handset connectivity — a technical differentiation validated commercially by AT&T, Verizon, and Rakuten. Iridium provides the infrastructure layer behind Apple Emergency SOS and Qualcomm Snapdragon Satellite, making it the critical enabler of smartphone-embedded satellite messaging adopted globally. Amazon Kuiper, still in beta as of Q1 2026, represents the most significant emerging competitive threat to Starlink’s enterprise broadband segment through Amazon’s distribution, cloud, and logistics relationships.

Top Key Players

- SpaceX (Starlink)

- AST SpaceMobile

- Iridium Communications

- Inmarsat (Viasat-owned)

- Globalstar

- SES S.A. (O3b mPOWER)

- Amazon (Project Kuiper)

- Telesat Lightspeed

- Skylo Technologies

- Lynk Global

- Qualcomm Technologies (Snapdragon Satellite)

- MediaTek (NTN Chipset Platform)

- Others

Related Markets: 5 Segments Shaping NTN Satellite-to-Mobile Communication

- LEO Satellite Market: Valued at USD 14.8B in 2025, reaching USD 89.3B by 2035 at 19.7% CAGR. LEO satellite market growth directly enables NTN mobile connectivity economics — Starship launch economics are compressing per-satellite orbit insertion costs toward USD 300,000, making continuous global coverage financially sustainable without government subsidy.

- IoT Satellite Communication Market: Valued at USD 4.32B in 2025, forecast to reach USD 24.1B by 2035 at 18.8% CAGR. IoT satellite market growth drives NTN adoption through 3GPP Release 17 NB-IoT specifications enabling standard cellular IoT chipsets to access satellite networks without custom hardware.

- Mobile Satellite Services (MSS) Market: Valued at USD 6.1B in 2025, growing at 12.4% CAGR through 2035. MSS market growth provides the regulatory licensing foundation — spectrum coordination, landing rights, and roaming agreements — that NTN direct-to-device operators require in each national market.

- Emergency Communication Market: Valued at USD 33.4B in 2025, projected to reach USD 68.7B by 2035 at 7.5% CAGR. Emergency communication market expansion is embedding satellite connectivity mandates following repeated terrestrial network failures — creating government procurement requirements providing NTN operators with recurring baseline revenue.

- 5G NTN Infrastructure Market: Valued at USD 1.87B in 2025, forecast to reach USD 19.4B by 2035 at 26.4% CAGR. 5G NTN market growth is driven by 3GPP Release 17 and 18 standardization enabling seamless handover between terrestrial 5G and NTN satellite networks manageable through unified core network architecture.

Regulatory Framework Deep Dive

3GPP, ITU, FCC, and National Spectrum Authorities Define the NTN Commercial Authorization Landscape

| Regulatory Body / Framework | Scope | Key Requirement / Status | Commercial Impact |

|---|---|---|---|

| 3GPP Release 17 (NTN IoT) | Global standard | NB-IoT and eMTC operation via satellite; commercially frozen 2022 | Enables standard IoT chipsets to access satellite — eliminates custom hardware barrier |

| 3GPP Release 18 (NTN Handheld) | Global standard | Broadband NTN for handheld devices; seamless 5G-NTN handover; frozen 2024 | Converts NTN from proprietary to standard 5G feature — unlocks mass-market device integration |

| FCC — SCS License (US) | United States | Supplemental Coverage from Space; first license granted T-Mobile/SpaceX 2023 | Regulatory template accelerating US D2D launch; sets global precedent for other regulators |

| ITU — MSS Coordination | Global / Multi-lateral | Non-GSO constellation filing, EPFD limits, interference coordination between operators | Controls spectrum access rights; ITU dispute proceedings can delay constellation expansion |

| EU — IRIS² Program | European Union | Sovereign LEO/MEO broadband constellation; EUR 6B funded; commercial from 2027 | Creates protected EU government procurement channel; limits non-EU operator access to sovereign contracts |

| TRAI — India NTN Consultation | India | Satellite spectrum assignment for broadband and IoT NTN; consultation ongoing 2025 | Determines commercial launch timeline for SpaceX, OneWeb, Amazon in India’s 1.4B population market |

| GSMA — NTN Guidelines | Industry body | API and network integration best practices for NTN-MNO partnerships | Reduces integration complexity; accelerates MNO partner onboarding timelines |

| Ofcom — SCS Policy (UK) | United Kingdom | UK SCS licensing framework; consultation completed Q4 2025 | Enables UK D2D commercial services from 2026; aligns with post-Brexit national space strategy |

The NTN regulatory landscape is bifurcating into two distinct authorization tracks. The first — national SCS licensing frameworks modeled on the FCC’s 2023 precedent — is reducing market entry barriers in the US, UK, Australia, and Canada, compressing approval timelines to 12–18 months. The second track — ITU inter-system coordination proceedings — operates on a multi-year timescale outside any single regulator’s control, creating an irreducible latency between constellation deployment and commercial spectrum authorization in contested orbital arc segments.

The most strategically significant near-term regulatory development is TRAI’s India NTN spectrum assignment conclusion. A determination favoring satellite-agnostic spectrum assignment rather than spectrum auctions will enable SpaceX, Amazon, and OneWeb to compete on service quality, accelerating the pricing that drives mass-market adoption. Operators without pre-existing TRAI processes in progress will face 18–24 month delays entering the Indian market after a spectrum framework is established — creating competitive urgency for regulatory filing completeness across all operators with India in their commercial roadmaps.

Key Growth Drivers of Satellite-to-Mobile (NTN) Communication Market

3GPP NTN Standardization and Smartphone Integration Drive Structural Mass-Market Adoption

3GPP’s formal NTN integration within 5G specifications — Release 17 for IoT NTN and Release 18 for broadband NTN with handheld device support — is the most consequential structural driver for long-term market scale. Standardization converts satellite connectivity from a proprietary hardware capability requiring custom handsets into a software-defined network feature chipset manufacturers integrate at commodity economics. Qualcomm and MediaTek, together commanding over 85% of global LTE and 5G baseband chipset supply, have both committed to NTN integration roadmaps delivering satellite connectivity on sub-USD 200 devices by 2027, creating a device installed base growing by hundreds of millions annually.

Coverage gap economics provide a second durable structural driver. GSMA estimates closing global coverage gaps through terrestrial infrastructure alone requires USD 400 billion in additional network investment — NTN satellite capacity can replace this at a fraction of the cost, creating a structural operator procurement incentive that does not require consumer premium willingness to pay. Climate resilience mandates add a third growth driver: emergency management agencies across the US, Japan, Australia, and EU are embedding satellite backup requirements into public safety procurement, providing NTN operators with multi-year government contracts that commercial subscriptions cannot match in revenue visibility.

Restraints

Spectrum Regulatory Fragmentation and Device Certification Complexity Compress Market Velocity

International spectrum regulatory fragmentation is the primary structural constraint on NTN market velocity. NTN operators require spectrum authorization in every national jurisdiction — a process involving ITU filing coordination, national spectrum authority approval, and mobile operator partnership agreements as licensing conditions in many markets. India, Brazil, and Indonesia impose additional requirements for local incorporation, domestic gateway infrastructure, and satellite manufacturing localization extending market entry timelines by 12–24 months. Regulatory sequencing across 50+ national markets creates multi-year launch dependencies that defer revenue recognition against constellation CAPEX already committed.

Device certification timelines add a parallel constraint. Each NTN-capable device requires type approval from national telecommunications regulators — FCC in the US, CE marking in Europe, BIS in India — before commercial sale. Certifying across 40+ national markets extends go-to-market timelines by 6–18 months versus purely terrestrial device launches. Orbital congestion and debris mitigation requirements add an emerging regulatory constraint: FCC rules requiring LEO satellite deorbit within 5 years and ITU constellation filing requirements add compliance cost and uncertainty that operators must model within constellation expansion CAPEX assumptions.

Opportunities

Enterprise Private Connectivity and Sovereign NTN Infrastructure Unlock Premium Revenue Segments

Enterprise private NTN deployments for maritime, energy, and mining operations represent the highest near-term average contract value expansion. Offshore oil and gas platforms, deep-sea mining vessels, and transoceanic shipping routes require guaranteed connectivity for SCADA control, crew welfare, and cargo tracking that cannot tolerate terrestrial coverage gaps. The International Chamber of Shipping estimates the global commercial fleet exceeds 55,000 vessels operating beyond terrestrial mobile coverage for the majority of each voyage — a recurring revenue opportunity measured in billions annually for broadband NTN operators with verified maritime SLA credentials.

Sovereign NTN infrastructure programs create structured government procurement pipelines. The EU’s IRIS² program — awarded to Airbus, SES, Eutelsat, and Hispasat — targets European sovereign broadband NTN with EUR 6 billion in funding through 2027. Australia’s Defence Space Strategy allocates AUD 7 billion to resilient satellite communications through 2031. Emerging market IoT agriculture represents additional white-space: Brazil, India, and sub-Saharan Africa represent over 900 million smallholder farming households where NTN operators partnering with agricultural input distributors can bundle IoT connectivity without direct-to-farmer retail infrastructure.

Latest Trends in Satellite-to-Mobile (NTN) Communication Market

AI-Optimized Constellation Management and Seamless 5G-NTN Handover Reshape Service Architecture

AI-driven satellite constellation management is transforming NTN operational economics. Machine learning models optimizing satellite beam steering, inter-satellite link routing, and spectrum sharing between NTN and terrestrial 5G are reducing per-bit delivery cost at a rate outpacing traditional engineering optimization. SpaceX’s onboard AI inference hardware for Starlink Gen 2 enabling real-time beam management and SES’s AI-driven O3b mPOWER optimization represent commercial deployments validating AI-native constellation management economics as ARPU pressure from competition intensifies.

Seamless 5G-NTN handover is the technical capability transitioning NTN from standalone satellite service to an integrated 5G network component. 3GPP Release 18 defines signaling and protocol specifications enabling mobile devices to transition seamlessly between terrestrial 5G and NTN satellite without call drops or application interruptions. Ericsson and Nokia demonstrated compliant 5G-NTN handover prototypes at MWC Barcelona 2026, with first commercial deployments targeted for H2 2026.

Regenerative satellite payloads — onboard digital signal processing converting satellites from passive transponders to active network nodes — enable LEO constellations to carry 5G core functions in space. Amazon Kuiper’s onboard processing architectures reduce ground station dependence, enabling service delivery in regions where gateway infrastructure investment is commercially unviable. Telesat’s Lightspeed constellation embeds software-defined payload architecture enabling in-orbit reprogramming as terrestrial standards evolve.

Recent Developments: SpaceX, AST SpaceMobile, and Iridium Lead 2025–2026

- February 2026 — SpaceX Starlink Direct to Cell commercially launched voice call capability across all US T-Mobile subscribers — the first mass-market satellite voice service delivered through standard unmodified LTE smartphones in a major developed market.

- January 2026 — AST SpaceMobile completed deployment of its first 5 BlueBird Block 2 satellites, expanding commercial coverage to 24 countries and initiating revenue-generating service with AT&T, Verizon, and Rakuten across North America and Japan.

- December 2025 — Amazon Project Kuiper completed its first commercial satellite launch, deploying 27 production satellites and initiating beta service trials with enterprise maritime and aviation customers in North America.

- November 2025 — Iridium Communications and Qualcomm announced expanded Snapdragon Satellite integration for Android devices, extending satellite messaging to 30+ new smartphone models from Samsung, Motorola, and OPPO targeting global launch in Q1 2026.

- October 2025 — Skylo Technologies launched NTN IoT service across India in partnership with BSNL and Tata Communications, enabling 3GPP Release 17 compliant NB-IoT NTN connectivity for agricultural and logistics IoT devices without hardware modification.

- September 2025 — SES completed first in-orbit demonstration of seamless 5G-NTN handover between O3b mPOWER MEO and terrestrial 5G with Deutsche Telekom, validating Release 18 handover protocols at commercial service latency requirements.

- August 2025 — Telesat Lightspeed secured a USD 2.4 billion Canadian government financing commitment for the Lightspeed LEO broadband constellation, targeting commercial service for remote Canadian communities and enterprise customers from 2027.

Report Features

| Feature | Description |

|---|---|

| Market Value (2025) | USD 0.65 billion |

| Forecast Revenue (2035) | USD 16.88 billion |

| CAGR (2026–2035) | 38.50% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020–2024 |

| Forecast Period | 2026–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Investment Landscape, Regulatory Framework, Recent Developments |

| Segments Covered | By Technology (D2D, NB-IoT/M2M NTN, Broadband NTN), By Orbit (LEO, MEO, GEO), By Application (Emergency, Maritime, IoT, Consumer, Gov/Defense), By End-Use (Consumer, Enterprise, Government), By Component (Space Segment, User Terminal, Ground Segment) |

| Regional Analysis | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Dominant Segment | D2D Satellite 42.3%; LEO 58.4%; Emergency 29.4%; Consumer 38.7% |

| Dominant Region | North America 38.2%; Asia-Pacific fastest-growing at 31.8% CAGR |

| Regulatory Framework | 3GPP Release 17/18 NTN, ITU MSS Coordination, FCC SCS License, GSMA NTN Guidelines, EU IRIS² Framework, Ofcom SCS Policy, TRAI NTN Consultation |

| Competitive Landscape | SpaceX Starlink, AST SpaceMobile, Iridium, Inmarsat (Viasat), Globalstar, SES, Amazon Kuiper, Telesat, Skylo, Lynk Global, Qualcomm, MediaTek |

Glossary of Key Terms

| Term | Definition |

|---|---|

| NTN (Non-Terrestrial Network) | 3GPP-defined network category encompassing satellite and high-altitude platform stations (HAPS) integrated into 5G architecture via Release 17 and 18 specifications. |

| D2D (Direct-to-Device) | Satellite service category enabling direct communication between a standard mobile handset and a satellite without external antenna hardware or SIM changes. |

| LEO (Low Earth Orbit) | Orbital altitude range of 500–2,000 km. Characterized by sub-100 ms signal latency and high satellite count requirements for global coverage. |

| MEO (Medium Earth Orbit) | Orbital altitude range of 2,000–35,786 km. Used by SES O3b mPOWER for high-throughput enterprise broadband with latency between LEO and GEO. |

| GEO (Geostationary Orbit) | Fixed orbital altitude of 35,786 km. Satellite remains stationary relative to Earth; provides continuous regional coverage with 600+ ms latency. |

| SCS (Supplemental Coverage from Space) | FCC licensing category authorizing LEO satellite operators to provide terrestrial mobile coverage supplementation in partnership with licensed MNOs. |

| 3GPP Release 17 / 18 | Iterations of the global mobile standard body’s specification; Release 17 standardizes NB-IoT NTN, Release 18 standardizes broadband NTN for handheld devices. |

| NB-IoT (Narrowband IoT) | Cellular IoT standard designed for low-power, low-data-rate devices. 3GPP Release 17 extends NB-IoT operation to satellite (NTN) for global IoT coverage. |

| CAGR | Compound Annual Growth Rate — the annualized growth rate of a market between two specified years, assuming compounding. |

| MSS (Mobile Satellite Services) | ITU-defined spectrum service category for satellite communications with mobile earth stations; governs frequency allocations used by NTN D2D services. |

| MNO (Mobile Network Operator) | Licensed terrestrial mobile operator. NTN commercial deployments are predominantly structured as MNO partnerships where the satellite operator provides NTN capacity. |

| EPFD (Equivalent Power Flux-Density) | ITU-defined interference limit for non-GSO satellite systems protecting GEO satellite networks — a key ITU coordination parameter for LEO constellation operators. |

| Regenerative Payload | Satellite architecture featuring onboard digital signal processing enabling the satellite to function as an active network node rather than a passive signal relay. |

| MEC (Multi-access Edge Computing) | Network architecture concept placing compute capacity at or near the network edge to reduce latency for IoT and enterprise applications — increasingly combined with NTN for remote deployments. |

| ARPU (Average Revenue Per User) | Revenue metric dividing total service revenue by total subscriber count; used to compare revenue efficiency across NTN service tiers and operator partnerships. |

Sources

- 3GPP — Release 17 NTN (IoT) and Release 18 NTN (Handheld): https://www.3gpp.org/release-17 | https://www.3gpp.org/release-18

- Iridium Communications — Annual Report 2024: https://www.iridium.com/investors/

- Globalstar Inc. — Annual Report 2024: https://www.globalstar.com/investors

- SES S.A. — Annual Report 2024: https://www.ses.com/investors

- AST SpaceMobile — Q4 2024 Earnings Release: https://investors.ast-science.com

- FCC — Supplemental Coverage from Space (SCS) Licensing Framework 2023: https://www.fcc.gov/document/fcc-authorizes-space-based-supplemental-coverage-applications

- GSMA — NTN Integration Guidelines and Mobile Economy 2025: https://www.gsma.com/solutions-and-impact/technologies/non-terrestrial-networks

- TRAI — Consultation Paper on Satellite Spectrum Assignment (2025): https://www.trai.gov.in

- European Commission — IRIS² Sovereign Connectivity Program: https://digital-strategy.ec.europa.eu/en/policies/iris2

- ITU — Non-Geostationary Satellite System Filing: https://www.itu.int/en/ITU-R/space/Pages/default.aspx

- Qualcomm — Snapdragon Satellite Platform: https://www.qualcomm.com/products/technology/modems/snapdragon-satellite

- SpaceX — Starlink Direct to Cell Commercial Launch (February 2026): https://www.starlink.com/business/cell

- Amazon — Project Kuiper Commercial Satellite Deployment (December 2025): https://www.aboutamazon.com/what-we-do/devices-services/project-kuiper

- Skylo Technologies — NTN IoT India Launch (October 2025): https://www.skylo.tech/news

- Telesat — Lightspeed Financing and Commercial Service Timeline: https://www.telesat.com/lightspeed